Corporate Finance Analysis Report: Woodside Petroleum Ltd

VerifiedAdded on 2020/05/28

|11

|2049

|76

Report

AI Summary

This comprehensive corporate finance report examines the financial performance and strategic decisions of Woodside Petroleum Ltd and Royal Dutch Shell. It begins with an overview of the companies' backgrounds, industry analysis, identification of key opportunities and threats, and then proceeds to calculate and analyze the cash conversion cycle for Woodside Petroleum. The report also explores short-term and long-term debt financing instruments, assessing the company's debt usage. Further analysis includes the valuation of bonds, the portrayal of share prices, and the projection of Free Cash Flow (FCF) for a gas project. Finally, the report calculates and evaluates the Net Present Value (NPV) of the gas project under different Weighted Average Cost of Capital (WACC) scenarios, providing insights into project viability and financial implications. The report concludes with a detailed reference and bibliography of the sources used.

Running head: CORPORATE FINANCE

Corporate Finance

Name of the Student:

Name of the University:

Authors Note:

Corporate Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

1

Table of Contents

2a. Describing background and the industry in which company operates. Identifying one key

opportunity and two key threats of the company:......................................................................2

2b. Calculating cash conversion cycle and comparing it with previous year and industry peer:

....................................................................................................................................................3

2c. Stating example of short term debt financing instrument and long-term debt financing

instrument, while depicting whether the company has used debt financing in 2016:................4

2d.i) Conniving bond price for 6/12/2018:................................................................................4

2d.ii) Evaluating the bond price with calculated figure and mentioned figure, while detecting

the reason behind its selling at par:............................................................................................5

2e.) Portraying share price of Shell in euros:.............................................................................5

3a) Portraying FCF of Shell’s gas project:.................................................................................6

3b.a) Portraying Net present value of the project at WACC 5.94%:.........................................7

3b.b) Portraying Net present value of the project at WACC 8.00%:.........................................7

Reference and Bibliography:......................................................................................................9

1

Table of Contents

2a. Describing background and the industry in which company operates. Identifying one key

opportunity and two key threats of the company:......................................................................2

2b. Calculating cash conversion cycle and comparing it with previous year and industry peer:

....................................................................................................................................................3

2c. Stating example of short term debt financing instrument and long-term debt financing

instrument, while depicting whether the company has used debt financing in 2016:................4

2d.i) Conniving bond price for 6/12/2018:................................................................................4

2d.ii) Evaluating the bond price with calculated figure and mentioned figure, while detecting

the reason behind its selling at par:............................................................................................5

2e.) Portraying share price of Shell in euros:.............................................................................5

3a) Portraying FCF of Shell’s gas project:.................................................................................6

3b.a) Portraying Net present value of the project at WACC 5.94%:.........................................7

3b.b) Portraying Net present value of the project at WACC 8.00%:.........................................7

Reference and Bibliography:......................................................................................................9

CORPORATE FINANCE

2

2a. Describing background and the industry in which company operates. Identifying

one key opportunity and two key threats of the company:

Woodside Petroleum Ltd is linked with petroleum exploration and production, which

is used in Australia. The company comes under Oil and Gas industry, while they deal in

producing petroleum products. Petroleum and LNG are the key product that is produced by

Woodside Petroleum Ltd, which is allowed them to accumulate profits over the past fiscal

years (Woodside.com.au 2018). From the valuation of company's operations relevant

opportunity and threats could be identified, which might affect its revenue generation

capacity. The major opportunity for your organization is the rising demand for Petroleum

products around the world. Majority of the manufacturing, production houses, and vehicles

uses petroleum products, which is an adequate opportunity for the company to improve its

profitability in future. This rising trend of using petroleum product has allowed majority of

the oil producing companies to increase their revenue to support future oil exploration

projects.

However, certain threats are also identified from the evaluation, which could hamper

profitability of the organization in immediate future. Threats from substitute is a major

problem for oil producing companies, where thermal power and solar energy are replacing

maximum of the sales conducted by oil producing companies. The second threat for Oil and

Gas companies is the declining value of crude oil in the market, which is reducing actual

revenue collection of Oil and Gas organization. The constant decline in value of oil in the

world market is threatening oil and gas company’s existence, which is a major threat to

Woodside Petroleum Ltd revenue. Both the threats identified would directly affect revenue

generation capacity of Woodside petroleum Limited and increase their expenditure. On the

other hand, Atil, Lahiani and Nguyen (2014) argued that due to the reduced prices of crude

2

2a. Describing background and the industry in which company operates. Identifying

one key opportunity and two key threats of the company:

Woodside Petroleum Ltd is linked with petroleum exploration and production, which

is used in Australia. The company comes under Oil and Gas industry, while they deal in

producing petroleum products. Petroleum and LNG are the key product that is produced by

Woodside Petroleum Ltd, which is allowed them to accumulate profits over the past fiscal

years (Woodside.com.au 2018). From the valuation of company's operations relevant

opportunity and threats could be identified, which might affect its revenue generation

capacity. The major opportunity for your organization is the rising demand for Petroleum

products around the world. Majority of the manufacturing, production houses, and vehicles

uses petroleum products, which is an adequate opportunity for the company to improve its

profitability in future. This rising trend of using petroleum product has allowed majority of

the oil producing companies to increase their revenue to support future oil exploration

projects.

However, certain threats are also identified from the evaluation, which could hamper

profitability of the organization in immediate future. Threats from substitute is a major

problem for oil producing companies, where thermal power and solar energy are replacing

maximum of the sales conducted by oil producing companies. The second threat for Oil and

Gas companies is the declining value of crude oil in the market, which is reducing actual

revenue collection of Oil and Gas organization. The constant decline in value of oil in the

world market is threatening oil and gas company’s existence, which is a major threat to

Woodside Petroleum Ltd revenue. Both the threats identified would directly affect revenue

generation capacity of Woodside petroleum Limited and increase their expenditure. On the

other hand, Atil, Lahiani and Nguyen (2014) argued that due to the reduced prices of crude

