Auditing Failures and Corporate Collapse: Harris Scarfe Case Study

VerifiedAdded on 2023/06/03

|12

|3800

|216

Essay

AI Summary

This essay examines the factors that contributed to the collapse of Harris Scarfe, a major Australian retailer, focusing on the critical auditing issues that led to its downfall. The analysis covers three primary audit issues: auditor independence, ethical considerations, and the composition and roles of the audit committee. The essay explores how a lack of auditor independence, ethical breaches, and a deficient audit committee structure undermined the company's financial reporting and governance. Furthermore, the essay discusses the relevance of developments following the Harris Scarfe collapse, such as the Corporate Law Economic Reform Program (CLERP 9), to the role of Australian auditors. A reflective essay component explores the essential attributes of a qualified auditor, drawing on the Harris Scarfe case to highlight the importance of statutory, professional, and personal qualities. It emphasizes the need for auditors to possess strong ethical standards, technical competence, and the ability to act independently to prevent future corporate failures, supported by academic research and real-world examples. The essay underscores the importance of robust auditing practices and effective corporate governance in safeguarding financial stability.

Auditing 1

Factors which can cause the Collapse of Corporate Organisations: Case of Harris Scarfe

By (Name)

Professor`s Name

Institution`s Name

Location of the Institution

Date

Factors which can cause the Collapse of Corporate Organisations: Case of Harris Scarfe

By (Name)

Professor`s Name

Institution`s Name

Location of the Institution

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 2

Factors which can cause the Collapse of Corporate Organisations: Case of Harris Scarfe

Assessment 2: Individual Essay, Part One

The Auditing Issues

Auditing is a vital activity in a company setup and if not done properly, a company

can suffer major financial losses and even collapses like the Harris Scarfe in Australia which

was shut down in 2000 (Sookhak et al. 2014). Harris Scarfe collapsed due to poor

management, poor internal control and poor auditing and accounting activities. The internal

auditors were not independent, and their decision was being influenced by some of the

management members (Jostern 15th May 2013)). An example is when the Harris Scarfe

accountant, Mr. Wight alleged that he was told to make false accounting reports by Hodgson

who was one of the Harris Scarfe management members. The collapse of Harris Scarfe has

brought the discussion about the role of auditors in a company growth (Clayfield 16th August

2011). Therefore, the paper has looked at three audit issues that led to the closure of Harris

Scarfe one of the biggest companies in South Australia. The issues to be discussed are

auditing ethics, independence of auditors, and the composition and the roles of audit

committee.

Independence

According to Hashem et al. (2015 p. 98), the auditor independence is where both the

external and the internal auditors are allowed to perform their duties without interference

from the company management they are working for or any other party of interest.

Independence of auditor is an issue that cannot be ignored by any business interested person.

Rasheed (2014 p. 367) states that if the auditor’s reports are influenced by other people then

those reports are not accurate and can lead the company in path of collapsing. It is the

responsibility of the auditors to ensure that they are not influence by the interested people

who may be harmed by the audit reports. Harris Scarfe suffered financial losses because

Factors which can cause the Collapse of Corporate Organisations: Case of Harris Scarfe

Assessment 2: Individual Essay, Part One

The Auditing Issues

Auditing is a vital activity in a company setup and if not done properly, a company

can suffer major financial losses and even collapses like the Harris Scarfe in Australia which

was shut down in 2000 (Sookhak et al. 2014). Harris Scarfe collapsed due to poor

management, poor internal control and poor auditing and accounting activities. The internal

auditors were not independent, and their decision was being influenced by some of the

management members (Jostern 15th May 2013)). An example is when the Harris Scarfe

accountant, Mr. Wight alleged that he was told to make false accounting reports by Hodgson

who was one of the Harris Scarfe management members. The collapse of Harris Scarfe has

brought the discussion about the role of auditors in a company growth (Clayfield 16th August

2011). Therefore, the paper has looked at three audit issues that led to the closure of Harris

Scarfe one of the biggest companies in South Australia. The issues to be discussed are

auditing ethics, independence of auditors, and the composition and the roles of audit

committee.

Independence

According to Hashem et al. (2015 p. 98), the auditor independence is where both the

external and the internal auditors are allowed to perform their duties without interference

from the company management they are working for or any other party of interest.

Independence of auditor is an issue that cannot be ignored by any business interested person.

Rasheed (2014 p. 367) states that if the auditor’s reports are influenced by other people then

those reports are not accurate and can lead the company in path of collapsing. It is the

responsibility of the auditors to ensure that they are not influence by the interested people

who may be harmed by the audit reports. Harris Scarfe suffered financial losses because

Auditing 3

some of the management did not allow the auditors to perform their work independently

(Kavrar and Yılmaz January 2017). A good case is where Mr. Wight testified that he was

compelled by Mr. Hodgson who was one of the Harris Scarfe management to prepare false

auditing reports for that company`s financial year. The work of the auditors is to act as

oversight and report any suspicion of mismanagement of funds and this cannot be done if

they are not independent (Sookhak et al. 2014). Therefore, to prevent collapse of companies

to today`s market, the management should not interfere with the auditors` work.

