Audit and Assurance Services: Auditor Independence and Risk Analysis

VerifiedAdded on 2020/05/16

|12

|2964

|29

Report

AI Summary

This report provides a comprehensive analysis of audit and assurance services, focusing on the critical aspects of auditor independence and the associated audit risks. It explores the various factors that can undermine auditor independence, including financial interests, long tenure, and intimidation threats. The report delves into the consequences of compromised independence, discussing the impact on audit quality and the potential for financial misstatements. Furthermore, it examines the corporate failures of Enron, Worldcom, and Lehman Brothers, highlighting the lessons learned by accounting professionals from these scandals. The analysis covers the manipulation of financial statements, accounting fraud, and the role of auditors in detecting and preventing such misconduct. The report emphasizes the importance of strong corporate governance, adherence to accounting standards, and the need for auditors to maintain objectivity and professional skepticism to safeguard investor interests and prevent future financial crises.

Running head: AUDIT AND ASSURANCE SERVICES

Audit and assurance services

Name of the university

Name of the student

Authors note

Audit and assurance services

Name of the university

Name of the student

Authors note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDIT AND ASSURANCE SERVICES

Table of Contents

Introduction:....................................................................................................................................2

Discussion:.......................................................................................................................................2

Auditor independence and audit risks:............................................................................................2

Situations leading to creation of threat to auditor’s independence:.................................................4

Reviewing the literature of Enron, Worldcom and Lehman brothers and lessons derived by

accounting professional from such collapses:.................................................................................6

Conclusion:......................................................................................................................................8

References list:...............................................................................................................................10

AUDIT AND ASSURANCE SERVICES

Table of Contents

Introduction:....................................................................................................................................2

Discussion:.......................................................................................................................................2

Auditor independence and audit risks:............................................................................................2

Situations leading to creation of threat to auditor’s independence:.................................................4

Reviewing the literature of Enron, Worldcom and Lehman brothers and lessons derived by

accounting professional from such collapses:.................................................................................6

Conclusion:......................................................................................................................................8

References list:...............................................................................................................................10

2

AUDIT AND ASSURANCE SERVICES

Introduction:

The report is prepared to analyze the literature review on key audit risks and threats to

auditor’s independence lying. It deals with further discussion on the factors that exactly

undermines the independence of auditors. Moreover, analysis of literature review on the cases of

Enron, Worldcom and Lehman Bros has been done for generating information’s on the lessons

that have been learnt. Independence is considered as critical issue in the auditor’s profession as it

has considerable impact n audit quality. There is a possibility of auditors impairing audit quality

if they are not independent as they are less likely to report irregularities. Establishment of

relationship between independence and risk helps in identification of where the key audit risks

and threat to their independence lies. Audit activity is considered as holistic activity where the

independence in fact, issues of competence and audit risks are linked inextricably (Appelbaum &

Vasarhelyi, 2017). Quality of audit is determined by auditor’s independence and it is regarded as

one of the fundamental causes of many corporate failures and leading to their collapse and

triggering global economic meltdown of the middle 2000.

Discussion:

Auditor independence and audit risks:

Independence is one of the most crucial attributes and it is measured by the honesty of

auditors in measuring material misstatements in the financial statements of any organizations.

Several factors are responsible for undermining the independence of auditors and independence

can be impaired depending upon circumstances. The possibility of being perceived as not being

objective increases by lack of independence of auditors (Arens et al., 2016). Auditor’s impaired

evidence results in poor quality of audit and allows for greater earning quality and greater

earning management.

AUDIT AND ASSURANCE SERVICES

Introduction:

The report is prepared to analyze the literature review on key audit risks and threats to

auditor’s independence lying. It deals with further discussion on the factors that exactly

undermines the independence of auditors. Moreover, analysis of literature review on the cases of

Enron, Worldcom and Lehman Bros has been done for generating information’s on the lessons

that have been learnt. Independence is considered as critical issue in the auditor’s profession as it

has considerable impact n audit quality. There is a possibility of auditors impairing audit quality

if they are not independent as they are less likely to report irregularities. Establishment of

relationship between independence and risk helps in identification of where the key audit risks

and threat to their independence lies. Audit activity is considered as holistic activity where the

independence in fact, issues of competence and audit risks are linked inextricably (Appelbaum &

Vasarhelyi, 2017). Quality of audit is determined by auditor’s independence and it is regarded as

one of the fundamental causes of many corporate failures and leading to their collapse and

triggering global economic meltdown of the middle 2000.

