Financial Analysis of Corporate Funding, Liabilities, and Assets

VerifiedAdded on 2022/08/19

|13

|2477

|12

Report

AI Summary

This report provides a detailed analysis of the financial statements of Westpac and National Australia Bank, two prominent Australian financial institutions. It examines their sources of funds, identifying deposits, borrowings, and equity as key components, and analyzes the evolution of these funding sources over a three-year period. The report delves into the merits and shortcomings of different funding sources, including equity and debt, and examines the composition of the companies' liabilities, including provisions and contingent liabilities, with reference to AASB 137. Furthermore, it identifies the different categories of assets recorded by the companies and critically examines the measurement basis used for each class of assets. The analysis highlights similarities in the financial structures of both organizations, providing insights into their financial management and reporting practices. The report concludes by summarizing the key findings and observations regarding the financial performance and position of these two major players in the Australian financial sector.

CORPORATE ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

The financial statements aid the stakeholders of the business in the decision making process

and must be mandatorily and efficiently prepared by the management of the entities. The

report evaluates the various facets of the financial statements of the two renowned

organisations from the financial sector of Australia, namely the Westpac and the National

Australia Bank. The sources of funds is examined to conclude that the deposits and

borrowings form the major part of the funding of the both entities. In addition, the pros and

cons of each source of funds has been provided. Further the report examines the assets and

liabilities of the organisations, and the composition of the same. In addition to the above,

there is a specific section for the analysis of the provisions and the contingent liabilities of the

organisations.

The financial statements aid the stakeholders of the business in the decision making process

and must be mandatorily and efficiently prepared by the management of the entities. The

report evaluates the various facets of the financial statements of the two renowned

organisations from the financial sector of Australia, namely the Westpac and the National

Australia Bank. The sources of funds is examined to conclude that the deposits and

borrowings form the major part of the funding of the both entities. In addition, the pros and

cons of each source of funds has been provided. Further the report examines the assets and

liabilities of the organisations, and the composition of the same. In addition to the above,

there is a specific section for the analysis of the provisions and the contingent liabilities of the

organisations.

Contents

Introduction................................................................................................................................3

Identification of the sources of funds.........................................................................................3

Evolution of sources of funds....................................................................................................4

Identification of percentage of fund...........................................................................................4

Merits and shortcomings of different sources of funds..............................................................5

Examination of different types of liabilities...............................................................................6

Examination of key provisions under AASB 137 Provisions, contingent assets and liabilities 7

Different categories of assets as being recorded by companies.................................................9

Critical Examination of the Measurement basis......................................................................10

Conclusion................................................................................................................................10

References................................................................................................................................11

Introduction................................................................................................................................3

Identification of the sources of funds.........................................................................................3

Evolution of sources of funds....................................................................................................4

Identification of percentage of fund...........................................................................................4

Merits and shortcomings of different sources of funds..............................................................5

Examination of different types of liabilities...............................................................................6

Examination of key provisions under AASB 137 Provisions, contingent assets and liabilities 7

Different categories of assets as being recorded by companies.................................................9

Critical Examination of the Measurement basis......................................................................10

Conclusion................................................................................................................................10

References................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The decision of financing is one of the most significant strategic business decisions. These

decisions are dependent on numerous factors, such as the objectives of the company, political

and economic environment, interest of the investors, legal regulations and others. In addition,

the vitality of the said decisions lies in the fact that these are irreversible decisions and

involves huge fun ds and legal compliances. The objective of the following assignment is to

evaluate the various aspects of the sources of the funds of the two renowned companies

namely the National Australia Bank and the Westpac, the stock of whose are listed on the

Australian Stock Exchange. In addition, the report would shed light on the application of the

AASB 137 ‘Provisions, Contingent Liabilities and Contingent Assets.’

Both the selected organisations belong to the financial industry and stand in the top four of

the country’s banks list. The entity National Australia Ba1nk (NAB) is engaged in the

provision of the personal, business and corporate financial service solutions (National

Australia Bank, 2020). While the personal financing solutions involve the services like

personal banking, personal loans, credit cards and others, the business solutions include

superannuation and insurance and other services. The other organisation that is Westpac has a

similar services to provide. The organisation Westpac was originally established in the year

1817 and the name of the organisation was changed to Westpac in the year 1982 (Westpac,

2020).

Identification of the sources of funds

The chief source of finance of the Westpac bank has been analysed to be the deposits and the

borrowings, followed by the Share Capital. It has been assessed from the balance sheet of

Westpac for the year 2019 that out of the total liabilities of $ 841119 million, the deposits,

and borrowings amount to $ 563247 million (Westpac, 2019). The second key source of

outside source of finance for both the organisations is that of the debt issues which includes

bonds, notes and subordinate sources of finance. The capital structure of the National

Australian Bank has the similar composition where the deposits and other borrowings amount

to $ 522085 million out of total liabilities of $ 791520 (National Australia Bank, 2019). Thus,

it can be stated that the outside borrowings and deposits are the main sources of funds for

both the organisations. The third key source of finance is the ordinary share capital, the

retained profits and the reserves for the both of the organisations.

The decision of financing is one of the most significant strategic business decisions. These

decisions are dependent on numerous factors, such as the objectives of the company, political

and economic environment, interest of the investors, legal regulations and others. In addition,

the vitality of the said decisions lies in the fact that these are irreversible decisions and

involves huge fun ds and legal compliances. The objective of the following assignment is to

evaluate the various aspects of the sources of the funds of the two renowned companies

namely the National Australia Bank and the Westpac, the stock of whose are listed on the

Australian Stock Exchange. In addition, the report would shed light on the application of the

AASB 137 ‘Provisions, Contingent Liabilities and Contingent Assets.’

