Corporate Accounting Report: Wesfarmers Financial Statement Analysis

VerifiedAdded on 2021/06/15

|12

|2895

|14

Report

AI Summary

This report provides a comprehensive analysis of Wesfarmers' corporate accounting practices. It begins with an examination of the cash flow statement, detailing cash flows from operating, investing, and financing activities, and compares the cash flow trends over a three-year period. The analysis then delves into the other comprehensive income statement, outlining key components such as retained earnings, foreign currency translation reserve, and cash flow hedge reserve, and explains their significance. Furthermore, the report investigates the accounting for corporate income tax, comparing the standard tax rate with the actual tax expenses incurred by Wesfarmers, and discusses the implications of deferred tax assets and liabilities. It also explores the relationship between income tax payable and income tax paid, highlighting the reasons for any discrepancies. The report concludes that there are no confusing or surprising elements in Wesfarmers' tax treatment due to the relevant disclosures in the financial statements.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Corporate Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Table of Contents

Cash flow statement:..................................................................................................................2

Part (i):...................................................................................................................................2

Part (ii):..................................................................................................................................3

Other comprehensive income statement:...................................................................................5

Part (iii):.................................................................................................................................5

Part (iv):.................................................................................................................................5

Part (v):...................................................................................................................................6

Accounting for corporate income tax:........................................................................................7

Part (vi):.................................................................................................................................7

Part (vii):................................................................................................................................7

Part (viii):...............................................................................................................................7

Part (ix):.................................................................................................................................8

Part (x):...................................................................................................................................8

Part (xi):.................................................................................................................................9

References:...............................................................................................................................10

Table of Contents

Cash flow statement:..................................................................................................................2

Part (i):...................................................................................................................................2

Part (ii):..................................................................................................................................3

Other comprehensive income statement:...................................................................................5

Part (iii):.................................................................................................................................5

Part (iv):.................................................................................................................................5

Part (v):...................................................................................................................................6

Accounting for corporate income tax:........................................................................................7

Part (vi):.................................................................................................................................7

Part (vii):................................................................................................................................7

Part (viii):...............................................................................................................................7

Part (ix):.................................................................................................................................8

Part (x):...................................................................................................................................8

Part (xi):.................................................................................................................................9

References:...............................................................................................................................10

2CORPORATE ACCOUNTING

Cash flow statement:

Part (i):

One of the primary financial statements of an organisation is the cash flow statement,

which signifies the primary accounts in the income and balance sheet accounts influencing

the cash and cash equivalents.

Cash flows from operations:

In Wesfarmers, the main items listed under this section comprise of customer receipts,

supplier payments, borrowing cost, interest received and others. The customer receipts denote

the sale proceeds obtained from credit sales (Akbar and Ahsan 2014). These receipts have

increased from $71,157 million in 2016 to $74,042 million in 2017. The supplier payments

signify the amount needed to incur for credit purchase and it has risen to $68,713 million in

2017 from $66,671 million in 2016 (Wesfarmers.com.au 2018). Interest received signifies the

amount obtained on the part of Wesfarmers from different business investments and others.

Due to the write-off of bad debt, decline in interest received could be observed to $83 million

in 2017 from $131 million in 2016. Borrowing costs denote the charge needed to incur in

case of debt covenant, interest payments and finance fees. The fall in this expense could be

observed to $234 million in 2017 from $288 million in 2016.

Cash flows from investing activities:

The most essential items under this section comprise of proceeds from and payment

of property, plant and equipment and intangibles, investment in joint ventures and associates,

subsidiary acquisition and loan note redemption along with proceeds from sale of associates

and businesses. The payments related to property, plant and equipment along with intangible

assets denote the amount needed to pay for acquiring and purchasing such items. Moreover,

Cash flow statement:

Part (i):

One of the primary financial statements of an organisation is the cash flow statement,

which signifies the primary accounts in the income and balance sheet accounts influencing

the cash and cash equivalents.

