Corporate Finance: Boral Limited Analysis and Recommendations

VerifiedAdded on 2021/04/24

|10

|2398

|52

Report

AI Summary

This report, focusing on corporate finance, analyzes Boral Limited's capital structure, capital budgeting, and dividend policy. Task 1 delves into the company's capital structure and dividend pay-out policy, examining historical data and evaluating the policy's implications. Task 2 involves a financial analysis of a proposed project using spreadsheet modeling, calculating NPV, IRR, payback period, and profitability index. A memo to the CEO justifies the chosen methods and recommendations based on the financial analysis. The report concludes that the project is a viable investment, recommending its commencement to generate high returns. The report uses financial data from 2015 to 2017 and incorporates relevant academic sources to support its findings. The analysis includes detailed calculations of cash flows, depreciation, and tax implications to assess the project's financial viability.

Running head: CORPORATE FINANCE

Corporate Finance

Name of the Student:

Name of the University:

Authors Note:

Corporate Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

1

Table of Contents

Assessment 4: Task for Case Study 2........................................................................................2

Task 1: Capital Structure and Pay-out Policy Analysis.............................................................2

1) Describing the policy based on current and historical data:..................................................2

2) Evaluating the policy, drawing on practical considerations covered applied to the

company’s current characteristics and situation:.......................................................................4

Task 2: Capital Budgeting Task.................................................................................................5

1) Spreadsheet financial analysis of the proposed project:........................................................5

2) Memo to the CEO addressing, explaining, and justifying the chosen methods:...................8

Reference and Bibliography:....................................................................................................11

1

Table of Contents

Assessment 4: Task for Case Study 2........................................................................................2

Task 1: Capital Structure and Pay-out Policy Analysis.............................................................2

1) Describing the policy based on current and historical data:..................................................2

2) Evaluating the policy, drawing on practical considerations covered applied to the

company’s current characteristics and situation:.......................................................................4

Task 2: Capital Budgeting Task.................................................................................................5

1) Spreadsheet financial analysis of the proposed project:........................................................5

2) Memo to the CEO addressing, explaining, and justifying the chosen methods:...................8

Reference and Bibliography:....................................................................................................11

CORPORATE FINANCE

2

Assessment 4: Task for Case Study 2

Task 1: Capital Structure and Pay-out Policy Analysis

1) Describing the policy based on current and historical data:

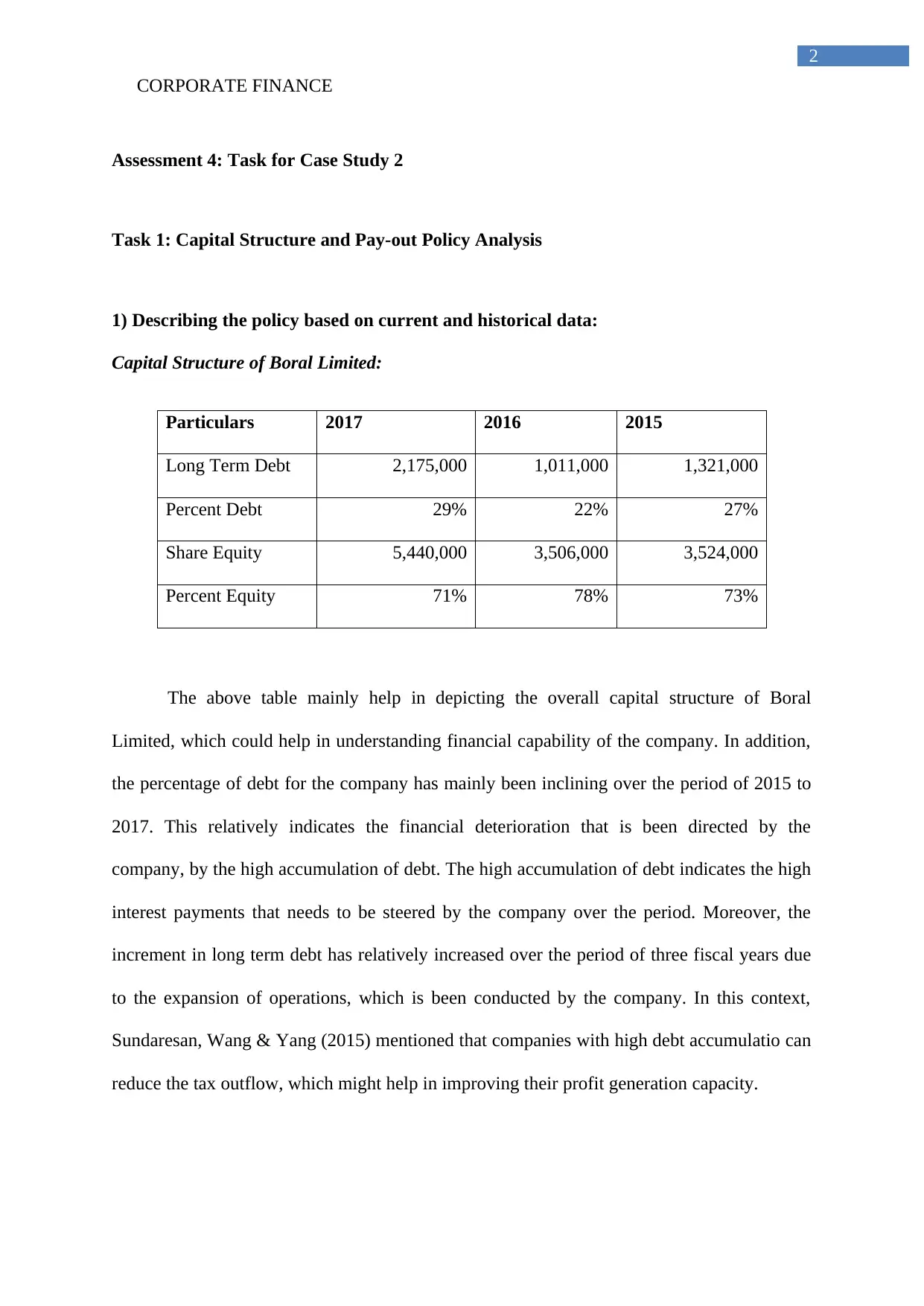

Capital Structure of Boral Limited:

Particulars 2017 2016 2015

Long Term Debt 2,175,000 1,011,000 1,321,000

Percent Debt 29% 22% 27%

Share Equity 5,440,000 3,506,000 3,524,000

Percent Equity 71% 78% 73%

The above table mainly help in depicting the overall capital structure of Boral

Limited, which could help in understanding financial capability of the company. In addition,

the percentage of debt for the company has mainly been inclining over the period of 2015 to

2017. This relatively indicates the financial deterioration that is been directed by the

company, by the high accumulation of debt. The high accumulation of debt indicates the high

interest payments that needs to be steered by the company over the period. Moreover, the

increment in long term debt has relatively increased over the period of three fiscal years due

to the expansion of operations, which is been conducted by the company. In this context,

Sundaresan, Wang & Yang (2015) mentioned that companies with high debt accumulatio can

reduce the tax outflow, which might help in improving their profit generation capacity.

2

Assessment 4: Task for Case Study 2

Task 1: Capital Structure and Pay-out Policy Analysis

1) Describing the policy based on current and historical data:

Capital Structure of Boral Limited:

Particulars 2017 2016 2015

Long Term Debt 2,175,000 1,011,000 1,321,000

Percent Debt 29% 22% 27%

Share Equity 5,440,000 3,506,000 3,524,000

Percent Equity 71% 78% 73%

The above table mainly help in depicting the overall capital structure of Boral

Limited, which could help in understanding financial capability of the company. In addition,

the percentage of debt for the company has mainly been inclining over the period of 2015 to

2017. This relatively indicates the financial deterioration that is been directed by the

company, by the high accumulation of debt. The high accumulation of debt indicates the high

interest payments that needs to be steered by the company over the period. Moreover, the

increment in long term debt has relatively increased over the period of three fiscal years due

to the expansion of operations, which is been conducted by the company. In this context,

Sundaresan, Wang & Yang (2015) mentioned that companies with high debt accumulatio can

reduce the tax outflow, which might help in improving their profit generation capacity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

