Corporate Finance Analysis Report

VerifiedAdded on 2020/02/05

|12

|2981

|114

Report

AI Summary

The report evaluates the investment project of Genetic Plc in genetically developed mustard seeds using capital budgeting techniques such as NPV, IRR, and payback period analysis. It provides recommendations to the Board of Directors based on the financial viability of the project, highlighting the importance of NPV over IRR in investment decisions. The report includes detailed calculations and a comprehensive analysis of cash inflows, costs, and the overall financial implications of the proposed investment.

CORPORATE

FINANCE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK-A...........................................................................................................................................3

Recommendations to Board Of Directors....................................................................................3

TASK-B...........................................................................................................................................6

CONCLUSION................................................................................................................................8

APPENDIX......................................................................................................................................9

REFERENCES..............................................................................................................................11

2

INTRODUCTION...........................................................................................................................3

TASK-A...........................................................................................................................................3

Recommendations to Board Of Directors....................................................................................3

TASK-B...........................................................................................................................................6

CONCLUSION................................................................................................................................8

APPENDIX......................................................................................................................................9

REFERENCES..............................................................................................................................11

2

INTRODUCTION

Capital budgeting is the branch in finance which deals in the evaluation of investments among

those available with the organisation. By applying the various evaluation tools, the organisation

can select the most beneficial and profitable investment. The present report will highlight the

different available techniques using discounted and non-discounted methods. The most

commonly used three methods have been discussed which are used for project evaluation

(Understanding the Difference Between NPV vs. IRR, 2017). The report is presented to the Board

Of Directors of Genetic Plc including an in-depth assessment of the investment and cost benefit

analysis on the proposal. In this reference, the financing and investment decisions are taken for

the company. Presently Genetik is considering an investment in the proposal of marketing and

production of new genetically developed mustard seeds. The duration of the project is five years.

TASK-A

Recommendations to Board Of Directors

In the present report, the discounted, as well as non-discounted methods, are used. A brief

understanding of the different methods used in the project evaluation is being provided as

follows-

Payback Period Evaluation- This is the period in which the initial investment is recovered of the

project. Hence it is used to evaluated the whether the period in which the investment is recovered

is feasible for making the investment or not. The project with less payback period is more viable

as it covers the initial investment in the lesser period than that of the duration of the project. In

the present case payback of the project is 4.13 years which means that the initial investment of £

2150000 will be recovered in this period (Understanding the Difference Between NPV vs. IRR,

2017). It is less than the total duration of the period and so is beneficial for the company to make

the investment in this project. Moreover, the payback period is higher because of the fact that

the initial cash inflows are negative which means instead of inflows there are going to be net

outflows. However, the situation got improved in the fourth year in which the cumulative cash

inflows were positive. The inflows are more skewed towards the end of the project. Hence it

would be not be generating immediate cash inflows in the initial years.

3

Capital budgeting is the branch in finance which deals in the evaluation of investments among

those available with the organisation. By applying the various evaluation tools, the organisation

can select the most beneficial and profitable investment. The present report will highlight the

different available techniques using discounted and non-discounted methods. The most

commonly used three methods have been discussed which are used for project evaluation

(Understanding the Difference Between NPV vs. IRR, 2017). The report is presented to the Board

Of Directors of Genetic Plc including an in-depth assessment of the investment and cost benefit

analysis on the proposal. In this reference, the financing and investment decisions are taken for

the company. Presently Genetik is considering an investment in the proposal of marketing and

production of new genetically developed mustard seeds. The duration of the project is five years.

TASK-A

Recommendations to Board Of Directors

In the present report, the discounted, as well as non-discounted methods, are used. A brief

understanding of the different methods used in the project evaluation is being provided as

follows-

Payback Period Evaluation- This is the period in which the initial investment is recovered of the

project. Hence it is used to evaluated the whether the period in which the investment is recovered

is feasible for making the investment or not. The project with less payback period is more viable

as it covers the initial investment in the lesser period than that of the duration of the project. In

the present case payback of the project is 4.13 years which means that the initial investment of £

2150000 will be recovered in this period (Understanding the Difference Between NPV vs. IRR,

2017). It is less than the total duration of the period and so is beneficial for the company to make

the investment in this project. Moreover, the payback period is higher because of the fact that

the initial cash inflows are negative which means instead of inflows there are going to be net

outflows. However, the situation got improved in the fourth year in which the cumulative cash

inflows were positive. The inflows are more skewed towards the end of the project. Hence it

would be not be generating immediate cash inflows in the initial years.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net Present Value Evaluation- This is the most suitable method for project evaluation. This is

due to the fact that it uses the discounted cash inflows. The consideration of time value of money

gives more accurate and clear picture about the feasibility of the project. The major assumptions

used for the purpose of project evaluation are-

Marketing Cost is assumed to be sunk costs and thus not included in the calculation.

