HI5020 Corporate Accounting: Comparative Analysis of AGL & Beach

VerifiedAdded on 2023/06/04

|12

|788

|243

Report

AI Summary

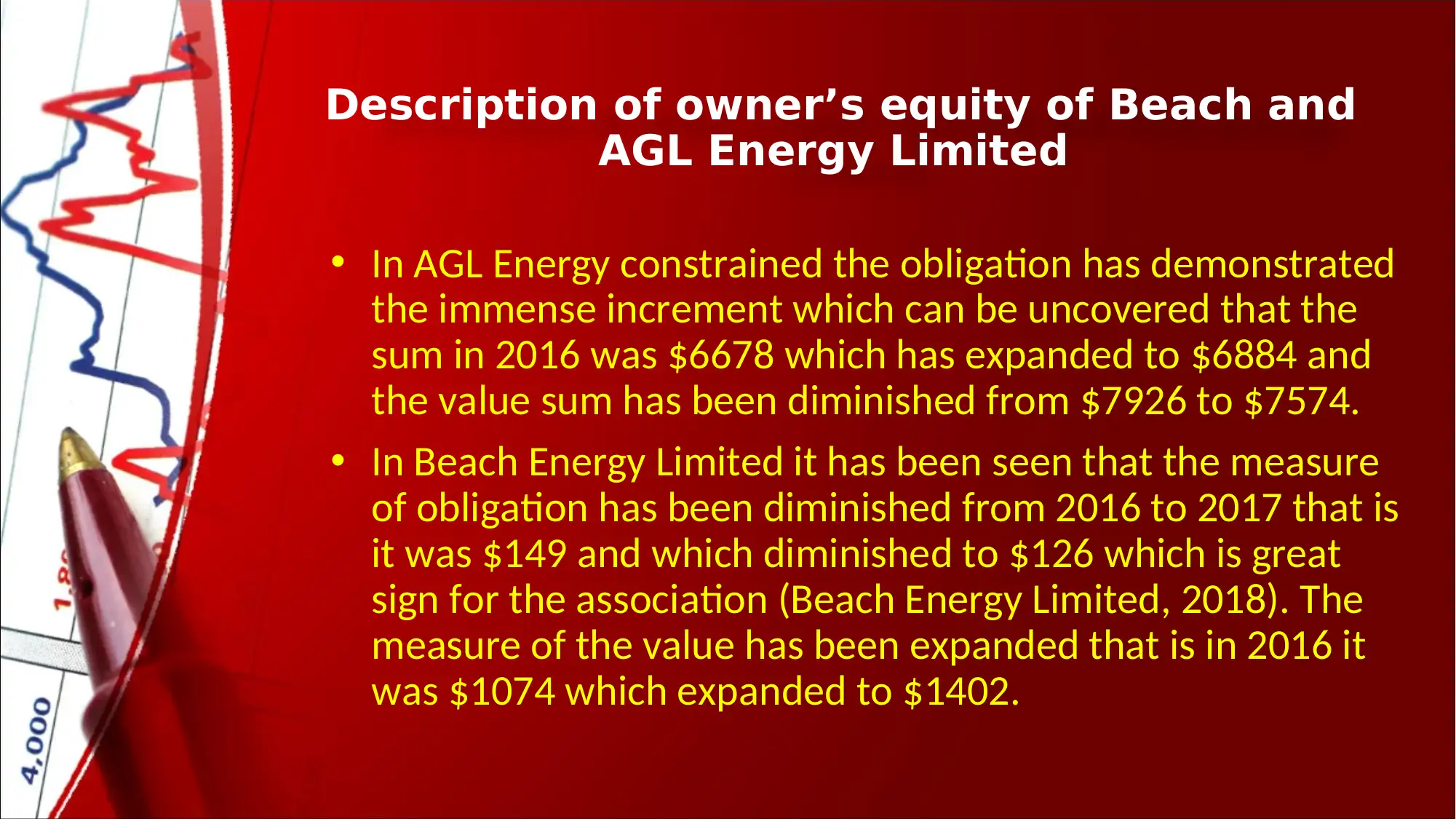

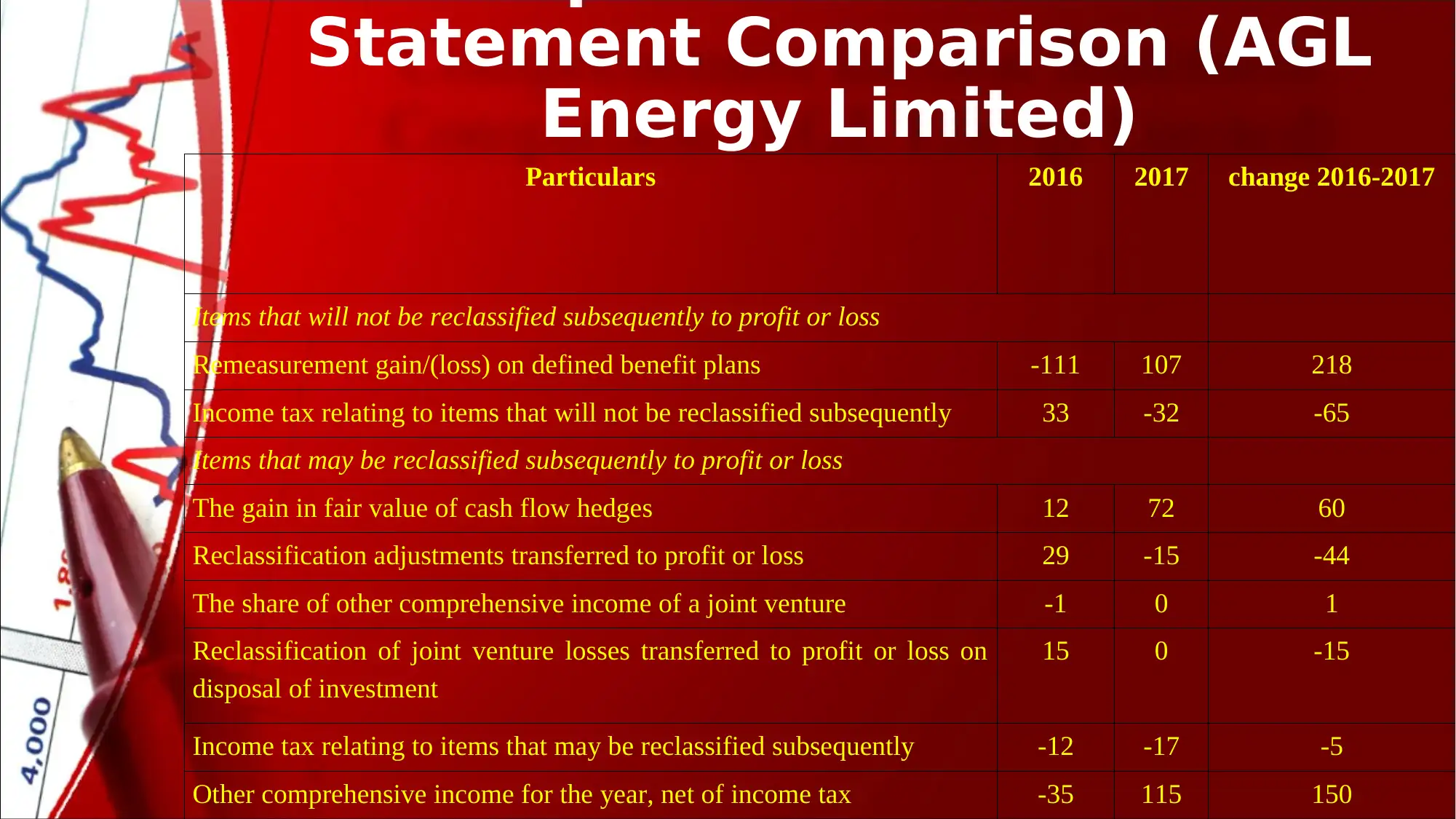

