Corporate Accounting Report: Emission Allowance, Financial Statements

VerifiedAdded on 2020/05/08

|11

|2567

|219

Report

AI Summary

This report provides an in-depth analysis of emission allowances within the context of corporate accounting, specifically addressing the European Union Emission Trading Scheme (EU ETS). It begins by defining the nature of emission allowances and their legal implications, followed by a detailed examination of initial and subsequent measurement methods, including the use of fair value and relevant journal entries. The report then explores the consequences of emission allowances on financial statements, focusing on their impact on the balance sheet, income statement, and cash flow statement, and how these are affected by different accounting models. The discussion covers the accounting treatment of emission allowances as intangible assets, the impact on expenses and income, and the classification of cash flows. The report concludes by summarizing the key aspects of emission allowance accounting and its implications for financial reporting.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Corporate Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................2

Nature of the Emission Allowance:...........................................................................................2

Initial and subsequent measurement of Emission Allowance:...................................................3

Consequences of Emission Allowance on Financial Statement:...............................................5

Conclusion:................................................................................................................................7

Reference List:...........................................................................................................................9

Table of Contents

Introduction:...............................................................................................................................2

Nature of the Emission Allowance:...........................................................................................2

Initial and subsequent measurement of Emission Allowance:...................................................3

Consequences of Emission Allowance on Financial Statement:...............................................5

Conclusion:................................................................................................................................7

Reference List:...........................................................................................................................9

2CORPORATE ACCOUNTING

Introduction:

The present study is concerned with the in depth discussion relating to the nature of

emission stated by the European Union ETS. The current study is also based on the

determination of the method involved in the measuring the initial and the subsequent level

together with the help of the appropriate journal entries. In addition to this, the report will be

placing emphasis on the consequences that arises from the inclusion of emission allowance

on the financial statement namely, balance sheet, income statement and cash flow statement.

Nature of the Emission Allowance:

The lawful nature concerning the emission allowance is issued and traded within the

guidelines of the European Union Emission Trading Scheme and it is not defined or

consistent at the European level. As defined under the Emission Trading Scheme Directive

Article 3 (a) provides the definition of the emission allowance. It further defines the right to

emit with one tonne of CO2 under the article 3 (a) of the Emission Trading Scheme Directive

(Zhang et al., 2015). This is will be considered to be valid for the purpose of complying with

the requirements stated under the Emission Trading Scheme Directive and it will be treated as

manageable in agreement with the provision that has been stated under the Emission Trading

Scheme Directive (Zakeri et al., 2015). The nature concerning the emission allowance will be

treated to be relevant under the issues that has been stated below;

a. At the time of determining the law that manages the creation, transfer and cessation of

the emission allowances,

b. Whether there is any kind of security that can be developed over the emission

allowance

c. Management of emission allowance relating to accounting and tax purpose

d. Management of emission allowance at the time of bankruptcy of the listed holder

Introduction:

The present study is concerned with the in depth discussion relating to the nature of

emission stated by the European Union ETS. The current study is also based on the

determination of the method involved in the measuring the initial and the subsequent level

together with the help of the appropriate journal entries. In addition to this, the report will be

placing emphasis on the consequences that arises from the inclusion of emission allowance

on the financial statement namely, balance sheet, income statement and cash flow statement.

Nature of the Emission Allowance:

The lawful nature concerning the emission allowance is issued and traded within the

guidelines of the European Union Emission Trading Scheme and it is not defined or

consistent at the European level. As defined under the Emission Trading Scheme Directive

Article 3 (a) provides the definition of the emission allowance. It further defines the right to

emit with one tonne of CO2 under the article 3 (a) of the Emission Trading Scheme Directive

(Zhang et al., 2015). This is will be considered to be valid for the purpose of complying with

the requirements stated under the Emission Trading Scheme Directive and it will be treated as

manageable in agreement with the provision that has been stated under the Emission Trading

Scheme Directive (Zakeri et al., 2015). The nature concerning the emission allowance will be

treated to be relevant under the issues that has been stated below;

a. At the time of determining the law that manages the creation, transfer and cessation of

the emission allowances,

b. Whether there is any kind of security that can be developed over the emission

allowance

c. Management of emission allowance relating to accounting and tax purpose

d. Management of emission allowance at the time of bankruptcy of the listed holder

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

To take into the considerations relating to the oversight of the carbon market it is vital

to determine the legality nature of the individual entity, which is being traded in the market.