Cash Flows for the are considered over a five-year period which constitutes the lifecycle

of the project.

An annual license fee of £1 M per annum has been included for making the necessary

conclusions.

Purchase of vehicles is the capital investment of £ 650 K and therefore will not be

discounted annually (Percoco and Borgonovo, 2012).

In the year five there will be realistic cash inflows of £ 120 K by the sale of the vehicles.

No tax implications are assumed, and so the effect of depreciation has not been

considered.

Assumed a £50 K reduction in the overheads costs from £750 K to £700 K as the

allocated overheads are not incremental to the group as the whole (Weijermars, 2013).

The analysis will not include depreciation as this is not the part of cash flows.

Working Capital will increase by £1.5 M in the starting of the project and will

subsequently reduce back down at the end of the project.

Assumed there is no inflation.

Discount Rates are assumed to be 11%.

NPV method is based on the principal of netting of the present values of the investments inflows

with that of the initial investment incurred. For the evaluation of the project using this method,

the following steps were performed in sequence- Identification of Initial Investment- In the present case the initial investment computed by

the accountant for calculating profits was not correct as it did not include the working

capital which had to apply in the current year. Than the cost of buying the fleet vehicles

will be directly added to the initial cost which brings the total initial investment to £

21,50,000.

4

due to the fact that it uses the discounted cash inflows. The consideration of time value of money

gives more accurate and clear picture about the feasibility of the project. The major assumptions

used for the purpose of project evaluation are-

Marketing Cost is assumed to be sunk costs and thus not included in the calculation.

Cash Flows for the are considered over a five-year period which constitutes the lifecycle

of the project.

An annual license fee of £1 M per annum has been included for making the necessary

conclusions.

Purchase of vehicles is the capital investment of £ 650 K and therefore will not be

discounted annually (Percoco and Borgonovo, 2012).

In the year five there will be realistic cash inflows of £ 120 K by the sale of the vehicles.

No tax implications are assumed, and so the effect of depreciation has not been

considered.

Assumed a £50 K reduction in the overheads costs from £750 K to £700 K as the

allocated overheads are not incremental to the group as the whole (Weijermars, 2013).

The analysis will not include depreciation as this is not the part of cash flows.

Working Capital will increase by £1.5 M in the starting of the project and will

subsequently reduce back down at the end of the project.

Assumed there is no inflation.

Discount Rates are assumed to be 11%.

NPV method is based on the principal of netting of the present values of the investments inflows

with that of the initial investment incurred. For the evaluation of the project using this method,

the following steps were performed in sequence- Identification of Initial Investment- In the present case the initial investment computed by

the accountant for calculating profits was not correct as it did not include the working

capital which had to apply in the current year. Than the cost of buying the fleet vehicles

will be directly added to the initial cost which brings the total initial investment to £

21,50,000.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Computation Of Cash Inflows- Cash inflows in the total duration of the project are

derived by deducting the relevant expenditures from the sales figures. In the given case

while arriving at the figure of cash inflows the effect of depreciation was not given. This

is because the company is not liable for taxes as it falls in the special status growth

company. Also, the annual allocation of the overhead expenses will not be deducted as it

is not directly related to this project. Also, the opportunity cost of the rent expenses has

not been considered as they were not the actual outflows. After making the necessary

adjustments, the inflows are evaluated. Residual Value- For the purpose of the computation of the residual values the working

capital applied initially to the project will be added back. Also, the residual value of the

vehicles will be realised at the end of the fifth year, and so the final residual value would

be £1620000. This residual value will be discounted by using the present values of the

fifth year as they are recovered in the fifth year. Discount Rate- The rate at which the present values in the project are discounted to bring

them at par with the present value is known as the discount rate. For the purpose of

evaluation of the present project the discount rate used will be 11%. This rate is given in

the proposal for carrying out the evaluation (Dorfman and Cather, 2012). Evaluation Of Project based on NPV- Finally the NPV is calculated by the netting of the

present values of the inflows with the initial investment in the project. If the NPV is

positive then the project must be accepted as it is yielding the return at the desired rate. In

the given case the NPV comes out to be £1396000. Thus the NPV is positive and

therefore it would be beneficial for the company to invest in the proposal of genetically

developed mustard seeds.