3

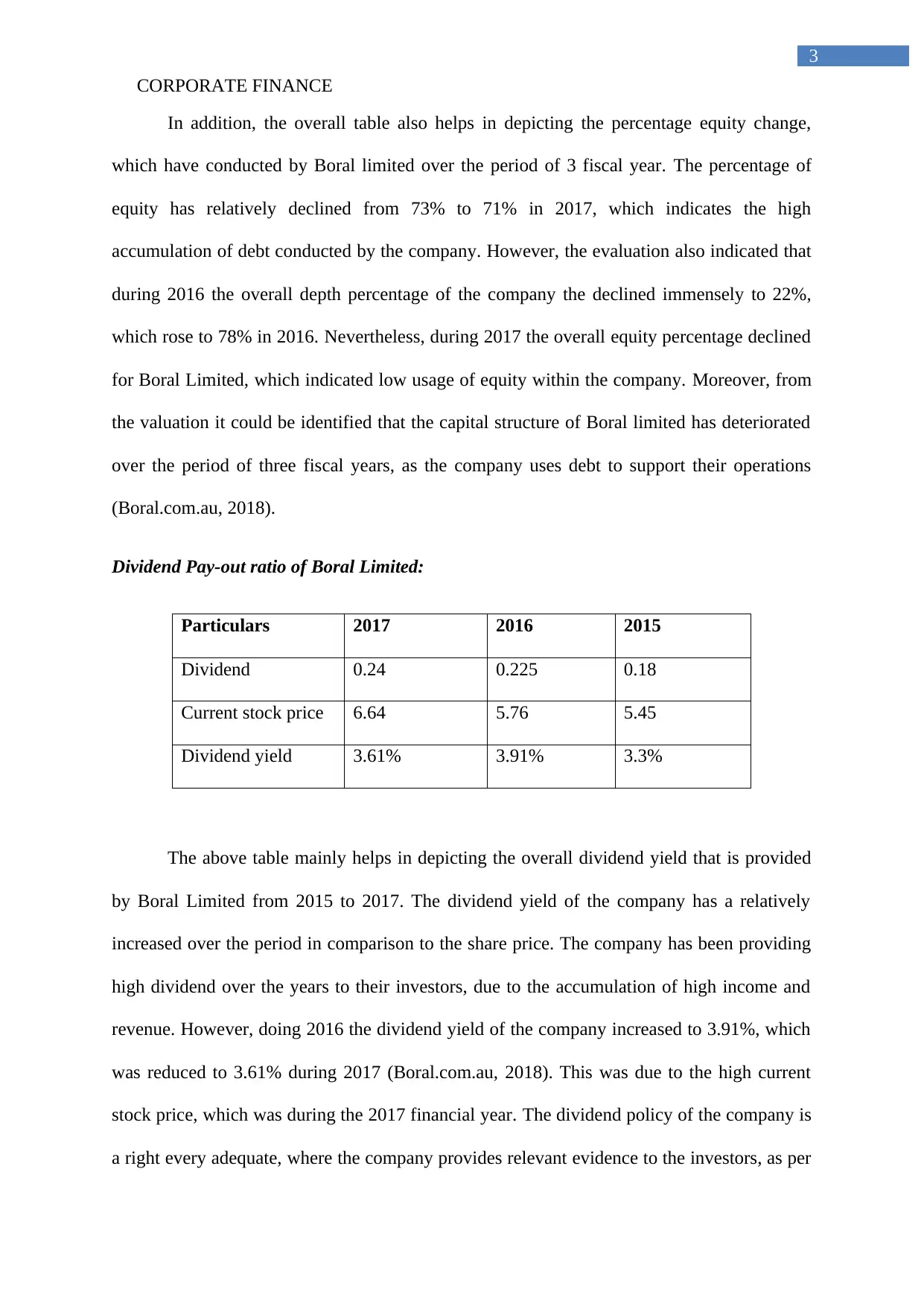

In addition, the overall table also helps in depicting the percentage equity change,

which have conducted by Boral limited over the period of 3 fiscal year. The percentage of

equity has relatively declined from 73% to 71% in 2017, which indicates the high

accumulation of debt conducted by the company. However, the evaluation also indicated that

during 2016 the overall depth percentage of the company the declined immensely to 22%,

which rose to 78% in 2016. Nevertheless, during 2017 the overall equity percentage declined

for Boral Limited, which indicated low usage of equity within the company. Moreover, from

the valuation it could be identified that the capital structure of Boral limited has deteriorated

over the period of three fiscal years, as the company uses debt to support their operations

(Boral.com.au, 2018).

Dividend Pay-out ratio of Boral Limited:

Particulars 2017 2016 2015

Dividend 0.24 0.225 0.18

Current stock price 6.64 5.76 5.45

Dividend yield 3.61% 3.91% 3.3%

The above table mainly helps in depicting the overall dividend yield that is provided

by Boral Limited from 2015 to 2017. The dividend yield of the company has a relatively

increased over the period in comparison to the share price. The company has been providing

high dividend over the years to their investors, due to the accumulation of high income and

revenue. However, doing 2016 the dividend yield of the company increased to 3.91%, which

was reduced to 3.61% during 2017 (Boral.com.au, 2018). This was due to the high current

stock price, which was during the 2017 financial year. The dividend policy of the company is

a right every adequate, where the company provides relevant evidence to the investors, as per

3

In addition, the overall table also helps in depicting the percentage equity change,

which have conducted by Boral limited over the period of 3 fiscal year. The percentage of

equity has relatively declined from 73% to 71% in 2017, which indicates the high

accumulation of debt conducted by the company. However, the evaluation also indicated that

during 2016 the overall depth percentage of the company the declined immensely to 22%,

which rose to 78% in 2016. Nevertheless, during 2017 the overall equity percentage declined

for Boral Limited, which indicated low usage of equity within the company. Moreover, from

the valuation it could be identified that the capital structure of Boral limited has deteriorated

over the period of three fiscal years, as the company uses debt to support their operations

(Boral.com.au, 2018).

Dividend Pay-out ratio of Boral Limited:

Particulars 2017 2016 2015

Dividend 0.24 0.225 0.18

Current stock price 6.64 5.76 5.45

Dividend yield 3.61% 3.91% 3.3%

The above table mainly helps in depicting the overall dividend yield that is provided

by Boral Limited from 2015 to 2017. The dividend yield of the company has a relatively

increased over the period in comparison to the share price. The company has been providing

high dividend over the years to their investors, due to the accumulation of high income and

revenue. However, doing 2016 the dividend yield of the company increased to 3.91%, which

was reduced to 3.61% during 2017 (Boral.com.au, 2018). This was due to the high current

stock price, which was during the 2017 financial year. The dividend policy of the company is

a right every adequate, where the company provides relevant evidence to the investors, as per

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

4

their income and revenue. Baker & Wurgler (2015) mentioned that investors evaluate

dividend yield of the company to determine whether there is an investment opportunity,

which could help in improving their profitability and return.