Cash flows from operations:

In Wesfarmers, the main items listed under this section comprise of customer receipts,

supplier payments, borrowing cost, interest received and others. The customer receipts denote

the sale proceeds obtained from credit sales (Akbar and Ahsan 2014). These receipts have

increased from $71,157 million in 2016 to $74,042 million in 2017. The supplier payments

signify the amount needed to incur for credit purchase and it has risen to $68,713 million in

2017 from $66,671 million in 2016 (Wesfarmers.com.au 2018). Interest received signifies the

amount obtained on the part of Wesfarmers from different business investments and others.

Due to the write-off of bad debt, decline in interest received could be observed to $83 million

in 2017 from $131 million in 2016. Borrowing costs denote the charge needed to incur in

case of debt covenant, interest payments and finance fees. The fall in this expense could be

observed to $234 million in 2017 from $288 million in 2016.

Cash flows from investing activities:

The most essential items under this section comprise of proceeds from and payment

of property, plant and equipment and intangibles, investment in joint ventures and associates,

subsidiary acquisition and loan note redemption along with proceeds from sale of associates

and businesses. The payments related to property, plant and equipment along with intangible

assets denote the amount needed to pay for acquiring and purchasing such items. Moreover,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

the proceeds from such items signify the monetary benefits to be obtained by utilising these

items (Arnold, Harris and Liu 2016). In accordance with the cash flow statement of

Wesfarmers, these items are minimised to $1,681 in 2017 from $1,899 in 2016. On the other

hand, rise could be observed in case of proceeds to $653 million in 2017 from $563 million in

2017, as some of these assets were sold. These sold and purchased non-current assets are

recognised as proceeds and investments respectively. Major proceeds have been realised in

2017 due to sale of businesses. However, constancy could be observed in case of investments

in both the years. Moreover, a particular financial instrument is loan note, which is an

obligation of loan repayment with interests (Ehrhardt and Brigham 2016). A loan amount of

$54 million has been redeemed in 2017.

Cash flows from financing activities:

The significant items under this section constitute of borrowing proceeds, borrowing

payment and equity dividend payment (Ferran and Ho 2014). Borrowing signifies the overall

disbursed amount, which the lenders could provide to the borrowers in case of a particular

loan covenant. As the loan terms to the debtors are extended, significant decline could be

observed in borrowing proceeds from $2,360 million in 2016 to $220 million in 2017. Along

with this, Wesfarmers is required to pay large amount for settling its bank loans. Equity

dividend denotes the annual cash flow provided to the shareholders of the organisation. Due

to the rise in retained earnings, Wesfarmers has incurred lower dividend payment in 2017

compared to the previous year.