Evaluation by IRR- Internal Rate of Return is used to make capital budgeting decisions. It is that

discount rate at which the NPV of all the cash inflows become zero. The IRR of the present

projects comes out to be 21.83% which is much higher than that of the discount rate used by the

company which is only 11%. Hence this project should be undertaken by the corporation due to

the high IRR of the cash inflows.

5

derived by deducting the relevant expenditures from the sales figures. In the given case

while arriving at the figure of cash inflows the effect of depreciation was not given. This

is because the company is not liable for taxes as it falls in the special status growth

company. Also, the annual allocation of the overhead expenses will not be deducted as it

is not directly related to this project. Also, the opportunity cost of the rent expenses has

not been considered as they were not the actual outflows. After making the necessary

adjustments, the inflows are evaluated. Residual Value- For the purpose of the computation of the residual values the working

capital applied initially to the project will be added back. Also, the residual value of the

vehicles will be realised at the end of the fifth year, and so the final residual value would

be £1620000. This residual value will be discounted by using the present values of the

fifth year as they are recovered in the fifth year. Discount Rate- The rate at which the present values in the project are discounted to bring

them at par with the present value is known as the discount rate. For the purpose of

evaluation of the present project the discount rate used will be 11%. This rate is given in

the proposal for carrying out the evaluation (Dorfman and Cather, 2012). Evaluation Of Project based on NPV- Finally the NPV is calculated by the netting of the

present values of the inflows with the initial investment in the project. If the NPV is

positive then the project must be accepted as it is yielding the return at the desired rate. In

the given case the NPV comes out to be £1396000. Thus the NPV is positive and

therefore it would be beneficial for the company to invest in the proposal of genetically

developed mustard seeds.

Evaluation by IRR- Internal Rate of Return is used to make capital budgeting decisions. It is that

discount rate at which the NPV of all the cash inflows become zero. The IRR of the present

projects comes out to be 21.83% which is much higher than that of the discount rate used by the

company which is only 11%. Hence this project should be undertaken by the corporation due to

the high IRR of the cash inflows.

5

Conclusion- As per all the investment appraisal methods, the project of advanced genetically

developed mustard seeds should be undertaken by the company. (All the necessary calculations

which form the basis of the conclusions form part of the appendix.)

TASK-B

Capital budgeting is a vital activity which includes different investment evaluation techniques.

These techniques are used by many organisations to perform evaluation regarding their long-

term investment decisions. In this section, the different methods that will be discussed are as

follows-

Net Present Value (NPV) & Internal Rate Of Return (IRR)

NPV is computed by the deducting the initial investment with the present values of cash inflows

that are expected from the investment and the respective outflows from the project. The NPV

rule states that the investment should be made in the project only if the NPV is a positive value.

This rule is based on the intuitive promise that the money held today is more than that same

amount of money tomorrow (Weijermars, 2013). The discount rate in NPV formula provides the

accountability for this rule. There are different ways used be the company to assess the discount

rates but the most common method is using the expected rate of return as the discount rate. This

rate is used to evaluate the various investment options with similar characteristics. An example

has been explained to illustrate this-

Consider the two projects A & B under the NPV method, and the discount rate is taken as 10%.

Investment Sale Price Cash flows (year-1) Cash Flows (year-2)

Investment A £50000 £ 0 £ 100000

Investment-B £50000 £50000 £ 50000.

NPV of Project A = £100000/(1+.10) ^2- £ 50000 = £ 32644.

NPV of project B = £ 50000/(1+.10)+ £25000/(1+.10)^2- £50000= £16115.

As per the NPV criteria, the decision favours Project A because it leads to higher NPV than that

of project B. As per the opinions of many financial decision makers. There are many other

methods in practice which are used that do not consider the discounted method of project

evaluation. However, the projects with a positive NPV should be taken only if the project does

not prevent another competing project from being undertaken because every project compete in

6

developed mustard seeds should be undertaken by the company. (All the necessary calculations

which form the basis of the conclusions form part of the appendix.)

