Corporate Accounting 1 Assignment: Detailed Task Solutions

VerifiedAdded on 2023/01/11

|10

|2307

|80

Homework Assignment

AI Summary

This document presents a comprehensive solution set for a corporate accounting assignment. It begins with the calculation of acquisition costs, journal entries, and explanations of maintained cost calculations for a machine. The solution then delves into debentures, calculating issue prices and providing corresponding journal entries. Further, it includes detailed journal entries for RCK limited, followed by an explanation of items adjusted directly against equity rather than profit or loss, such as other comprehensive income. Finally, the assignment concludes with a cash flow statement for Fool’s Paradise Limited, providing interpretations and analysis of operating, investing, and financing activities, offering a complete overview of the financial accounting principles. The assignment references accounting standards and provides an in-depth analysis of the financial concepts.

CORPORATE ACCOUTING

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

TASK1.............................................................................................................................................3

Calculation of acquisition cost of the Gizmo Machine...............................................................3

Journal entries in the books of Gizmo Machine..........................................................................3

Explanation of maintained cost calculation.................................................................................3

TASK2.............................................................................................................................................4

Calculation of issue price of debenture.......................................................................................4

Journal entry of debenture...........................................................................................................4

TASK3.............................................................................................................................................5

Journal entries of RCK limited....................................................................................................5

TASK4.............................................................................................................................................6

Example of items that would be adjust directly against equity rather than being as part of profit

or loss...........................................................................................................................................6

TASK5.............................................................................................................................................8

Cash flow statement of Fool’s Paradise Limited.........................................................................8

2

Contents...........................................................................................................................................2

TASK1.............................................................................................................................................3

Calculation of acquisition cost of the Gizmo Machine...............................................................3

Journal entries in the books of Gizmo Machine..........................................................................3

Explanation of maintained cost calculation.................................................................................3

TASK2.............................................................................................................................................4

Calculation of issue price of debenture.......................................................................................4

Journal entry of debenture...........................................................................................................4

TASK3.............................................................................................................................................5

Journal entries of RCK limited....................................................................................................5

TASK4.............................................................................................................................................6

Example of items that would be adjust directly against equity rather than being as part of profit

or loss...........................................................................................................................................6

TASK5.............................................................................................................................................8

Cash flow statement of Fool’s Paradise Limited.........................................................................8