2) Evaluating the policy, drawing on practical considerations covered applied to the

company’s current characteristics and situation:

The valuation of dividend policy mainly indicates your payments that needs to be

conducted by the company to its shareholders. The relevant increment of dividend policy

between 50% to 70% of the earnings before significant items is considered in line with the

commitments of Boral Limited. Boral Limited Dividend policy never changes given with the

acquisition of headwaters which is being finalized by the organization. The board of directors

relatively determine the determinant policy, amount, nature and timing of the dividend that

needs to be paid by the company (Boral.com.au, 2018). The directors of the organization

relatively review the Dividend policy regularly in context of the group’s ability to continue its

operations. The dividend policy is actually evaluated on the basis of the cash outflow that will

be conducted by the company each year. This evaluation helps the organization to detect

whether relevant investment opportunities or dividend payments needs to be conducted by the

company over the period. Moreover, the directors need to take adequate decision regarding

the investments conducted for growing the business to enhance shareholder value. This

decision is fully based on capability of the company to conduct its business in future fiscal

years. In this context, Baghai, Servaes & Tamayo (2014) mentioned that companies with

adequate dividend policy can maintain adequate cash flow, which could help them reduce the

problems related to cash stagnation.

The capital structure of the organization is relatively based on the decisions made by

directors regarding the current condition of the organization. In addition, adequate capital

4

their income and revenue. Baker & Wurgler (2015) mentioned that investors evaluate

dividend yield of the company to determine whether there is an investment opportunity,

which could help in improving their profitability and return.

2) Evaluating the policy, drawing on practical considerations covered applied to the

company’s current characteristics and situation:

The valuation of dividend policy mainly indicates your payments that needs to be

conducted by the company to its shareholders. The relevant increment of dividend policy

between 50% to 70% of the earnings before significant items is considered in line with the

commitments of Boral Limited. Boral Limited Dividend policy never changes given with the

acquisition of headwaters which is being finalized by the organization. The board of directors

relatively determine the determinant policy, amount, nature and timing of the dividend that

needs to be paid by the company (Boral.com.au, 2018). The directors of the organization

relatively review the Dividend policy regularly in context of the group’s ability to continue its

operations. The dividend policy is actually evaluated on the basis of the cash outflow that will

be conducted by the company each year. This evaluation helps the organization to detect

whether relevant investment opportunities or dividend payments needs to be conducted by the

company over the period. Moreover, the directors need to take adequate decision regarding

the investments conducted for growing the business to enhance shareholder value. This

decision is fully based on capability of the company to conduct its business in future fiscal

years. In this context, Baghai, Servaes & Tamayo (2014) mentioned that companies with

adequate dividend policy can maintain adequate cash flow, which could help them reduce the

problems related to cash stagnation.

The capital structure of the organization is relatively based on the decisions made by

directors regarding the current condition of the organization. In addition, adequate capital

CORPORATE FINANCE

5

structure is followed by increasing both equity and debt of the organization at the same time.

The debt position of the company is not increased abruptly without the increment of equity

position, which helps in maintaining adequate weightage and ratio (Boral.com.au, 2018).