There are large number of legalised administrations, which is traded in the market (Chao,

2014). A large number of lawful regimes is found to be involved in the regulations of the

emission allowance, which brings forward the number of legal questions relating to law of

property, law relating to financial service or law relating to contracts and accounting

standard. An entity can break into the all-encompassing markets which usually consists of the

distributions of the allowance from the accountable agency or any institutions relating to the

parties which is under the obligations of complying with the emission trading system.

The secondary market on the other hand consist of purchase and sale of allowance

together with numerous contracts for future sales of allowance (Goulder & Schein, 2013).

Emission allowance under the market for trading have resemblances with commodities and

monetary market that possess unlikely feature in either of the market. The oversight relating

to any form of carbon market is largely reliant on the current institutional infrastructure with

jurisdiction have role to play in adopting the correct approach to the market oversight (Dong

et al., 2016). The characteristics that have been defined in article 40 of registry principles

defines an allowance to be dematerialized tool that is tradable in the market.

Initial and subsequent measurement of Emission Allowance:

Tentatively the board has come up to the decision of measuring the emission

allowance. The board has specifically stated in its decision that there must be consistent in the

liability of the emission allowance together with the allocation of the liability must be

executed initially and subsequently under the terms of fair value (Zhang & Xu, 2013).

Tentatively the board has undertook the decision relating to the purchase allowance, which

should be measured under the terms of fair value both initially and subsequently.

To take into the considerations relating to the oversight of the carbon market it is vital

to determine the legality nature of the individual entity, which is being traded in the market.

There are large number of legalised administrations, which is traded in the market (Chao,

2014). A large number of lawful regimes is found to be involved in the regulations of the

emission allowance, which brings forward the number of legal questions relating to law of

property, law relating to financial service or law relating to contracts and accounting

standard. An entity can break into the all-encompassing markets which usually consists of the

distributions of the allowance from the accountable agency or any institutions relating to the

parties which is under the obligations of complying with the emission trading system.

The secondary market on the other hand consist of purchase and sale of allowance

together with numerous contracts for future sales of allowance (Goulder & Schein, 2013).

Emission allowance under the market for trading have resemblances with commodities and

monetary market that possess unlikely feature in either of the market. The oversight relating

to any form of carbon market is largely reliant on the current institutional infrastructure with

jurisdiction have role to play in adopting the correct approach to the market oversight (Dong

et al., 2016). The characteristics that have been defined in article 40 of registry principles

defines an allowance to be dematerialized tool that is tradable in the market.

Initial and subsequent measurement of Emission Allowance:

Tentatively the board has come up to the decision of measuring the emission

allowance. The board has specifically stated in its decision that there must be consistent in the

liability of the emission allowance together with the allocation of the liability must be

executed initially and subsequently under the terms of fair value (Zhang & Xu, 2013).

Tentatively the board has undertook the decision relating to the purchase allowance, which

should be measured under the terms of fair value both initially and subsequently.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

A preference has been introduced by the IASB that describes the gross presentation

should be made relating to the assets and liabilities on the balance sheet (Du et al., 2013).

Additionally, in accordance with the linked presentations, the assets and liabilities should be

presented under the gross value but the value should be obtainable with the total amount of

net emission or the emission liability. Tentatively the FASB has bought forward an assertion

by stating that the asset and liabilities should be stated in the balance sheet by using the

linked presentation (Agee et al., 2014). The FASB additionally bought forward that in no

circumstances it believes that any commercial entity will be obligatory required to possess

the intent of setting off the asset and liabilities to present the items through using linked

presentation.