Both the selected organisations belong to the financial industry and stand in the top four of

the country’s banks list. The entity National Australia Ba1nk (NAB) is engaged in the

provision of the personal, business and corporate financial service solutions (National

Australia Bank, 2020). While the personal financing solutions involve the services like

personal banking, personal loans, credit cards and others, the business solutions include

superannuation and insurance and other services. The other organisation that is Westpac has a

similar services to provide. The organisation Westpac was originally established in the year

1817 and the name of the organisation was changed to Westpac in the year 1982 (Westpac,

2020).

Identification of the sources of funds

The chief source of finance of the Westpac bank has been analysed to be the deposits and the

borrowings, followed by the Share Capital. It has been assessed from the balance sheet of

Westpac for the year 2019 that out of the total liabilities of $ 841119 million, the deposits,

and borrowings amount to $ 563247 million (Westpac, 2019). The second key source of

outside source of finance for both the organisations is that of the debt issues which includes

bonds, notes and subordinate sources of finance. The capital structure of the National

Australian Bank has the similar composition where the deposits and other borrowings amount

to $ 522085 million out of total liabilities of $ 791520 (National Australia Bank, 2019). Thus,

it can be stated that the outside borrowings and deposits are the main sources of funds for

both the organisations. The third key source of finance is the ordinary share capital, the

retained profits and the reserves for the both of the organisations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

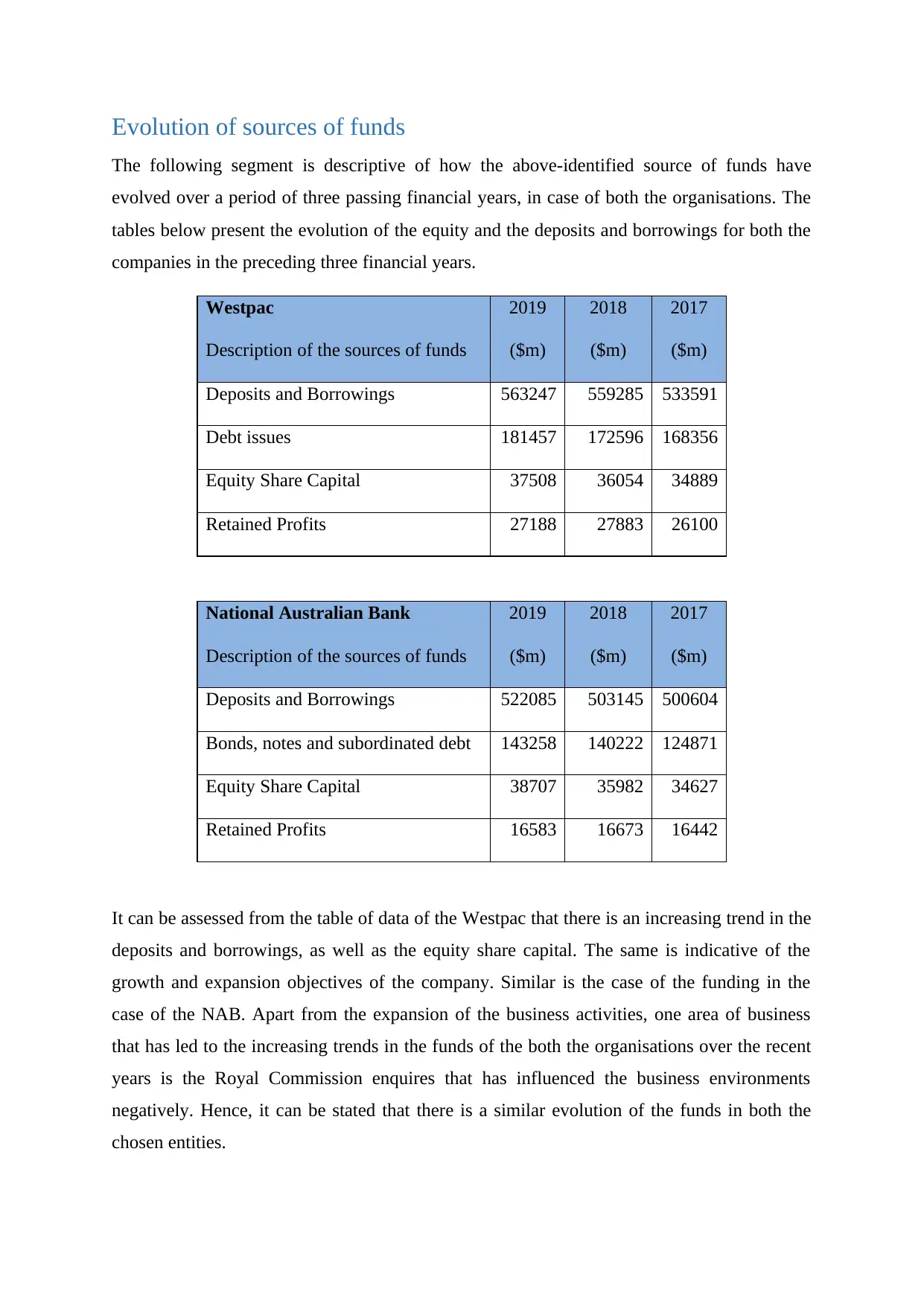

Evolution of sources of funds

The following segment is descriptive of how the above-identified source of funds have

evolved over a period of three passing financial years, in case of both the organisations. The

tables below present the evolution of the equity and the deposits and borrowings for both the

companies in the preceding three financial years.

