University Corporate Accounting Report: Wesfarmers Financial Analysis

VerifiedAdded on 2021/06/16

|15

|2617

|169

Report

AI Summary

This report provides a comprehensive analysis of Wesfarmers Ltd's corporate accounting practices, examining its financial statements for the years 2015, 2016, and 2017. The analysis delves into the cash flow statement, dissecting operating, investing, and financing activities, and highlighting significant trends such as the increase in cash inflow from operating activities in 2017. The report also scrutinizes the statement of comprehensive income, focusing on the profit attributable to the parent firm and other comprehensive income components, including foreign currency translation and cash flow hedge reserves. Furthermore, it addresses the treatment of income tax, including current and deferred tax assets and liabilities, and reconciles income tax expense with cash flow payments. The report concludes by comparing income tax expense in the income account with income tax disbursements in the cash flow statement, offering insights into the company's financial performance and accounting strategies.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

University Name

Student Name

Authors’ Note

Corporate Accounting

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

CORPORATE ACCOUNTING

Table of Contents

Solution i)...................................................................................................................................2

Solution ii)..................................................................................................................................3

Solution iii).................................................................................................................................5

Solution iv).................................................................................................................................6

Solution v)..................................................................................................................................6

Solution vi).................................................................................................................................7

Solution to vii)............................................................................................................................7

Solution viii)...............................................................................................................................8

Solution ix).................................................................................................................................8

Solution x)..................................................................................................................................9

Solution xi).................................................................................................................................9

References................................................................................................................................10

Appendix:.................................................................................................................................11

CORPORATE ACCOUNTING

Table of Contents

Solution i)...................................................................................................................................2

Solution ii)..................................................................................................................................3

Solution iii).................................................................................................................................5

Solution iv).................................................................................................................................6

Solution v)..................................................................................................................................6

Solution vi).................................................................................................................................7

Solution to vii)............................................................................................................................7

Solution viii)...............................................................................................................................8

Solution ix).................................................................................................................................8

Solution x)..................................................................................................................................9

Solution xi).................................................................................................................................9

References................................................................................................................................10

Appendix:.................................................................................................................................11

3

CORPORATE ACCOUNTING

The company selected for evaluating the yearly financial report is Wesfarmers Ltd that is an

Australian multinational that operates in the segment of retail, industrial and safety products,

coal mining, chemicals as well as fertilisers. This company is listed in the Australian Stock

Exchange (ASX) has an operating income of approximately AUD 3.61 billion, total assets of

AUD 0.78 billion and net income of AUD 2.35 billion.

Solution i)

The cash flow statement of the firm Wesfarmers Limited consist of conventional three

sections namely cash flow from operational, investing along with financing activities. In

operating actions, the cash flows are either provided by or utilized in primarily depreciation,

definite adjustments to net earnings, alterations in accounts receivables, liabilities, inventories

as well as alterations in diverse operating actions. As per the financial assertions of the firm,

list of items under the operational activities include receipts of the firm from their customers,

disbursements to diverse suppliers as well as employees, movement in particularly finance

advances as well as loans, firm’s dividends along with distributions accepted from associates,

interests accepted, costs of firms borrowings together with payment of income tax

(Schaltegger and Burritt 2017). Again, the exhaustive list of items mentioned under investing

activities includes disbursements for property, plant, and equipment (simply referred to as

PPE) along with intangibles. Also cash used in investing functionalities comprise of proceeds

from mainly sale or else disposal of the PPE, overall proceeds from disposal of businesses

along with associates, overall investments in mainly associates and varied joint arrangements

of the firm. Also, for the purpose of investing activities, cash is used for acquisition of

various subsidiaries and redemption of otherwise investment in loan notes (Siew 2015).

Again, the list of items that are listed under the cash used for Wesfarmers financing activities

take in proceeds of the company from borrowing, pay offs or in other words repayments of

CORPORATE ACCOUNTING

The company selected for evaluating the yearly financial report is Wesfarmers Ltd that is an

Australian multinational that operates in the segment of retail, industrial and safety products,

coal mining, chemicals as well as fertilisers. This company is listed in the Australian Stock

Exchange (ASX) has an operating income of approximately AUD 3.61 billion, total assets of

AUD 0.78 billion and net income of AUD 2.35 billion.