2

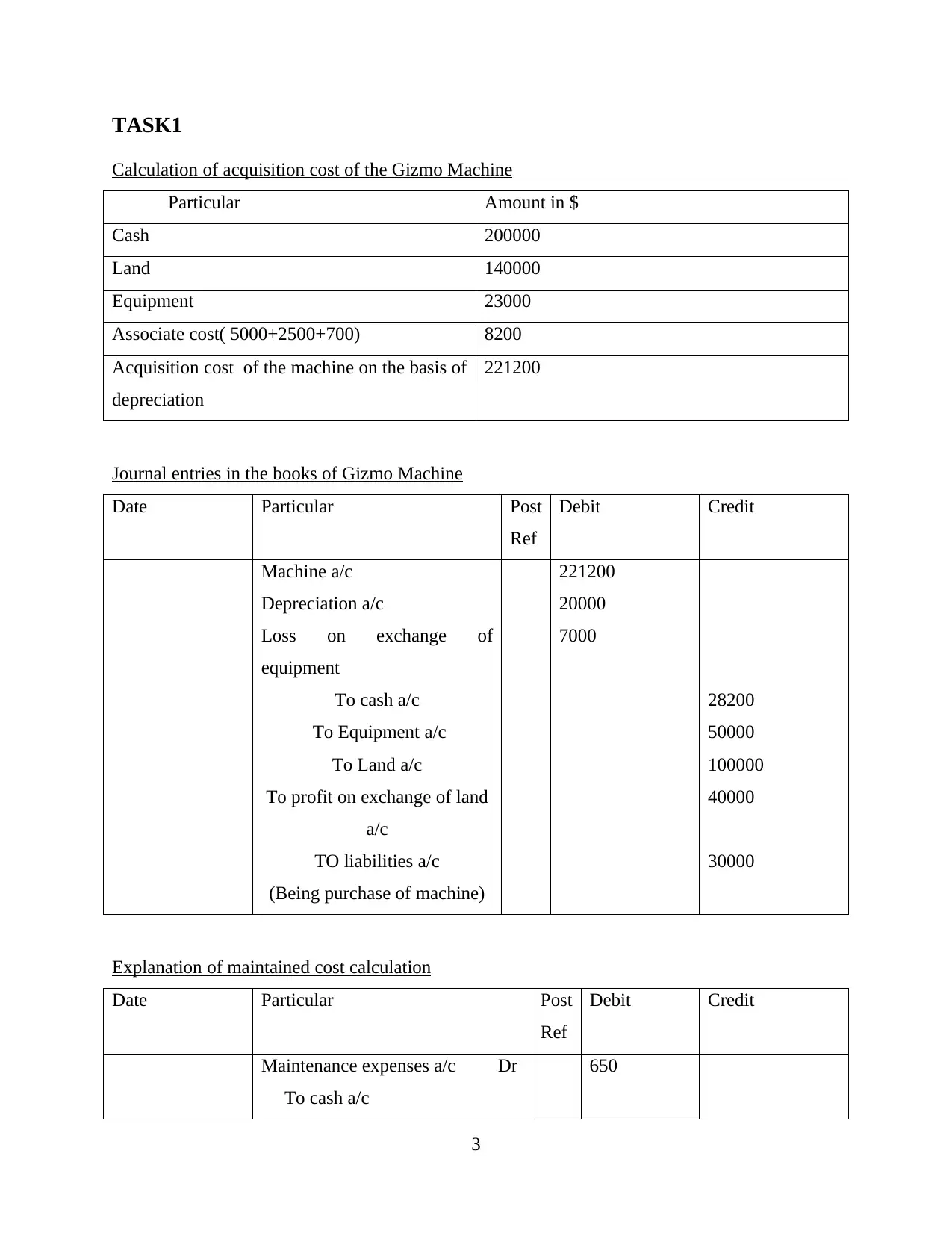

TASK1

Calculation of acquisition cost of the Gizmo Machine

Particular Amount in $

Cash 200000

Land 140000

Equipment 23000

Associate cost( 5000+2500+700) 8200

Acquisition cost of the machine on the basis of

depreciation

221200

Journal entries in the books of Gizmo Machine

Date Particular Post

Ref

Debit Credit

Machine a/c

Depreciation a/c

Loss on exchange of

equipment

To cash a/c

To Equipment a/c

To Land a/c

To profit on exchange of land

a/c

TO liabilities a/c

(Being purchase of machine)

221200

20000

7000

28200

50000

100000

40000

30000

Explanation of maintained cost calculation

Date Particular Post

Ref

Debit Credit

Maintenance expenses a/c Dr

To cash a/c

650

3

Calculation of acquisition cost of the Gizmo Machine

Particular Amount in $

Cash 200000

Land 140000

Equipment 23000

Associate cost( 5000+2500+700) 8200

Acquisition cost of the machine on the basis of

depreciation

221200

Journal entries in the books of Gizmo Machine

Date Particular Post

Ref

Debit Credit

Machine a/c

Depreciation a/c

Loss on exchange of

equipment

To cash a/c

To Equipment a/c

To Land a/c

To profit on exchange of land

a/c

TO liabilities a/c

(Being purchase of machine)

221200

20000

7000

28200

50000

100000

40000

30000

Explanation of maintained cost calculation

Date Particular Post

Ref

Debit Credit

Maintenance expenses a/c Dr

To cash a/c

650

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

650

The value of the maintained cost is not considered in the cost of acquisition of machine as the

rule of the accounting standard of Australia. The maintenance cost shod benched after the

purchasing of asset and it charge on the basis of expenditure incurred on the maintain thus it

cannot be caudate. The entry of maintain cost is recorded n the separate accounting and it not

included in the cost of purchasing of man chine( Tayob, 2019).

TASK2

Calculation of issue price of debenture

Debentures can be defined as long tern security and liability for business organization. It is a

yield with fixed rate of interpret rate issued by business organization and it was secured against

the business assets. Credit worthiness and resultants of the issuer take back debentures. It can be

refer as one of the best source of garneting funds for business organizations.

In this case the Bombo limited issued their debentures with coupon rate. Coupon rate can be

defined as actual value of the interest gained by debenture holders yearly while the yield o

maturing can be defined as the total rate of return values. If the value of interest rate is higher

than the coupon value they use to go for market rate as they gave more profits through the

interest rate. In this questing, the value of debenture issue can be calculating though this manner

(Arimany,Fitó, Moyaand Orgaz, 2018).

Face value: 200000

Coupon rate: 8 %

Maturity period 6 years

Interest payment: Semi annually

Numbers of interest payment till debenture maturity: 6*2 = 12

Interest payment= Face value 8 coupon rate /2

200000*8%/2 = 80000

The issue price of debenture 280000

Journal entry of debenture

Date Particular Debit Credit

4

The value of the maintained cost is not considered in the cost of acquisition of machine as the

rule of the accounting standard of Australia. The maintenance cost shod benched after the

purchasing of asset and it charge on the basis of expenditure incurred on the maintain thus it

cannot be caudate. The entry of maintain cost is recorded n the separate accounting and it not

included in the cost of purchasing of man chine( Tayob, 2019).

TASK2

Calculation of issue price of debenture

Debentures can be defined as long tern security and liability for business organization. It is a

yield with fixed rate of interpret rate issued by business organization and it was secured against

the business assets. Credit worthiness and resultants of the issuer take back debentures. It can be

refer as one of the best source of garneting funds for business organizations.