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

3

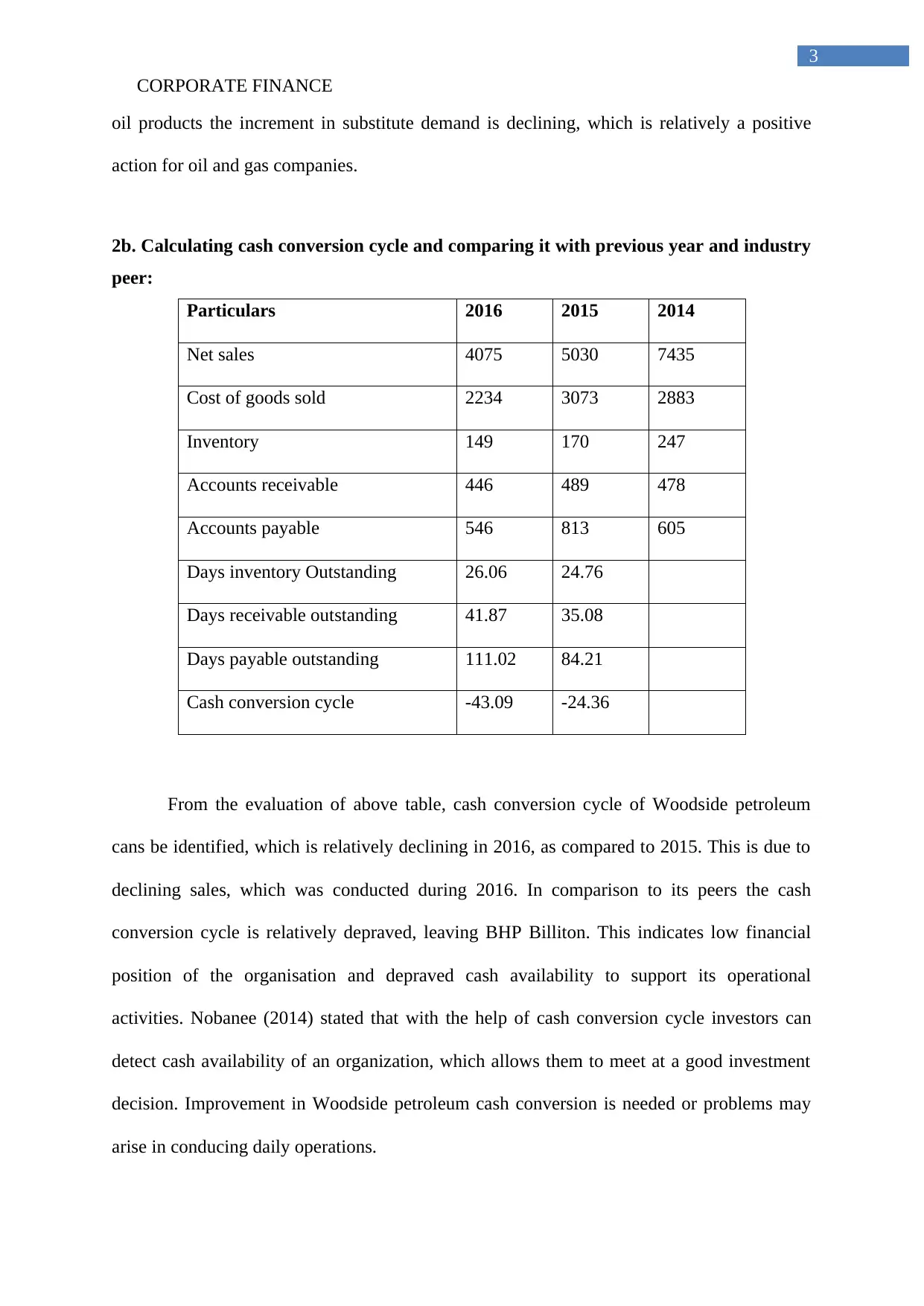

oil products the increment in substitute demand is declining, which is relatively a positive

action for oil and gas companies.

2b. Calculating cash conversion cycle and comparing it with previous year and industry

peer:

Particulars 2016 2015 2014

Net sales 4075 5030 7435

Cost of goods sold 2234 3073 2883

Inventory 149 170 247

Accounts receivable 446 489 478

Accounts payable 546 813 605

Days inventory Outstanding 26.06 24.76

Days receivable outstanding 41.87 35.08

Days payable outstanding 111.02 84.21

Cash conversion cycle -43.09 -24.36

From the evaluation of above table, cash conversion cycle of Woodside petroleum

cans be identified, which is relatively declining in 2016, as compared to 2015. This is due to

declining sales, which was conducted during 2016. In comparison to its peers the cash

conversion cycle is relatively depraved, leaving BHP Billiton. This indicates low financial

position of the organisation and depraved cash availability to support its operational

activities. Nobanee (2014) stated that with the help of cash conversion cycle investors can

detect cash availability of an organization, which allows them to meet at a good investment

decision. Improvement in Woodside petroleum cash conversion is needed or problems may

arise in conducing daily operations.

3

oil products the increment in substitute demand is declining, which is relatively a positive

action for oil and gas companies.

2b. Calculating cash conversion cycle and comparing it with previous year and industry

peer:

Particulars 2016 2015 2014

Net sales 4075 5030 7435

Cost of goods sold 2234 3073 2883

Inventory 149 170 247

Accounts receivable 446 489 478

Accounts payable 546 813 605

Days inventory Outstanding 26.06 24.76

Days receivable outstanding 41.87 35.08

Days payable outstanding 111.02 84.21

Cash conversion cycle -43.09 -24.36

From the evaluation of above table, cash conversion cycle of Woodside petroleum

cans be identified, which is relatively declining in 2016, as compared to 2015. This is due to

declining sales, which was conducted during 2016. In comparison to its peers the cash

conversion cycle is relatively depraved, leaving BHP Billiton. This indicates low financial

position of the organisation and depraved cash availability to support its operational

activities. Nobanee (2014) stated that with the help of cash conversion cycle investors can

detect cash availability of an organization, which allows them to meet at a good investment

decision. Improvement in Woodside petroleum cash conversion is needed or problems may

arise in conducing daily operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