TASK-B

Capital budgeting is a vital activity which includes different investment evaluation techniques.

These techniques are used by many organisations to perform evaluation regarding their long-

term investment decisions. In this section, the different methods that will be discussed are as

follows-

Net Present Value (NPV) & Internal Rate Of Return (IRR)

NPV is computed by the deducting the initial investment with the present values of cash inflows

that are expected from the investment and the respective outflows from the project. The NPV

rule states that the investment should be made in the project only if the NPV is a positive value.

This rule is based on the intuitive promise that the money held today is more than that same

amount of money tomorrow (Weijermars, 2013). The discount rate in NPV formula provides the

accountability for this rule. There are different ways used be the company to assess the discount

rates but the most common method is using the expected rate of return as the discount rate. This

rate is used to evaluate the various investment options with similar characteristics. An example

has been explained to illustrate this-

Consider the two projects A & B under the NPV method, and the discount rate is taken as 10%.

Investment Sale Price Cash flows (year-1) Cash Flows (year-2)

Investment A £50000 £ 0 £ 100000

Investment-B £50000 £50000 £ 50000.

NPV of Project A = £100000/(1+.10) ^2- £ 50000 = £ 32644.

NPV of project B = £ 50000/(1+.10)+ £25000/(1+.10)^2- £50000= £16115.

As per the NPV criteria, the decision favours Project A because it leads to higher NPV than that

of project B. As per the opinions of many financial decision makers. There are many other

methods in practice which are used that do not consider the discounted method of project

evaluation. However, the projects with a positive NPV should be taken only if the project does

not prevent another competing project from being undertaken because every project compete in

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

itself delayed in time (Coles, Lemmon, and Meschke, 2012). On the contrary, IRR is the measure

of profitability of the investment that is internally invested over a period to period and has not

been recovered or recaptured by the investor. The major limitation of IRR is it uses the same

discount rate to evaluate every investment. However, if the all the other factors remain constant,

the IRR and NPV method will give the same results. The higher the IRR of the project the most

desirable it will become. Although the single discount rate simplifies the matters, there are ample

situations in which IRR does not produce profitable outcomes (Difference Between NPV and

IRR, 2017). For making the analysis of the simpler projects which have a common discount rates

and carry equal risks and a shorter period IRR is appropriate. But for the purpose of evaluating

those projects which are subject to different risk factors and are of longer duration IRR method

will not produce profitable results. In such case, NPV methods bring a more clear picture. IRR

method is redundant due to the single discount rate used by it whereas in an actual scenario the

discount rates change eventually over a period (Brealey, and et, al., 2012). Hence without

adequate modifications, IRR will not be appropriate for the evaluation of complex investment

projects. An illustration of how IRR is ineffective in the projects has been illustrated as follows-

Example- Consider a project with the cash flows of -£50000 as the first year outlay and the

inflows in the year 2 are £ 115000, and there are additional costs to be incurred in the third year

of £66000. Now since the project has been subsequently revised due to the additional outflows,

IRR evaluation technique could not be used. IRR rate makes the project break even but if the

market conditions change over a period than the project has different IRR's. Hence there are

multiple rates at which the project will be discounted (Understanding the Difference Between

NPV vs. IRR, 2017). Here lies the advantage of using NPV method which can handle multiple

discount rates without any problem and produce relevant solutions. Each of the cash flows can be

discounted separately from that of others.

Another problem in using IRR is when the project is with unknown discount rates. To analyse

the viability of the project, IRR must be compared with the discount rate. In the event of

unknown discount rate such comparison cannot be made and IRR may produce indefeasible

results. Therefore NPV is a better analytical tool than IRR.

