Corporate Accounting Report: Financial Analysis of Energy Companies

VerifiedAdded on 2020/10/05

|38

|6057

|214

Report

AI Summary

This report provides a comprehensive analysis of corporate accounting practices within the energy sector, focusing on three key companies: Horizon Oil Limited, Universal Coal Plc, and Beach Energy Limited. The report meticulously examines various aspects of their financial statements, beginning with an in-depth review of equity and liabilities, including changes over the past three years and their underlying causes, alongside a comparative analysis of debt-equity positions. It then delves into the cash flow statements, dissecting each item and offering a comparative analysis across the three companies, highlighting significant insights. The report further investigates the other comprehensive income statements, detailing the items included and excluded from the profit and loss statements, along with a comparative assessment of these items and a discussion on their relevance in evaluating managerial performance. Finally, the report addresses accounting for corporate income tax, calculating effective tax rates, commenting on deferred tax assets and liabilities, and analyzing the differences between cash tax and book tax rates, providing a holistic view of the financial performance and accounting practices of these energy companies.

CORPORATE ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Corporate accounting is referred as branch of accounting which deals with accounting on

basis of organization and for framing final accounts along with cash flow statements. The

present report will discuss about Horizon oil limited, Universal Coal Plc and Beach Energy

Limited company which comprises in energy sector. This report will reflect various information

on basis of other comprehensive income statements such as reason for not including these items

in income statement. Lastly, this report will state accounting for corporate income tax which

comprises effective tax rate, deferred tax asset and liability and difference among cash tax and

book tax rate. Thus, it had been evaluated that other comprehensive income should not be stated

in profit and loss statement as it could be used for elaborating manager's performance.

Corporate accounting is referred as branch of accounting which deals with accounting on

basis of organization and for framing final accounts along with cash flow statements. The

present report will discuss about Horizon oil limited, Universal Coal Plc and Beach Energy

Limited company which comprises in energy sector. This report will reflect various information

on basis of other comprehensive income statements such as reason for not including these items

in income statement. Lastly, this report will state accounting for corporate income tax which

comprises effective tax rate, deferred tax asset and liability and difference among cash tax and

book tax rate. Thus, it had been evaluated that other comprehensive income should not be stated

in profit and loss statement as it could be used for elaborating manager's performance.

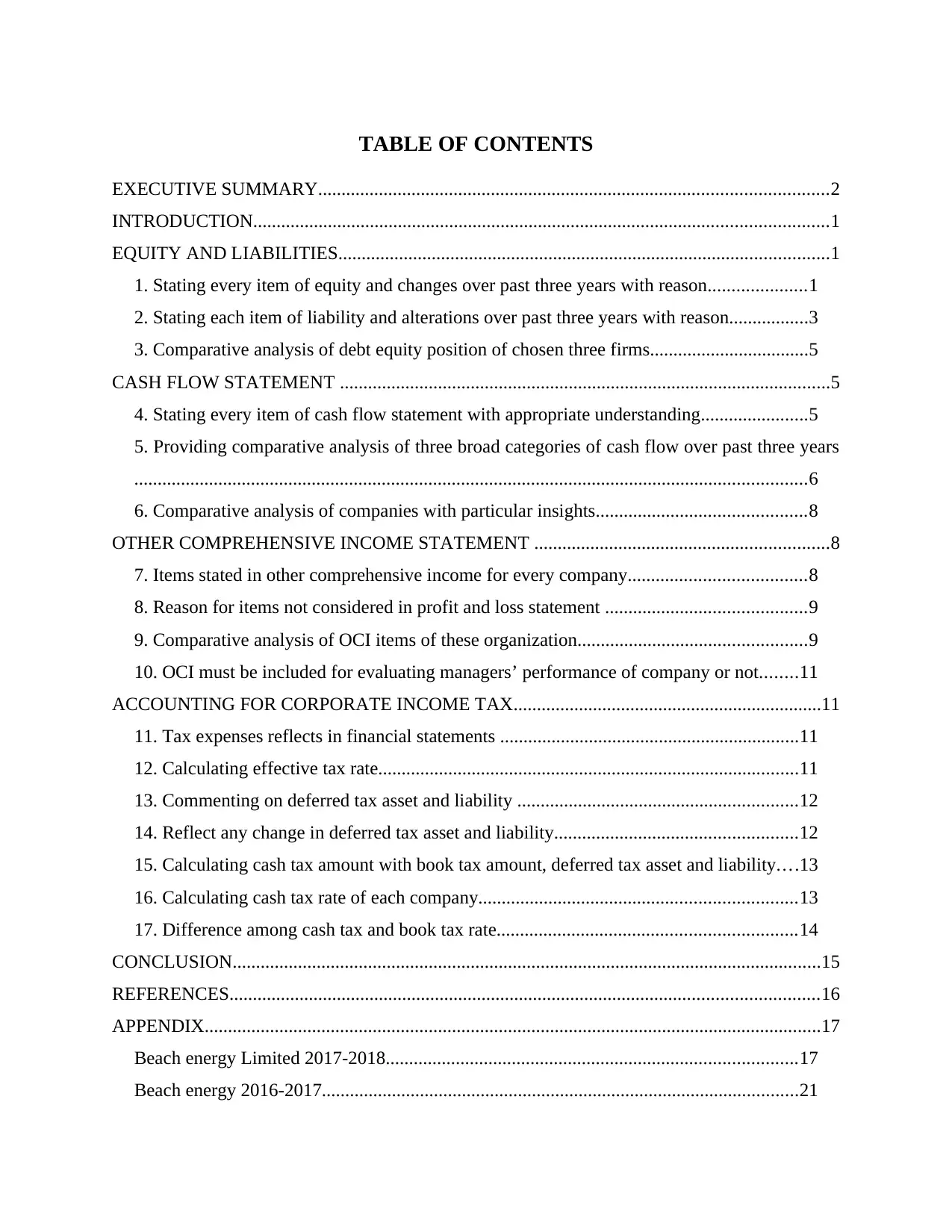

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

EQUITY AND LIABILITIES.........................................................................................................1

1. Stating every item of equity and changes over past three years with reason.....................1

2. Stating each item of liability and alterations over past three years with reason.................3

3. Comparative analysis of debt equity position of chosen three firms..................................5

CASH FLOW STATEMENT .........................................................................................................5

4. Stating every item of cash flow statement with appropriate understanding.......................5

5. Providing comparative analysis of three broad categories of cash flow over past three years

................................................................................................................................................6

6. Comparative analysis of companies with particular insights.............................................8

OTHER COMPREHENSIVE INCOME STATEMENT ...............................................................8

7. Items stated in other comprehensive income for every company......................................8

8. Reason for items not considered in profit and loss statement ...........................................9

9. Comparative analysis of OCI items of these organization.................................................9

10. OCI must be included for evaluating managers’ performance of company or not........11

ACCOUNTING FOR CORPORATE INCOME TAX..................................................................11

11. Tax expenses reflects in financial statements ................................................................11

12. Calculating effective tax rate..........................................................................................11

