Corporate Accounting Assignment Solution: Consolidation & Tax

VerifiedAdded on 2020/04/01

|19

|2997

|38

Homework Assignment

AI Summary

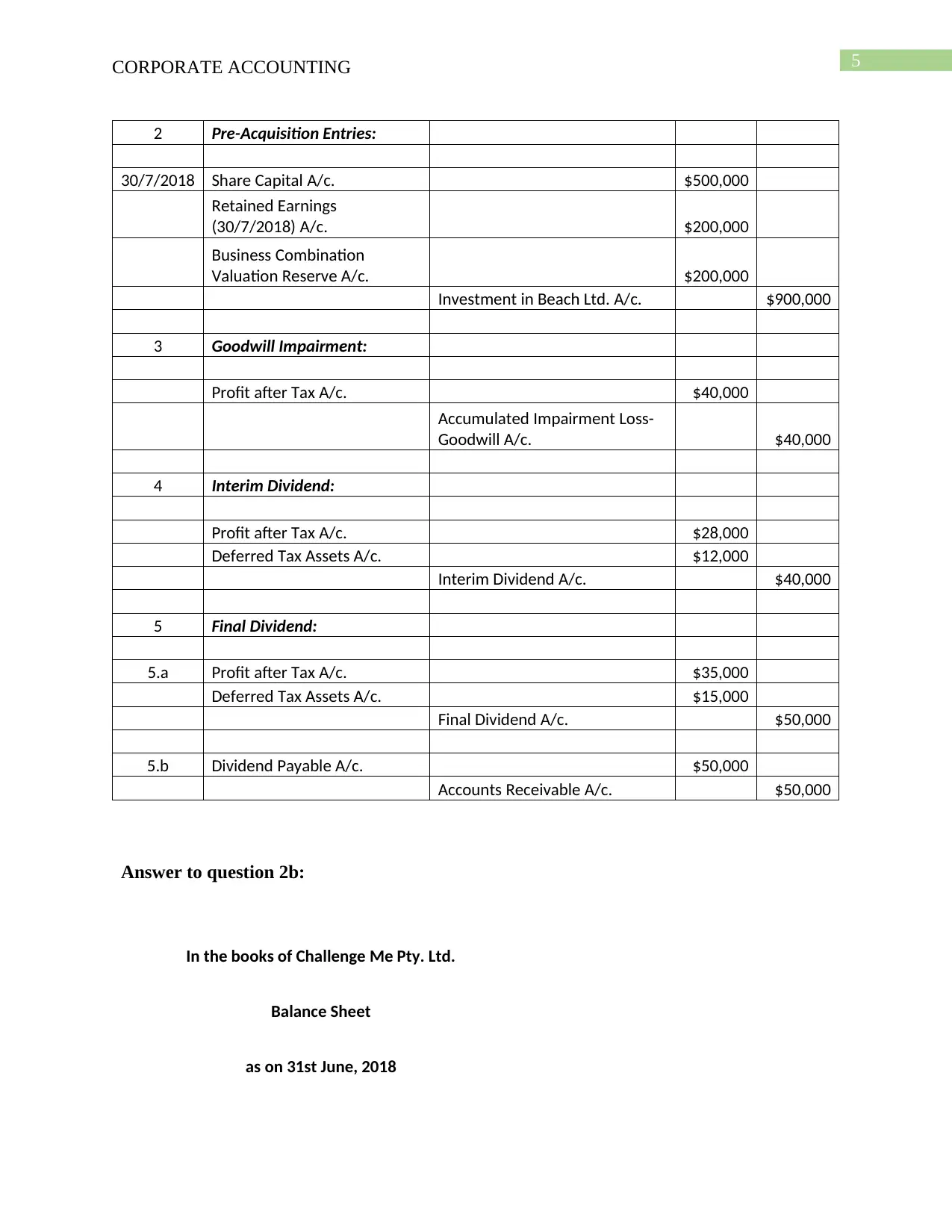

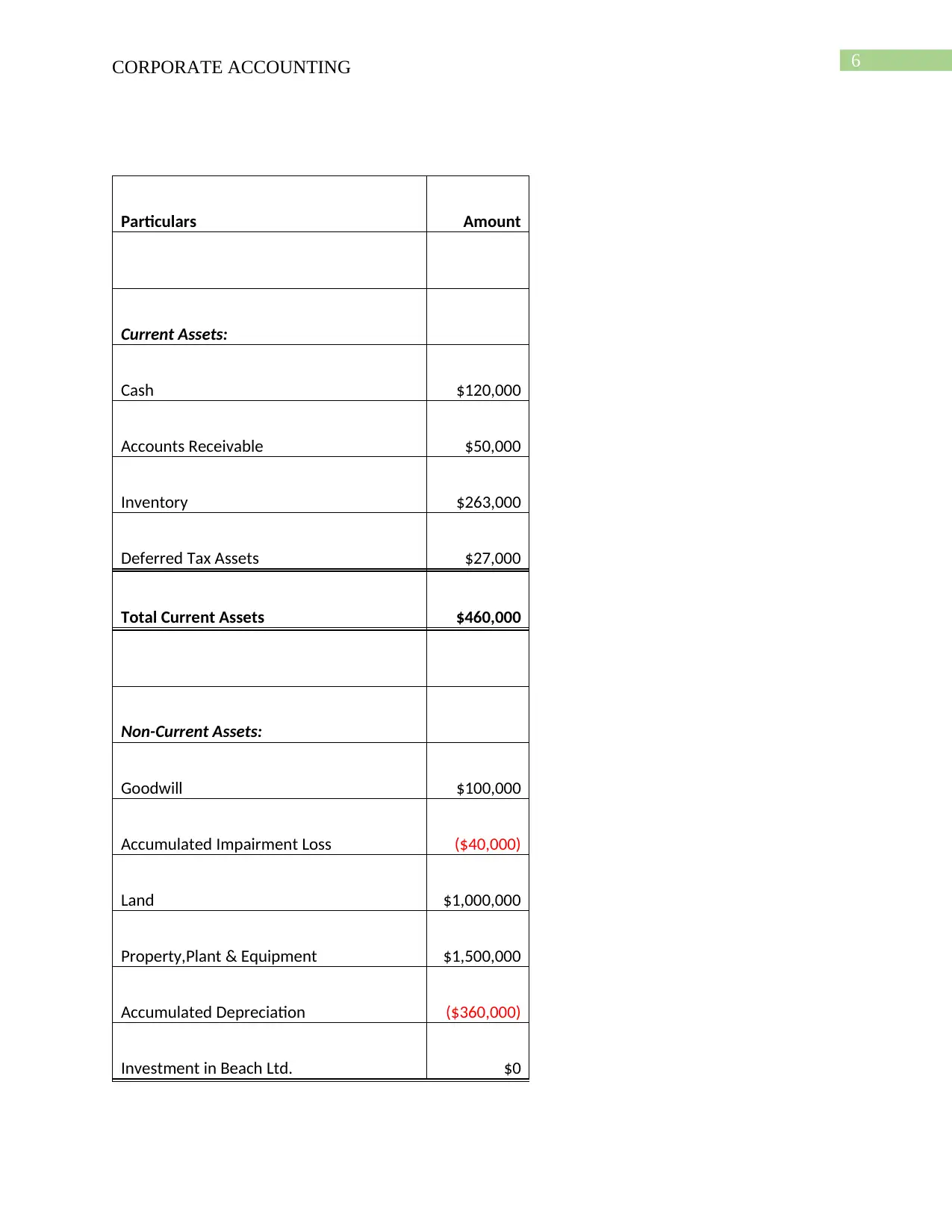

