Corporate Finance: Funding Sources and Entity Classifications

VerifiedAdded on 2022/10/09

|19

|4040

|34

Report

AI Summary

This report analyzes the corporate financial accounting practices of Wesfarmers and Woolworths Group, focusing on their equity and liabilities over a three-year period. It examines the movement in equity components like capital equity, reserves, and retained earnings, highlighting significant changes such as the decrease in Wesfarmers' equity due to demerger capital distribution. The report assesses the liabilities sections, detailing the fluctuations in current and non-current liabilities, including the impact of asset sales and borrowings. Furthermore, it provides a comparative analysis of the advantages and disadvantages of equity and debt financing for both companies. Finally, the report discusses the concepts of large and small proprietary companies and reporting entities, outlining their classification implications and reporting requirements.

CORPORATE FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ABSTRACT

Corporate accounting can be referred to as special branch of accounting which comprises

accounting for companies, drafting of financial statements, interpretation of financial results of

companies etc. The present study provides discussion relating to movement in equity and

liabilities of Wesfarmers and Woolworths Group. It has been assessed that liabilities of

Woolworths Group have fluctuating trend comparatively as significant increase and decrease has

been analyzed in same. In terms of equity parameters, the decrease has been accessed in case of

Wesfarmers. Thus it is recommended to reconstruct the capital structure in order to provide

adequate return to shareholders. Further concepts of small proprietary company, large

proprietary company and reporting entity has also been discussed in which it has been assessed

that each company, inclusive of Small Proprietary Company, is required to have enough

accounting or financial transactions records and enough to enable to pile up financial statement

when required.

Corporate accounting can be referred to as special branch of accounting which comprises

accounting for companies, drafting of financial statements, interpretation of financial results of

companies etc. The present study provides discussion relating to movement in equity and

liabilities of Wesfarmers and Woolworths Group. It has been assessed that liabilities of

Woolworths Group have fluctuating trend comparatively as significant increase and decrease has

been analyzed in same. In terms of equity parameters, the decrease has been accessed in case of

Wesfarmers. Thus it is recommended to reconstruct the capital structure in order to provide

adequate return to shareholders. Further concepts of small proprietary company, large

proprietary company and reporting entity has also been discussed in which it has been assessed

that each company, inclusive of Small Proprietary Company, is required to have enough

accounting or financial transactions records and enough to enable to pile up financial statement

when required.

TABLE OF CONTENTS

Introduction......................................................................................................................................4

Part A...............................................................................................................................................4

Explanation of items recorded under equity section of both the companies...............................4

Explanation of movement in each item under owner’s equity section of both the companies. . .5

Assessment of liabilities section of Wesfarmers and Woolworths..............................................6

Explanation of movement in each item under liabilities section of both the companies............7

Advantages and disadvantages of each source of funds used by each company.........................8

Part B.............................................................................................................................................10

Large proprietary company........................................................................................................10

Small proprietary company........................................................................................................11

Reporting entity.............................................................................................................................12

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

Introduction......................................................................................................................................4

Part A...............................................................................................................................................4

Explanation of items recorded under equity section of both the companies...............................4

Explanation of movement in each item under owner’s equity section of both the companies. . .5

Assessment of liabilities section of Wesfarmers and Woolworths..............................................6

Explanation of movement in each item under liabilities section of both the companies............7

Advantages and disadvantages of each source of funds used by each company.........................8

Part B.............................................................................................................................................10

Large proprietary company........................................................................................................10

Small proprietary company........................................................................................................11

Reporting entity.............................................................................................................................12

Conclusion.....................................................................................................................................12

References......................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Corporate finance is referred to as an area of finance which assists in analyzing sources of

funding in order to increase the organization’s value to shareholders (Eisenschmidt and Schmidt,

2018). The specified subject assists in taking adequate capital investment decision through

application of various strategies. The present study provides details relating to assessment of

equity and liabilities of Wesfarmers and Woolworths group. In order to assess the movement in

liabilities and equity of both the company’s balance sheet of recent three years have been

analysed in an appropriate manner. Eventually, advantages and disadvantages of sources applied

by each company has been discussed. Further, discussion has also been provided relating to

concepts of small proprietary company and large proprietary company and reporting entity to

assess the implications of their classification adequately.

PART A

Explanation of items recorded under the equity section of both the companies

Woolworths is Australia’s largest supermarket chain. It operates approximately 995 stores and

makes efficient attempt to provide superior services, variety, value and convenience to its

customers. The main purpose of the group is to develop a better experience together to make

their customer’s life better (Woolworths Annual Report. 2017). It equity section comprises

capital equity, reserves, retained earnings and non-controlling interest. Equity represents the

amount of capital which has been financed through help of common shares. In January 2018

Non-executive director had provided plan to encourage and facilitate ownership of board

members. The specified plan provided auto mechanism for participants to acquire shares.