13. Commenting on deferred tax asset and liability ............................................................12

14. Reflect any change in deferred tax asset and liability....................................................12

15. Calculating cash tax amount with book tax amount, deferred tax asset and liability....13

16. Calculating cash tax rate of each company....................................................................13

17. Difference among cash tax and book tax rate................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

APPENDIX....................................................................................................................................17

Beach energy Limited 2017-2018........................................................................................17

Beach energy 2016-2017......................................................................................................21

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

EQUITY AND LIABILITIES.........................................................................................................1

1. Stating every item of equity and changes over past three years with reason.....................1

2. Stating each item of liability and alterations over past three years with reason.................3

3. Comparative analysis of debt equity position of chosen three firms..................................5

CASH FLOW STATEMENT .........................................................................................................5

4. Stating every item of cash flow statement with appropriate understanding.......................5

5. Providing comparative analysis of three broad categories of cash flow over past three years

................................................................................................................................................6

6. Comparative analysis of companies with particular insights.............................................8

OTHER COMPREHENSIVE INCOME STATEMENT ...............................................................8

7. Items stated in other comprehensive income for every company......................................8

8. Reason for items not considered in profit and loss statement ...........................................9

9. Comparative analysis of OCI items of these organization.................................................9

10. OCI must be included for evaluating managers’ performance of company or not........11

ACCOUNTING FOR CORPORATE INCOME TAX..................................................................11

11. Tax expenses reflects in financial statements ................................................................11

12. Calculating effective tax rate..........................................................................................11

13. Commenting on deferred tax asset and liability ............................................................12

14. Reflect any change in deferred tax asset and liability....................................................12

15. Calculating cash tax amount with book tax amount, deferred tax asset and liability....13

16. Calculating cash tax rate of each company....................................................................13

17. Difference among cash tax and book tax rate................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

APPENDIX....................................................................................................................................17

Beach energy Limited 2017-2018........................................................................................17

Beach energy 2016-2017......................................................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

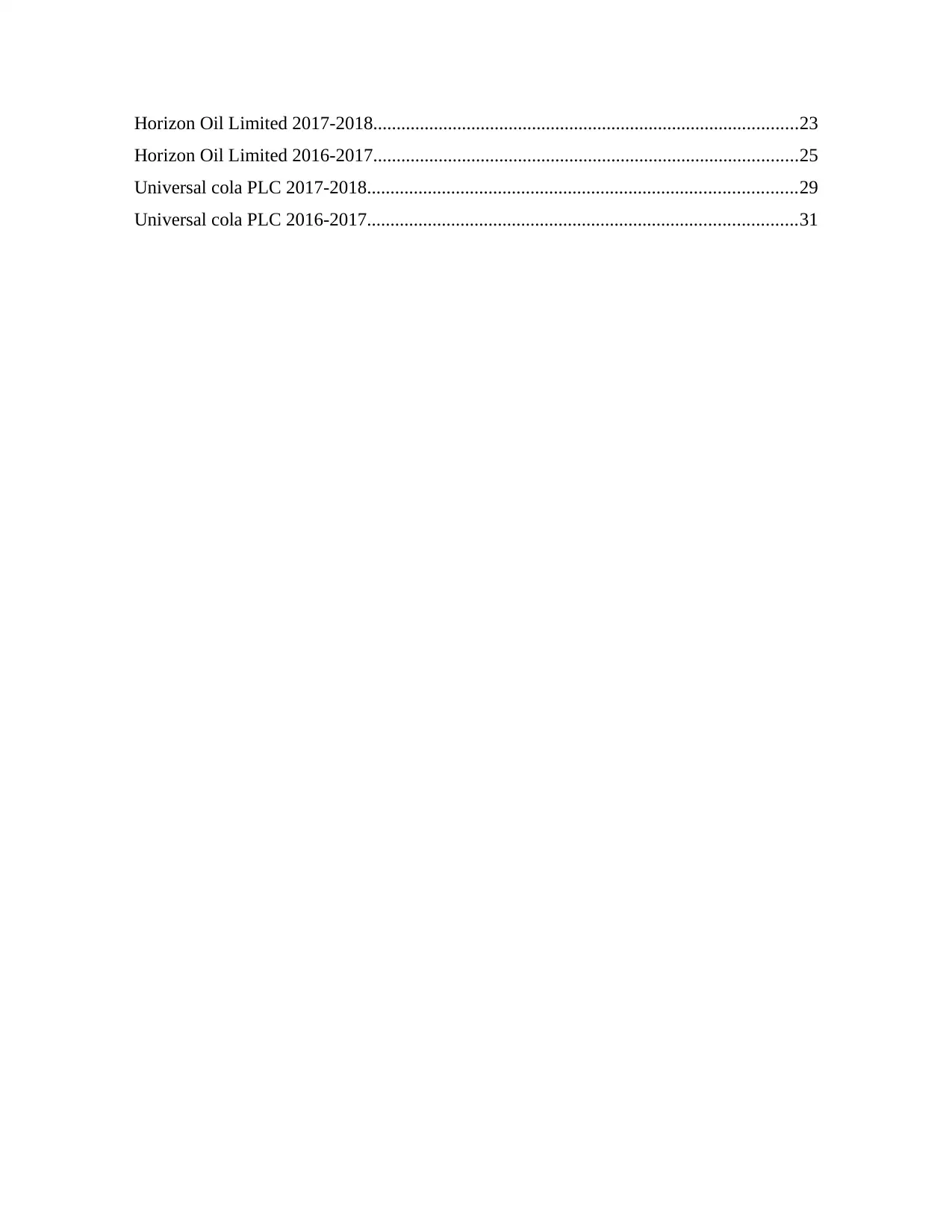

Horizon Oil Limited 2017-2018...........................................................................................23

Horizon Oil Limited 2016-2017...........................................................................................25

Universal cola PLC 2017-2018............................................................................................29

Universal cola PLC 2016-2017............................................................................................31

Horizon Oil Limited 2016-2017...........................................................................................25

Universal cola PLC 2017-2018............................................................................................29

Universal cola PLC 2016-2017............................................................................................31

