Corporate & Financial Accounting: Equity, Debt & Regulations

VerifiedAdded on 2023/06/05

|15

|3057

|120

Report

AI Summary

This report assesses various aspects of financial reporting to help investors understand a company's financial standing. It discusses the importance of owners’ equity and analyzes the debt and equity positions of four selected firms to identify changes made to maintain competitiveness. The report also examines corporate regulations, including whether financial reporting should be regulated or left to managers' discretion, and the role of the Australian Accounting Standards Board (AASB) in global accounting standards, explaining why IFRS is not mandatory for IASB member countries. The analysis includes a detailed look at equity items for the selected firms and a comparative evaluation of their debt and equity positions to understand their current financial health.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate and Financial Accounting

Name of the Student:

Name of the University:

Authors Note:

Corporate and Financial Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE AND FINANCIAL ACCOUNTING

1

Executive Summary:

The assessment evaluates different segments of financial reports, which can allow the

investor to understand the current financial position of the organisation. The significance of

owners’ equity is also discussed, where the current financial position of the organisation can

be used for detecting the level of changes in their current positions. The comparative analysis

is been conducted on four of the selected firms by analysing the debt and equity position of

the organisation. This analysis helps in detecting the relevant changes, which has been

conducted by the companies for continuing the operating in the competitive market.

1

Executive Summary:

The assessment evaluates different segments of financial reports, which can allow the

investor to understand the current financial position of the organisation. The significance of

owners’ equity is also discussed, where the current financial position of the organisation can

be used for detecting the level of changes in their current positions. The comparative analysis

is been conducted on four of the selected firms by analysing the debt and equity position of

the organisation. This analysis helps in detecting the relevant changes, which has been

conducted by the companies for continuing the operating in the competitive market.

CORPORATE AND FINANCIAL ACCOUNTING

2

Table of Contents

Introduction:...............................................................................................................................3

Corporate Regulations:...............................................................................................................3

i) Critically discussing whether financial reporting needs to be regulated or managers should

be allowed to disclose the information voluntarily:...................................................................3

Accounting Standard Setting:....................................................................................................5

ii) Crucially examining the AASB in taking part with the global accounting standards setting

process, while depicting why IFRS is not compulsory for members of the IASB countries:....5

Owners’ Equity:.........................................................................................................................6

iii) Listing each items of equity for the selected firms, while discussing the changes in each

item:............................................................................................................................................6

iv) Providing a comparative analysis of the debt and equity position of the four firms that

have been selected:.....................................................................................................................9

Conclusion:..............................................................................................................................10

References and Bibliography:..................................................................................................12

2

Table of Contents

Introduction:...............................................................................................................................3

Corporate Regulations:...............................................................................................................3

i) Critically discussing whether financial reporting needs to be regulated or managers should

be allowed to disclose the information voluntarily:...................................................................3

Accounting Standard Setting:....................................................................................................5

ii) Crucially examining the AASB in taking part with the global accounting standards setting

process, while depicting why IFRS is not compulsory for members of the IASB countries:....5

Owners’ Equity:.........................................................................................................................6

iii) Listing each items of equity for the selected firms, while discussing the changes in each

item:............................................................................................................................................6

iv) Providing a comparative analysis of the debt and equity position of the four firms that

have been selected:.....................................................................................................................9

Conclusion:..............................................................................................................................10

References and Bibliography:..................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE AND FINANCIAL ACCOUNTING

3

Introduction:

The assessment aims in detecting the presence of corporate regulations, accounting

standard settings and owners’ equity. The evaluation directly helps in understanding the

significance of financial accounting and reporting, which needs to be conducted by the

organisation over the period of time. In addition, the need for the financial reports to be

regulated or the mangers can disclose the reports in accordance with their requirements.

Further evaluations are also conducted in the assessment that the IFRS settings proposed by

the IASB is not compulsory for members countries. The relevant evaluation of equity

selection has been conducted for understanding the financial performance of the selected four

companies. Hence, the debt and equity position of the companies are comparatively evaluated

to understand their current financial position.

