Corporate Accounting Assignment Solution - Question 1-5

VerifiedAdded on 2023/01/10

|9

|1547

|53

Homework Assignment

AI Summary

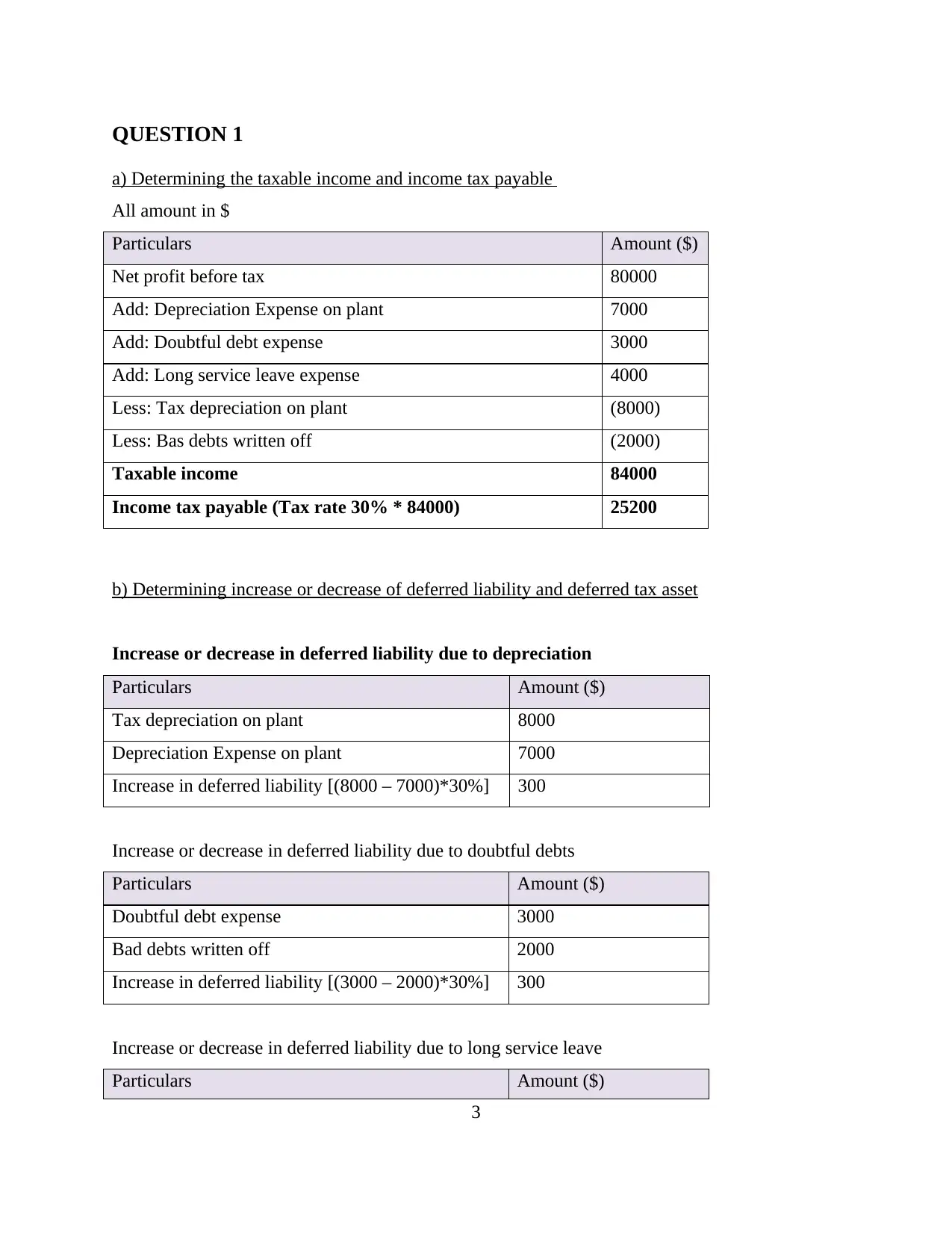