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Corporate accounting is considered as branch of accounting which directly deals with

accounting with context of organization and to prepare final accounts along with cash flow

statements. In the similar aspect, it will analyse and interpret financial outcome of organization

and accounting with reference to some particular events like absorption, amalgamation and

preparation of consolidated financial statements. The present report will discuss about Horizon

oil limited, Universal Coal Plc and Beach Energy Limited company with various important

sections. At the initial stage, it will reflect every item of equity along with changes over past

three years with their reasons and comparative analysis of their debt equity position. In the

similar aspect, it will be stating every item of cash flow statement with three broad categories

and comparative analysis of these three companies. This report will reflect various information

on basis of other comprehensive income statements such as reason for not including these items

in income statement. Lastly, this report will state accounting for corporate income tax which

comprises effective tax rate, deferred tax ass

EQUITY AND LIABILITIES

1. Stating every item of equity and changes over past three years with reason

2016 2017

%

change

in 2017 2017 2018

%

change

in 2018

Universal coal Plc

Share capital 43374 44466 2.52% 44466 44466 0.00%

Reserves 2498 755 -69.78% 755 625 -17.22%

Retained earnings/

Accumulated losses -42183 15403

-

136.51% 15403 6863 -55.44%

Share premium 52941 0

-

100.00% 0 0 0.00%

Total equity 56630 60624 7.05% 60624 51954 -14.30%

The above change in equity has provided with shared capital, reserves, retained earnings,

and share premium. The share capital is the amount which is issued to the public. Moreover, the

reserves are the profit of the firm which are retained for the future use. Retained earning are

1

Corporate accounting is considered as branch of accounting which directly deals with

accounting with context of organization and to prepare final accounts along with cash flow

statements. In the similar aspect, it will analyse and interpret financial outcome of organization

and accounting with reference to some particular events like absorption, amalgamation and

preparation of consolidated financial statements. The present report will discuss about Horizon

oil limited, Universal Coal Plc and Beach Energy Limited company with various important

sections. At the initial stage, it will reflect every item of equity along with changes over past

three years with their reasons and comparative analysis of their debt equity position. In the

similar aspect, it will be stating every item of cash flow statement with three broad categories

and comparative analysis of these three companies. This report will reflect various information

on basis of other comprehensive income statements such as reason for not including these items

in income statement. Lastly, this report will state accounting for corporate income tax which

comprises effective tax rate, deferred tax ass

EQUITY AND LIABILITIES

1. Stating every item of equity and changes over past three years with reason

2016 2017

%

change

in 2017 2017 2018

%

change

in 2018

Universal coal Plc

Share capital 43374 44466 2.52% 44466 44466 0.00%

Reserves 2498 755 -69.78% 755 625 -17.22%

Retained earnings/

Accumulated losses -42183 15403

-

136.51% 15403 6863 -55.44%

Share premium 52941 0

-

100.00% 0 0 0.00%

Total equity 56630 60624 7.05% 60624 51954 -14.30%

The above change in equity has provided with shared capital, reserves, retained earnings,

and share premium. The share capital is the amount which is issued to the public. Moreover, the

reserves are the profit of the firm which are retained for the future use. Retained earning are

1

those which are used in business activities rather than providing as the divided to the

shareholders. Share premium is the amount received by the company which exceeds the face

value of the shares.

From the above table it is to be analyzed that in 2017, Universal coal Plc has reduced their

reserves with -69.78% and increased their share premium with 100.00%. In 2018, again

company reduced their reserves and share premium with -17.22 and 0.00%. Because of this there

is a change in equity with 7.05% in 2017 and -14.30% in 2018. Therefore, in order to generate

return on equity company have to use more financial leverages where company finance

themselves with debt and equity capital. Effective dividend policy also helps in gaining return in

equity.

2016 2017

%

change

in 2017 2017 2018

%

change

in 2018

Horizon oil Limited

Contributed equity 174801 174801 0.00% 174801 174801 0.00%

Reserves 12030 14558 21.01% 14558 5740 -60.57%

Accumulated losses (82217) (82633) 0.51% (82633) (85232) 3.15%

Non controlling interest 80 0

-

100.00% 0 0 0.00%

Total equity 104534 106726 2.10% 106726 95309 -10.70%

It can be interpretate from above table that in 2017, Horizon Oil Ltd. Increased their

reserves and non controlling interest with 21.01% and with 100.00%. In 2018, company have

reduced their reserve and non controlling interest with -60.57% and 0.00%. Because of this

change, in 2017 change in equity is 2.10% and in 2018, it is -10.70% Major effect on change in

equity is because of its non controlling interest by which its total equity reduced. With this

statement it can be analyzed that owner's needs to work upon its strategies like effective dividend

policy, increase of profit margin which helps in improving change in equity.

2016 2017 % 2017 2018 %

2

shareholders. Share premium is the amount received by the company which exceeds the face

value of the shares.

From the above table it is to be analyzed that in 2017, Universal coal Plc has reduced their

reserves with -69.78% and increased their share premium with 100.00%. In 2018, again

company reduced their reserves and share premium with -17.22 and 0.00%. Because of this there

is a change in equity with 7.05% in 2017 and -14.30% in 2018. Therefore, in order to generate

return on equity company have to use more financial leverages where company finance

themselves with debt and equity capital. Effective dividend policy also helps in gaining return in

equity.

2016 2017

%

change

in 2017 2017 2018

%

change

in 2018

Horizon oil Limited

Contributed equity 174801 174801 0.00% 174801 174801 0.00%

Reserves 12030 14558 21.01% 14558 5740 -60.57%

Accumulated losses (82217) (82633) 0.51% (82633) (85232) 3.15%

Non controlling interest 80 0

-

100.00% 0 0 0.00%

Total equity 104534 106726 2.10% 106726 95309 -10.70%

It can be interpretate from above table that in 2017, Horizon Oil Ltd. Increased their

reserves and non controlling interest with 21.01% and with 100.00%. In 2018, company have

reduced their reserve and non controlling interest with -60.57% and 0.00%. Because of this

change, in 2017 change in equity is 2.10% and in 2018, it is -10.70% Major effect on change in

equity is because of its non controlling interest by which its total equity reduced. With this

statement it can be analyzed that owner's needs to work upon its strategies like effective dividend

policy, increase of profit margin which helps in improving change in equity.