Corporate Regulations:

i) Critically discussing whether financial reporting needs to be regulated or managers

should be allowed to disclose the information voluntarily:

The financial reporting system needs to be regulated with adequate measures and

standards, as it allows the stakeholders of the organisation for detecting the accurate financial

position of the organisation. The regulated financial reporting subsystem will ensure the

stakeholders about the correct financial position of the organisation and detect the measures,

which has been taken by the management for securing their future operations. In addition, the

financial reporting system helps in understanding the accurate operational details of the

organisation and the growth, which has been obtained over the past fiscal years. Dumay

(2016) mentioned that the presence of scandal and misleading reports conducted by

3

Introduction:

The assessment aims in detecting the presence of corporate regulations, accounting

standard settings and owners’ equity. The evaluation directly helps in understanding the

significance of financial accounting and reporting, which needs to be conducted by the

organisation over the period of time. In addition, the need for the financial reports to be

regulated or the mangers can disclose the reports in accordance with their requirements.

Further evaluations are also conducted in the assessment that the IFRS settings proposed by

the IASB is not compulsory for members countries. The relevant evaluation of equity

selection has been conducted for understanding the financial performance of the selected four

companies. Hence, the debt and equity position of the companies are comparatively evaluated

to understand their current financial position.

Corporate Regulations:

i) Critically discussing whether financial reporting needs to be regulated or managers

should be allowed to disclose the information voluntarily:

The financial reporting system needs to be regulated with adequate measures and

standards, as it allows the stakeholders of the organisation for detecting the accurate financial

position of the organisation. The regulated financial reporting subsystem will ensure the

stakeholders about the correct financial position of the organisation and detect the measures,

which has been taken by the management for securing their future operations. In addition, the

financial reporting system helps in understanding the accurate operational details of the

organisation and the growth, which has been obtained over the past fiscal years. Dumay

(2016) mentioned that the presence of scandal and misleading reports conducted by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE AND FINANCIAL ACCOUNTING

4

companies with the presence of regulations indicates the importance of regulations, which is

needed for controlling the unethical action of the organisations.

There have been many instances, where scandals are conducted by the management of

the organisation for inflating their annual report and presenting the wrong financial position

to their investors. Therefore, giving powers to the managers in handling the overall financial

reporting system will create chaos and decreases the risk of the investors. Furthermore,

problems can be detected, where the manager will directly manipulate the financial report in

accordance with their preference, which can directly reduce reliability of the financial report.

The managers will also use the manipulative structure for reducing the level of profits for

declining the dividend payment and inflating the financial position during low performance

years. In this context, Wahlen, Baginski and Bradshaw (2014) stated that the biggest scandals

such as ABC learning and HIH Insurance directly indicates the manipulative measures, which

can be taken into consideration by the managers for altering the financial report according to

their needs. Hence, it can be understood that the preparation of the financial report cannot be

handed over to the managers of the organisation, as they will not comply with the fair

representation of the data in their annual report.

Therefore, with the presence of an accurate regulatory conceptual framework for

preparing the annual report can eventually help in portraying the accurate financial position

of the organisation. In addition, the different standards have been included for analysing

different segments of the organisation, which help in depicting the accurate financial position

of the company. In addition, the standards governing the fair value method and amortization

method has mainly forced the organisation to represent their fair value of the total assets held

in the current date. Hameed (2014) argued that there is different level of loopholes, which are

currently present within the current standards and is utilised by the management for inflating

their annual report.

4

companies with the presence of regulations indicates the importance of regulations, which is

needed for controlling the unethical action of the organisations.

There have been many instances, where scandals are conducted by the management of

the organisation for inflating their annual report and presenting the wrong financial position

to their investors. Therefore, giving powers to the managers in handling the overall financial

reporting system will create chaos and decreases the risk of the investors. Furthermore,

problems can be detected, where the manager will directly manipulate the financial report in

accordance with their preference, which can directly reduce reliability of the financial report.

The managers will also use the manipulative structure for reducing the level of profits for

declining the dividend payment and inflating the financial position during low performance

years. In this context, Wahlen, Baginski and Bradshaw (2014) stated that the biggest scandals

such as ABC learning and HIH Insurance directly indicates the manipulative measures, which

can be taken into consideration by the managers for altering the financial report according to

their needs. Hence, it can be understood that the preparation of the financial report cannot be

handed over to the managers of the organisation, as they will not comply with the fair

representation of the data in their annual report.