Discussion:

Auditor independence and audit risks:

Independence is one of the most crucial attributes and it is measured by the honesty of

auditors in measuring material misstatements in the financial statements of any organizations.

Several factors are responsible for undermining the independence of auditors and independence

can be impaired depending upon circumstances. The possibility of being perceived as not being

objective increases by lack of independence of auditors (Arens et al., 2016). Auditor’s impaired

evidence results in poor quality of audit and allows for greater earning quality and greater

earning management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDIT AND ASSURANCE SERVICES

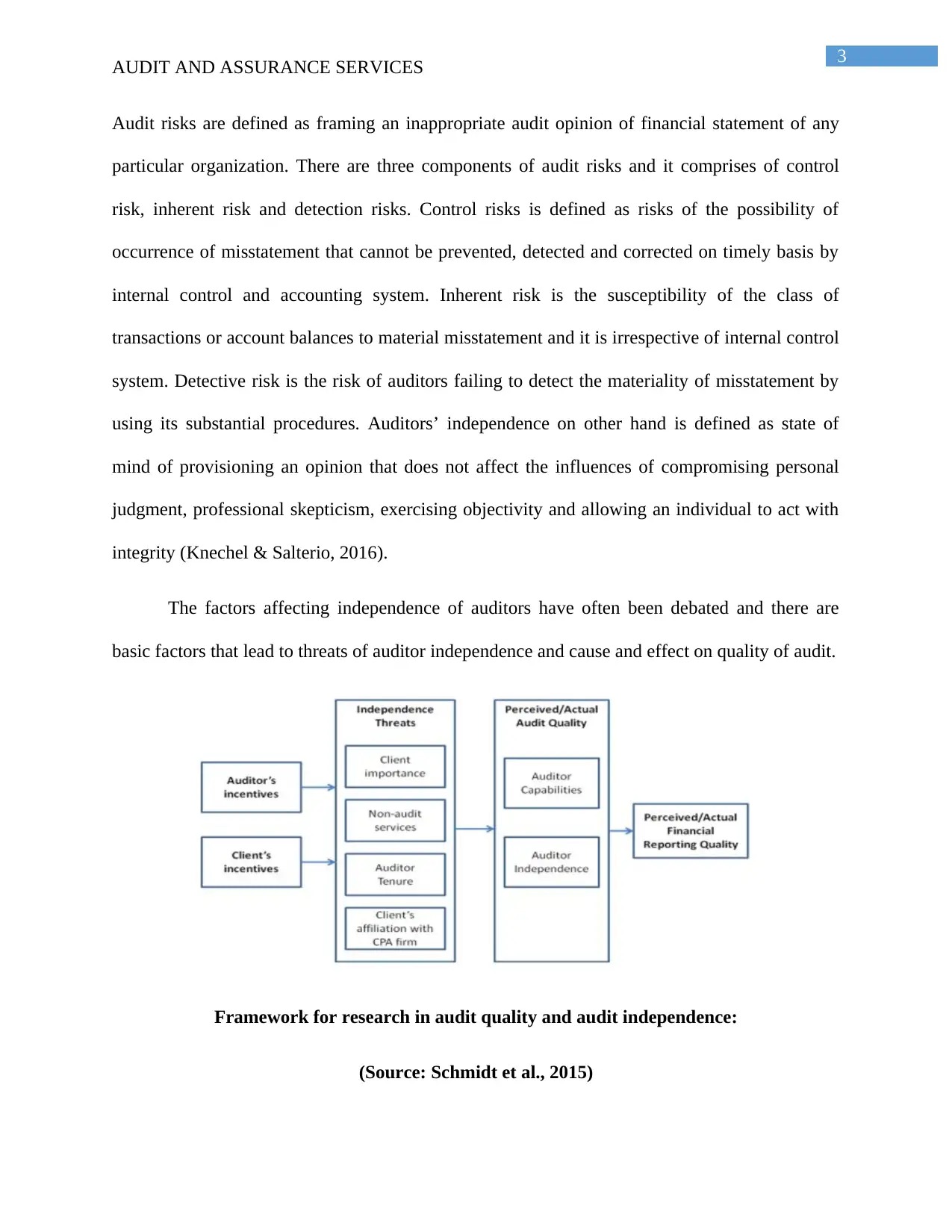

Audit risks are defined as framing an inappropriate audit opinion of financial statement of any

particular organization. There are three components of audit risks and it comprises of control

risk, inherent risk and detection risks. Control risks is defined as risks of the possibility of

occurrence of misstatement that cannot be prevented, detected and corrected on timely basis by

internal control and accounting system. Inherent risk is the susceptibility of the class of

transactions or account balances to material misstatement and it is irrespective of internal control

system. Detective risk is the risk of auditors failing to detect the materiality of misstatement by

using its substantial procedures. Auditors’ independence on other hand is defined as state of

mind of provisioning an opinion that does not affect the influences of compromising personal

judgment, professional skepticism, exercising objectivity and allowing an individual to act with

integrity (Knechel & Salterio, 2016).

The factors affecting independence of auditors have often been debated and there are

basic factors that lead to threats of auditor independence and cause and effect on quality of audit.

Framework for research in audit quality and audit independence:

(Source: Schmidt et al., 2015)

AUDIT AND ASSURANCE SERVICES

Audit risks are defined as framing an inappropriate audit opinion of financial statement of any

particular organization. There are three components of audit risks and it comprises of control

risk, inherent risk and detection risks. Control risks is defined as risks of the possibility of