Reserves comprise hedging reserve, foreign currency translation reserve, remuneration reserve,

asset revaluation reserve and equity instrument reserve. Retained earnings represent the amount

of profit which has been held by company instead of paying it to shareholders. Non-controlling

interest is also referred as minority interest, representing ownership position where shareholder

owns less than fifty per cent (Leuz and Wysocki, 2016).

Wesfarmers Ltd has a diversified portfolio business which deals in department stores, energy

distribution, chemicals, fertiliser, safety products etc. (Wesfarmers 2017 Annual Report, 2017.).

Corporate finance is referred to as an area of finance which assists in analyzing sources of

funding in order to increase the organization’s value to shareholders (Eisenschmidt and Schmidt,

2018). The specified subject assists in taking adequate capital investment decision through

application of various strategies. The present study provides details relating to assessment of

equity and liabilities of Wesfarmers and Woolworths group. In order to assess the movement in

liabilities and equity of both the company’s balance sheet of recent three years have been

analysed in an appropriate manner. Eventually, advantages and disadvantages of sources applied

by each company has been discussed. Further, discussion has also been provided relating to

concepts of small proprietary company and large proprietary company and reporting entity to

assess the implications of their classification adequately.

PART A

Explanation of items recorded under the equity section of both the companies

Woolworths is Australia’s largest supermarket chain. It operates approximately 995 stores and

makes efficient attempt to provide superior services, variety, value and convenience to its

customers. The main purpose of the group is to develop a better experience together to make

their customer’s life better (Woolworths Annual Report. 2017). It equity section comprises

capital equity, reserves, retained earnings and non-controlling interest. Equity represents the

amount of capital which has been financed through help of common shares. In January 2018

Non-executive director had provided plan to encourage and facilitate ownership of board

members. The specified plan provided auto mechanism for participants to acquire shares.

Reserves comprise hedging reserve, foreign currency translation reserve, remuneration reserve,

asset revaluation reserve and equity instrument reserve. Retained earnings represent the amount

of profit which has been held by company instead of paying it to shareholders. Non-controlling

interest is also referred as minority interest, representing ownership position where shareholder

owns less than fifty per cent (Leuz and Wysocki, 2016).

Wesfarmers Ltd has a diversified portfolio business which deals in department stores, energy

distribution, chemicals, fertiliser, safety products etc. (Wesfarmers 2017 Annual Report, 2017.).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The primary objective of company is to provide adequate returns to shareholders. The equity

section of Wesfarmers comprises issues capital, reserved shares, accumulated losses/ retained

earnings and reserves. Reserved shares represent ordinary shares which have been repurchased

and held for future use. Demerger reserve, share-based payment reserve, cash-flow hedge

reserve, financial asset reserve, capital reserve and foreign currency translation reserve are part

of company’s reserve (Wesfarmers 2019 Annual Report., 2019).

Explanation of movement in each item under the owner’s equity section of both the

companies

Woolworths Ltd (Figures in %)

Year 2019 2018 2017

Equity -4% 8% 7%

Increase / Decrease in percentage

Reserve 39% -1% 4%

Increase / Decrease in percentage

Retained Earning -3% 15% 14%

Increase / Decrease in percentage

Non controlling interest 4% 5% 12%

Increase / Decrease in percentage

Total Equity -2% 10% 12%

Increase / Decrease in percentage

Wesfarmers (Figures in %)

Year 2019 2017 2017

Equity

Increase / Decrease in percentage -29% 0.04% 2.00%

Reserved shares 88% 65.38% -7.00%

Increase / Decrease in percentage

section of Wesfarmers comprises issues capital, reserved shares, accumulated losses/ retained

earnings and reserves. Reserved shares represent ordinary shares which have been repurchased

and held for future use. Demerger reserve, share-based payment reserve, cash-flow hedge

reserve, financial asset reserve, capital reserve and foreign currency translation reserve are part

of company’s reserve (Wesfarmers 2019 Annual Report., 2019).