Therefore, with the presence of an accurate regulatory conceptual framework for

preparing the annual report can eventually help in portraying the accurate financial position

of the organisation. In addition, the different standards have been included for analysing

different segments of the organisation, which help in depicting the accurate financial position

of the company. In addition, the standards governing the fair value method and amortization

method has mainly forced the organisation to represent their fair value of the total assets held

in the current date. Hameed (2014) argued that there is different level of loopholes, which are

currently present within the current standards and is utilised by the management for inflating

their annual report.

CORPORATE AND FINANCIAL ACCOUNTING

5

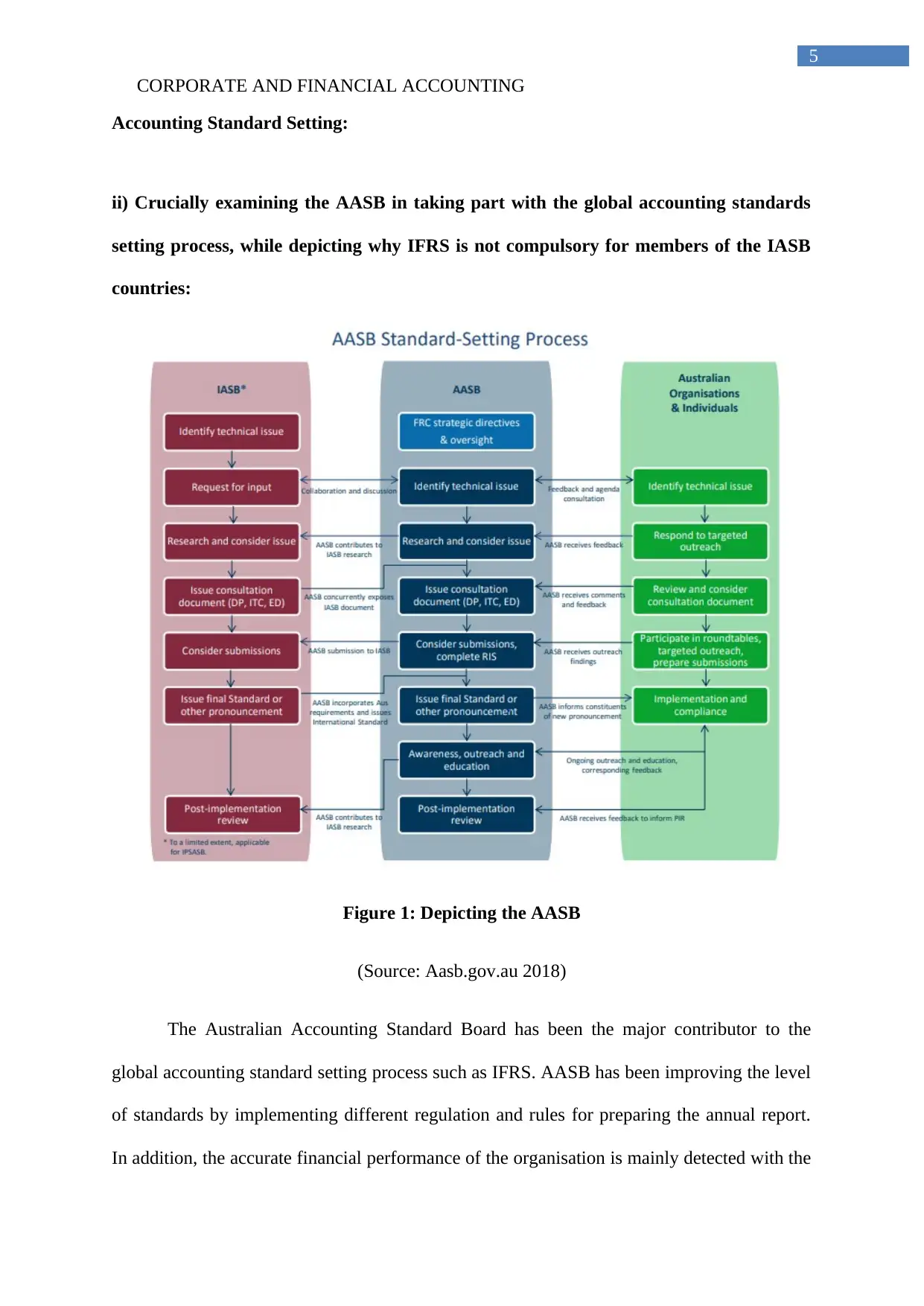

Accounting Standard Setting:

ii) Crucially examining the AASB in taking part with the global accounting standards

setting process, while depicting why IFRS is not compulsory for members of the IASB

countries:

Figure 1: Depicting the AASB

(Source: Aasb.gov.au 2018)

The Australian Accounting Standard Board has been the major contributor to the

global accounting standard setting process such as IFRS. AASB has been improving the level

of standards by implementing different regulation and rules for preparing the annual report.

In addition, the accurate financial performance of the organisation is mainly detected with the

5

Accounting Standard Setting:

ii) Crucially examining the AASB in taking part with the global accounting standards

setting process, while depicting why IFRS is not compulsory for members of the IASB

countries:

Figure 1: Depicting the AASB

(Source: Aasb.gov.au 2018)

The Australian Accounting Standard Board has been the major contributor to the

global accounting standard setting process such as IFRS. AASB has been improving the level

of standards by implementing different regulation and rules for preparing the annual report.

In addition, the accurate financial performance of the organisation is mainly detected with the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE AND FINANCIAL ACCOUNTING

6

changes that has been conducted by AASB over the period of time. The AASB standard

setting process has been depicted in the above figure, which has been evaluated by the

standards for generating adequate financial report of the organisations. The AASB measures

have relevantly added awareness, outreach and education, which needs to be conducted for

detecting the accurate level of reports (Nobes 2014).

There are also provisions conducted in the IASB, where the member countries can

choose not use the IFRS accounting system in preparing their annual report. This measure

eventually allows the member countries for formulate the annual report in accordance with

the accurate financial performance of the company. The IFRS system is mainly a complex

measure, which can only be used by multinational companies whose financial report is

needed for different stocks markets around the world. Moreover, adequate expenses is needed

to be conducted by the organisation in preparing the annual report in accordance with the

IFRS regulation, which directly increases the level of expenses of medium and small

companies. Hence, the IFRS regulations have been altered, where the companies listed in the

financial market in overseas needs to follow the IFRS regulations system. The excessive

expenses, which needs to be incurred by organisation in preparing the annual report in

accordance with the IFRS setting is the main reason, why the regulation is not imposed in

member countries (Leuz and Wysocki 2016).

Owners’ Equity:

iii) Listing each items of equity for the selected firms, while discussing the changes in

each item:

Equity Components Explanation

Contributed equity This section is known as the paid-up capital, where the cash and

6

changes that has been conducted by AASB over the period of time. The AASB standard

setting process has been depicted in the above figure, which has been evaluated by the

standards for generating adequate financial report of the organisations. The AASB measures

have relevantly added awareness, outreach and education, which needs to be conducted for

detecting the accurate level of reports (Nobes 2014).

There are also provisions conducted in the IASB, where the member countries can

choose not use the IFRS accounting system in preparing their annual report. This measure

eventually allows the member countries for formulate the annual report in accordance with

the accurate financial performance of the company. The IFRS system is mainly a complex

measure, which can only be used by multinational companies whose financial report is

needed for different stocks markets around the world. Moreover, adequate expenses is needed

to be conducted by the organisation in preparing the annual report in accordance with the

IFRS regulation, which directly increases the level of expenses of medium and small

companies. Hence, the IFRS regulations have been altered, where the companies listed in the

financial market in overseas needs to follow the IFRS regulations system. The excessive

expenses, which needs to be incurred by organisation in preparing the annual report in

accordance with the IFRS setting is the main reason, why the regulation is not imposed in

member countries (Leuz and Wysocki 2016).

Owners’ Equity:

iii) Listing each items of equity for the selected firms, while discussing the changes in

each item:

Equity Components Explanation

Contributed equity This section is known as the paid-up capital, where the cash and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE AND FINANCIAL ACCOUNTING

7

other assets given by shareholders given to the company

Reserves

Reserves is mainly a measure, which has been preserved used by

the organisation for the purchase of an asset.

Retained earnings

The total profits that the organisation has earned till date after

deducting the dividends.