Westpac

Description of the sources of funds

2019

($m)

2018

($m)

2017

($m)

Deposits and Borrowings 563247 559285 533591

Debt issues 181457 172596 168356

Equity Share Capital 37508 36054 34889

Retained Profits 27188 27883 26100

National Australian Bank

Description of the sources of funds

2019

($m)

2018

($m)

2017

($m)

Deposits and Borrowings 522085 503145 500604

Bonds, notes and subordinated debt 143258 140222 124871

Equity Share Capital 38707 35982 34627

Retained Profits 16583 16673 16442

It can be assessed from the table of data of the Westpac that there is an increasing trend in the

deposits and borrowings, as well as the equity share capital. The same is indicative of the

growth and expansion objectives of the company. Similar is the case of the funding in the

case of the NAB. Apart from the expansion of the business activities, one area of business

that has led to the increasing trends in the funds of the both the organisations over the recent

years is the Royal Commission enquires that has influenced the business environments

negatively. Hence, it can be stated that there is a similar evolution of the funds in both the

chosen entities.

The following segment is descriptive of how the above-identified source of funds have

evolved over a period of three passing financial years, in case of both the organisations. The

tables below present the evolution of the equity and the deposits and borrowings for both the

companies in the preceding three financial years.

Westpac

Description of the sources of funds

2019

($m)

2018

($m)

2017

($m)

Deposits and Borrowings 563247 559285 533591

Debt issues 181457 172596 168356

Equity Share Capital 37508 36054 34889

Retained Profits 27188 27883 26100

National Australian Bank

Description of the sources of funds

2019

($m)

2018

($m)

2017

($m)

Deposits and Borrowings 522085 503145 500604

Bonds, notes and subordinated debt 143258 140222 124871

Equity Share Capital 38707 35982 34627

Retained Profits 16583 16673 16442

It can be assessed from the table of data of the Westpac that there is an increasing trend in the

deposits and borrowings, as well as the equity share capital. The same is indicative of the

growth and expansion objectives of the company. Similar is the case of the funding in the

case of the NAB. Apart from the expansion of the business activities, one area of business

that has led to the increasing trends in the funds of the both the organisations over the recent

years is the Royal Commission enquires that has influenced the business environments

negatively. Hence, it can be stated that there is a similar evolution of the funds in both the

chosen entities.