Explanation of movement in each item under the owner’s equity section of both the

companies

Woolworths Ltd (Figures in %)

Year 2019 2018 2017

Equity -4% 8% 7%

Increase / Decrease in percentage

Reserve 39% -1% 4%

Increase / Decrease in percentage

Retained Earning -3% 15% 14%

Increase / Decrease in percentage

Non controlling interest 4% 5% 12%

Increase / Decrease in percentage

Total Equity -2% 10% 12%

Increase / Decrease in percentage

Wesfarmers (Figures in %)

Year 2019 2017 2017

Equity

Increase / Decrease in percentage -29% 0.04% 2.00%

Reserved shares 88% 65.38% -7.00%

Increase / Decrease in percentage

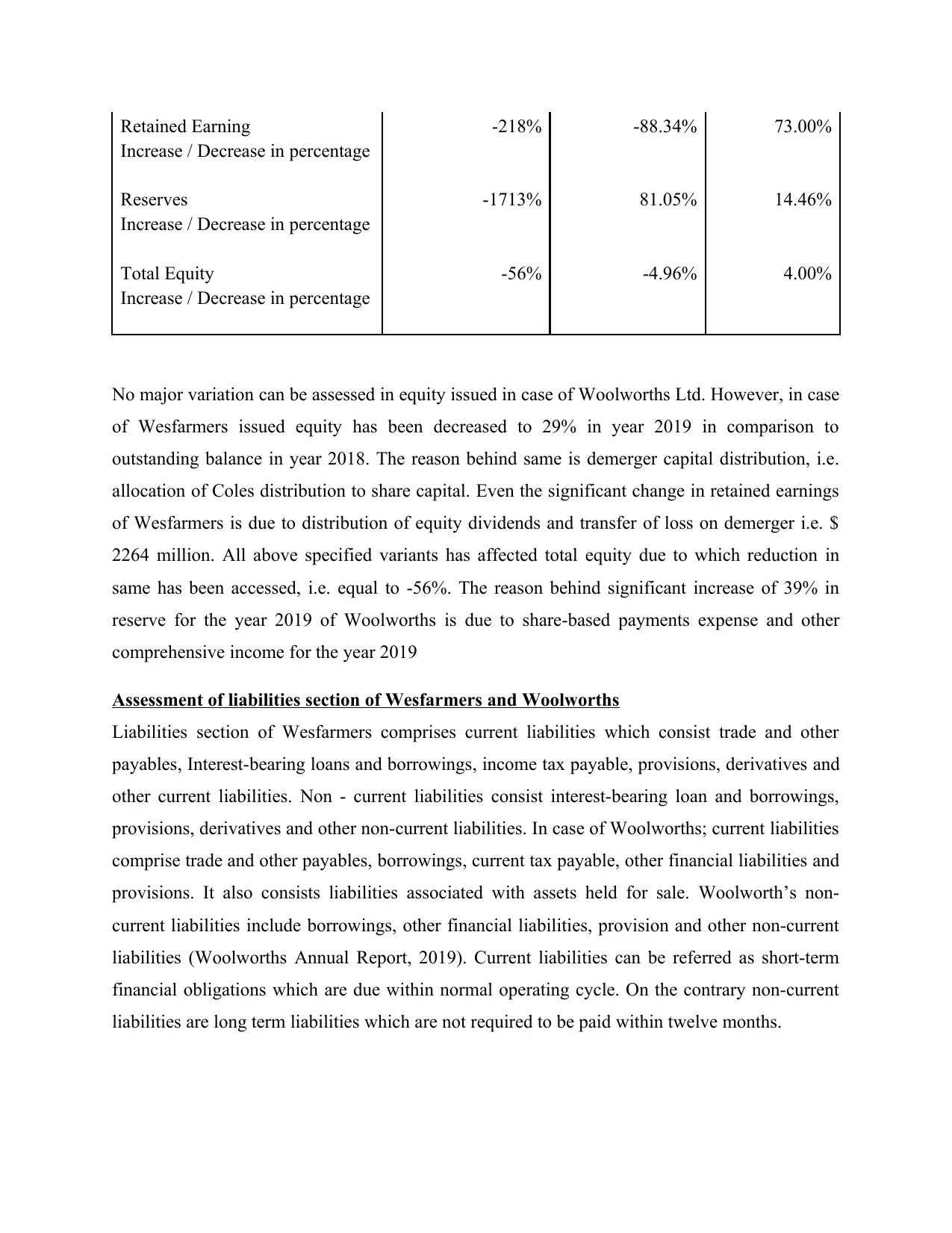

Retained Earning -218% -88.34% 73.00%

Increase / Decrease in percentage

Reserves -1713% 81.05% 14.46%

Increase / Decrease in percentage

Total Equity -56% -4.96% 4.00%

Increase / Decrease in percentage

No major variation can be assessed in equity issued in case of Woolworths Ltd. However, in case

of Wesfarmers issued equity has been decreased to 29% in year 2019 in comparison to

outstanding balance in year 2018. The reason behind same is demerger capital distribution, i.e.

allocation of Coles distribution to share capital. Even the significant change in retained earnings

of Wesfarmers is due to distribution of equity dividends and transfer of loss on demerger i.e. $