Auditing Ethics

Every department in an institution must run in accordance with the code of ethics that

have been dictated by the institution in question and the state in which that organisation is

based. In that manner auditing processes must also be done in compliance with the code of

ethics in auditing profession (Sookhak et al. 2015). One of the ethics is independence which

has been discussed as the first issue in the part above. Other ethical codes that auditors should

follow as prescribed in the Australian law include competency, integrity, objectivity and

confidentiality (Griffin and Wright 2015). Competency requires the auditors to take part in

auditing activities that they are knowledgeable on, they should not take part in auditing

activities that they do not know. Integrity requires the auditors to perform their work based on

trust, and write their recommendation based on their judgment not influence form other

people (Fernie and Sparks 2014 p. 10). Objectivity requires the auditors to conduct their

activities in an objective manner and assess the reports without the influence form the

interested parties in the audit process. And lastly, confidentiality requires auditors to only

show the contents of the auditing report to the relevant people and not every person who want

to see the report (Sookhak et al. 2015). Auditors from Harris Scarfe did not follow the code

of ethics and that is one of the reasons why the company collapsed. Wight could have not

some of the management did not allow the auditors to perform their work independently

(Kavrar and Yılmaz January 2017). A good case is where Mr. Wight testified that he was

compelled by Mr. Hodgson who was one of the Harris Scarfe management to prepare false

auditing reports for that company`s financial year. The work of the auditors is to act as

oversight and report any suspicion of mismanagement of funds and this cannot be done if

they are not independent (Sookhak et al. 2014). Therefore, to prevent collapse of companies

to today`s market, the management should not interfere with the auditors` work.

Auditing Ethics

Every department in an institution must run in accordance with the code of ethics that

have been dictated by the institution in question and the state in which that organisation is

based. In that manner auditing processes must also be done in compliance with the code of

ethics in auditing profession (Sookhak et al. 2015). One of the ethics is independence which

has been discussed as the first issue in the part above. Other ethical codes that auditors should

follow as prescribed in the Australian law include competency, integrity, objectivity and

confidentiality (Griffin and Wright 2015). Competency requires the auditors to take part in

auditing activities that they are knowledgeable on, they should not take part in auditing

activities that they do not know. Integrity requires the auditors to perform their work based on

trust, and write their recommendation based on their judgment not influence form other

people (Fernie and Sparks 2014 p. 10). Objectivity requires the auditors to conduct their

activities in an objective manner and assess the reports without the influence form the

interested parties in the audit process. And lastly, confidentiality requires auditors to only

show the contents of the auditing report to the relevant people and not every person who want

to see the report (Sookhak et al. 2015). Auditors from Harris Scarfe did not follow the code

of ethics and that is one of the reasons why the company collapsed. Wight could have not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing 4

agreed to be influenced by his boss because ethically, he should not agree to influence by

external forces.