Solution i)

The cash flow statement of the firm Wesfarmers Limited consist of conventional three

sections namely cash flow from operational, investing along with financing activities. In

operating actions, the cash flows are either provided by or utilized in primarily depreciation,

definite adjustments to net earnings, alterations in accounts receivables, liabilities, inventories

as well as alterations in diverse operating actions. As per the financial assertions of the firm,

list of items under the operational activities include receipts of the firm from their customers,

disbursements to diverse suppliers as well as employees, movement in particularly finance

advances as well as loans, firm’s dividends along with distributions accepted from associates,

interests accepted, costs of firms borrowings together with payment of income tax

(Schaltegger and Burritt 2017). Again, the exhaustive list of items mentioned under investing

activities includes disbursements for property, plant, and equipment (simply referred to as

PPE) along with intangibles. Also cash used in investing functionalities comprise of proceeds

from mainly sale or else disposal of the PPE, overall proceeds from disposal of businesses

along with associates, overall investments in mainly associates and varied joint arrangements

of the firm. Also, for the purpose of investing activities, cash is used for acquisition of

various subsidiaries and redemption of otherwise investment in loan notes (Siew 2015).

Again, the list of items that are listed under the cash used for Wesfarmers financing activities

take in proceeds of the company from borrowing, pay offs or in other words repayments of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

CORPORATE ACCOUNTING

borrowed amounts and equity dividend disbursed. Also, cash is used for proceeds from

specifically exercise of different in-substance options mainly covered in employee share plan.

Solution ii)