In this case the Bombo limited issued their debentures with coupon rate. Coupon rate can be

defined as actual value of the interest gained by debenture holders yearly while the yield o

maturing can be defined as the total rate of return values. If the value of interest rate is higher

than the coupon value they use to go for market rate as they gave more profits through the

interest rate. In this questing, the value of debenture issue can be calculating though this manner

(Arimany,Fitó, Moyaand Orgaz, 2018).

Face value: 200000

Coupon rate: 8 %

Maturity period 6 years

Interest payment: Semi annually

Numbers of interest payment till debenture maturity: 6*2 = 12

Interest payment= Face value 8 coupon rate /2

200000*8%/2 = 80000

The issue price of debenture 280000

Journal entry of debenture

Date Particular Debit Credit

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bank a/c Dr

To 8 % debenture application

a/c(Being application money

received)

200000

200000

8 % Debenture application a/c Dr

Debenture interest a/c Dr

To 8 % debenture a/c

(Being debenture are redeemable

with its interest price)

200000

800000

280000

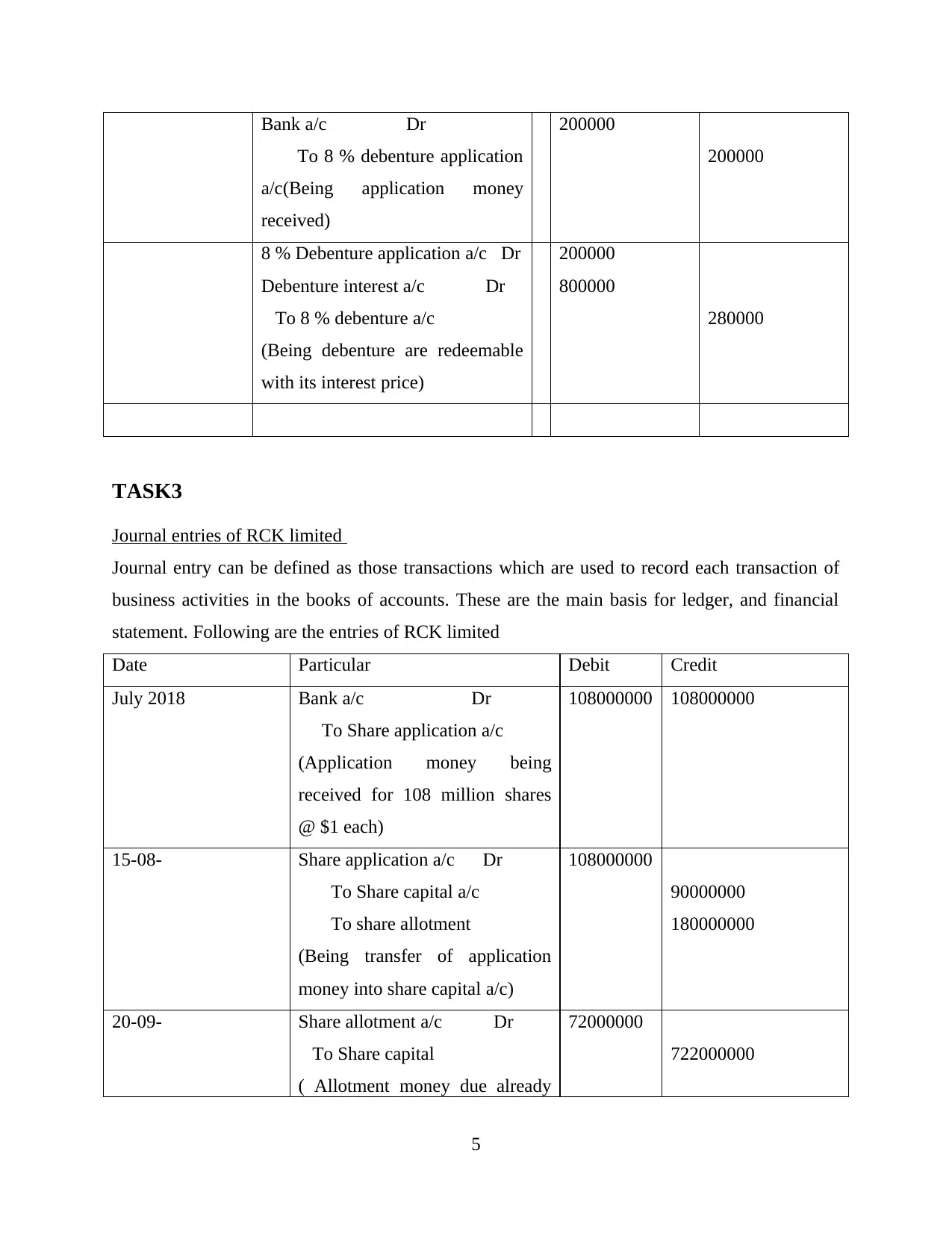

TASK3

Journal entries of RCK limited

Journal entry can be defined as those transactions which are used to record each transaction of

business activities in the books of accounts. These are the main basis for ledger, and financial

statement. Following are the entries of RCK limited

Date Particular Debit Credit

July 2018 Bank a/c Dr

To Share application a/c

(Application money being

received for 108 million shares

@ $1 each)