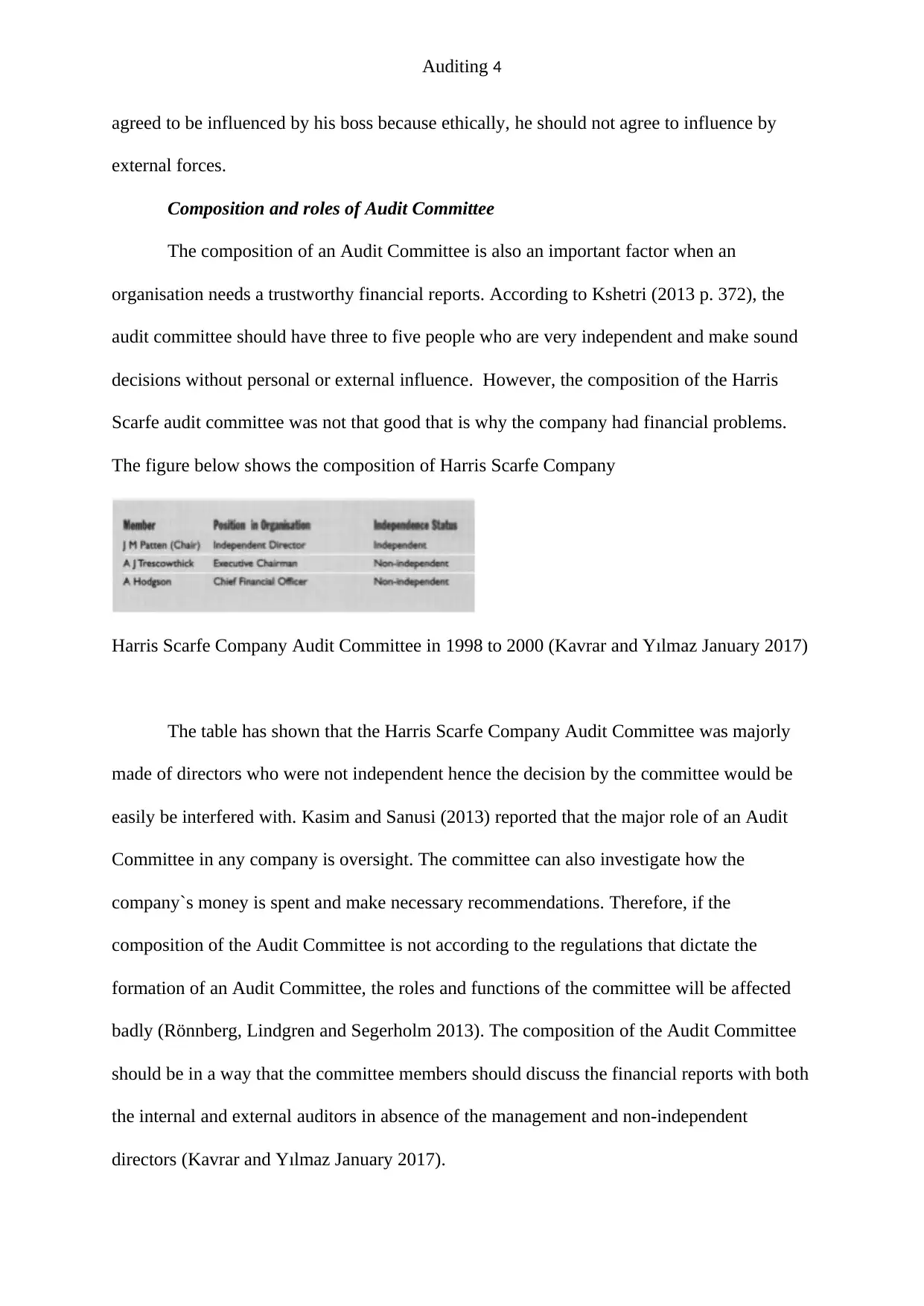

Composition and roles of Audit Committee

The composition of an Audit Committee is also an important factor when an

organisation needs a trustworthy financial reports. According to Kshetri (2013 p. 372), the

audit committee should have three to five people who are very independent and make sound

decisions without personal or external influence. However, the composition of the Harris

Scarfe audit committee was not that good that is why the company had financial problems.

The figure below shows the composition of Harris Scarfe Company

Harris Scarfe Company Audit Committee in 1998 to 2000 (Kavrar and Yılmaz January 2017)

The table has shown that the Harris Scarfe Company Audit Committee was majorly

made of directors who were not independent hence the decision by the committee would be

easily be interfered with. Kasim and Sanusi (2013) reported that the major role of an Audit

Committee in any company is oversight. The committee can also investigate how the

company`s money is spent and make necessary recommendations. Therefore, if the

composition of the Audit Committee is not according to the regulations that dictate the

formation of an Audit Committee, the roles and functions of the committee will be affected

badly (Rönnberg, Lindgren and Segerholm 2013). The composition of the Audit Committee

should be in a way that the committee members should discuss the financial reports with both

the internal and external auditors in absence of the management and non-independent

directors (Kavrar and Yılmaz January 2017).

agreed to be influenced by his boss because ethically, he should not agree to influence by

external forces.

Composition and roles of Audit Committee

The composition of an Audit Committee is also an important factor when an

organisation needs a trustworthy financial reports. According to Kshetri (2013 p. 372), the

audit committee should have three to five people who are very independent and make sound

decisions without personal or external influence. However, the composition of the Harris

Scarfe audit committee was not that good that is why the company had financial problems.

The figure below shows the composition of Harris Scarfe Company

Harris Scarfe Company Audit Committee in 1998 to 2000 (Kavrar and Yılmaz January 2017)

The table has shown that the Harris Scarfe Company Audit Committee was majorly

made of directors who were not independent hence the decision by the committee would be

easily be interfered with. Kasim and Sanusi (2013) reported that the major role of an Audit

Committee in any company is oversight. The committee can also investigate how the

company`s money is spent and make necessary recommendations. Therefore, if the

composition of the Audit Committee is not according to the regulations that dictate the

formation of an Audit Committee, the roles and functions of the committee will be affected

badly (Rönnberg, Lindgren and Segerholm 2013). The composition of the Audit Committee

should be in a way that the committee members should discuss the financial reports with both

the internal and external auditors in absence of the management and non-independent

directors (Kavrar and Yılmaz January 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 5

Part Two

The relevance of Developments following the Collapse of Harris Scarfe

Harris Scarfe was a giant industry in the South Australia, hence its collapse brought

about major developments in accounting and auditing professions (Kavrar and Yılmaz

January 2017). Harris Scarfe was closed with the debt of close to $ 265 million which was a

huge loss for the Australian stoke market hence an investigation was conducted to study the

reasons for the collapse of the company (Fernie and Sparks 2014 p. 10). Other companies

also suffered the same fate in that same period when the Harris Scarfe collapsed and

therefore, the Australian business fraternity came with developments to prevent closure of

other such business entities. The developments included the amendments of Corporate Law

Economic Reform Program so that the problem could be eradicated (Kasim and Sanusi

2013).

