HI5020 Corporate Accounting: Comparative Analysis of Woolworths

VerifiedAdded on 2023/06/11

|20

|4235

|414

Report

AI Summary

This report presents a comprehensive financial analysis of two major Australian companies, Woolworths and Wesfarmers, both operating within the food and staples industry. The analysis encompasses various financial and accounting concepts to evaluate the companies' performance. Key areas explored include an analysis of owners' equity, detailing changes in issued capital, retained earnings, and reserves. The report also provides a comparative analysis of cash flow statements, examining cash flows from operating, investing, and financing activities over the past three years. Furthermore, it delves into other comprehensive income, identifying reported items and their impact on performance evaluation. Finally, the report analyzes corporate income tax, including tax expenses, effective tax rates, deferred tax assets and liabilities, and cash tax calculations, concluding with a discussion on the reasons for differences between cash and book tax rates. This report is designed to provide a thorough understanding of the financial health and operational efficiency of Woolworths and Wesfarmers.

Corporate Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The following assignment contains an analysis on the financial statement of the two major

companies in Australia- Woolworths and Wesfarmers. Both the company belong to the food

and staples industry in Australia. We have used various financial and accounting concepts to

conduct the following analysis.

2

The following assignment contains an analysis on the financial statement of the two major

companies in Australia- Woolworths and Wesfarmers. Both the company belong to the food

and staples industry in Australia. We have used various financial and accounting concepts to

conduct the following analysis.

2

Contents

Introduction...........................................................................................................................................4

Analysis of Owners Equity....................................................................................................................5

Understanding of Equity....................................................................................................................5

Debt and equity of both the companies..............................................................................................7

Analysis of Cash flow statement...........................................................................................................8

Overview of the cash flow statement.................................................................................................8

Comparison of the cash flows of last three years...............................................................................9

Overall Analysis of cash flow of both the companies:.....................................................................10

Analysis of other comprehensive income............................................................................................12

Items reported in the other comprehensive income statement..........................................................12

Reasons of reporting these items in other comprehensive income statement...................................12

Comparative analysis of the items of both the companies...............................................................12

Consideration of Items of OCI in evaluating the performance of the managers..............................13

Analysis of Corporate income tax.......................................................................................................14

Tax expenses of the companies.......................................................................................................14

Effective tax rate of both the companies..........................................................................................14

Deferred tax assets and liabilities....................................................................................................14

Change in deferred tax for the companies........................................................................................15

Calculation of cash tax for the companies using book tax...............................................................15

Analysis of cash tax rate for both the companies.............................................................................16

Reasons of difference between the cash and book tax rates.............................................................16

Conclusion...........................................................................................................................................18

Bibliography........................................................................................................................................19

3

Introduction...........................................................................................................................................4

Analysis of Owners Equity....................................................................................................................5

Understanding of Equity....................................................................................................................5

Debt and equity of both the companies..............................................................................................7

Analysis of Cash flow statement...........................................................................................................8

Overview of the cash flow statement.................................................................................................8

Comparison of the cash flows of last three years...............................................................................9

Overall Analysis of cash flow of both the companies:.....................................................................10

Analysis of other comprehensive income............................................................................................12

Items reported in the other comprehensive income statement..........................................................12

Reasons of reporting these items in other comprehensive income statement...................................12

Comparative analysis of the items of both the companies...............................................................12

Consideration of Items of OCI in evaluating the performance of the managers..............................13

Analysis of Corporate income tax.......................................................................................................14

Tax expenses of the companies.......................................................................................................14

Effective tax rate of both the companies..........................................................................................14

Deferred tax assets and liabilities....................................................................................................14

Change in deferred tax for the companies........................................................................................15

Calculation of cash tax for the companies using book tax...............................................................15

Analysis of cash tax rate for both the companies.............................................................................16

Reasons of difference between the cash and book tax rates.............................................................16

Conclusion...........................................................................................................................................18

Bibliography........................................................................................................................................19

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The following report contains a detailed analysis on equity, other comprehensive income,

cash flow statement and the tax expense of the two top players of the food and retail industry

in Australia, Woolworths and Wesfarmers group.

Woolworths group is a top retail group which has its business spread across Australia and

major parts of New Zealand. It is the second largest revenue generating company in Australia

and New Zealand. The company is also engages in the business of takeaway liquor store,

hotel business and gaming poker machines. The company was ranked as the nineteenth

largest retailer in world in the year 2008. The company when established in 1924 was popular

for using the cash registers which printed electronic receipts. Later with the growth in

business the company got listed in the early nineteen nineties.

Wesfarmers limited is an Australian conglomerate which has its headquarters situated in

Perth, Western Australia, which also has its business spread across New Zealand. It is the

largest revenue generating company of Australia. Also, it is the top private employer of about

220000 employees in Australia. The company is engaged in business of chemicals, industrial

and safety products along with retail. The group was first formed as a cooperative society in

1914 and later got converted and listed on the Australian stock exchange in 1984.

