Corporate Accounting: Income Tax Assignment for HI5020, T1 2020

VerifiedAdded on 2022/09/11

|11

|563

|15

Homework Assignment

AI Summary

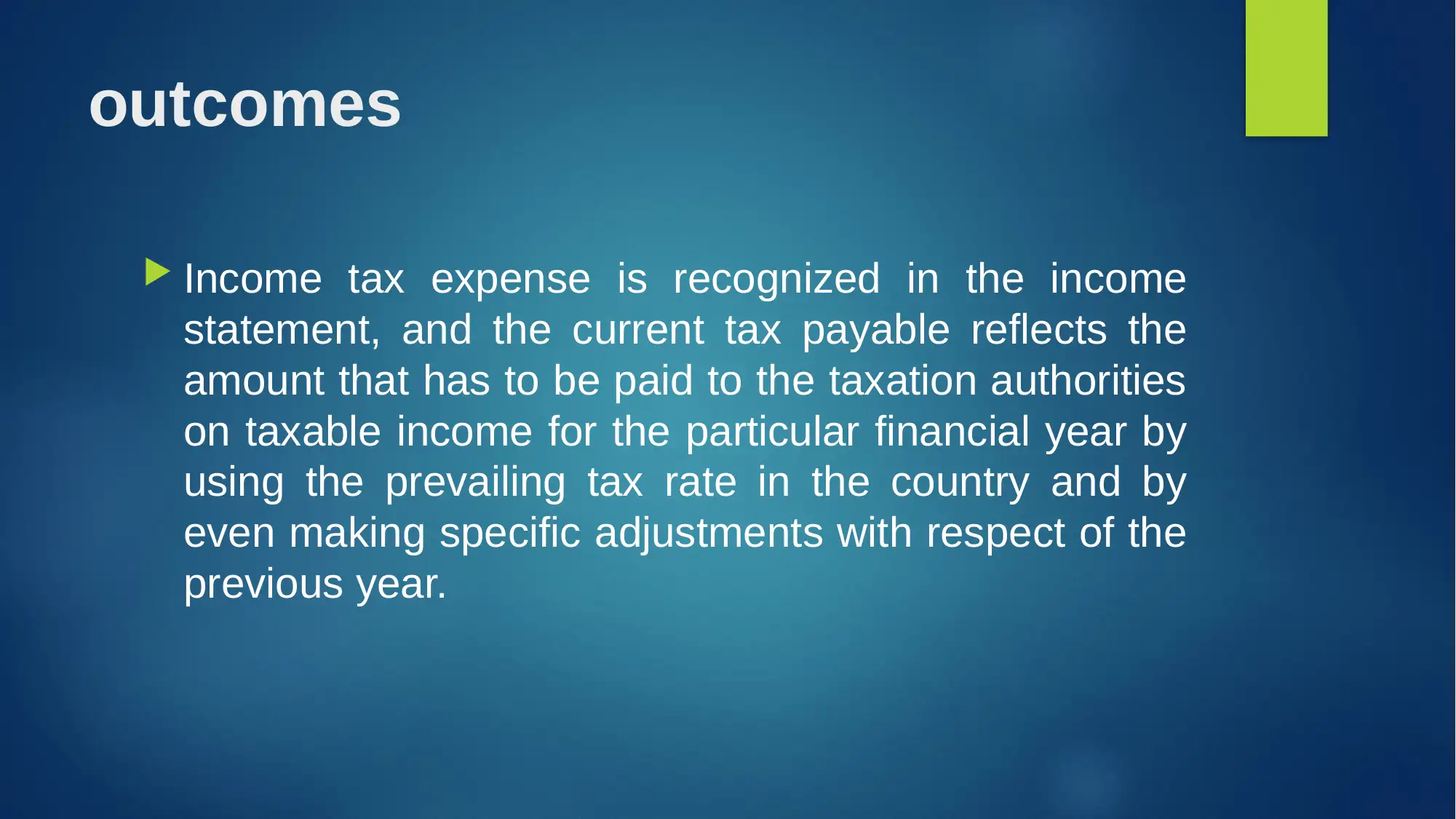

This assignment solution analyzes the impact of income tax on corporate accounting, using Woolworths corporation ltd. as a case study. It defines key terminologies such as accounting profit, taxable profit, temporary differences, deferred tax assets and liabilities, and income tax expense. The solution explains the differences between income tax paid and income tax expense, highlighting the role of deferred tax. It also clarifies the concepts of current tax assets and the reasons for differences in tax amounts, emphasizing the divergence between accounting standards and tax regulations. The solution concludes by summarizing how income tax expense is recognized and the nature of current tax payable. This comprehensive overview helps students understand and apply accounting principles related to income tax in a corporate setting.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.