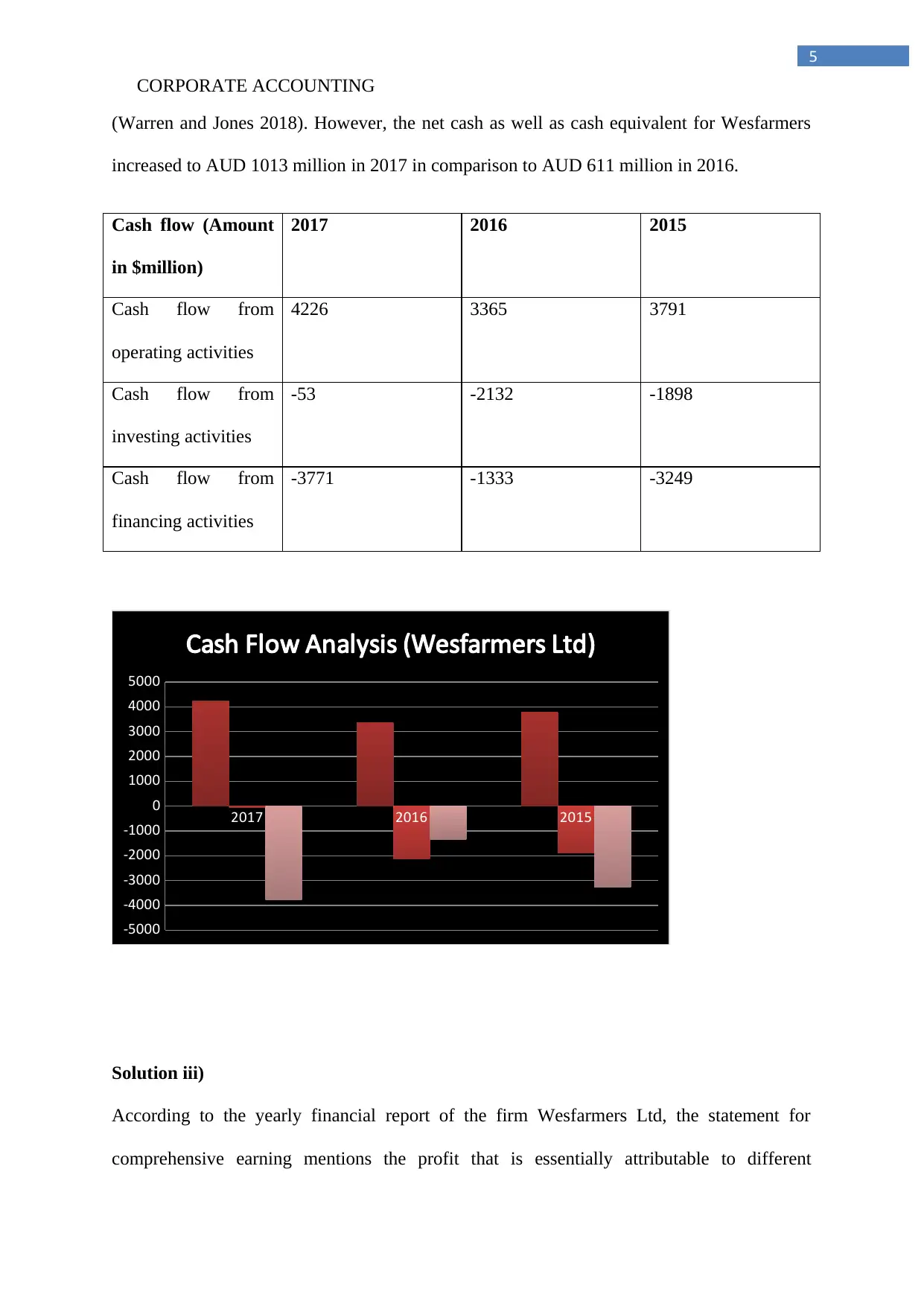

Analytical evaluation of the cash flow assertion of the firm Wesfarmers reveal that cash

utilized for operative actions is documented to be AUD 4226 million in the year 2017 in

comparison to the year ago figure that stood at approximately AUD 3365 million. Thus, it

can be seen that the cash flow from operating actions declined from AUD3791 in 2015 to

AUD 3365 million in 2016 and thereafter again increased during 2017 (Wesfarmers.com.au

2018). The increase in cash inflow during 2017 is mainly due to increase in receipts from the

company’s customers, increase in interests received and at the same time decrease in costs

incurred for borrowing and decrease in disbursements for income tax paid (Tschopp and

Nastanski 2014).

Detailed study of cash utilized in investing activities reflect that cash outflow enhanced

sharply from (AUD 1898 million) in 2015 to (AUD 2132 million) in 2016. However, it

declined significantly to just (AUD 53 million) (Wesfarmers.com.au 2018). This is mainly

due to decrease in outflow of cash for payments for PPE, decline in outflow for acquirement

of subsidiaries (net of particularly cash acquired) and at the higher inflow of cash from

proceeds from disposal of PPE and augmented proceeds from sale of mainly businesses as

well as associates.

Again, it can be hereby observed that cash outflow for the firm Wesfarmers’s financing

activities decreased to (AUD 1333 million) in 2016 in comparison to the figure of (AUD

3249 million) (Wesfarmers.com.au 2018). However, the same is observed to have again

considerably increased to (AUD 3771 million). This is chiefly owing to the fact that proceeds

obtained from firm’s borrowings decreased while pay off for the borrowings increased

CORPORATE ACCOUNTING

borrowed amounts and equity dividend disbursed. Also, cash is used for proceeds from

specifically exercise of different in-substance options mainly covered in employee share plan.

Solution ii)

Analytical evaluation of the cash flow assertion of the firm Wesfarmers reveal that cash

utilized for operative actions is documented to be AUD 4226 million in the year 2017 in

comparison to the year ago figure that stood at approximately AUD 3365 million. Thus, it

can be seen that the cash flow from operating actions declined from AUD3791 in 2015 to

AUD 3365 million in 2016 and thereafter again increased during 2017 (Wesfarmers.com.au

2018). The increase in cash inflow during 2017 is mainly due to increase in receipts from the

company’s customers, increase in interests received and at the same time decrease in costs

incurred for borrowing and decrease in disbursements for income tax paid (Tschopp and

Nastanski 2014).

Detailed study of cash utilized in investing activities reflect that cash outflow enhanced

sharply from (AUD 1898 million) in 2015 to (AUD 2132 million) in 2016. However, it

declined significantly to just (AUD 53 million) (Wesfarmers.com.au 2018). This is mainly

due to decrease in outflow of cash for payments for PPE, decline in outflow for acquirement

of subsidiaries (net of particularly cash acquired) and at the higher inflow of cash from

proceeds from disposal of PPE and augmented proceeds from sale of mainly businesses as

well as associates.

Again, it can be hereby observed that cash outflow for the firm Wesfarmers’s financing

activities decreased to (AUD 1333 million) in 2016 in comparison to the figure of (AUD

3249 million) (Wesfarmers.com.au 2018). However, the same is observed to have again

considerably increased to (AUD 3771 million). This is chiefly owing to the fact that proceeds

obtained from firm’s borrowings decreased while pay off for the borrowings increased

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

CORPORATE ACCOUNTING

(Warren and Jones 2018). However, the net cash as well as cash equivalent for Wesfarmers

increased to AUD 1013 million in 2017 in comparison to AUD 611 million in 2016.