Therefore, we see that both the companies are the top players of the food and staples industry

in Australia.

4

The following report contains a detailed analysis on equity, other comprehensive income,

cash flow statement and the tax expense of the two top players of the food and retail industry

in Australia, Woolworths and Wesfarmers group.

Woolworths group is a top retail group which has its business spread across Australia and

major parts of New Zealand. It is the second largest revenue generating company in Australia

and New Zealand. The company is also engages in the business of takeaway liquor store,

hotel business and gaming poker machines. The company was ranked as the nineteenth

largest retailer in world in the year 2008. The company when established in 1924 was popular

for using the cash registers which printed electronic receipts. Later with the growth in

business the company got listed in the early nineteen nineties.

Wesfarmers limited is an Australian conglomerate which has its headquarters situated in

Perth, Western Australia, which also has its business spread across New Zealand. It is the

largest revenue generating company of Australia. Also, it is the top private employer of about

220000 employees in Australia. The company is engaged in business of chemicals, industrial

and safety products along with retail. The group was first formed as a cooperative society in

1914 and later got converted and listed on the Australian stock exchange in 1984.

Therefore, we see that both the companies are the top players of the food and staples industry

in Australia.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

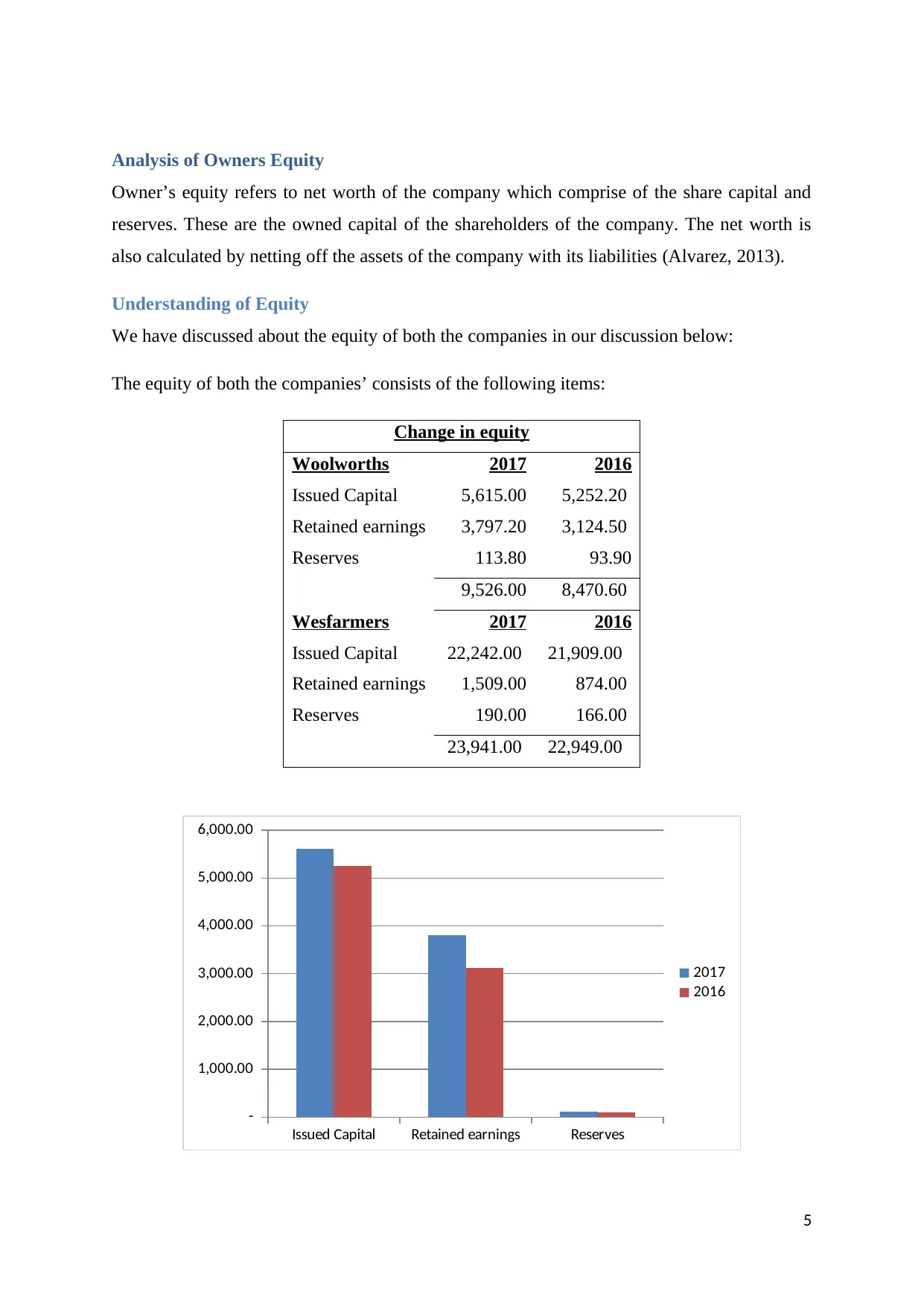

Analysis of Owners Equity

Owner’s equity refers to net worth of the company which comprise of the share capital and

reserves. These are the owned capital of the shareholders of the company. The net worth is

also calculated by netting off the assets of the company with its liabilities (Alvarez, 2013).

