King's Own Institute Corporate Accounting and Reporting Assignment

VerifiedAdded on 2022/11/13

|7

|773

|167

Homework Assignment

AI Summary

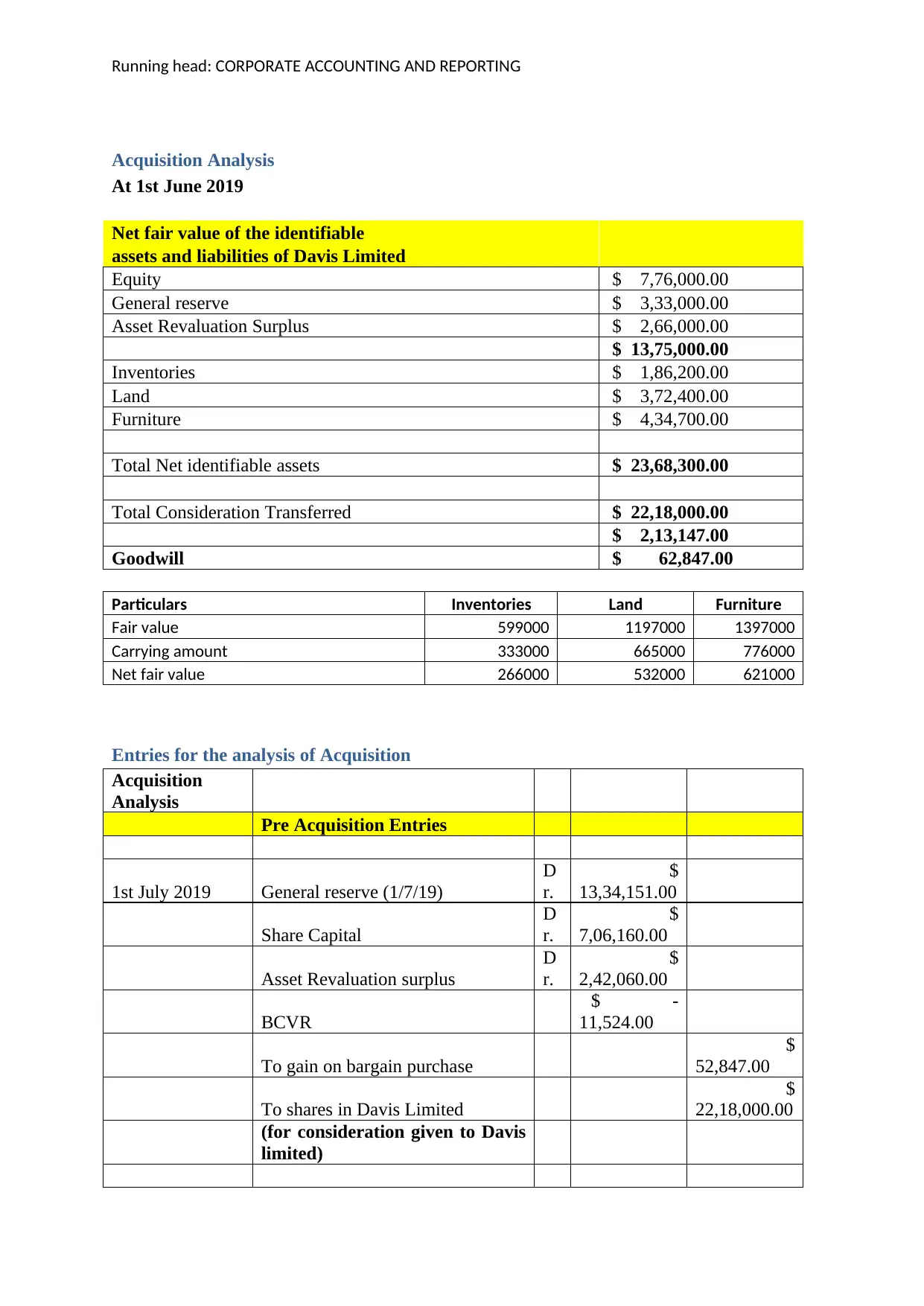

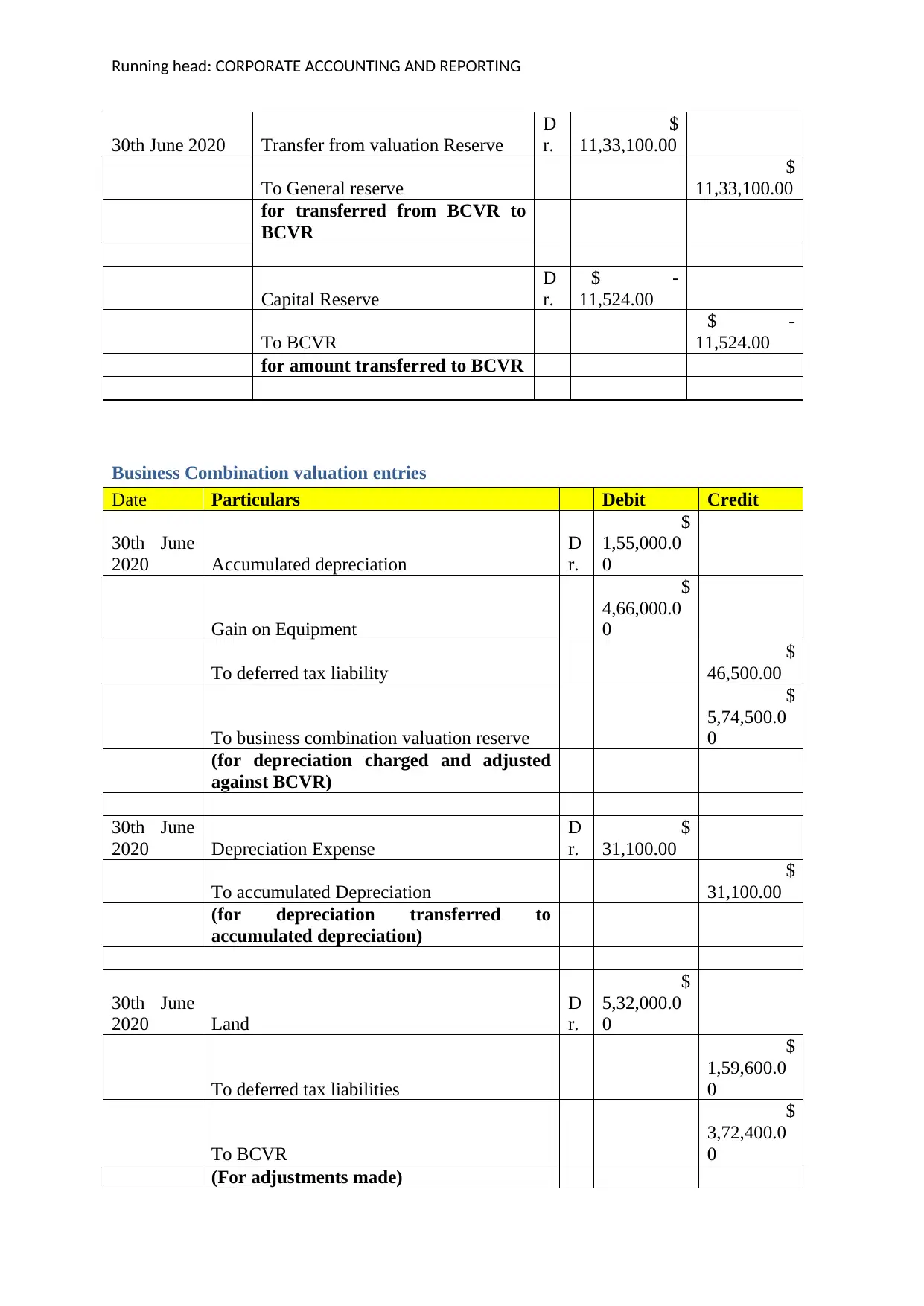

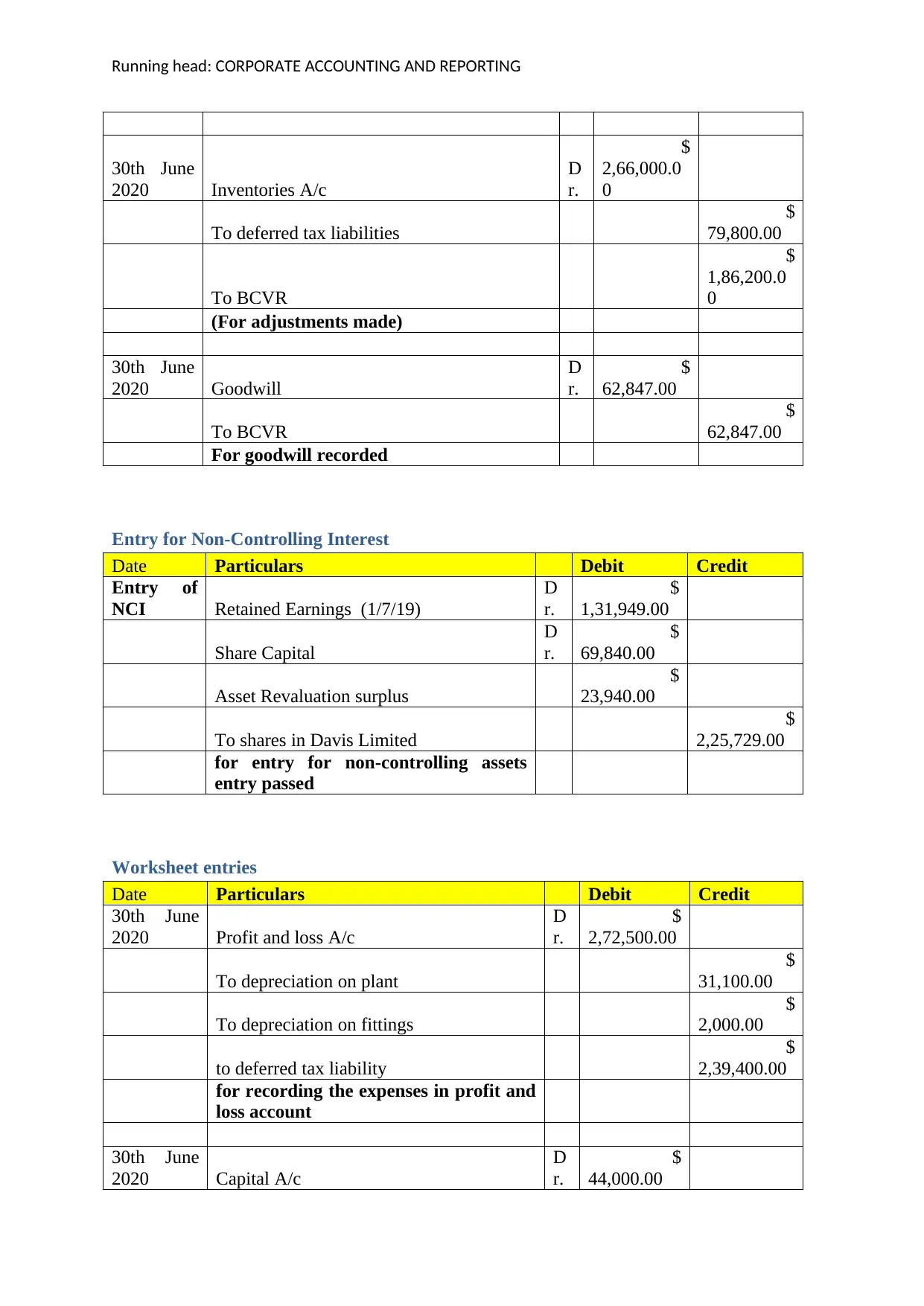

