Corporate Financial Management (ACC705): Acquisition Analysis Solution

VerifiedAdded on 2023/01/06

|4

|453

|88

Homework Assignment

AI Summary

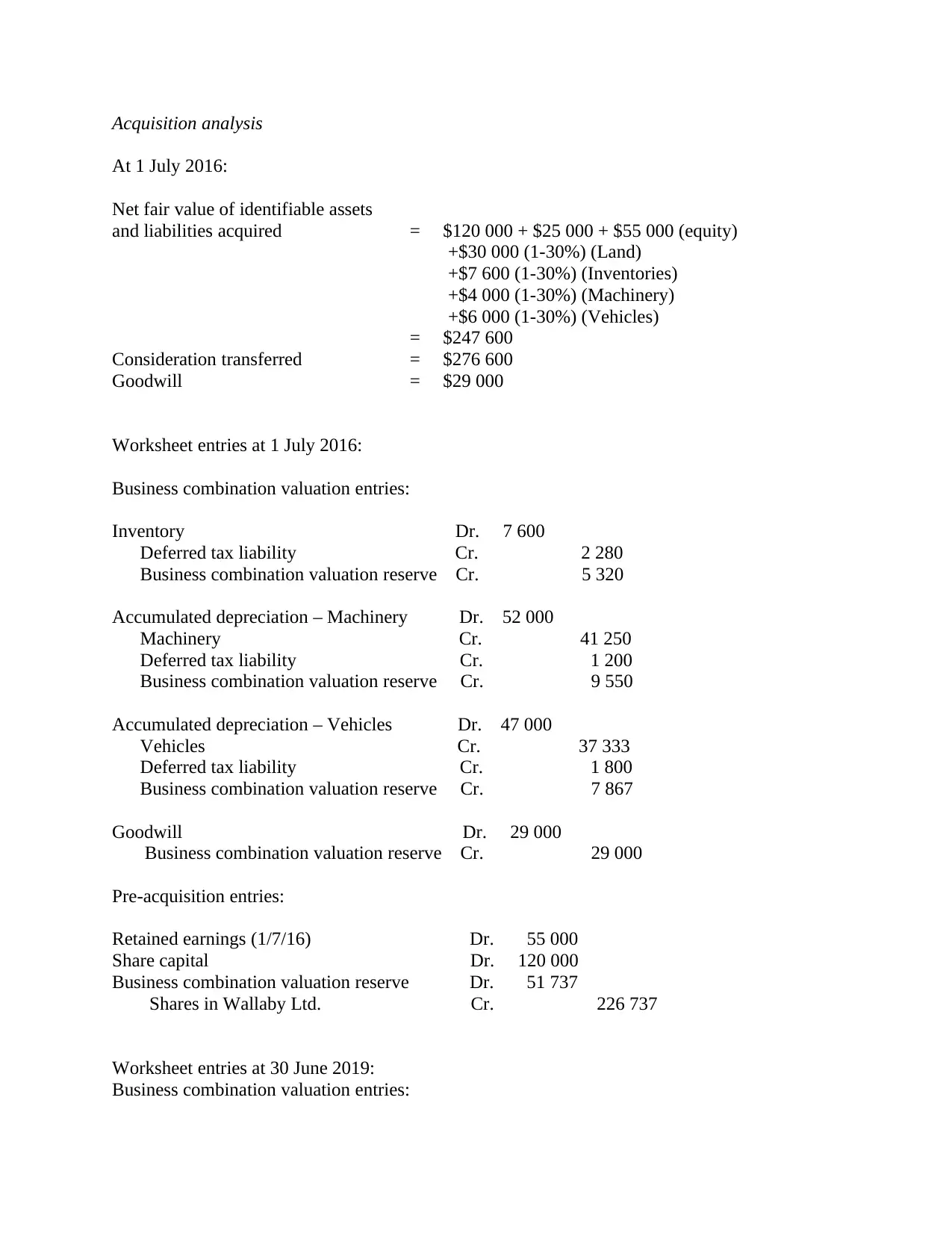

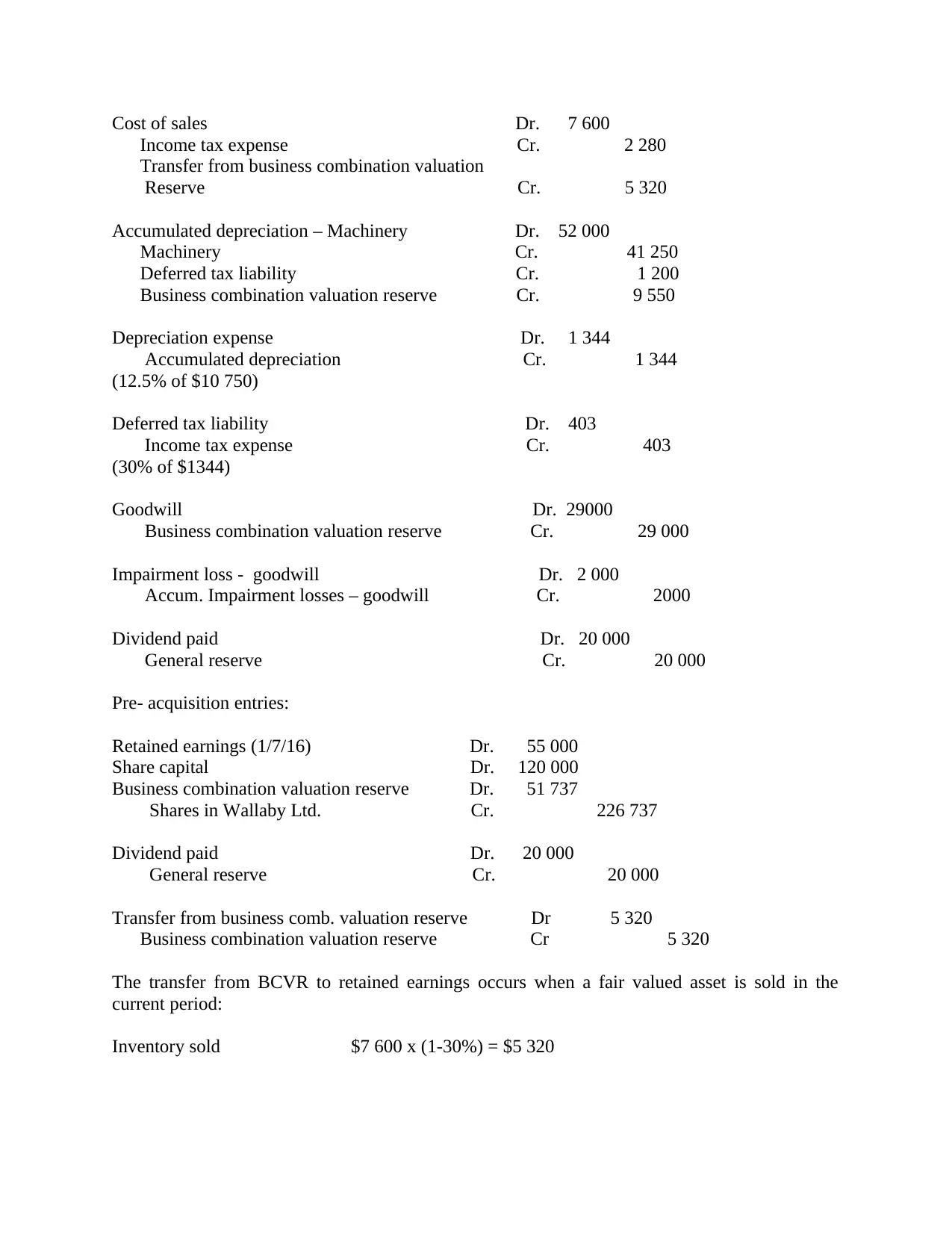

This document presents a detailed solution for an acquisition analysis assignment, likely for a Corporate Financial Management course (ACC705). The solution meticulously outlines the net fair value of identifiable assets and liabilities acquired, calculating goodwill based on consideration transferred. It provides comprehensive worksheet entries at both July 1, 2016, and June 30, 2019, covering business combination valuation entries, pre-acquisition entries, and adjustments for items like inventory, machinery, vehicles, and deferred tax liabilities. The solution also addresses goodwill impairment and dividend payments, providing a complete financial analysis of the acquisition and its subsequent impact on the financial statements. The document includes calculations and entries related to cost of sales, income tax expense, depreciation, and the transfer from business combination valuation reserve, offering a practical application of accounting principles in a business combination scenario.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.