Understanding of Equity

We have discussed about the equity of both the companies in our discussion below:

The equity of both the companies’ consists of the following items:

Change in equity

Woolworths 2017 2016

Issued Capital 5,615.00 5,252.20

Retained earnings 3,797.20 3,124.50

Reserves 113.80 93.90

9,526.00 8,470.60

Wesfarmers 2017 2016

Issued Capital 22,242.00 21,909.00

Retained earnings 1,509.00 874.00

Reserves 190.00 166.00

23,941.00 22,949.00

Issued Capital Retained earnings Reserves

-

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

6,000.00

2017

2016

5

Owner’s equity refers to net worth of the company which comprise of the share capital and

reserves. These are the owned capital of the shareholders of the company. The net worth is

also calculated by netting off the assets of the company with its liabilities (Alvarez, 2013).

Understanding of Equity

We have discussed about the equity of both the companies in our discussion below:

The equity of both the companies’ consists of the following items:

Change in equity

Woolworths 2017 2016

Issued Capital 5,615.00 5,252.20

Retained earnings 3,797.20 3,124.50

Reserves 113.80 93.90

9,526.00 8,470.60

Wesfarmers 2017 2016

Issued Capital 22,242.00 21,909.00

Retained earnings 1,509.00 874.00

Reserves 190.00 166.00

23,941.00 22,949.00

Issued Capital Retained earnings Reserves

-

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

6,000.00

2017

2016

5

Share capital of Woolworths

Issued Capital Retained earnings Reserves

-

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

2017

2016

Share capital of Wesfarmers

The issues share capital of the companies represents the shares issues and subscribed by the

public and other shareholders. The share capital may consist of preference or equity share.

Both the type of shareholders has their respective characteristics. The shareholders also have

the right to vote in certain decision making matters of the company.

The issued share capital of Woolworth’s group has increased from $5252 million to $5615

million, and that of Wesfarmers have increased from $21909 million to $22242 million.

Increase in the share capital represents issue of new shares or capitalisation of profits by the

company. The reserves of Woolworths have increased from 93.9 million to 113.8 million and

that of Wesfarmers have increased from 166 million to 190 million. The reserves of the

company represent the excess profits of the company which have been set aside in order to

fulfil certain obligations. The retained earnings of the company represent the profits earned

by the company which have accumulated over the years. The retained earnings of

Wesfarmers have increased from 3124.5 million to 3797.2 million, and the retained earnings

of Wesfarmers have increased from 874 million to 1509 million.

Therefore we see that the owner’s equity of both the companies has increased from last year.

The total increase in owners’ equity of Woolworths was for 1055.40 million and than for the

Wesfarmers group was 992 million.

6

Issued Capital Retained earnings Reserves

-

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

2017

2016

Share capital of Wesfarmers

The issues share capital of the companies represents the shares issues and subscribed by the

public and other shareholders. The share capital may consist of preference or equity share.

Both the type of shareholders has their respective characteristics. The shareholders also have

the right to vote in certain decision making matters of the company.

The issued share capital of Woolworth’s group has increased from $5252 million to $5615

million, and that of Wesfarmers have increased from $21909 million to $22242 million.

Increase in the share capital represents issue of new shares or capitalisation of profits by the

company. The reserves of Woolworths have increased from 93.9 million to 113.8 million and

that of Wesfarmers have increased from 166 million to 190 million. The reserves of the

company represent the excess profits of the company which have been set aside in order to

fulfil certain obligations. The retained earnings of the company represent the profits earned

by the company which have accumulated over the years. The retained earnings of

Wesfarmers have increased from 3124.5 million to 3797.2 million, and the retained earnings

of Wesfarmers have increased from 874 million to 1509 million.

Therefore we see that the owner’s equity of both the companies has increased from last year.