2016 2017 % 2017 2018 %

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

change

in 2017

change

in 2018

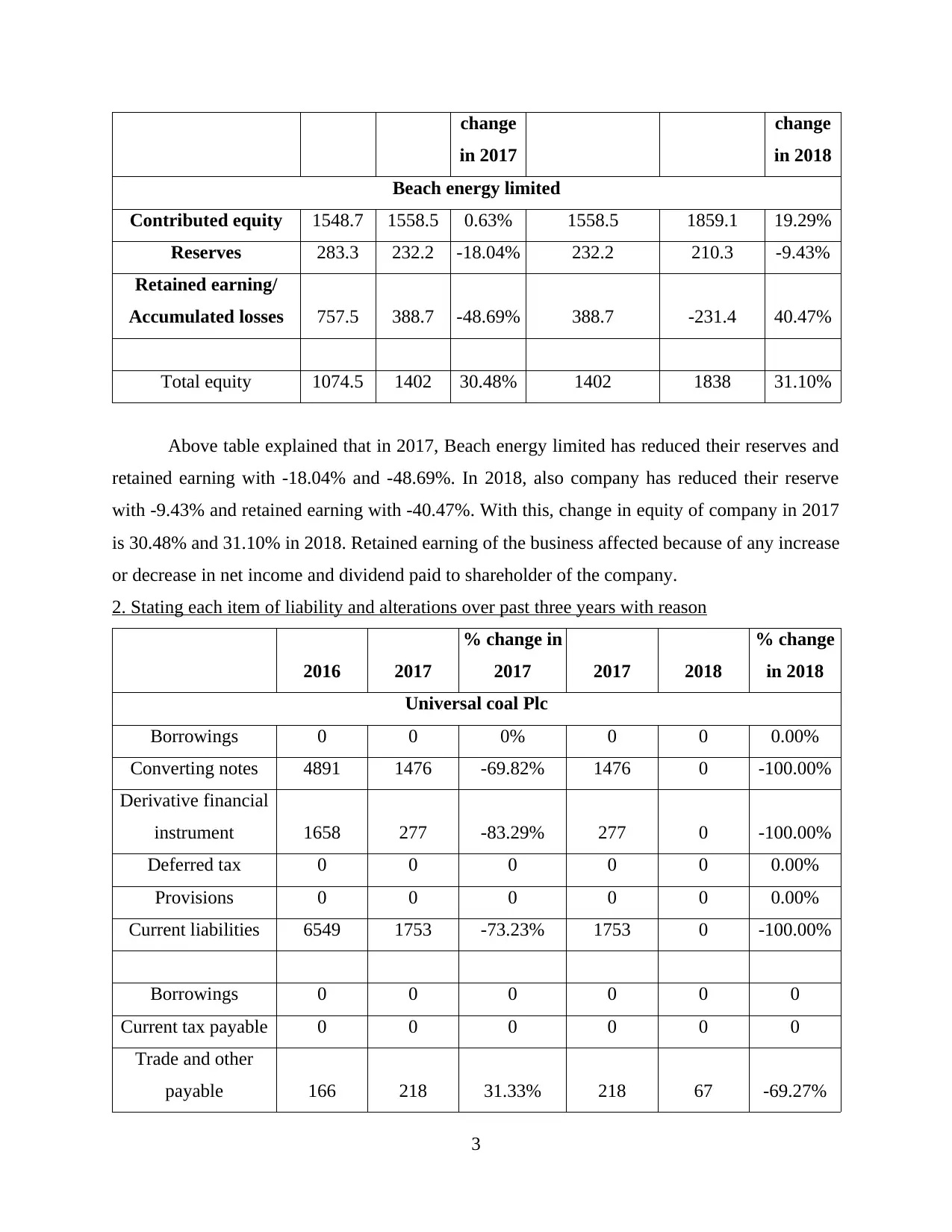

Beach energy limited

Contributed equity 1548.7 1558.5 0.63% 1558.5 1859.1 19.29%

Reserves 283.3 232.2 -18.04% 232.2 210.3 -9.43%

Retained earning/

Accumulated losses 757.5 388.7 -48.69% 388.7 -231.4 40.47%

Total equity 1074.5 1402 30.48% 1402 1838 31.10%

Above table explained that in 2017, Beach energy limited has reduced their reserves and

retained earning with -18.04% and -48.69%. In 2018, also company has reduced their reserve

with -9.43% and retained earning with -40.47%. With this, change in equity of company in 2017

is 30.48% and 31.10% in 2018. Retained earning of the business affected because of any increase

or decrease in net income and dividend paid to shareholder of the company.

2. Stating each item of liability and alterations over past three years with reason

2016 2017

% change in

2017 2017 2018

% change

in 2018

Universal coal Plc

Borrowings 0 0 0% 0 0 0.00%

Converting notes 4891 1476 -69.82% 1476 0 -100.00%

Derivative financial

instrument 1658 277 -83.29% 277 0 -100.00%

Deferred tax 0 0 0 0 0 0.00%

Provisions 0 0 0 0 0 0.00%

Current liabilities 6549 1753 -73.23% 1753 0 -100.00%

Borrowings 0 0 0 0 0 0

Current tax payable 0 0 0 0 0 0

Trade and other

payable 166 218 31.33% 218 67 -69.27%

3

in 2017

change

in 2018

Beach energy limited

Contributed equity 1548.7 1558.5 0.63% 1558.5 1859.1 19.29%

Reserves 283.3 232.2 -18.04% 232.2 210.3 -9.43%

Retained earning/

Accumulated losses 757.5 388.7 -48.69% 388.7 -231.4 40.47%

Total equity 1074.5 1402 30.48% 1402 1838 31.10%

Above table explained that in 2017, Beach energy limited has reduced their reserves and

retained earning with -18.04% and -48.69%. In 2018, also company has reduced their reserve

with -9.43% and retained earning with -40.47%. With this, change in equity of company in 2017

is 30.48% and 31.10% in 2018. Retained earning of the business affected because of any increase

or decrease in net income and dividend paid to shareholder of the company.