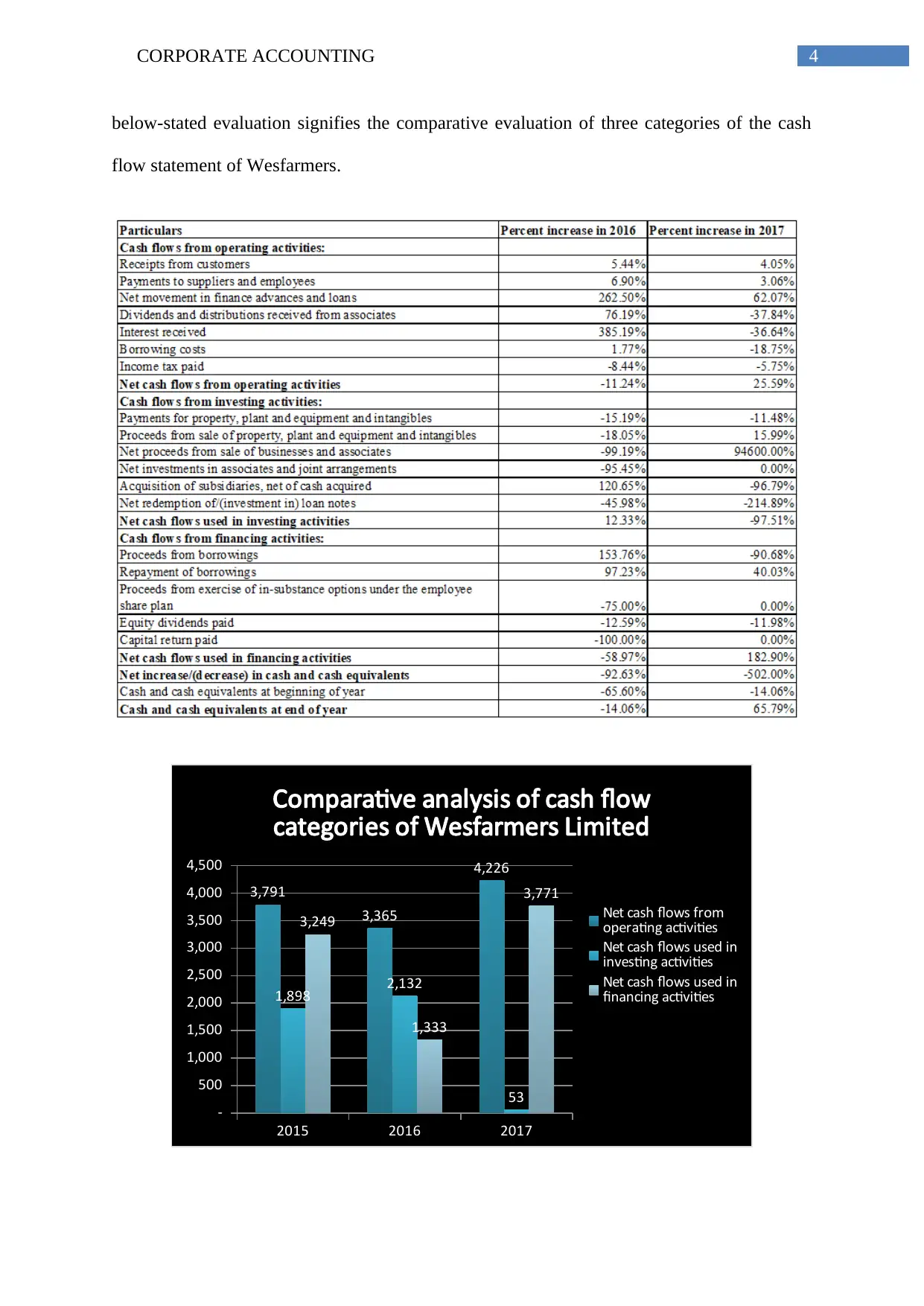

Part (ii):

The above evaluation highlights on the significant aspects of the cash flow statement

of Wesfarmers from operating activities, investing activities and financing activities. The

the proceeds from such items signify the monetary benefits to be obtained by utilising these

items (Arnold, Harris and Liu 2016). In accordance with the cash flow statement of

Wesfarmers, these items are minimised to $1,681 in 2017 from $1,899 in 2016. On the other

hand, rise could be observed in case of proceeds to $653 million in 2017 from $563 million in

2017, as some of these assets were sold. These sold and purchased non-current assets are

recognised as proceeds and investments respectively. Major proceeds have been realised in

2017 due to sale of businesses. However, constancy could be observed in case of investments

in both the years. Moreover, a particular financial instrument is loan note, which is an

obligation of loan repayment with interests (Ehrhardt and Brigham 2016). A loan amount of

$54 million has been redeemed in 2017.

Cash flows from financing activities:

The significant items under this section constitute of borrowing proceeds, borrowing

payment and equity dividend payment (Ferran and Ho 2014). Borrowing signifies the overall

disbursed amount, which the lenders could provide to the borrowers in case of a particular

loan covenant. As the loan terms to the debtors are extended, significant decline could be

observed in borrowing proceeds from $2,360 million in 2016 to $220 million in 2017. Along

with this, Wesfarmers is required to pay large amount for settling its bank loans. Equity

dividend denotes the annual cash flow provided to the shareholders of the organisation. Due

to the rise in retained earnings, Wesfarmers has incurred lower dividend payment in 2017

compared to the previous year.