7

of profitability of the investment that is internally invested over a period to period and has not

been recovered or recaptured by the investor. The major limitation of IRR is it uses the same

discount rate to evaluate every investment. However, if the all the other factors remain constant,

the IRR and NPV method will give the same results. The higher the IRR of the project the most

desirable it will become. Although the single discount rate simplifies the matters, there are ample

situations in which IRR does not produce profitable outcomes (Difference Between NPV and

IRR, 2017). For making the analysis of the simpler projects which have a common discount rates

and carry equal risks and a shorter period IRR is appropriate. But for the purpose of evaluating

those projects which are subject to different risk factors and are of longer duration IRR method

will not produce profitable results. In such case, NPV methods bring a more clear picture. IRR

method is redundant due to the single discount rate used by it whereas in an actual scenario the

discount rates change eventually over a period (Brealey, and et, al., 2012). Hence without

adequate modifications, IRR will not be appropriate for the evaluation of complex investment

projects. An illustration of how IRR is ineffective in the projects has been illustrated as follows-

Example- Consider a project with the cash flows of -£50000 as the first year outlay and the

inflows in the year 2 are £ 115000, and there are additional costs to be incurred in the third year

of £66000. Now since the project has been subsequently revised due to the additional outflows,

IRR evaluation technique could not be used. IRR rate makes the project break even but if the

market conditions change over a period than the project has different IRR's. Hence there are

multiple rates at which the project will be discounted (Understanding the Difference Between

NPV vs. IRR, 2017). Here lies the advantage of using NPV method which can handle multiple

discount rates without any problem and produce relevant solutions. Each of the cash flows can be

discounted separately from that of others.

Another problem in using IRR is when the project is with unknown discount rates. To analyse

the viability of the project, IRR must be compared with the discount rate. In the event of

unknown discount rate such comparison cannot be made and IRR may produce indefeasible

results. Therefore NPV is a better analytical tool than IRR.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

The present report evaluates the project of producing and marketing the genetically

developed mustard seeds by Genetic Plc. Payback, NPV and IRR methods are used to reach a

reasonable conclusion of undertaking the investment project. Section B covers the importance of

using NPV over IRR method along with some supporting illustrations.

8

The present report evaluates the project of producing and marketing the genetically

developed mustard seeds by Genetic Plc. Payback, NPV and IRR methods are used to reach a

reasonable conclusion of undertaking the investment project. Section B covers the importance of

using NPV over IRR method along with some supporting illustrations.