Non-controlling interests

The non-controlling interest indicate that the investor has less than

50% of the outstanding shares, while it does not have control over

the decision of the organisation.

Rio Tinto 2017 2016 2015 2014

Share capital 4,360 4,139 4,174 4,765

Share premium account 4,306 4,304 4,300 4,288

Other reserves 12,284 9,216 9,139 11,122

Retained earnings 23,761 21,631 19,736 26,110

Attributable to non-controlling

interests 6,404 6,440 6,779 8,309

Total Equity 51,115 45,730 44,128 54,594

The total equity of the organisation has mainly declined over the period of four years,

which can be detected from the above table. The reduction in share capital is witnessed for

the organisation, while slight increment in share premium account is detected. The other

reserves have increased over the period, while drastic decline in retained earnings and non-

controlling interests have been witnessed during the past four fiscal years (Riotinto.com

2018).

Fortescue Metals Group

Limited 2018 2017 2016 2015

7

other assets given by shareholders given to the company

Reserves

Reserves is mainly a measure, which has been preserved used by

the organisation for the purchase of an asset.

Retained earnings

The total profits that the organisation has earned till date after

deducting the dividends.

Non-controlling interests

The non-controlling interest indicate that the investor has less than

50% of the outstanding shares, while it does not have control over

the decision of the organisation.

Rio Tinto 2017 2016 2015 2014

Share capital 4,360 4,139 4,174 4,765

Share premium account 4,306 4,304 4,300 4,288

Other reserves 12,284 9,216 9,139 11,122

Retained earnings 23,761 21,631 19,736 26,110

Attributable to non-controlling

interests 6,404 6,440 6,779 8,309

Total Equity 51,115 45,730 44,128 54,594

The total equity of the organisation has mainly declined over the period of four years,

which can be detected from the above table. The reduction in share capital is witnessed for

the organisation, while slight increment in share premium account is detected. The other

reserves have increased over the period, while drastic decline in retained earnings and non-

controlling interests have been witnessed during the past four fiscal years (Riotinto.com

2018).

Fortescue Metals Group

Limited 2018 2017 2016 2015

CORPORATE AND FINANCIAL ACCOUNTING

8

Contributed equity 1,287 1,289 1,301 1,294

Reserves 46 39 33 46

Retained earnings 8,386 8,392 7,058 6,184

Non-controlling interest 12 14 14 13

Total Equity 9,731 9,734 8,406 7,537

The increment in total equity of the Fortescue Metals Group Limited is due to the rise

in retained earnings of the organization. The other components of the equity segments have

altered slightly, which has low influence in the change of the organization equity section

(Fmgl.com.au 2018).

BHP Billiton 2018 2017 2016 2015

Share capital 2,243 2,243 2,243 2,255

Treasury shares (5) (3) (76) (587)

Reserves 2,290 2,400 2,557 2,927

Retained earnings 51,064 52,618 60,044 74,548

Non-controlling

interest 5,078 5,468 5,777 6,239

Total Equity 60,670 62,726 70,545 85,382

Th decline in the total equity has been witnessed in the above table for BHP Billiton,

which has been conducted due to the falling retained earnings of the organisation. The

alternations in other segments of the equity section is relevantly minor, which did not

influence drastic decline in the total equity of the organisation (Bhp.com 2018).

Amcor Limited 2018 2017 2016 2015

Contributed equity 1,400.7 1,416.9 1,445.1 1,680.6

Reserves (907.1) (881.7) (800.2) (666.5)

Retained earnings 528.1 264.9 139.0 452.1

Non-controlling

interest 68.8 69.6 61.6 120.8

Total Equity 1,090.5 869.7 845.5 1,587.0

8

Contributed equity 1,287 1,289 1,301 1,294

Reserves 46 39 33 46

Retained earnings 8,386 8,392 7,058 6,184

Non-controlling interest 12 14 14 13

Total Equity 9,731 9,734 8,406 7,537

The increment in total equity of the Fortescue Metals Group Limited is due to the rise

in retained earnings of the organization. The other components of the equity segments have

altered slightly, which has low influence in the change of the organization equity section

(Fmgl.com.au 2018).