Part (ii):

The above evaluation highlights on the significant aspects of the cash flow statement

of Wesfarmers from operating activities, investing activities and financing activities. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

below-stated evaluation signifies the comparative evaluation of three categories of the cash

flow statement of Wesfarmers.

2015 2016 2017

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

3,791

3,365

4,226

1,898 2,132

53

3,249

1,333

3,771

Comparative analysis of cash flow

categories of Wesfarmers Limited

Net cash flows from

operating activities

Net cash flows used in

investing activities

Net cash flows used in

financing activities

below-stated evaluation signifies the comparative evaluation of three categories of the cash

flow statement of Wesfarmers.

2015 2016 2017

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

3,791

3,365

4,226

1,898 2,132

53

3,249

1,333

3,771

Comparative analysis of cash flow

categories of Wesfarmers Limited

Net cash flows from

operating activities

Net cash flows used in

investing activities

Net cash flows used in

financing activities

5CORPORATE ACCOUNTING

In accordance with the above table and figure, there is decline in operating cash flows

to $3,365 million in 2016 from $3,791 million in 2015; however, the amount has increased

considerably to $4,226 million in 2017. This is because the cash recovered from the

customers has increased by 5.44% in 2016 and 4.05% in 2017 and income tax payment has

been reduced by 8.44% in 2016 and 5.75% in 2017. In addition, rise could be observed in

investing cash flows as well from 1,898 million in 2015 to $2,132 million in 2016; however,

the fall is massive in 2017 to ($53 million). This is because of the fall in investment on fixed

assets by -15.19% in 2016 and by -11.48% in 2017. Finally, there is considerable decline in

financing cash flows in 2017 due to the loan clearance. By combining all these reasons,

increase in cash and cash equivalents for Wesfarmers could be observed over the three-year

period.

Other comprehensive income statement:

Part (iii):

In accordance with the 2017 annual report of Wesfarmers, the major items listed

under this section include the following:

Retained earnings

Foreign currency translation reserve

Cash flow hedge reserve

Part (iv):

The corporate entities utilise foreign currency translation reserve for transfer of the

outcomes of the cross-border subsidiaries of the parent entities to the reporting currency. This

is taken into account in the form of a significant portion of the consolidation procedure of the

financial reports. Thus, it enables in determining the functional currency of the foreign entity

In accordance with the above table and figure, there is decline in operating cash flows

to $3,365 million in 2016 from $3,791 million in 2015; however, the amount has increased

considerably to $4,226 million in 2017. This is because the cash recovered from the

customers has increased by 5.44% in 2016 and 4.05% in 2017 and income tax payment has

been reduced by 8.44% in 2016 and 5.75% in 2017. In addition, rise could be observed in

investing cash flows as well from 1,898 million in 2015 to $2,132 million in 2016; however,

the fall is massive in 2017 to ($53 million). This is because of the fall in investment on fixed

assets by -15.19% in 2016 and by -11.48% in 2017. Finally, there is considerable decline in

financing cash flows in 2017 due to the loan clearance. By combining all these reasons,

increase in cash and cash equivalents for Wesfarmers could be observed over the three-year

period.

Other comprehensive income statement:

Part (iii):

In accordance with the 2017 annual report of Wesfarmers, the major items listed

under this section include the following:

Retained earnings

Foreign currency translation reserve

Cash flow hedge reserve

Part (iv):

The corporate entities utilise foreign currency translation reserve for transfer of the

outcomes of the cross-border subsidiaries of the parent entities to the reporting currency. This

is taken into account in the form of a significant portion of the consolidation procedure of the

financial reports. Thus, it enables in determining the functional currency of the foreign entity

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

(Fracassi 2016). Moreover, such aspect helps in regauging the foreign firm to the reporting

currency of the parent firm. The final stage comprise of the translation of currency of the

profit and loss recorded.

The organisations utilise cash flow hedge reserve when reversing or minimisation of

exposures are planned, which occur due to the cash flow change in particular assets or

liabilities because of the variation in interest risk rate on debt instrument depending on the

floating interest rate (Gitman, Juchau and Flanagan 2015).