4

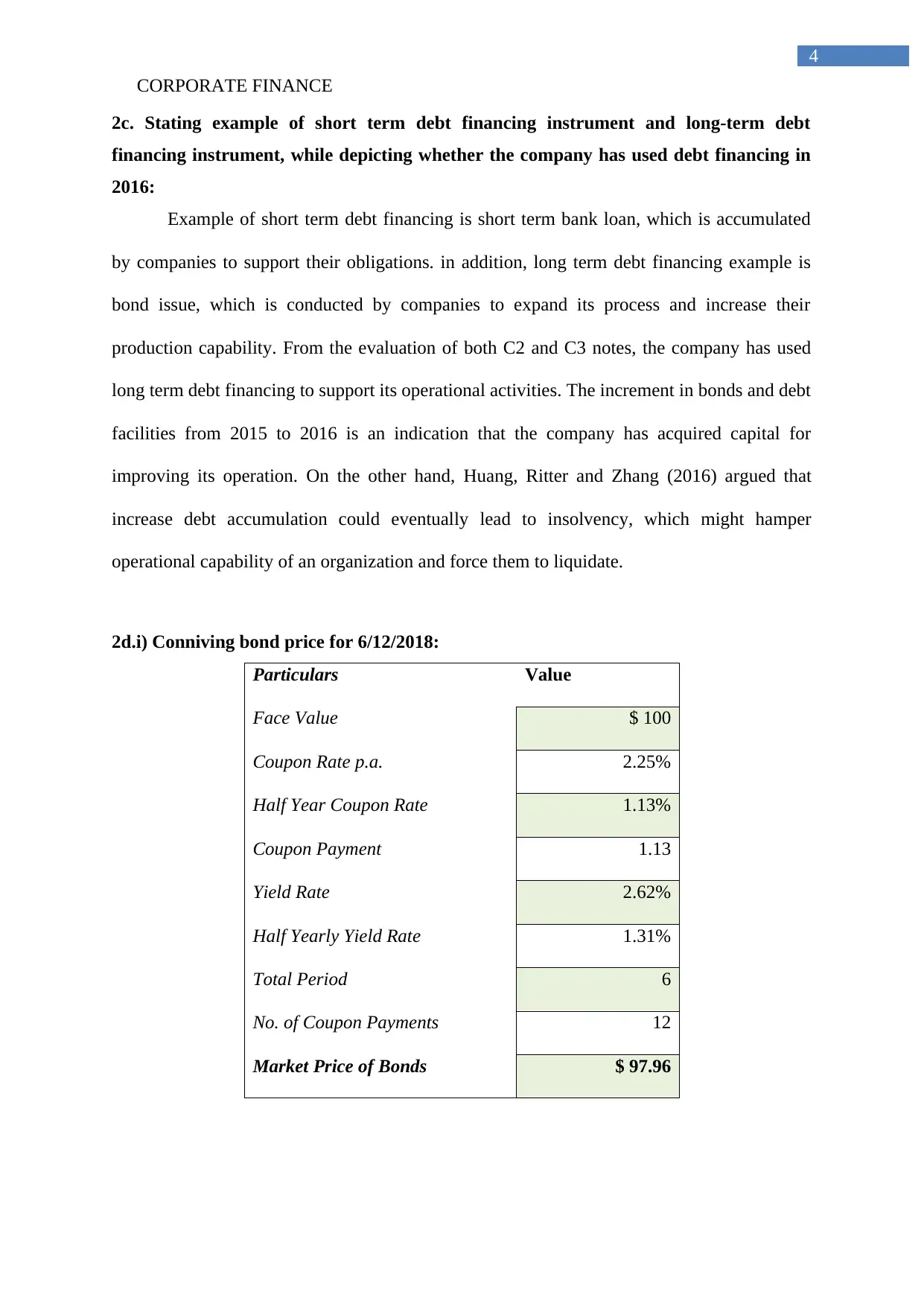

2c. Stating example of short term debt financing instrument and long-term debt

financing instrument, while depicting whether the company has used debt financing in

2016:

Example of short term debt financing is short term bank loan, which is accumulated

by companies to support their obligations. in addition, long term debt financing example is

bond issue, which is conducted by companies to expand its process and increase their

production capability. From the evaluation of both C2 and C3 notes, the company has used

long term debt financing to support its operational activities. The increment in bonds and debt

facilities from 2015 to 2016 is an indication that the company has acquired capital for

improving its operation. On the other hand, Huang, Ritter and Zhang (2016) argued that

increase debt accumulation could eventually lead to insolvency, which might hamper

operational capability of an organization and force them to liquidate.

2d.i) Conniving bond price for 6/12/2018:

Particulars Value

Face Value $ 100

Coupon Rate p.a. 2.25%

Half Year Coupon Rate 1.13%

Coupon Payment 1.13

Yield Rate 2.62%

Half Yearly Yield Rate 1.31%

Total Period 6

No. of Coupon Payments 12

Market Price of Bonds $ 97.96

4

2c. Stating example of short term debt financing instrument and long-term debt

financing instrument, while depicting whether the company has used debt financing in

2016:

Example of short term debt financing is short term bank loan, which is accumulated

by companies to support their obligations. in addition, long term debt financing example is

bond issue, which is conducted by companies to expand its process and increase their

production capability. From the evaluation of both C2 and C3 notes, the company has used

long term debt financing to support its operational activities. The increment in bonds and debt

facilities from 2015 to 2016 is an indication that the company has acquired capital for

improving its operation. On the other hand, Huang, Ritter and Zhang (2016) argued that

increase debt accumulation could eventually lead to insolvency, which might hamper

operational capability of an organization and force them to liquidate.

2d.i) Conniving bond price for 6/12/2018:

Particulars Value

Face Value $ 100

Coupon Rate p.a. 2.25%

Half Year Coupon Rate 1.13%

Coupon Payment 1.13

Yield Rate 2.62%

Half Yearly Yield Rate 1.31%

Total Period 6

No. of Coupon Payments 12

Market Price of Bonds $ 97.96

CORPORATE FINANCE

5

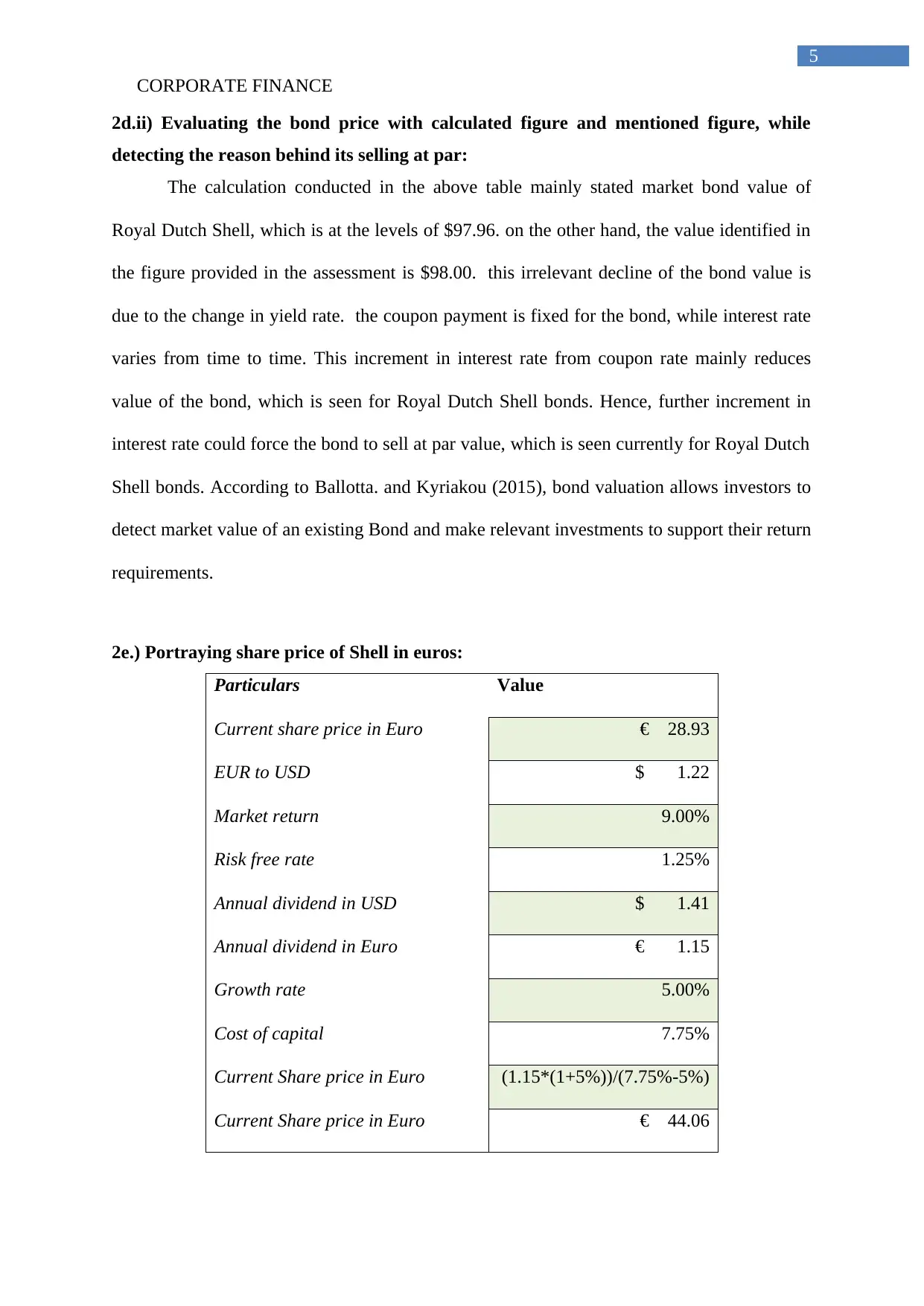

2d.ii) Evaluating the bond price with calculated figure and mentioned figure, while

detecting the reason behind its selling at par:

The calculation conducted in the above table mainly stated market bond value of

Royal Dutch Shell, which is at the levels of $97.96. on the other hand, the value identified in

the figure provided in the assessment is $98.00. this irrelevant decline of the bond value is

due to the change in yield rate. the coupon payment is fixed for the bond, while interest rate

varies from time to time. This increment in interest rate from coupon rate mainly reduces

value of the bond, which is seen for Royal Dutch Shell bonds. Hence, further increment in

interest rate could force the bond to sell at par value, which is seen currently for Royal Dutch

Shell bonds. According to Ballotta. and Kyriakou (2015), bond valuation allows investors to

detect market value of an existing Bond and make relevant investments to support their return

requirements.

2e.) Portraying share price of Shell in euros:

Particulars Value

Current share price in Euro € 28.93

EUR to USD $ 1.22

Market return 9.00%

Risk free rate 1.25%

Annual dividend in USD $ 1.41

Annual dividend in Euro € 1.15

Growth rate 5.00%

Cost of capital 7.75%

Current Share price in Euro (1.15*(1+5%))/(7.75%-5%)

Current Share price in Euro € 44.06

5

2d.ii) Evaluating the bond price with calculated figure and mentioned figure, while

detecting the reason behind its selling at par:

The calculation conducted in the above table mainly stated market bond value of

Royal Dutch Shell, which is at the levels of $97.96. on the other hand, the value identified in

the figure provided in the assessment is $98.00. this irrelevant decline of the bond value is

due to the change in yield rate. the coupon payment is fixed for the bond, while interest rate

varies from time to time. This increment in interest rate from coupon rate mainly reduces

value of the bond, which is seen for Royal Dutch Shell bonds. Hence, further increment in

interest rate could force the bond to sell at par value, which is seen currently for Royal Dutch

Shell bonds. According to Ballotta. and Kyriakou (2015), bond valuation allows investors to

detect market value of an existing Bond and make relevant investments to support their return

requirements.

2e.) Portraying share price of Shell in euros:

Particulars Value

Current share price in Euro € 28.93

EUR to USD $ 1.22

Market return 9.00%

Risk free rate 1.25%

Annual dividend in USD $ 1.41

Annual dividend in Euro € 1.15

Growth rate 5.00%

Cost of capital 7.75%

Current Share price in Euro (1.15*(1+5%))/(7.75%-5%)