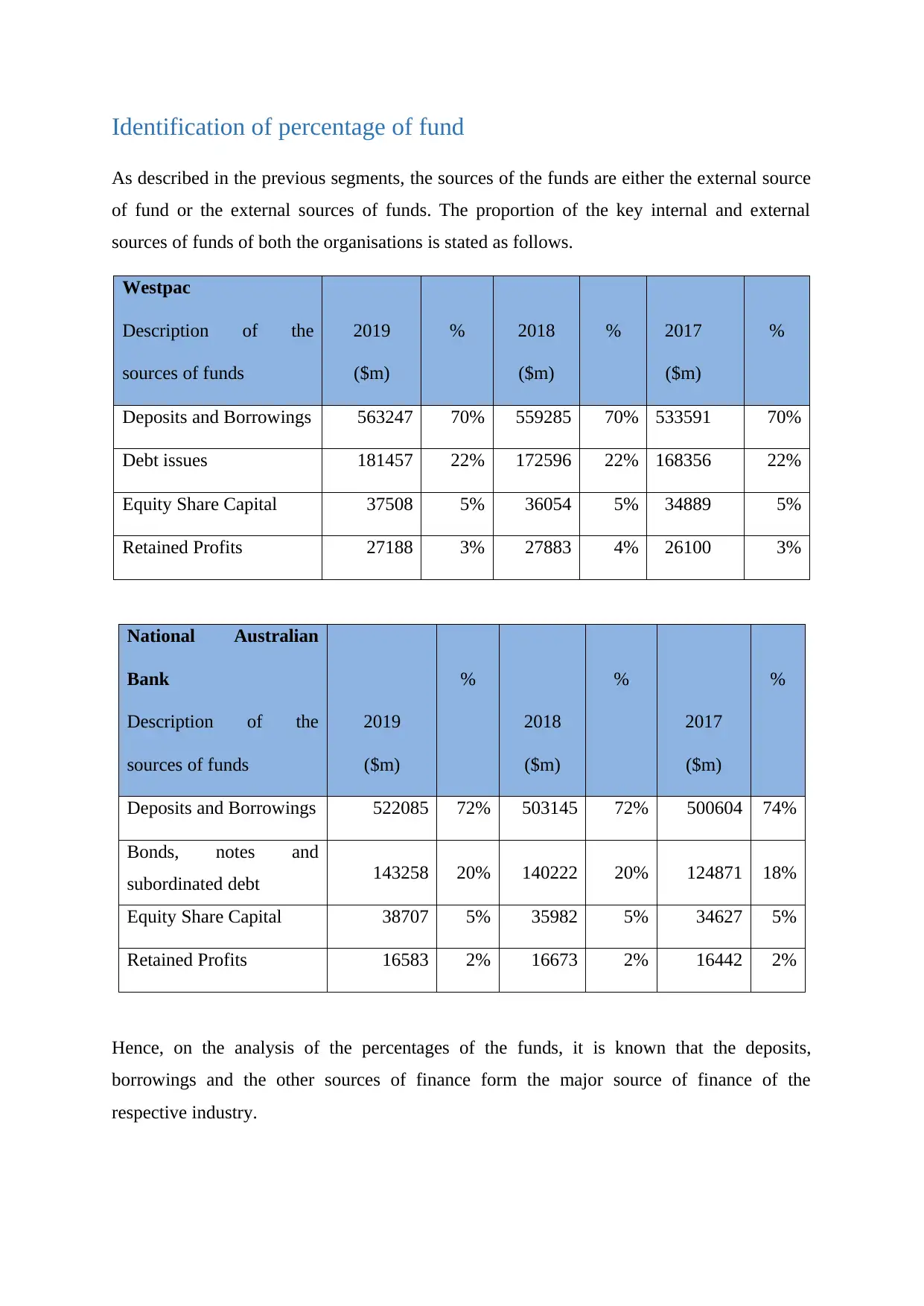

Identification of percentage of fund

As described in the previous segments, the sources of the funds are either the external source

of fund or the external sources of funds. The proportion of the key internal and external

sources of funds of both the organisations is stated as follows.

Westpac

Description of the

sources of funds

2019

($m)

% 2018

($m)

% 2017

($m)

%

Deposits and Borrowings 563247 70% 559285 70% 533591 70%

Debt issues 181457 22% 172596 22% 168356 22%

Equity Share Capital 37508 5% 36054 5% 34889 5%

Retained Profits 27188 3% 27883 4% 26100 3%

National Australian

Bank

Description of the

sources of funds

2019

($m)

%

2018

($m)

%

2017

($m)

%

Deposits and Borrowings 522085 72% 503145 72% 500604 74%

Bonds, notes and

subordinated debt 143258 20% 140222 20% 124871 18%

Equity Share Capital 38707 5% 35982 5% 34627 5%

Retained Profits 16583 2% 16673 2% 16442 2%

Hence, on the analysis of the percentages of the funds, it is known that the deposits,

borrowings and the other sources of finance form the major source of finance of the

respective industry.

As described in the previous segments, the sources of the funds are either the external source

of fund or the external sources of funds. The proportion of the key internal and external

sources of funds of both the organisations is stated as follows.

Westpac

Description of the

sources of funds

2019

($m)

% 2018

($m)

% 2017

($m)

%

Deposits and Borrowings 563247 70% 559285 70% 533591 70%

Debt issues 181457 22% 172596 22% 168356 22%

Equity Share Capital 37508 5% 36054 5% 34889 5%

Retained Profits 27188 3% 27883 4% 26100 3%

National Australian

Bank

Description of the

sources of funds

2019

($m)

%

2018

($m)

%

2017

($m)

%

Deposits and Borrowings 522085 72% 503145 72% 500604 74%

Bonds, notes and

subordinated debt 143258 20% 140222 20% 124871 18%

Equity Share Capital 38707 5% 35982 5% 34627 5%

Retained Profits 16583 2% 16673 2% 16442 2%

Hence, on the analysis of the percentages of the funds, it is known that the deposits,

borrowings and the other sources of finance form the major source of finance of the

respective industry.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Merits and shortcomings of different sources of funds

The two key sources of funds that have been used are in the form of debt- long term and short

term and the owners’ equity.

Merits of equity

The advantages of the share capital as the source of finance is that it is less risky because of

the absence of the fixed monthly repayments. In addition, the companies do not need

necessarily to get bothered of the credit ratings to garner the capital contribution (Robinson

et. al, 2015). Further benefit is in the fact that the cash remains in the business and useful for

the organisations where the owners have the long term view from the investments made.

Shortcomings of equity

In spite of the above mentioned advantages, there are few limitations as well of the equity

financing. These are that the equity financing generally has a higher cost because of the

expectations of the profit sharing and the absence of the tax benefits on the dividend

payments. In addition, this leads to the dilution of control.

Merits of debt

The key benefits of the short term and the long term sources of finances is that the control is

retained by the owners of the entity, and as the interest payments are tax deductible, the

organisations save the taxes on the profits (Williams and Dobelman, 2017). In addition, the

borrowings can be availed as per the needs and requirements to be long term, medium term or

the short term.

Shortcomings of debt financing

The debt financing suffers shortcomings in the form of fixed interest payments irrespective of

the profits earned by the entity, and the cash flowing out of the entity in the form of the

mandatory periodical payments. Thus, there is a higher risk associated in the debt financing.

Examination of different types of liabilities

The composition of the liabilities of both the companies has been highlighted through the

glimpse of the financial statements of the both entities as provided below.

The two key sources of funds that have been used are in the form of debt- long term and short

term and the owners’ equity.

Merits of equity

The advantages of the share capital as the source of finance is that it is less risky because of

the absence of the fixed monthly repayments. In addition, the companies do not need

necessarily to get bothered of the credit ratings to garner the capital contribution (Robinson

et. al, 2015). Further benefit is in the fact that the cash remains in the business and useful for

the organisations where the owners have the long term view from the investments made.

Shortcomings of equity

In spite of the above mentioned advantages, there are few limitations as well of the equity

financing. These are that the equity financing generally has a higher cost because of the

expectations of the profit sharing and the absence of the tax benefits on the dividend

payments. In addition, this leads to the dilution of control.

Merits of debt

The key benefits of the short term and the long term sources of finances is that the control is

retained by the owners of the entity, and as the interest payments are tax deductible, the

organisations save the taxes on the profits (Williams and Dobelman, 2017). In addition, the

borrowings can be availed as per the needs and requirements to be long term, medium term or

the short term.