Finally, the amount from net income that an organisation does not distribute to its

shareholders as dividend is termed as retained earnings. This is because the organisation

plans in retaining this part to pay debt or investment in new assets in its core business

operations (Hillier et al. 2014).

Part (v):

The net profit diversification is taken into account as other comprehensive income

statement. In the past, the business organisations use to take into account the profit changes

as external factors in their core business activities and highly volatile equity shares are

provided to the shareholders (Hussey and Ong 2017). In case of Wesfarmers, the other

comprehensive income statement is treated as a tool for providing important information

regarding the stated factors. Thus, comprehensive income is a blend of standard new income

as well as other comprehensive income. The primary reason that these activities are reported

is that the users are provided with holistic and comprehensive view of the significant business

drivers, since reporting could not be made in the income statement.

(Fracassi 2016). Moreover, such aspect helps in regauging the foreign firm to the reporting

currency of the parent firm. The final stage comprise of the translation of currency of the

profit and loss recorded.

The organisations utilise cash flow hedge reserve when reversing or minimisation of

exposures are planned, which occur due to the cash flow change in particular assets or

liabilities because of the variation in interest risk rate on debt instrument depending on the

floating interest rate (Gitman, Juchau and Flanagan 2015).

Finally, the amount from net income that an organisation does not distribute to its

shareholders as dividend is termed as retained earnings. This is because the organisation

plans in retaining this part to pay debt or investment in new assets in its core business

operations (Hillier et al. 2014).

Part (v):

The net profit diversification is taken into account as other comprehensive income

statement. In the past, the business organisations use to take into account the profit changes

as external factors in their core business activities and highly volatile equity shares are

provided to the shareholders (Hussey and Ong 2017). In case of Wesfarmers, the other

comprehensive income statement is treated as a tool for providing important information

regarding the stated factors. Thus, comprehensive income is a blend of standard new income

as well as other comprehensive income. The primary reason that these activities are reported

is that the users are provided with holistic and comprehensive view of the significant business

drivers, since reporting could not be made in the income statement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

Accounting for corporate income tax:

Part (vi):

In accordance with the Australian taxation law, Wesfarmers is needed to pay a certain

portion of its earnings as tax. The annual report states that the organisation has reported

$1,265 million and $631 million as tax expenses for the years 2017 and 2016 respectively.

However, if Wesfarmers follows the standard corporate tax rate of 30% in Australia, it would

have to incur $1,241.40 million ($4,138 million x 30%) for the year 2017 and $311.40

million ($1,038 million x 30%) for the year 2016 as tax expenses (Ijiri 2018).

Part (vii):

The latest annual report of Wesfarmers states that the organisation has recorded

$4,138 million as earnings before income tax in 2017, which were $1,038 million in 2016 and

the standard tax rate in Australia is 30%. When this rate is applied on the disclosed earnings,

the tax expense for the organisation would be $1,241.40 million in 2017 and $311.40 million

in 2016. Hence, no similarity could be found in the disclosed and standard tax expense for

Wesfarmers. This is because the organisation has considered some additional items while

calculating its actual tax expense. One of them is non-deductible expenses and another is the

location of its subsidiaries in New Zealand, in which the applicable tax rate is 28%. In

addition, it has considered deferred tax as another significant item for such variation, since it

could obtain tax benefits. Finally, the non-assessable income could be accounted for this

variation as well (Lerner and Seru 2017).

Part (viii):

The scenario in which either greater tax payments or advance tax payments are made,

it leads to creation of deferred tax assets. On the contrary, deferred tax liabilities denote such

situation, which is obtained by deducting the carrying amount of tax from the disclosed profit

Accounting for corporate income tax:

Part (vi):

In accordance with the Australian taxation law, Wesfarmers is needed to pay a certain

portion of its earnings as tax. The annual report states that the organisation has reported

$1,265 million and $631 million as tax expenses for the years 2017 and 2016 respectively.