2. Stating each item of liability and alterations over past three years with reason

2016 2017

% change in

2017 2017 2018

% change

in 2018

Universal coal Plc

Borrowings 0 0 0% 0 0 0.00%

Converting notes 4891 1476 -69.82% 1476 0 -100.00%

Derivative financial

instrument 1658 277 -83.29% 277 0 -100.00%

Deferred tax 0 0 0 0 0 0.00%

Provisions 0 0 0 0 0 0.00%

Current liabilities 6549 1753 -73.23% 1753 0 -100.00%

Borrowings 0 0 0 0 0 0

Current tax payable 0 0 0 0 0 0

Trade and other

payable 166 218 31.33% 218 67 -69.27%

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

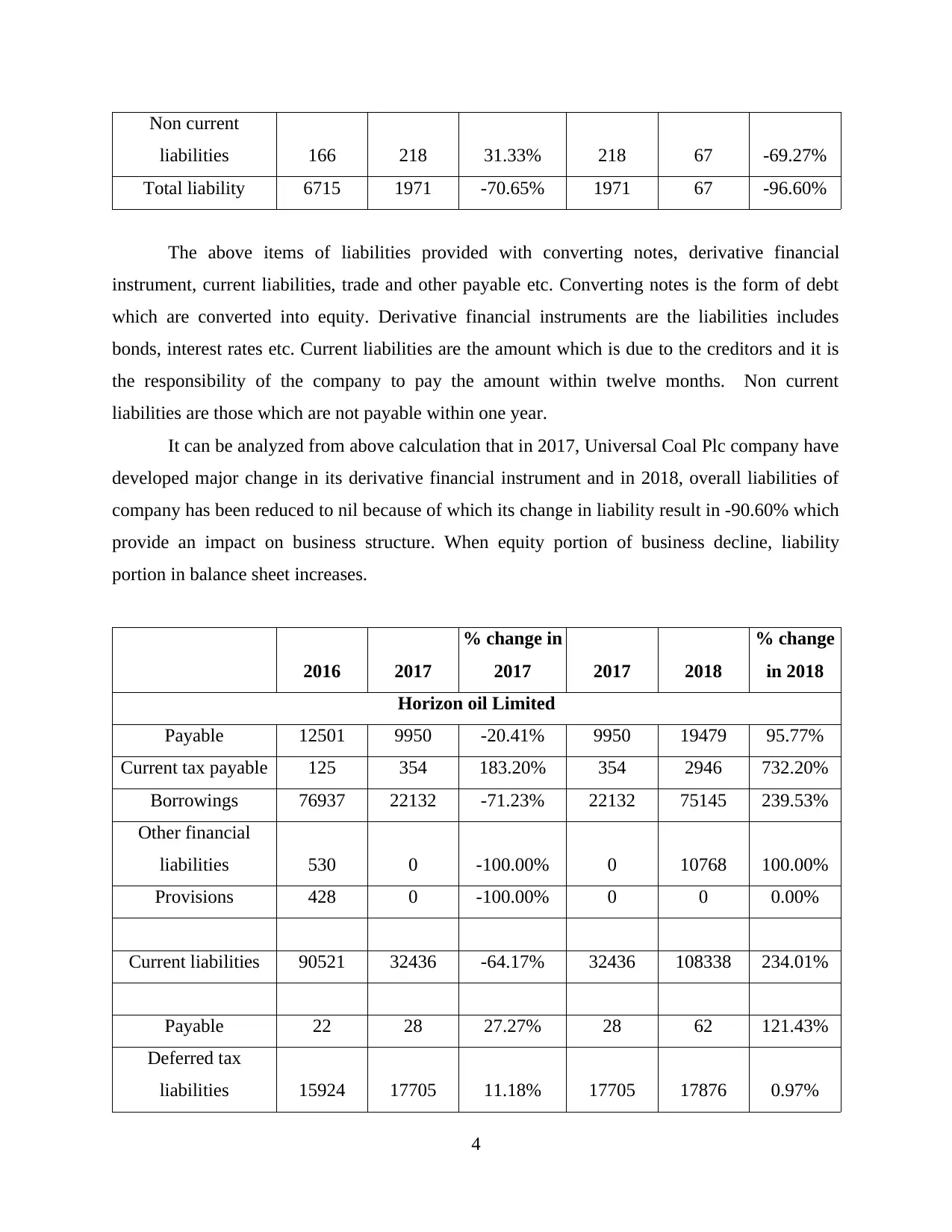

Non current

liabilities 166 218 31.33% 218 67 -69.27%

Total liability 6715 1971 -70.65% 1971 67 -96.60%

The above items of liabilities provided with converting notes, derivative financial

instrument, current liabilities, trade and other payable etc. Converting notes is the form of debt

which are converted into equity. Derivative financial instruments are the liabilities includes

bonds, interest rates etc. Current liabilities are the amount which is due to the creditors and it is

the responsibility of the company to pay the amount within twelve months. Non current

liabilities are those which are not payable within one year.

It can be analyzed from above calculation that in 2017, Universal Coal Plc company have

developed major change in its derivative financial instrument and in 2018, overall liabilities of

company has been reduced to nil because of which its change in liability result in -90.60% which

provide an impact on business structure. When equity portion of business decline, liability

portion in balance sheet increases.

2016 2017

% change in

2017 2017 2018

% change

in 2018

Horizon oil Limited

Payable 12501 9950 -20.41% 9950 19479 95.77%

Current tax payable 125 354 183.20% 354 2946 732.20%

Borrowings 76937 22132 -71.23% 22132 75145 239.53%

Other financial

liabilities 530 0 -100.00% 0 10768 100.00%

Provisions 428 0 -100.00% 0 0 0.00%

Current liabilities 90521 32436 -64.17% 32436 108338 234.01%

Payable 22 28 27.27% 28 62 121.43%

Deferred tax

liabilities 15924 17705 11.18% 17705 17876 0.97%

4

liabilities 166 218 31.33% 218 67 -69.27%

Total liability 6715 1971 -70.65% 1971 67 -96.60%

The above items of liabilities provided with converting notes, derivative financial

instrument, current liabilities, trade and other payable etc. Converting notes is the form of debt

which are converted into equity. Derivative financial instruments are the liabilities includes

bonds, interest rates etc. Current liabilities are the amount which is due to the creditors and it is

the responsibility of the company to pay the amount within twelve months. Non current

liabilities are those which are not payable within one year.

It can be analyzed from above calculation that in 2017, Universal Coal Plc company have

developed major change in its derivative financial instrument and in 2018, overall liabilities of

company has been reduced to nil because of which its change in liability result in -90.60% which

provide an impact on business structure. When equity portion of business decline, liability

portion in balance sheet increases.