Cash flow (Amount

in $million)

2017 2016 2015

Cash flow from

operating activities

4226 3365 3791

Cash flow from

investing activities

-53 -2132 -1898

Cash flow from

financing activities

-3771 -1333 -3249

2017 2016 2015

-5000

-4000

-3000

-2000

-1000

0

1000

2000

3000

4000

5000

Cash Flow Analysis (Wesfarmers Ltd)

Solution iii)

According to the yearly financial report of the firm Wesfarmers Ltd, the statement for

comprehensive earning mentions the profit that is essentially attributable to different

CORPORATE ACCOUNTING

(Warren and Jones 2018). However, the net cash as well as cash equivalent for Wesfarmers

increased to AUD 1013 million in 2017 in comparison to AUD 611 million in 2016.

Cash flow (Amount

in $million)

2017 2016 2015

Cash flow from

operating activities

4226 3365 3791

Cash flow from

investing activities

-53 -2132 -1898

Cash flow from

financing activities

-3771 -1333 -3249

2017 2016 2015

-5000

-4000

-3000

-2000

-1000

0

1000

2000

3000

4000

5000

Cash Flow Analysis (Wesfarmers Ltd)

Solution iii)

According to the yearly financial report of the firm Wesfarmers Ltd, the statement for

comprehensive earning mentions the profit that is essentially attributable to different

6

CORPORATE ACCOUNTING

members of particularly the parent firm. This is recorded to be AUD 2873 million in 2017

while the same was documented to be AUD 407 million in 2016 (Wesfarmers.com.au 2018).

This assertion also includes other comprehensive income that comprises of varied items that

might perhaps be reclassified for profit/loss of the firm (Siew 2015). As such, this includes

reserves for foreign currency translation that mentions the variance in exchange on definite

translation of varied foreign operations. However, exchange variance was registered to be

(AUD 2 million) during 2017 while the same was registered to be AUD 15 million during

2016 (Wesfarmers.com.au 2018). Also, this statement for comprehensive earning reflects

cash flow reserve for hedge. This hedge reserve contains unrealised losses on particularly

hedges for cash reserve, varied realised losses of the firm that is transferred to total profit,

diverse realised loss/profit that gets transferred to various non-financial resources of the

company, share of different associates along with joint venture reserves together with tax

effect. Also, this statement mentions about the items that shall not be reclassified for the

firm’s gain or else loss and takes in retained earnings (Brooks 2015). In the end, this

pronouncement reflects overall comprehensive earning of Wesfarmers for the particular

financial year that is essentially net of total tax amount, and is attributable to different

members of the parent company. However, the total comprehensive income stands at AUD

2891 million in 2017 while the same was recorded to be AUD 329 during 2016

(Wesfarmers.com.au 2018).

Solution iv)

The comprehensive income of Wesfarmers recorded to be AUD 2891 million is significantly

high during the period 2017 in comparison to 2016 (Wesfarmers.com.au 2018). This is

mainly because of higher amount of profit attributable to different members of the parent

firm. Also, an outflow for exchange difference can also be noticed. Further, there is increased

CORPORATE ACCOUNTING

members of particularly the parent firm. This is recorded to be AUD 2873 million in 2017

while the same was documented to be AUD 407 million in 2016 (Wesfarmers.com.au 2018).

This assertion also includes other comprehensive income that comprises of varied items that

might perhaps be reclassified for profit/loss of the firm (Siew 2015). As such, this includes

reserves for foreign currency translation that mentions the variance in exchange on definite

translation of varied foreign operations. However, exchange variance was registered to be

(AUD 2 million) during 2017 while the same was registered to be AUD 15 million during

2016 (Wesfarmers.com.au 2018). Also, this statement for comprehensive earning reflects

cash flow reserve for hedge. This hedge reserve contains unrealised losses on particularly

hedges for cash reserve, varied realised losses of the firm that is transferred to total profit,

diverse realised loss/profit that gets transferred to various non-financial resources of the

company, share of different associates along with joint venture reserves together with tax

effect. Also, this statement mentions about the items that shall not be reclassified for the

firm’s gain or else loss and takes in retained earnings (Brooks 2015). In the end, this

pronouncement reflects overall comprehensive earning of Wesfarmers for the particular

financial year that is essentially net of total tax amount, and is attributable to different

members of the parent company. However, the total comprehensive income stands at AUD

2891 million in 2017 while the same was recorded to be AUD 329 during 2016

(Wesfarmers.com.au 2018).