Current Share price in Euro € 44.06

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

6

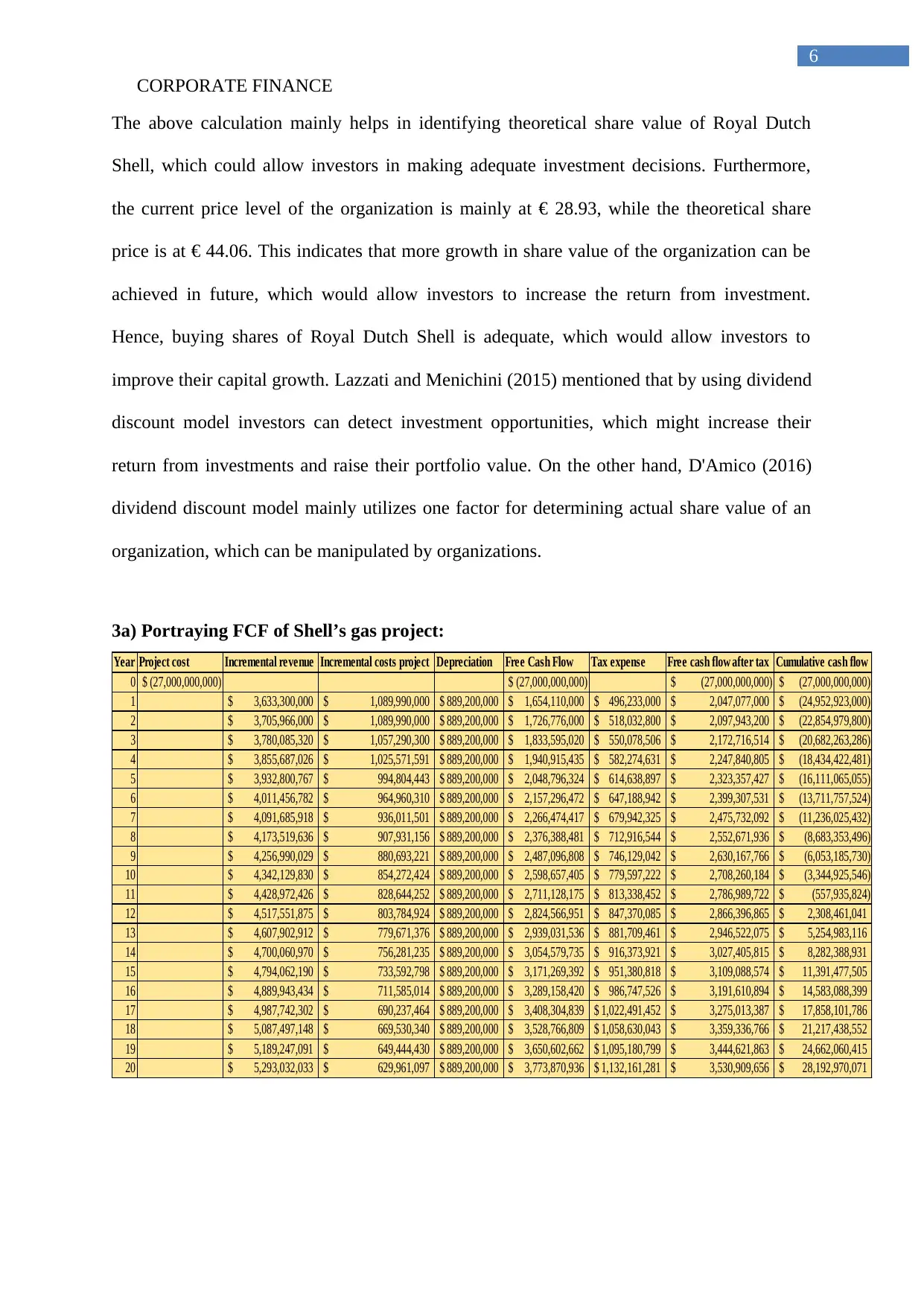

The above calculation mainly helps in identifying theoretical share value of Royal Dutch

Shell, which could allow investors in making adequate investment decisions. Furthermore,

the current price level of the organization is mainly at € 28.93, while the theoretical share

price is at € 44.06. This indicates that more growth in share value of the organization can be

achieved in future, which would allow investors to increase the return from investment.

Hence, buying shares of Royal Dutch Shell is adequate, which would allow investors to

improve their capital growth. Lazzati and Menichini (2015) mentioned that by using dividend

discount model investors can detect investment opportunities, which might increase their

return from investments and raise their portfolio value. On the other hand, D'Amico (2016)

dividend discount model mainly utilizes one factor for determining actual share value of an

organization, which can be manipulated by organizations.

3a) Portraying FCF of Shell’s gas project:

Year Project cost Incremental revenue Incremental costs project Depreciation Free Cash Flow Tax expense Free cash flow after tax Cumulative cash flow

0 (27,000,000,000)$ (27,000,000,000)$ (27,000,000,000)$ (27,000,000,000)$

1 3,633,300,000$ 1,089,990,000$ 889,200,000$ 1,654,110,000$ 496,233,000$ 2,047,077,000$ (24,952,923,000)$

2 3,705,966,000$ 1,089,990,000$ 889,200,000$ 1,726,776,000$ 518,032,800$ 2,097,943,200$ (22,854,979,800)$

3 3,780,085,320$ 1,057,290,300$ 889,200,000$ 1,833,595,020$ 550,078,506$ 2,172,716,514$ (20,682,263,286)$

4 3,855,687,026$ 1,025,571,591$ 889,200,000$ 1,940,915,435$ 582,274,631$ 2,247,840,805$ (18,434,422,481)$

5 3,932,800,767$ 994,804,443$ 889,200,000$ 2,048,796,324$ 614,638,897$ 2,323,357,427$ (16,111,065,055)$

6 4,011,456,782$ 964,960,310$ 889,200,000$ 2,157,296,472$ 647,188,942$ 2,399,307,531$ (13,711,757,524)$

7 4,091,685,918$ 936,011,501$ 889,200,000$ 2,266,474,417$ 679,942,325$ 2,475,732,092$ (11,236,025,432)$

8 4,173,519,636$ 907,931,156$ 889,200,000$ 2,376,388,481$ 712,916,544$ 2,552,671,936$ (8,683,353,496)$

9 4,256,990,029$ 880,693,221$ 889,200,000$ 2,487,096,808$ 746,129,042$ 2,630,167,766$ (6,053,185,730)$

10 4,342,129,830$ 854,272,424$ 889,200,000$ 2,598,657,405$ 779,597,222$ 2,708,260,184$ (3,344,925,546)$

11 4,428,972,426$ 828,644,252$ 889,200,000$ 2,711,128,175$ 813,338,452$ 2,786,989,722$ (557,935,824)$

12 4,517,551,875$ 803,784,924$ 889,200,000$ 2,824,566,951$ 847,370,085$ 2,866,396,865$ 2,308,461,041$