2264 million. All above specified variants has affected total equity due to which reduction in

same has been accessed, i.e. equal to -56%. The reason behind significant increase of 39% in

reserve for the year 2019 of Woolworths is due to share-based payments expense and other

comprehensive income for the year 2019

Assessment of liabilities section of Wesfarmers and Woolworths

Liabilities section of Wesfarmers comprises current liabilities which consist trade and other

payables, Interest-bearing loans and borrowings, income tax payable, provisions, derivatives and

other current liabilities. Non - current liabilities consist interest-bearing loan and borrowings,

provisions, derivatives and other non-current liabilities. In case of Woolworths; current liabilities

comprise trade and other payables, borrowings, current tax payable, other financial liabilities and

provisions. It also consists liabilities associated with assets held for sale. Woolworth’s non-

current liabilities include borrowings, other financial liabilities, provision and other non-current

liabilities (Woolworths Annual Report, 2019). Current liabilities can be referred as short-term

financial obligations which are due within normal operating cycle. On the contrary non-current

liabilities are long term liabilities which are not required to be paid within twelve months.

Increase / Decrease in percentage

Reserves -1713% 81.05% 14.46%

Increase / Decrease in percentage

Total Equity -56% -4.96% 4.00%

Increase / Decrease in percentage

No major variation can be assessed in equity issued in case of Woolworths Ltd. However, in case

of Wesfarmers issued equity has been decreased to 29% in year 2019 in comparison to

outstanding balance in year 2018. The reason behind same is demerger capital distribution, i.e.

allocation of Coles distribution to share capital. Even the significant change in retained earnings

of Wesfarmers is due to distribution of equity dividends and transfer of loss on demerger i.e. $

2264 million. All above specified variants has affected total equity due to which reduction in

same has been accessed, i.e. equal to -56%. The reason behind significant increase of 39% in

reserve for the year 2019 of Woolworths is due to share-based payments expense and other

comprehensive income for the year 2019

Assessment of liabilities section of Wesfarmers and Woolworths

Liabilities section of Wesfarmers comprises current liabilities which consist trade and other

payables, Interest-bearing loans and borrowings, income tax payable, provisions, derivatives and

other current liabilities. Non - current liabilities consist interest-bearing loan and borrowings,

provisions, derivatives and other non-current liabilities. In case of Woolworths; current liabilities

comprise trade and other payables, borrowings, current tax payable, other financial liabilities and

provisions. It also consists liabilities associated with assets held for sale. Woolworth’s non-

current liabilities include borrowings, other financial liabilities, provision and other non-current

liabilities (Woolworths Annual Report, 2019). Current liabilities can be referred as short-term

financial obligations which are due within normal operating cycle. On the contrary non-current

liabilities are long term liabilities which are not required to be paid within twelve months.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

