MAA363 Corporate Accounting Project - Taxable Profit & Tax Liability

VerifiedAdded on 2020/07/22

|5

|1100

|70

Project

AI Summary

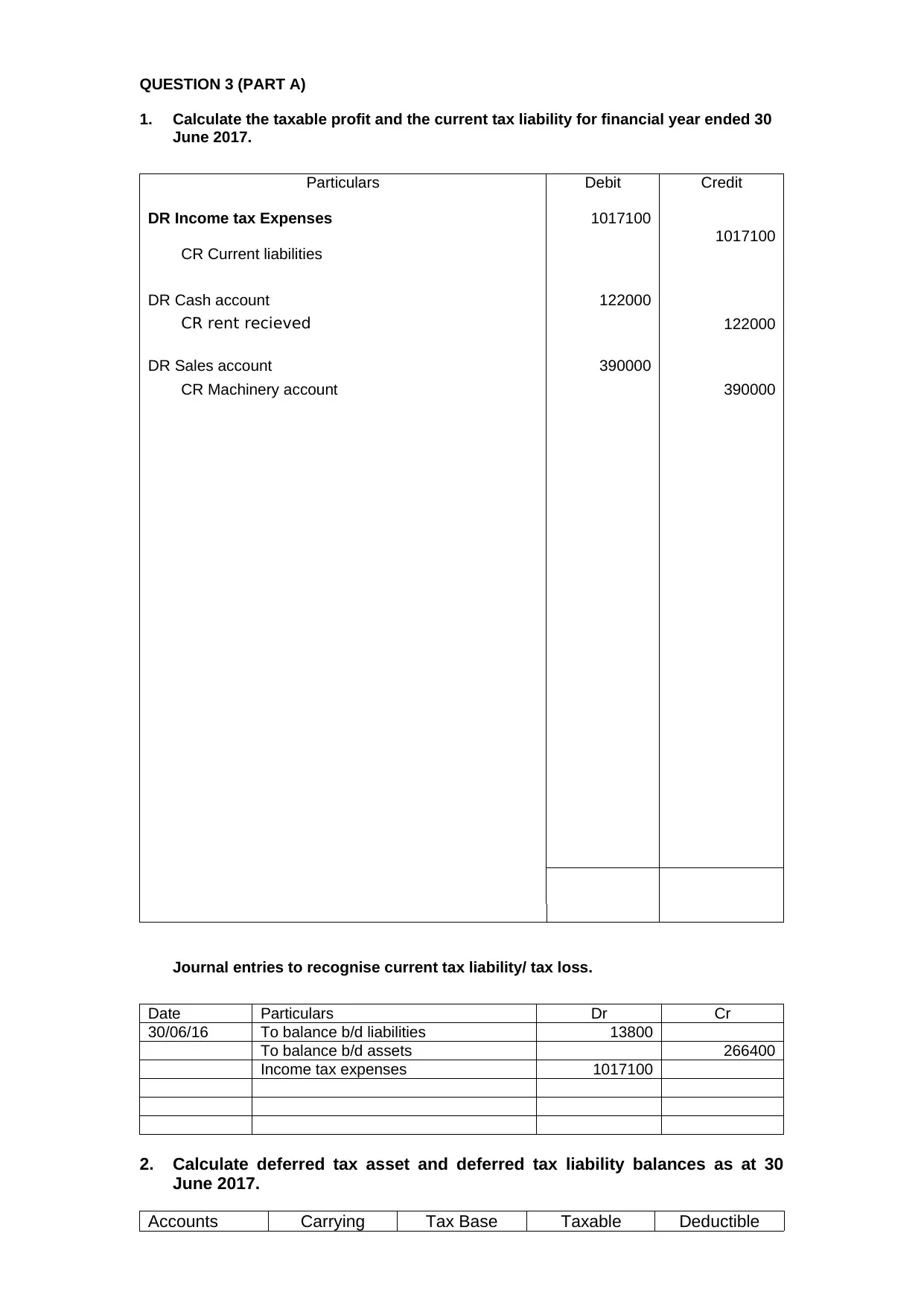

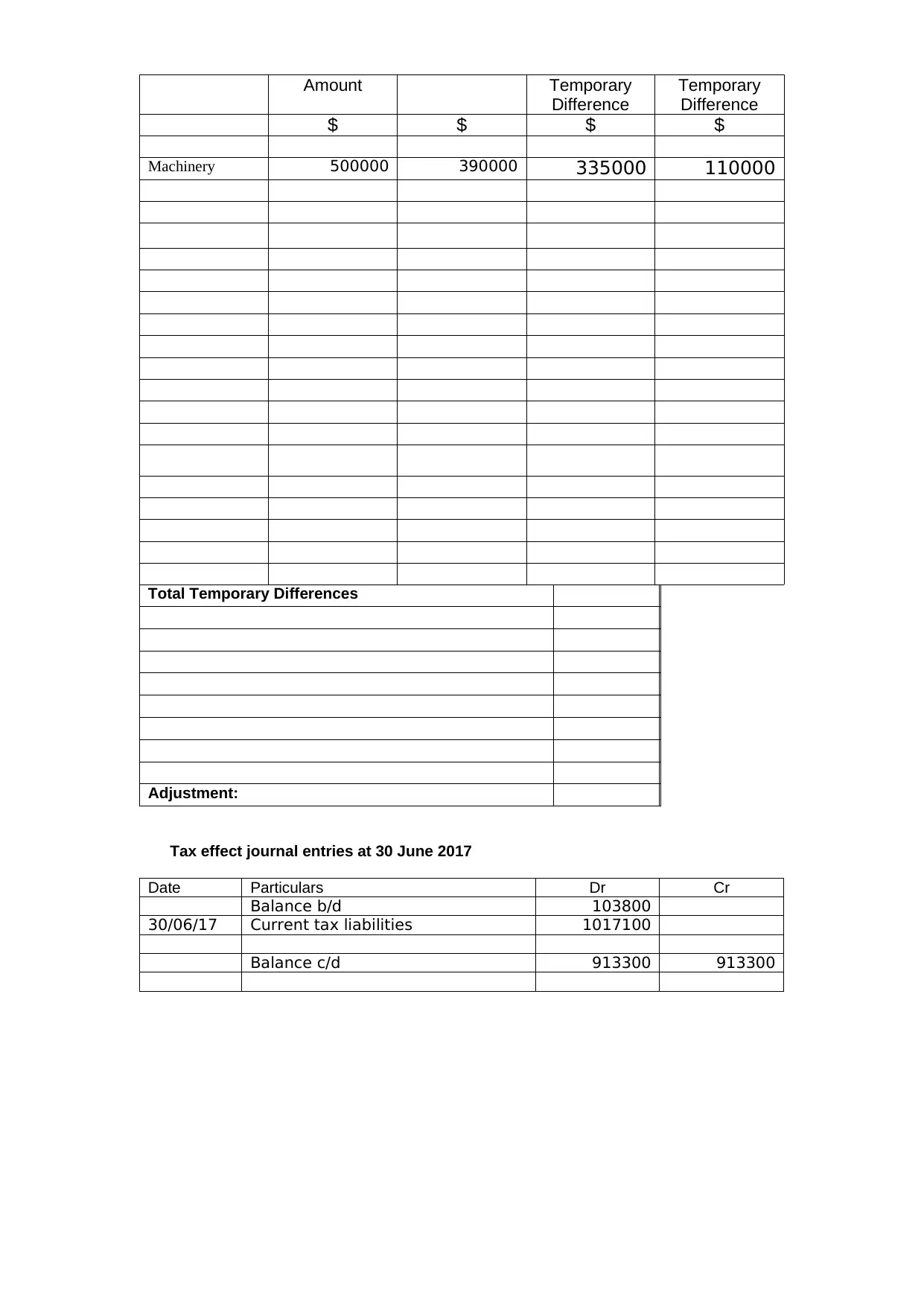

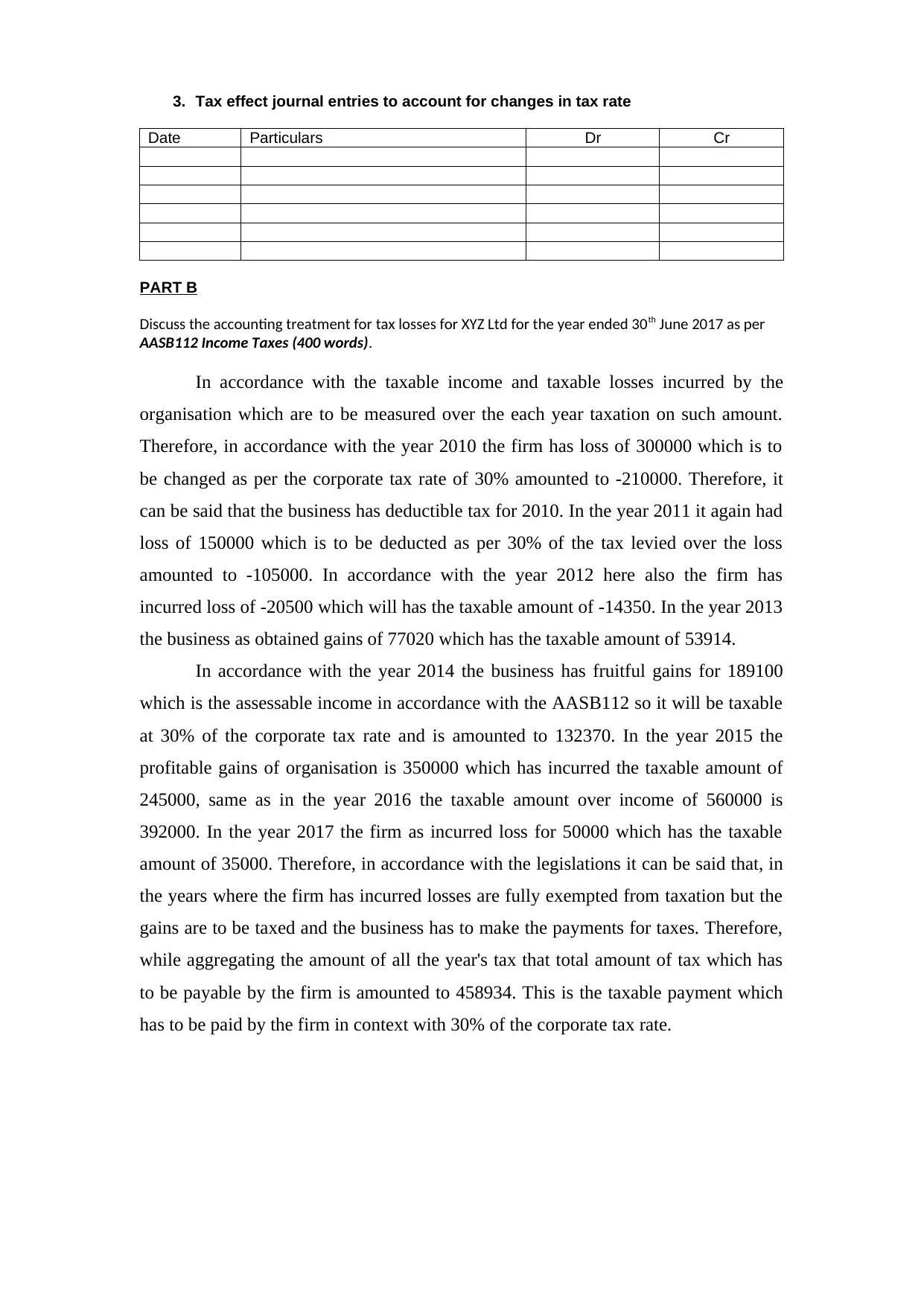

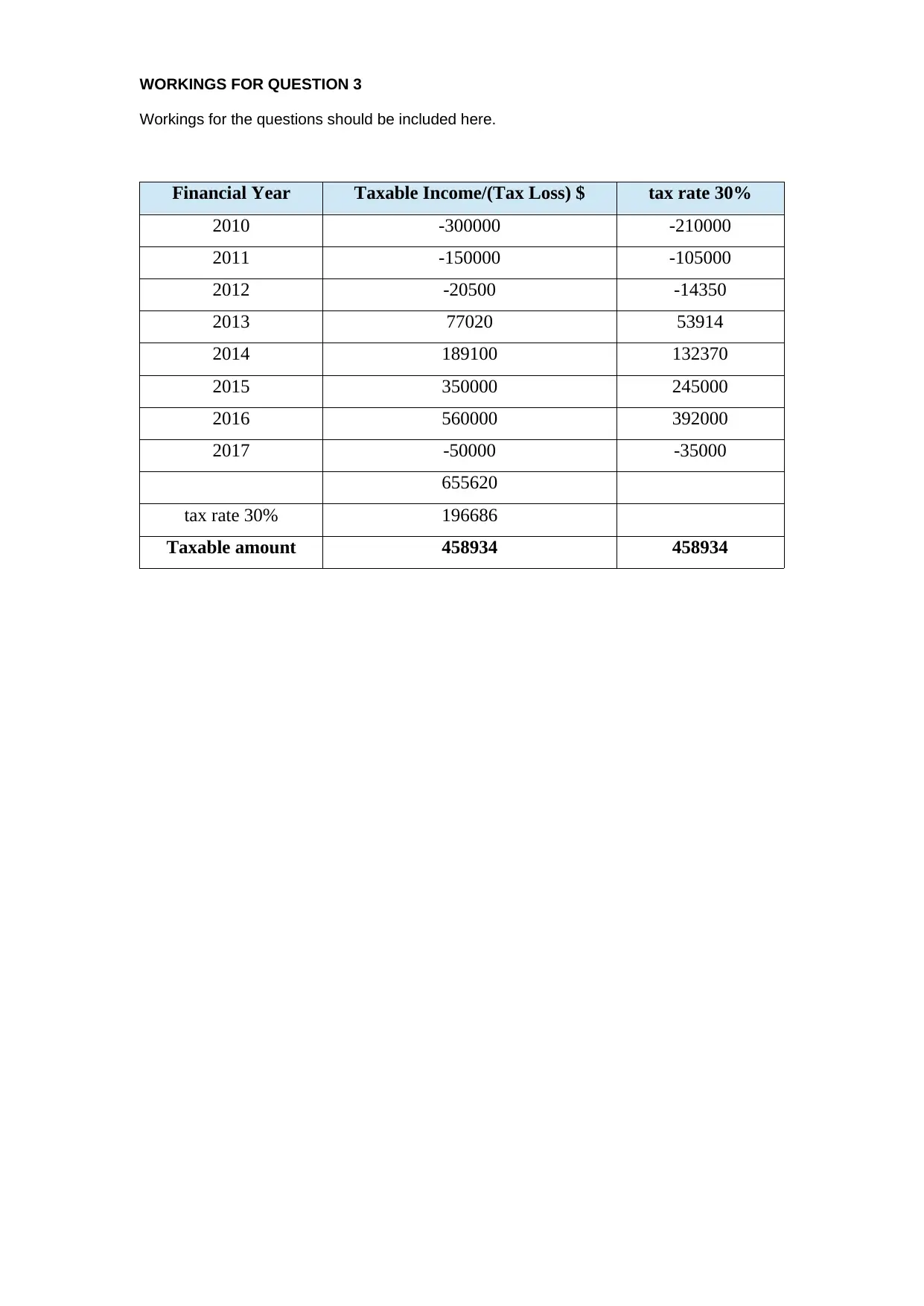

This project addresses corporate accounting principles related to taxable profit, current tax liability, and deferred tax assets and liabilities. Part A involves calculating the taxable profit and current tax liability for the financial year ending June 30, 2017, including relevant journal entries. It also calculates deferred tax asset and liability balances. Part B discusses the accounting treatment for tax losses under AASB112 Income Taxes, analyzing tax losses and gains from 2010 to 2017 and calculating the total tax payable. The solution includes detailed workings to support the calculations and analysis. This assignment showcases the application of accounting standards in a practical context, providing a comprehensive understanding of tax-related accounting procedures.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.