The total increase in owners’ equity of Woolworths was for 1055.40 million and than for the

Wesfarmers group was 992 million.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

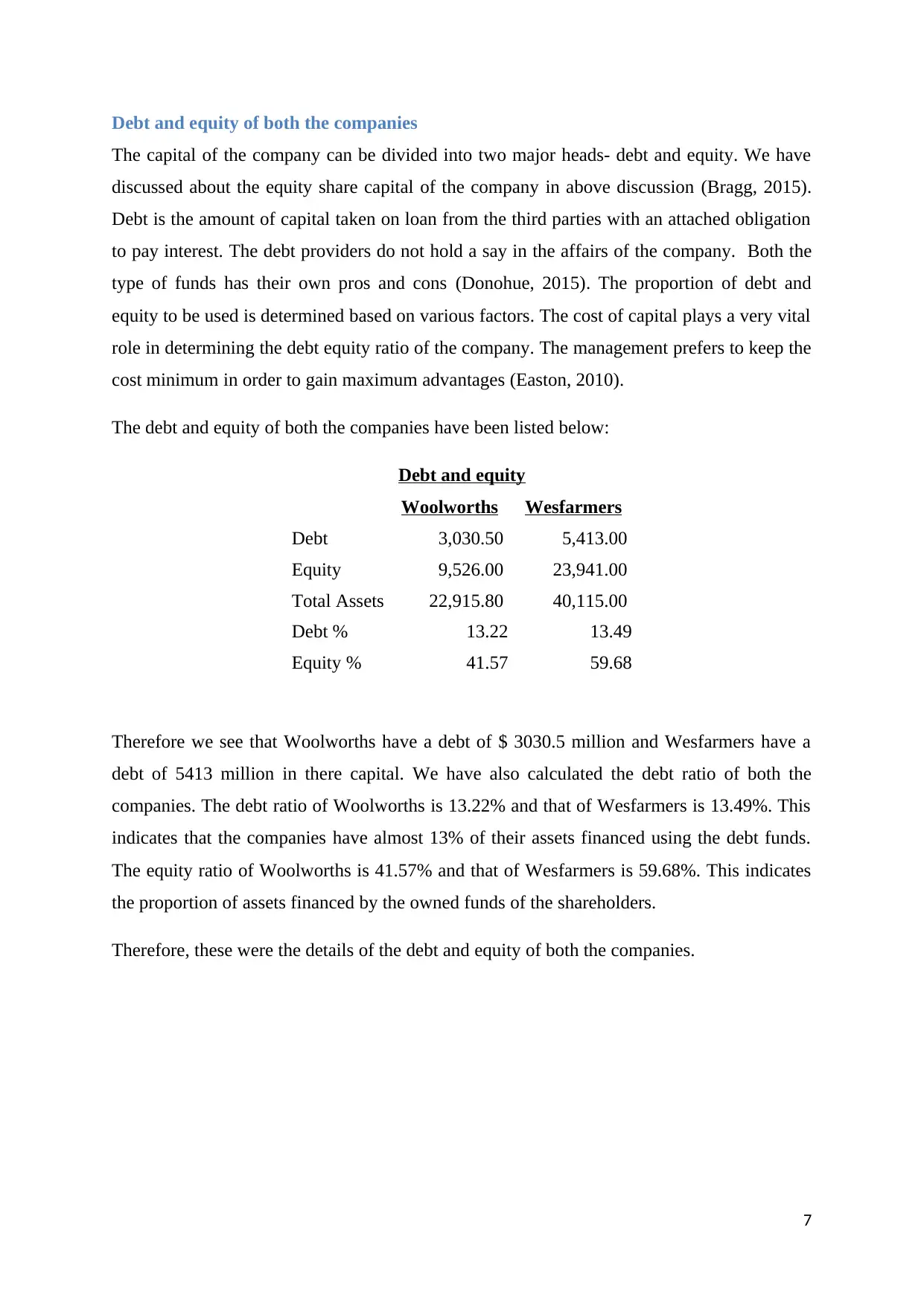

Debt and equity of both the companies

The capital of the company can be divided into two major heads- debt and equity. We have

discussed about the equity share capital of the company in above discussion (Bragg, 2015).

Debt is the amount of capital taken on loan from the third parties with an attached obligation

to pay interest. The debt providers do not hold a say in the affairs of the company. Both the

type of funds has their own pros and cons (Donohue, 2015). The proportion of debt and

equity to be used is determined based on various factors. The cost of capital plays a very vital

role in determining the debt equity ratio of the company. The management prefers to keep the

cost minimum in order to gain maximum advantages (Easton, 2010).

The debt and equity of both the companies have been listed below:

Debt and equity

Woolworths Wesfarmers

Debt 3,030.50 5,413.00

Equity 9,526.00 23,941.00

Total Assets 22,915.80 40,115.00

Debt % 13.22 13.49

Equity % 41.57 59.68

Therefore we see that Woolworths have a debt of $ 3030.5 million and Wesfarmers have a

debt of 5413 million in there capital. We have also calculated the debt ratio of both the

companies. The debt ratio of Woolworths is 13.22% and that of Wesfarmers is 13.49%. This

indicates that the companies have almost 13% of their assets financed using the debt funds.

The equity ratio of Woolworths is 41.57% and that of Wesfarmers is 59.68%. This indicates

the proportion of assets financed by the owned funds of the shareholders.

Therefore, these were the details of the debt and equity of both the companies.

7

The capital of the company can be divided into two major heads- debt and equity. We have

discussed about the equity share capital of the company in above discussion (Bragg, 2015).

