Corporate Accounting: Consolidation Journal & Worksheet Solution

VerifiedAdded on 2023/06/05

|8

|1193

|291

Homework Assignment

AI Summary

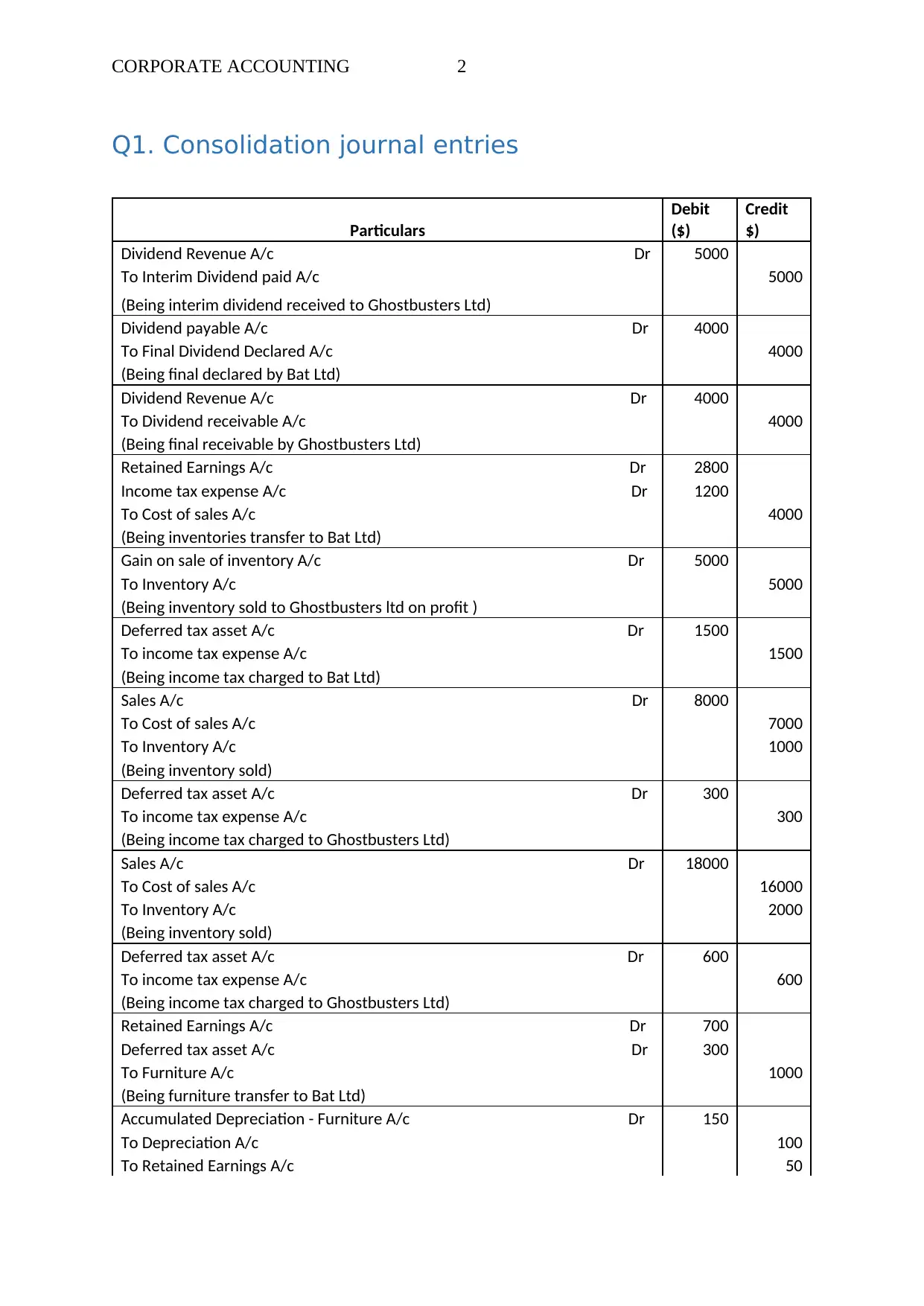

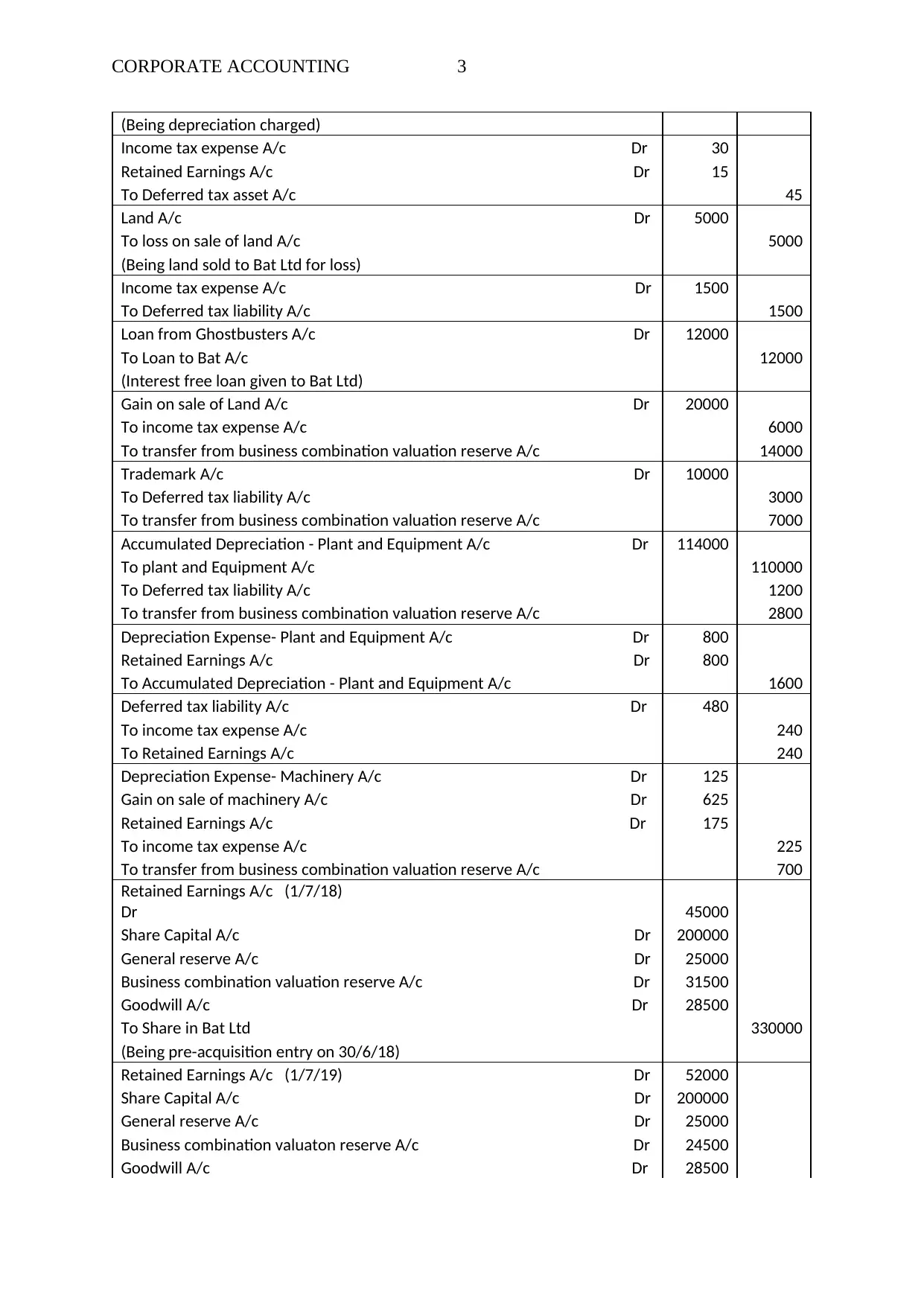