Solution iv)

The comprehensive income of Wesfarmers recorded to be AUD 2891 million is significantly

high during the period 2017 in comparison to 2016 (Wesfarmers.com.au 2018). This is

mainly because of higher amount of profit attributable to different members of the parent

firm. Also, an outflow for exchange difference can also be noticed. Further, there is increased

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

CORPORATE ACCOUNTING

outflow of unrealised losses on particularly various losses on mainly hedges of cash flow

(Siew 2015).

Solution v)

As rightly indicated by Tschopp and Nastanski (2014), other comprehensive income also

simply referred to as OCI is said to contain varied items of particularly of firm’s income as

well as expenses incurred (counting adjustments of reclassification) which are not necessarily

identified in the assertion for profit and loss of reporting entities. Essentially, the alterations

in the amount of equity during a specified period ensuing from business dealings as well as

other incidents other than the alterations from business transactions oriented to owners in

their potential as owners. On the other hand, the profit and loss assertion needs to include

outcomes of the transactions, different consumptions along with impairment of assets and

satisfaction of liabilities during the period in which they take place. In addition to this, the P-

L statement would also identify all the alterations in the asset costs and liability costs in

addition to any sort of profit/losses ensuing from initial recognition (Brooks 2015).

Therefore, it can be said that the role of OCI is mainly to uphold the profit as well as loss. As

such, any profit/loss can only be recognized in the statement of OCI in case if that made other

comprehensive earnings more relevant. For the case under consideration, the reclassification

adjustment for PPE losses/gains is not presented from equity to P-L.

Solution vi)

As mentioned in the annual report of the firm Wesfarmers, the tax expenditure of the firm

stands at (AUD 1265 million) in 2017 while the same is recorded to be (AUD 631 million) in

2016 (Wesfarmers.com.au 2018). This stands for the current tax expends of the firm

Wesfarmers. In essence, the current tax assets or else liabilities of the firm Wesfarmers are

enumerated at the specific amount that is anticipated to be essentially recovered otherwise

CORPORATE ACCOUNTING

outflow of unrealised losses on particularly various losses on mainly hedges of cash flow

(Siew 2015).

Solution v)

As rightly indicated by Tschopp and Nastanski (2014), other comprehensive income also

simply referred to as OCI is said to contain varied items of particularly of firm’s income as

well as expenses incurred (counting adjustments of reclassification) which are not necessarily

identified in the assertion for profit and loss of reporting entities. Essentially, the alterations

in the amount of equity during a specified period ensuing from business dealings as well as

other incidents other than the alterations from business transactions oriented to owners in

their potential as owners. On the other hand, the profit and loss assertion needs to include

outcomes of the transactions, different consumptions along with impairment of assets and

satisfaction of liabilities during the period in which they take place. In addition to this, the P-

L statement would also identify all the alterations in the asset costs and liability costs in

addition to any sort of profit/losses ensuing from initial recognition (Brooks 2015).

Therefore, it can be said that the role of OCI is mainly to uphold the profit as well as loss. As

such, any profit/loss can only be recognized in the statement of OCI in case if that made other

comprehensive earnings more relevant. For the case under consideration, the reclassification

adjustment for PPE losses/gains is not presented from equity to P-L.

Solution vi)

As mentioned in the annual report of the firm Wesfarmers, the tax expenditure of the firm

stands at (AUD 1265 million) in 2017 while the same is recorded to be (AUD 631 million) in

2016 (Wesfarmers.com.au 2018). This stands for the current tax expends of the firm

Wesfarmers. In essence, the current tax assets or else liabilities of the firm Wesfarmers are

enumerated at the specific amount that is anticipated to be essentially recovered otherwise

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

CORPORATE ACCOUNTING

paid to definite taxation authorities at the particular tax rates as well as laws of tax enacted

else wise considerably enacted by the firm’s date of balance sheet statement (Brooks 2015).

Solution to vii)

The income tax of the firm Wesfarmers is essentially enumerated by utilizing ascertained rate

of tax that are mainly imposed by the pronouncement on financial position and regulation of

tax. Detailed examination of the yearly report of the firm replicates the fact that the current

expenditure of the corporation during the year 2017 was observed to be (AUD 1265 million)

in 2017 while the same is recorded to be (AUD 631 million) in 2016 (Wesfarmers.com.au

2018). Hence, it cannot be analysed whether the figure for income tax expenditure are similar

to the particular tax rate times the total firm’s earnings.