As evident from the discussion, the board has defined that the measurement

concerning the emission allowance assets and liabilities should be in accordance with the

scheme of cap and trade. Tentatively the board has made the decision that the allocation of

emission allowance liability should be consistent (Bang et al., 2017). The board members has

lend their backing for the model that helps in the measurement of the allocated allowance

along with the liability associated with allocation must be measured in terms of the fair value.

The board discussion has stated that the business unit should determine the level of

emission allowance, which the unit will be returning under the liability associated with the

allocation at the time when the business unit is required to identify the obligations associated

to emission (Rabe, 2016). A support has been lend by the board relating to the adoption of

approach which determines the quantity of the emission allowance to be returned in respect

of the business unit expectations related to emission or lessening of emission.

A preference has been introduced by the IASB that describes the gross presentation

should be made relating to the assets and liabilities on the balance sheet (Du et al., 2013).

Additionally, in accordance with the linked presentations, the assets and liabilities should be

presented under the gross value but the value should be obtainable with the total amount of

net emission or the emission liability. Tentatively the FASB has bought forward an assertion

by stating that the asset and liabilities should be stated in the balance sheet by using the

linked presentation (Agee et al., 2014). The FASB additionally bought forward that in no

circumstances it believes that any commercial entity will be obligatory required to possess

the intent of setting off the asset and liabilities to present the items through using linked

presentation.

As evident from the discussion, the board has defined that the measurement

concerning the emission allowance assets and liabilities should be in accordance with the

scheme of cap and trade. Tentatively the board has made the decision that the allocation of

emission allowance liability should be consistent (Bang et al., 2017). The board members has

lend their backing for the model that helps in the measurement of the allocated allowance

along with the liability associated with allocation must be measured in terms of the fair value.

The board discussion has stated that the business unit should determine the level of

emission allowance, which the unit will be returning under the liability associated with the

allocation at the time when the business unit is required to identify the obligations associated

to emission (Rabe, 2016). A support has been lend by the board relating to the adoption of

approach which determines the quantity of the emission allowance to be returned in respect

of the business unit expectations related to emission or lessening of emission.

