Corporate Finance: Stock Return and Market Return Relationship

VerifiedAdded on 2020/01/28

|9

|1985

|208

Report

AI Summary

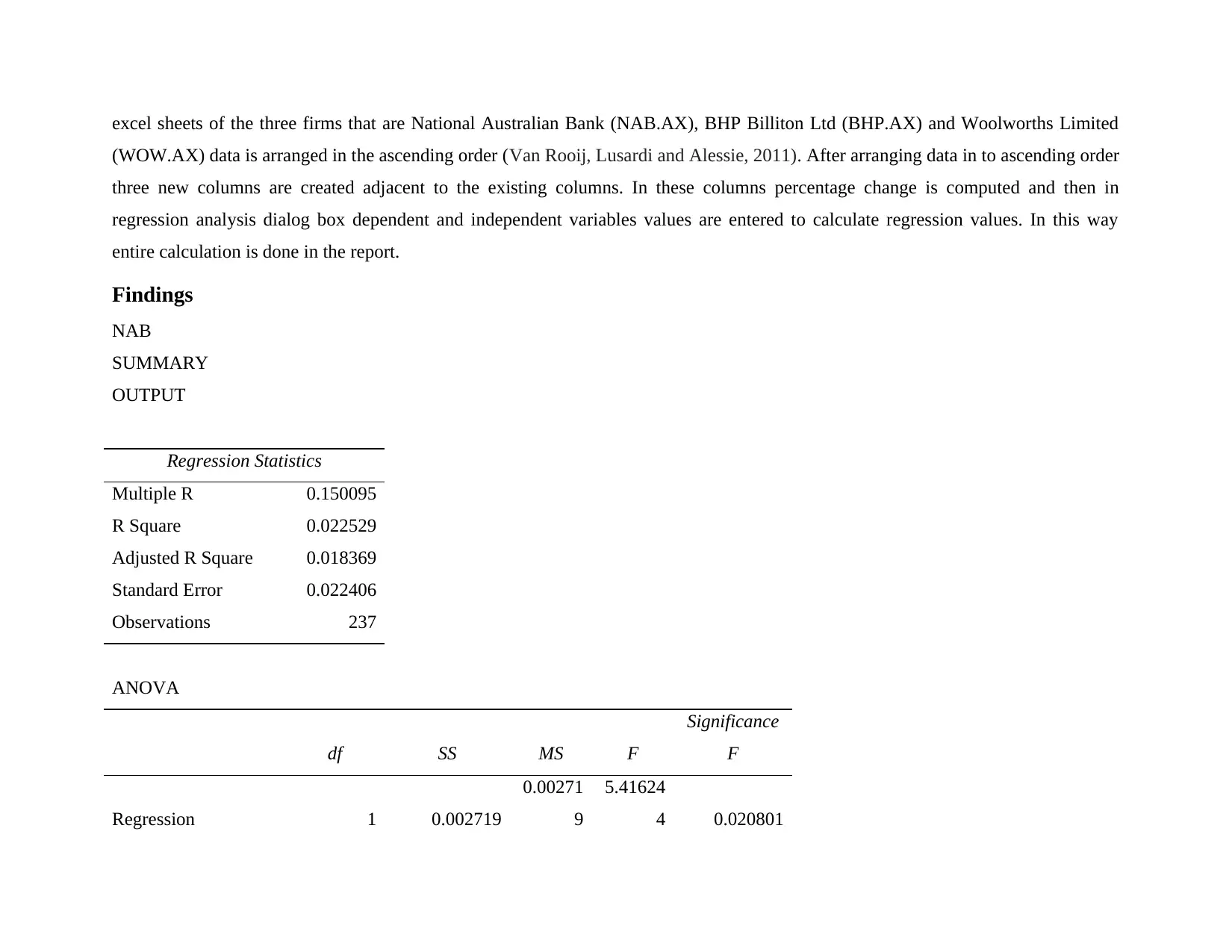

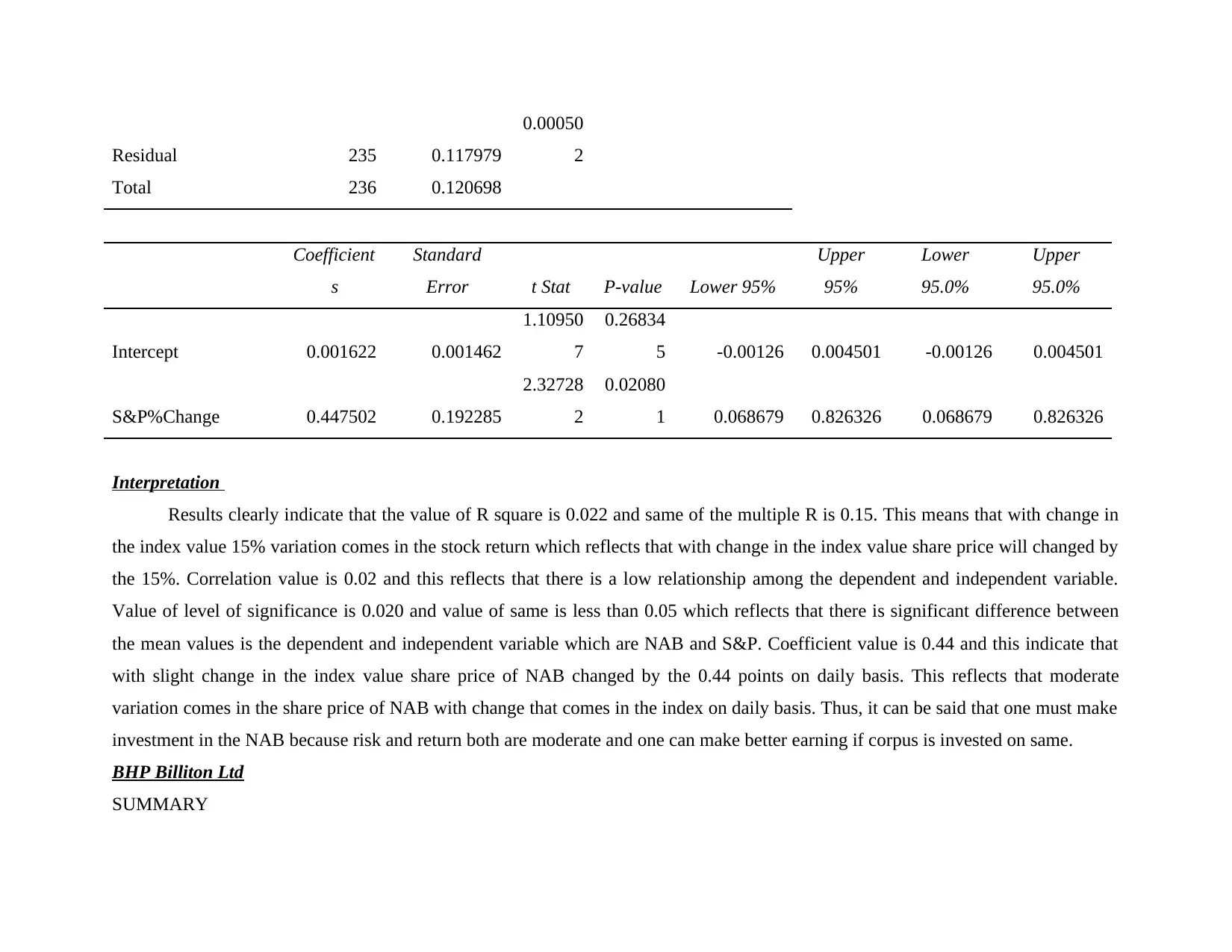

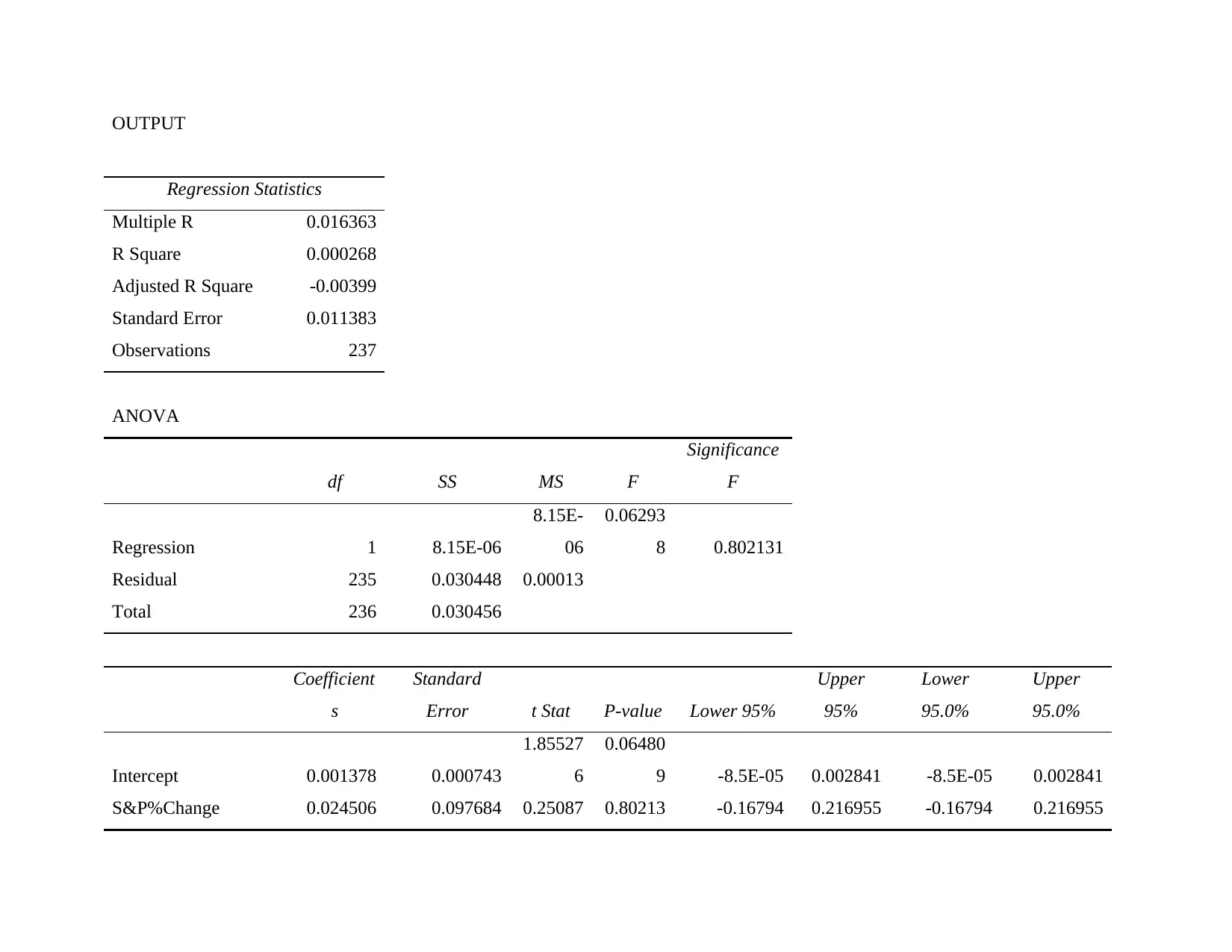