The government of Australia responded to the collapse of the companies by giving the

International Accounting Standards the legal baking. Even though these standards were there

before the companies started to collapse, the government did not efficiently backed these

policies and from that experience, the government backed the International Accounting

Standards fully ((Rönnberg, Lindgren and Segerholm 2013). Other reform was that the Audit

Committee of any corporate institution must be involved in the auditing process. In other

words, the Audit Committees, should not just wait for the final reports form the auditors, they

should be part of the auditing process (Sookhak et al. 2015). They should ensure that the

auditors conducting the process are independent, competent, and qualified for the job. The

Audit Committees should also select and arrange the auditors who should conduct the

auditing process according to the law. The analysts’ independence were also mentioned in the

reforms (Griffin and Wright 2015). The analysts should study the report by the auditors and

make recommendations which are fair and true so that the investors should not be

Part Two

The relevance of Developments following the Collapse of Harris Scarfe

Harris Scarfe was a giant industry in the South Australia, hence its collapse brought

about major developments in accounting and auditing professions (Kavrar and Yılmaz

January 2017). Harris Scarfe was closed with the debt of close to $ 265 million which was a

huge loss for the Australian stoke market hence an investigation was conducted to study the

reasons for the collapse of the company (Fernie and Sparks 2014 p. 10). Other companies

also suffered the same fate in that same period when the Harris Scarfe collapsed and

therefore, the Australian business fraternity came with developments to prevent closure of

other such business entities. The developments included the amendments of Corporate Law

Economic Reform Program so that the problem could be eradicated (Kasim and Sanusi

2013).

The government of Australia responded to the collapse of the companies by giving the

International Accounting Standards the legal baking. Even though these standards were there

before the companies started to collapse, the government did not efficiently backed these

policies and from that experience, the government backed the International Accounting

Standards fully ((Rönnberg, Lindgren and Segerholm 2013). Other reform was that the Audit

Committee of any corporate institution must be involved in the auditing process. In other

words, the Audit Committees, should not just wait for the final reports form the auditors, they

should be part of the auditing process (Sookhak et al. 2015). They should ensure that the

auditors conducting the process are independent, competent, and qualified for the job. The

Audit Committees should also select and arrange the auditors who should conduct the

auditing process according to the law. The analysts’ independence were also mentioned in the

reforms (Griffin and Wright 2015). The analysts should study the report by the auditors and

make recommendations which are fair and true so that the investors should not be

Auditing 6

misinformed. The recommendations by analyst is very vital in determining the fate of the

corporate organisation. Therefore, if their analytic work is interfered with, they will cost

investors a lot of money and the public will not know the truth about the company being

analysed (Hashem et al. 2015 p. 98).

Another development that was made was creation of the Corporate Governance

Council in Australia to monitor the way managements are governing their corporate

organisations (Jostern 15th May 2013). It was found out that not only the accountants and

auditors were the cause of corporate collapses, the leaders of the organisations which

collapsed were also to be blamed (Clayfield 16th August 2011). For example there was bad

governance at Harris Scarfe because some of the directors compelled the auditors to record

false financial reports. Therefore, the Corporate Governance Council has the role of

regulation how the leaders of corporate companies should behave (Kavrar and Yılmaz

January 2017).

Conclusion

The collapse of Harris Scarfe and other corporate organisations shaded some light on

the accounting and auditing issues that should be treated with outmost care. The

independence of accountants and auditors should be respected at any cost (Fernie and Sparks

2014 p. 10). The corporate managers should allow their accountants to conduct their activities

in an independent way for an accurate report to come out. The auditors should also know

their code of ethics and comply with them every time they are auditing a firm (Clayfield 16th

August 2011). Lastly to tackle well the accounting and auditing issues, the corporate

management should appoint Audit Committees which are totally independent form others

(Sookhak et al. 2015). The developments that were brought as a result of collapse of the

corporate organisations in 2000s have played a significant role in the corporate growth in

Australia (Kavrar and Yılmaz January 2017).

misinformed. The recommendations by analyst is very vital in determining the fate of the

corporate organisation. Therefore, if their analytic work is interfered with, they will cost

investors a lot of money and the public will not know the truth about the company being

analysed (Hashem et al. 2015 p. 98).

Another development that was made was creation of the Corporate Governance

Council in Australia to monitor the way managements are governing their corporate

organisations (Jostern 15th May 2013). It was found out that not only the accountants and

auditors were the cause of corporate collapses, the leaders of the organisations which

collapsed were also to be blamed (Clayfield 16th August 2011). For example there was bad

governance at Harris Scarfe because some of the directors compelled the auditors to record

false financial reports. Therefore, the Corporate Governance Council has the role of

regulation how the leaders of corporate companies should behave (Kavrar and Yılmaz

January 2017).