Task 2: Capital Budgeting Task

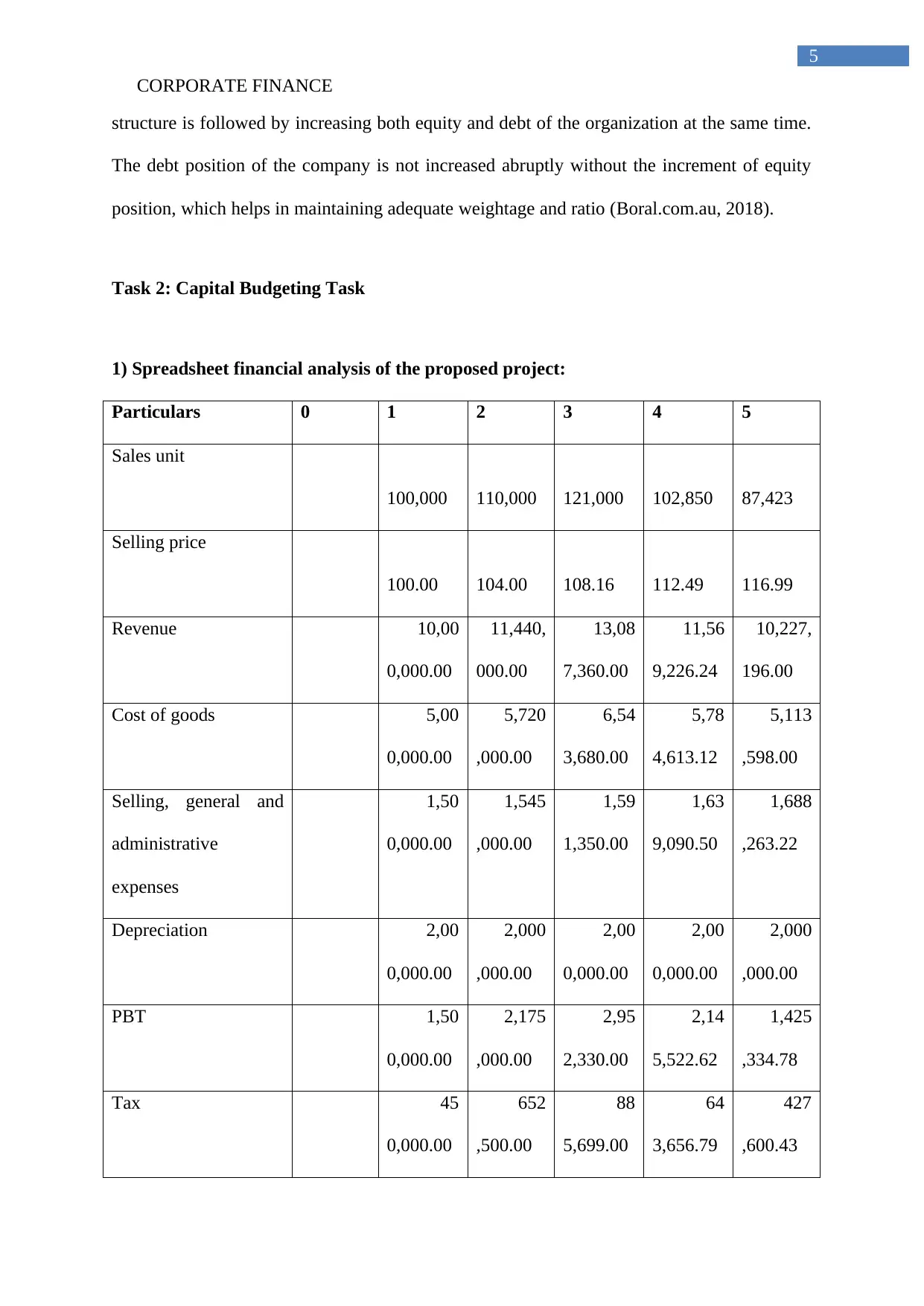

1) Spreadsheet financial analysis of the proposed project:

Particulars 0 1 2 3 4 5

Sales unit

100,000 110,000 121,000 102,850 87,423

Selling price

100.00 104.00 108.16 112.49 116.99

Revenue 10,00

0,000.00

11,440,

000.00

13,08

7,360.00

11,56

9,226.24

10,227,

196.00

Cost of goods 5,00

0,000.00

5,720

,000.00

6,54

3,680.00

5,78

4,613.12

5,113

,598.00

Selling, general and

administrative

expenses

1,50

0,000.00

1,545

,000.00

1,59

1,350.00

1,63

9,090.50

1,688

,263.22

Depreciation 2,00

0,000.00

2,000

,000.00

2,00

0,000.00

2,00

0,000.00

2,000

,000.00

PBT 1,50

0,000.00

2,175

,000.00

2,95

2,330.00

2,14

5,522.62

1,425

,334.78

Tax 45

0,000.00

652

,500.00

88

5,699.00

64

3,656.79

427

,600.43

5

structure is followed by increasing both equity and debt of the organization at the same time.

The debt position of the company is not increased abruptly without the increment of equity

position, which helps in maintaining adequate weightage and ratio (Boral.com.au, 2018).

Task 2: Capital Budgeting Task

1) Spreadsheet financial analysis of the proposed project:

Particulars 0 1 2 3 4 5

Sales unit

100,000 110,000 121,000 102,850 87,423

Selling price

100.00 104.00 108.16 112.49 116.99

Revenue 10,00

0,000.00

11,440,

000.00

13,08

7,360.00

11,56

9,226.24

10,227,

196.00

Cost of goods 5,00

0,000.00

5,720

,000.00

6,54

3,680.00

5,78

4,613.12

5,113

,598.00

Selling, general and

administrative

expenses

1,50

0,000.00

1,545

,000.00

1,59

1,350.00

1,63

9,090.50

1,688

,263.22

Depreciation 2,00

0,000.00

2,000

,000.00

2,00

0,000.00

2,00

0,000.00

2,000

,000.00

PBT 1,50

0,000.00

2,175

,000.00

2,95

2,330.00

2,14

5,522.62

1,425

,334.78

Tax 45

0,000.00

652

,500.00

88

5,699.00

64

3,656.79

427

,600.43

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

6

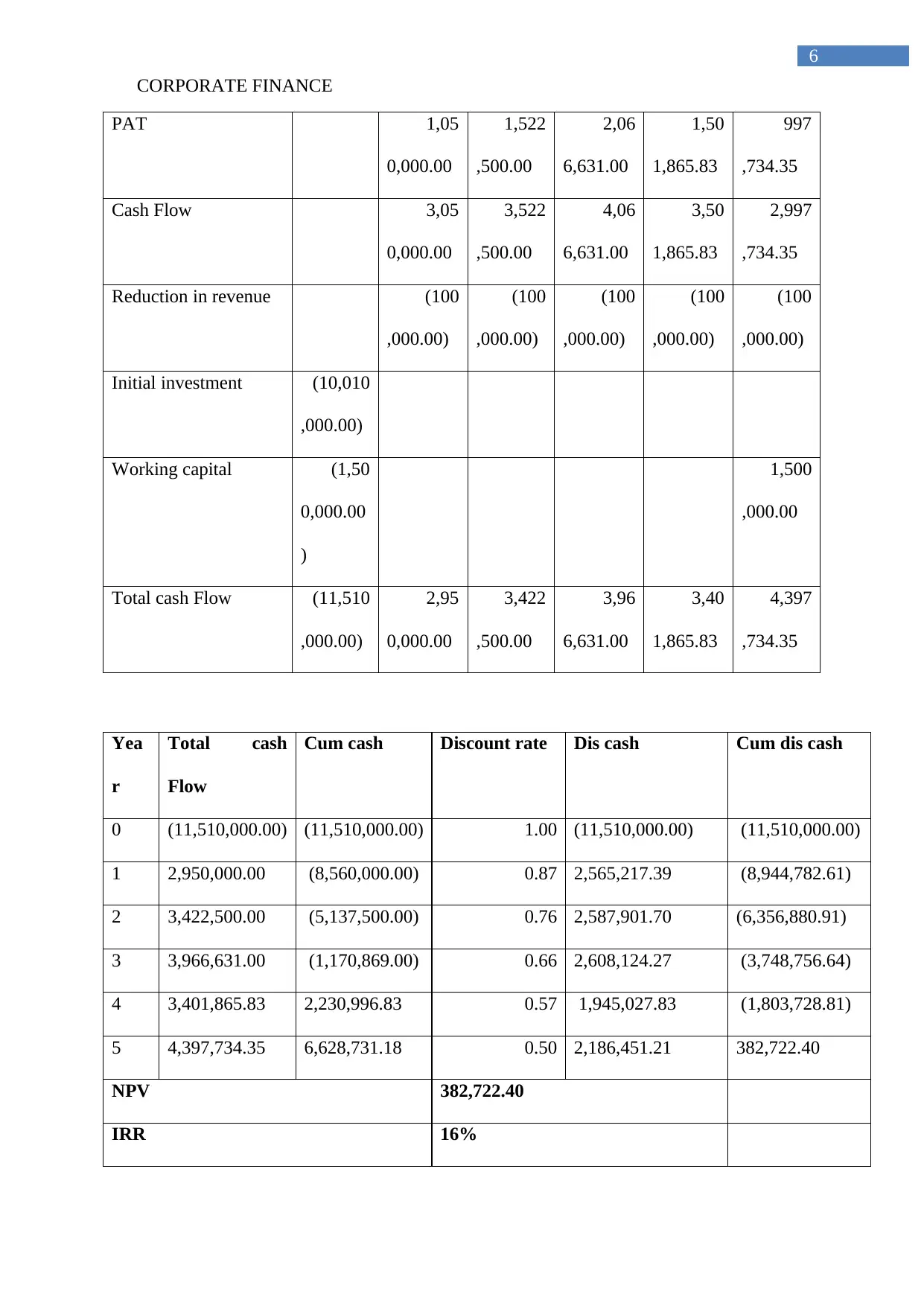

PAT 1,05

0,000.00

1,522

,500.00

2,06

6,631.00

1,50

1,865.83

997

,734.35

Cash Flow 3,05

0,000.00

3,522

,500.00

4,06

6,631.00

3,50

1,865.83

2,997

,734.35

Reduction in revenue (100

,000.00)

(100

,000.00)

(100

,000.00)

(100

,000.00)

(100

,000.00)

Initial investment (10,010

,000.00)

Working capital (1,50

0,000.00

)

1,500

,000.00

Total cash Flow (11,510

,000.00)

2,95

0,000.00

3,422

,500.00

3,96

6,631.00

3,40

1,865.83

4,397

,734.35

Yea

r

Total cash

Flow

Cum cash Discount rate Dis cash Cum dis cash

0 (11,510,000.00) (11,510,000.00) 1.00 (11,510,000.00) (11,510,000.00)

1 2,950,000.00 (8,560,000.00) 0.87 2,565,217.39 (8,944,782.61)

2 3,422,500.00 (5,137,500.00) 0.76 2,587,901.70 (6,356,880.91)

3 3,966,631.00 (1,170,869.00) 0.66 2,608,124.27 (3,748,756.64)

4 3,401,865.83 2,230,996.83 0.57 1,945,027.83 (1,803,728.81)

5 4,397,734.35 6,628,731.18 0.50 2,186,451.21 382,722.40

NPV 382,722.40

IRR 16%

6

PAT 1,05

0,000.00

1,522

,500.00

2,06

6,631.00

1,50

1,865.83

997

,734.35

Cash Flow 3,05

0,000.00

3,522

,500.00

4,06

6,631.00

3,50

1,865.83

2,997

,734.35

Reduction in revenue (100

,000.00)

(100

,000.00)

(100

,000.00)

(100

,000.00)

(100

,000.00)

Initial investment (10,010

,000.00)

Working capital (1,50

0,000.00

)

1,500

,000.00

Total cash Flow (11,510

,000.00)

2,95

0,000.00

3,422

,500.00

3,96

6,631.00

3,40

1,865.83

4,397

,734.35

Yea

r

Total cash

Flow

Cum cash Discount rate Dis cash Cum dis cash

0 (11,510,000.00) (11,510,000.00) 1.00 (11,510,000.00) (11,510,000.00)

1 2,950,000.00 (8,560,000.00) 0.87 2,565,217.39 (8,944,782.61)

2 3,422,500.00 (5,137,500.00) 0.76 2,587,901.70 (6,356,880.91)

3 3,966,631.00 (1,170,869.00) 0.66 2,608,124.27 (3,748,756.64)

4 3,401,865.83 2,230,996.83 0.57 1,945,027.83 (1,803,728.81)