BHP Billiton 2018 2017 2016 2015

Share capital 2,243 2,243 2,243 2,255

Treasury shares (5) (3) (76) (587)

Reserves 2,290 2,400 2,557 2,927

Retained earnings 51,064 52,618 60,044 74,548

Non-controlling

interest 5,078 5,468 5,777 6,239

Total Equity 60,670 62,726 70,545 85,382

Th decline in the total equity has been witnessed in the above table for BHP Billiton,

which has been conducted due to the falling retained earnings of the organisation. The

alternations in other segments of the equity section is relevantly minor, which did not

influence drastic decline in the total equity of the organisation (Bhp.com 2018).

Amcor Limited 2018 2017 2016 2015

Contributed equity 1,400.7 1,416.9 1,445.1 1,680.6

Reserves (907.1) (881.7) (800.2) (666.5)

Retained earnings 528.1 264.9 139.0 452.1

Non-controlling

interest 68.8 69.6 61.6 120.8

Total Equity 1,090.5 869.7 845.5 1,587.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE AND FINANCIAL ACCOUNTING

9

The changes in total equity of the organisation has mainly declined over the four

years. This demise in total equity has been conducted by the negative reserves, declining

contributed equity and non-controlling interest (Assets.ctfassets.net 2018).

iv) Providing a comparative analysis of the debt and equity position of the four firms

that have been selected:

Rio Tinto 2017 2016 2015 2014

Equity 51,115 45,730 44,128 54,594

Debt 3,845 9,587 13,783 12,495

The above table analyses the different equity and debt position of Rio Tinto during the

past four fiscal year, which helps in detecting the current financial position of the

organisation. In addition, both the equity and debt of Rio Tinto has mainly declined over the

period of four fiscal year, which has relevantly improved their current financial performance.

Moreover, the debt of the organisation has mainly declined substantially, while equity has

reduced slowly in comparison to debt, which indicates that the company has effectively

achieved solvent condition (Riotinto.com 2018).

Fortescue Metals Group

Limited 2018 2017 2016 2015

Equity 9,731 9,734 8,406 7,537

Debt 3,112 2,633 5,188 7,188

The decline in debt and improvement of equity has been witnessed in the Fortescue

Metals Group Limited, which indicates the incremental financial position of the firm. In

addition, the equity value has mainly increased from 7,537 in 2015 to 9,731 in 2018, while

the debt values have declined in half from 7,188 in 2015 to 3,112 in 2018 (Fmgl.com.au

2018).

9

The changes in total equity of the organisation has mainly declined over the four

years. This demise in total equity has been conducted by the negative reserves, declining

contributed equity and non-controlling interest (Assets.ctfassets.net 2018).

iv) Providing a comparative analysis of the debt and equity position of the four firms

that have been selected:

Rio Tinto 2017 2016 2015 2014

Equity 51,115 45,730 44,128 54,594

Debt 3,845 9,587 13,783 12,495

The above table analyses the different equity and debt position of Rio Tinto during the

past four fiscal year, which helps in detecting the current financial position of the

organisation. In addition, both the equity and debt of Rio Tinto has mainly declined over the

period of four fiscal year, which has relevantly improved their current financial performance.

Moreover, the debt of the organisation has mainly declined substantially, while equity has

reduced slowly in comparison to debt, which indicates that the company has effectively

achieved solvent condition (Riotinto.com 2018).

Fortescue Metals Group

Limited 2018 2017 2016 2015

Equity 9,731 9,734 8,406 7,537

Debt 3,112 2,633 5,188 7,188

The decline in debt and improvement of equity has been witnessed in the Fortescue

Metals Group Limited, which indicates the incremental financial position of the firm. In

addition, the equity value has mainly increased from 7,537 in 2015 to 9,731 in 2018, while

the debt values have declined in half from 7,188 in 2015 to 3,112 in 2018 (Fmgl.com.au

2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE AND FINANCIAL ACCOUNTING

10

BHP Billiton 2018 2017 2016 2015

Equity 60,670 62,726 70,545 85,382

Debt 10,934 16,321 26,102 24,417

Both the equity and debt position of BHP Billiton has mainly declined over the period

of four fiscal years, which has improved the current financial position of the organisation.

The decline in debt of BHP Billion is almost more than half, while the equity values have not

declined substantially in comparisons to the debt, which directly indicates the financial

performance of the organisation (Bhp.com 2018).