Conclusion

The collapse of Harris Scarfe and other corporate organisations shaded some light on

the accounting and auditing issues that should be treated with outmost care. The

independence of accountants and auditors should be respected at any cost (Fernie and Sparks

2014 p. 10). The corporate managers should allow their accountants to conduct their activities

in an independent way for an accurate report to come out. The auditors should also know

their code of ethics and comply with them every time they are auditing a firm (Clayfield 16th

August 2011). Lastly to tackle well the accounting and auditing issues, the corporate

management should appoint Audit Committees which are totally independent form others

(Sookhak et al. 2015). The developments that were brought as a result of collapse of the

corporate organisations in 2000s have played a significant role in the corporate growth in

Australia (Kavrar and Yılmaz January 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing 7

Assessment Three: Reflective Essay

Important Attributes of a Qualified Auditor

Qualified auditors are vital for a progress of any corporate organisation (Christensen

et al. 2016), the auditors who handle the auditing processes of Harris Scarfe and other

corporates that were shut down on that period lacked a lot of qualities and attributes. The

knowledge I have gained in my study that the important attributes of a qualified auditors are

not just learned in class, some are personal. Yeh et al. (2014 p. 98), supported my argument

in their research and argued that there are three types of qualities and attributes of an auditor.

They include, the statutory qualification, professional qualification and general personal

qualities. Huang and Nicol (2013) discussed the statutory qualification as the situation where

the auditor must be a certified member of a chattered Auditing organisation as per the laws of

Australia for example, the Institute of Internal Auditors in Australia. The auditors must also

pass the examinations set by the charted organisation to qualify as a professional accountant

(Kavrar and Yılmaz January 2017).

The professional qualification measures the professionalism of the auditor, it defines

what the auditor should know in order to be considered as a professional auditor (Khlif and

Samaha 2014). One, the auditor must have knowledge of the various laws that govern

businesses and corporations which include the banking acts, Companies act, the contract acts

and the sale of goods acts. Second quality is that the auditor should know almost all the

auditing techniques and should be up to date with the changes and reforms in the auditing

sector (Kavrar and Yılmaz January 2017). Third, the auditor should have vast knowledge of

the auditing principles, its practices and theory of auditing Al-Khaddash, Al Nawas and

Ramadan 2013). Fourth and one of the most important professional attributes is that the

auditor must be educated in computer auditing and have knowledge on auditing software

available in the market (Lim et al. 2016 p. 185). Lastly the auditor should understand the

Assessment Three: Reflective Essay

Important Attributes of a Qualified Auditor

Qualified auditors are vital for a progress of any corporate organisation (Christensen

et al. 2016), the auditors who handle the auditing processes of Harris Scarfe and other

corporates that were shut down on that period lacked a lot of qualities and attributes. The

knowledge I have gained in my study that the important attributes of a qualified auditors are

not just learned in class, some are personal. Yeh et al. (2014 p. 98), supported my argument

in their research and argued that there are three types of qualities and attributes of an auditor.

They include, the statutory qualification, professional qualification and general personal

qualities. Huang and Nicol (2013) discussed the statutory qualification as the situation where

the auditor must be a certified member of a chattered Auditing organisation as per the laws of

Australia for example, the Institute of Internal Auditors in Australia. The auditors must also

pass the examinations set by the charted organisation to qualify as a professional accountant

(Kavrar and Yılmaz January 2017).

The professional qualification measures the professionalism of the auditor, it defines

what the auditor should know in order to be considered as a professional auditor (Khlif and

Samaha 2014). One, the auditor must have knowledge of the various laws that govern

businesses and corporations which include the banking acts, Companies act, the contract acts

and the sale of goods acts. Second quality is that the auditor should know almost all the

auditing techniques and should be up to date with the changes and reforms in the auditing

sector (Kavrar and Yılmaz January 2017). Third, the auditor should have vast knowledge of

the auditing principles, its practices and theory of auditing Al-Khaddash, Al Nawas and

Ramadan 2013). Fourth and one of the most important professional attributes is that the

auditor must be educated in computer auditing and have knowledge on auditing software

available in the market (Lim et al. 2016 p. 185). Lastly the auditor should understand the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 8

economic principles, the commercial laws and should be knowledgeable in mathematics and

statistics.

When I was analysing the journal by Kavrar and Yılmaz (January 2017) about the

collapse of corporate organisations including Harris Scarfe, I learned that the accountants and

auditors in these firms had the attributes that I have mentioned in the paragraph above. The

socking thing is that even though the auditors of Harris Scarfe and other fallen corporations

had both statutory and professional qualities, they still did mistakes which affected their

various corporations a lot. I discovered that most of the auditors lacked the third type of

attribute which are the personal qualities and are not learned in class. Al-Khaddash, Al

Nawas and Ramadan (2013) outlined these qualities as honesty, impartial, cautious and

vigilant, courage, common sense, and ability to investigate and come up with facts. If Mr.