8

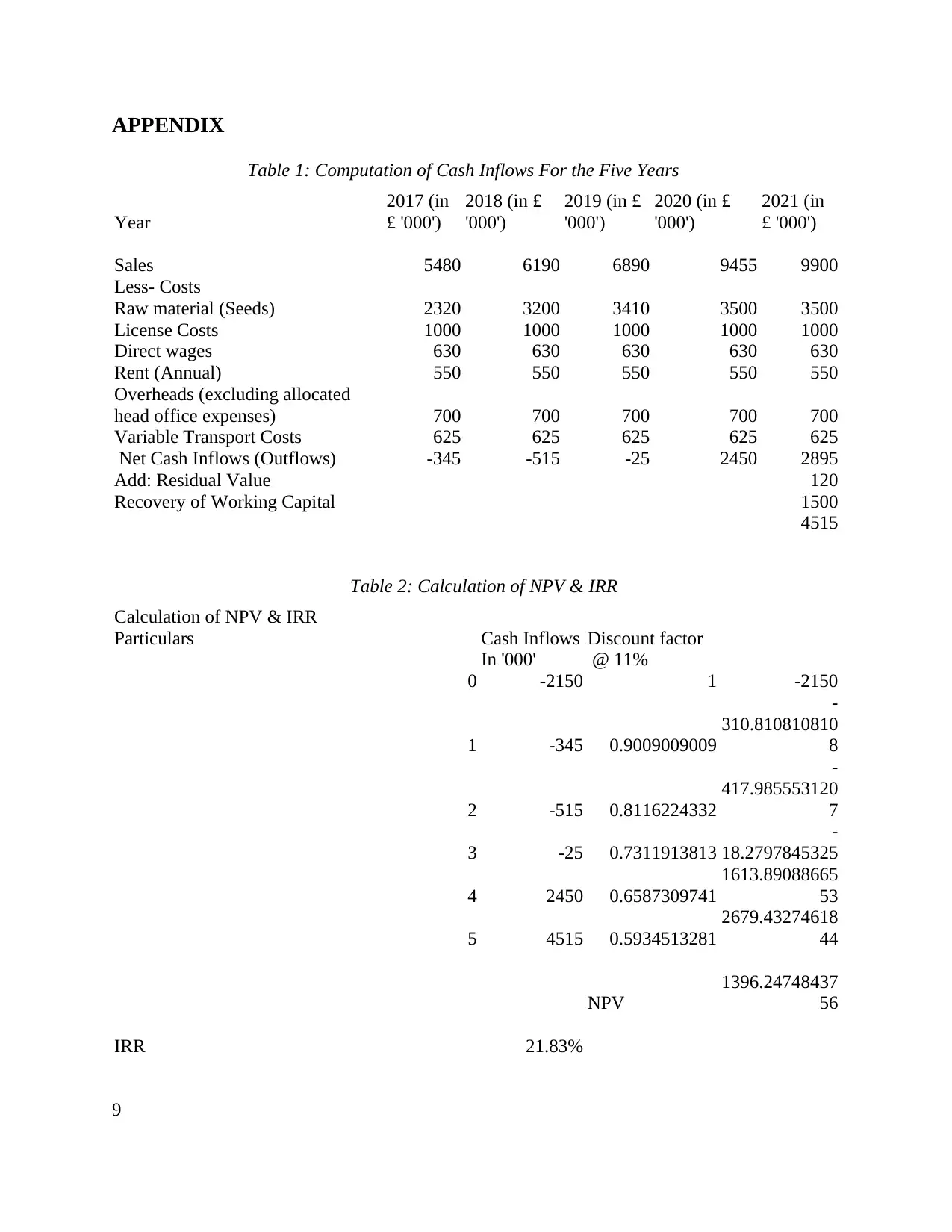

APPENDIX

Table 1: Computation of Cash Inflows For the Five Years

Year

2017 (in

£ '000')

2018 (in £

'000')

2019 (in £

'000')

2020 (in £

'000')

2021 (in

£ '000')

Sales 5480 6190 6890 9455 9900

Less- Costs

Raw material (Seeds) 2320 3200 3410 3500 3500

License Costs 1000 1000 1000 1000 1000

Direct wages 630 630 630 630 630

Rent (Annual) 550 550 550 550 550

Overheads (excluding allocated

head office expenses) 700 700 700 700 700

Variable Transport Costs 625 625 625 625 625

Net Cash Inflows (Outflows) -345 -515 -25 2450 2895

Add: Residual Value 120

Recovery of Working Capital 1500

4515

Table 2: Calculation of NPV & IRR

Calculation of NPV & IRR

Particulars Cash Inflows Discount factor

In '000' @ 11%

0 -2150 1 -2150

1 -345 0.9009009009

-

310.810810810

8

2 -515 0.8116224332

-

417.985553120

7

3 -25 0.7311913813

-

18.2797845325

4 2450 0.6587309741

1613.89088665

53

5 4515 0.5934513281

2679.43274618

44

NPV

1396.24748437

56

IRR 21.83%

9

Table 1: Computation of Cash Inflows For the Five Years

Year

2017 (in

£ '000')

2018 (in £

'000')

2019 (in £

'000')

2020 (in £

'000')

2021 (in

£ '000')

