Corporate Finance Analysis: Capital Structure and Discount Rate

VerifiedAdded on 2022/11/28

|10

|2194

|470

Report

AI Summary

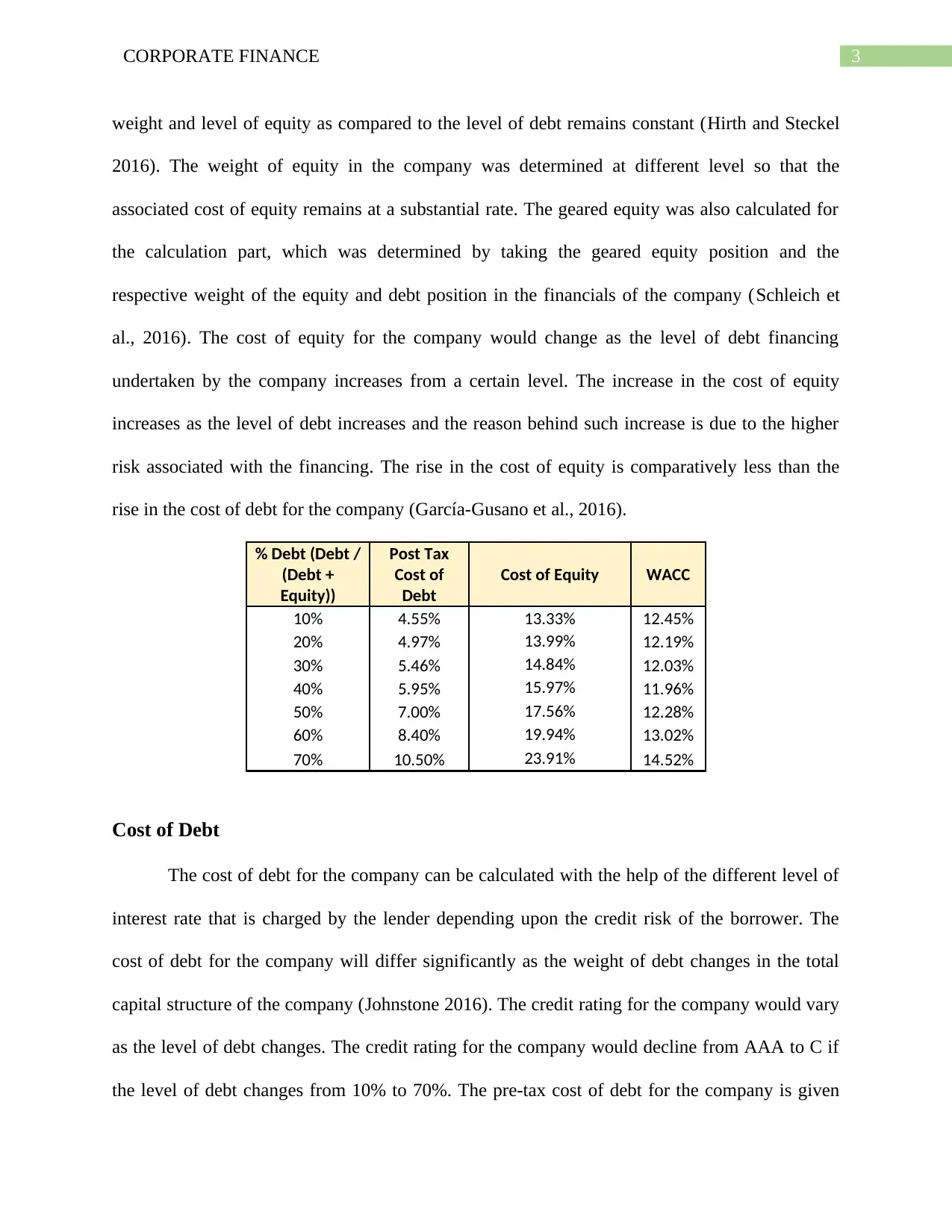

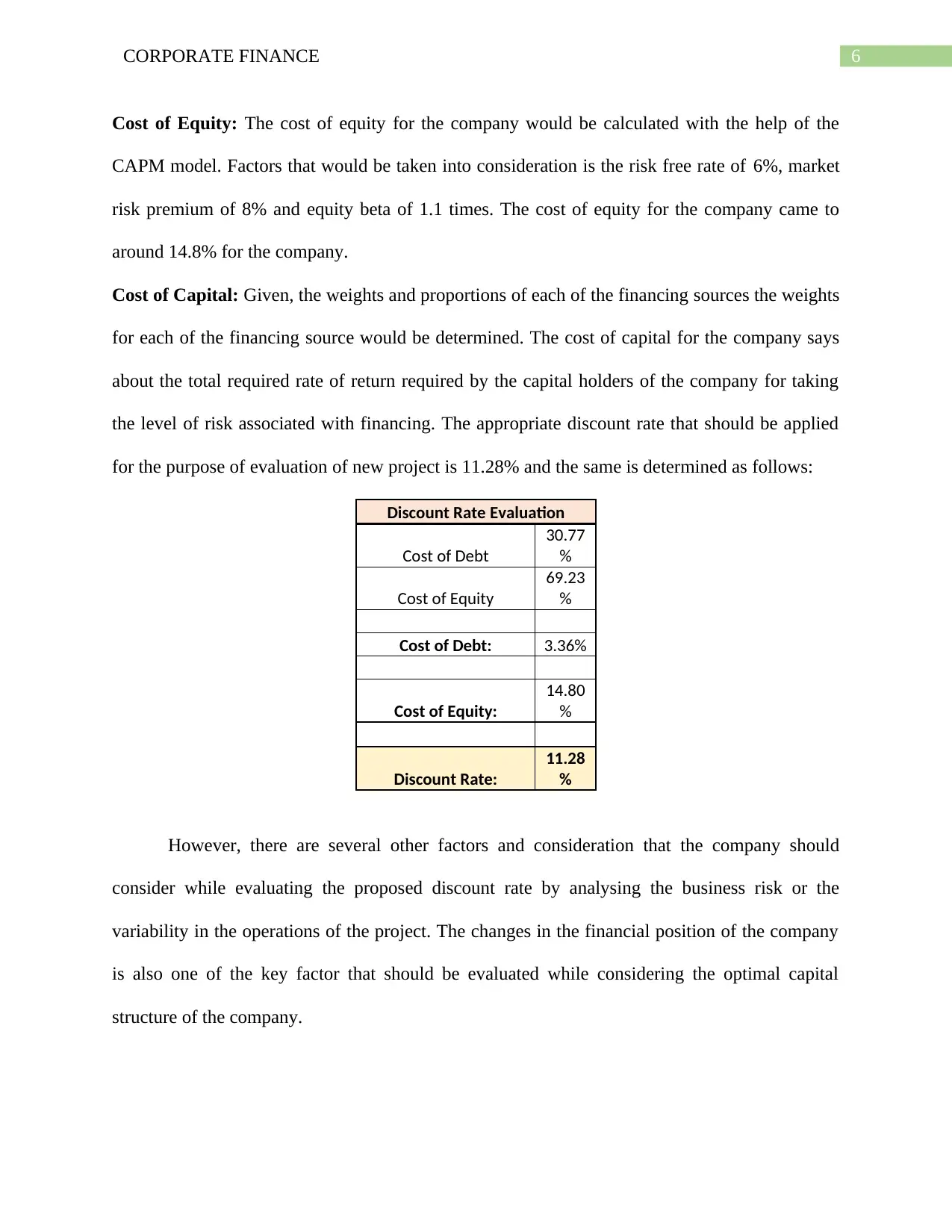

This report provides a comprehensive analysis of corporate finance, focusing on the capital structure and discount rate of Middle East Machinery Plc. It begins by discussing the importance of capital structure in determining the level of finance and associated costs, emphasizing the balance between debt, equity, and other financing sources. The report calculates the cost of equity using the Capital Asset Pricing Model (CAPM), considering both geared and ungeared beta. It then evaluates the cost of debt based on interest rates and credit ratings, which are influenced by the level of debt. The weighted average cost of capital (WACC) is determined to find the optimal mix of debt and equity that minimizes the cost of capital. The appropriate discount rate for evaluating new projects is also discussed, incorporating the cost of debt and equity. The analysis concludes with recommendations on the optimal capital structure and discount rate, providing insights for financial decision-making, considering both business and financial risks.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.