2016 2017

% change in

2017 2017 2018

% change

in 2018

Horizon oil Limited

Payable 12501 9950 -20.41% 9950 19479 95.77%

Current tax payable 125 354 183.20% 354 2946 732.20%

Borrowings 76937 22132 -71.23% 22132 75145 239.53%

Other financial

liabilities 530 0 -100.00% 0 10768 100.00%

Provisions 428 0 -100.00% 0 0 0.00%

Current liabilities 90521 32436 -64.17% 32436 108338 234.01%

Payable 22 28 27.27% 28 62 121.43%

Deferred tax

liabilities 15924 17705 11.18% 17705 17876 0.97%

4

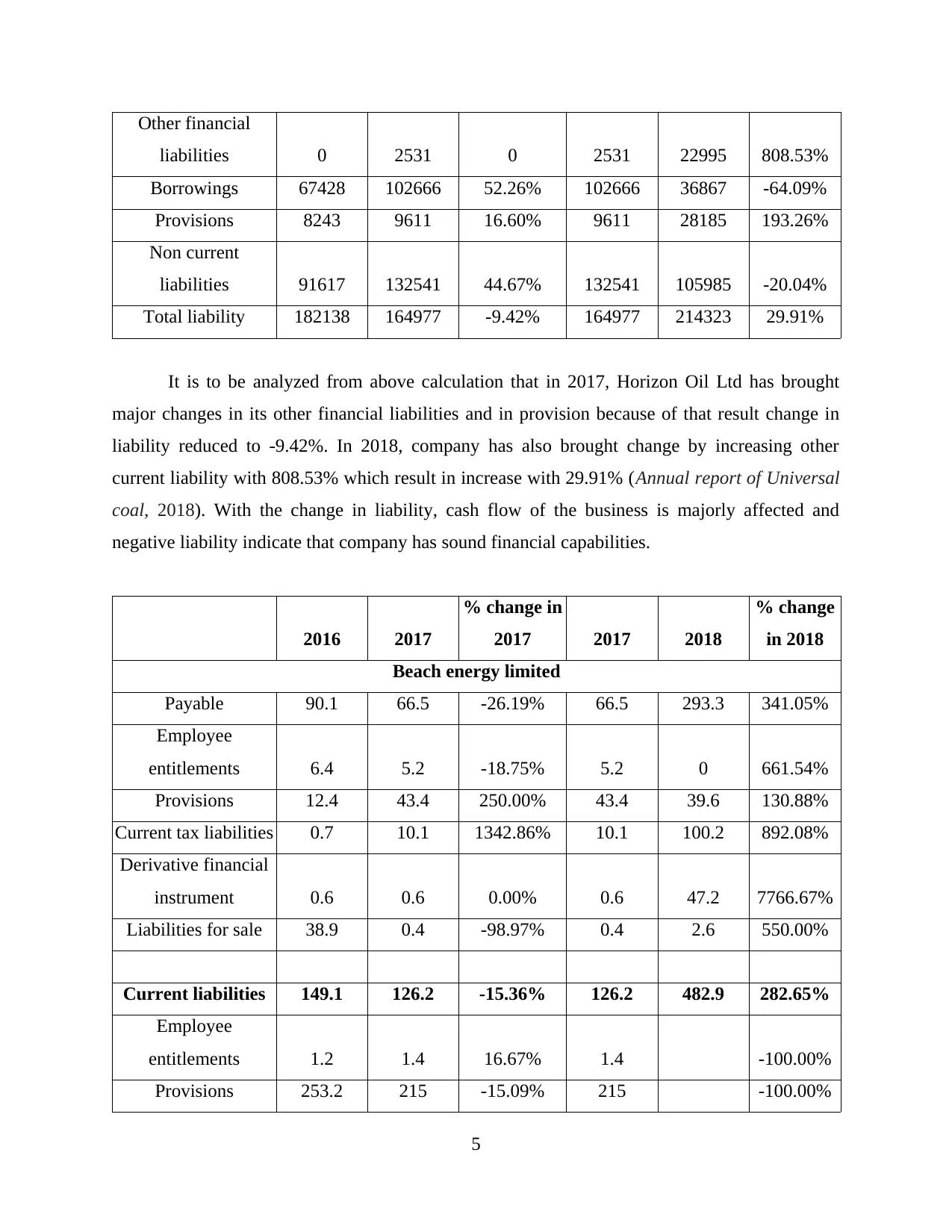

Other financial

liabilities 0 2531 0 2531 22995 808.53%

Borrowings 67428 102666 52.26% 102666 36867 -64.09%

Provisions 8243 9611 16.60% 9611 28185 193.26%

Non current

liabilities 91617 132541 44.67% 132541 105985 -20.04%

Total liability 182138 164977 -9.42% 164977 214323 29.91%

It is to be analyzed from above calculation that in 2017, Horizon Oil Ltd has brought

major changes in its other financial liabilities and in provision because of that result change in

liability reduced to -9.42%. In 2018, company has also brought change by increasing other

current liability with 808.53% which result in increase with 29.91% (Annual report of Universal

coal, 2018). With the change in liability, cash flow of the business is majorly affected and

negative liability indicate that company has sound financial capabilities.

2016 2017

% change in

2017 2017 2018

% change

in 2018

Beach energy limited

Payable 90.1 66.5 -26.19% 66.5 293.3 341.05%

Employee

entitlements 6.4 5.2 -18.75% 5.2 0 661.54%

Provisions 12.4 43.4 250.00% 43.4 39.6 130.88%

Current tax liabilities 0.7 10.1 1342.86% 10.1 100.2 892.08%

Derivative financial

instrument 0.6 0.6 0.00% 0.6 47.2 7766.67%

Liabilities for sale 38.9 0.4 -98.97% 0.4 2.6 550.00%

Current liabilities 149.1 126.2 -15.36% 126.2 482.9 282.65%

Employee

entitlements 1.2 1.4 16.67% 1.4 -100.00%

Provisions 253.2 215 -15.09% 215 -100.00%

5

liabilities 0 2531 0 2531 22995 808.53%

Borrowings 67428 102666 52.26% 102666 36867 -64.09%

Provisions 8243 9611 16.60% 9611 28185 193.26%

Non current

liabilities 91617 132541 44.67% 132541 105985 -20.04%

Total liability 182138 164977 -9.42% 164977 214323 29.91%

It is to be analyzed from above calculation that in 2017, Horizon Oil Ltd has brought

major changes in its other financial liabilities and in provision because of that result change in

liability reduced to -9.42%. In 2018, company has also brought change by increasing other

current liability with 808.53% which result in increase with 29.91% (Annual report of Universal

coal, 2018). With the change in liability, cash flow of the business is majorly affected and

negative liability indicate that company has sound financial capabilities.

