Corporate Accounting: AASB 136 and Impairment of Assets Analysis

VerifiedAdded on 2021/06/17

|8

|1586

|18

Homework Assignment

AI Summary

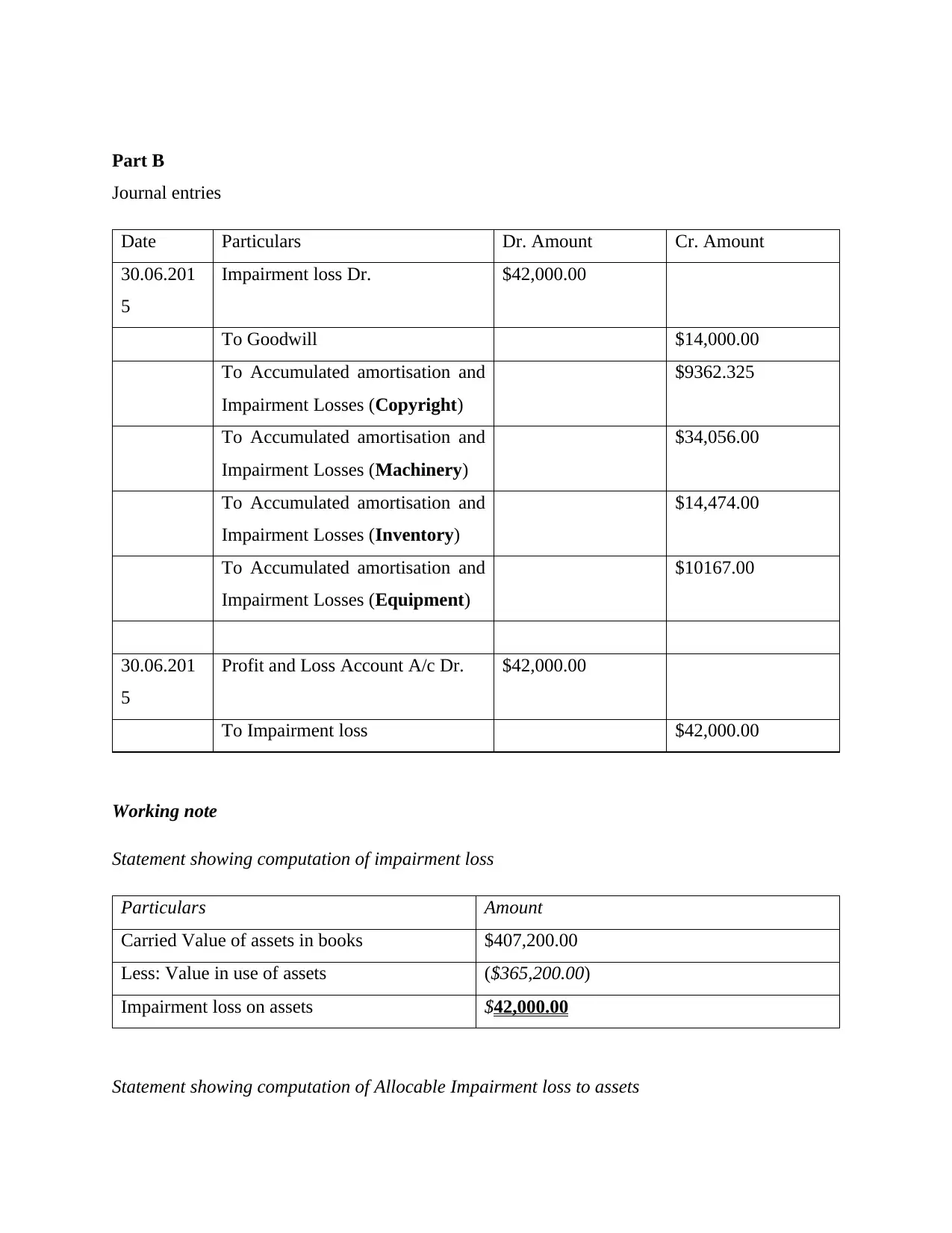

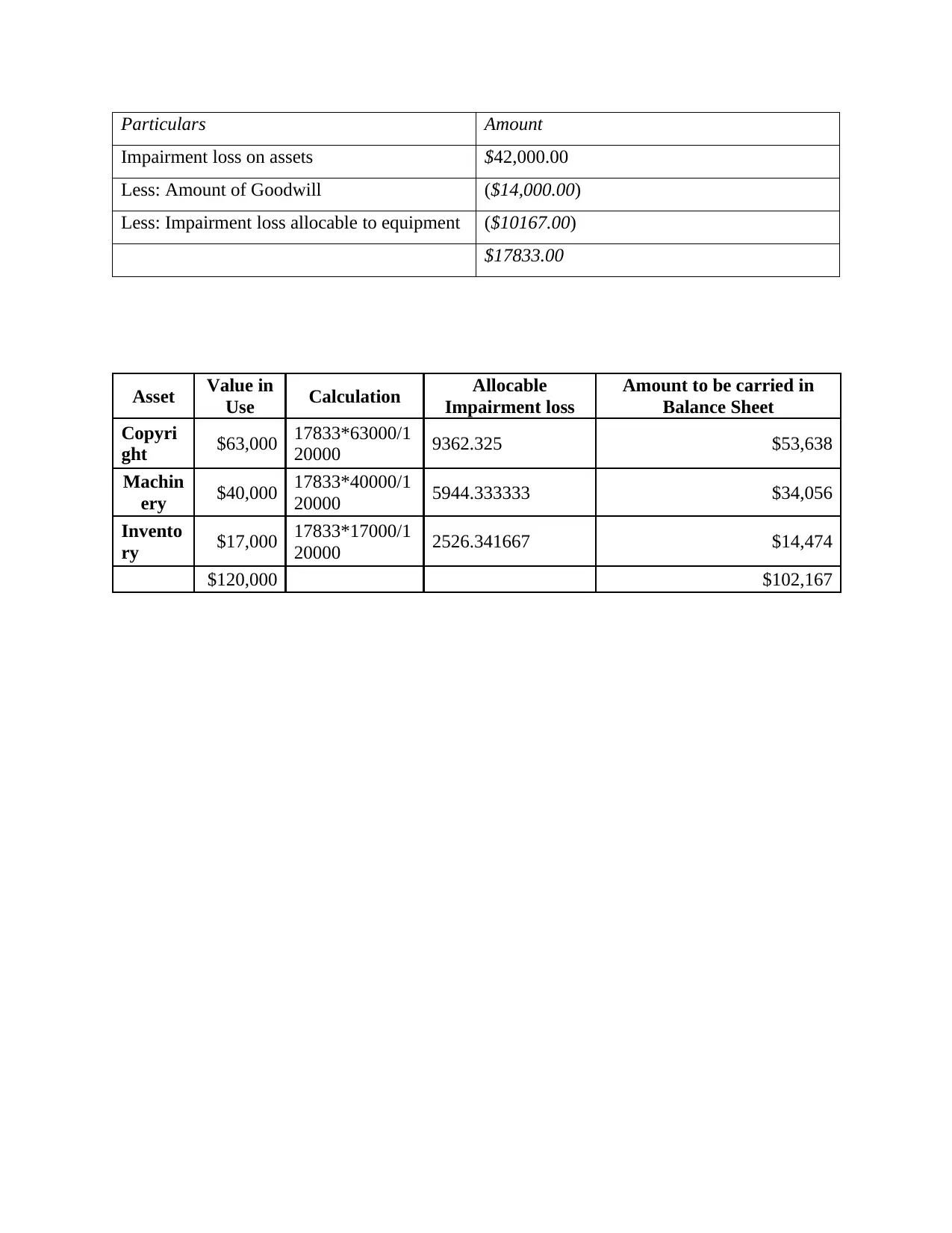

This assignment provides a comprehensive analysis of AASB 136, focusing on the impairment of assets in corporate accounting. The assignment begins with an overview of the standard, explaining its applicability to reporting entities and its objective of ensuring that the carrying amount of an asset does not exceed its recoverable amount. It details the conditions under which impairment losses may occur, distinguishing between external and internal sources of information. The core of the assignment explains the concept of recoverable amount, which is defined as the higher of fair value less costs of disposal and value in use. The calculation of both fair value and value in use are elaborated, including the steps involved in estimating future cash flows and applying an appropriate discount rate. The assignment then moves on to provide the journal entries for impairment loss, along with the working notes showing the computation of the impairment loss and its allocation to different assets like copyright, machinery, inventory and equipment. The assignment concludes with a list of relevant references.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.