5 4,397,734.35 6,628,731.18 0.50 2,186,451.21 382,722.40

NPV 382,722.40

IRR 16%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

7

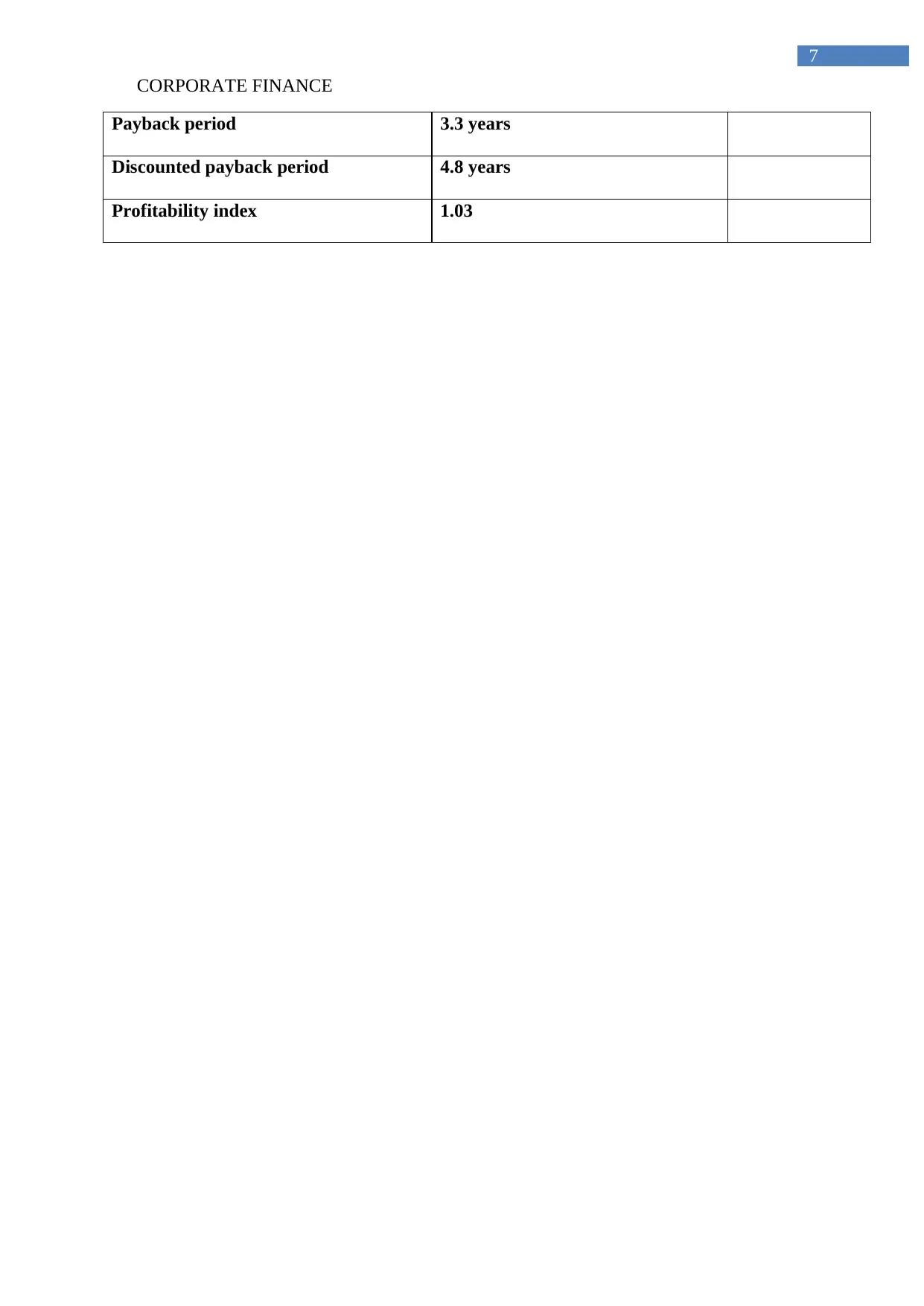

Payback period 3.3 years

Discounted payback period 4.8 years

Profitability index 1.03

7

Payback period 3.3 years

Discounted payback period 4.8 years

Profitability index 1.03

CORPORATE FINANCE

8

2) Memo to the CEO addressing, explaining, and justifying the chosen methods:

Memorandum

To: CEO of Masters Limited

From: Project Analyst

Date: 25-03-2018

Subject: Recommendation for choosing the appropriate method

The capital budgeting decision that needs to be conducted for Master Limited can be

conducted with the help of Net Present Value (NPV), Internal Rate of Return (IRR), Payback

period, Discounted payback period and Profitability index. The above-mentioned investment appraisal

techniques could eventually help in detecting the actual financial condition of the proposed project. In

addition, the presented scenario of the project is being evaluated, which indicates the position

qualities of the investment. Moreover, the building lease income, which is being accumulated by the

Master limited is considered as the expenses in the project for deriving the actual income generated

from investment. the expenses of $100,000 is been detected from the cash flow of the company to

compensate the loss in income generated from each year by renting the place. The assumption

considered in the project evaluation is according to the laid down assumptions.