5CORPORATE ACCOUNTING

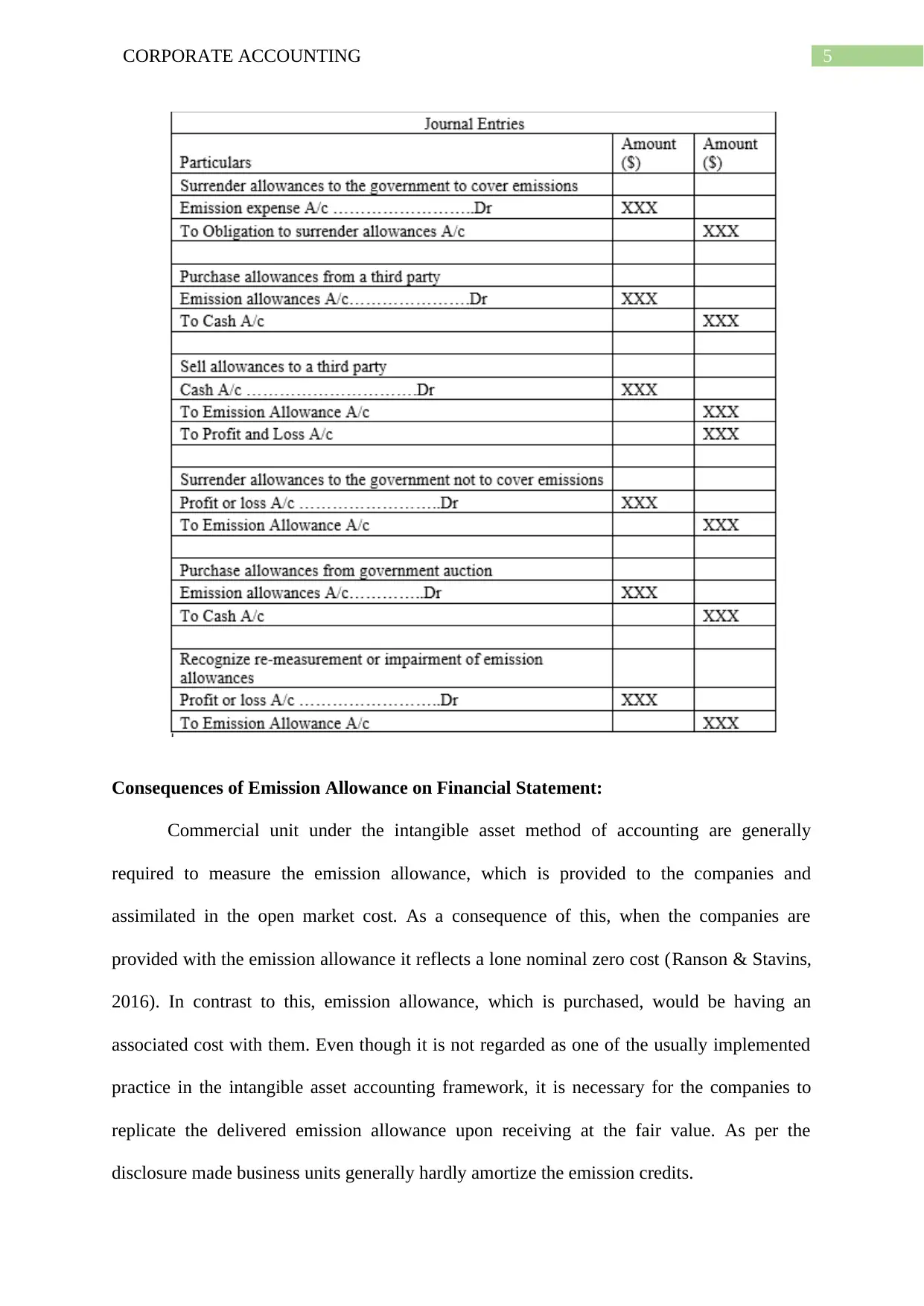

Consequences of Emission Allowance on Financial Statement:

Commercial unit under the intangible asset method of accounting are generally

required to measure the emission allowance, which is provided to the companies and

assimilated in the open market cost. As a consequence of this, when the companies are

provided with the emission allowance it reflects a lone nominal zero cost (Ranson & Stavins,

2016). In contrast to this, emission allowance, which is purchased, would be having an

associated cost with them. Even though it is not regarded as one of the usually implemented

practice in the intangible asset accounting framework, it is necessary for the companies to

replicate the delivered emission allowance upon receiving at the fair value. As per the

disclosure made business units generally hardly amortize the emission credits.

Consequences of Emission Allowance on Financial Statement:

Commercial unit under the intangible asset method of accounting are generally

required to measure the emission allowance, which is provided to the companies and

assimilated in the open market cost. As a consequence of this, when the companies are

provided with the emission allowance it reflects a lone nominal zero cost (Ranson & Stavins,

2016). In contrast to this, emission allowance, which is purchased, would be having an

associated cost with them. Even though it is not regarded as one of the usually implemented

practice in the intangible asset accounting framework, it is necessary for the companies to

replicate the delivered emission allowance upon receiving at the fair value. As per the

disclosure made business units generally hardly amortize the emission credits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

The reason behind this is that their economic benefit is not diminished till it is

consumed. Consequently, no cost of credit is charged to the expenditure till they are disposed

or used. The emission credits allowance is treated as the substance of impairment under the

indefinite livid intangible asset model of the impairment or they are under the model of the

fixed asset for the purpose of determinate intangible asset till the degree the business is

amortizing the emission allowance (Schneider et al., 2017). Emission allowance are

characterized in the long term balance sheet with cash inflows and outflows related to

emissions allowance are categorized in the investment activities under the cash flow

statement.