Solution viii)

Analysis of annual financial assertion of the firm reveals that the deferred tax asset of the

firm Wesfarmers as mentioned in the balance sheet stands at AUD 971 million while the

same was recorded to be AUD 1042 million in 2016 (Wesfarmers.com.au 2018). In this

regard, it can be said that deferred tax assets are necessarily recognized for diverse deductible

temporary variances, also carried forward unutilized tax assets as well as unutilized losses of

tax, to the point that it is quite probable that the firm’s taxable gain shall be available to use

them (Reid and Myddelton 2017). In essence, the carrying amount of particularly tax asset

(referring to deferred ones) are as such enumerated at the rate of tax that are expected to be

implemented to the entire year at the time when the specific asset is realised otherwise this

liability of the firm gets settled, founded on rates of tax as well as regulations of tax that are

imposed or else considerably imposed at the date mentioned in the balance sheet.

CORPORATE ACCOUNTING

paid to definite taxation authorities at the particular tax rates as well as laws of tax enacted

else wise considerably enacted by the firm’s date of balance sheet statement (Brooks 2015).

Solution to vii)

The income tax of the firm Wesfarmers is essentially enumerated by utilizing ascertained rate

of tax that are mainly imposed by the pronouncement on financial position and regulation of

tax. Detailed examination of the yearly report of the firm replicates the fact that the current

expenditure of the corporation during the year 2017 was observed to be (AUD 1265 million)

in 2017 while the same is recorded to be (AUD 631 million) in 2016 (Wesfarmers.com.au

2018). Hence, it cannot be analysed whether the figure for income tax expenditure are similar

to the particular tax rate times the total firm’s earnings.

Solution viii)

Analysis of annual financial assertion of the firm reveals that the deferred tax asset of the

firm Wesfarmers as mentioned in the balance sheet stands at AUD 971 million while the

same was recorded to be AUD 1042 million in 2016 (Wesfarmers.com.au 2018). In this

regard, it can be said that deferred tax assets are necessarily recognized for diverse deductible

temporary variances, also carried forward unutilized tax assets as well as unutilized losses of

tax, to the point that it is quite probable that the firm’s taxable gain shall be available to use

them (Reid and Myddelton 2017). In essence, the carrying amount of particularly tax asset

(referring to deferred ones) are as such enumerated at the rate of tax that are expected to be

implemented to the entire year at the time when the specific asset is realised otherwise this

liability of the firm gets settled, founded on rates of tax as well as regulations of tax that are

imposed or else considerably imposed at the date mentioned in the balance sheet.

9

CORPORATE ACCOUNTING

Solution ix)

Expenses for current tax disbursements during the financial year 2017 was recorded to be

(AUD 1265 million) in 2017 while the same is recorded to be (AUD 631 million) in 2016.

However, alternatively, income tax payable by the firm Wesfarmers Limited is recorded to be

AUD 292 million in 2017 and AUD 29 million in 2016 (Wesfarmers.com.au 2018). Thus, it

can be seen that the income tax payable is not the same as the income tax expense. This

reflects a reconciliation of expenditure of income tax to income tax amount that is payable. In

essence, this procedure of reconciliation takes in adjustments for primarily temporary

variances. In essence, the adjustments include different provisions, enumeration of different

financial assets, several other items together with prior year’s variances (Miao et al. 2016). In

particular, temporary variances are mainly for inventories, plant, property as well as

equipment, sales revenue acquired by the firm in advance with payables.

Solution x)

Analysis of annual report of the company Wesfarmers Ltd replicates that income tax

expenditure mentioned in the income account is not analogous to that of disbursement of

income tax represented in the pronouncement on cash flow. Fundamentally, payments for

income tax inevitably comprises of influence of income tax of specific losses or else gains

associated to financing deeds so that cash flow calculated after tax is represented in the sub

heads of overall cash flow (Warren and Jones 2018). All over again, in opposition, payments

of the reporting entity on taxation are unavoidably the specific amount that reflects tax costs.

Solution xi)

Comprehensive evaluation of yearly report helps in identification of the fact for Wesfarmers

there is in essence a charge for present taxation on earnings of the reporting entity.