The initial investment of the project is mainly calculated by adding the plant, equipment,

consultation fees and working capital cost. The total initial investment is at the levels of

11,510,000, which is needed for the project to commence and start. The working capital

requirement is at the level of 15% of the revenue generated in 1st year. This initial investment

conducted in year 0 might help in reducing the actual financial position of the project in

generating high rate of returns.

The total revenue is calculated from the rising sales and selling price of the project over the

period of five years. In addition, the cost of goods is assumed to be at the levels, of 50% of

the revenue, which will be generated from investment. Moreover, the depreciation is

8

2) Memo to the CEO addressing, explaining, and justifying the chosen methods:

Memorandum

To: CEO of Masters Limited

From: Project Analyst

Date: 25-03-2018

Subject: Recommendation for choosing the appropriate method

The capital budgeting decision that needs to be conducted for Master Limited can be

conducted with the help of Net Present Value (NPV), Internal Rate of Return (IRR), Payback

period, Discounted payback period and Profitability index. The above-mentioned investment appraisal

techniques could eventually help in detecting the actual financial condition of the proposed project. In

addition, the presented scenario of the project is being evaluated, which indicates the position

qualities of the investment. Moreover, the building lease income, which is being accumulated by the

Master limited is considered as the expenses in the project for deriving the actual income generated

from investment. the expenses of $100,000 is been detected from the cash flow of the company to

compensate the loss in income generated from each year by renting the place. The assumption

considered in the project evaluation is according to the laid down assumptions.

The initial investment of the project is mainly calculated by adding the plant, equipment,

consultation fees and working capital cost. The total initial investment is at the levels of

11,510,000, which is needed for the project to commence and start. The working capital

requirement is at the level of 15% of the revenue generated in 1st year. This initial investment

conducted in year 0 might help in reducing the actual financial position of the project in

generating high rate of returns.

The total revenue is calculated from the rising sales and selling price of the project over the

period of five years. In addition, the cost of goods is assumed to be at the levels, of 50% of

the revenue, which will be generated from investment. Moreover, the depreciation is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

9

calculated to be at straight line for the duration of the project. The Selling, general and

administrative expenses is assumed to rise at the levels of 3% per year. The assumption of cash inflow

and outflow is conducted to determine the actual cash inflow of the project over the period of five

fiscal years.

The above-mentioned assumptions of cash inflow and outflow mainly helps in deriving the

overall investment appraisal techniques, which could help in detecting actual financial

capability of the project. From the overall evaluation discounting rate is detected to be at the

levels of 15% and tax rate is detected to be at 30%. This measure of adequate calculation

might help in identifying the actual value of the cash inflow conducted by the company over

the period of five fiscal year. The NPV calculation is detected to be at 382,722.40, which

helps in discounting the cash inflow of the company over the period of 5 fiscal year. In

addition, the internal rate of return for the project is calculated to be at the levels of 16%,

which is relevantly higher than the discounting rate of the project. Moreover, the high internal

rate of return could eventually allow the investor in generating high level of returns from

investment.

The payback period is detected to be at the level of 3.3 years, while the discounted payback

period is at 4.8 years. This relevantly indicates that investment of the project is accumulated

before its completion, which depicts its viability. Therefore, from the evaluation of payback

period project is considered a viable investment options, which could help Masters Limited to

increase the return from investment in future. The discounted payback period mainly

accommodates the time value of money and represent the actual time in which initial

investment will be collected from the investment.

The calculation of profitability index might help in detecting the overall profits, which will be

generated from investment of project. Th profitability index is mainly detected to be at the

levels of 1.03, which is higher than 1 and indicates the profits that will be generated from

investment. the profitability index is derived by deducting NPV with the initial investments,

9

calculated to be at straight line for the duration of the project. The Selling, general and

administrative expenses is assumed to rise at the levels of 3% per year. The assumption of cash inflow

and outflow is conducted to determine the actual cash inflow of the project over the period of five

fiscal years.

The above-mentioned assumptions of cash inflow and outflow mainly helps in deriving the

overall investment appraisal techniques, which could help in detecting actual financial

capability of the project. From the overall evaluation discounting rate is detected to be at the

levels of 15% and tax rate is detected to be at 30%. This measure of adequate calculation

might help in identifying the actual value of the cash inflow conducted by the company over

the period of five fiscal year. The NPV calculation is detected to be at 382,722.40, which

helps in discounting the cash inflow of the company over the period of 5 fiscal year. In

addition, the internal rate of return for the project is calculated to be at the levels of 16%,

which is relevantly higher than the discounting rate of the project. Moreover, the high internal

rate of return could eventually allow the investor in generating high level of returns from

investment.

The payback period is detected to be at the level of 3.3 years, while the discounted payback

period is at 4.8 years. This relevantly indicates that investment of the project is accumulated

before its completion, which depicts its viability. Therefore, from the evaluation of payback

period project is considered a viable investment options, which could help Masters Limited to

increase the return from investment in future. The discounted payback period mainly

accommodates the time value of money and represent the actual time in which initial

investment will be collected from the investment.

The calculation of profitability index might help in detecting the overall profits, which will be

generated from investment of project. Th profitability index is mainly detected to be at the

levels of 1.03, which is higher than 1 and indicates the profits that will be generated from

investment. the profitability index is derived by deducting NPV with the initial investments,

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.