108000000 108000000

15-08- Share application a/c Dr

To Share capital a/c

To share allotment

(Being transfer of application

money into share capital a/c)

108000000

90000000

180000000

20-09- Share allotment a/c Dr

To Share capital

( Allotment money due already

72000000

722000000

5

To 8 % debenture application

a/c(Being application money

received)

200000

200000

8 % Debenture application a/c Dr

Debenture interest a/c Dr

To 8 % debenture a/c

(Being debenture are redeemable

with its interest price)

200000

800000

280000

TASK3

Journal entries of RCK limited

Journal entry can be defined as those transactions which are used to record each transaction of

business activities in the books of accounts. These are the main basis for ledger, and financial

statement. Following are the entries of RCK limited

Date Particular Debit Credit

July 2018 Bank a/c Dr

To Share application a/c

(Application money being

received for 108 million shares

@ $1 each)

108000000 108000000

15-08- Share application a/c Dr

To Share capital a/c

To share allotment

(Being transfer of application

money into share capital a/c)

108000000

90000000

180000000

20-09- Share allotment a/c Dr

To Share capital

( Allotment money due already

72000000

722000000

5

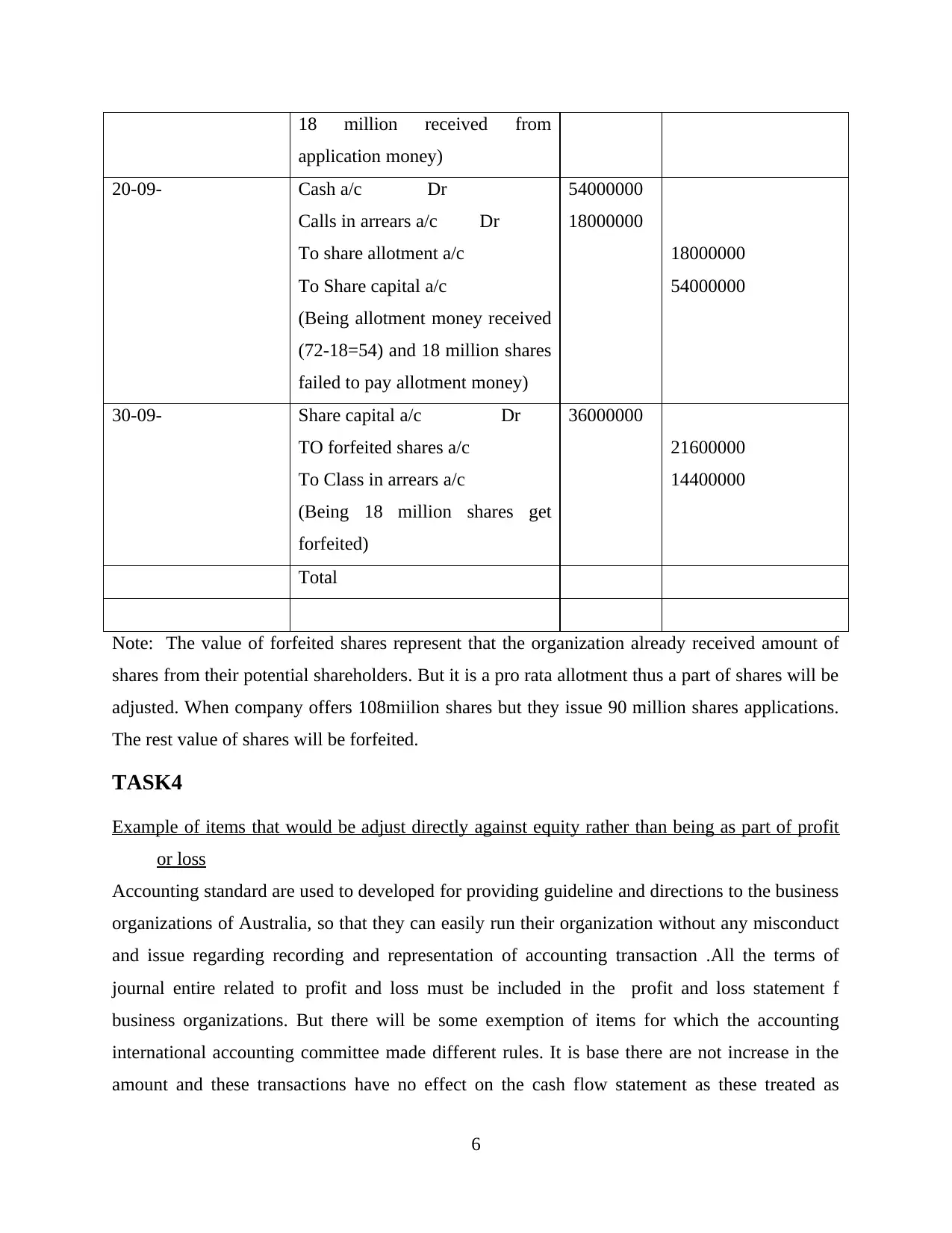

18 million received from

application money)