Debt is the amount of capital taken on loan from the third parties with an attached obligation

to pay interest. The debt providers do not hold a say in the affairs of the company. Both the

type of funds has their own pros and cons (Donohue, 2015). The proportion of debt and

equity to be used is determined based on various factors. The cost of capital plays a very vital

role in determining the debt equity ratio of the company. The management prefers to keep the

cost minimum in order to gain maximum advantages (Easton, 2010).

The debt and equity of both the companies have been listed below:

Debt and equity

Woolworths Wesfarmers

Debt 3,030.50 5,413.00

Equity 9,526.00 23,941.00

Total Assets 22,915.80 40,115.00

Debt % 13.22 13.49

Equity % 41.57 59.68

Therefore we see that Woolworths have a debt of $ 3030.5 million and Wesfarmers have a

debt of 5413 million in there capital. We have also calculated the debt ratio of both the

companies. The debt ratio of Woolworths is 13.22% and that of Wesfarmers is 13.49%. This

indicates that the companies have almost 13% of their assets financed using the debt funds.

The equity ratio of Woolworths is 41.57% and that of Wesfarmers is 59.68%. This indicates

the proportion of assets financed by the owned funds of the shareholders.

Therefore, these were the details of the debt and equity of both the companies.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analysis of Cash flow statement

The books of accounts of the companies are required to be made on accrual basis in order to

determine the profitability of the business for a given period (Elaine, 2015). The actual cash

inflows and outflows are not taken into consideration while evaluating the profitability. But it

is important that cash flows of the companies are also reported in order to keep the liquidity

of the company in check (Fisher, 2012). In our discussion below we have discussed about the

cash flow statement of both the companies. The cash flow statement of the companies

consists of three broad heads- cash from operating, investing and financing activities (Fridson

& Alvarez, 2012).

Overview of the cash flow statement

The cash from operating activities of Woolworths group mainly comprise of cash flows from

activities like receipts from customers, payment to suppliers. The net cash flow from

operating activities of Woolworths increased from 2357.5 million to 3122 million. The major

increase was result of increase in inflows from customers and decline in payments made to

the suppliers.

The cash from operating activities of Wesfarmers mainly comprise of receipts and payment

for sales and purchases, and other adjustments made in order to arrive at cash from operating

activities. The cash flow from operating activities increased from 3365 million to 4226

million. The major contributor to the increase in cash was a result of increased cash flow

from customers and lower payments made to the suppliers.

The cash outflows from investing activities of Woolworths increased from 1266.7 million to

1431.4 million. The increase in the outflows was a result of increased investments made in

plant and other assets by the company in the current year.

The cash outflows from investing activities of the Wesfarmers declined from 2132 million to

53 million. The decline in cash outflows was a result of increased cash inflows from sale of

subsidiaries which offset the outflows of cash made in connection with other investments.

The cash outflows from financing activities of Woolworths increased from 1474.9 million to

1729.3 million. The increase in outflows was due to increased payments made in connections

with the borrowings.

8

The books of accounts of the companies are required to be made on accrual basis in order to

determine the profitability of the business for a given period (Elaine, 2015). The actual cash

inflows and outflows are not taken into consideration while evaluating the profitability. But it

is important that cash flows of the companies are also reported in order to keep the liquidity

of the company in check (Fisher, 2012). In our discussion below we have discussed about the

cash flow statement of both the companies. The cash flow statement of the companies

consists of three broad heads- cash from operating, investing and financing activities (Fridson

& Alvarez, 2012).

Overview of the cash flow statement

The cash from operating activities of Woolworths group mainly comprise of cash flows from

activities like receipts from customers, payment to suppliers. The net cash flow from

operating activities of Woolworths increased from 2357.5 million to 3122 million. The major

increase was result of increase in inflows from customers and decline in payments made to

the suppliers.

The cash from operating activities of Wesfarmers mainly comprise of receipts and payment

for sales and purchases, and other adjustments made in order to arrive at cash from operating

activities. The cash flow from operating activities increased from 3365 million to 4226

million. The major contributor to the increase in cash was a result of increased cash flow

from customers and lower payments made to the suppliers.

The cash outflows from investing activities of Woolworths increased from 1266.7 million to

1431.4 million. The increase in the outflows was a result of increased investments made in

plant and other assets by the company in the current year.

The cash outflows from investing activities of the Wesfarmers declined from 2132 million to

53 million. The decline in cash outflows was a result of increased cash inflows from sale of

subsidiaries which offset the outflows of cash made in connection with other investments.

The cash outflows from financing activities of Woolworths increased from 1474.9 million to

1729.3 million. The increase in outflows was due to increased payments made in connections

with the borrowings.

