FIN203 Corporate Finance Assignment: Apple Inc. Analysis, Assessment 2

VerifiedAdded on 2023/03/17

|5

|1851

|42

Homework Assignment

AI Summary

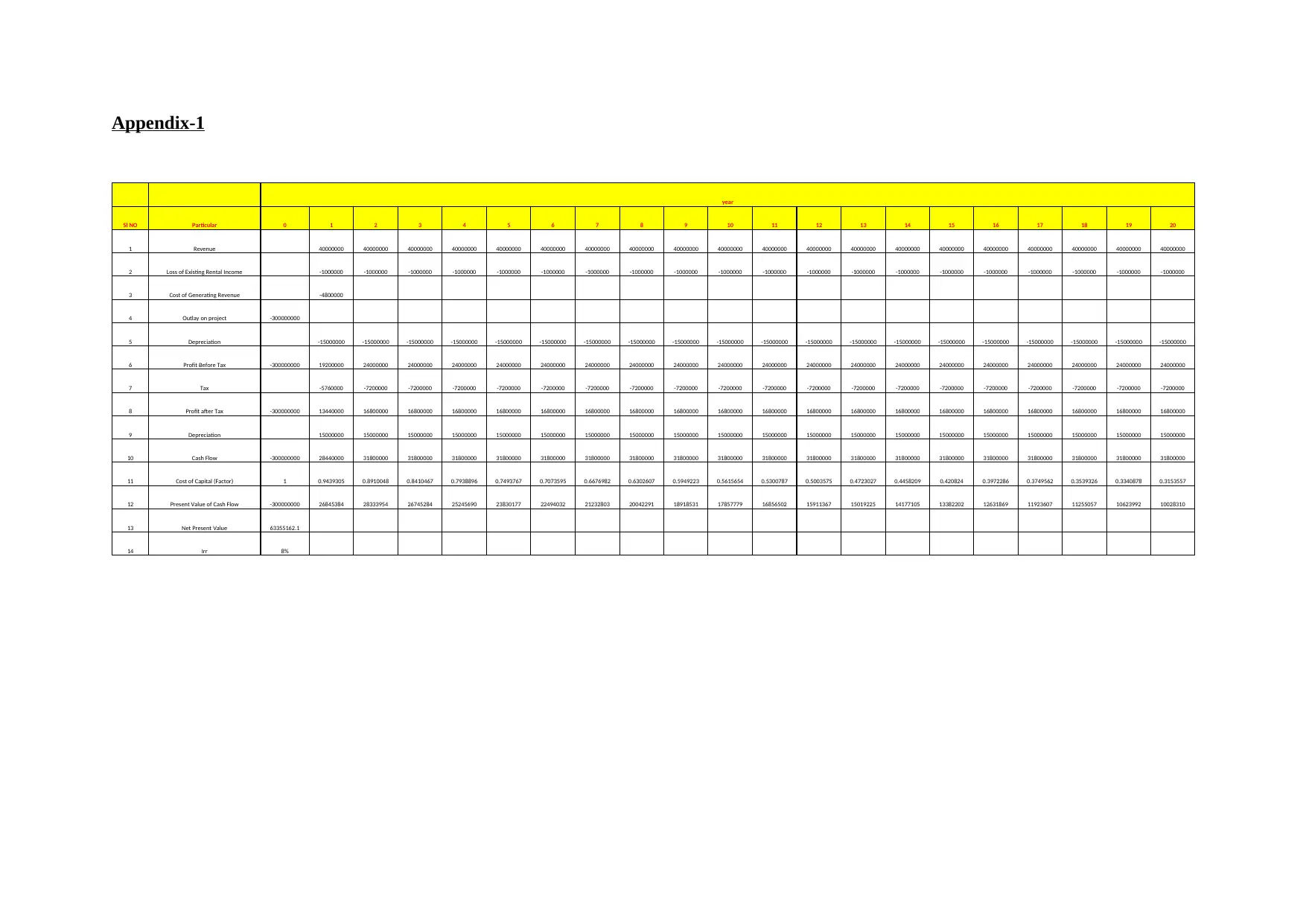

This assignment analyzes Apple Inc.'s financial performance from a corporate finance perspective. Part 1 examines Apple's cash conversion cycle, comparing it to Samsung's, and identifies market, technological, and supply chain risks. It also assesses Apple's stock performance relative to market indices and evaluates the company's debt levels and bond pricing. Part 2 focuses on a hypothetical project, using Net Present Value (NPV) and Internal Rate of Return (IRR) analysis to determine whether Apple should build a new store, considering relevant costs, free cash flows, and the project's feasibility, ultimately recommending the project's acceptance based on positive financial metrics and a higher IRR than the cost of capital. The solution includes detailed calculations and appendices supporting the financial analysis and decision-making process.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.