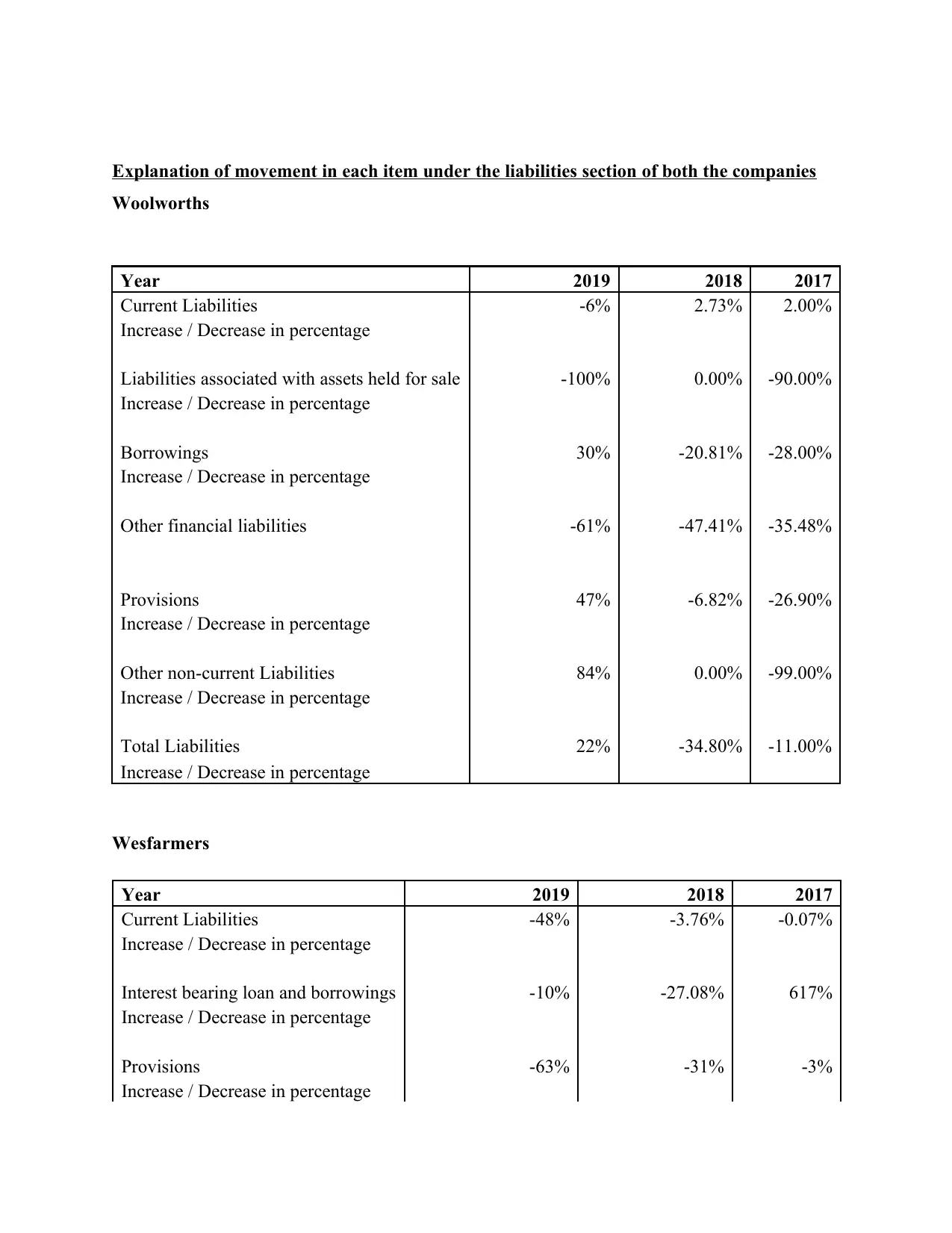

Explanation of movement in each item under the liabilities section of both the companies

Woolworths

Year 2019 2018 2017

Current Liabilities -6% 2.73% 2.00%

Increase / Decrease in percentage

Liabilities associated with assets held for sale -100% 0.00% -90.00%

Increase / Decrease in percentage

Borrowings 30% -20.81% -28.00%

Increase / Decrease in percentage

Other financial liabilities -61% -47.41% -35.48%

Provisions 47% -6.82% -26.90%

Increase / Decrease in percentage

Other non-current Liabilities 84% 0.00% -99.00%

Increase / Decrease in percentage

Total Liabilities 22% -34.80% -11.00%

Increase / Decrease in percentage

Wesfarmers

Year 2019 2018 2017

Current Liabilities -48% -3.76% -0.07%

Increase / Decrease in percentage

Interest bearing loan and borrowings -10% -27.08% 617%

Increase / Decrease in percentage

Provisions -63% -31% -3%

Increase / Decrease in percentage

Woolworths

Year 2019 2018 2017

Current Liabilities -6% 2.73% 2.00%

Increase / Decrease in percentage

Liabilities associated with assets held for sale -100% 0.00% -90.00%

Increase / Decrease in percentage

Borrowings 30% -20.81% -28.00%

Increase / Decrease in percentage

Other financial liabilities -61% -47.41% -35.48%

Provisions 47% -6.82% -26.90%

Increase / Decrease in percentage

Other non-current Liabilities 84% 0.00% -99.00%

Increase / Decrease in percentage

Total Liabilities 22% -34.80% -11.00%

Increase / Decrease in percentage

Wesfarmers

Year 2019 2018 2017

Current Liabilities -48% -3.76% -0.07%

Increase / Decrease in percentage

Interest bearing loan and borrowings -10% -27.08% 617%

Increase / Decrease in percentage

Provisions -63% -31% -3%

Increase / Decrease in percentage

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Derivatives NA -100% -70.37%

Increase / Decrease in percentage

Others -42% 0.00% 50%

Increase / Decrease in percentage

Total Liabilities -41% -12.33% -9%

Increase / Decrease in percentage

A significant change can be accessed in assets held for sale in case of Woolworths Company.

The reason behind the same is that in year 2019, sale of home timber and hardware which were

previously recognized as assets held for sale was completed during the period. The reason behind

vital increase in other-noncurrent liabilities of Woolworths is recognition of Lowe’s put option

liability of $205.8 million followed by acquisition of Lowe’s one-third share of home

improvement. A major change in interest-bearing liabilities in case of Wesfarmers in year 2017

was due to borrowing funds as interest-bearing liabilities. It would be appropriate of state that

liabilities of Woolworths have increased with significant change in comparison to Wesfarmers.

Advantages and disadvantages of each source of funds used by each company

Both the companies are making use of debt and equity source for funding of operational

activities. Description of Relative advantages or disadvantages of each source of fund selected by

Wesfarmers and Woolworths is enumerated as below:

Equity source of finance

Preference capital, equity capital and retained earnings are represented by equity source of

finance (Schwienbacher, Baker, and Welter, 2015). Perpetual life is possessed by equity shares,

and fund provider is allowed to the firm’s residual income.