occurrence of misstatement that cannot be prevented, detected and corrected on timely basis by

internal control and accounting system. Inherent risk is the susceptibility of the class of

transactions or account balances to material misstatement and it is irrespective of internal control

system. Detective risk is the risk of auditors failing to detect the materiality of misstatement by

using its substantial procedures. Auditors’ independence on other hand is defined as state of

mind of provisioning an opinion that does not affect the influences of compromising personal

judgment, professional skepticism, exercising objectivity and allowing an individual to act with

integrity (Knechel & Salterio, 2016).

The factors affecting independence of auditors have often been debated and there are

basic factors that lead to threats of auditor independence and cause and effect on quality of audit.

Framework for research in audit quality and audit independence:

(Source: Schmidt et al., 2015)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDIT AND ASSURANCE SERVICES

Main threat to independence of auditors arise from auditor client relationships as clients

and auditors in different level and in different firms have diverse incentives resulting in different

perceptions and its impact on auditor independence. The quality of audit is likely to be impacted

considerably by threats such as non-audit services, auditor tenure, client importance and

affiliation of client with firm (Byrnes et al,. 2014). However, it is difficult to determine the

threats of quality of audit on their influences on dependence. Normally, the independence of

auditors are reduced by threats and the net effect between independence and auditors capabilities

helps in determining the impact of independent threat on audit quality.

Auditor tenure may also lead to impairment of auditor independence as auditors tent to

develop close relationship with clients if the auditor client relationships lengthens and they are

more likely to act in favor of management and thereby reducing audit quality and objectivity

(Ahmed & Anifowose, 2015). In some of recent corporate scandals that occurred simultaneously

involved auditors and the lack of auditors, independence was attributable to occurrence of such

scandals. There are certain situations that results in creation of threat to auditor’s independence

as deduced by reviewing literature.