2016 2017

% change in

2017 2017 2018

% change

in 2018

Beach energy limited

Payable 90.1 66.5 -26.19% 66.5 293.3 341.05%

Employee

entitlements 6.4 5.2 -18.75% 5.2 0 661.54%

Provisions 12.4 43.4 250.00% 43.4 39.6 130.88%

Current tax liabilities 0.7 10.1 1342.86% 10.1 100.2 892.08%

Derivative financial

instrument 0.6 0.6 0.00% 0.6 47.2 7766.67%

Liabilities for sale 38.9 0.4 -98.97% 0.4 2.6 550.00%

Current liabilities 149.1 126.2 -15.36% 126.2 482.9 282.65%

Employee

entitlements 1.2 1.4 16.67% 1.4 -100.00%

Provisions 253.2 215 -15.09% 215 -100.00%

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

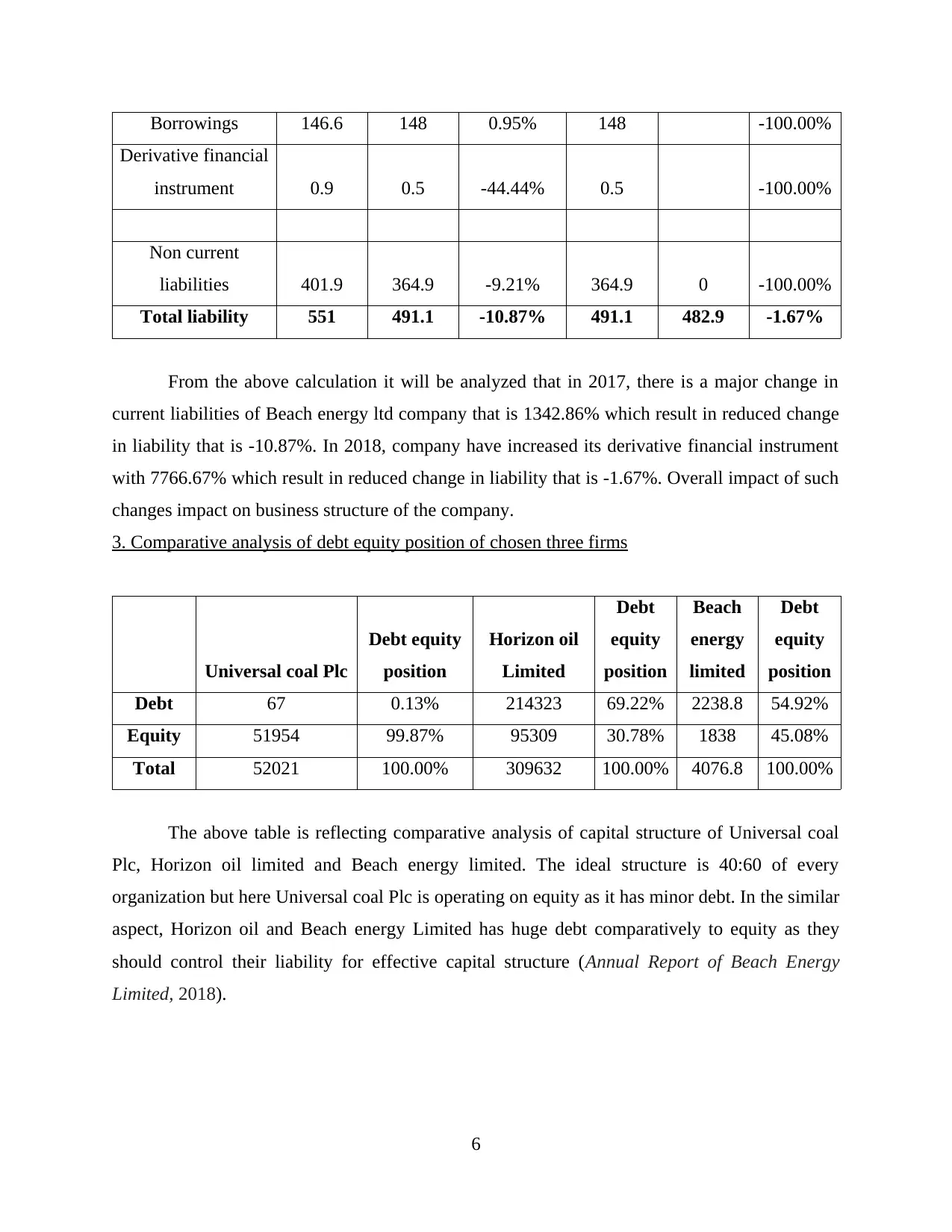

Borrowings 146.6 148 0.95% 148 -100.00%

Derivative financial

instrument 0.9 0.5 -44.44% 0.5 -100.00%

Non current

liabilities 401.9 364.9 -9.21% 364.9 0 -100.00%

Total liability 551 491.1 -10.87% 491.1 482.9 -1.67%

From the above calculation it will be analyzed that in 2017, there is a major change in

current liabilities of Beach energy ltd company that is 1342.86% which result in reduced change

in liability that is -10.87%. In 2018, company have increased its derivative financial instrument

with 7766.67% which result in reduced change in liability that is -1.67%. Overall impact of such

changes impact on business structure of the company.

3. Comparative analysis of debt equity position of chosen three firms

Universal coal Plc

Debt equity

position

Horizon oil

Limited

Debt

equity

position

Beach

energy

limited

Debt

equity

position

Debt 67 0.13% 214323 69.22% 2238.8 54.92%

Equity 51954 99.87% 95309 30.78% 1838 45.08%

Total 52021 100.00% 309632 100.00% 4076.8 100.00%

The above table is reflecting comparative analysis of capital structure of Universal coal

Plc, Horizon oil limited and Beach energy limited. The ideal structure is 40:60 of every

organization but here Universal coal Plc is operating on equity as it has minor debt. In the similar

aspect, Horizon oil and Beach energy Limited has huge debt comparatively to equity as they

should control their liability for effective capital structure (Annual Report of Beach Energy

Limited, 2018).

6

Derivative financial

instrument 0.9 0.5 -44.44% 0.5 -100.00%

Non current

liabilities 401.9 364.9 -9.21% 364.9 0 -100.00%

Total liability 551 491.1 -10.87% 491.1 482.9 -1.67%

From the above calculation it will be analyzed that in 2017, there is a major change in

current liabilities of Beach energy ltd company that is 1342.86% which result in reduced change

in liability that is -10.87%. In 2018, company have increased its derivative financial instrument

with 7766.67% which result in reduced change in liability that is -1.67%. Overall impact of such

changes impact on business structure of the company.

3. Comparative analysis of debt equity position of chosen three firms

Universal coal Plc

Debt equity

position

Horizon oil

Limited

Debt

equity

position

Beach

energy

limited

Debt

equity

position

Debt 67 0.13% 214323 69.22% 2238.8 54.92%

Equity 51954 99.87% 95309 30.78% 1838 45.08%

Total 52021 100.00% 309632 100.00% 4076.8 100.00%

The above table is reflecting comparative analysis of capital structure of Universal coal

Plc, Horizon oil limited and Beach energy limited. The ideal structure is 40:60 of every

organization but here Universal coal Plc is operating on equity as it has minor debt. In the similar

aspect, Horizon oil and Beach energy Limited has huge debt comparatively to equity as they

should control their liability for effective capital structure (Annual Report of Beach Energy

Limited, 2018).

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CASH FLOW STATEMENT

4. Stating every item of cash flow statement with appropriate understanding

Cash flow statement comprises three broad categories such as operating, investing

and financing activities (Jackson, 2015). This statement reflects cash position of organization in

actual manner. The first category changes in operating assets and liabilities are adjusted as they

reflect conversion of liabilities or assets to cash flow which is derived through income items

prior to reporting period.

Universal coal: In operating activities it comprises cash utilised from operations and tax

paid. With context of investing activities, it includes acquisition of plant, property, equipment

and other intangible assets. There is also consideration purchase, sale, loans related to parties and

finance income. The activity of investment is not referred as operational transaction and should

be adjusted for cash flow on basis of investments. Lastly in its financing activities drawdown

through investec project finance facility, shareholder loan repayment, dividend paid and all

finance expense.

Universal coal Plc: There is consideration of receipts through customers, payment to

employees and suppliers, income tax paid and interest received and paid for generating cash

through operating activities. On basis of investing activities it comprises payments for oil and

gas assets, plant and equipment and exploration for oil and gas assets. Lastly, with financing

activities it comprises proceeds and repayment of borrowings.

Beach energy Limited: The operating activities was raising due to huge change in

proportion of receipts through customers and payment to its employees and supplies in Beach

energy Limited. The major change is because of huge payments for acquisition of its joint

operations and subsidiaries along with acquired net cash. The investing activities are payments

for property, equipment, plant along with proceeds from government grants as well. It also

considers sale of subsidiary and proceeds through sales of equity investments and non current

assets as well. Simultaneously, financing activities includes costs associated with issuance of

shares, repayment of borrowings, debt facility establishments cost and payment of dividend as

well. The business would issue stock or debt for raising cash and source of fund as debt

retirement and repurchases of stock would be considered as cash reduction.

