Corporate Finance Assignment: Analysis of Risk and Return Concepts

VerifiedAdded on 2022/08/15

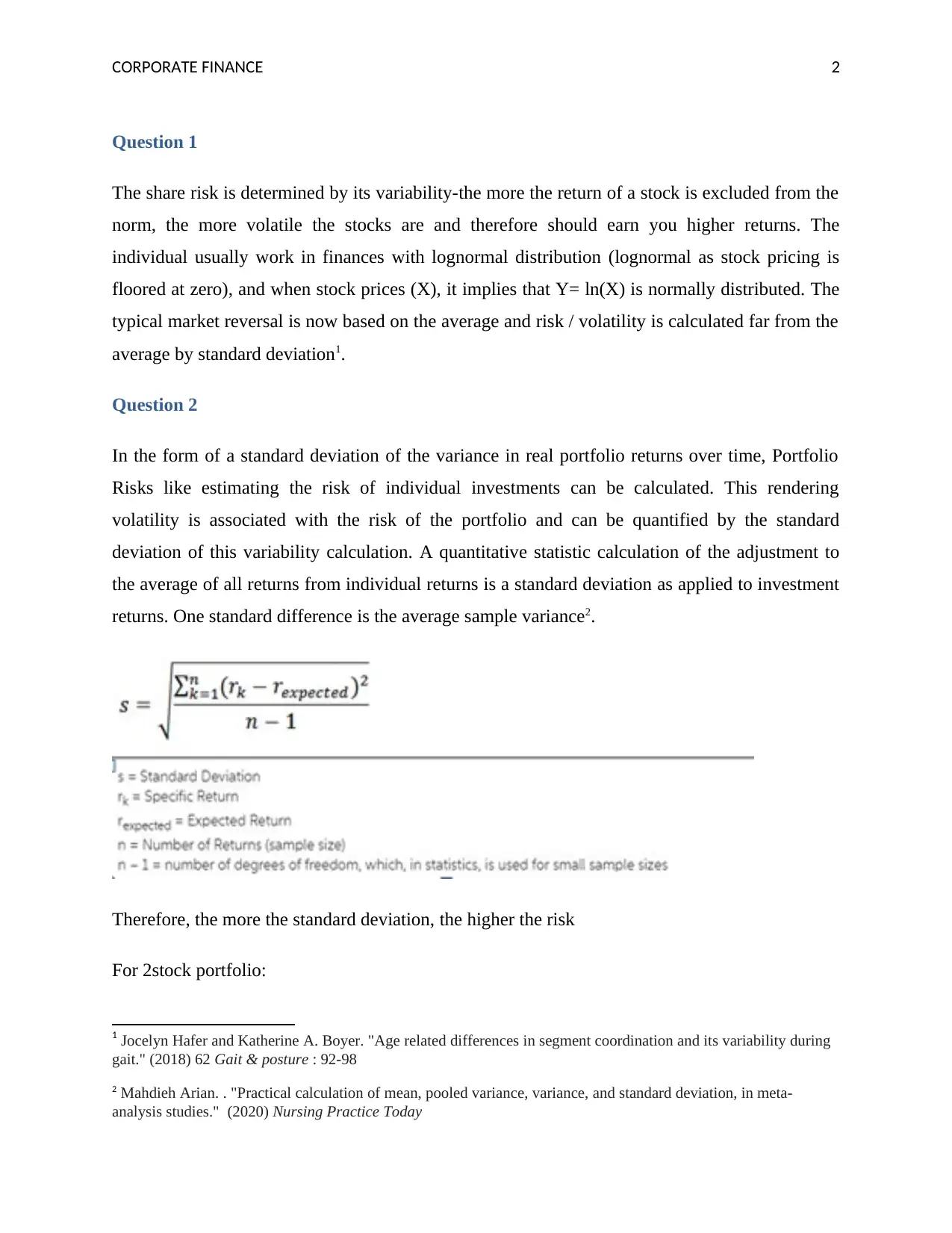

|6

|1065

|12

Homework Assignment

AI Summary

This document provides solutions to a corporate finance assignment, addressing key concepts such as risk and return. The assignment explores how share risk is calculated using standard deviation and dispersion statistics, including the application of the normal distribution. It delves into portfolio risk, explaining how standard deviation of variance in real portfolio returns over time is used to estimate the risk of individual investments, and how portfolio variance is calculated for 2-stock portfolios. The assignment further analyzes the impact of risk-free assets on portfolio risk, demonstrating how the standard deviation simplifies when one asset is risk-free. Finally, it differentiates between systematic and unsystematic risks, explaining how diversification can reduce unsystematic risk while systematic risk affects the entire economy. The document includes references to support the analysis.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.