However, if Wesfarmers follows the standard corporate tax rate of 30% in Australia, it would

have to incur $1,241.40 million ($4,138 million x 30%) for the year 2017 and $311.40

million ($1,038 million x 30%) for the year 2016 as tax expenses (Ijiri 2018).

Part (vii):

The latest annual report of Wesfarmers states that the organisation has recorded

$4,138 million as earnings before income tax in 2017, which were $1,038 million in 2016 and

the standard tax rate in Australia is 30%. When this rate is applied on the disclosed earnings,

the tax expense for the organisation would be $1,241.40 million in 2017 and $311.40 million

in 2016. Hence, no similarity could be found in the disclosed and standard tax expense for

Wesfarmers. This is because the organisation has considered some additional items while

calculating its actual tax expense. One of them is non-deductible expenses and another is the

location of its subsidiaries in New Zealand, in which the applicable tax rate is 28%. In

addition, it has considered deferred tax as another significant item for such variation, since it

could obtain tax benefits. Finally, the non-assessable income could be accounted for this

variation as well (Lerner and Seru 2017).

Part (viii):

The scenario in which either greater tax payments or advance tax payments are made,

it leads to creation of deferred tax assets. On the contrary, deferred tax liabilities denote such

situation, which is obtained by deducting the carrying amount of tax from the disclosed profit

8CORPORATE ACCOUNTING

of the organisation (Nobes and Stadler 2015). It has been identified from the latest annual

report of Wesfarmers, that the disclosed amounts of deferred tax assets and deferred tax

liabilities have been $971 million and $722 million in 2017 respectively, which were $1,042

million and $611 million respectively. There are certain reasons that Wesfarmers has

recorded deferred tax assets and deferred tax liabilities in its annual report. Deferred tax

assets are reported to represent the difference between the amount of depreciation and taxable

rate pertaining to depreciation. On the other hand, deferred tax liabilities are reported to

represent the profit variation and lower tax payments in 2017.

Part (ix):

For any business entity, income tax payable is a significant aspect in order to ensure

its operations in the nation (Schaltegger, Etxeberria and Ortas 2017). However, it has been

observed for every business organisation that the amounts of income tax payable and income

tax paid are not identical. Wesfarmers is not an exception to this case as well. As per the 2017

annual report of Wesfarmers, difference could be observed as well, for which deferred tax

assets are considered as the significant reason. The logic supporting this reason is the

payment of additional tax amount beyond the actual tax rate of 30%. Hence, this excess

amount of payment of tax has lead to difference between the two above-stated items. Besides

this, certain prevailing regulations are inherent for tax accounting and financial accounting, in

which depreciation is taken as an instance. As the depreciation rate differs from asset to asset,

there are differences in accordance with financial accounting and tax accounting and as a

result, depreciation expenses for some assets are higher than the other assets (Scholes 2015).

Part (x):

According to the annual report of Wesfarmers in 2017, the disclosed income tax

expense has been $1,261 million, which was $951 million in 2016. On the other hand, it

could be found that the income tax paid reported in the cash flow statement do not resemble

of the organisation (Nobes and Stadler 2015). It has been identified from the latest annual

report of Wesfarmers, that the disclosed amounts of deferred tax assets and deferred tax

liabilities have been $971 million and $722 million in 2017 respectively, which were $1,042

million and $611 million respectively. There are certain reasons that Wesfarmers has

recorded deferred tax assets and deferred tax liabilities in its annual report. Deferred tax

assets are reported to represent the difference between the amount of depreciation and taxable

rate pertaining to depreciation. On the other hand, deferred tax liabilities are reported to

represent the profit variation and lower tax payments in 2017.

Part (ix):

For any business entity, income tax payable is a significant aspect in order to ensure

its operations in the nation (Schaltegger, Etxeberria and Ortas 2017). However, it has been

observed for every business organisation that the amounts of income tax payable and income

tax paid are not identical. Wesfarmers is not an exception to this case as well. As per the 2017

annual report of Wesfarmers, difference could be observed as well, for which deferred tax

assets are considered as the significant reason. The logic supporting this reason is the

payment of additional tax amount beyond the actual tax rate of 30%. Hence, this excess

amount of payment of tax has lead to difference between the two above-stated items. Besides

this, certain prevailing regulations are inherent for tax accounting and financial accounting, in

which depreciation is taken as an instance. As the depreciation rate differs from asset to asset,

there are differences in accordance with financial accounting and tax accounting and as a

result, depreciation expenses for some assets are higher than the other assets (Scholes 2015).