Fundamentally, this is for the most part founded on adjusted profit figure of the corporation

CORPORATE ACCOUNTING

Solution ix)

Expenses for current tax disbursements during the financial year 2017 was recorded to be

(AUD 1265 million) in 2017 while the same is recorded to be (AUD 631 million) in 2016.

However, alternatively, income tax payable by the firm Wesfarmers Limited is recorded to be

AUD 292 million in 2017 and AUD 29 million in 2016 (Wesfarmers.com.au 2018). Thus, it

can be seen that the income tax payable is not the same as the income tax expense. This

reflects a reconciliation of expenditure of income tax to income tax amount that is payable. In

essence, this procedure of reconciliation takes in adjustments for primarily temporary

variances. In essence, the adjustments include different provisions, enumeration of different

financial assets, several other items together with prior year’s variances (Miao et al. 2016). In

particular, temporary variances are mainly for inventories, plant, property as well as

equipment, sales revenue acquired by the firm in advance with payables.

Solution x)

Analysis of annual report of the company Wesfarmers Ltd replicates that income tax

expenditure mentioned in the income account is not analogous to that of disbursement of

income tax represented in the pronouncement on cash flow. Fundamentally, payments for

income tax inevitably comprises of influence of income tax of specific losses or else gains

associated to financing deeds so that cash flow calculated after tax is represented in the sub

heads of overall cash flow (Warren and Jones 2018). All over again, in opposition, payments

of the reporting entity on taxation are unavoidably the specific amount that reflects tax costs.

Solution xi)

Comprehensive evaluation of yearly report helps in identification of the fact for Wesfarmers

there is in essence a charge for present taxation on earnings of the reporting entity.

Fundamentally, this is for the most part founded on adjusted profit figure of the corporation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

CORPORATE ACCOUNTING

that can be attributed to any sort of rejection or non-assessable piece (Warren and Jones

2018). Over and above this, there also subsists notes for particularly financial assertions that

are prepared as well as arranged by the business concern Wesfarmers. In essence, this aids in

gaining thorough understanding regarding reconciliation of income tax expenditure of the

firm to the amount of payable tax of the firm. Basically, this kind of illustrations on

reconciliation delivered in the notes section of the report provides particular information to

diverse users concerning calculation of income tax of the firm. As a result, the most

significant part in this regard is necessarily realisation of expenditure of the firm as income

tax that is based on reconciliation of certain temporary variation and kind of net loss that the

company bears.

CORPORATE ACCOUNTING

that can be attributed to any sort of rejection or non-assessable piece (Warren and Jones

2018). Over and above this, there also subsists notes for particularly financial assertions that

are prepared as well as arranged by the business concern Wesfarmers. In essence, this aids in

gaining thorough understanding regarding reconciliation of income tax expenditure of the

firm to the amount of payable tax of the firm. Basically, this kind of illustrations on

reconciliation delivered in the notes section of the report provides particular information to

diverse users concerning calculation of income tax of the firm. As a result, the most

significant part in this regard is necessarily realisation of expenditure of the firm as income

tax that is based on reconciliation of certain temporary variation and kind of net loss that the

company bears.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

CORPORATE ACCOUNTING

References

Brooks, R., 2015. Financial management: core concepts. Pearson.

Miao, B., Teoh, S.H. and Zhu, Z., 2016. Limited attention, statement of cash flow disclosure,

and the valuation of accruals. Review of Accounting Studies, 21(2), pp.473-515.

Reid, W. and Myddelton, D.R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Schaltegger, S., and Burritt, R. 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Siew, R.Y., 2015. A review of corporate sustainability reporting tools (SRTs). Journal of

environmental management, 164, pp.180-195.

Tschopp, D. and Nastanski, M., 2014. The harmonization and convergence of corporate

social responsibility reporting standards. Journal of Business Ethics, 125(1), pp.147-162.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Wesfarmers.com.au. 2018. Home - Wesfarmers. [online] Available at:

http://www.wesfarmers.com.au [Accessed 22 Apr. 2018].

CORPORATE ACCOUNTING

References

Brooks, R., 2015. Financial management: core concepts. Pearson.

Miao, B., Teoh, S.H. and Zhu, Z., 2016. Limited attention, statement of cash flow disclosure,

and the valuation of accruals. Review of Accounting Studies, 21(2), pp.473-515.

Reid, W. and Myddelton, D.R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Schaltegger, S., and Burritt, R. 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Siew, R.Y., 2015. A review of corporate sustainability reporting tools (SRTs). Journal of

environmental management, 164, pp.180-195.

