Corporate Finance Assessment 3: Case Study Analysis

VerifiedAdded on 2021/04/21

|8

|1614

|63

Case Study

AI Summary

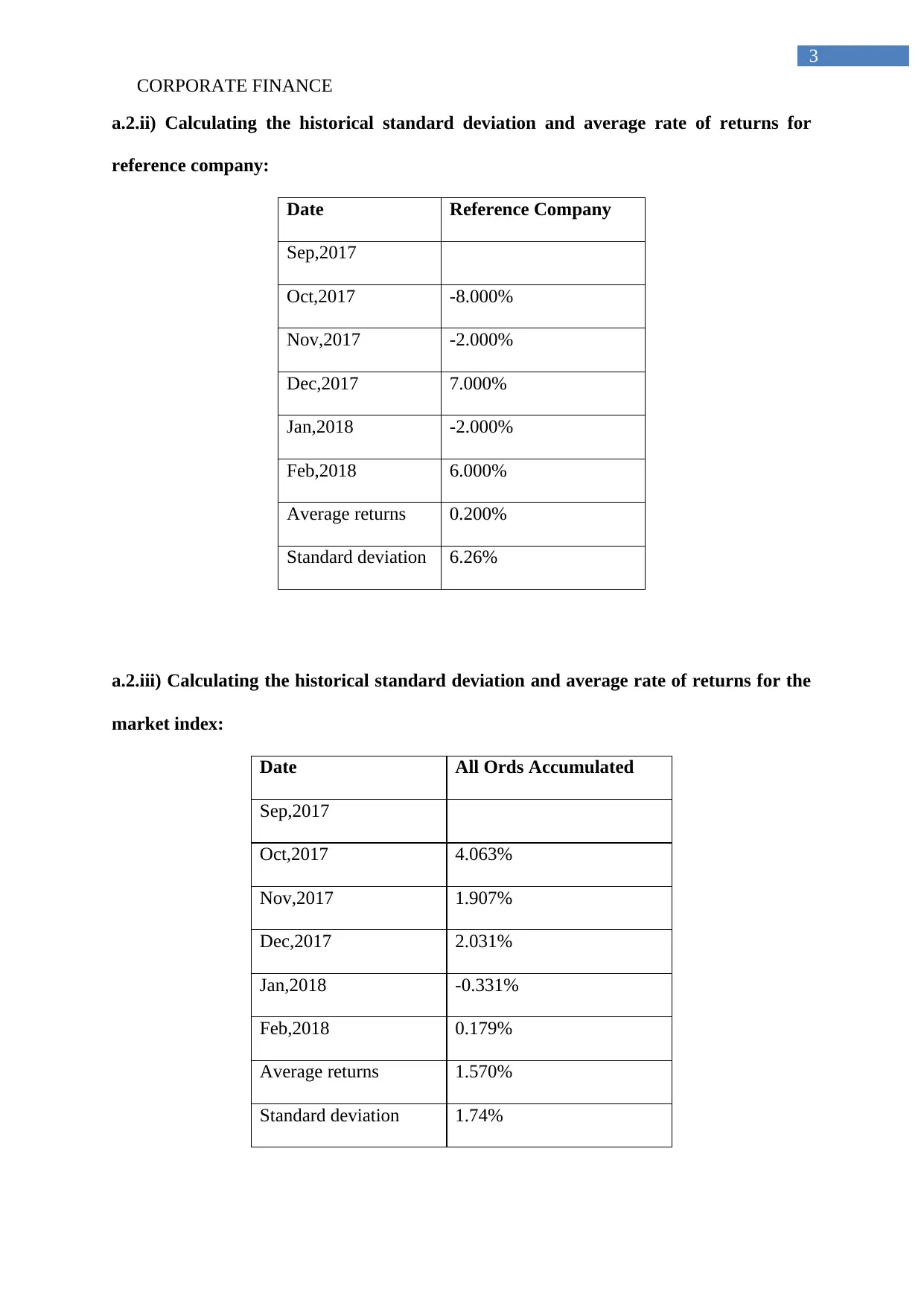

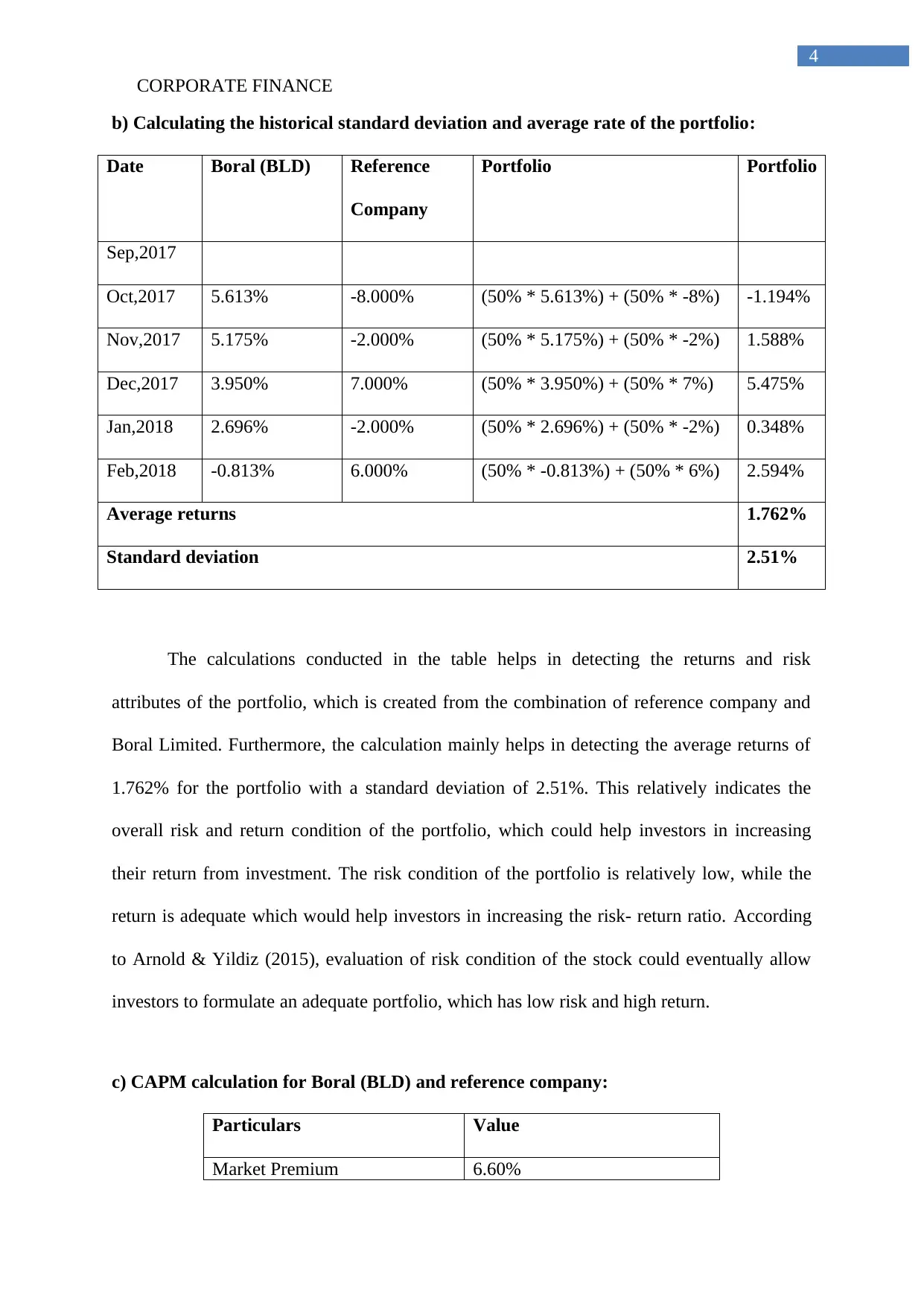

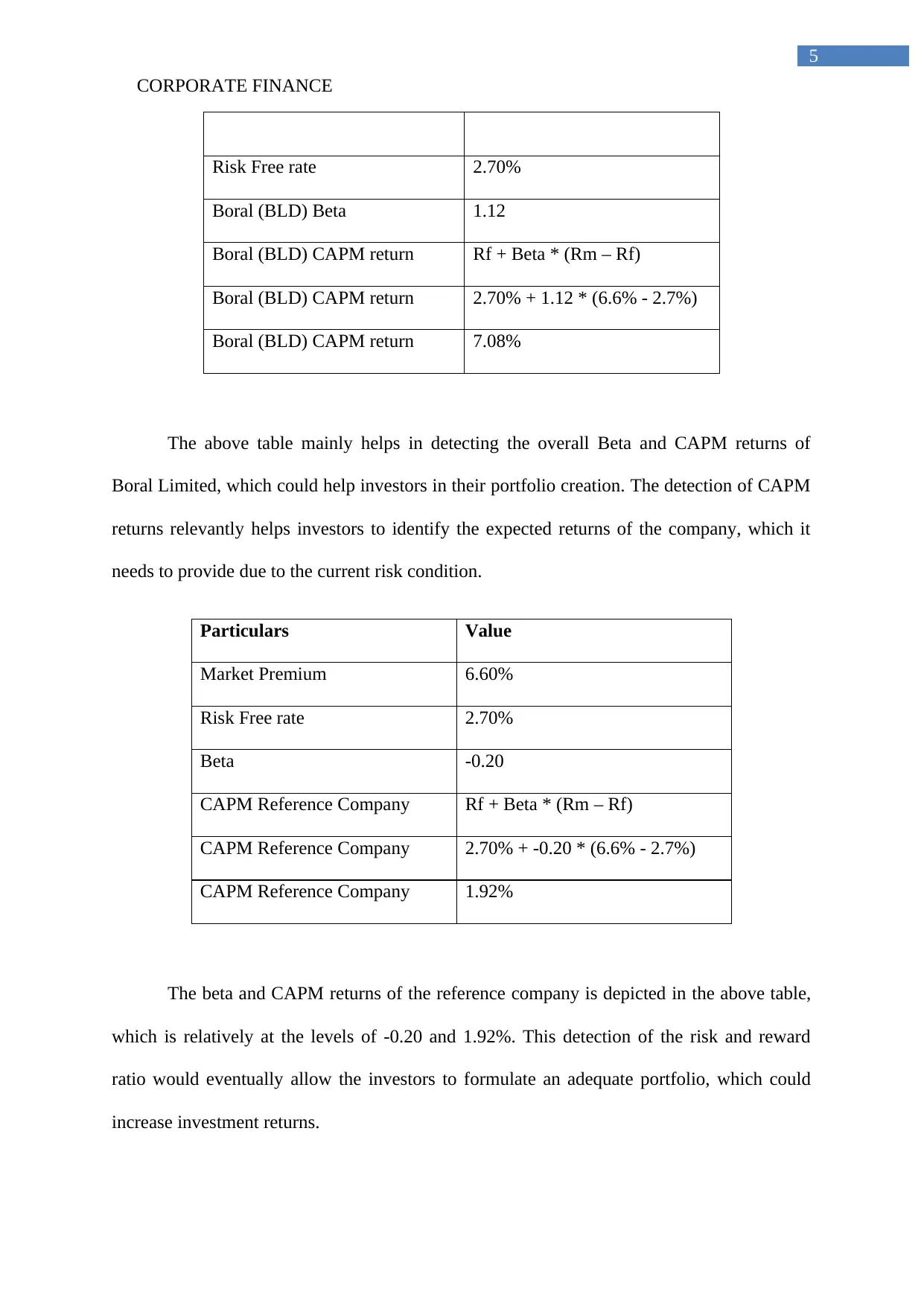

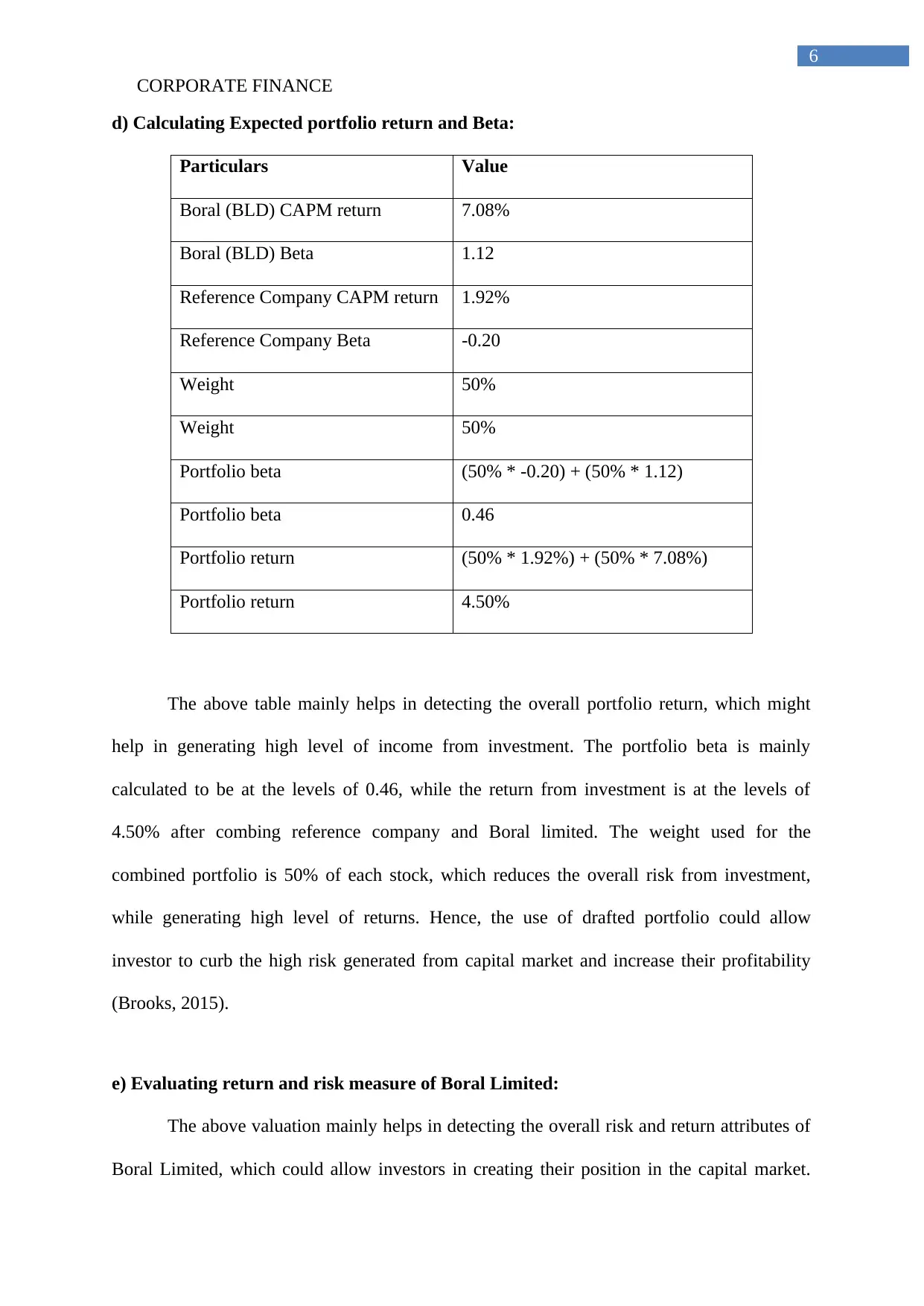

This case study analyzes the financial performance of Boral Limited and a reference company, focusing on risk and return metrics. It calculates historical monthly returns for the market index, Boral (BLD), and the reference company, along with their respective standard deviations and average rates of return. The analysis extends to portfolio calculations, determining the historical standard deviation and average rate of return for a portfolio composed of Boral (BLD) and the reference company. The study then applies the Capital Asset Pricing Model (CAPM) to both Boral (BLD) and the reference company to determine expected returns. Furthermore, it calculates the expected portfolio return and beta, providing insights into portfolio risk and return characteristics. The evaluation concludes with an assessment of the return and risk measures of Boral Limited, offering a comprehensive financial analysis. The findings highlight the importance of risk-return relationships and portfolio diversification in financial decision-making, supported by relevant academic references.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.