Situations leading to creation of threat to auditor’s independence:

Threats’ arising from self interest- It is a type of threat that incorporates self-interest or

any other financial conflicts and including a direct and indirect financial interest, motivation of

retaining the client and dependence on non-audit and client fees. Auditor’s independence could

be impaired by auditor fee dependence. They would try to retain their clients in order to secure

future revenues. Intuitively, auditors will be depending upon clients to a greater degree if they

generate higher revenue. In order to retain the clients, auditors will be hesitating in taking actions

AUDIT AND ASSURANCE SERVICES

Main threat to independence of auditors arise from auditor client relationships as clients

and auditors in different level and in different firms have diverse incentives resulting in different

perceptions and its impact on auditor independence. The quality of audit is likely to be impacted

considerably by threats such as non-audit services, auditor tenure, client importance and

affiliation of client with firm (Byrnes et al,. 2014). However, it is difficult to determine the

threats of quality of audit on their influences on dependence. Normally, the independence of

auditors are reduced by threats and the net effect between independence and auditors capabilities

helps in determining the impact of independent threat on audit quality.

Auditor tenure may also lead to impairment of auditor independence as auditors tent to

develop close relationship with clients if the auditor client relationships lengthens and they are

more likely to act in favor of management and thereby reducing audit quality and objectivity

(Ahmed & Anifowose, 2015). In some of recent corporate scandals that occurred simultaneously

involved auditors and the lack of auditors, independence was attributable to occurrence of such

scandals. There are certain situations that results in creation of threat to auditor’s independence

as deduced by reviewing literature.

Situations leading to creation of threat to auditor’s independence:

Threats’ arising from self interest- It is a type of threat that incorporates self-interest or

any other financial conflicts and including a direct and indirect financial interest, motivation of

retaining the client and dependence on non-audit and client fees. Auditor’s independence could

be impaired by auditor fee dependence. They would try to retain their clients in order to secure

future revenues. Intuitively, auditors will be depending upon clients to a greater degree if they

generate higher revenue. In order to retain the clients, auditors will be hesitating in taking actions

5

AUDIT AND ASSURANCE SERVICES

that would have any adverse impact on them. It has been argued that auditor independence will

decrease by a greater share between auditors and their clients.

Familiarity and advocacy threat arises from audit tenure and long-term consecutive

assignments with the same clients. The longer auditors conduct auditing for the same clients,

there will be more impairment of auditor independence. Long tenure lead to impairment of

auditors independence due to auditors experiencing a belief perseverance syndrome that lead to

failure of auditors in revising the appropriateness of assertion of management even though there

has been change in conditions and facts (Leung et al., 2014).

Furthermore, auditors might be deterred to exercise their professional skepticism and act

independently due to threat that are caused by intimidation and that arises on management part.

Threat of replacement is one of the common types of intimidation threat. Due to imbalance of

power and asymmetrical relationship between auditors and their clients, auditors are considered

in weak position. In a conflict situation, auditors are vulnerable to intimidation by clients in the

events when there occurs disagreements between auditors and clients over accounting issues

such as appropriateness of accounting principles applied by clients, any sort of adjustments in the

financial statements and inadequacy of disclosure of financial statements (Caya, 2016).

In association of above discussed points, various other factors can lead to impairment of

independence of auditors. One of such point is social pressures that can be exerted by any

individual within authority in a hierarchical context such as upper level of management.

Conformity pressure and obedience pressure are the two types of social pressures. Conformity

pressure is a pressure that is exerted by colleague or peers and upper management in an

organization exerts obedience pressure. These two pressures can impair Independence of audit

when the independent principle is contracted by suggestions or command of auditor’s colleagues

AUDIT AND ASSURANCE SERVICES

that would have any adverse impact on them. It has been argued that auditor independence will

decrease by a greater share between auditors and their clients.

Familiarity and advocacy threat arises from audit tenure and long-term consecutive

assignments with the same clients. The longer auditors conduct auditing for the same clients,

there will be more impairment of auditor independence. Long tenure lead to impairment of

auditors independence due to auditors experiencing a belief perseverance syndrome that lead to

failure of auditors in revising the appropriateness of assertion of management even though there

has been change in conditions and facts (Leung et al., 2014).

Furthermore, auditors might be deterred to exercise their professional skepticism and act

independently due to threat that are caused by intimidation and that arises on management part.

Threat of replacement is one of the common types of intimidation threat. Due to imbalance of

power and asymmetrical relationship between auditors and their clients, auditors are considered

in weak position. In a conflict situation, auditors are vulnerable to intimidation by clients in the

events when there occurs disagreements between auditors and clients over accounting issues

such as appropriateness of accounting principles applied by clients, any sort of adjustments in the

financial statements and inadequacy of disclosure of financial statements (Caya, 2016).