8

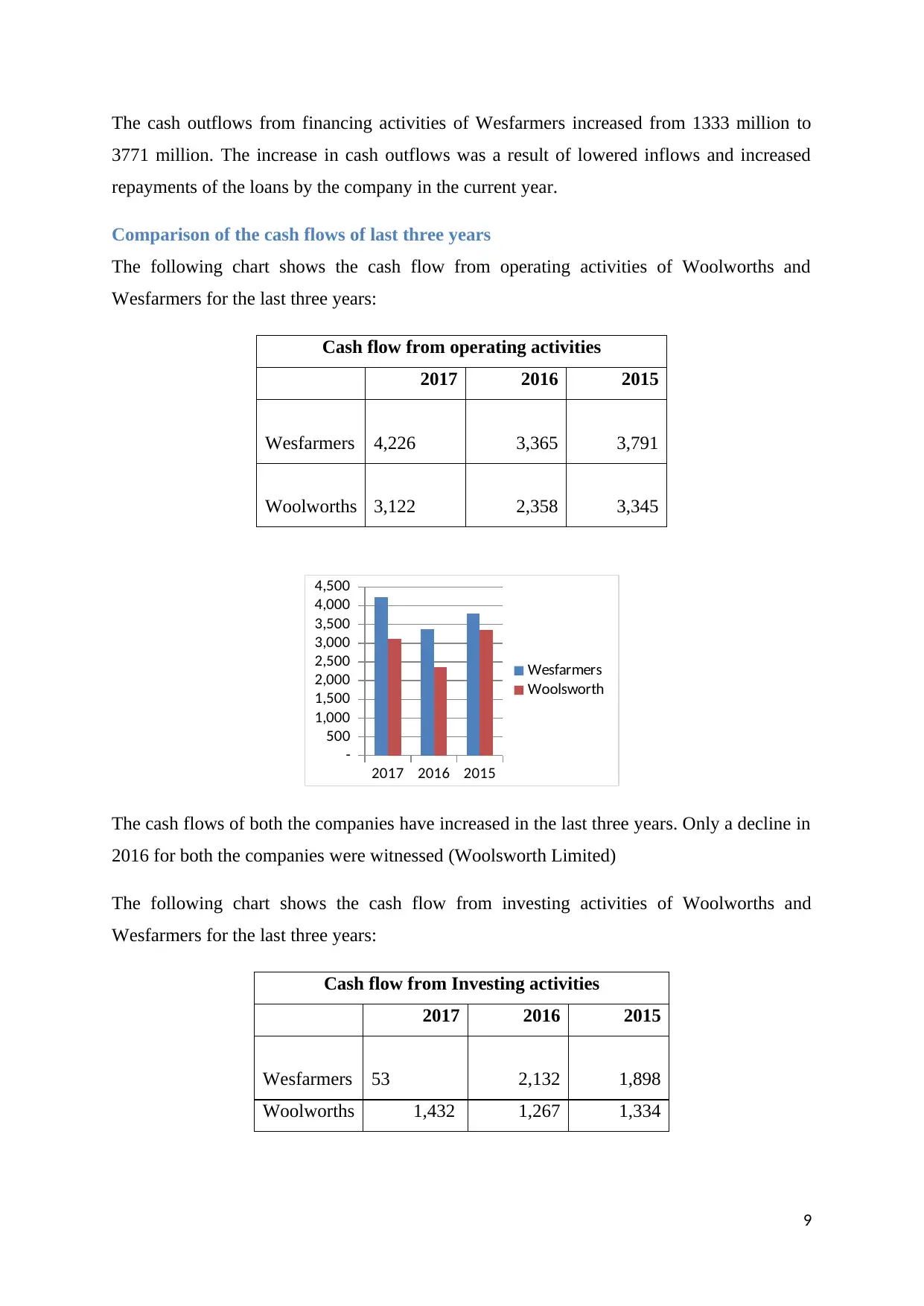

The cash outflows from financing activities of Wesfarmers increased from 1333 million to

3771 million. The increase in cash outflows was a result of lowered inflows and increased

repayments of the loans by the company in the current year.

Comparison of the cash flows of last three years

The following chart shows the cash flow from operating activities of Woolworths and

Wesfarmers for the last three years:

Cash flow from operating activities

2017 2016 2015

Wesfarmers 4,226 3,365 3,791

Woolworths 3,122 2,358 3,345

2017 2016 2015

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Wesfarmers

Woolsworth

The cash flows of both the companies have increased in the last three years. Only a decline in

2016 for both the companies were witnessed (Woolsworth Limited)

The following chart shows the cash flow from investing activities of Woolworths and

Wesfarmers for the last three years:

Cash flow from Investing activities

2017 2016 2015

Wesfarmers 53 2,132 1,898

Woolworths 1,432 1,267 1,334

9

3771 million. The increase in cash outflows was a result of lowered inflows and increased

repayments of the loans by the company in the current year.