Wight could be honest, he should have not tempered with the auditing reports even if he was

compelled to record false reports. Impartiality is the ability of an auditor to discourage

internal or external influence in his/her judgement (Eshleman and Guo 2013). He or she

should not be bias, rather he should produce a balanced report.

The auditors should always be vigilant and cautious and should always be alert in

working setup and have open eyes (Emeh and Appah 2013 p. 14). If the Harris Scarfe

auditors could be vigilant and cautious, they could have found out that there was a financial

problem and give recommendations on how to fix the problem before the corporation

collapsed. The common sense could have helped the auditors in Harris Scarfe to make good

decisions while working, however, many people do not possess common sense (Al-

Khaddash, Al Nawas and Ramadan 2013). Lastly, the auditors of Harris Scarfe other firms

did not have the investigative attribute. Investigations can help and auditor to come up with a

lot of facts which can help the company grow (Siriwardane et al. 2014 p. 193).

economic principles, the commercial laws and should be knowledgeable in mathematics and

statistics.

When I was analysing the journal by Kavrar and Yılmaz (January 2017) about the

collapse of corporate organisations including Harris Scarfe, I learned that the accountants and

auditors in these firms had the attributes that I have mentioned in the paragraph above. The

socking thing is that even though the auditors of Harris Scarfe and other fallen corporations

had both statutory and professional qualities, they still did mistakes which affected their

various corporations a lot. I discovered that most of the auditors lacked the third type of

attribute which are the personal qualities and are not learned in class. Al-Khaddash, Al

Nawas and Ramadan (2013) outlined these qualities as honesty, impartial, cautious and

vigilant, courage, common sense, and ability to investigate and come up with facts. If Mr.

Wight could be honest, he should have not tempered with the auditing reports even if he was

compelled to record false reports. Impartiality is the ability of an auditor to discourage

internal or external influence in his/her judgement (Eshleman and Guo 2013). He or she

should not be bias, rather he should produce a balanced report.

The auditors should always be vigilant and cautious and should always be alert in

working setup and have open eyes (Emeh and Appah 2013 p. 14). If the Harris Scarfe

auditors could be vigilant and cautious, they could have found out that there was a financial

problem and give recommendations on how to fix the problem before the corporation

collapsed. The common sense could have helped the auditors in Harris Scarfe to make good

decisions while working, however, many people do not possess common sense (Al-

Khaddash, Al Nawas and Ramadan 2013). Lastly, the auditors of Harris Scarfe other firms

did not have the investigative attribute. Investigations can help and auditor to come up with a

lot of facts which can help the company grow (Siriwardane et al. 2014 p. 193).

Auditing 9

How the Knowledge in the Subject will help me in Future

As an aspiring auditor, the knowledge I have gained while studying this subject will

be of help to me in my future career. I have learned many mistakes that auditors make while

working which costs them a great deal. The case of Mr. Wight has taught me that no matter

the pressure, I can never compromise the outcome of the audit report even if the manager has

threatened to sack me. I have learned that there are laws which protect the auditors from

being exploited by their bosses. Therefore, if any boss will threaten me in the future because I

have disagreed with him or her, I will take legal actions against him. I have also learned the

attributes of a qualified auditor which I am going to practice so that I can be perfect. I have

learned that auditing is all about knowing what you are doing and stand by your principles.

The subject has been a big impact in my career life.

Conclusion

Auditors should learn to have all the three types of attributes which are statutory,

professional, and personal qualities so that they can deliver quality work (Kavrar and Yılmaz

January 2017). I have learned that the auditors of Harris Scarfe and other corporation that

collapsed in 2000s lacked the personal qualities of a good auditor and that why they failed

their corporations. I will not make the same mistake in future, I will consider all the qualities

and attributes of a qualified auditors in my line of work. I have also learned that auditing

department is a vital body and must be independent so that it can perform its duties perfectly.

Above all the auditors should work hand in hand with the management and other departments

so that they can get accurate data during auditing (Siriwardane et al. 2014 p. 193). Huang

and Nicol (2013) found out that poor relationship between the accounting and auditing

departments and the other departments the source of false financial reporting. Hence in

future, as an auditor I will ensure that there good relationship between my department and

others within the company and outside.

How the Knowledge in the Subject will help me in Future

As an aspiring auditor, the knowledge I have gained while studying this subject will

be of help to me in my future career. I have learned many mistakes that auditors make while

working which costs them a great deal. The case of Mr. Wight has taught me that no matter

the pressure, I can never compromise the outcome of the audit report even if the manager has

threatened to sack me. I have learned that there are laws which protect the auditors from

being exploited by their bosses. Therefore, if any boss will threaten me in the future because I

have disagreed with him or her, I will take legal actions against him. I have also learned the

attributes of a qualified auditor which I am going to practice so that I can be perfect. I have

learned that auditing is all about knowing what you are doing and stand by your principles.

The subject has been a big impact in my career life.