20-09- Cash a/c Dr

Calls in arrears a/c Dr

To share allotment a/c

To Share capital a/c

(Being allotment money received

(72-18=54) and 18 million shares

failed to pay allotment money)

54000000

18000000

18000000

54000000

30-09- Share capital a/c Dr

TO forfeited shares a/c

To Class in arrears a/c

(Being 18 million shares get

forfeited)

36000000

21600000

14400000

Total

Note: The value of forfeited shares represent that the organization already received amount of

shares from their potential shareholders. But it is a pro rata allotment thus a part of shares will be

adjusted. When company offers 108miilion shares but they issue 90 million shares applications.

The rest value of shares will be forfeited.

TASK4

Example of items that would be adjust directly against equity rather than being as part of profit

or loss

Accounting standard are used to developed for providing guideline and directions to the business

organizations of Australia, so that they can easily run their organization without any misconduct

and issue regarding recording and representation of accounting transaction .All the terms of

journal entire related to profit and loss must be included in the profit and loss statement f

business organizations. But there will be some exemption of items for which the accounting

international accounting committee made different rules. It is base there are not increase in the

amount and these transactions have no effect on the cash flow statement as these treated as

6

application money)

20-09- Cash a/c Dr

Calls in arrears a/c Dr

To share allotment a/c

To Share capital a/c

(Being allotment money received

(72-18=54) and 18 million shares

failed to pay allotment money)

54000000

18000000

18000000

54000000

30-09- Share capital a/c Dr

TO forfeited shares a/c

To Class in arrears a/c

(Being 18 million shares get

forfeited)

36000000

21600000

14400000

Total

Note: The value of forfeited shares represent that the organization already received amount of

shares from their potential shareholders. But it is a pro rata allotment thus a part of shares will be

adjusted. When company offers 108miilion shares but they issue 90 million shares applications.

The rest value of shares will be forfeited.

TASK4

Example of items that would be adjust directly against equity rather than being as part of profit

or loss

Accounting standard are used to developed for providing guideline and directions to the business

organizations of Australia, so that they can easily run their organization without any misconduct

and issue regarding recording and representation of accounting transaction .All the terms of

journal entire related to profit and loss must be included in the profit and loss statement f

business organizations. But there will be some exemption of items for which the accounting

international accounting committee made different rules. It is base there are not increase in the

amount and these transactions have no effect on the cash flow statement as these treated as

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

unrealistic account transaction. All these item should be recognized as those accounts items

which not effect the profit and loss statement and directly link with the liability side of equality.

There will be some items of accounting transactions which directly concern with the adjustment

of equity and in balance sheet and not become the part of profit and loss of statement of business

organization(Ramachandra, S., Olesen, Narayan and Tsoy, 2014).

Other comprehensive income: These are those items which cannot be considered as the part of

profit and loss statement .Theses items shown below line of profit and loss statement. They can

be known as unrealized profit and loss of business assets. For examples if an assets is ready for

sold then the gain aeries from that assets considers as the part of other comprehensive income.

Unrealized profit and loss on bonds: If value of securities to be sold is reduce an or increase tat it

will be treated as unrealized income.

Foreign currency transaction : If organization sales their products and service outside Australia

then gain or loses incurs during the changes of value offering currency should be treated as the

unrealized transaction .

Profit and loss related with pension plans: If government changes the rules and schemes related

to pension plans then the profit earn from these policies should be treated another comprehensive

income.

Australian accounting standard also define the treatment of other comprehensive income. If the

value of assets of business organization increase after its revaluation then it should be treated as

other comprehensive income and the amount of accumulate profit should be added in the liability

side of equity., under the heading of surplus of profits. And if the revaluation effects the

decrement in the value of assets then it should be treated as deduction in the surplus heading of

liability side equity.

Value of unclear dividend: Dividend can be defining as part of revenue which is available for the

shareholders o the business organization. Unclear divided should add in the equity side of the

financial statement. Which describe future dividend value which is distributed in future among

the shareholders (Silva, Vale. and Branco, 2018).

All these items considered as the part of balance sheet and adjust in the equity side of balance

sheet either it increase the surplus value of the equity side or deserves the value of profit and

reserve or surplus account. These items are used for adjusting of unwanted risk and loss it means

within the business organizations.

7

which not effect the profit and loss statement and directly link with the liability side of equality.

There will be some items of accounting transactions which directly concern with the adjustment

of equity and in balance sheet and not become the part of profit and loss of statement of business

organization(Ramachandra, S., Olesen, Narayan and Tsoy, 2014).