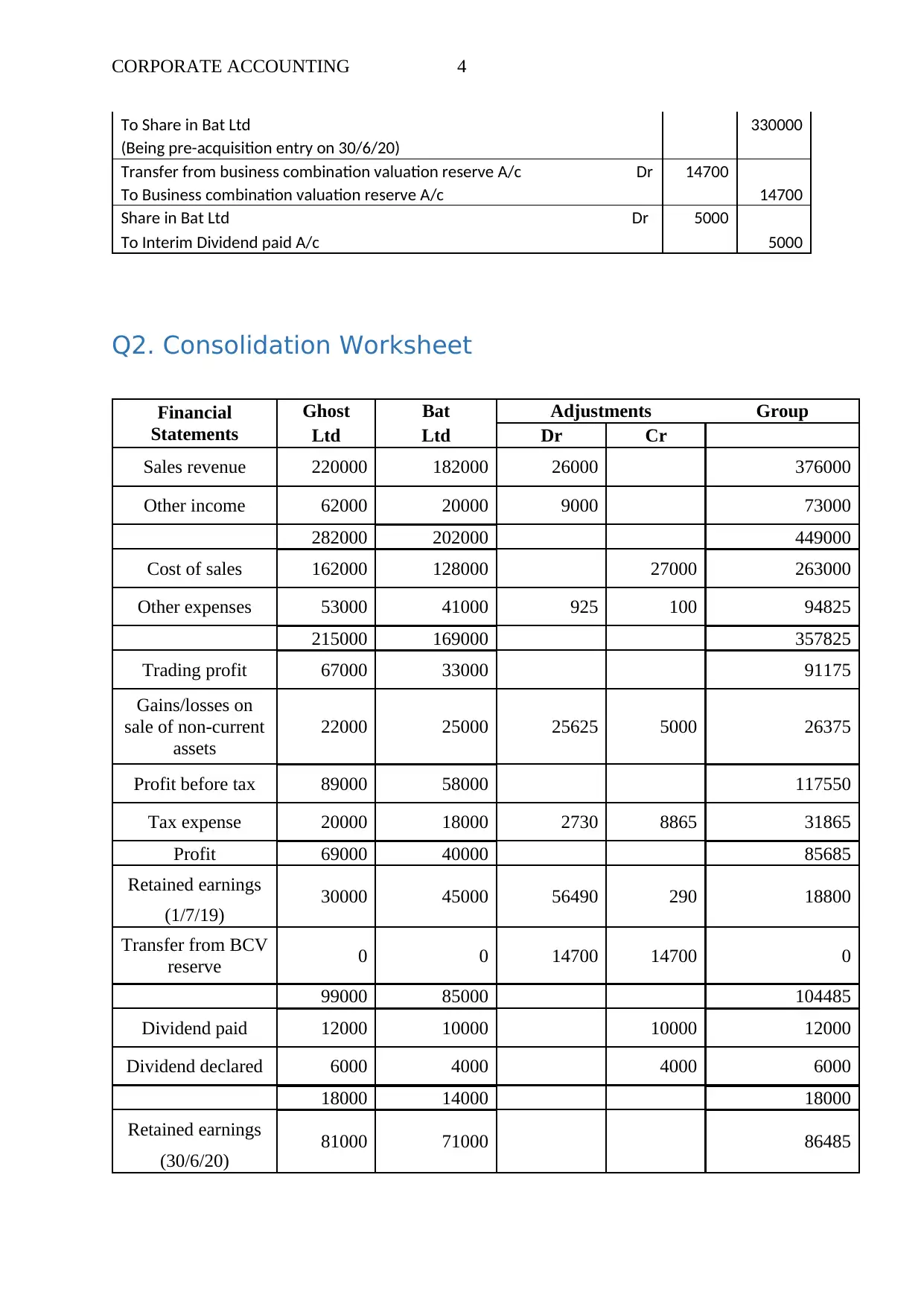

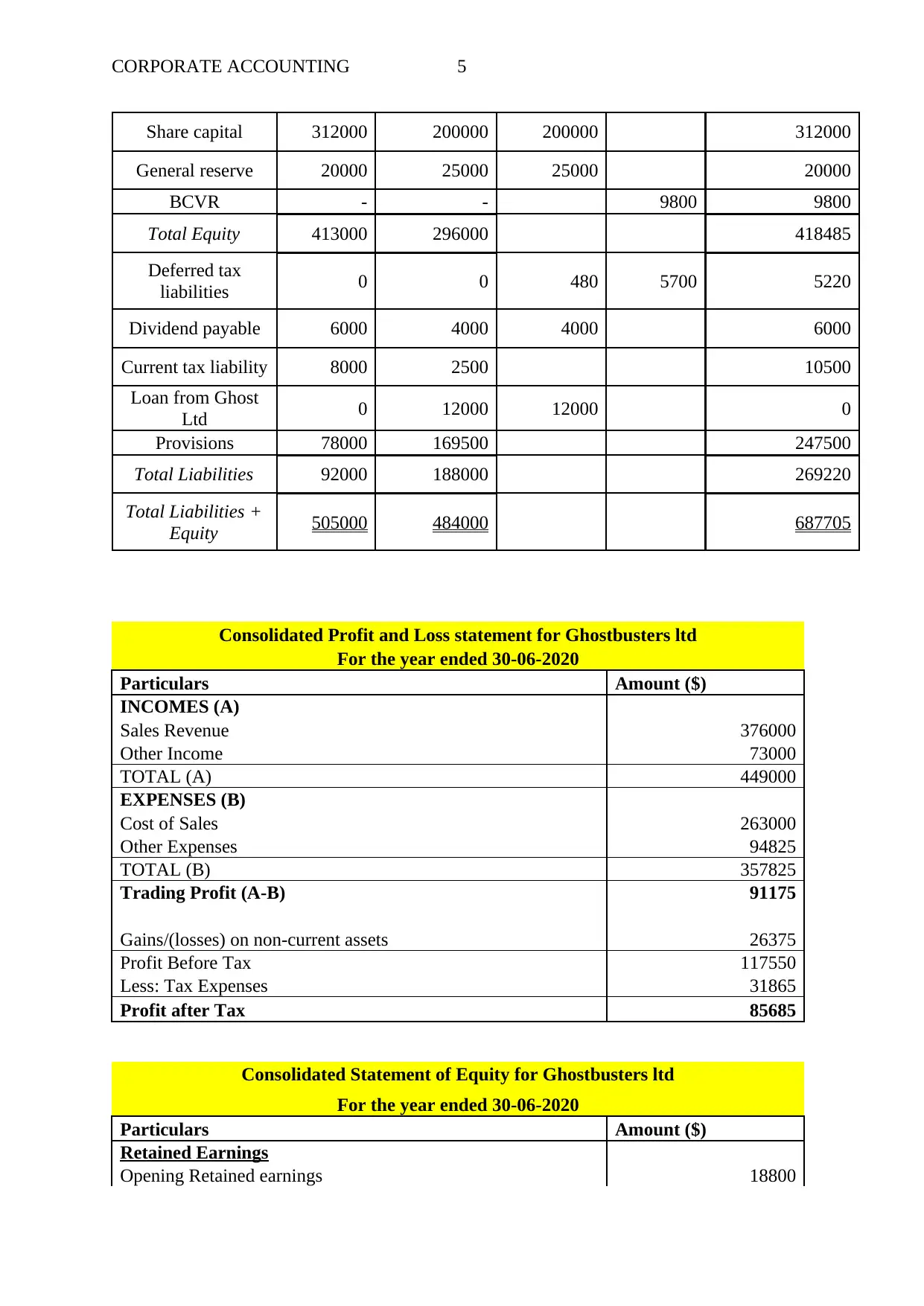

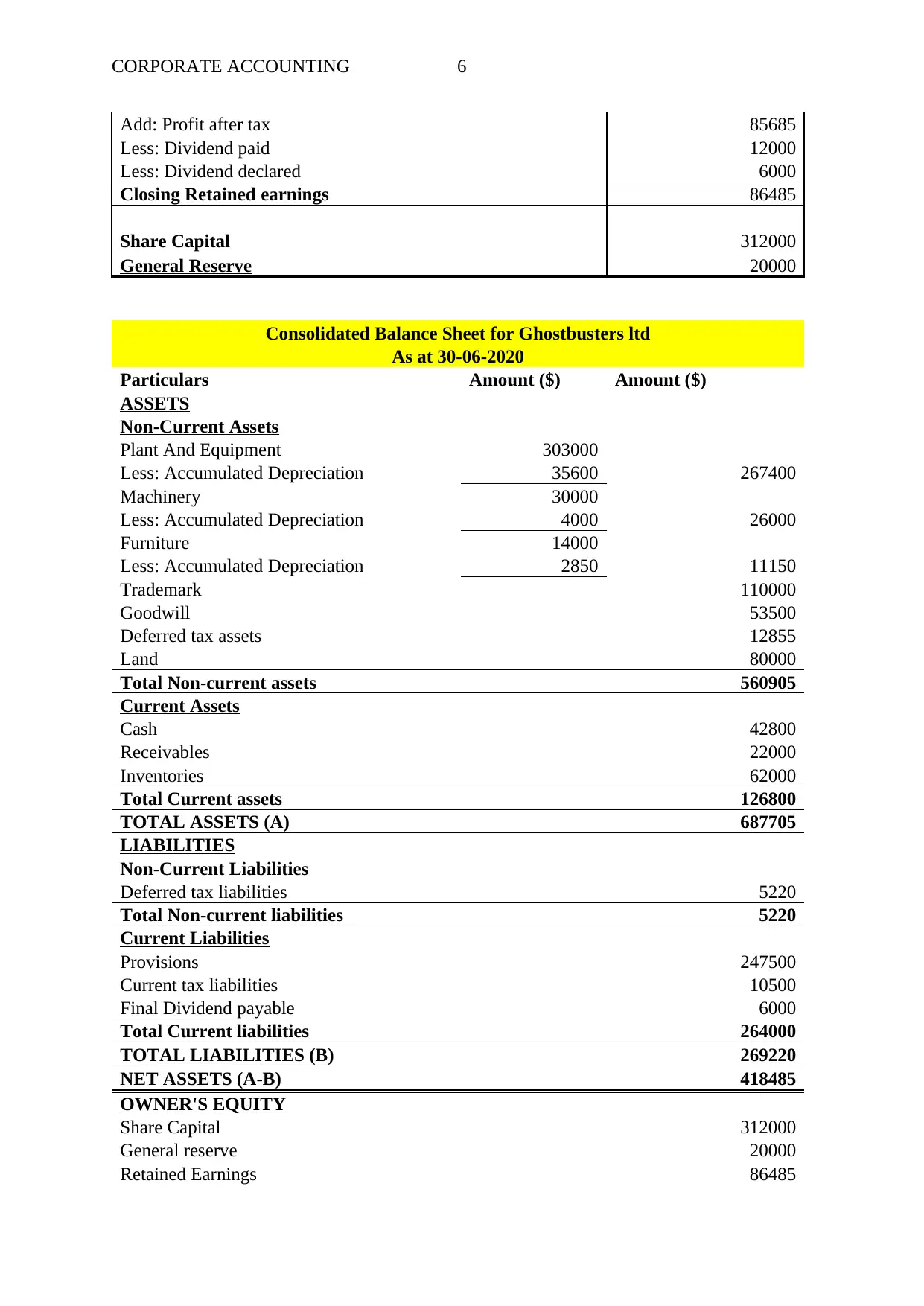

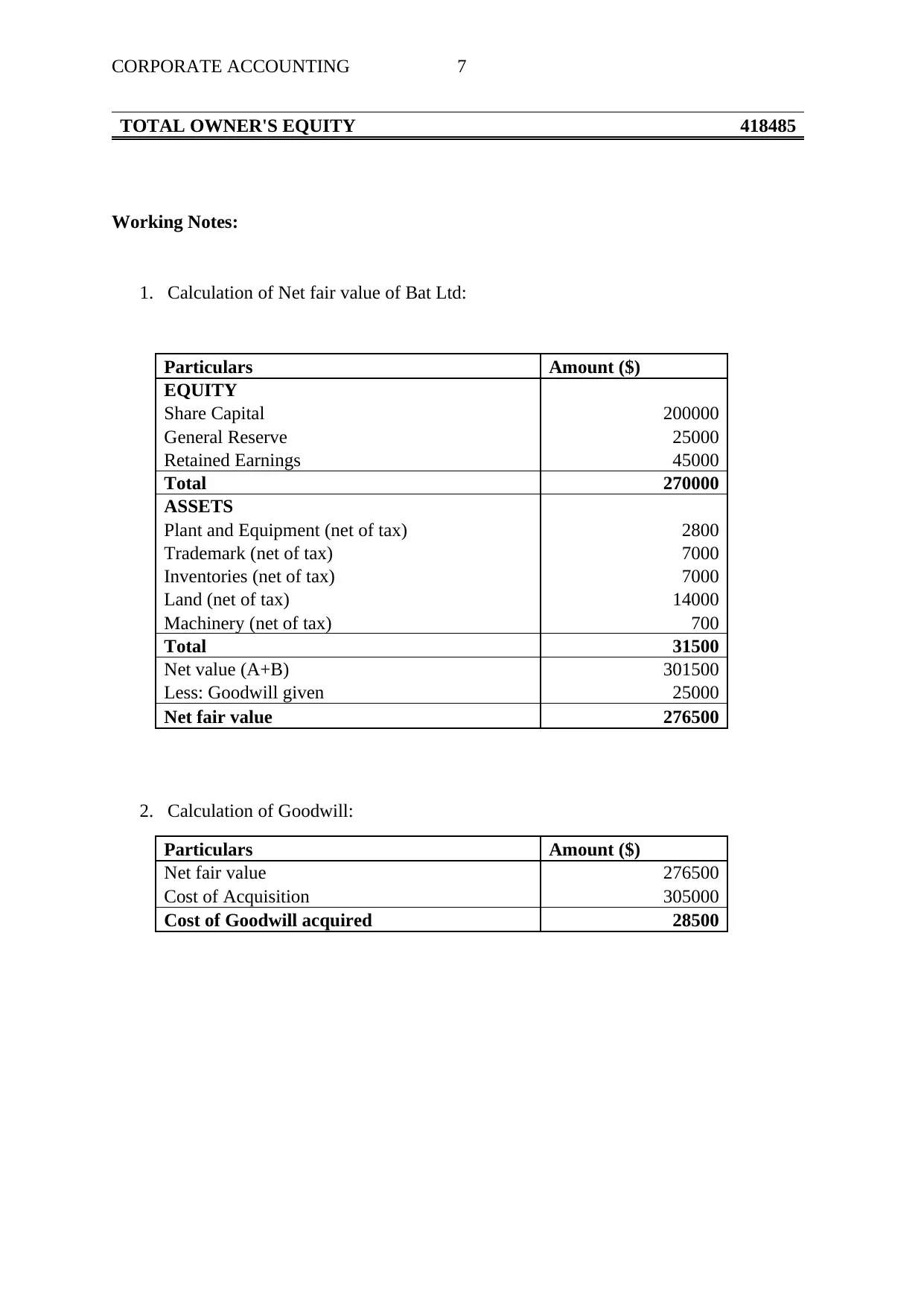

This document presents a detailed solution to a corporate accounting assignment centered on the consolidation of financial statements. It includes a series of consolidation journal entries addressing various intercompany transactions, such as dividends, inventory transfers, and asset sales. The solution also features a comprehensive consolidation worksheet, integrating the financial statements of the parent and subsidiary companies to derive consolidated figures. Furthermore, the document provides the consolidated profit and loss statement, statement of equity, and balance sheet, offering a complete picture of the consolidated financial position. Working notes are included to demonstrate the calculations of net fair value and goodwill. This assignment is a great resource for students studying corporate accounting, covering key concepts like consolidation, intercompany eliminations, and the preparation of consolidated financial statements.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.