Conclusion

Auditors should learn to have all the three types of attributes which are statutory,

professional, and personal qualities so that they can deliver quality work (Kavrar and Yılmaz

January 2017). I have learned that the auditors of Harris Scarfe and other corporation that

collapsed in 2000s lacked the personal qualities of a good auditor and that why they failed

their corporations. I will not make the same mistake in future, I will consider all the qualities

and attributes of a qualified auditors in my line of work. I have also learned that auditing

department is a vital body and must be independent so that it can perform its duties perfectly.

Above all the auditors should work hand in hand with the management and other departments

so that they can get accurate data during auditing (Siriwardane et al. 2014 p. 193). Huang

and Nicol (2013) found out that poor relationship between the accounting and auditing

departments and the other departments the source of false financial reporting. Hence in

future, as an auditor I will ensure that there good relationship between my department and

others within the company and outside.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing 10

Bibliography

Al-Khaddash, H., Al Nawas, R. and Ramadan, A. (2013). Factors affecting the quality of

auditing: The case of Jordanian commercial banks. International Journal of Business and

Social Science, 4(11).

Butcher, K., Harrison, G. and Ross, P., 2013. Perceptions of audit service quality and auditor

retention. International Journal of Auditing, 17(1), pp.54-74.

Christensen, B.E., Glover, S.M., Omer, T.C. and Shelley, M.K. (2016). Understanding audit

quality: Insights from audit professionals and investors. Contemporary Accounting Research,

33(4), pp.1648-1684.

Clayfield M. (16th August 2011). The role of Corporate Managers in the Fall of Corporate

organisations. Sydney Morning Herald (SMH), p 29-30.

Emeh, Y. and Appah, E. (2013). Audit committee and timeliness of financial reports:

Empirical evidence from Nigeria. Journal of Economics and sustainable Development, 4(20),

pp.14-25.

Eshleman, J.D. and Guo, P. (2013). Abnormal audit fees and audit quality: The importance of

considering managerial incentives in tests of earnings management. Auditing: A Journal of

Practice & Theory, 33(1), pp.117-138.

Fernie, J. and Sparks, L. (2014). Logistics and retail management: emerging issues and new

challenges in the retail supply chain. Kogan page publishers.

Griffin, P.A. and Wright, A.M. (2015). Commentaries on Big Data's importance for

accounting and auditing. Accounting Horizons, 29(2), pp.377-379.

Bibliography

Al-Khaddash, H., Al Nawas, R. and Ramadan, A. (2013). Factors affecting the quality of

auditing: The case of Jordanian commercial banks. International Journal of Business and

Social Science, 4(11).

Butcher, K., Harrison, G. and Ross, P., 2013. Perceptions of audit service quality and auditor

retention. International Journal of Auditing, 17(1), pp.54-74.

Christensen, B.E., Glover, S.M., Omer, T.C. and Shelley, M.K. (2016). Understanding audit

quality: Insights from audit professionals and investors. Contemporary Accounting Research,

33(4), pp.1648-1684.

Clayfield M. (16th August 2011). The role of Corporate Managers in the Fall of Corporate

organisations. Sydney Morning Herald (SMH), p 29-30.

Emeh, Y. and Appah, E. (2013). Audit committee and timeliness of financial reports:

Empirical evidence from Nigeria. Journal of Economics and sustainable Development, 4(20),

pp.14-25.

Eshleman, J.D. and Guo, P. (2013). Abnormal audit fees and audit quality: The importance of

considering managerial incentives in tests of earnings management. Auditing: A Journal of

Practice & Theory, 33(1), pp.117-138.

Fernie, J. and Sparks, L. (2014). Logistics and retail management: emerging issues and new

challenges in the retail supply chain. Kogan page publishers.

Griffin, P.A. and Wright, A.M. (2015). Commentaries on Big Data's importance for

accounting and auditing. Accounting Horizons, 29(2), pp.377-379.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing 11

Hashem, I.A.T., Yaqoob, I., Anuar, N.B., Mokhtar, S., Gani, A. and Khan, S.U. (2015). The

general of benefits accounting for workers benefits in Australia. Journal of Business Finance

and Accounting, 47, pp.98-115.

Huang, J. and Nicol, D.M. (2013). Fair value accounting and gains from asset securitizations:

A convenient earnings management tool with compensation side-benefits. Journal of

accounting and economics, 2(1), p.9.

Jostern K.L. (15th May 2013). What made the corporate organisations to collapse: The

Collapse of Harris Scarfe. Australian Financial Review Newspaper, p. 18.

Kasim, N. and Sanusi, Z.M. (2013). Emerging issues for auditing in Islamic financial

institutions: Empirical evidence from Malaysia. IOSR Journal of Business and Management,

8(5), pp.10-17.