Shortcomings of debt financing

The debt financing suffers shortcomings in the form of fixed interest payments irrespective of

the profits earned by the entity, and the cash flowing out of the entity in the form of the

mandatory periodical payments. Thus, there is a higher risk associated in the debt financing.

Examination of different types of liabilities

The composition of the liabilities of both the companies has been highlighted through the

glimpse of the financial statements of the both entities as provided below.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

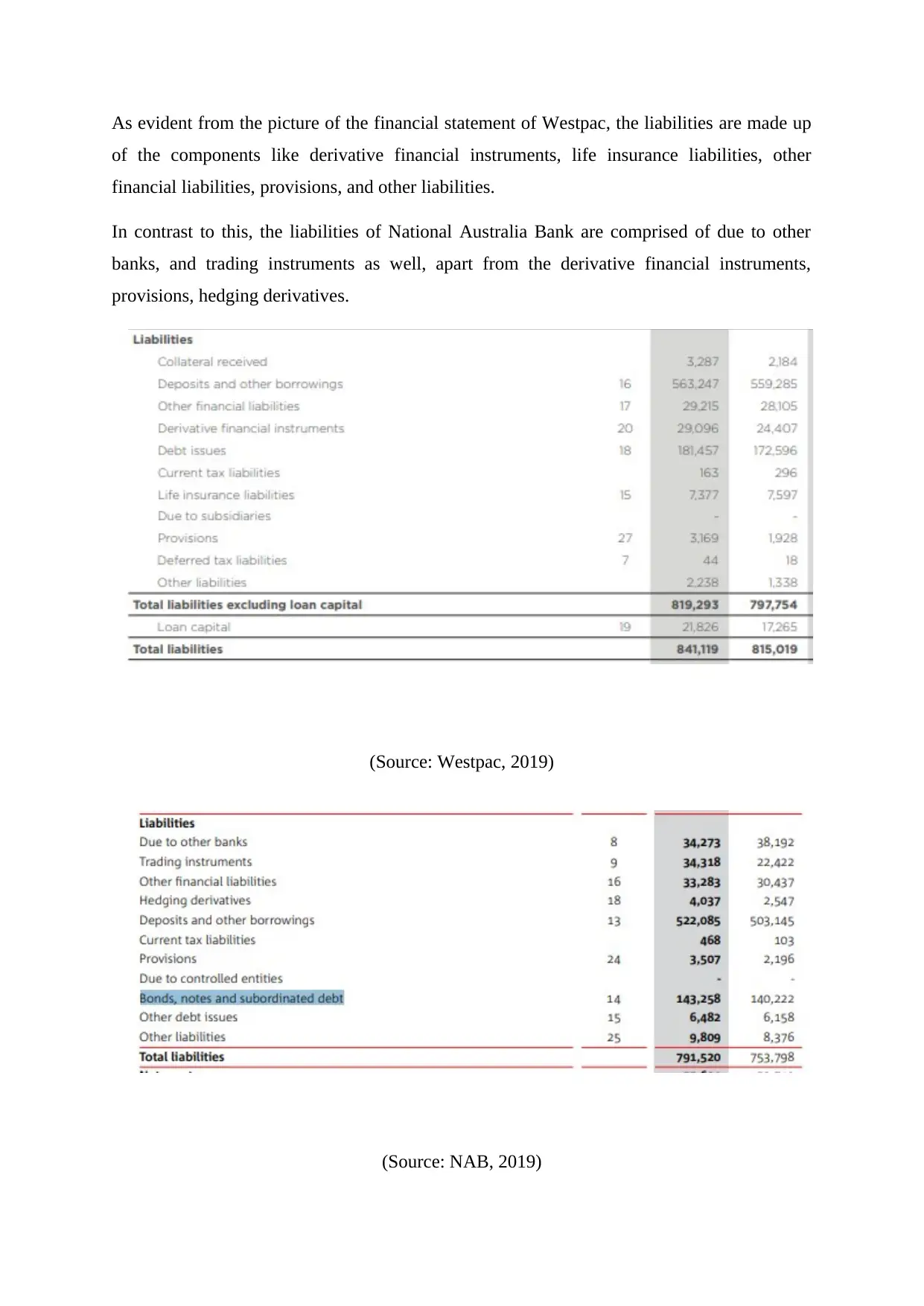

As evident from the picture of the financial statement of Westpac, the liabilities are made up

of the components like derivative financial instruments, life insurance liabilities, other

financial liabilities, provisions, and other liabilities.

In contrast to this, the liabilities of National Australia Bank are comprised of due to other

banks, and trading instruments as well, apart from the derivative financial instruments,

provisions, hedging derivatives.

(Source: Westpac, 2019)

(Source: NAB, 2019)

of the components like derivative financial instruments, life insurance liabilities, other

financial liabilities, provisions, and other liabilities.

In contrast to this, the liabilities of National Australia Bank are comprised of due to other

banks, and trading instruments as well, apart from the derivative financial instruments,

provisions, hedging derivatives.