In association of above discussed points, various other factors can lead to impairment of

independence of auditors. One of such point is social pressures that can be exerted by any

individual within authority in a hierarchical context such as upper level of management.

Conformity pressure and obedience pressure are the two types of social pressures. Conformity

pressure is a pressure that is exerted by colleague or peers and upper management in an

organization exerts obedience pressure. These two pressures can impair Independence of audit

when the independent principle is contracted by suggestions or command of auditor’s colleagues

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDIT AND ASSURANCE SERVICES

or superior. Recognition of audit risk existence is incorporated in the description of functions and

responsibilities of independent auditors (Knechel & Salterio, 2016). Therefore, it can be seen that

there are various factors that poses threat to auditor’s independence

Reviewing the literature of Enron, Worldcom and Lehman brothers and lessons derived by

accounting professional from such collapses:

Enron Corporation being the seventh largest company in United States misguided its

shareholders by engaging them in fraud and reported its profit unfaithfully. Organization

manipulated its financial statements along with financial strategy when they started facing

financing difficulties. Collapse of Enron was preceded by three major violations of the principles

of GAAP. Another accounting fraud principle is attributable to mark to market method that

helped in pumping up the stock prices for gaining capital investments that was regarded as

immoral and illegal. Derivative manipulation was another violation that helped in concealing

derivative loss from investors (Messier et al., 2015). Several potentially fraudulent acts and

unusual transactions were discovered and investigated by the auditor of Enron. Financial

outcomes that was attributable to this organization resulting from poor accounting policies for

recognition of revenue, lack of financial policies and improper segregation accounting duties

(William et al., 2016). It has been ascertained after the failure of Enron that there has been

increase in compliance costs with the internal costing systems with the largest accounting firms

have increased over time.

Lehman brother failure was one of the largest bankruptcies in United States. Business

model used by this bank was mainly to rely on short-term loans and assets was predominantly

long-term when they were largely large short-terms. Factors that accounted for the failure of the

organization was poor choice of management accompanies with some unethical practices.

AUDIT AND ASSURANCE SERVICES

or superior. Recognition of audit risk existence is incorporated in the description of functions and

responsibilities of independent auditors (Knechel & Salterio, 2016). Therefore, it can be seen that

there are various factors that poses threat to auditor’s independence

Reviewing the literature of Enron, Worldcom and Lehman brothers and lessons derived by

accounting professional from such collapses:

Enron Corporation being the seventh largest company in United States misguided its

shareholders by engaging them in fraud and reported its profit unfaithfully. Organization

manipulated its financial statements along with financial strategy when they started facing

financing difficulties. Collapse of Enron was preceded by three major violations of the principles

of GAAP. Another accounting fraud principle is attributable to mark to market method that

helped in pumping up the stock prices for gaining capital investments that was regarded as

immoral and illegal. Derivative manipulation was another violation that helped in concealing

derivative loss from investors (Messier et al., 2015). Several potentially fraudulent acts and

unusual transactions were discovered and investigated by the auditor of Enron. Financial

outcomes that was attributable to this organization resulting from poor accounting policies for

recognition of revenue, lack of financial policies and improper segregation accounting duties

(William et al., 2016). It has been ascertained after the failure of Enron that there has been

increase in compliance costs with the internal costing systems with the largest accounting firms

have increased over time.

Lehman brother failure was one of the largest bankruptcies in United States. Business

model used by this bank was mainly to rely on short-term loans and assets was predominantly

long-term when they were largely large short-terms. Factors that accounted for the failure of the

organization was poor choice of management accompanies with some unethical practices.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDIT AND ASSURANCE SERVICES

Liquidity crisis, financial leverage, complex capital structure, subprime mortgage crisis and

massive credit default swaps. Adversity in several organizations is reported by the collapse of

Lehman brothers as the failure led to depreciation in price of commercial real estates and

extinguishing billions of market value and market for trade receivables (Byrnes et al., 2015).

