University Accounting Assignment: Corporate Structure Analysis

VerifiedAdded on 2020/02/24

|13

|1684

|95

Homework Assignment

AI Summary

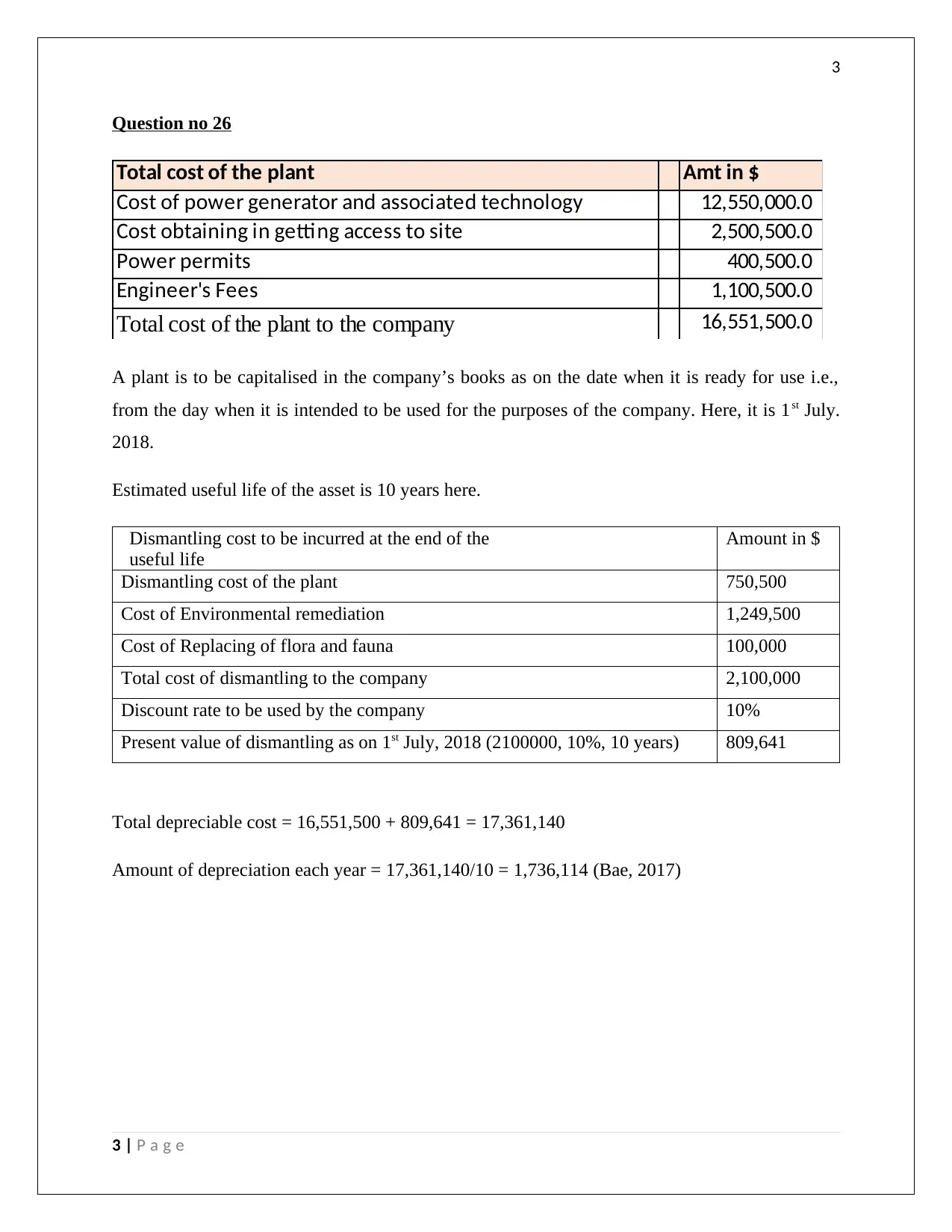

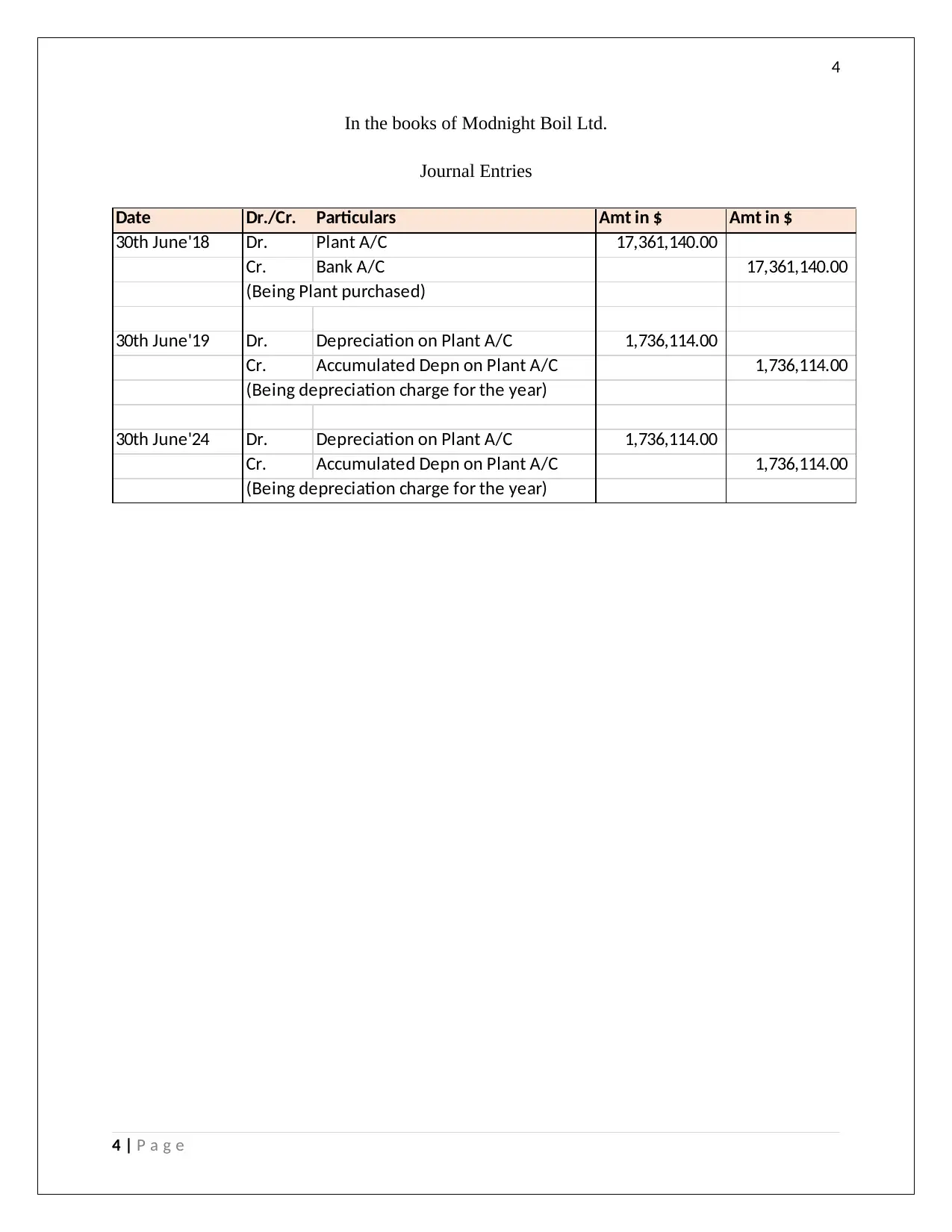