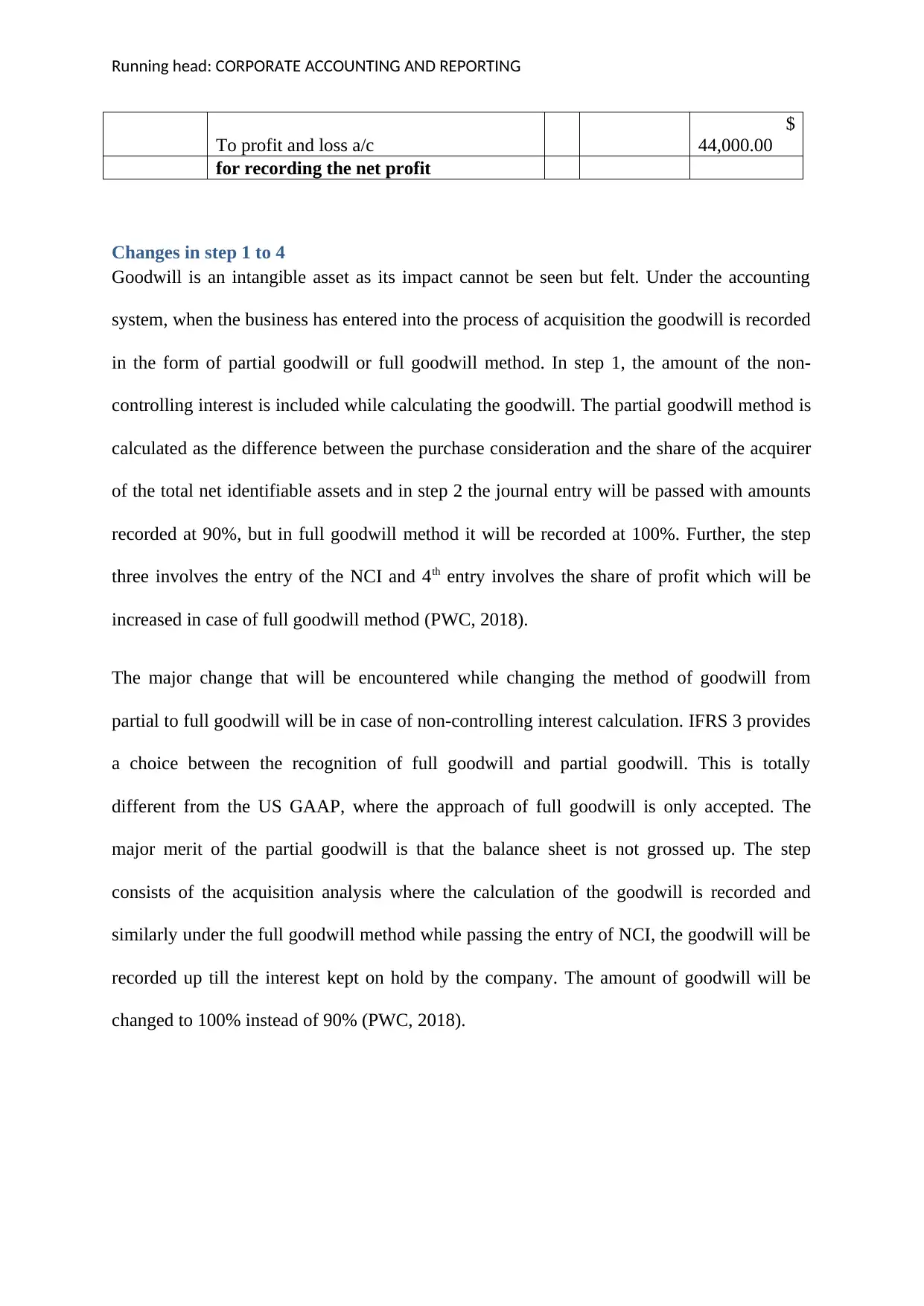

This assignment solution addresses a corporate accounting problem focused on the acquisition of Davis Limited. It provides detailed calculations and journal entries related to the acquisition, including the analysis of net fair values of identifiable assets and liabilities. The solution covers the entries for acquisition, business combination valuation, and non-controlling interest. It also includes worksheet entries and a discussion of the impact of changing from partial to full goodwill methods. The assignment incorporates accounting standards and provides relevant explanations for each step, including the treatment of goodwill and the non-controlling interest. References to relevant sources, such as PWC publications, are also included to support the analysis and conclusions presented.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.