Comparison of the cash flows of last three years

The following chart shows the cash flow from operating activities of Woolworths and

Wesfarmers for the last three years:

Cash flow from operating activities

2017 2016 2015

Wesfarmers 4,226 3,365 3,791

Woolworths 3,122 2,358 3,345

2017 2016 2015

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Wesfarmers

Woolsworth

The cash flows of both the companies have increased in the last three years. Only a decline in

2016 for both the companies were witnessed (Woolsworth Limited)

The following chart shows the cash flow from investing activities of Woolworths and

Wesfarmers for the last three years:

Cash flow from Investing activities

2017 2016 2015

Wesfarmers 53 2,132 1,898

Woolworths 1,432 1,267 1,334

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2017 2016 2015

-

500

1,000

1,500

2,000

2,500

Wesfarmers

Woolsworth

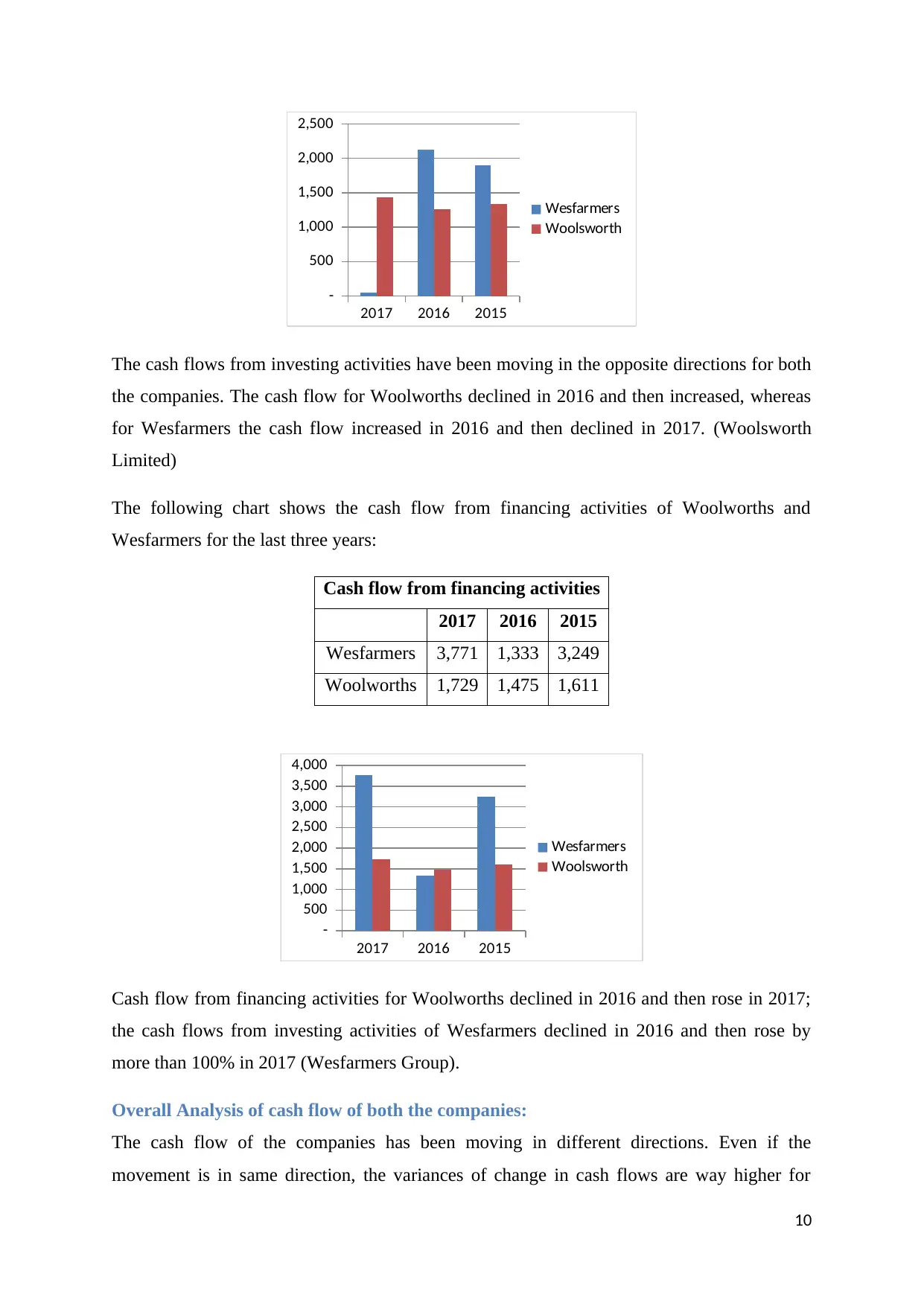

The cash flows from investing activities have been moving in the opposite directions for both

the companies. The cash flow for Woolworths declined in 2016 and then increased, whereas

for Wesfarmers the cash flow increased in 2016 and then declined in 2017. (Woolsworth

Limited)

The following chart shows the cash flow from financing activities of Woolworths and

Wesfarmers for the last three years:

Cash flow from financing activities

2017 2016 2015

Wesfarmers 3,771 1,333 3,249

Woolworths 1,729 1,475 1,611

2017 2016 2015

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Wesfarmers

Woolsworth

Cash flow from financing activities for Woolworths declined in 2016 and then rose in 2017;

the cash flows from investing activities of Wesfarmers declined in 2016 and then rose by

more than 100% in 2017 (Wesfarmers Group).