The consequences relating to emission allowance is reflected in the financial

statements in the inventory model of accounting and emission credits are weighted in respect

of the average cost. The EPA issues emission credits or any sort of regulatory model having

zero cost basis. Most notably the weighted average cost of emission allowance used in every

period is charged to the fuel costs (Kaufman, 2013). Under the market, approach the emission

credits is subject to lowered cost market approach for impairment under the model of

inventory. Because of this, the emission allowance are categorized as the inventory in balance

sheet with inflow and outflow of cash is related to the emission credits that is categorized in

the operating activities in the cash flow statement. Commercial unit that trade under the

emission allowance are under the compulsion of following the inventory model.

As evident from both the models the practice of the industry states that business units

are generally not required to record the requirements of delivering the emission allowance to

the regulatory agency till it is found that actual level of emission for a given time period has

exceeded the credits which is held on the balance sheet (Harris, 2016). Consequently, the

gain is characteristically recognized during the given period in which the emission credits are

disposed off. This kind of practice generally differs from the recognition of gain as numerous

The reason behind this is that their economic benefit is not diminished till it is

consumed. Consequently, no cost of credit is charged to the expenditure till they are disposed

or used. The emission credits allowance is treated as the substance of impairment under the

indefinite livid intangible asset model of the impairment or they are under the model of the

fixed asset for the purpose of determinate intangible asset till the degree the business is

amortizing the emission allowance (Schneider et al., 2017). Emission allowance are

characterized in the long term balance sheet with cash inflows and outflows related to

emissions allowance are categorized in the investment activities under the cash flow

statement.

The consequences relating to emission allowance is reflected in the financial

statements in the inventory model of accounting and emission credits are weighted in respect

of the average cost. The EPA issues emission credits or any sort of regulatory model having

zero cost basis. Most notably the weighted average cost of emission allowance used in every

period is charged to the fuel costs (Kaufman, 2013). Under the market, approach the emission

credits is subject to lowered cost market approach for impairment under the model of

inventory. Because of this, the emission allowance are categorized as the inventory in balance

sheet with inflow and outflow of cash is related to the emission credits that is categorized in

the operating activities in the cash flow statement. Commercial unit that trade under the

emission allowance are under the compulsion of following the inventory model.

As evident from both the models the practice of the industry states that business units

are generally not required to record the requirements of delivering the emission allowance to

the regulatory agency till it is found that actual level of emission for a given time period has

exceeded the credits which is held on the balance sheet (Harris, 2016). Consequently, the

gain is characteristically recognized during the given period in which the emission credits are

disposed off. This kind of practice generally differs from the recognition of gain as numerous

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

such companies have undertaken the accounting policies that needs the deferral of gain if the

emission credits is granted in the upcoming years but it is disposed in the current year.

Concerning the income statement there are primary two forms of significances of

emission that is noticed. Initially it arises due to the usage of several diverse attributes for the

correct asset and the liabilities under the IFRIC3 model. It arises because of the use of the

IAS 38 model of cost for accounting the emission allowance asset along with the result

originating from the mismatch amid the dimension of liability and it is measured again to

ascertain the market value together with the changes in the net income by measuring the asset

at cost (Schwager & Etzkorn, 2017). Conversely if the commercial unit uses the method of

revaluation in respect of the IAS 38, it is under the obligation of displaying the changes under

the fair value of the allowance asset in the income statement together with changes that has

occurred in the fair value of the liability in the net income.

The second effect that originates in the income statement is the outline of expenses

which is identified in the income statement. The approach of the IFRIC 3 states that present

period of expense is equal to the amount of fair value emission which is generated all through

the period and recognizes the income which is equal to the amortization of the government

grant associated with the allowance. Implementing the net approach will lead the liability to

be reflected in the balance sheet and expenses is recorded in the income statement provided

that the actual level of emission has surpassed the whole amount of allowance allotted to the

unit on free price by the administration.