13 4,607,902,912$ 779,671,376$ 889,200,000$ 2,939,031,536$ 881,709,461$ 2,946,522,075$ 5,254,983,116$

14 4,700,060,970$ 756,281,235$ 889,200,000$ 3,054,579,735$ 916,373,921$ 3,027,405,815$ 8,282,388,931$

15 4,794,062,190$ 733,592,798$ 889,200,000$ 3,171,269,392$ 951,380,818$ 3,109,088,574$ 11,391,477,505$

16 4,889,943,434$ 711,585,014$ 889,200,000$ 3,289,158,420$ 986,747,526$ 3,191,610,894$ 14,583,088,399$

17 4,987,742,302$ 690,237,464$ 889,200,000$ 3,408,304,839$ 1,022,491,452$ 3,275,013,387$ 17,858,101,786$

18 5,087,497,148$ 669,530,340$ 889,200,000$ 3,528,766,809$ 1,058,630,043$ 3,359,336,766$ 21,217,438,552$

19 5,189,247,091$ 649,444,430$ 889,200,000$ 3,650,602,662$ 1,095,180,799$ 3,444,621,863$ 24,662,060,415$

20 5,293,032,033$ 629,961,097$ 889,200,000$ 3,773,870,936$ 1,132,161,281$ 3,530,909,656$ 28,192,970,071$

6

The above calculation mainly helps in identifying theoretical share value of Royal Dutch

Shell, which could allow investors in making adequate investment decisions. Furthermore,

the current price level of the organization is mainly at € 28.93, while the theoretical share

price is at € 44.06. This indicates that more growth in share value of the organization can be

achieved in future, which would allow investors to increase the return from investment.

Hence, buying shares of Royal Dutch Shell is adequate, which would allow investors to

improve their capital growth. Lazzati and Menichini (2015) mentioned that by using dividend

discount model investors can detect investment opportunities, which might increase their

return from investments and raise their portfolio value. On the other hand, D'Amico (2016)

dividend discount model mainly utilizes one factor for determining actual share value of an

organization, which can be manipulated by organizations.

3a) Portraying FCF of Shell’s gas project:

Year Project cost Incremental revenue Incremental costs project Depreciation Free Cash Flow Tax expense Free cash flow after tax Cumulative cash flow

0 (27,000,000,000)$ (27,000,000,000)$ (27,000,000,000)$ (27,000,000,000)$

1 3,633,300,000$ 1,089,990,000$ 889,200,000$ 1,654,110,000$ 496,233,000$ 2,047,077,000$ (24,952,923,000)$

2 3,705,966,000$ 1,089,990,000$ 889,200,000$ 1,726,776,000$ 518,032,800$ 2,097,943,200$ (22,854,979,800)$

3 3,780,085,320$ 1,057,290,300$ 889,200,000$ 1,833,595,020$ 550,078,506$ 2,172,716,514$ (20,682,263,286)$

4 3,855,687,026$ 1,025,571,591$ 889,200,000$ 1,940,915,435$ 582,274,631$ 2,247,840,805$ (18,434,422,481)$

5 3,932,800,767$ 994,804,443$ 889,200,000$ 2,048,796,324$ 614,638,897$ 2,323,357,427$ (16,111,065,055)$

6 4,011,456,782$ 964,960,310$ 889,200,000$ 2,157,296,472$ 647,188,942$ 2,399,307,531$ (13,711,757,524)$

7 4,091,685,918$ 936,011,501$ 889,200,000$ 2,266,474,417$ 679,942,325$ 2,475,732,092$ (11,236,025,432)$

8 4,173,519,636$ 907,931,156$ 889,200,000$ 2,376,388,481$ 712,916,544$ 2,552,671,936$ (8,683,353,496)$

9 4,256,990,029$ 880,693,221$ 889,200,000$ 2,487,096,808$ 746,129,042$ 2,630,167,766$ (6,053,185,730)$

10 4,342,129,830$ 854,272,424$ 889,200,000$ 2,598,657,405$ 779,597,222$ 2,708,260,184$ (3,344,925,546)$

11 4,428,972,426$ 828,644,252$ 889,200,000$ 2,711,128,175$ 813,338,452$ 2,786,989,722$ (557,935,824)$

12 4,517,551,875$ 803,784,924$ 889,200,000$ 2,824,566,951$ 847,370,085$ 2,866,396,865$ 2,308,461,041$

13 4,607,902,912$ 779,671,376$ 889,200,000$ 2,939,031,536$ 881,709,461$ 2,946,522,075$ 5,254,983,116$

14 4,700,060,970$ 756,281,235$ 889,200,000$ 3,054,579,735$ 916,373,921$ 3,027,405,815$ 8,282,388,931$

15 4,794,062,190$ 733,592,798$ 889,200,000$ 3,171,269,392$ 951,380,818$ 3,109,088,574$ 11,391,477,505$

16 4,889,943,434$ 711,585,014$ 889,200,000$ 3,289,158,420$ 986,747,526$ 3,191,610,894$ 14,583,088,399$

17 4,987,742,302$ 690,237,464$ 889,200,000$ 3,408,304,839$ 1,022,491,452$ 3,275,013,387$ 17,858,101,786$

18 5,087,497,148$ 669,530,340$ 889,200,000$ 3,528,766,809$ 1,058,630,043$ 3,359,336,766$ 21,217,438,552$

19 5,189,247,091$ 649,444,430$ 889,200,000$ 3,650,602,662$ 1,095,180,799$ 3,444,621,863$ 24,662,060,415$

20 5,293,032,033$ 629,961,097$ 889,200,000$ 3,773,870,936$ 1,132,161,281$ 3,530,909,656$ 28,192,970,071$