Collapse of failure of Lehman brothers was unthinkable and the lessons that were learned

from such failure are attributable to high hazard industries and preventing of such financial

accidents by adopting an equivalent approach for managing and understating risks in culture of

organization and control of management. Management of company was attributable to the failure

as they were involved in manipulating financial documents and financial transactions leading to

its ultimate collapse (Parwada et al., 2015).

Worldcom was engaged in accounting scandal and rapid erosion of profits that created

illusionary earnings. The accounting practices of organization were questionable and internal

auditors have uncovered an additional of $ 3.831 billion due to improper accounting (Knechel,

2016). Detecting errors is an easy task for auditors and sophisticated fraud involves earning

management that it can covert. Management requirement for asserting that accounts have been

prepared properly does not provide for any protections from entering into any fraud and deceits.

Auditors need to make the identification of presence of intention and it was found in the case of

Worldcom that there were changes in financial metrics due to accounting manipulations.

Operating margin was not regarded as satisfactory and for making earning stable; Worldcom was

engaged in accounting manipulations. The purpose of obtaining desired earnings in light of

accounting manipulations was mainly to boost up the stock price of company. Auditors miss this

elementary fraud conducted by Worldcom that ultimately led its failure (Duncan & Whittington,

2014).

AUDIT AND ASSURANCE SERVICES

Liquidity crisis, financial leverage, complex capital structure, subprime mortgage crisis and

massive credit default swaps. Adversity in several organizations is reported by the collapse of

Lehman brothers as the failure led to depreciation in price of commercial real estates and

extinguishing billions of market value and market for trade receivables (Byrnes et al., 2015).

Collapse of failure of Lehman brothers was unthinkable and the lessons that were learned

from such failure are attributable to high hazard industries and preventing of such financial

accidents by adopting an equivalent approach for managing and understating risks in culture of

organization and control of management. Management of company was attributable to the failure

as they were involved in manipulating financial documents and financial transactions leading to

its ultimate collapse (Parwada et al., 2015).

Worldcom was engaged in accounting scandal and rapid erosion of profits that created

illusionary earnings. The accounting practices of organization were questionable and internal

auditors have uncovered an additional of $ 3.831 billion due to improper accounting (Knechel,

2016). Detecting errors is an easy task for auditors and sophisticated fraud involves earning

management that it can covert. Management requirement for asserting that accounts have been

prepared properly does not provide for any protections from entering into any fraud and deceits.

Auditors need to make the identification of presence of intention and it was found in the case of

Worldcom that there were changes in financial metrics due to accounting manipulations.

Operating margin was not regarded as satisfactory and for making earning stable; Worldcom was

engaged in accounting manipulations. The purpose of obtaining desired earnings in light of

accounting manipulations was mainly to boost up the stock price of company. Auditors miss this

elementary fraud conducted by Worldcom that ultimately led its failure (Duncan & Whittington,

2014).

8

AUDIT AND ASSURANCE SERVICES

Failure of such business have affected large spectrum of business globally and such

collapse can be prevented by taking pro-active actions by management in spite of taking any

reactive measures. After the crisis, it becomes difficult for management to identify any right

solutions to curtail after effect of such crisis.

All the collapse of above-mentioned organization was attributable to their financial

failure due to manipulation of financial activities and engaging in the financial activities. This

has led to deterioration in quality of profits reported by company and the standards that have

been applicable to companies. Management of organizations should prevent engagement in

shoddy auditing; misleading accounts and appropriate measures should be taken to outright

frauds (Sirois et al., 2016). All such scandals entail organization to make their corporate

governance more stringent and taking adhering to all the principles of accounting standard

without violating them. From auditors perspective, it can be seen that failure of auditors to

conduct proper verification of all the related accounts and disclosing the same to public led to

fall of such organization and loss of investors money (Chambers & Odar, 2015). Therefore, they

should try to investigate into any sort of accounts that are misleading investors by providing

irrelevant financial information.