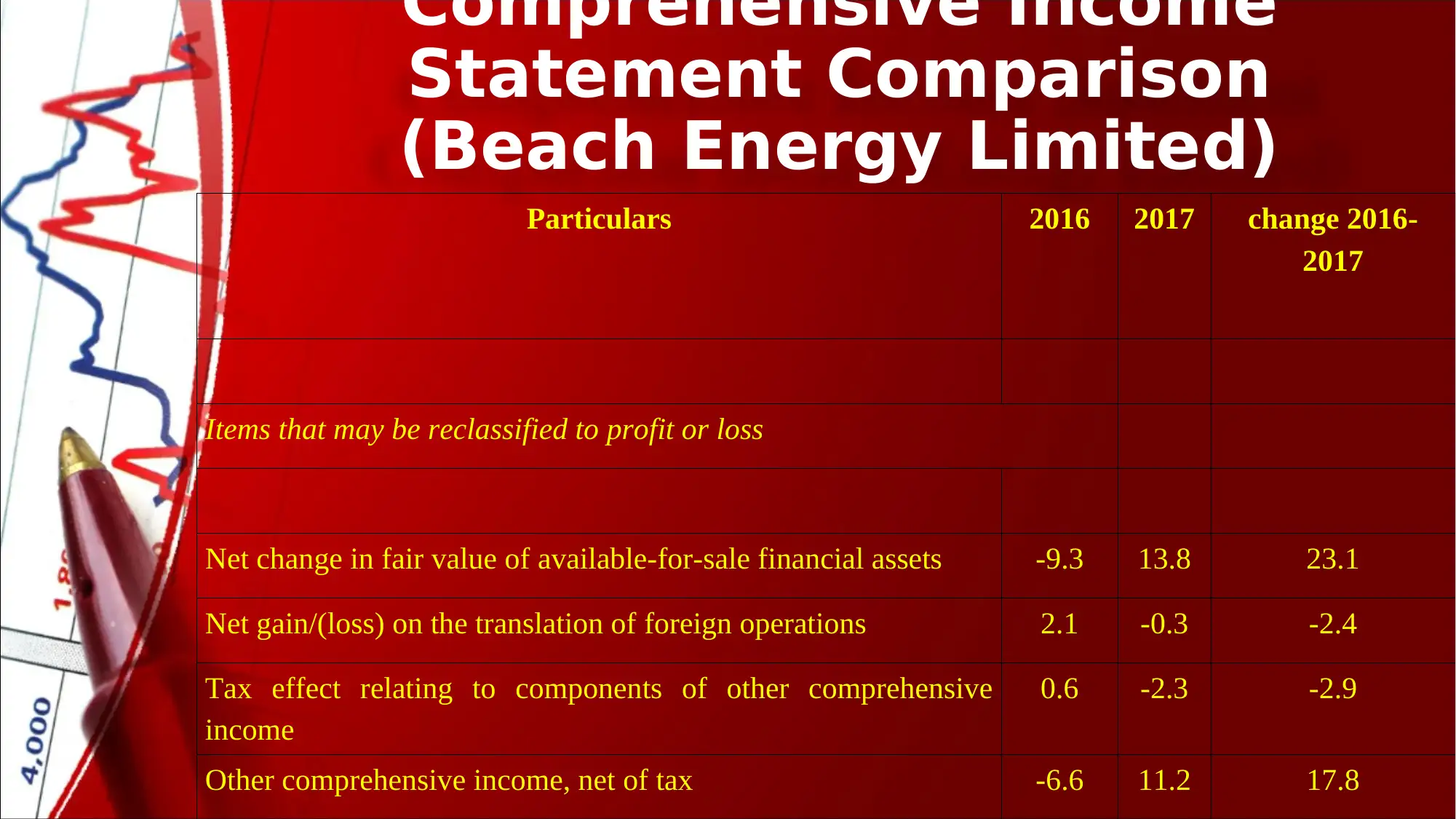

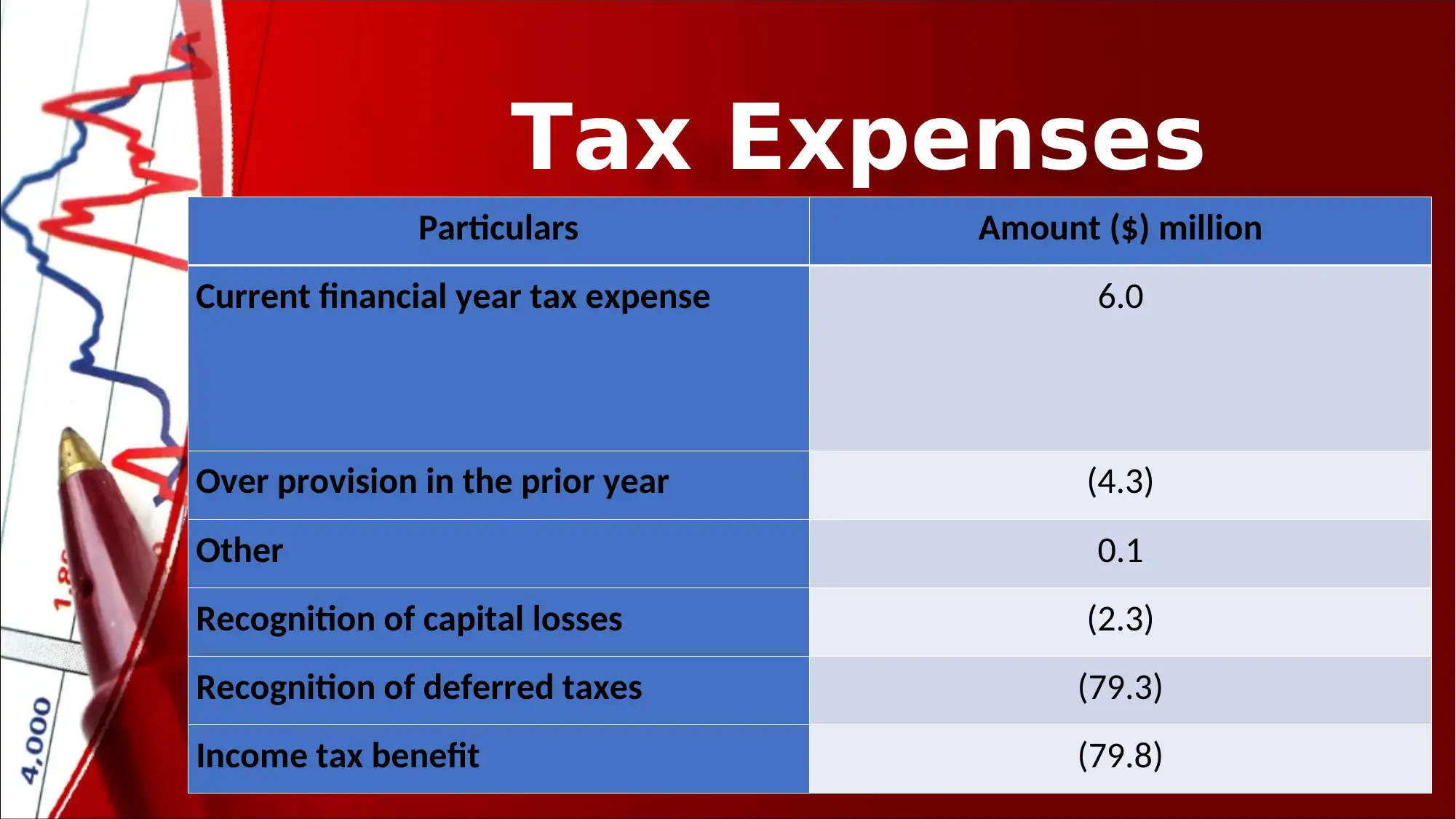

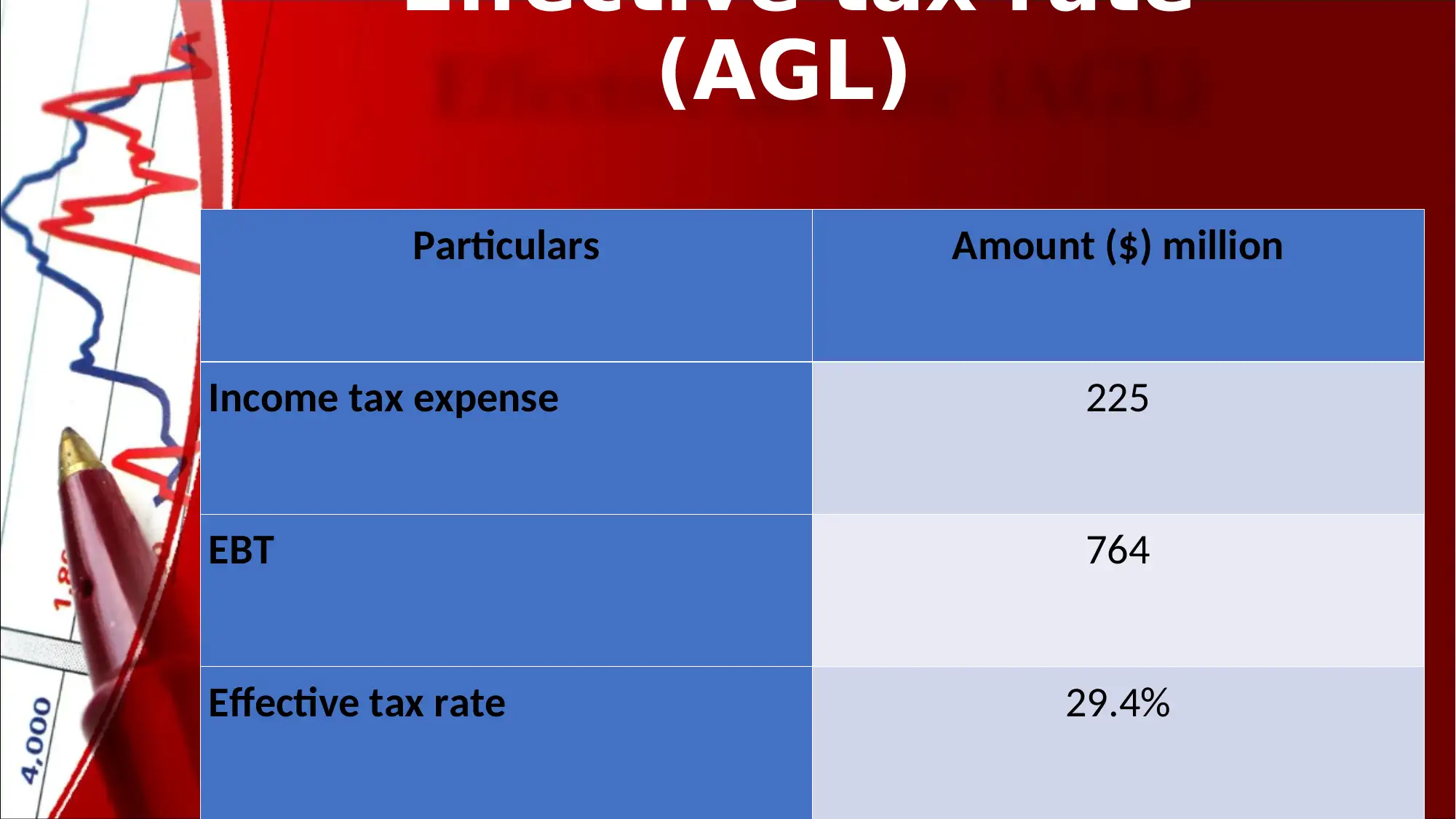

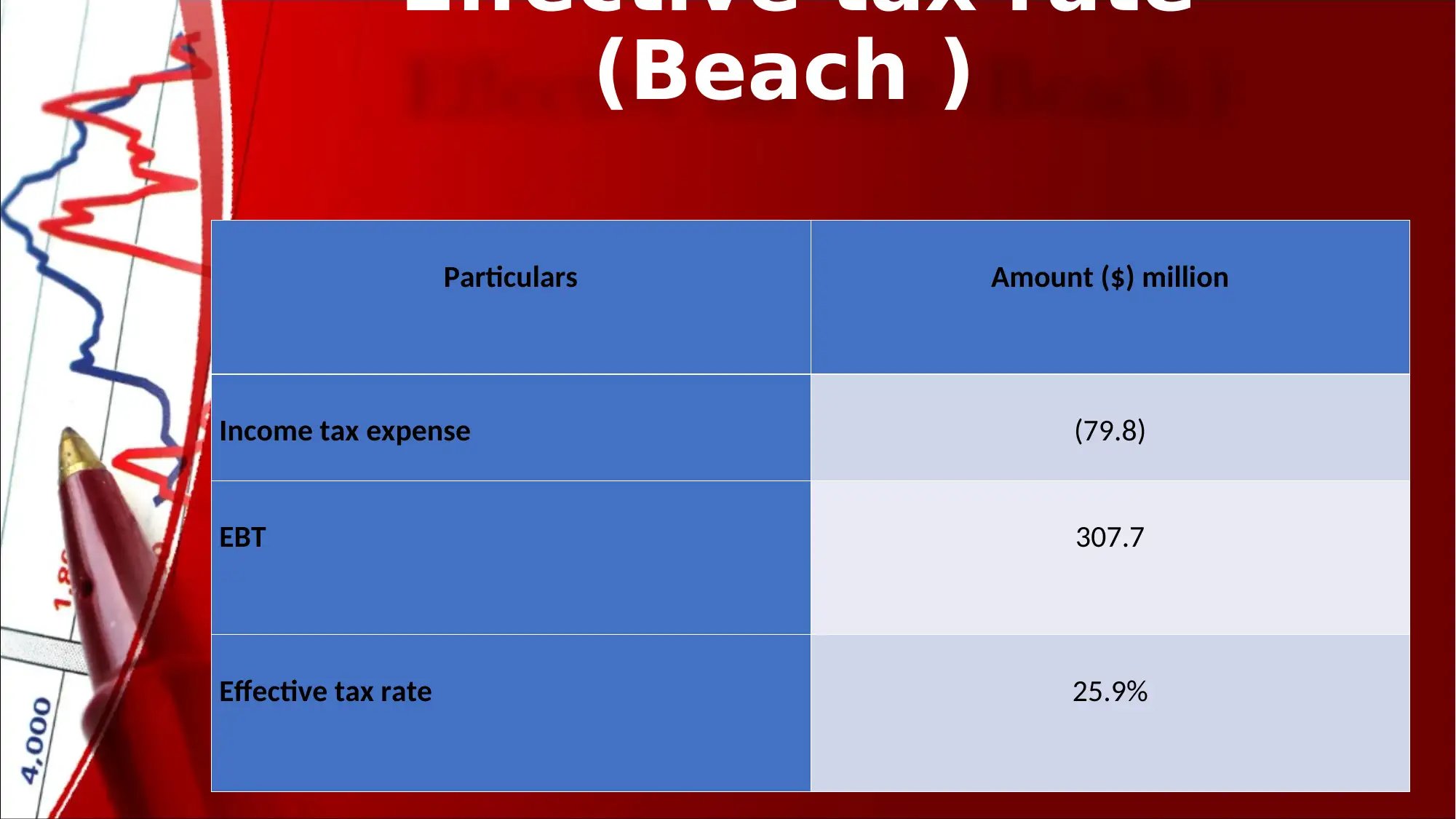

This report provides a comprehensive analysis of AGL Energy Limited and Beach Energy Limited, focusing on key corporate accounting aspects. It examines the owner's equity, compares comprehensive income statements, and analyzes tax expenses, effective tax rates, and deferred tax assets and liabilities for both companies. The report uses data from the companies' annual reports to evaluate their financial positions and changes in their financial performance between 2016 and 2017. The analysis helps in understanding the financial health and tax strategies of AGL Energy and Beach Energy, providing insights into their corporate accounting practices. This document is available on Desklib, a platform offering a range of study tools and solved assignments for students.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.