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

7

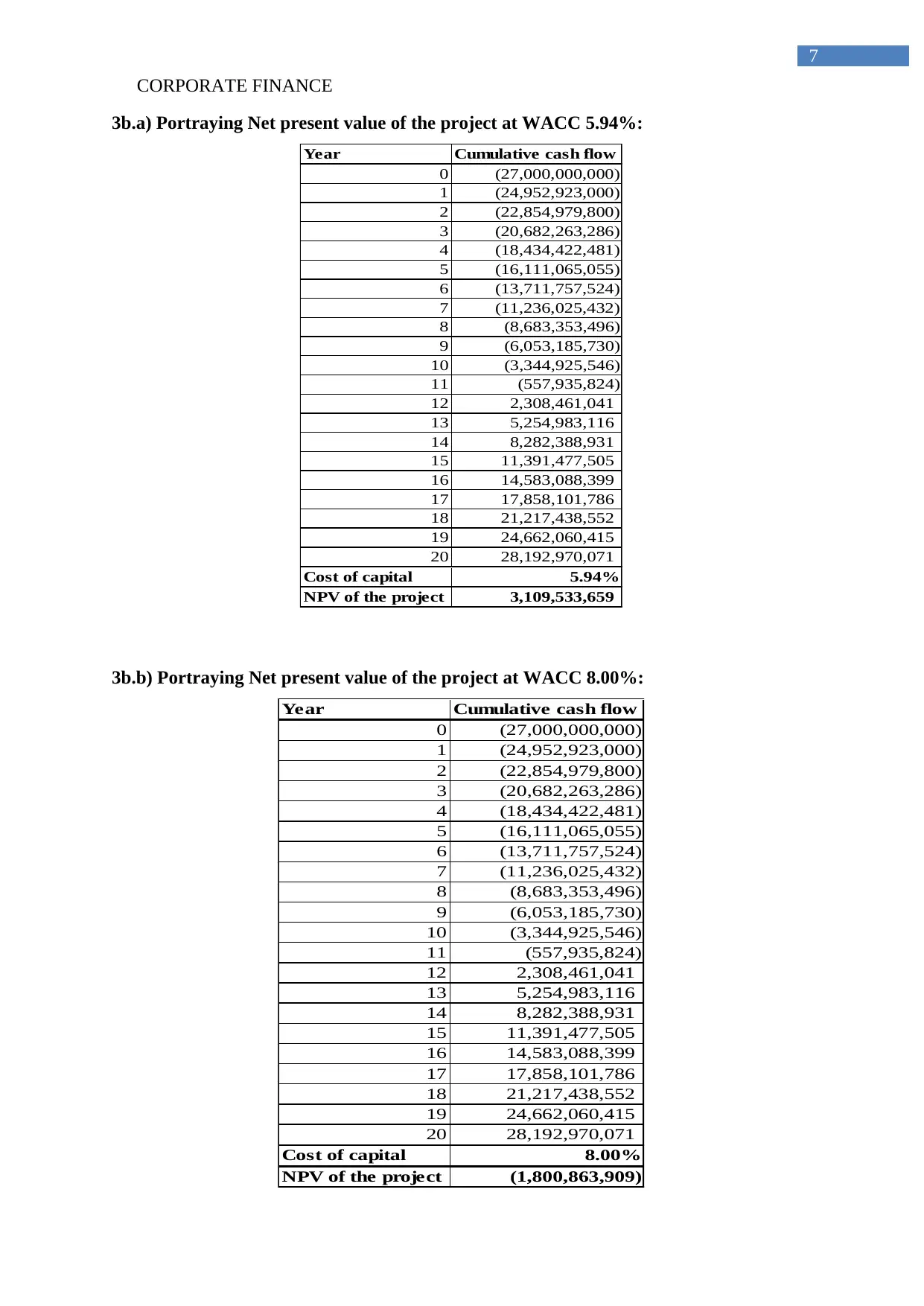

3b.a) Portraying Net present value of the project at WACC 5.94%:

Year Cumulative cash flow

0 (27,000,000,000)

1 (24,952,923,000)

2 (22,854,979,800)

3 (20,682,263,286)

4 (18,434,422,481)

5 (16,111,065,055)

6 (13,711,757,524)

7 (11,236,025,432)

8 (8,683,353,496)

9 (6,053,185,730)

10 (3,344,925,546)

11 (557,935,824)

12 2,308,461,041

13 5,254,983,116

14 8,282,388,931

15 11,391,477,505

16 14,583,088,399

17 17,858,101,786

18 21,217,438,552

19 24,662,060,415

20 28,192,970,071

Cost of capital 5.94%

NPV of the project 3,109,533,659

3b.b) Portraying Net present value of the project at WACC 8.00%:

Year Cumulative cash flow

0 (27,000,000,000)

1 (24,952,923,000)

2 (22,854,979,800)

3 (20,682,263,286)

4 (18,434,422,481)

5 (16,111,065,055)

6 (13,711,757,524)

7 (11,236,025,432)

8 (8,683,353,496)

9 (6,053,185,730)

10 (3,344,925,546)

11 (557,935,824)

12 2,308,461,041

13 5,254,983,116

14 8,282,388,931

15 11,391,477,505

16 14,583,088,399

17 17,858,101,786

18 21,217,438,552

19 24,662,060,415

20 28,192,970,071

Cost of capital 8.00%

NPV of the project (1,800,863,909)

7

3b.a) Portraying Net present value of the project at WACC 5.94%:

Year Cumulative cash flow

0 (27,000,000,000)

1 (24,952,923,000)

2 (22,854,979,800)

3 (20,682,263,286)

4 (18,434,422,481)

5 (16,111,065,055)

6 (13,711,757,524)

7 (11,236,025,432)

8 (8,683,353,496)

9 (6,053,185,730)

10 (3,344,925,546)

11 (557,935,824)

12 2,308,461,041

13 5,254,983,116

14 8,282,388,931

15 11,391,477,505

16 14,583,088,399

17 17,858,101,786

18 21,217,438,552

19 24,662,060,415

20 28,192,970,071

Cost of capital 5.94%

NPV of the project 3,109,533,659

3b.b) Portraying Net present value of the project at WACC 8.00%:

Year Cumulative cash flow

0 (27,000,000,000)

1 (24,952,923,000)

2 (22,854,979,800)

3 (20,682,263,286)

4 (18,434,422,481)

5 (16,111,065,055)

6 (13,711,757,524)

7 (11,236,025,432)

8 (8,683,353,496)

9 (6,053,185,730)

10 (3,344,925,546)

11 (557,935,824)

12 2,308,461,041

13 5,254,983,116

14 8,282,388,931

15 11,391,477,505

16 14,583,088,399

17 17,858,101,786

18 21,217,438,552

19 24,662,060,415

20 28,192,970,071

Cost of capital 8.00%

NPV of the project (1,800,863,909)