Tschopp, D. and Nastanski, M., 2014. The harmonization and convergence of corporate

social responsibility reporting standards. Journal of Business Ethics, 125(1), pp.147-162.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Wesfarmers.com.au. 2018. Home - Wesfarmers. [online] Available at:

http://www.wesfarmers.com.au [Accessed 22 Apr. 2018].

12

CORPORATE ACCOUNTING

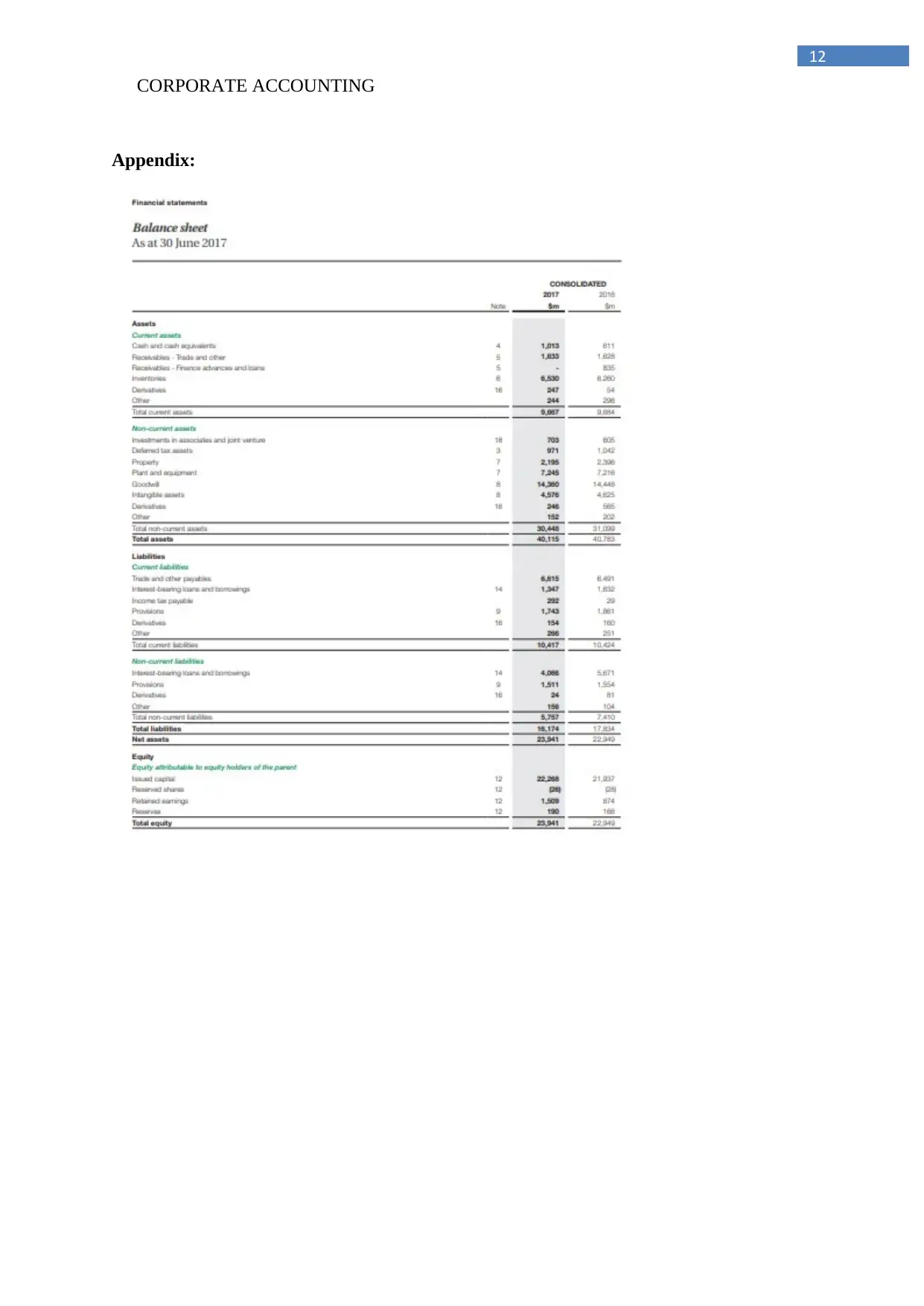

Appendix:

CORPORATE ACCOUNTING

Appendix:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.