Conclusion:

The above stated report can be concluded by stating that an explanation to the nature

of the emission has been discussed in this report. Additionally, the report has discussed on the

emission relating to the method of emission of the allowance at the time of measurement

such companies have undertaken the accounting policies that needs the deferral of gain if the

emission credits is granted in the upcoming years but it is disposed in the current year.

Concerning the income statement there are primary two forms of significances of

emission that is noticed. Initially it arises due to the usage of several diverse attributes for the

correct asset and the liabilities under the IFRIC3 model. It arises because of the use of the

IAS 38 model of cost for accounting the emission allowance asset along with the result

originating from the mismatch amid the dimension of liability and it is measured again to

ascertain the market value together with the changes in the net income by measuring the asset

at cost (Schwager & Etzkorn, 2017). Conversely if the commercial unit uses the method of

revaluation in respect of the IAS 38, it is under the obligation of displaying the changes under

the fair value of the allowance asset in the income statement together with changes that has

occurred in the fair value of the liability in the net income.

The second effect that originates in the income statement is the outline of expenses

which is identified in the income statement. The approach of the IFRIC 3 states that present

period of expense is equal to the amount of fair value emission which is generated all through

the period and recognizes the income which is equal to the amortization of the government

grant associated with the allowance. Implementing the net approach will lead the liability to

be reflected in the balance sheet and expenses is recorded in the income statement provided

that the actual level of emission has surpassed the whole amount of allowance allotted to the

unit on free price by the administration.

Conclusion:

The above stated report can be concluded by stating that an explanation to the nature

of the emission has been discussed in this report. Additionally, the report has discussed on the

emission relating to the method of emission of the allowance at the time of measurement

8CORPORATE ACCOUNTING

during the initial and the subsequent level by citing the examples of appropriate journal

entries. The report has in detailed discussed the consequences of emission allowance on the

financial statements. The discussion of consequences has placed emphasis on the key areas of

balance sheet, income statement and cash flow statement.

during the initial and the subsequent level by citing the examples of appropriate journal

entries. The report has in detailed discussed the consequences of emission allowance on the

financial statements. The discussion of consequences has placed emphasis on the key areas of

balance sheet, income statement and cash flow statement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

Reference List:

Agee, M. D., Atkinson, S. E., Crocker, T. D., & Williams, J. W. (2014). Non-separable

pollution control: implications for a CO 2 emissions cap and trade system. Resource

and Energy Economics, 36(1), 64-82.

Bang, G., Victor, D. G., & Andresen, S. (2017). California’s Cap-and-Trade System:

Diffusion and Lessons. Global Environmental Politics.

Chao, C. C. (2014). Assessment of carbon emission costs for air cargo

transportation. Transportation Research Part D: Transport and Environment, 33,

186-195.

Dong, C., Shen, B., Chow, P. S., Yang, L., & Ng, C. T. (2016). Sustainability investment

under cap-and-trade regulation. Annals of Operations Research, 240(2), 509-531.

Du, S., Zhu, L., Liang, L., & Ma, F. (2013). Emission-dependent supply chain and

environment-policy-making in the ‘cap-and-trade’system. Energy Policy, 57, 61-67.

Goulder, L. H., & Schein, A. R. (2013). Carbon taxes versus cap and trade: a critical

review. Climate Change Economics, 4(03), 1350010.

Harris, L. (2016). Trading and Electronic Markets: What Investment Professionals Need to

Know (a summary). Research Foundation Publications, 2016(1), 24-30.

Kaufman, P. J. (2013). Trading systems and methods. John Wiley & Sons.

Rabe, B. G. (2016). The Durability of Carbon Cap‐and‐Trade Policy. Governance, 29(1),

103-119.

Ranson, M., & Stavins, R. N. (2016). Linkage of greenhouse gas emissions trading systems:

Learning from experience. Climate Policy, 16(3), 284-300.