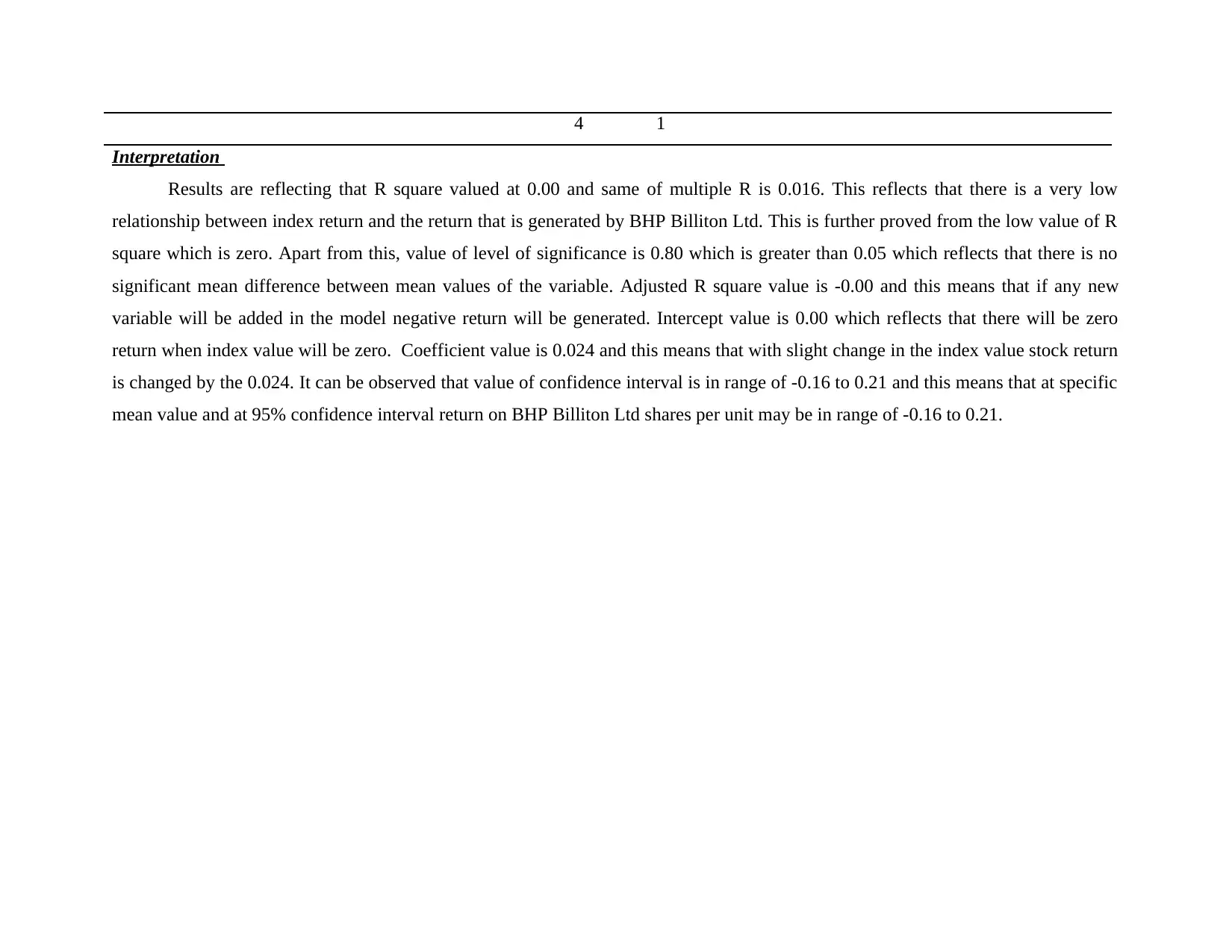

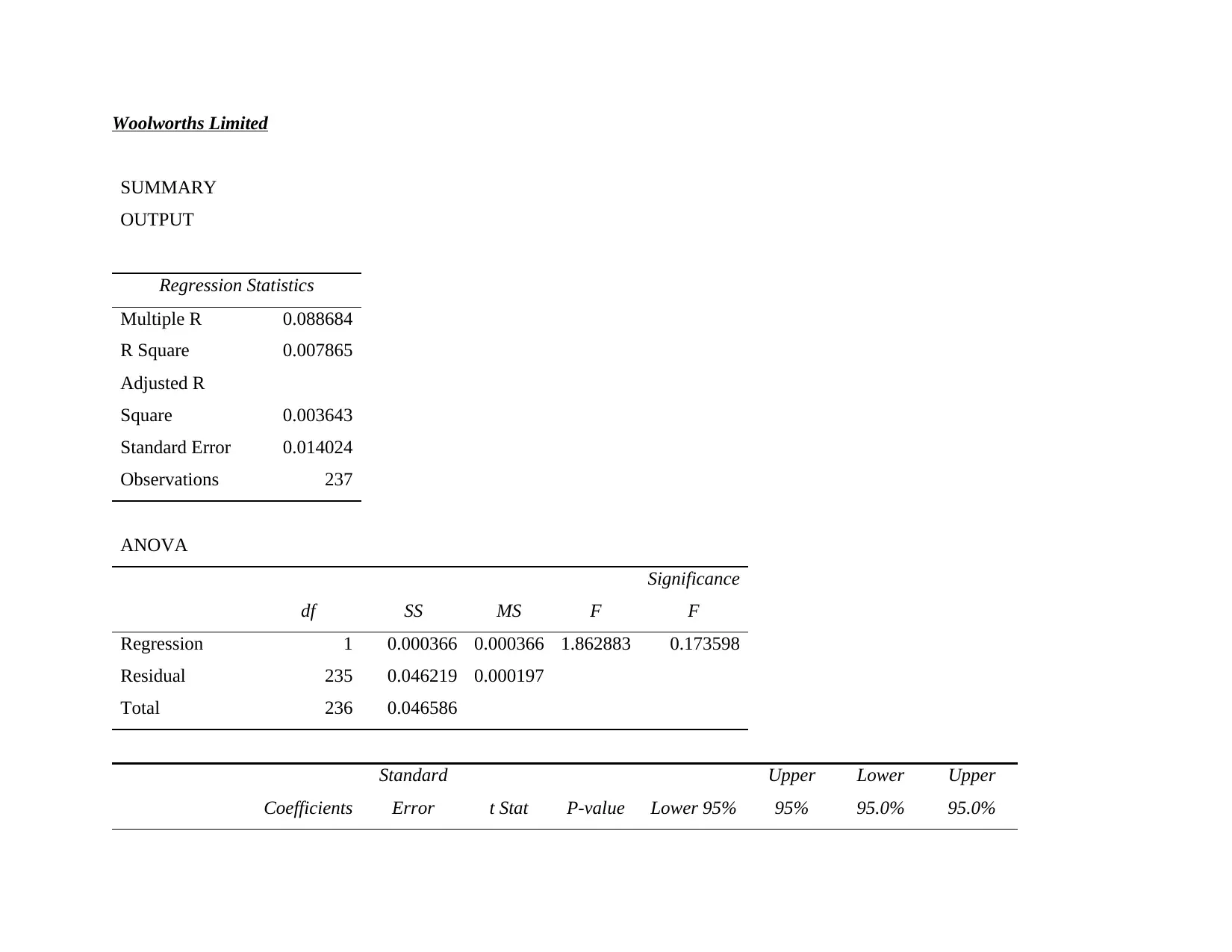

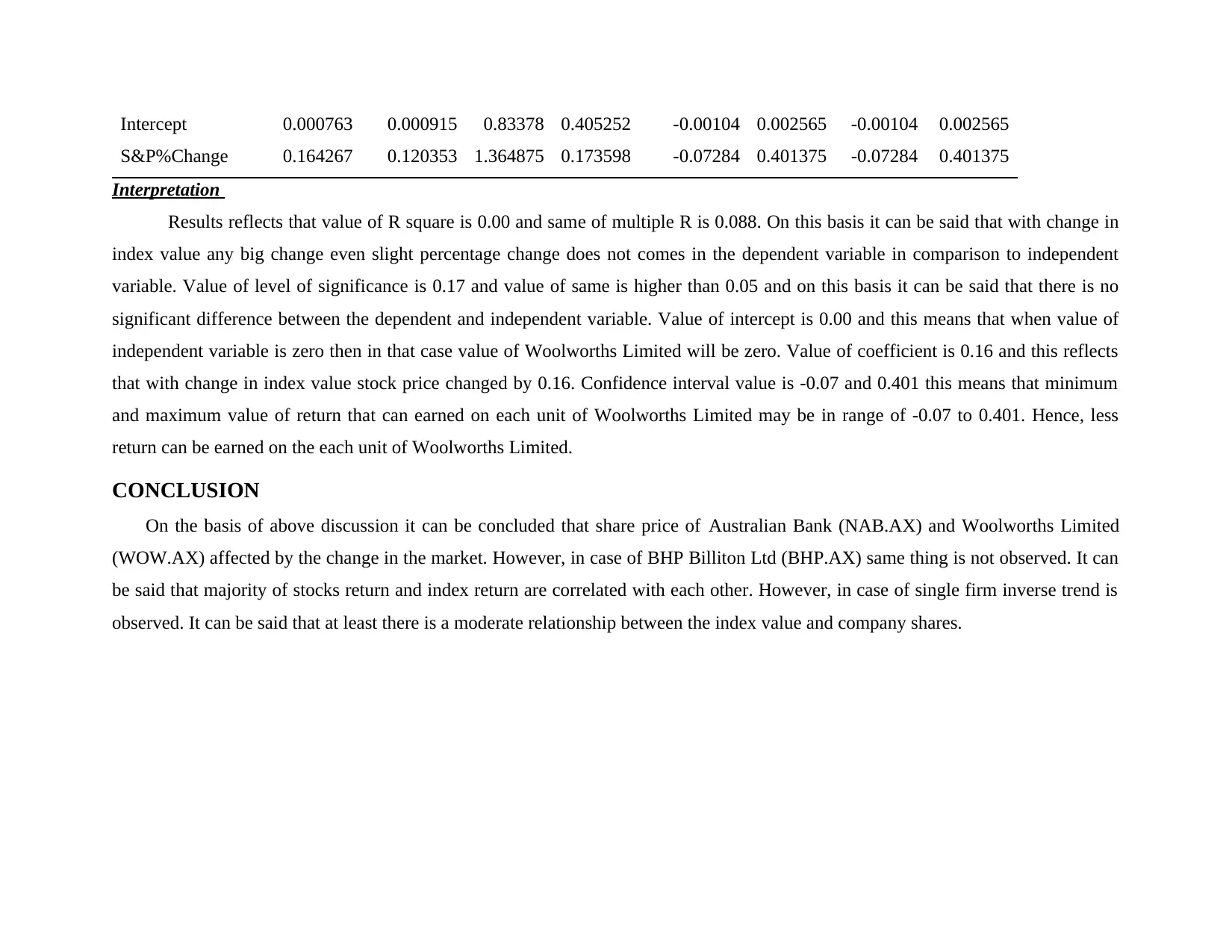

This report delves into the realm of corporate finance, employing regression models to assess the sensitivity of stock returns to market fluctuations. The methodology involves utilizing regression analysis to evaluate the performance of three firms: National Australian Bank (NAB.AX), BHP Billiton Ltd (BHP.AX), and Woolworths Limited (WOW.AX), using data sourced from Yahoo Finance. The findings reveal varying degrees of correlation between stock returns and market returns for each company. The analysis of NAB.AX indicates a moderate relationship, while BHP Billiton Ltd (BHP.AX) shows a very low correlation, and Woolworths Limited (WOW.AX) demonstrates a slight relationship. The report concludes that while most stocks exhibit a correlation with index returns, individual firm performance can deviate, emphasizing the importance of considering market dynamics in investment strategies. The report provides detailed interpretations of the regression results, including R-squared values, coefficients, and levels of significance, offering insights into the potential risks and returns associated with each stock.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.