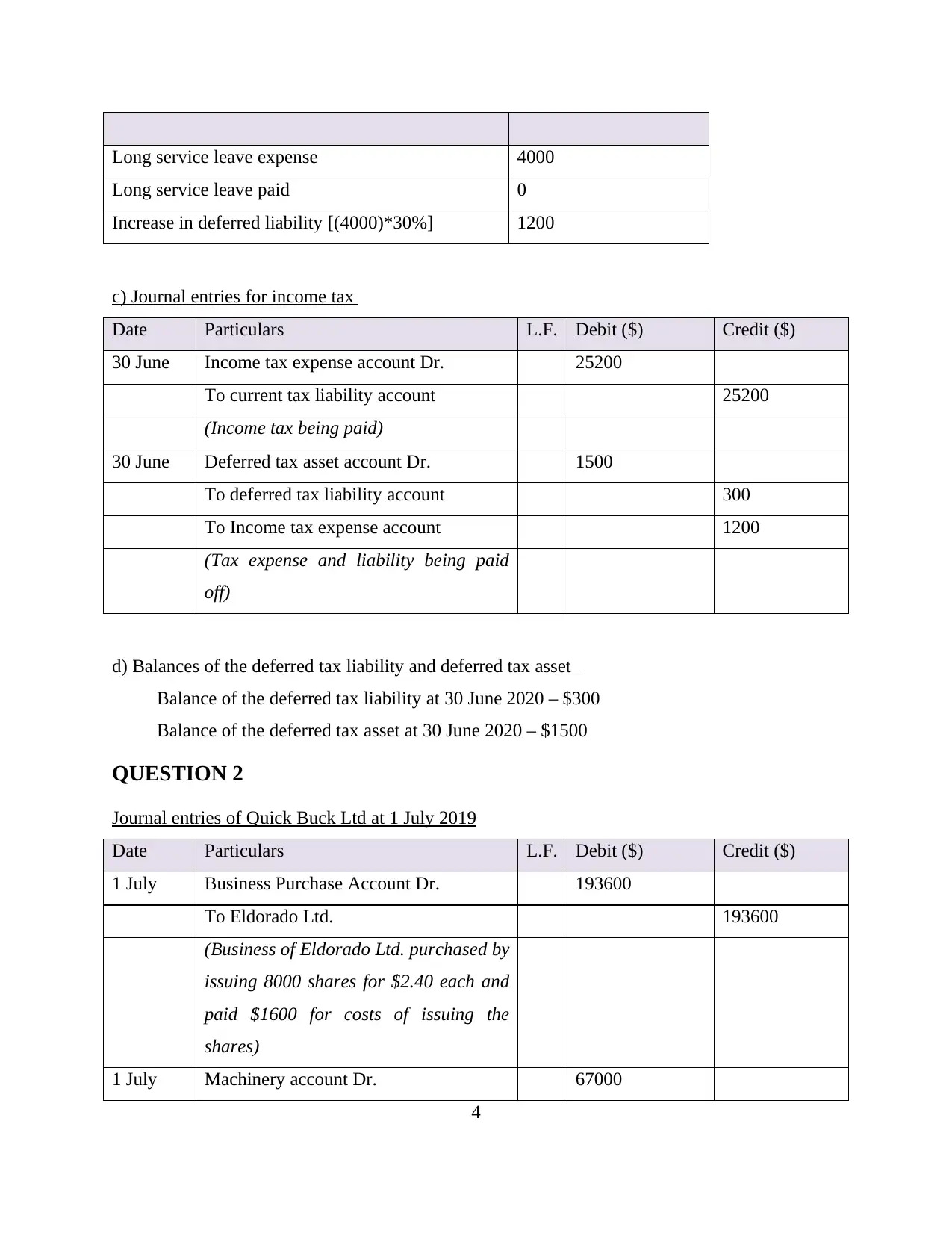

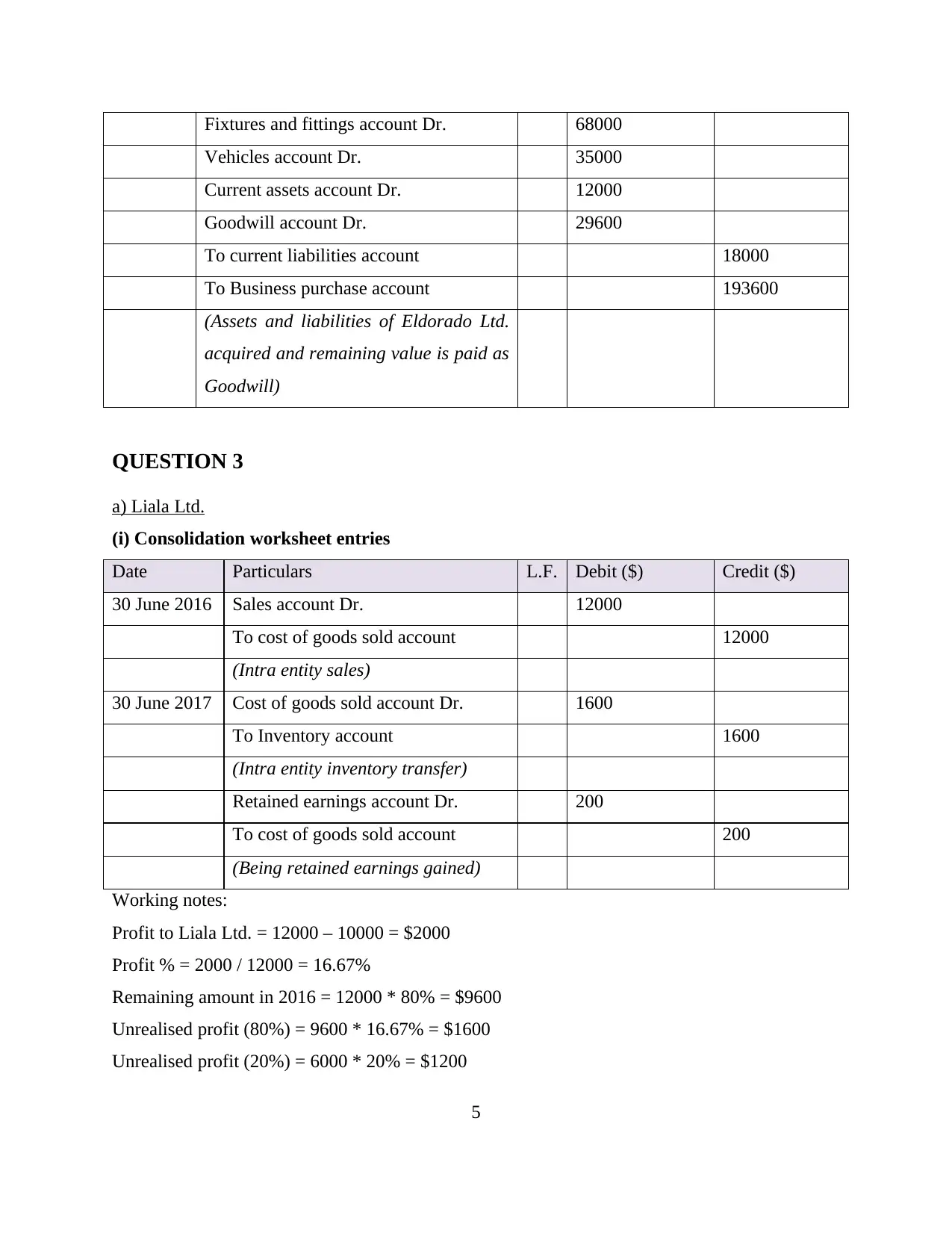

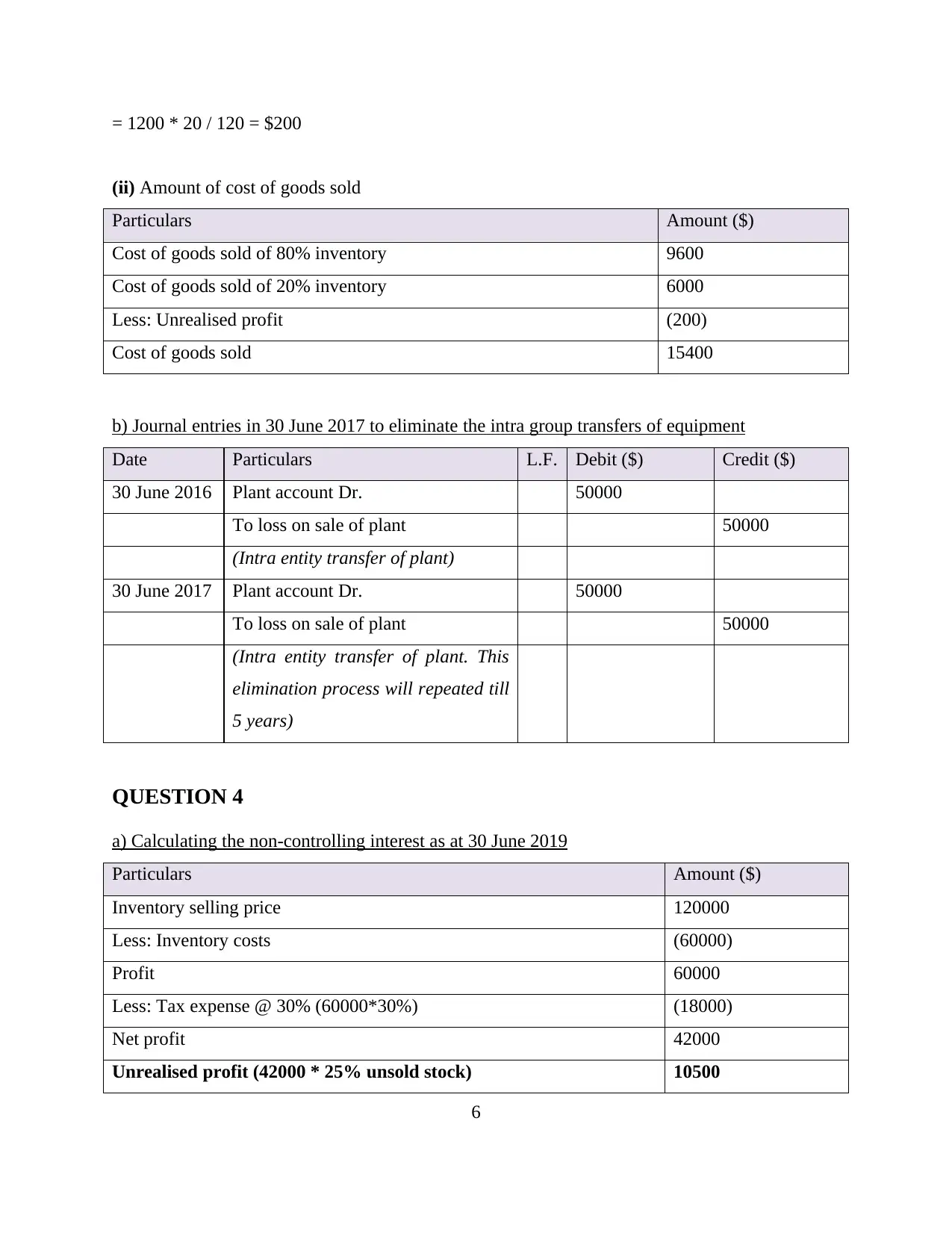

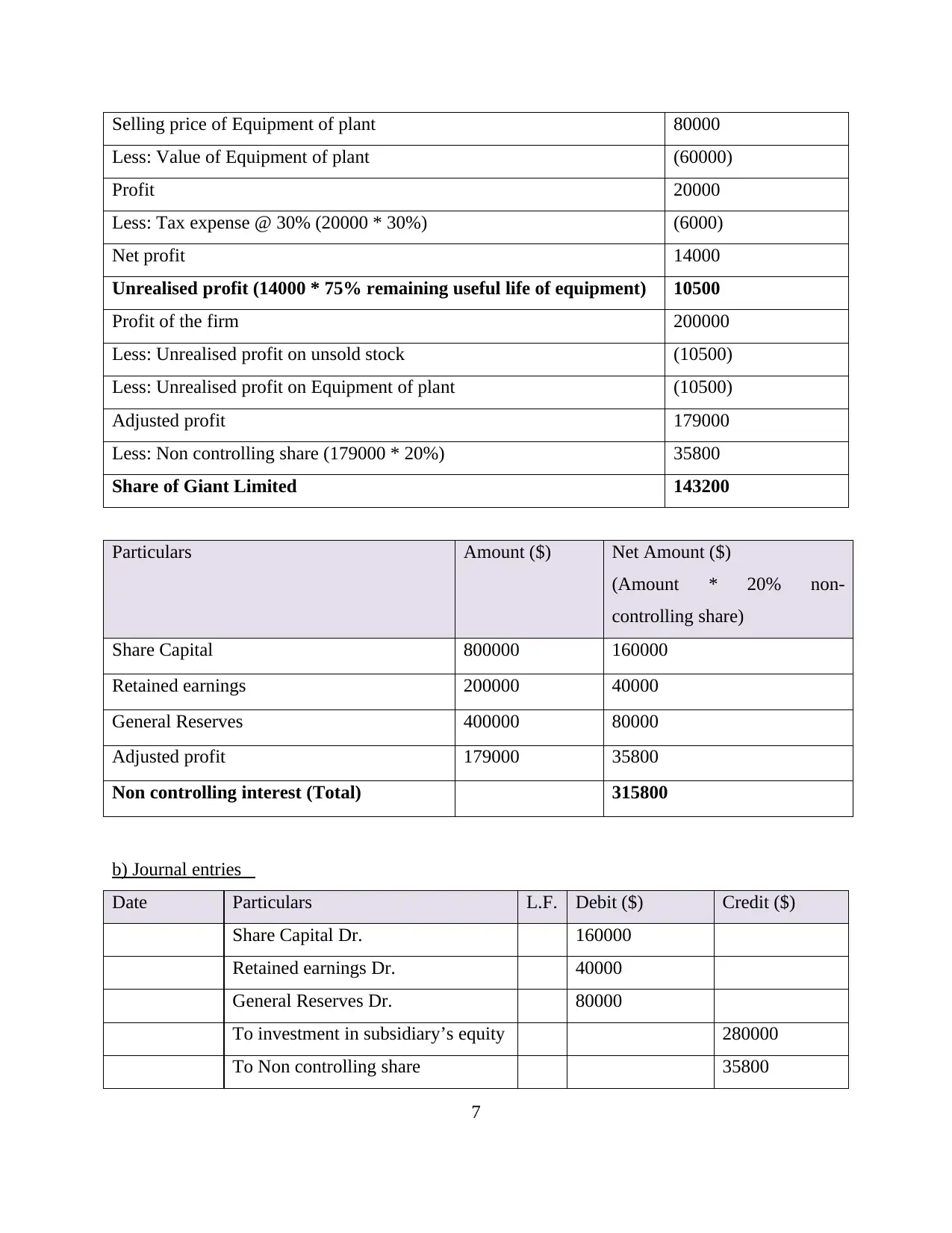

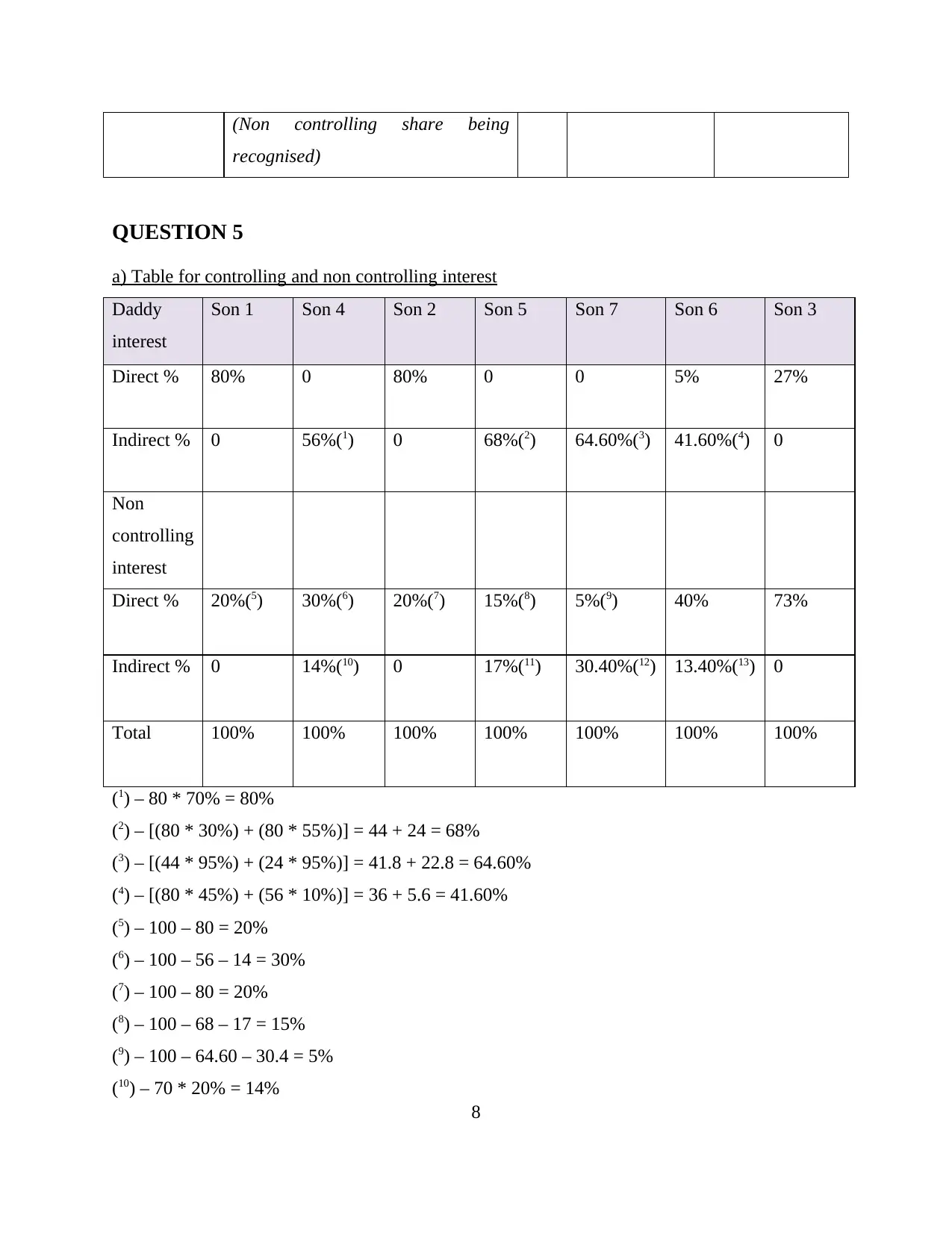