Sales 5480 6190 6890 9455 9900

Less- Costs

Raw material (Seeds) 2320 3200 3410 3500 3500

License Costs 1000 1000 1000 1000 1000

Direct wages 630 630 630 630 630

Rent (Annual) 550 550 550 550 550

Overheads (excluding allocated

head office expenses) 700 700 700 700 700

Variable Transport Costs 625 625 625 625 625

Net Cash Inflows (Outflows) -345 -515 -25 2450 2895

Add: Residual Value 120

Recovery of Working Capital 1500

4515

Table 2: Calculation of NPV & IRR

Calculation of NPV & IRR

Particulars Cash Inflows Discount factor

In '000' @ 11%

0 -2150 1 -2150

1 -345 0.9009009009

-

310.810810810

8

2 -515 0.8116224332

-

417.985553120

7

3 -25 0.7311913813

-

18.2797845325

4 2450 0.6587309741

1613.89088665

53

5 4515 0.5934513281

2679.43274618

44

NPV

1396.24748437

56

IRR 21.83%

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

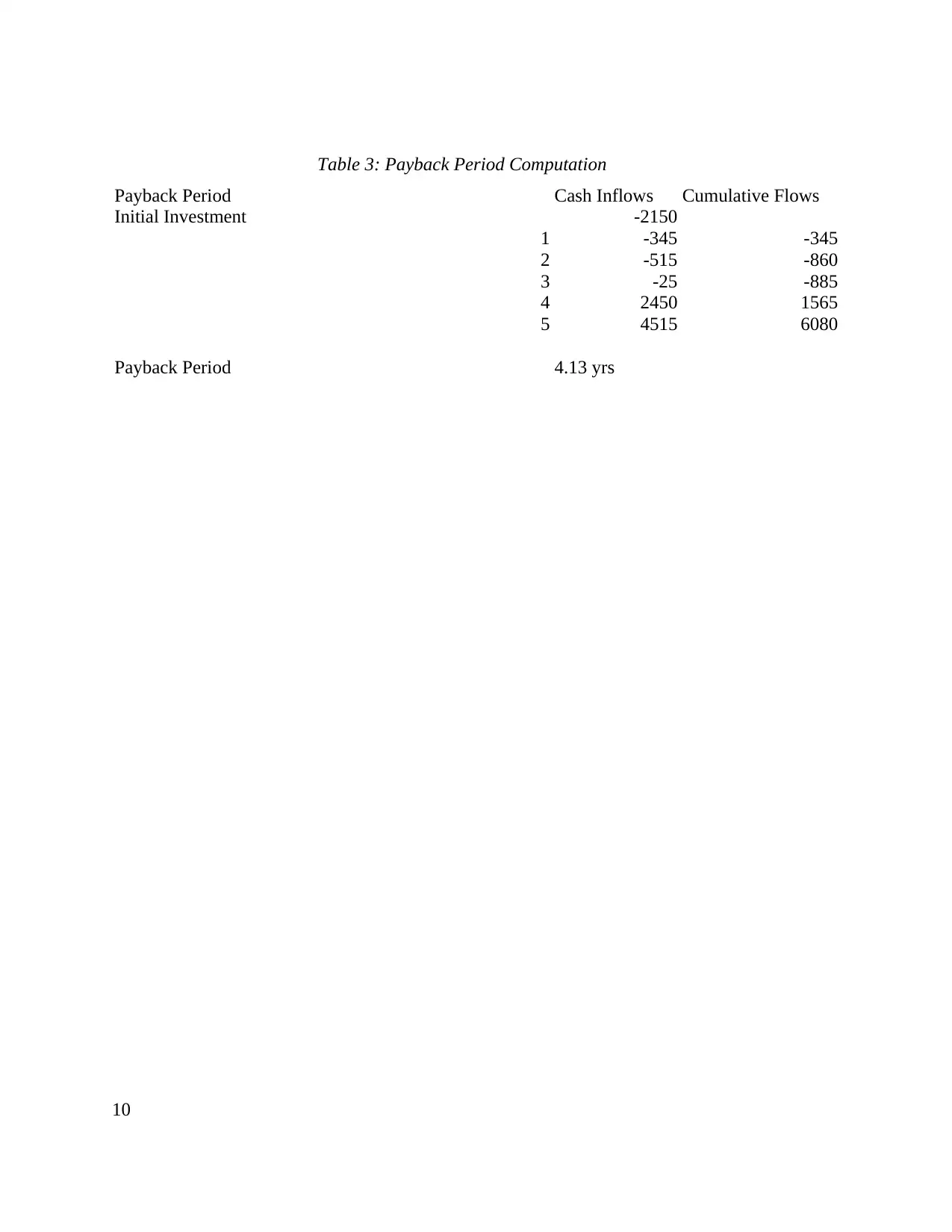

Table 3: Payback Period Computation

Payback Period Cash Inflows Cumulative Flows

Initial Investment -2150

1 -345 -345

2 -515 -860

3 -25 -885

4 2450 1565

5 4515 6080

Payback Period 4.13 yrs

10

Payback Period Cash Inflows Cumulative Flows

Initial Investment -2150

1 -345 -345

2 -515 -860

3 -25 -885

4 2450 1565

5 4515 6080

Payback Period 4.13 yrs

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Brealey, R. A., and et,al., 2012. Principles of corporate finance. Tata McGraw-Hill Education.

Charnes, J., 2012. Financial modeling with crystal ball and excel. John Wiley & Sons.

Clayman, M .R., Fridson, M. S. and Troughton, G.H., 2012. Corporate finance: A practical

approach (Vol. 42). John Wiley & Sons.

Coles, J .L., Lemmon, M. L. and Meschke, J. F., 2012. Structural models and endogeneity in

corporate finance: The link between managerial ownership and corporate performance.