Reference List:

Agee, M. D., Atkinson, S. E., Crocker, T. D., & Williams, J. W. (2014). Non-separable

pollution control: implications for a CO 2 emissions cap and trade system. Resource

and Energy Economics, 36(1), 64-82.

Bang, G., Victor, D. G., & Andresen, S. (2017). California’s Cap-and-Trade System:

Diffusion and Lessons. Global Environmental Politics.

Chao, C. C. (2014). Assessment of carbon emission costs for air cargo

transportation. Transportation Research Part D: Transport and Environment, 33,

186-195.

Dong, C., Shen, B., Chow, P. S., Yang, L., & Ng, C. T. (2016). Sustainability investment

under cap-and-trade regulation. Annals of Operations Research, 240(2), 509-531.

Du, S., Zhu, L., Liang, L., & Ma, F. (2013). Emission-dependent supply chain and

environment-policy-making in the ‘cap-and-trade’system. Energy Policy, 57, 61-67.

Goulder, L. H., & Schein, A. R. (2013). Carbon taxes versus cap and trade: a critical

review. Climate Change Economics, 4(03), 1350010.

Harris, L. (2016). Trading and Electronic Markets: What Investment Professionals Need to

Know (a summary). Research Foundation Publications, 2016(1), 24-30.

Kaufman, P. J. (2013). Trading systems and methods. John Wiley & Sons.

Rabe, B. G. (2016). The Durability of Carbon Cap‐and‐Trade Policy. Governance, 29(1),

103-119.

Ranson, M., & Stavins, R. N. (2016). Linkage of greenhouse gas emissions trading systems:

Learning from experience. Climate Policy, 16(3), 284-300.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

Schneider, L., Lazarus, M., Lee, C., & van Asselt, H. (2017). Restricted linking of emissions

trading systems: options, benefits, and challenges. International Environmental

Agreements: Politics, Law and Economics, 1-16.

Schwager, J. D., & Etzkorn, M. (2017). An Introduction to Options on Futures. A Complete

Guide to the Futures Market: Technical Analysis and Trading Systems, Fundamental

Analysis, Options, Spreads, and Trading Principles, 477-485.

Zakeri, A., Dehghanian, F., Fahimnia, B., & Sarkis, J. (2015). Carbon pricing versus

emissions trading: A supply chain planning perspective. International Journal of

Production Economics, 164, 197-205.

Zhang, B., & Xu, L. (2013). Multi-item production planning with carbon cap and trade

mechanism. International Journal of Production Economics, 144(1), 118-127.

Zhang, Y. J., Wang, A. D., & Tan, W. (2015). The impact of China's carbon allowance

allocation rules on the product prices and emission reduction behaviors of ETS-

covered enterprises. Energy Policy, 86, 176-185.

Schneider, L., Lazarus, M., Lee, C., & van Asselt, H. (2017). Restricted linking of emissions

trading systems: options, benefits, and challenges. International Environmental

Agreements: Politics, Law and Economics, 1-16.

Schwager, J. D., & Etzkorn, M. (2017). An Introduction to Options on Futures. A Complete

Guide to the Futures Market: Technical Analysis and Trading Systems, Fundamental

Analysis, Options, Spreads, and Trading Principles, 477-485.

Zakeri, A., Dehghanian, F., Fahimnia, B., & Sarkis, J. (2015). Carbon pricing versus

emissions trading: A supply chain planning perspective. International Journal of

Production Economics, 164, 197-205.

Zhang, B., & Xu, L. (2013). Multi-item production planning with carbon cap and trade

mechanism. International Journal of Production Economics, 144(1), 118-127.

Zhang, Y. J., Wang, A. D., & Tan, W. (2015). The impact of China's carbon allowance

allocation rules on the product prices and emission reduction behaviors of ETS-

covered enterprises. Energy Policy, 86, 176-185.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.