Conclusion:

From the analysis, it can be inferred that the threat of auditor’s independence arises from

multiple factors ranging from internal to external. Auditors are faced with several risks while

conducting audits and the failure of them to identify such risks would pose a threat to their

independence. Moreover, organization should operated and engage within the confines of

business jurisdiction and auditors should keep a blank eye on illegal and unethical activities of

organizations. For analyzing the liquidity issue of company, auditors should place careful

AUDIT AND ASSURANCE SERVICES

Failure of such business have affected large spectrum of business globally and such

collapse can be prevented by taking pro-active actions by management in spite of taking any

reactive measures. After the crisis, it becomes difficult for management to identify any right

solutions to curtail after effect of such crisis.

All the collapse of above-mentioned organization was attributable to their financial

failure due to manipulation of financial activities and engaging in the financial activities. This

has led to deterioration in quality of profits reported by company and the standards that have

been applicable to companies. Management of organizations should prevent engagement in

shoddy auditing; misleading accounts and appropriate measures should be taken to outright

frauds (Sirois et al., 2016). All such scandals entail organization to make their corporate

governance more stringent and taking adhering to all the principles of accounting standard

without violating them. From auditors perspective, it can be seen that failure of auditors to

conduct proper verification of all the related accounts and disclosing the same to public led to

fall of such organization and loss of investors money (Chambers & Odar, 2015). Therefore, they

should try to investigate into any sort of accounts that are misleading investors by providing

irrelevant financial information.

Conclusion:

From the analysis, it can be inferred that the threat of auditor’s independence arises from

multiple factors ranging from internal to external. Auditors are faced with several risks while

conducting audits and the failure of them to identify such risks would pose a threat to their

independence. Moreover, organization should operated and engage within the confines of

business jurisdiction and auditors should keep a blank eye on illegal and unethical activities of

organizations. For analyzing the liquidity issue of company, auditors should place careful

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDIT AND ASSURANCE SERVICES

consideration of indicators of cash flow that will help in preventing such problems. Stringent

policies must be initiated by different regulatory standards for addressing the failure to avert

occurrence of such financial collapses. Organizations are also required to adhere to practices of

good corporate governances. For auditors to discover such fraudulent activities, it is essential to

detect the main indicators of occurrence of such frauds. For avoiding the collapse of such firms,

it must be ensured by business international communities that ethical culture and high standards

should be held by businesses.

AUDIT AND ASSURANCE SERVICES

consideration of indicators of cash flow that will help in preventing such problems. Stringent

policies must be initiated by different regulatory standards for addressing the failure to avert

occurrence of such financial collapses. Organizations are also required to adhere to practices of

good corporate governances. For auditors to discover such fraudulent activities, it is essential to

detect the main indicators of occurrence of such frauds. For avoiding the collapse of such firms,

it must be ensured by business international communities that ethical culture and high standards

should be held by businesses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDIT AND ASSURANCE SERVICES

References list:

Ahmed Haji, A., & Anifowose, M. (2016). Audit committee and integrated reporting practice:

does internal assurance matter?. Managerial Auditing Journal, 31(8/9), 915-948.

Appelbaum, D., Kogan, A., & Vasarhelyi, M. A. (2017). Big Data and analytics in the modern

audit engagement: Research needs. Auditing: A Journal of Practice & Theory, 36(4), 1-

27.

Arens, A. A., Elder, R. J., Beasley, M. S., & Hogan, C. E. (2016). Auditing and assurance

services. Pearson.

Azibi, J., Azibi, H., & Tondeur, H. (2017). Institutional Activism, Auditor’s Choice and Earning

Management after the Enron Collapse: Evidence from France. International Business

Research, 10(2), 154.

Byrnes, P. E., Al-Awadhi, C. A., Gullvist, B., Brown-Liburd, H., Teeter, C. R., Warren Jr, J. D.,

& Vasarhelyi, M. (2015). Evolution of auditing: From the traditional approach to the

future audit. Audit Analytics, 71.

Caya, E. (2016). Make the most of assurance: assurance maps can enable internal audit to team

with other assurance providers to visually convey how risk is managed. Internal Auditor,

73(4), 21-23

Chambers, A. D., & Odar, M. (2015). A new vision for internal audit. Managerial Auditing

Journal, 30(1), 34-55.