Advantages

Credit problems: In a situation of less profit, equity sources of finance might be the only

option for funding of operational activities. This is because in such situation if debt is taken

then finance cost may be too high and steep for making a financial decision.

Increase / Decrease in percentage

Others -42% 0.00% 50%

Increase / Decrease in percentage

Total Liabilities -41% -12.33% -9%

Increase / Decrease in percentage

A significant change can be accessed in assets held for sale in case of Woolworths Company.

The reason behind the same is that in year 2019, sale of home timber and hardware which were

previously recognized as assets held for sale was completed during the period. The reason behind

vital increase in other-noncurrent liabilities of Woolworths is recognition of Lowe’s put option

liability of $205.8 million followed by acquisition of Lowe’s one-third share of home

improvement. A major change in interest-bearing liabilities in case of Wesfarmers in year 2017

was due to borrowing funds as interest-bearing liabilities. It would be appropriate of state that

liabilities of Woolworths have increased with significant change in comparison to Wesfarmers.

Advantages and disadvantages of each source of funds used by each company

Both the companies are making use of debt and equity source for funding of operational

activities. Description of Relative advantages or disadvantages of each source of fund selected by

Wesfarmers and Woolworths is enumerated as below:

Equity source of finance

Preference capital, equity capital and retained earnings are represented by equity source of

finance (Schwienbacher, Baker, and Welter, 2015). Perpetual life is possessed by equity shares,

and fund provider is allowed to the firm’s residual income.

Advantages

Credit problems: In a situation of less profit, equity sources of finance might be the only

option for funding of operational activities. This is because in such situation if debt is taken

then finance cost may be too high and steep for making a financial decision.

Cash flow: Equity financing generally does not take out finance out of business, however

debt loan repayment takes the financial out of the cash flow of company, thereby decreasing

the money required to fund growth (Amess, Stiebale and Wright, 2016).

Long-term planning: It is not expected by equity investors to gain an instant return over

their investment. Similarly, they have a long-run opinion and experience the changes in

money loss is there is failure in business.

Disadvantages

Loss of Control: Equity shareholders can have full control over the business affairs, as

they take benefit of the voting rights.

Cost: It has been expected by equity investors to hold a return on their money. Further,

the owner of the business should be keen to share certain corporate proceeds with their

equity partners. The payable money to the partner can be more than the rate of interest on

debt financing.

Potential for Conflict: Each and every partner are not always agreeable to the made

decisions (Buerger, Mladenow, and Strauss, 2017). Further, the conflicts keep on arising

from distinct company’s visions and thereby results in disagreements on management

structures, so the owner should address the differences of opinions.

Debt source of finance

Borrowings may be for short term, medium-term and long term as per the requirement of the

borrower. Long terms finances are provided by the banks and financial institutions in the form of

loans. Further, Debentures and mortgage loan are long term loans made to the business. Another

example of long term finance is leasing or hire purchase, which is used for the credit purchase of

equipment in which payments are paid on a monthly basis. (Carbo‐Valverde, Rodriguez‐

Fernandez, and Udell, 2016).

Advantages

Control: taking out a loan is considered as a short-term process; the relationship comes to

an end when there is repayment of debt. Further, the lender does not have control over

business operations.

debt loan repayment takes the financial out of the cash flow of company, thereby decreasing

the money required to fund growth (Amess, Stiebale and Wright, 2016).

Long-term planning: It is not expected by equity investors to gain an instant return over

their investment. Similarly, they have a long-run opinion and experience the changes in

money loss is there is failure in business.

Disadvantages

Loss of Control: Equity shareholders can have full control over the business affairs, as

they take benefit of the voting rights.

Cost: It has been expected by equity investors to hold a return on their money. Further,

the owner of the business should be keen to share certain corporate proceeds with their

equity partners. The payable money to the partner can be more than the rate of interest on

debt financing.

Potential for Conflict: Each and every partner are not always agreeable to the made

decisions (Buerger, Mladenow, and Strauss, 2017). Further, the conflicts keep on arising

from distinct company’s visions and thereby results in disagreements on management

structures, so the owner should address the differences of opinions.

Debt source of finance

Borrowings may be for short term, medium-term and long term as per the requirement of the

borrower. Long terms finances are provided by the banks and financial institutions in the form of

loans. Further, Debentures and mortgage loan are long term loans made to the business. Another

example of long term finance is leasing or hire purchase, which is used for the credit purchase of

equipment in which payments are paid on a monthly basis. (Carbo‐Valverde, Rodriguez‐

Fernandez, and Udell, 2016).