Part (x):

According to the annual report of Wesfarmers in 2017, the disclosed income tax

expense has been $1,261 million, which was $951 million in 2016. On the other hand, it

could be found that the income tax paid reported in the cash flow statement do not resemble

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

with the one disclosed in the income statement. The income tax paid for the organisation has

been $951 million in 2017 in contrast to $1,009 million in 2016. The tax expenses are mainly

computed after consideration is made in relation to tax rate and other aspects (Titman, Keown

and Martin 2017). However, it is to be noted that the income tax paid is reported under the

operating cash flow section in the cash flow statement of the organisation. This denotes the

payment of greater income tax on the part of Wesfarmers and thus, they are considered in the

form of operating cash outflows. In the statement of cash flows, any minimisation in tax

expense signifies that the amount saved is used as cash (Vernimmen et al. 2014). Thus, it

could be stated that Wesfarmers has not taken into account certain items for calculating its

tax expense in its cash flow statement.

Part (xi):

Based on the above assessment, it is evident that no confusing, difficult or surprising

elements could be found in the tax treatment of Wesfarmers Limited due to relevant

disclosures attached in the form of notes to the financial statements. It further signifies that

the organisation has adhered to the taxation law of Australia in order to perform its tax

treatment. By providing the notes to the financial statements, support has been provided

behind the calculation of taxation expense through significant explanations and justifications.

After careful evaluation of the tax treatment of the organisation, it is possible to develop an

in-depth knowledge about the roles of deferred tax, current tax assets or income tax payable

and other important items. All these aspects have adequately supported the taxation treatment

of Wesfarmers and the knowledge gathered could be used to evaluate the financial statements

of the other business organisations as well.

with the one disclosed in the income statement. The income tax paid for the organisation has

been $951 million in 2017 in contrast to $1,009 million in 2016. The tax expenses are mainly

computed after consideration is made in relation to tax rate and other aspects (Titman, Keown

and Martin 2017). However, it is to be noted that the income tax paid is reported under the

operating cash flow section in the cash flow statement of the organisation. This denotes the

payment of greater income tax on the part of Wesfarmers and thus, they are considered in the

form of operating cash outflows. In the statement of cash flows, any minimisation in tax

expense signifies that the amount saved is used as cash (Vernimmen et al. 2014). Thus, it

could be stated that Wesfarmers has not taken into account certain items for calculating its

tax expense in its cash flow statement.

Part (xi):

Based on the above assessment, it is evident that no confusing, difficult or surprising

elements could be found in the tax treatment of Wesfarmers Limited due to relevant

disclosures attached in the form of notes to the financial statements. It further signifies that

the organisation has adhered to the taxation law of Australia in order to perform its tax

treatment. By providing the notes to the financial statements, support has been provided

behind the calculation of taxation expense through significant explanations and justifications.

After careful evaluation of the tax treatment of the organisation, it is possible to develop an

in-depth knowledge about the roles of deferred tax, current tax assets or income tax payable

and other important items. All these aspects have adequately supported the taxation treatment

of Wesfarmers and the knowledge gathered could be used to evaluate the financial statements

of the other business organisations as well.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

References:

Akbar, S. and Ahsan, K., 2014. Analysis of corporate social disclosure practices of Australian

retail firms. International Journal of Managerial and Financial Accounting, 6(4), pp.375-

396.

Arnold, L.W., Harris, P. and Liu, M., 2016, January. CORPORATE ACCOUNTING

MALFEASANCE: AN OVERVIEW. In Global Conference on Business & Finance

Proceedings (Vol. 11, No. 1, p. 202). Institute for Business & Finance Research.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

learning.