Kavrar, O. and Yılmaz, B. (January 2017) Corporate Collapses in Australia: Case of Harris

Scarfe. Journal of Economics, Business and Management, Vol. 5, No. 1,

Khlif, H. and Samaha, K. (2014). Internal Control Quality, E gyptian Standards on Auditing

and External Audit Delays: Evidence from the E gyptian Stock Exchange. International

Journal of Auditing, 18(2), pp.139-154.

Kshetri, N. (2013). Accounting and Auditing in an Organisation: The role of institutions and

institutional evolution. Accounting Journal, 37(4-5), pp.372-386.

Lim, Y.M., Lee, T.H., Yap, C.S. and Ling, C.C. (2016). Employability skills, personal

qualities, and early employment problems of entry-level auditors: Perspectives from

employers, lecturers, auditors, and students. Journal of Education for Business, 91(4),

pp.185-192.

Hashem, I.A.T., Yaqoob, I., Anuar, N.B., Mokhtar, S., Gani, A. and Khan, S.U. (2015). The

general of benefits accounting for workers benefits in Australia. Journal of Business Finance

and Accounting, 47, pp.98-115.

Huang, J. and Nicol, D.M. (2013). Fair value accounting and gains from asset securitizations:

A convenient earnings management tool with compensation side-benefits. Journal of

accounting and economics, 2(1), p.9.

Jostern K.L. (15th May 2013). What made the corporate organisations to collapse: The

Collapse of Harris Scarfe. Australian Financial Review Newspaper, p. 18.

Kasim, N. and Sanusi, Z.M. (2013). Emerging issues for auditing in Islamic financial

institutions: Empirical evidence from Malaysia. IOSR Journal of Business and Management,

8(5), pp.10-17.

Kavrar, O. and Yılmaz, B. (January 2017) Corporate Collapses in Australia: Case of Harris

Scarfe. Journal of Economics, Business and Management, Vol. 5, No. 1,

Khlif, H. and Samaha, K. (2014). Internal Control Quality, E gyptian Standards on Auditing

and External Audit Delays: Evidence from the E gyptian Stock Exchange. International

Journal of Auditing, 18(2), pp.139-154.

Kshetri, N. (2013). Accounting and Auditing in an Organisation: The role of institutions and

institutional evolution. Accounting Journal, 37(4-5), pp.372-386.

Lim, Y.M., Lee, T.H., Yap, C.S. and Ling, C.C. (2016). Employability skills, personal

qualities, and early employment problems of entry-level auditors: Perspectives from

employers, lecturers, auditors, and students. Journal of Education for Business, 91(4),

pp.185-192.

Auditing 12

Rasheed, H. (2014). Data and infrastructure security auditing in cloud computing

environments. International Journal of Information Management, 34(3), pp.364-368.

Rönnberg, L., Lindgren, J. and Segerholm, C. (2013). In the public eye: Swedish school

inspection and local newspapers: exploring the audit–media relationship. Journal of

Education Policy, 28(2), pp.178-197.

Siriwardane, H.P., Kin Hoi Hu, B. and Low, K.Y. (2014). Skills, Knowledge, and Attitudes

Important for Present‐Day Auditors. International journal of auditing, 18(3), pp.193-205.

Sookhak, M., Gani, A., Talebian, H., Akhunzada, A., Khan, S.U., Buyya, R. and Zomaya,

A.Y. (2015). Qualities of Accountants and Auditors in performing their duties. ACM

accounting Surveys (CSUR), 47(4), p.65.

Sookhak, M., Talebian, H., Ahmed, E., Gani, A. and Khan, M.K. (2014). A review on

Accounting and Auditing Qualities: Accounting issues. International journal of auditing, 43,

pp.121-141.

Yeh, C.C., Chi, D.J. and Lin, Y.R. (2014). Corporate Governance and Accounting in

Corporate Management. Business Journal, 254, pp.98-110.

Rasheed, H. (2014). Data and infrastructure security auditing in cloud computing

environments. International Journal of Information Management, 34(3), pp.364-368.

Rönnberg, L., Lindgren, J. and Segerholm, C. (2013). In the public eye: Swedish school

inspection and local newspapers: exploring the audit–media relationship. Journal of

Education Policy, 28(2), pp.178-197.

Siriwardane, H.P., Kin Hoi Hu, B. and Low, K.Y. (2014). Skills, Knowledge, and Attitudes

Important for Present‐Day Auditors. International journal of auditing, 18(3), pp.193-205.

Sookhak, M., Gani, A., Talebian, H., Akhunzada, A., Khan, S.U., Buyya, R. and Zomaya,

A.Y. (2015). Qualities of Accountants and Auditors in performing their duties. ACM

accounting Surveys (CSUR), 47(4), p.65.

Sookhak, M., Talebian, H., Ahmed, E., Gani, A. and Khan, M.K. (2014). A review on

Accounting and Auditing Qualities: Accounting issues. International journal of auditing, 43,

pp.121-141.

Yeh, C.C., Chi, D.J. and Lin, Y.R. (2014). Corporate Governance and Accounting in

Corporate Management. Business Journal, 254, pp.98-110.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.