AUDIT AND ASSURANCE SERVICES

References list:

Ahmed Haji, A., & Anifowose, M. (2016). Audit committee and integrated reporting practice:

does internal assurance matter?. Managerial Auditing Journal, 31(8/9), 915-948.

Appelbaum, D., Kogan, A., & Vasarhelyi, M. A. (2017). Big Data and analytics in the modern

audit engagement: Research needs. Auditing: A Journal of Practice & Theory, 36(4), 1-

27.

Arens, A. A., Elder, R. J., Beasley, M. S., & Hogan, C. E. (2016). Auditing and assurance

services. Pearson.

Azibi, J., Azibi, H., & Tondeur, H. (2017). Institutional Activism, Auditor’s Choice and Earning

Management after the Enron Collapse: Evidence from France. International Business

Research, 10(2), 154.

Byrnes, P. E., Al-Awadhi, C. A., Gullvist, B., Brown-Liburd, H., Teeter, C. R., Warren Jr, J. D.,

& Vasarhelyi, M. (2015). Evolution of auditing: From the traditional approach to the

future audit. Audit Analytics, 71.

Caya, E. (2016). Make the most of assurance: assurance maps can enable internal audit to team

with other assurance providers to visually convey how risk is managed. Internal Auditor,

73(4), 21-23

Chambers, A. D., & Odar, M. (2015). A new vision for internal audit. Managerial Auditing

Journal, 30(1), 34-55.

11

AUDIT AND ASSURANCE SERVICES

Duncan, B., & Whittington, M. (2014, September). Compliance with standards, assurance and

audit: does this equal security?. In Proceedings of the 7th International Conference on

Security of Information and Networks (p. 77). ACM.

Knechel, W. R. (2016). Audit quality and regulation. International Journal of Auditing, 20(3),

215-223.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Taylor & Francis.

Leung, P., Coram, P., Cooper, B. J., & Richardson, P. (2014). Modern Auditing and Assurance

Services 6e. Wiley.

Messier, W. F., Glover, S. M., & Prawitt, D. F. (2015). Auditing & Assurance Services: A

Systematic Approach. Qing hua da xue chu ban she.

Parwada, J. T., Shen, J., Siaw, K., & Tan, E. K. (2015). The Value of Institutional Brokerage

Relationships: Evidence From The Collapse of Lehman Brothers.

Schmidt, P., Steele, A. J., & Grabski, S. V. (2015). Cloud Computing: Governance and Audit

Research Questions. Washburn University School of Business.

Sirois, L. P., Marmousez, S., & Simunic, D. A. (2016). Auditor size and audit quality revisited:

The importance of audit technology. Comptabilité-Contrôle-Audit, 22(3), 111-144.

Waldron, M. (2016). The Future of Audit. CFA Institute Magazine, 27(3), 55-55.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

AUDIT AND ASSURANCE SERVICES

Duncan, B., & Whittington, M. (2014, September). Compliance with standards, assurance and

audit: does this equal security?. In Proceedings of the 7th International Conference on

Security of Information and Networks (p. 77). ACM.

Knechel, W. R. (2016). Audit quality and regulation. International Journal of Auditing, 20(3),

215-223.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Taylor & Francis.

Leung, P., Coram, P., Cooper, B. J., & Richardson, P. (2014). Modern Auditing and Assurance

Services 6e. Wiley.

Messier, W. F., Glover, S. M., & Prawitt, D. F. (2015). Auditing & Assurance Services: A

Systematic Approach. Qing hua da xue chu ban she.

Parwada, J. T., Shen, J., Siaw, K., & Tan, E. K. (2015). The Value of Institutional Brokerage

Relationships: Evidence From The Collapse of Lehman Brothers.

Schmidt, P., Steele, A. J., & Grabski, S. V. (2015). Cloud Computing: Governance and Audit

Research Questions. Washburn University School of Business.

Sirois, L. P., Marmousez, S., & Simunic, D. A. (2016). Auditor size and audit quality revisited:

The importance of audit technology. Comptabilité-Contrôle-Audit, 22(3), 111-144.

Waldron, M. (2016). The Future of Audit. CFA Institute Magazine, 27(3), 55-55.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.