(Source: Westpac, 2019)

(Source: NAB, 2019)

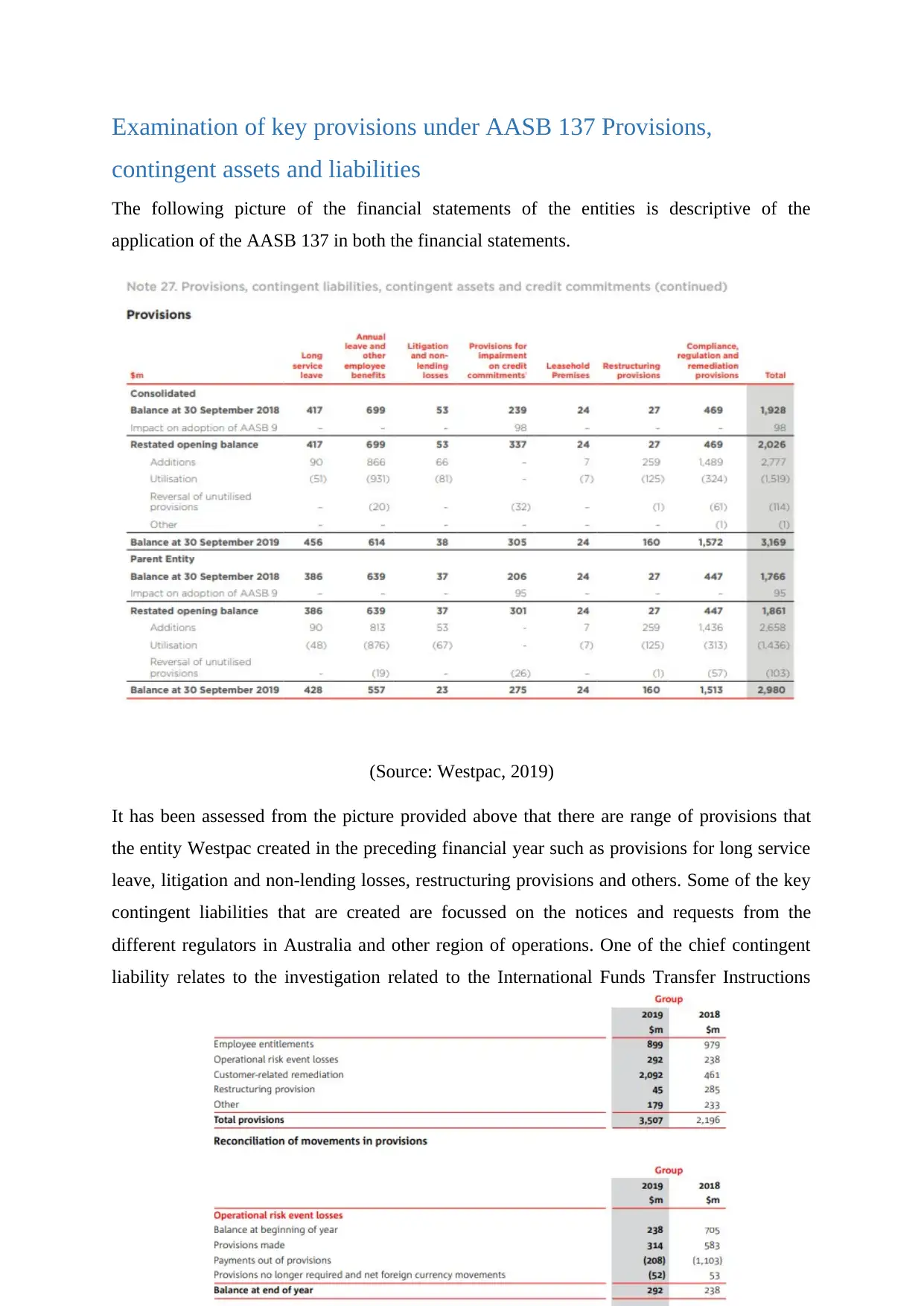

Examination of key provisions under AASB 137 Provisions,

contingent assets and liabilities

The following picture of the financial statements of the entities is descriptive of the

application of the AASB 137 in both the financial statements.

(Source: Westpac, 2019)

It has been assessed from the picture provided above that there are range of provisions that

the entity Westpac created in the preceding financial year such as provisions for long service

leave, litigation and non-lending losses, restructuring provisions and others. Some of the key

contingent liabilities that are created are focussed on the notices and requests from the

different regulators in Australia and other region of operations. One of the chief contingent

liability relates to the investigation related to the International Funds Transfer Instructions

contingent assets and liabilities

The following picture of the financial statements of the entities is descriptive of the

application of the AASB 137 in both the financial statements.

(Source: Westpac, 2019)

It has been assessed from the picture provided above that there are range of provisions that

the entity Westpac created in the preceding financial year such as provisions for long service

leave, litigation and non-lending losses, restructuring provisions and others. Some of the key

contingent liabilities that are created are focussed on the notices and requests from the

different regulators in Australia and other region of operations. One of the chief contingent

liability relates to the investigation related to the International Funds Transfer Instructions

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(IFTIs), as stated on the 255 of the annual report 2019. The reference has not been made to

AASB 137 in the financial statements.

The provisions of the NAB are depicted in the picture above.

Apart from this, the contingent liabilities of the entity includes, legal proceedings such as that

of the Bank Bill Swap Reference Rate US class action, UK conduct issues – potential action

and contingent asset, Adviser service fees and fee disclosure statements (FDS) under the

Royal commission inquiries, Anti-Money Laundering (AML) and Counter-Terrorist

Financing (CTF) program uplift and compliance issues as notified time to time by

AUSTRAC and other regulators, and likewise. The above information has been mentioned in

the note 29 of the financial statements. The reference has not been made to AASB 137 in the

financial statements.