Journal of Financial Economics .103(1). pp.149-168.

De Luca, A.I., and et.al, 2014. Sustainability assessment of quality-oriented citrus growing

systems in Mediterranean area. Calitatea .15(141). p.103.

Dorfman, M.S. and Cather, D.A., 2012. Introduction to risk management and insurance. Pearson

Higher Ed.

Palomino, R.G. and Nebra, S.A., 2012. The potential of natural gas use including cogeneration

in large-sized industry and commercial sector in Peru. Energy policy, 50, pp.192-206.

Percoco, M. and Borgonovo, E., 2012. A note on the sensitivity analysis of the internal rate of

return. International Journal of Production Economics, 135(1), pp.526-529.

Roberts, M.R. and Whited, T.M., 2012. Endogeneity in empirical corporate finance.

Sawaengsak, W., and et.al, 2014. Life cycle cost of biodiesel production from microalgae in

Thailand. Energy for Sustainable Development, 18, pp.67-74.

Sontamino, P. and Drebenstedt, C., 2013, April. A Prototype Dynamics Decision Making Model

of Mining Feasibility Study on Investment. In International Forum-Competition of Young

Researches, St. Petersburg.

Weijermars, R., 2013. Economic appraisal of shale gas plays in Continental Europe. Applied

Energy, 106, pp.100-115.

Yoshizaki, T., and et.al, 2013. Improved economic viability of integrated biogas energy and

compost production for sustainable palm oil mill management. Journal of Cleaner

Production. 44. pp.1-7.

ONLINE

11

Brealey, R. A., and et,al., 2012. Principles of corporate finance. Tata McGraw-Hill Education.

Charnes, J., 2012. Financial modeling with crystal ball and excel. John Wiley & Sons.

Clayman, M .R., Fridson, M. S. and Troughton, G.H., 2012. Corporate finance: A practical

approach (Vol. 42). John Wiley & Sons.

Coles, J .L., Lemmon, M. L. and Meschke, J. F., 2012. Structural models and endogeneity in

corporate finance: The link between managerial ownership and corporate performance.

Journal of Financial Economics .103(1). pp.149-168.

De Luca, A.I., and et.al, 2014. Sustainability assessment of quality-oriented citrus growing

systems in Mediterranean area. Calitatea .15(141). p.103.

Dorfman, M.S. and Cather, D.A., 2012. Introduction to risk management and insurance. Pearson

Higher Ed.

Palomino, R.G. and Nebra, S.A., 2012. The potential of natural gas use including cogeneration

in large-sized industry and commercial sector in Peru. Energy policy, 50, pp.192-206.

Percoco, M. and Borgonovo, E., 2012. A note on the sensitivity analysis of the internal rate of

return. International Journal of Production Economics, 135(1), pp.526-529.

Roberts, M.R. and Whited, T.M., 2012. Endogeneity in empirical corporate finance.

Sawaengsak, W., and et.al, 2014. Life cycle cost of biodiesel production from microalgae in

Thailand. Energy for Sustainable Development, 18, pp.67-74.

Sontamino, P. and Drebenstedt, C., 2013, April. A Prototype Dynamics Decision Making Model

of Mining Feasibility Study on Investment. In International Forum-Competition of Young

Researches, St. Petersburg.

Weijermars, R., 2013. Economic appraisal of shale gas plays in Continental Europe. Applied

Energy, 106, pp.100-115.

Yoshizaki, T., and et.al, 2013. Improved economic viability of integrated biogas energy and

compost production for sustainable palm oil mill management. Journal of Cleaner

Production. 44. pp.1-7.

ONLINE

11

Difference Between NPV and IRR, 2017. Avaliable

through<http://keydifferences.com/difference-between-npv-and-irr.html> Assessed on 07th

January 2016.

Understanding the Difference Between NPV vs IRR, 2017.Avaliable

through<http://www.propertymetrics.com/blog/2013/06/28/npv-vs-irr/> Assessed on 07th

January 2016.

12

through<http://keydifferences.com/difference-between-npv-and-irr.html> Assessed on 07th

January 2016.

Understanding the Difference Between NPV vs IRR, 2017.Avaliable

through<http://www.propertymetrics.com/blog/2013/06/28/npv-vs-irr/> Assessed on 07th

January 2016.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.