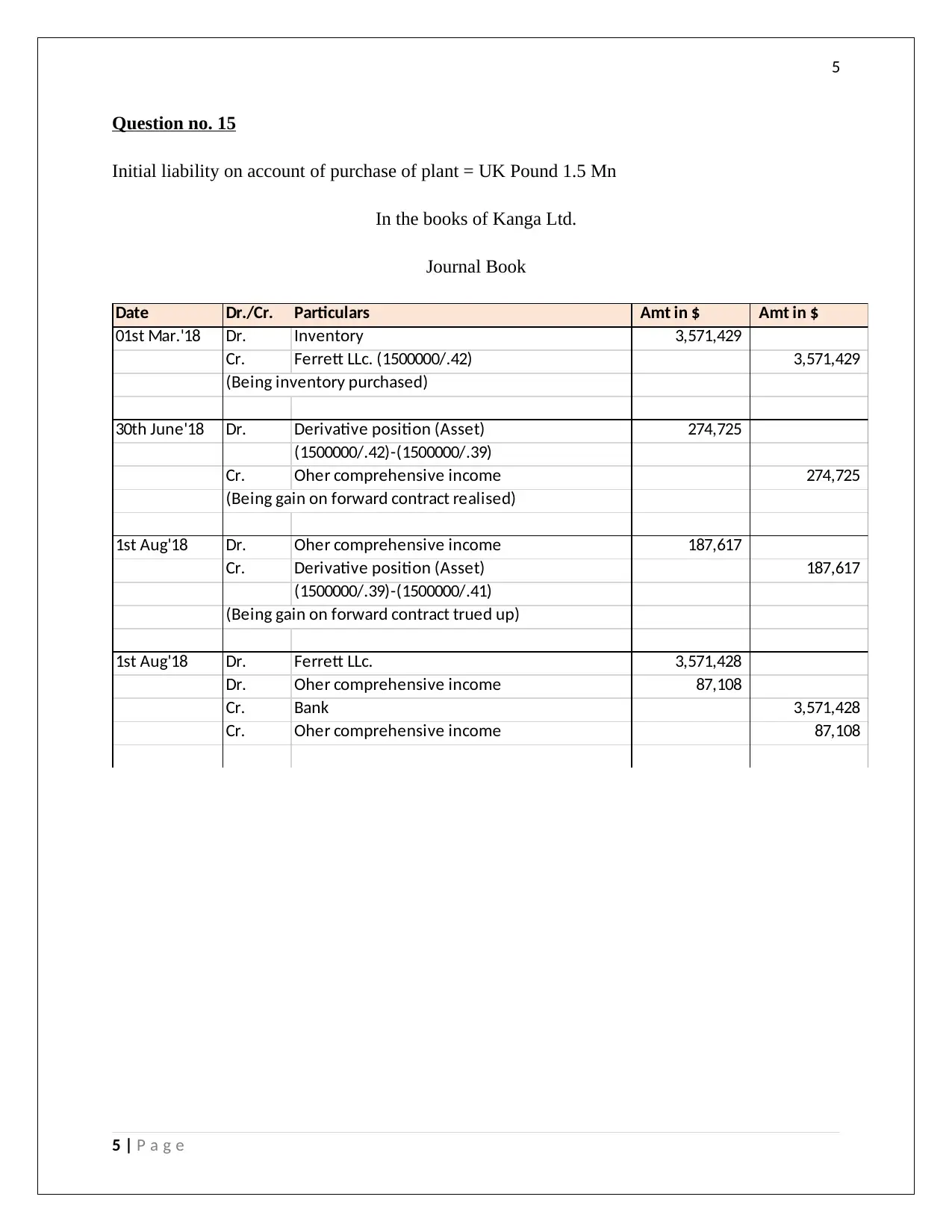

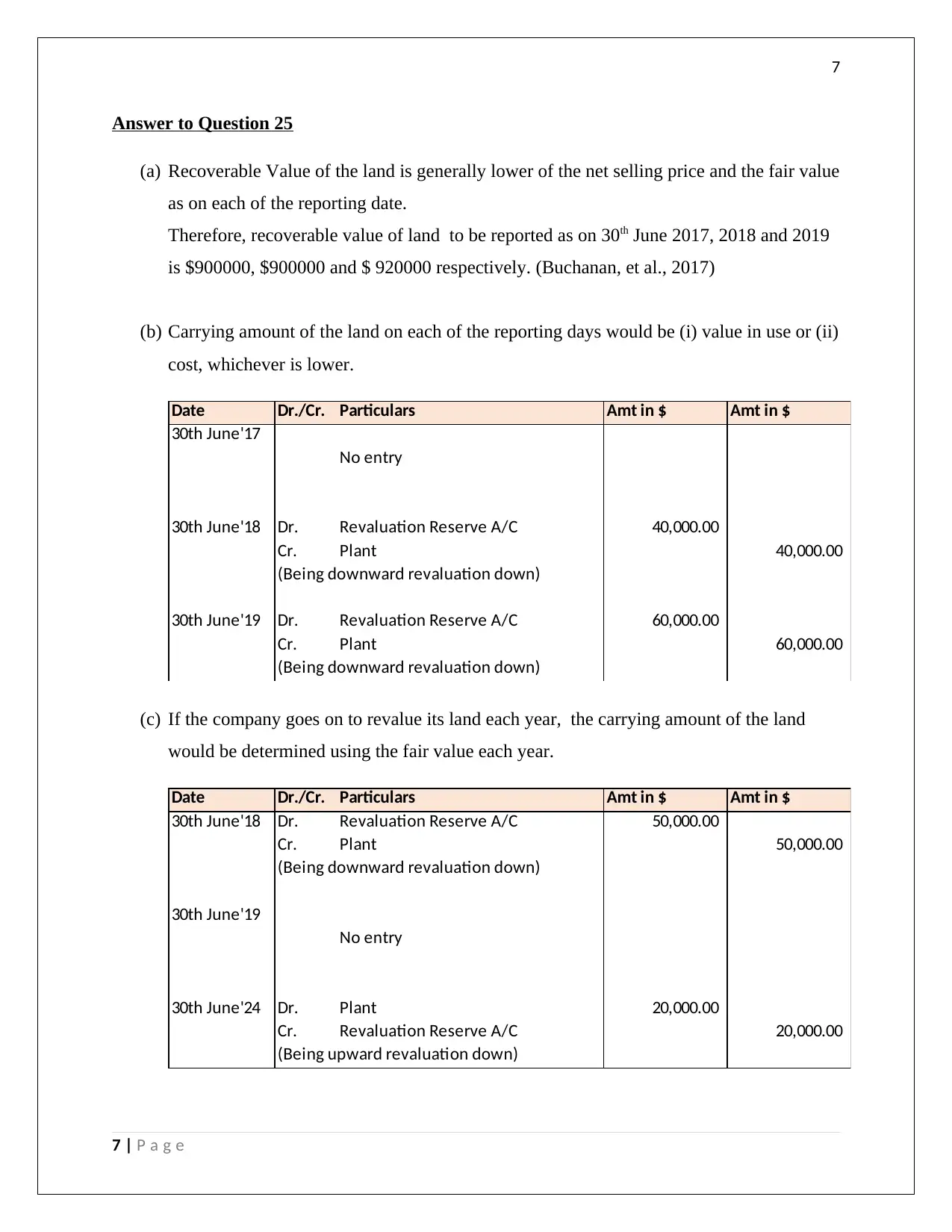

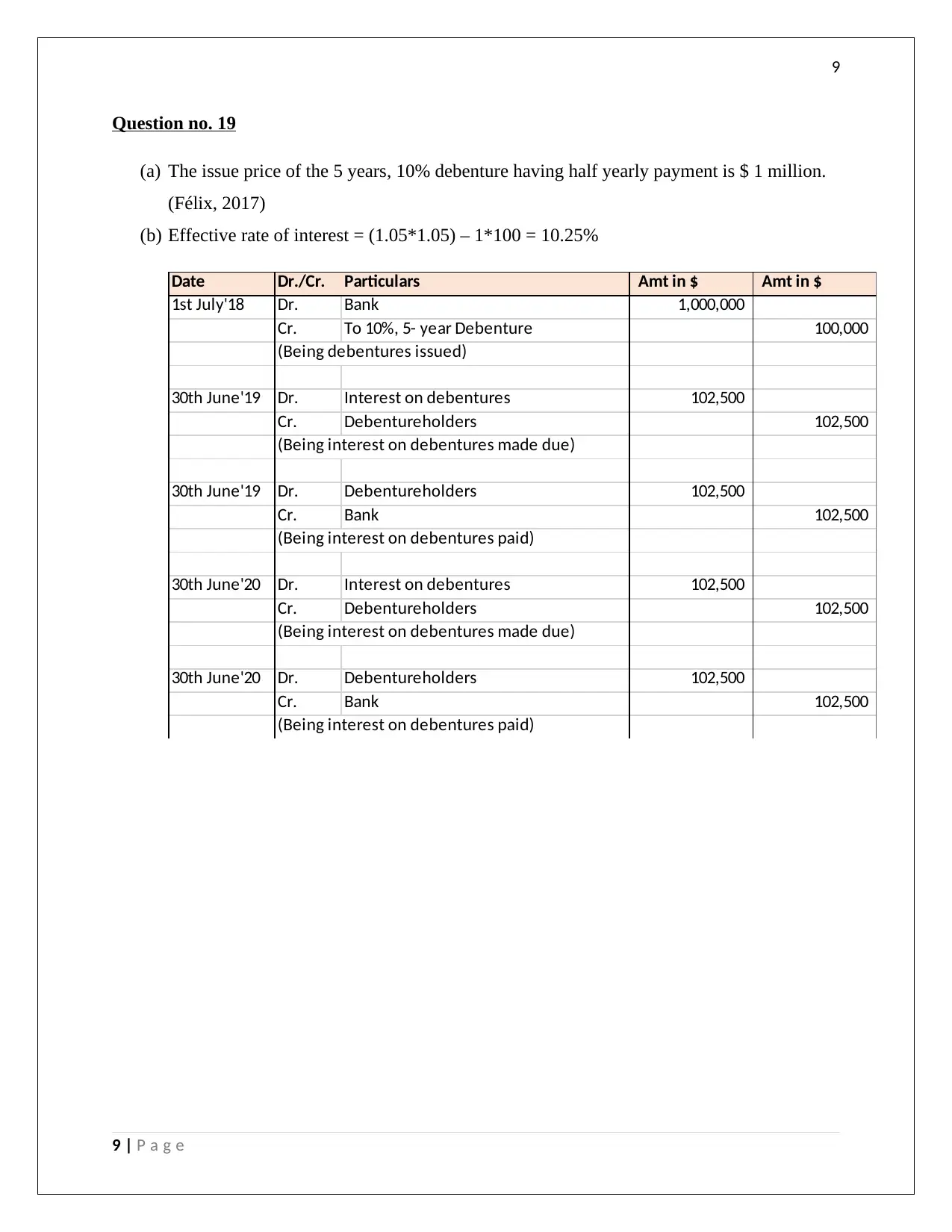

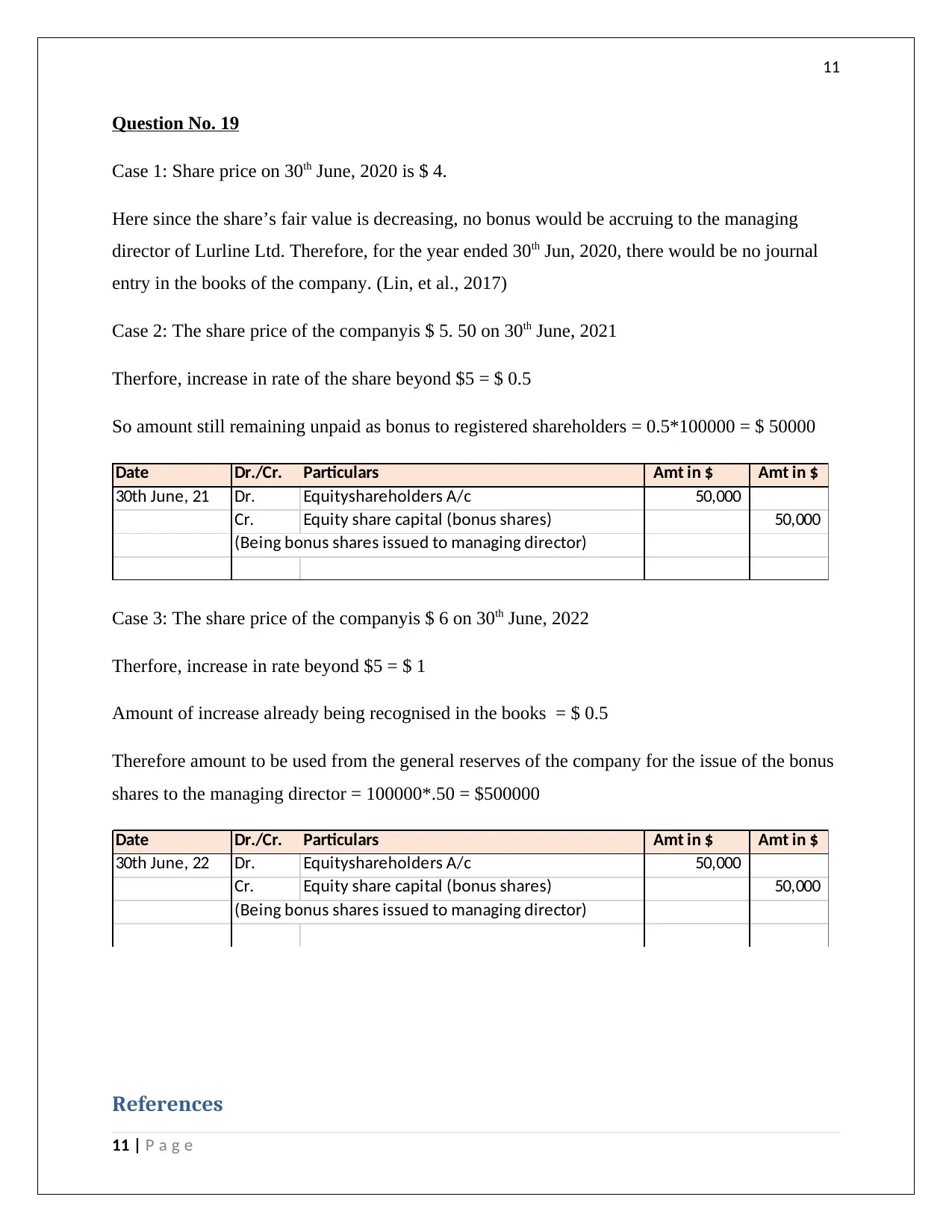

This document presents a comprehensive solution to an accounting assignment focused on corporate structure. It covers several key areas, including the capitalization of a plant with depreciation calculations, journal entries related to plant purchases, and adjustments for foreign currency transactions, including translation reserves and the impact of exchange rate fluctuations on monetary items. The assignment also addresses the valuation of goodwill in acquisitions, the effective interest rate on debentures, and the use of forward contracts to mitigate foreign exchange risk. Furthermore, it analyzes bonus share scenarios for a managing director based on share price performance. The solutions are supported by references to relevant accounting standards and literature, providing a detailed analysis of each question and its corresponding solution.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.