CORPORATE FINANCE

8

From the valuation of 5.94% and 8% WACC, Adequate cost of capital for the

organization is identified. The NPV provided from 5.94% WACC was relatively at the levels

of 3,109,533,659, which is high and provides the company with adequate returns. However,

the WACC of 8% mainly indicates a negative value of -1,800,863,909, while stating the loss

portrayed from the project. Hence, with 5.94% WACC the gas project is viable, while with

8% WACC the project is not viable for Royal Dutch Shell. With the use of net present value

organizations can detect actual viability of the project and understand the returns that could

be provided from their investment (Lokman et al. 2017). However, certain projects due to no

cash inflow are not able to support time value of money, which could directly affect

company's ability to increase firm value. Currently, the WACC of 5.94% is providing a

positive net present value for Royal Dutch Shell, which is a positive indication for the

company. On the other hand, the WACC of 8% is portraying a negative valuation for the

project, which indicates that cash flow of the project is not supporting time value of money.

8

From the valuation of 5.94% and 8% WACC, Adequate cost of capital for the

organization is identified. The NPV provided from 5.94% WACC was relatively at the levels

of 3,109,533,659, which is high and provides the company with adequate returns. However,

the WACC of 8% mainly indicates a negative value of -1,800,863,909, while stating the loss

portrayed from the project. Hence, with 5.94% WACC the gas project is viable, while with

8% WACC the project is not viable for Royal Dutch Shell. With the use of net present value

organizations can detect actual viability of the project and understand the returns that could

be provided from their investment (Lokman et al. 2017). However, certain projects due to no

cash inflow are not able to support time value of money, which could directly affect

company's ability to increase firm value. Currently, the WACC of 5.94% is providing a

positive net present value for Royal Dutch Shell, which is a positive indication for the

company. On the other hand, the WACC of 8% is portraying a negative valuation for the

project, which indicates that cash flow of the project is not supporting time value of money.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

9

Reference and Bibliography:

Atil, A., Lahiani, A. and Nguyen, D.K., 2014. Asymmetric and nonlinear pass-through of

crude oil prices to gasoline and natural gas prices. Energy Policy, 65, pp.567-573.

Ballotta, L. and Kyriakou, I., 2015. Convertible bond valuation in a jump diffusion setting

with stochastic interest rates. Quantitative Finance, 15(1), pp.115-129.

D'Amico, G., 2016. Generalized semi-Markovian dividend discount model: risk and

return. arXiv preprint arXiv:1605.02472.

Eliasson, J. and Börjesson, M., 2014. On timetable assumptions in railway investment

appraisal. Transport Policy, 36, pp.118-126.

Florou, A. and Kosi, U., 2015. Does mandatory IFRS adoption facilitate debt

financing?. Review of Accounting Studies, 20(4), pp.1407-1456.

Huang, R., Ritter, J.R. and Zhang, D., 2016. Private equity firms’ reputational concerns and

the costs of debt financing. Journal of Financial and Quantitative Analysis, 51(1), pp.29-54.

Lazzati, N. and Menichini, A.A., 2015. A dynamic approach to the dividend discount

model. Review of Pacific Basin Financial Markets and Policies, 18(03), p.1550018.

Lokman, S., Volker, D., Zijlstra-Vlasveld, M.C., Brouwers, E.P., Boon, B., Beekman, A.T.,

Smit, F. and Van der Feltz-Cornelis, C.M., 2017. Return-to-work intervention versus usual

care for sick-listed employees: health-economic investment appraisal alongside a cluster

randomised trial. BMJ open, 7(10), p.e016348.

Nobanee, H., 2014. Working capital management and firm's profitability: an optimal cash

conversion cycle. International Research Journal of Finance and Economics. March (120),

pp.13-22.

9

Reference and Bibliography:

Atil, A., Lahiani, A. and Nguyen, D.K., 2014. Asymmetric and nonlinear pass-through of

crude oil prices to gasoline and natural gas prices. Energy Policy, 65, pp.567-573.

Ballotta, L. and Kyriakou, I., 2015. Convertible bond valuation in a jump diffusion setting

with stochastic interest rates. Quantitative Finance, 15(1), pp.115-129.

D'Amico, G., 2016. Generalized semi-Markovian dividend discount model: risk and

return. arXiv preprint arXiv:1605.02472.

Eliasson, J. and Börjesson, M., 2014. On timetable assumptions in railway investment

appraisal. Transport Policy, 36, pp.118-126.

Florou, A. and Kosi, U., 2015. Does mandatory IFRS adoption facilitate debt

financing?. Review of Accounting Studies, 20(4), pp.1407-1456.

Huang, R., Ritter, J.R. and Zhang, D., 2016. Private equity firms’ reputational concerns and

the costs of debt financing. Journal of Financial and Quantitative Analysis, 51(1), pp.29-54.

Lazzati, N. and Menichini, A.A., 2015. A dynamic approach to the dividend discount

model. Review of Pacific Basin Financial Markets and Policies, 18(03), p.1550018.

Lokman, S., Volker, D., Zijlstra-Vlasveld, M.C., Brouwers, E.P., Boon, B., Beekman, A.T.,

Smit, F. and Van der Feltz-Cornelis, C.M., 2017. Return-to-work intervention versus usual

care for sick-listed employees: health-economic investment appraisal alongside a cluster

randomised trial. BMJ open, 7(10), p.e016348.

Nobanee, H., 2014. Working capital management and firm's profitability: an optimal cash

conversion cycle. International Research Journal of Finance and Economics. March (120),

pp.13-22.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

10

Woodside.com.au. (2018). Woodside Energy | Home. [online] Available at:

http://www.woodside.com.au/Pages/home.aspx [Accessed 20 Jan. 2018].

Yazdanfar, D. and Öhman, P., 2014. The impact of cash conversion cycle on firm

profitability: an empirical study based on Swedish data. International Journal of Managerial

Finance, 10(4), pp.442-452.

10

Woodside.com.au. (2018). Woodside Energy | Home. [online] Available at:

http://www.woodside.com.au/Pages/home.aspx [Accessed 20 Jan. 2018].

Yazdanfar, D. and Öhman, P., 2014. The impact of cash conversion cycle on firm

profitability: an empirical study based on Swedish data. International Journal of Managerial

Finance, 10(4), pp.442-452.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.