Ferran, E. and Ho, L.C., 2014. Principles of corporate finance law. Oxford University Press.

Fracassi, C., 2016. Corporate finance policies and social networks. Management

Science, 63(8), pp.2420-2438.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Hillier, D., Clacher, I., Ross, S., Westerfield, R. and Jordan, B., 2014. Fundamentals of

corporate finance. McGraw Hill.

Hussey, R. and Ong, A., 2017. Corporate Financial Reporting. Macmillan International

Higher Education.

Ijiri, Y., 2018. An Introduction to Corporate Accounting Standards: A Review. Accounting,

Economics, and Law: A Convivium, 8(1).

References:

Akbar, S. and Ahsan, K., 2014. Analysis of corporate social disclosure practices of Australian

retail firms. International Journal of Managerial and Financial Accounting, 6(4), pp.375-

396.

Arnold, L.W., Harris, P. and Liu, M., 2016, January. CORPORATE ACCOUNTING

MALFEASANCE: AN OVERVIEW. In Global Conference on Business & Finance

Proceedings (Vol. 11, No. 1, p. 202). Institute for Business & Finance Research.

Ehrhardt, M.C. and Brigham, E.F., 2016. Corporate finance: A focused approach. Cengage

learning.

Ferran, E. and Ho, L.C., 2014. Principles of corporate finance law. Oxford University Press.

Fracassi, C., 2016. Corporate finance policies and social networks. Management

Science, 63(8), pp.2420-2438.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Hillier, D., Clacher, I., Ross, S., Westerfield, R. and Jordan, B., 2014. Fundamentals of

corporate finance. McGraw Hill.

Hussey, R. and Ong, A., 2017. Corporate Financial Reporting. Macmillan International

Higher Education.

Ijiri, Y., 2018. An Introduction to Corporate Accounting Standards: A Review. Accounting,

Economics, and Law: A Convivium, 8(1).

11CORPORATE ACCOUNTING

Lerner, J. and Seru, A., 2017. The use and misuse of patent data: Issues for corporate finance

and beyond (No. w24053). National Bureau of Economic Research.

Nobes, C.W. and Stadler, C., 2015. The qualitative characteristics of financial information,

and managers’ accounting decisions: evidence from IFRS policy changes. Accounting and

Business Research, 45(5), pp.572-601.

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating corporate accounting and

reporting for sustainability–attributes and challenges. Sustainable Development, 25(2),

pp.113-122.

Scholes, M.S., 2015. Taxes and business strategy. Prentice Hall.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate finance:

theory and practice. John Wiley & Sons.

Wesfarmers.com.au., 2018. 2017 Annual Report. [online] Available at:

http://www.wesfarmers.com.au/docs/default-source/reports/j000901-

ar17_interactive_final.pdf?sfvrsn=4 [Accessed 18 May 2018].

Lerner, J. and Seru, A., 2017. The use and misuse of patent data: Issues for corporate finance

and beyond (No. w24053). National Bureau of Economic Research.

Nobes, C.W. and Stadler, C., 2015. The qualitative characteristics of financial information,

and managers’ accounting decisions: evidence from IFRS policy changes. Accounting and

Business Research, 45(5), pp.572-601.

Schaltegger, S., Etxeberria, I.Á. and Ortas, E., 2017. Innovating corporate accounting and

reporting for sustainability–attributes and challenges. Sustainable Development, 25(2),

pp.113-122.

Scholes, M.S., 2015. Taxes and business strategy. Prentice Hall.

Titman, S., Keown, A.J. and Martin, J.D., 2017. Financial management: Principles and

applications. Pearson.

Vernimmen, P., Quiry, P., Dallocchio, M., Le Fur, Y. and Salvi, A., 2014. Corporate finance:

theory and practice. John Wiley & Sons.

Wesfarmers.com.au., 2018. 2017 Annual Report. [online] Available at:

http://www.wesfarmers.com.au/docs/default-source/reports/j000901-

ar17_interactive_final.pdf?sfvrsn=4 [Accessed 18 May 2018].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.