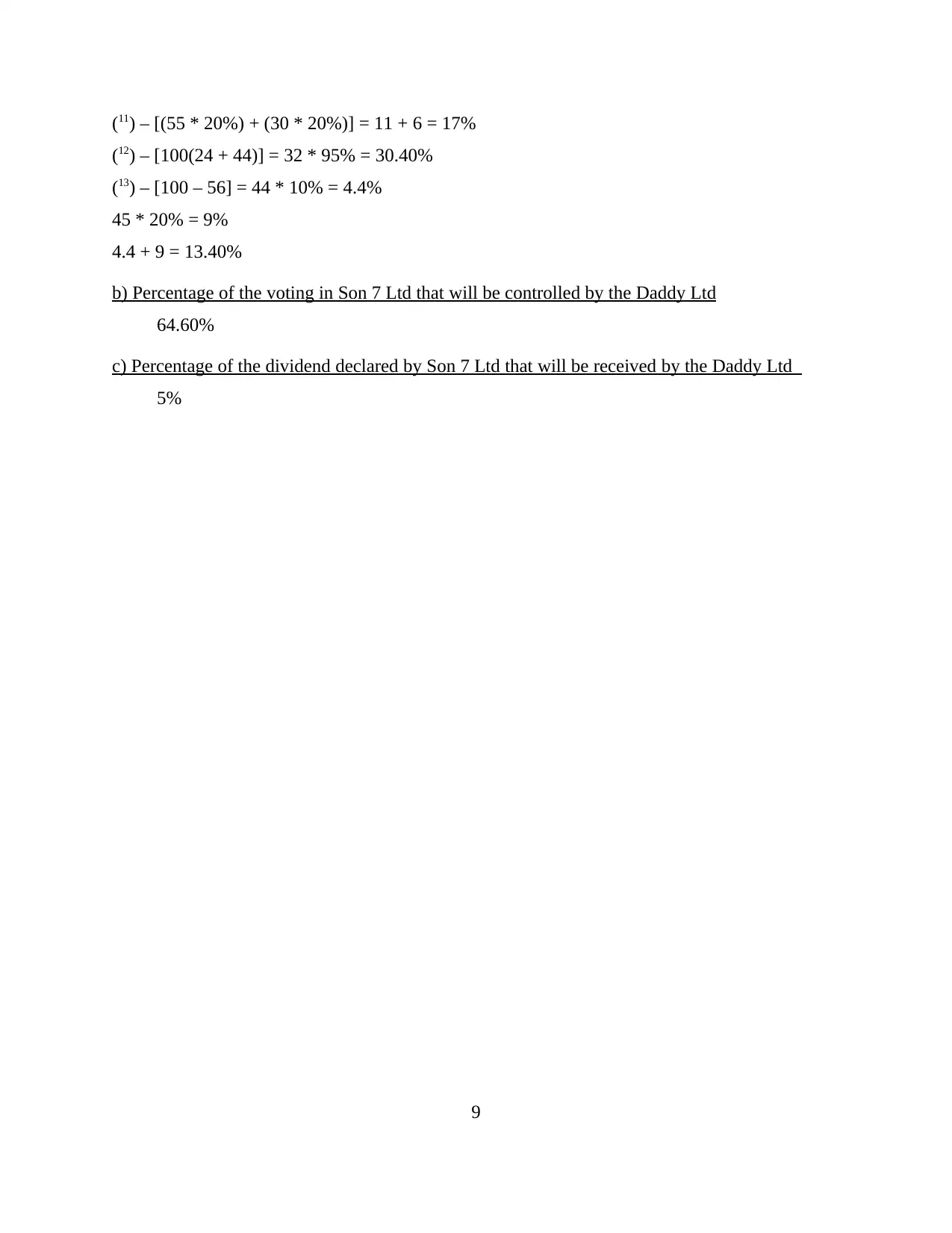

This assignment solution for a corporate accounting course covers several key areas of financial accounting. It begins with the determination of taxable income, income tax payable, and the impact on deferred tax liabilities and assets, including relevant journal entries. The solution then addresses business combinations, specifically the purchase of a business and the associated journal entries, including goodwill calculations. Further, the assignment delves into consolidation accounting, including the elimination of intra-group transactions and the calculation of unrealized profits. It also examines the calculation of non-controlling interests, the preparation of journal entries, and the analysis of subsidiary relationships. The solution includes detailed calculations and explanations to help students understand the concepts of financial accounting.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.