Other comprehensive income: These are those items which cannot be considered as the part of

profit and loss statement .Theses items shown below line of profit and loss statement. They can

be known as unrealized profit and loss of business assets. For examples if an assets is ready for

sold then the gain aeries from that assets considers as the part of other comprehensive income.

Unrealized profit and loss on bonds: If value of securities to be sold is reduce an or increase tat it

will be treated as unrealized income.

Foreign currency transaction : If organization sales their products and service outside Australia

then gain or loses incurs during the changes of value offering currency should be treated as the

unrealized transaction .

Profit and loss related with pension plans: If government changes the rules and schemes related

to pension plans then the profit earn from these policies should be treated another comprehensive

income.

Australian accounting standard also define the treatment of other comprehensive income. If the

value of assets of business organization increase after its revaluation then it should be treated as

other comprehensive income and the amount of accumulate profit should be added in the liability

side of equity., under the heading of surplus of profits. And if the revaluation effects the

decrement in the value of assets then it should be treated as deduction in the surplus heading of

liability side equity.

Value of unclear dividend: Dividend can be defining as part of revenue which is available for the

shareholders o the business organization. Unclear divided should add in the equity side of the

financial statement. Which describe future dividend value which is distributed in future among

the shareholders (Silva, Vale. and Branco, 2018).

All these items considered as the part of balance sheet and adjust in the equity side of balance

sheet either it increase the surplus value of the equity side or deserves the value of profit and

reserve or surplus account. These items are used for adjusting of unwanted risk and loss it means

within the business organizations.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK5

Cash flow statement of Fool’s Paradise Limited

Cash flow: it can be defined as the statement which is used to determine the value of cash inflow

and out flow activities in a systematic manner. Cash flow is a part of financial reports and it can

be calculated by direct and indirect method of business accounting(Cruz, and Dias-Teixeira,

2016). One of the most important capital budgeting tasks for the evaluation of the project capital

investments is the estimation of the relevant cash flows for each project, which refers to the

incremental cash flow arising from each project. Because companies rely on accrual accounting

rather than cash accounting, adjustments are necessary to derive the cash flows from the

conventional financial accounting records. Estimating project cash flows is critical because

inaccurate or unreliable data can corrupt the entire capital budgeting process. Accurately

forecasting cash flows can be an arduous task. Experience help to identify factors influencing the

cash flows of some projects, but historical data may be unavailable on others. Estimating a new

project's cash flows involves great uncertainty and may be little more than educated guesswork.

Therefore, those individuals who prepare cash flow estimates should explicitly state the

assumptions underlying their estimates. Corporate managers should thoroughly evaluate and test

these assumptions, because faulty assumptions can easily translate into bad investment decisions.

The financial staff plays a key role in the cash flow estimation process by coordinating with

other departments, maintaining consistency of assumptions, and eliminating biases in the

forecasts. Firms use several methods to estimate cash flows. Some firms rely on sophisticated

mathematical models and computer simulation. Others use more qualitative methods to forecast

cash flows including management's subjective estimates and a survey of expert opinions. Large

corporations often combine quantitative and judgmental forecasts to improve their estimates.

In the accounting standard of Austria there will be a separate provision has to be made regarding

cash flow adjustment, which determine the whole process used the provision and last regarding

the cash flow statement. It considers 3 activities which is operating investing financial and

investing activities. Cash flow statement is different from fund flow statement as fund down

statement considered the calculation of working capital more this format is no made working

capital statement it just show all the calculation and adjustment within a systematic format

(Vasconcelos de Andrade and Dal Ri Murcia, 2019).

8

Cash flow statement of Fool’s Paradise Limited

Cash flow: it can be defined as the statement which is used to determine the value of cash inflow

and out flow activities in a systematic manner. Cash flow is a part of financial reports and it can

be calculated by direct and indirect method of business accounting(Cruz, and Dias-Teixeira,

2016). One of the most important capital budgeting tasks for the evaluation of the project capital

investments is the estimation of the relevant cash flows for each project, which refers to the

incremental cash flow arising from each project. Because companies rely on accrual accounting

rather than cash accounting, adjustments are necessary to derive the cash flows from the

conventional financial accounting records. Estimating project cash flows is critical because

inaccurate or unreliable data can corrupt the entire capital budgeting process. Accurately

forecasting cash flows can be an arduous task. Experience help to identify factors influencing the

cash flows of some projects, but historical data may be unavailable on others. Estimating a new

project's cash flows involves great uncertainty and may be little more than educated guesswork.

Therefore, those individuals who prepare cash flow estimates should explicitly state the

assumptions underlying their estimates. Corporate managers should thoroughly evaluate and test

these assumptions, because faulty assumptions can easily translate into bad investment decisions.

The financial staff plays a key role in the cash flow estimation process by coordinating with

other departments, maintaining consistency of assumptions, and eliminating biases in the

forecasts. Firms use several methods to estimate cash flows. Some firms rely on sophisticated

mathematical models and computer simulation. Others use more qualitative methods to forecast

cash flows including management's subjective estimates and a survey of expert opinions. Large

corporations often combine quantitative and judgmental forecasts to improve their estimates.