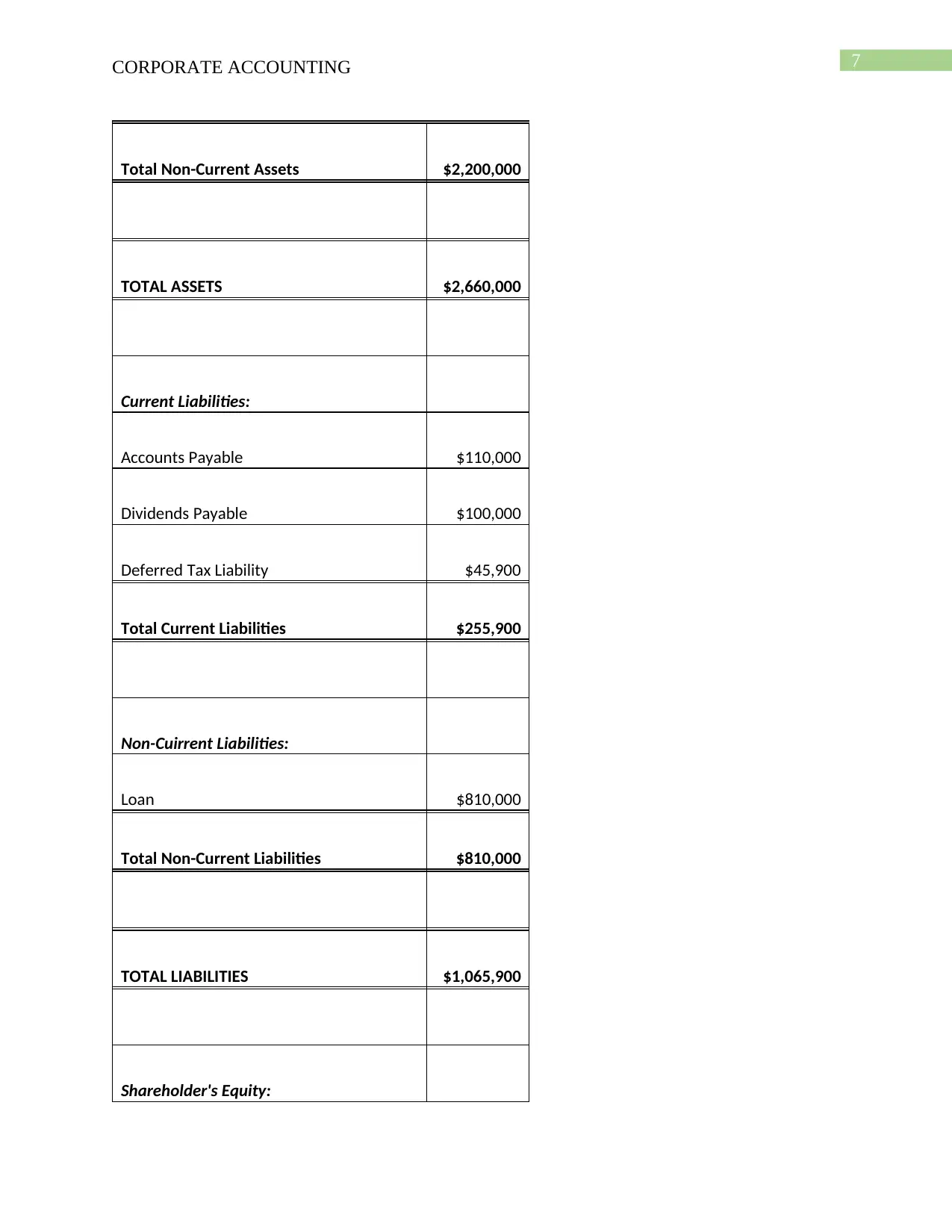

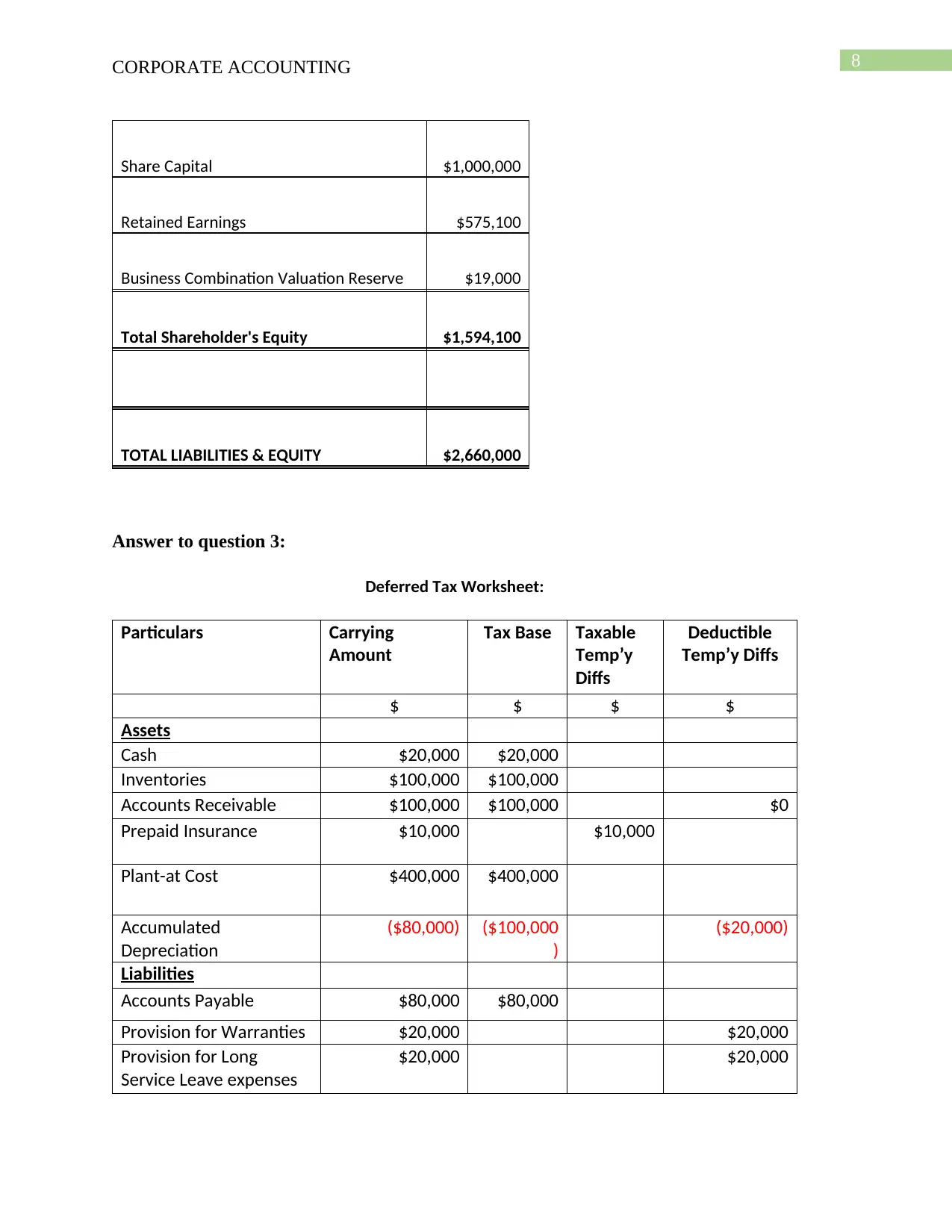

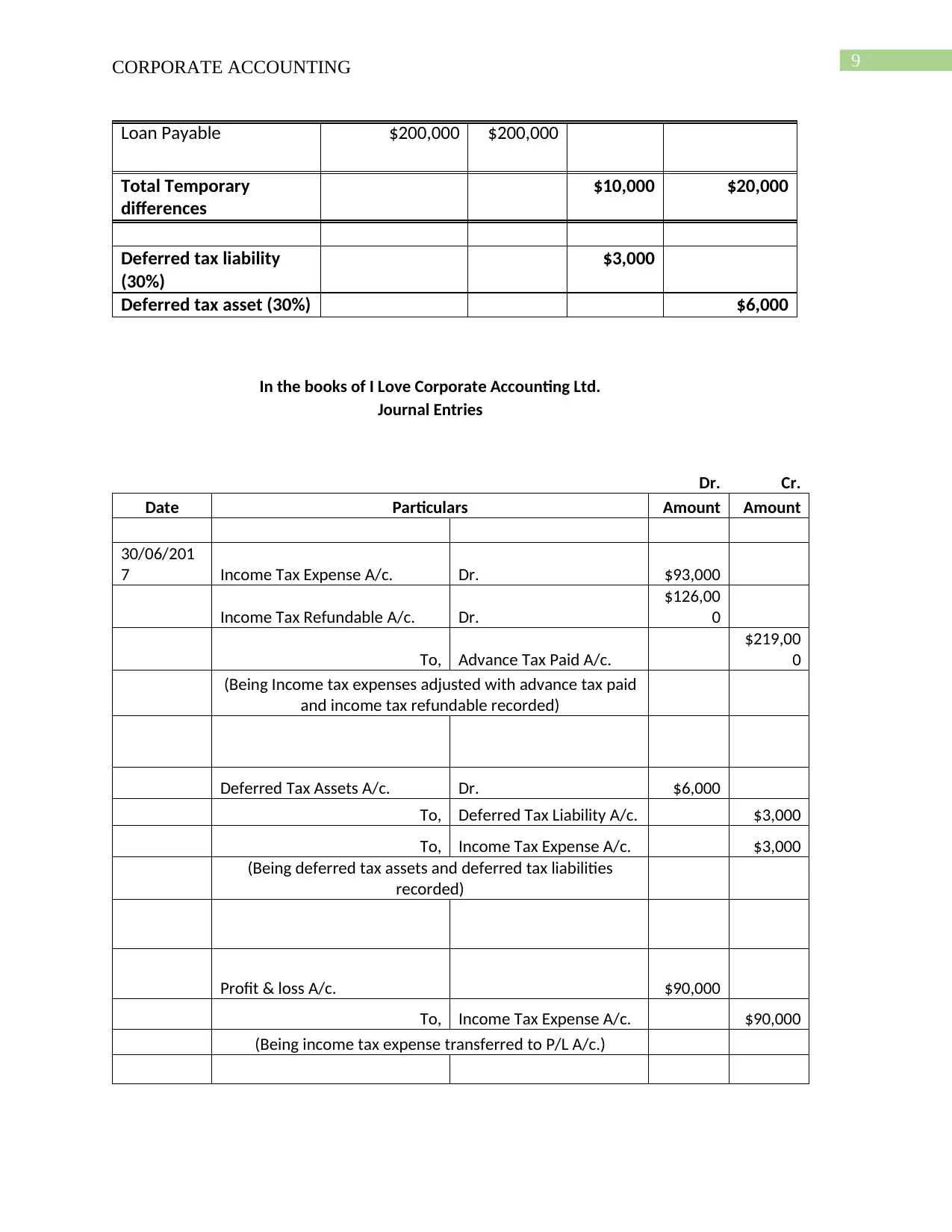

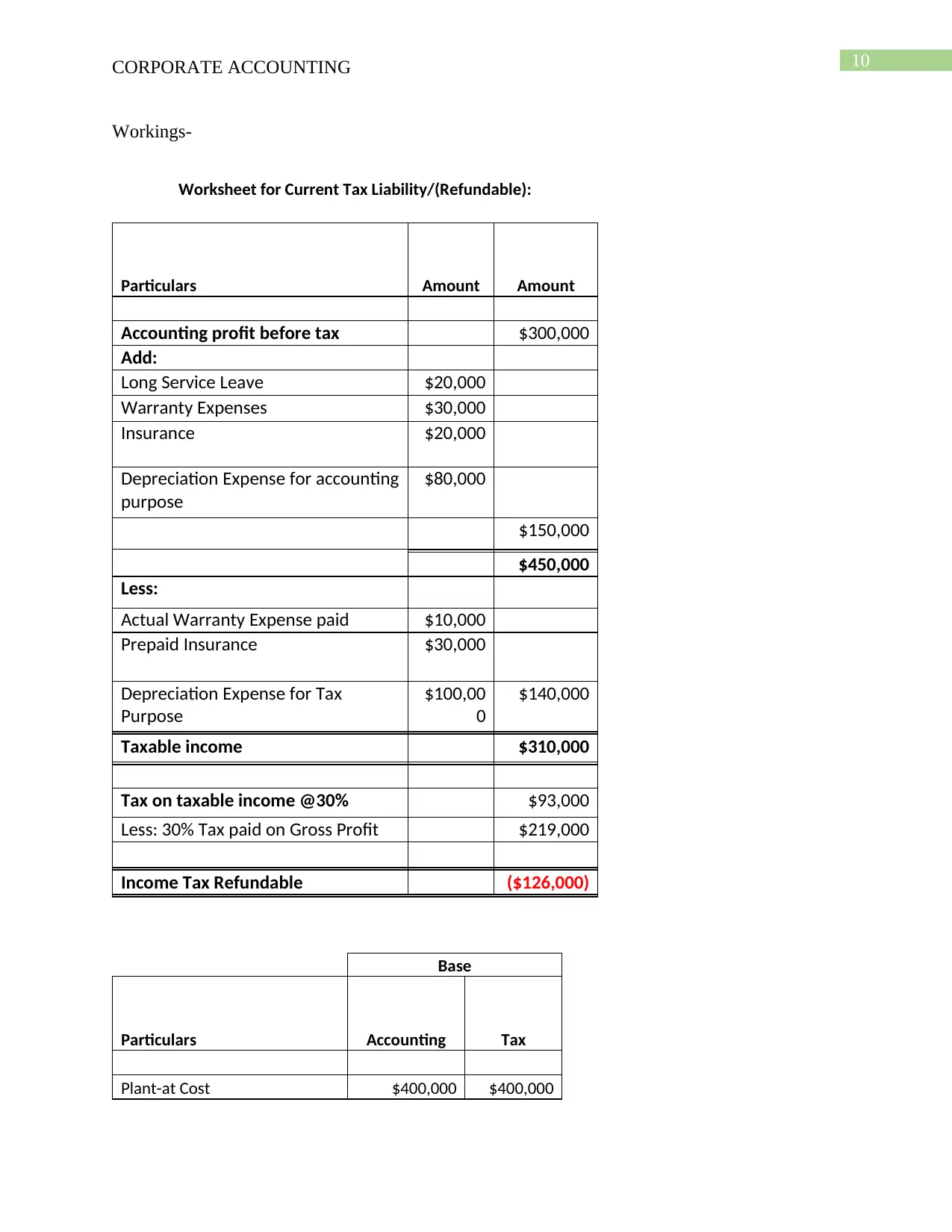

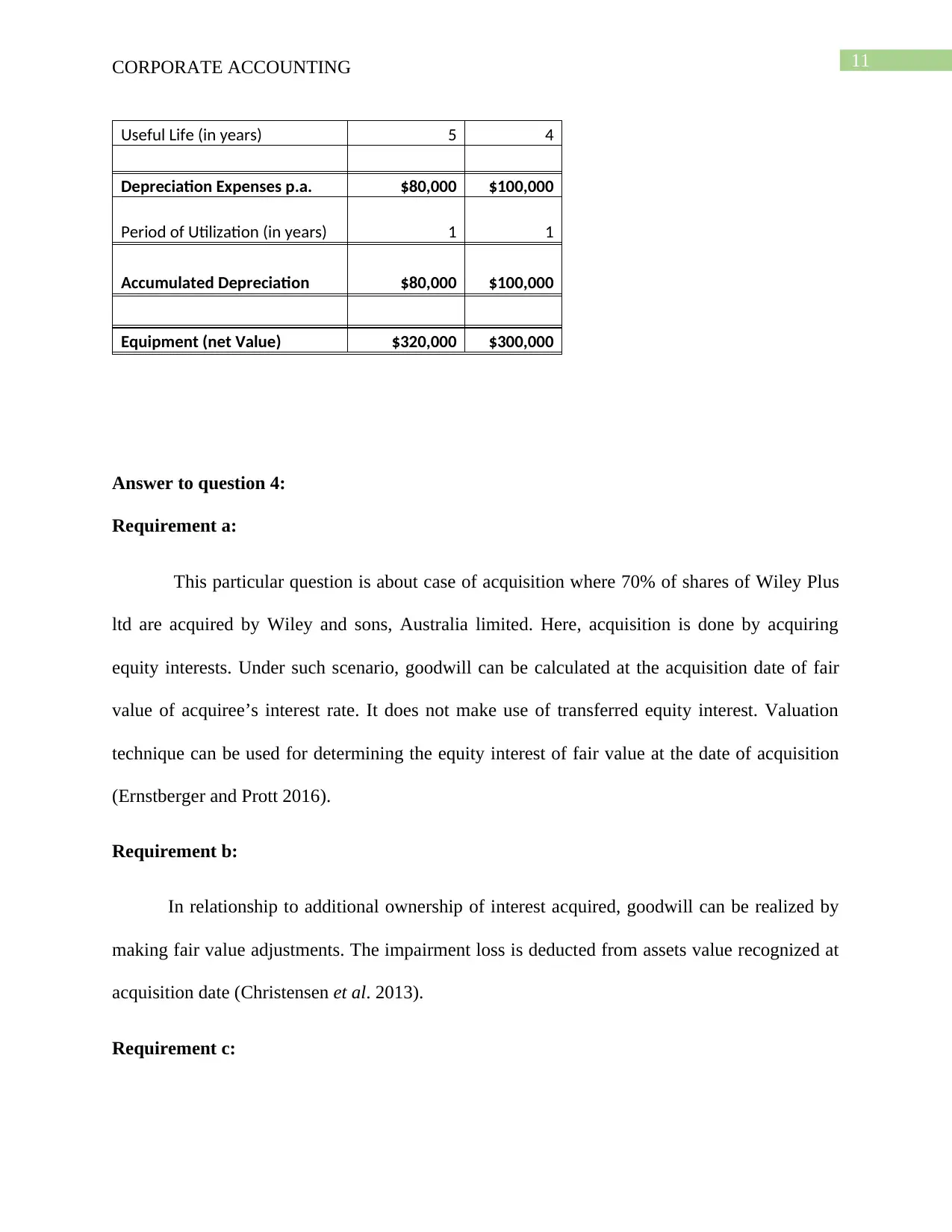

This corporate accounting assignment solution covers several key areas of financial accounting. It begins by analyzing various investment relationships, determining the presence of control and the need for consolidation based on the specifics of each scenario, including voting rights and management involvement. The solution then proceeds to an acquisition analysis, including journal entries and the preparation of a balance sheet, detailing the calculation of goodwill and its subsequent impairment. Further, a deferred tax worksheet and related journal entries are presented, demonstrating the calculation of deferred tax assets and liabilities. The assignment also addresses goodwill valuation in different acquisition scenarios and concludes with a consolidated income statement and balance sheet, incorporating intergroup transactions, profit eliminations, and the impact of bargain purchases, providing a comprehensive overview of consolidation principles and related accounting treatments.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.