Advantages

Control: taking out a loan is considered as a short-term process; the relationship comes to

an end when there is repayment of debt. Further, the lender does not have control over

business operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxes: There is tax deductibility in loan interest; on the other hand, it is not present in

dividends to be paid to shareholders (Boubaker, Rouatbi, and Saffar, 2017).

Predictability: There is an advance stating in principal as well as interest payments;

therefore, it is easy to work these into the cash flow of company.

Disadvantages

Qualification: An acceptable credit rating is required from the company for effective

qualification.

Fixed payments: By nature, they are contractual. Therefore, borrowing sources are

restricted to obtain a fixed interest rate, regardless of profit which is needed to be repaid on

a fixed date.

Cash flow: Considering a higher amount of debt makes drags the business into problems in

order to meet the loan payments if there is declination in cash flows. However, the investors

will also believe that company is at higher risk and is unwilling to make further equity

investments (Abor, 2017).

Collateral: Lends will classically call out for some company assets are that are held as

collateral, and the business owner is generally required to ensure the loan individually.

PART B

Examination of the concept of different entities, their implication of classifications and

their reporting and compliance requirements is enumerated as below:

Large proprietary company

From financial year beginning on or after the 1 July 2019, it can be stated that a proprietary

corporation is described as large for a financial year, in a situation where it meets at least two of

the provided criteria:

Company’s or any other business enterprise’s consolidates revenues meant for financial

year it supervises $50 million or higher than that.

The consolidates gross assets value at the financial year-end of the corporation and any

other business enterprise it supervises $25 million or higher than that

dividends to be paid to shareholders (Boubaker, Rouatbi, and Saffar, 2017).

Predictability: There is an advance stating in principal as well as interest payments;

therefore, it is easy to work these into the cash flow of company.

Disadvantages

Qualification: An acceptable credit rating is required from the company for effective

qualification.

Fixed payments: By nature, they are contractual. Therefore, borrowing sources are

restricted to obtain a fixed interest rate, regardless of profit which is needed to be repaid on

a fixed date.

Cash flow: Considering a higher amount of debt makes drags the business into problems in

order to meet the loan payments if there is declination in cash flows. However, the investors

will also believe that company is at higher risk and is unwilling to make further equity

investments (Abor, 2017).

Collateral: Lends will classically call out for some company assets are that are held as

collateral, and the business owner is generally required to ensure the loan individually.

PART B

Examination of the concept of different entities, their implication of classifications and

their reporting and compliance requirements is enumerated as below:

Large proprietary company

From financial year beginning on or after the 1 July 2019, it can be stated that a proprietary

corporation is described as large for a financial year, in a situation where it meets at least two of

the provided criteria:

Company’s or any other business enterprise’s consolidates revenues meant for financial

year it supervises $50 million or higher than that.

The consolidates gross assets value at the financial year-end of the corporation and any

other business enterprise it supervises $25 million or higher than that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The corporation and any other business enterprise it supervises have over 100 employees

at the financial year-end.

Further, the large proprietary companies are required to do the preparation and lodging of a

financial report and the report of direct for every financial year (Australian Securities &

Investments Commissions, 2014). In addition, the accounts should be audit until the time grants

have been relieved by ASIC.

Small proprietary company

A small proprietary company for a financial year is when if it meets at least two of the below-

provided paragraphs:

The consolidated gross operating revenue meant for the financial statement of the

company’s or any other entity in oversees is not more than $10 million

The consolidated gross assets valued at the financial year-end of the company and its

entities it supervises is not more than $5 million

The company and its related entities it supervises have less than 50 employees at the

financial year-end.

Moreover, a Small Proprietary Company does not possess financial accounts and obligations

related to reporting, apart from as given in sec. 292(2), i.e. it is intended to do the same as per the

sec. 293 (shareholder direction) or sec. 294 (ASIC direction), or 2. Furthermore, it is supervised

by a foreign corporation that is a company’s subsidiary registered in a jurisdiction external of

Australia and has not been gone through consolidation lodged with ASIC by a foreign company

that is registered (Company Secretarial Services, 2019).

Therefore, each company is required to hold financial records for at least 7 years. It is vital that

business prepare their accounts on a daily basis so that the directors of the company are totally

realized of their financial trading and performance, if or if not there are due funding needs etc.

Along with this it will call for financial information for several other rationales like tax return

preparation and offering reports to lenders.

Reporting entity

A reporting entity is an entity where the users generally and reasonably depend on the general-

purpose financial report (GPFR) to fetch an understanding of the financial position and the

at the financial year-end.

Further, the large proprietary companies are required to do the preparation and lodging of a

financial report and the report of direct for every financial year (Australian Securities &

Investments Commissions, 2014). In addition, the accounts should be audit until the time grants

have been relieved by ASIC.

