FIN203 Assessment: Corporate Finance Report on Fortescue Metals Group

VerifiedAdded on 2022/08/23

|12

|2200

|18

Report

AI Summary

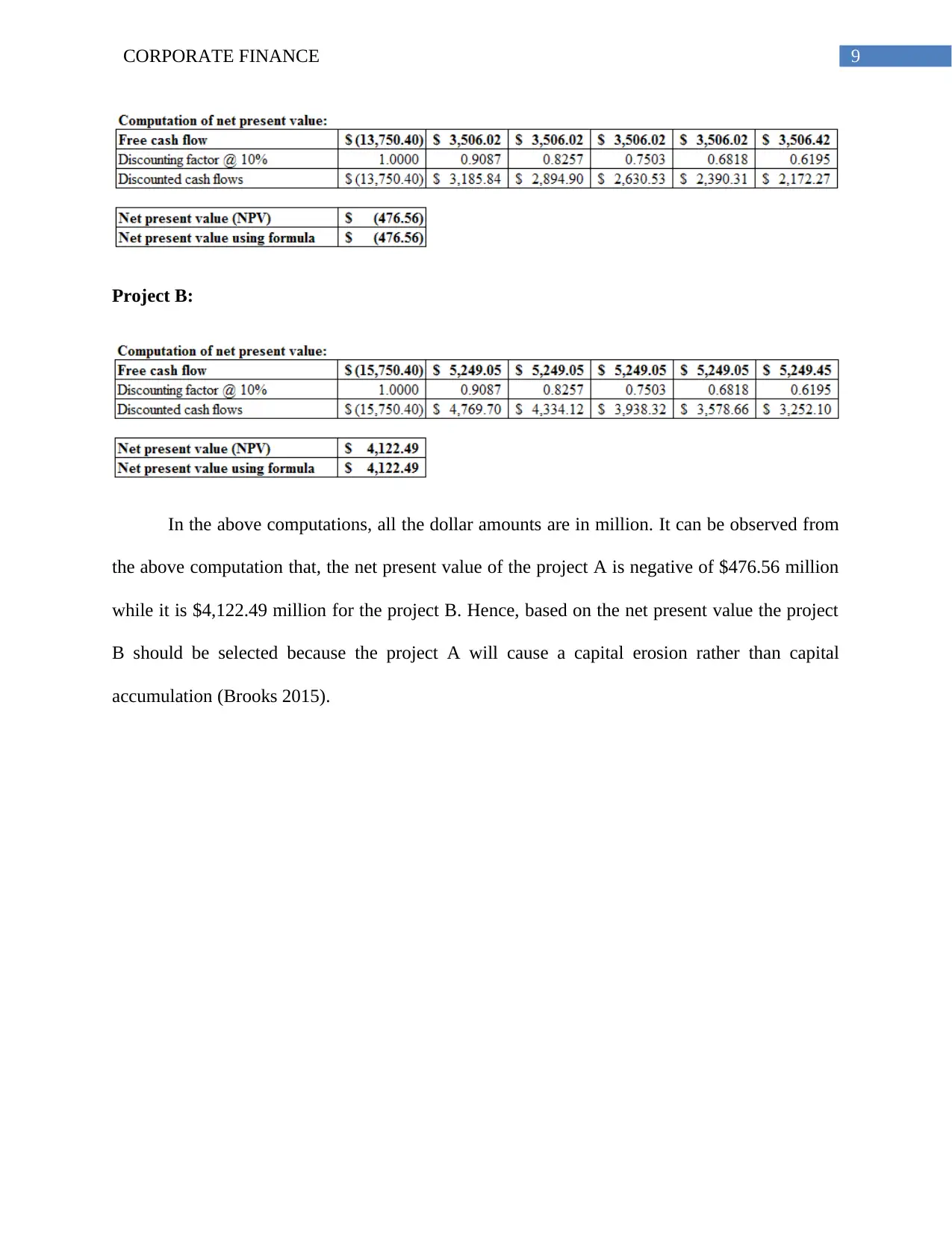

This report provides a detailed corporate finance analysis of Fortescue Metals Group (FMG). It begins with a background of the company, its operations, and its position in the iron ore industry. The report then delves into key financial metrics, including an analysis of FMG's cash conversion cycle, evaluating its efficiency in managing working capital. The report also includes a bond valuation, determining the fair price of FMG's bonds based on coupon rates, face value, and yield to maturity, as well as an analysis of bond ratings and their implications. Furthermore, the report assesses share valuation, calculating the intrinsic value of FMG's shares using the CAPM model and dividend discount model, and comparing this value to the market price to determine if the shares are undervalued or overvalued. Finally, the report addresses capital budgeting, evaluating two potential projects (A and B) using the Net Present Value (NPV) method to determine which project would be more financially beneficial, and providing the financial calculations and rationale for the optimal investment decision. The report concludes with a list of references used.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.