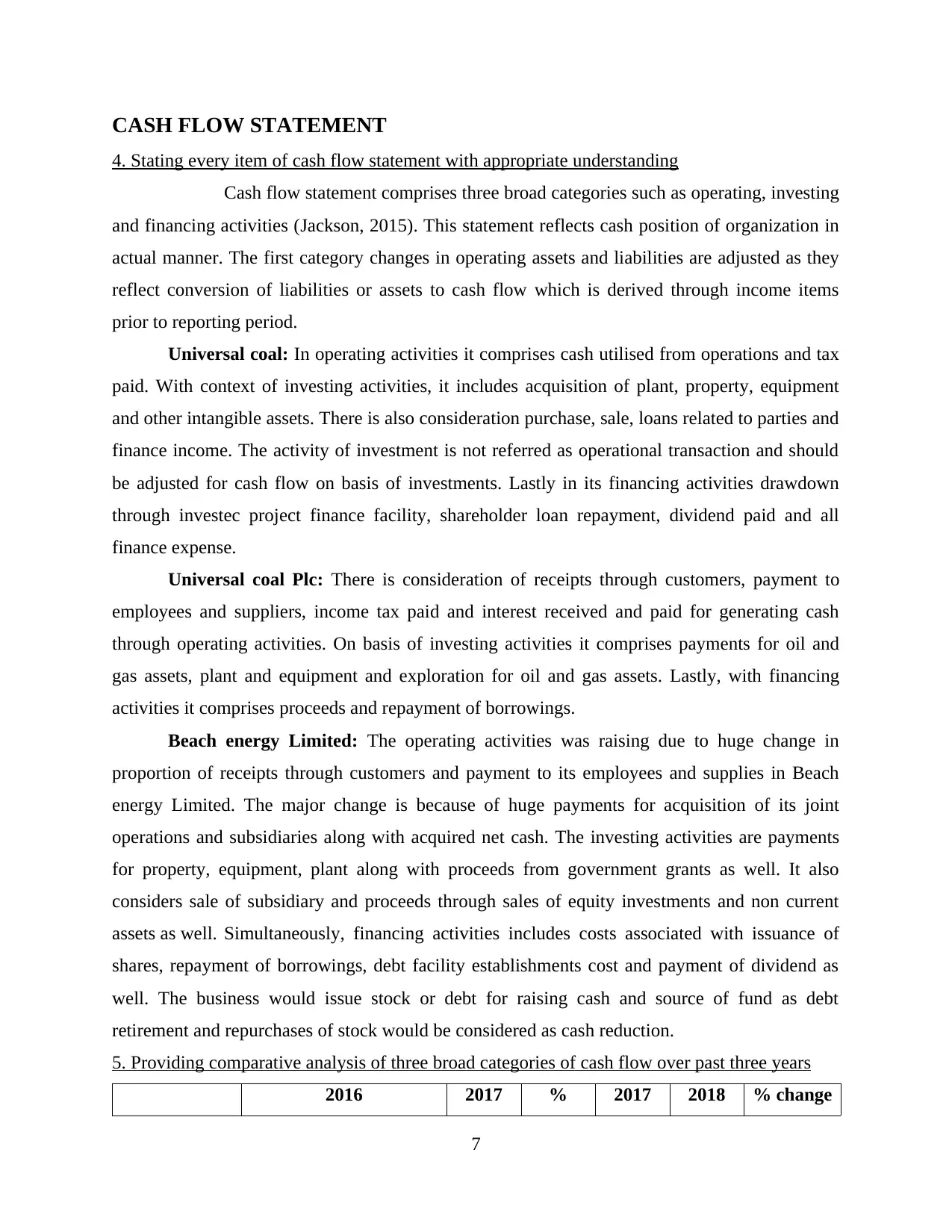

5. Providing comparative analysis of three broad categories of cash flow over past three years

2016 2017 % 2017 2018 % change

7

4. Stating every item of cash flow statement with appropriate understanding

Cash flow statement comprises three broad categories such as operating, investing

and financing activities (Jackson, 2015). This statement reflects cash position of organization in

actual manner. The first category changes in operating assets and liabilities are adjusted as they

reflect conversion of liabilities or assets to cash flow which is derived through income items

prior to reporting period.

Universal coal: In operating activities it comprises cash utilised from operations and tax

paid. With context of investing activities, it includes acquisition of plant, property, equipment

and other intangible assets. There is also consideration purchase, sale, loans related to parties and

finance income. The activity of investment is not referred as operational transaction and should

be adjusted for cash flow on basis of investments. Lastly in its financing activities drawdown

through investec project finance facility, shareholder loan repayment, dividend paid and all

finance expense.

Universal coal Plc: There is consideration of receipts through customers, payment to

employees and suppliers, income tax paid and interest received and paid for generating cash

through operating activities. On basis of investing activities it comprises payments for oil and

gas assets, plant and equipment and exploration for oil and gas assets. Lastly, with financing

activities it comprises proceeds and repayment of borrowings.

Beach energy Limited: The operating activities was raising due to huge change in

proportion of receipts through customers and payment to its employees and supplies in Beach

energy Limited. The major change is because of huge payments for acquisition of its joint

operations and subsidiaries along with acquired net cash. The investing activities are payments

for property, equipment, plant along with proceeds from government grants as well. It also

considers sale of subsidiary and proceeds through sales of equity investments and non current

assets as well. Simultaneously, financing activities includes costs associated with issuance of

shares, repayment of borrowings, debt facility establishments cost and payment of dividend as

well. The business would issue stock or debt for raising cash and source of fund as debt

retirement and repurchases of stock would be considered as cash reduction.

5. Providing comparative analysis of three broad categories of cash flow over past three years

2016 2017 % 2017 2018 % change

7

change

in 2017 in 2018

Universal coal Plc

Net cash flow

from operating

activities 5375 507 -90.57% -507 155 -130.57%

Net cash flow in

investing

activities 6185 2987 -51.71% 2987 13896 365.22%

Net cash flow in

financing

activities 1357 2328 71.55% 2328 12482 436.17%

Net cash -547 1166

-

313.16% 152 1569 932.24%

2016 2017

%

change

in 2017 2017 2018

% change

in 2018

Horizon oil Limited

Net cash flow

from operating

activities 84553 109722 29.77% 109722 144976 32.13%

Net cash flow in

investing

activities 15046 148298 885.63% 148298 52517 -64.59%

Net cash flow in

financing

activities 55749 18656 -66.54% 18656 99247 431.98%

Net cash 13758 -19920

-

244.79% -19920 -6788 -65.92%

8

in 2017 in 2018

Universal coal Plc

Net cash flow

from operating

activities 5375 507 -90.57% -507 155 -130.57%

Net cash flow in

investing

activities 6185 2987 -51.71% 2987 13896 365.22%

Net cash flow in

financing

activities 1357 2328 71.55% 2328 12482 436.17%

Net cash -547 1166

-

313.16% 152 1569 932.24%

2016 2017

%

change

in 2017 2017 2018

% change

in 2018

Horizon oil Limited

Net cash flow

from operating

activities 84553 109722 29.77% 109722 144976 32.13%

Net cash flow in

investing

activities 15046 148298 885.63% 148298 52517 -64.59%

Net cash flow in

financing

activities 55749 18656 -66.54% 18656 99247 431.98%

Net cash 13758 -19920

-

244.79% -19920 -6788 -65.92%

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 38

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.