Small proprietary company

A small proprietary company for a financial year is when if it meets at least two of the below-

provided paragraphs:

The consolidated gross operating revenue meant for the financial statement of the

company’s or any other entity in oversees is not more than $10 million

The consolidated gross assets valued at the financial year-end of the company and its

entities it supervises is not more than $5 million

The company and its related entities it supervises have less than 50 employees at the

financial year-end.

Moreover, a Small Proprietary Company does not possess financial accounts and obligations

related to reporting, apart from as given in sec. 292(2), i.e. it is intended to do the same as per the

sec. 293 (shareholder direction) or sec. 294 (ASIC direction), or 2. Furthermore, it is supervised

by a foreign corporation that is a company’s subsidiary registered in a jurisdiction external of

Australia and has not been gone through consolidation lodged with ASIC by a foreign company

that is registered (Company Secretarial Services, 2019).

Therefore, each company is required to hold financial records for at least 7 years. It is vital that

business prepare their accounts on a daily basis so that the directors of the company are totally

realized of their financial trading and performance, if or if not there are due funding needs etc.

Along with this it will call for financial information for several other rationales like tax return

preparation and offering reports to lenders.

Reporting entity

A reporting entity is an entity where the users generally and reasonably depend on the general-

purpose financial report (GPFR) to fetch an understanding of the financial position and the

performing ability on an entity, eventually making decisions based on this available financial

information and data’s obtained by the financial report. Hence, to be defined as a reporting entity

for a particular entity, one requires preparing a GPFR. It means that all the Australian

Accounting Standards have to be applied before preparing the financial report. For reporting an

entity in Australia one needs to connect with the Australian Securities and Investments

Commission (ASIC). There are various regulatory guidelines that the entity needs to abide by.

The definition of the reporting entity registered has to be correct. For any wrong information the

Australian Securities and Investments Commission (ASIC) investigates, followed by a charge

with governance for tempering the financial report. Therefore, the reporting entity will end up

with breaching the reporting requirements of the corporations Act 2001 and the Australian

Accounting Standards. Entities classified as reporting entities are prima facie, needing to

generate complete financial reports that are based on GAAP, under the concerned statutory time

intervals and are required to be accessible to all users (PKF, 2017). Australian based company

must consider the preparation and lodging of financial reports with the help of ASIC, generally at

financial year-end. In addition to this, annual financial reports are mandatory to be audited. In

some scenarios, companies might get exempted from the financial reporting; thus Australian

reporting entities might be needed to report to ATO, ASIC and ASX.

CONCLUSION

It can be concluded that appropriate investment decision can be taken through the application of

corporate finance accounting strategies. After assessing financial statement of Wesfarmers and

Woolworth it can be stated that fluctuating trend does exist in liabilities of Woolworths. Further,

it would be appropriate for both the companies to reconstruct their capital structure after

assessing advantages and disadvantages of source of funds. Lastly, it could be stated that it is

necessary for reporting entity to comply with the requirements of GPFR while drafting financial

statements and auditing for entities subjected to Corporations Act.

information and data’s obtained by the financial report. Hence, to be defined as a reporting entity

for a particular entity, one requires preparing a GPFR. It means that all the Australian

Accounting Standards have to be applied before preparing the financial report. For reporting an

entity in Australia one needs to connect with the Australian Securities and Investments

Commission (ASIC). There are various regulatory guidelines that the entity needs to abide by.

The definition of the reporting entity registered has to be correct. For any wrong information the

Australian Securities and Investments Commission (ASIC) investigates, followed by a charge

with governance for tempering the financial report. Therefore, the reporting entity will end up

with breaching the reporting requirements of the corporations Act 2001 and the Australian

Accounting Standards. Entities classified as reporting entities are prima facie, needing to

generate complete financial reports that are based on GAAP, under the concerned statutory time

intervals and are required to be accessible to all users (PKF, 2017). Australian based company

must consider the preparation and lodging of financial reports with the help of ASIC, generally at

financial year-end. In addition to this, annual financial reports are mandatory to be audited. In

some scenarios, companies might get exempted from the financial reporting; thus Australian

reporting entities might be needed to report to ATO, ASIC and ASX.

CONCLUSION

It can be concluded that appropriate investment decision can be taken through the application of

corporate finance accounting strategies. After assessing financial statement of Wesfarmers and

Woolworth it can be stated that fluctuating trend does exist in liabilities of Woolworths. Further,

it would be appropriate for both the companies to reconstruct their capital structure after

assessing advantages and disadvantages of source of funds. Lastly, it could be stated that it is

necessary for reporting entity to comply with the requirements of GPFR while drafting financial

statements and auditing for entities subjected to Corporations Act.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.