In the accounting standard of Austria there will be a separate provision has to be made regarding

cash flow adjustment, which determine the whole process used the provision and last regarding

the cash flow statement. It considers 3 activities which is operating investing financial and

investing activities. Cash flow statement is different from fund flow statement as fund down

statement considered the calculation of working capital more this format is no made working

capital statement it just show all the calculation and adjustment within a systematic format

(Vasconcelos de Andrade and Dal Ri Murcia, 2019).

8

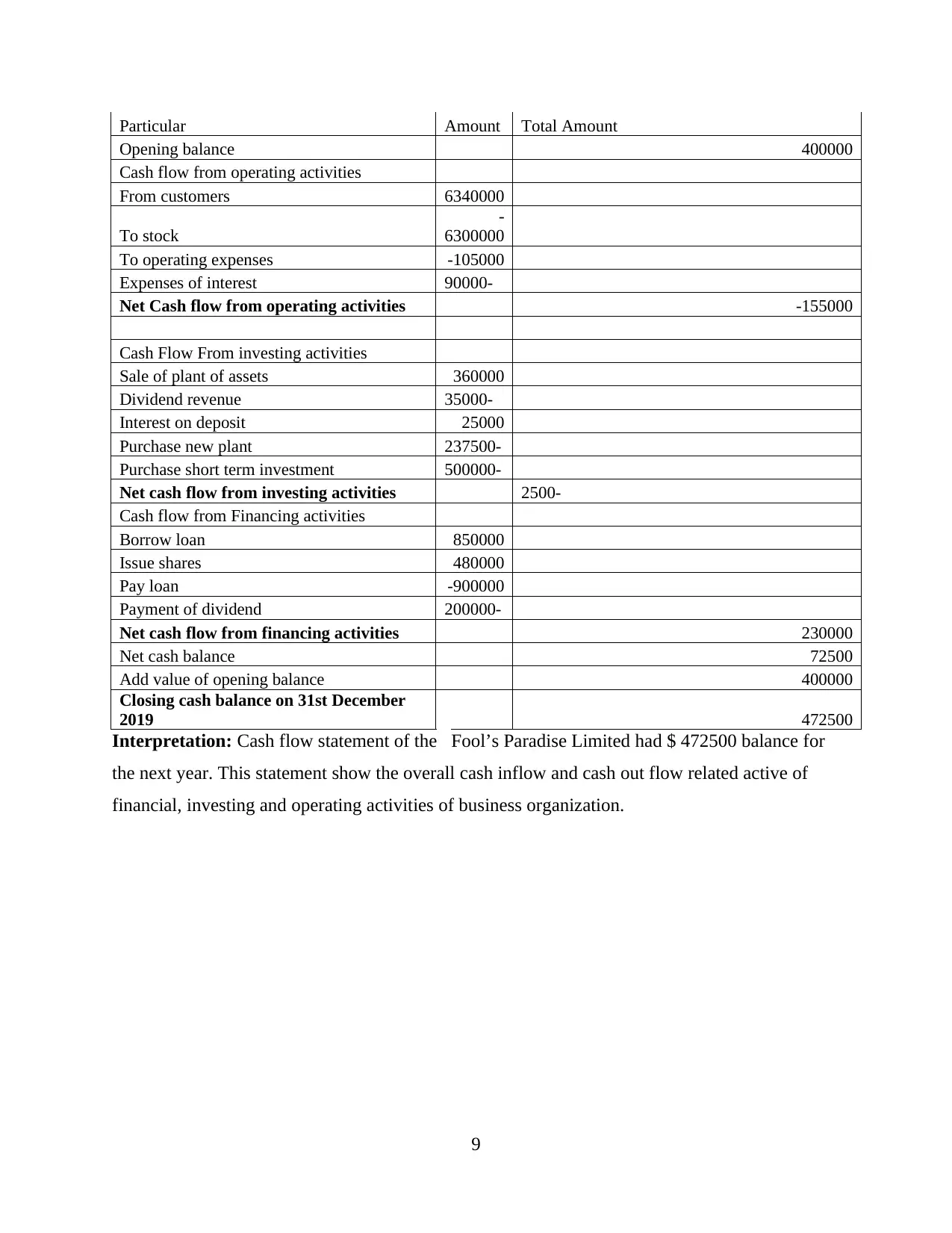

Particular Amount Total Amount

Opening balance 400000

Cash flow from operating activities

From customers 6340000

To stock

-

6300000

To operating expenses -105000

Expenses of interest 90000-

Net Cash flow from operating activities -155000

Cash Flow From investing activities

Sale of plant of assets 360000

Dividend revenue 35000-

Interest on deposit 25000

Purchase new plant 237500-

Purchase short term investment 500000-

Net cash flow from investing activities 2500-

Cash flow from Financing activities

Borrow loan 850000

Issue shares 480000

Pay loan -900000

Payment of dividend 200000-

Net cash flow from financing activities 230000

Net cash balance 72500

Add value of opening balance 400000

Closing cash balance on 31st December

2019 472500

Interpretation: Cash flow statement of the Fool’s Paradise Limited had $ 472500 balance for

the next year. This statement show the overall cash inflow and cash out flow related active of

financial, investing and operating activities of business organization.