Overall Analysis of cash flow of both the companies:

The cash flow of the companies has been moving in different directions. Even if the

movement is in same direction, the variances of change in cash flows are way higher for

10

-

500

1,000

1,500

2,000

2,500

Wesfarmers

Woolsworth

The cash flows from investing activities have been moving in the opposite directions for both

the companies. The cash flow for Woolworths declined in 2016 and then increased, whereas

for Wesfarmers the cash flow increased in 2016 and then declined in 2017. (Woolsworth

Limited)

The following chart shows the cash flow from financing activities of Woolworths and

Wesfarmers for the last three years:

Cash flow from financing activities

2017 2016 2015

Wesfarmers 3,771 1,333 3,249

Woolworths 1,729 1,475 1,611

2017 2016 2015

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Wesfarmers

Woolsworth

Cash flow from financing activities for Woolworths declined in 2016 and then rose in 2017;

the cash flows from investing activities of Wesfarmers declined in 2016 and then rose by

more than 100% in 2017 (Wesfarmers Group).

Overall Analysis of cash flow of both the companies:

The cash flow of the companies has been moving in different directions. Even if the

movement is in same direction, the variances of change in cash flows are way higher for

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Wesfarmers than the Woolworths. A gradual increase or decrease in the cash flows of the

Woolworths can be seen, whereas the cash flows of Wesfarmers seem to be volatile with high

variances than the last year.

11

Woolworths can be seen, whereas the cash flows of Wesfarmers seem to be volatile with high

variances than the last year.

11

Analysis of other comprehensive income

Items reported in the other comprehensive income statement

The other comprehensive income of the Woolworths consists of the following items:

- Changes in fair value of the cash flow hedges

- Changes in the exchange rates related to foreign operations

- Changes the fair value of the equity instruments held as investments

- Changes in the value of superannuation fund

- Tax effect on all the above

The other comprehensive income of Wesfarmers consists of the following items:

- Changes in the exchange rate of foreign currency

- Changes in fair value of the cash flow hedges

- Re-measurement of the defined benefit plan

- Tax effect on all the above (Wesfarmers Group)

Therefore we see that the other comprehensive income statement of both the companies have

reported similar items for the year ending 2017.

Reasons of reporting these items in other comprehensive income statement

The items which are recorded in the other comprehensive income represent the amount of

profit and losses that affect the financial statements of the company, but which have not been

realised yet (Girard, 2014). Since, the books are made on accrual basis, these items cannot be

reported in the profit and loss, but in order to meet up with the GAAP requirements, it is

important that they are shown in the books (Ittelson, 2009). Hence the other comprehensive

income shows these items. When they are realised, the relevant amounts are recognised in the

profit and loss statement (Lerner, 2009).

Comparative analysis of the items of both the companies

The other comprehensive income of Woolworths reported about $4.8 million for cash flow

hedge, and that of Wesfarmers reported $23 million. Woolworths reported about 6.9$million

in connection with the foreign exchange fluctuations and Wesfarmers reported $2 million.

The amount reported for changes in the provisions made for payments to employees by

12

Items reported in the other comprehensive income statement

The other comprehensive income of the Woolworths consists of the following items:

- Changes in fair value of the cash flow hedges

- Changes in the exchange rates related to foreign operations

- Changes the fair value of the equity instruments held as investments

- Changes in the value of superannuation fund

- Tax effect on all the above

The other comprehensive income of Wesfarmers consists of the following items:

- Changes in the exchange rate of foreign currency

- Changes in fair value of the cash flow hedges

- Re-measurement of the defined benefit plan

- Tax effect on all the above (Wesfarmers Group)

Therefore we see that the other comprehensive income statement of both the companies have

reported similar items for the year ending 2017.

Reasons of reporting these items in other comprehensive income statement

The items which are recorded in the other comprehensive income represent the amount of

profit and losses that affect the financial statements of the company, but which have not been

realised yet (Girard, 2014). Since, the books are made on accrual basis, these items cannot be

reported in the profit and loss, but in order to meet up with the GAAP requirements, it is

important that they are shown in the books (Ittelson, 2009). Hence the other comprehensive

income shows these items. When they are realised, the relevant amounts are recognised in the

profit and loss statement (Lerner, 2009).

Comparative analysis of the items of both the companies

The other comprehensive income of Woolworths reported about $4.8 million for cash flow

hedge, and that of Wesfarmers reported $23 million. Woolworths reported about 6.9$million

in connection with the foreign exchange fluctuations and Wesfarmers reported $2 million.

The amount reported for changes in the provisions made for payments to employees by

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.