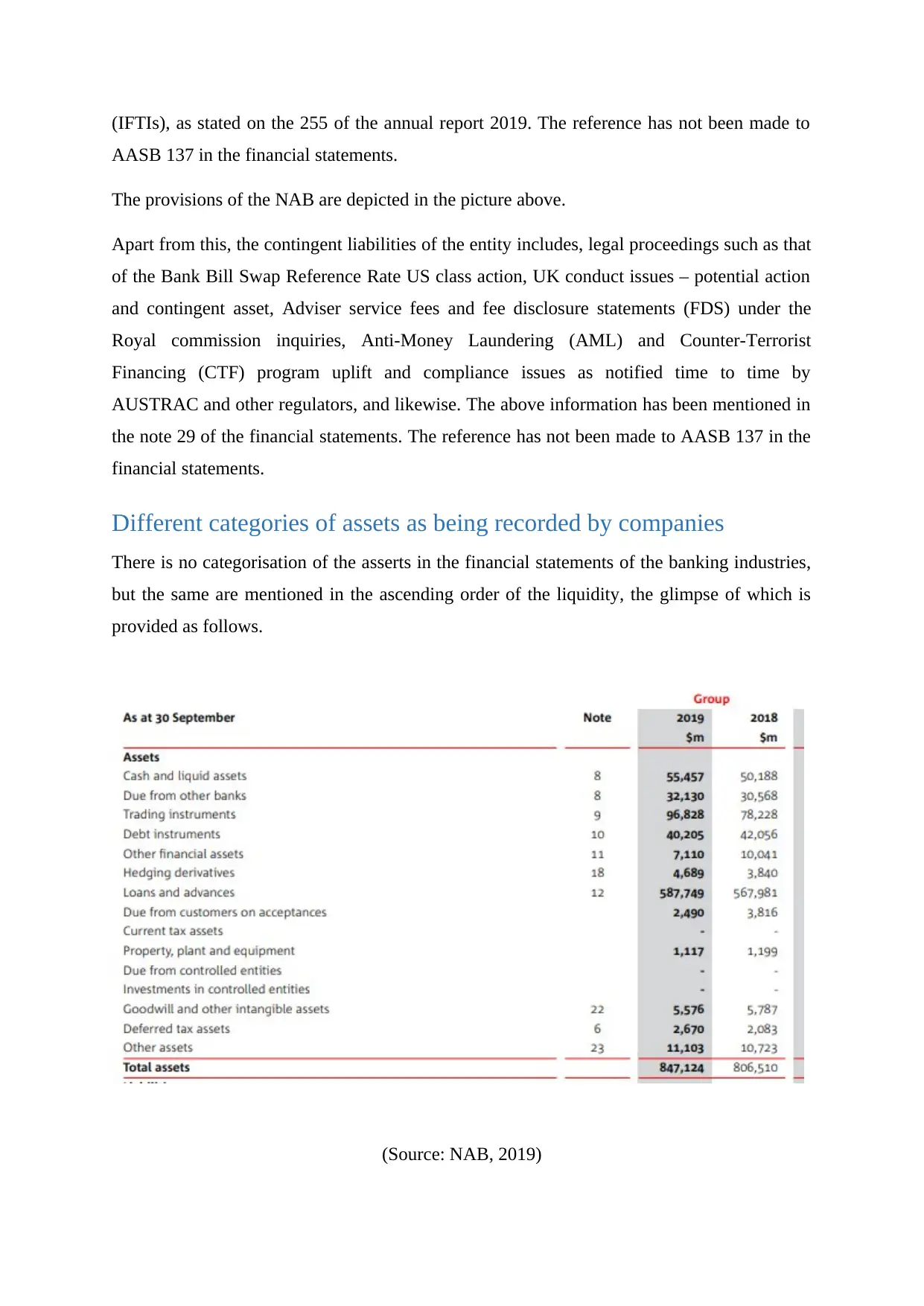

Different categories of assets as being recorded by companies

There is no categorisation of the asserts in the financial statements of the banking industries,

but the same are mentioned in the ascending order of the liquidity, the glimpse of which is

provided as follows.

(Source: NAB, 2019)

AASB 137 in the financial statements.

The provisions of the NAB are depicted in the picture above.

Apart from this, the contingent liabilities of the entity includes, legal proceedings such as that

of the Bank Bill Swap Reference Rate US class action, UK conduct issues – potential action

and contingent asset, Adviser service fees and fee disclosure statements (FDS) under the

Royal commission inquiries, Anti-Money Laundering (AML) and Counter-Terrorist

Financing (CTF) program uplift and compliance issues as notified time to time by

AUSTRAC and other regulators, and likewise. The above information has been mentioned in

the note 29 of the financial statements. The reference has not been made to AASB 137 in the

financial statements.

Different categories of assets as being recorded by companies

There is no categorisation of the asserts in the financial statements of the banking industries,

but the same are mentioned in the ascending order of the liquidity, the glimpse of which is

provided as follows.

(Source: NAB, 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Thus, while the cash and cash equivalents are the most liquid assets, the fixed assets like that

of goodwill, property plant and equipment are mentioned later in the list.

This is to state that while the total assets of the NAB for the year 2019 were $ 847124

million, the same for the Westpac were $ 906626 million as on the September 30th.