9

Opening balance 400000

Cash flow from operating activities

From customers 6340000

To stock

-

6300000

To operating expenses -105000

Expenses of interest 90000-

Net Cash flow from operating activities -155000

Cash Flow From investing activities

Sale of plant of assets 360000

Dividend revenue 35000-

Interest on deposit 25000

Purchase new plant 237500-

Purchase short term investment 500000-

Net cash flow from investing activities 2500-

Cash flow from Financing activities

Borrow loan 850000

Issue shares 480000

Pay loan -900000

Payment of dividend 200000-

Net cash flow from financing activities 230000

Net cash balance 72500

Add value of opening balance 400000

Closing cash balance on 31st December

2019 472500

Interpretation: Cash flow statement of the Fool’s Paradise Limited had $ 472500 balance for

the next year. This statement show the overall cash inflow and cash out flow related active of

financial, investing and operating activities of business organization.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFRENCES

Books and journals

Sanguino, R., Barroso, A. and Gochhait, S., 2018. Entrepreneurship in Family Firms in

Developed and Developing Countries. In Entrepreneurship and Structural Change in

Dynamic Territories (pp. 91-108). Springer, Cham.

Arimany, N., Fitó, M .A., Moya, S. and Orgaz, N., 2018. What lies behind compliance with

operating leases disclosure?. Spanish Journal of Finance and Accounting/Revista

Española de Financiación y Contabilidad, 47(4), pp.485-506.

Tayob, S., 2019. Molecular Halal: Producing, Debating, and Evading Halal Certification in

South Africa. In Insatiable Appetite: Food as Cultural Signifier in the Middle East and

Beyond (pp. 100-118). Brill.

Silva, C., Vale, J. and Branco, M., 2018, September. Intellectual capital disclosure: a study

applied to the Shanghai ranking. In ECKM 2018 19th European Conference on

Knowledge Management (p. 783). Academic Conferences and publishing limited.

Ramachandra, S., Olesen, K., Narayan, A. K. and Tsoy, A., 2014. Compliance with international

financial reporting paradigm: A tale of two transition paths. CORPORATE OWNERSHIP

& CONTROL, p.338.

Cruz, J. and Dias-Teixeira, M., 2016. Work-related musculoskeletal disorders among the

hairdressers: a pilot study. In Advances in Physical Ergonomics and Human Factors (pp.

133-140). Springer, Cham.

Vasconcelos de Andrade, G. and Dal Ri Murcia, F., 2019. A critical analysis on the additional

adjustments considered in the disclosure of the non-GAAP" adjusted EBITDA" measure

in the reports of Brazilian listed companies. Revista de Educação e Pesquisa em

Contabilidade, 13(4).

10

Books and journals

Sanguino, R., Barroso, A. and Gochhait, S., 2018. Entrepreneurship in Family Firms in

Developed and Developing Countries. In Entrepreneurship and Structural Change in

Dynamic Territories (pp. 91-108). Springer, Cham.

Arimany, N., Fitó, M .A., Moya, S. and Orgaz, N., 2018. What lies behind compliance with

operating leases disclosure?. Spanish Journal of Finance and Accounting/Revista

Española de Financiación y Contabilidad, 47(4), pp.485-506.

Tayob, S., 2019. Molecular Halal: Producing, Debating, and Evading Halal Certification in

South Africa. In Insatiable Appetite: Food as Cultural Signifier in the Middle East and

Beyond (pp. 100-118). Brill.

Silva, C., Vale, J. and Branco, M., 2018, September. Intellectual capital disclosure: a study

applied to the Shanghai ranking. In ECKM 2018 19th European Conference on

Knowledge Management (p. 783). Academic Conferences and publishing limited.

Ramachandra, S., Olesen, K., Narayan, A. K. and Tsoy, A., 2014. Compliance with international

financial reporting paradigm: A tale of two transition paths. CORPORATE OWNERSHIP

& CONTROL, p.338.

Cruz, J. and Dias-Teixeira, M., 2016. Work-related musculoskeletal disorders among the

hairdressers: a pilot study. In Advances in Physical Ergonomics and Human Factors (pp.

133-140). Springer, Cham.

Vasconcelos de Andrade, G. and Dal Ri Murcia, F., 2019. A critical analysis on the additional

adjustments considered in the disclosure of the non-GAAP" adjusted EBITDA" measure

in the reports of Brazilian listed companies. Revista de Educação e Pesquisa em

Contabilidade, 13(4).

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.