Amcor 2018 2017 2016 2015

Equity 1,090.5 869.7 845.5 1,587.0

Debt 3,872.2 4,049.5 3,829.4 2,880.4

The equity and debt combination of Amcor is relevant different from other

companies, where the equity values have declined over the period of four fiscal years, while

the debt has increased. This increment in the debt values of the organisation has mainly

indicated the low financial performance of the company, which led to the accumulation of

high debt and low equity (Assets.ctfassets.net 2018).

Therefore, from the evaluation of the above table the overall equity and debt of the

four companies can be detected. In addition, the reduction in debt accumulation of Rio Tinto,

Fortescue Metals Group Limited, and BHP Billiton can be witnessed during the past four

fiscal years. However, only Amcor Limited debt values have increased during the four fiscal

years, which directly indicates the low financial performance of the organization. Therefore,

it could be assumed that the financial performance of Rio Tinto, Fortescue Metals Group

Limited, and BHP Billiton has improved, while Amcor Limited performance has declined.

10

BHP Billiton 2018 2017 2016 2015

Equity 60,670 62,726 70,545 85,382

Debt 10,934 16,321 26,102 24,417

Both the equity and debt position of BHP Billiton has mainly declined over the period

of four fiscal years, which has improved the current financial position of the organisation.

The decline in debt of BHP Billion is almost more than half, while the equity values have not

declined substantially in comparisons to the debt, which directly indicates the financial

performance of the organisation (Bhp.com 2018).

Amcor 2018 2017 2016 2015

Equity 1,090.5 869.7 845.5 1,587.0

Debt 3,872.2 4,049.5 3,829.4 2,880.4

The equity and debt combination of Amcor is relevant different from other

companies, where the equity values have declined over the period of four fiscal years, while

the debt has increased. This increment in the debt values of the organisation has mainly

indicated the low financial performance of the company, which led to the accumulation of

high debt and low equity (Assets.ctfassets.net 2018).

Therefore, from the evaluation of the above table the overall equity and debt of the

four companies can be detected. In addition, the reduction in debt accumulation of Rio Tinto,

Fortescue Metals Group Limited, and BHP Billiton can be witnessed during the past four

fiscal years. However, only Amcor Limited debt values have increased during the four fiscal

years, which directly indicates the low financial performance of the organization. Therefore,

it could be assumed that the financial performance of Rio Tinto, Fortescue Metals Group

Limited, and BHP Billiton has improved, while Amcor Limited performance has declined.

CORPORATE AND FINANCIAL ACCOUNTING

11

Conclusion:

The overall assessment mainly comprises of different segments, which helps in

supporting the different level of segments of financial reporting. In addition, the financial

report needs to be regulated, as it might help in portraying the accurate financial performance

of the organisation. the regulation might reduce the level of unethical measure, which can be

used by managers in inflating their financial performance. Furthermore, the IFRS system has

been evaluated, which can help in detecting the accurate financial reports of an organisation.

Likewise, the accountings standard settings have also been conducted, where the contribution

of the AASB has been highlighted for preparing the annual report of the organisation.

Furthermore, the financial performance of the selected companies has been conducted for

identifying the level of debt and equity, which has been acquired by the organisations. Lastly,

the level of comparative study has been conducted for the current financial performance of

the organisations, where only Amcor’s financial position is seen to decline over the period of

four fiscal years.

11

Conclusion:

The overall assessment mainly comprises of different segments, which helps in

supporting the different level of segments of financial reporting. In addition, the financial

report needs to be regulated, as it might help in portraying the accurate financial performance

of the organisation. the regulation might reduce the level of unethical measure, which can be

used by managers in inflating their financial performance. Furthermore, the IFRS system has

been evaluated, which can help in detecting the accurate financial reports of an organisation.

Likewise, the accountings standard settings have also been conducted, where the contribution

of the AASB has been highlighted for preparing the annual report of the organisation.

Furthermore, the financial performance of the selected companies has been conducted for

identifying the level of debt and equity, which has been acquired by the organisations. Lastly,

the level of comparative study has been conducted for the current financial performance of

the organisations, where only Amcor’s financial position is seen to decline over the period of

four fiscal years.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.