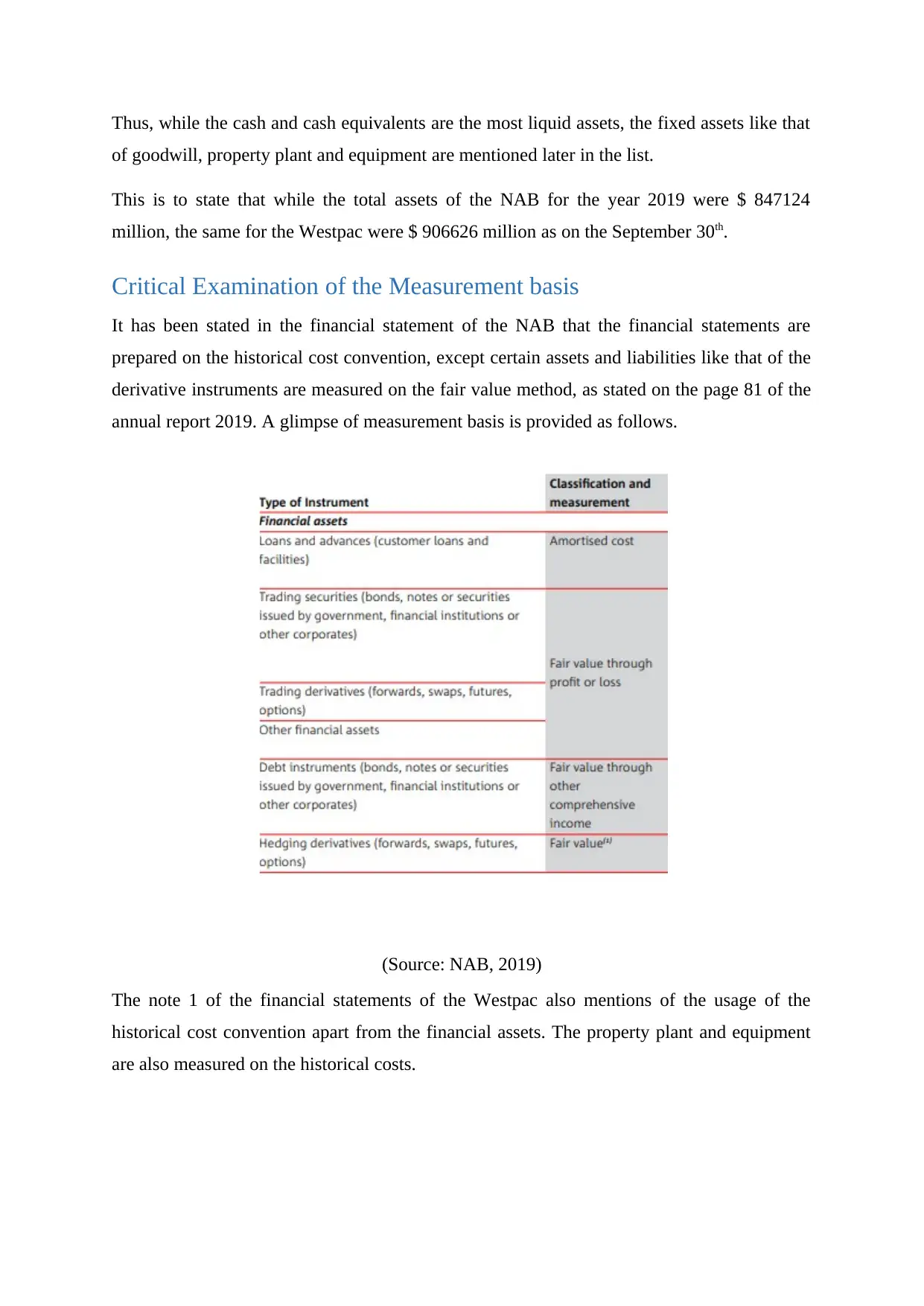

Critical Examination of the Measurement basis

It has been stated in the financial statement of the NAB that the financial statements are

prepared on the historical cost convention, except certain assets and liabilities like that of the

derivative instruments are measured on the fair value method, as stated on the page 81 of the

annual report 2019. A glimpse of measurement basis is provided as follows.

(Source: NAB, 2019)

The note 1 of the financial statements of the Westpac also mentions of the usage of the

historical cost convention apart from the financial assets. The property plant and equipment

are also measured on the historical costs.

of goodwill, property plant and equipment are mentioned later in the list.

This is to state that while the total assets of the NAB for the year 2019 were $ 847124

million, the same for the Westpac were $ 906626 million as on the September 30th.

Critical Examination of the Measurement basis

It has been stated in the financial statement of the NAB that the financial statements are

prepared on the historical cost convention, except certain assets and liabilities like that of the

derivative instruments are measured on the fair value method, as stated on the page 81 of the

annual report 2019. A glimpse of measurement basis is provided as follows.

(Source: NAB, 2019)

The note 1 of the financial statements of the Westpac also mentions of the usage of the

historical cost convention apart from the financial assets. The property plant and equipment

are also measured on the historical costs.

Conclusion

The discussions conducted in the previous parts aid to conclude that the financial statements

of the both the companies are comprised of various assets and liabilities. Each of the above

segments highlights a different aspect of the financial statement, such as sources of funds,

assets and the liabilities. As both the companies belong to the same industry, no major

changes are seen in the composition of the balance sheets.

The discussions conducted in the previous parts aid to conclude that the financial statements

of the both the companies are comprised of various assets and liabilities. Each of the above

segments highlights a different aspect of the financial statement, such as sources of funds,

assets and the liabilities. As both the companies belong to the same industry, no major

changes are seen in the composition of the balance sheets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.