Corporate Finance Assignment: CWC Project Evaluation and Analysis

VerifiedAdded on 2021/04/21

|9

|1061

|26

Homework Assignment

AI Summary

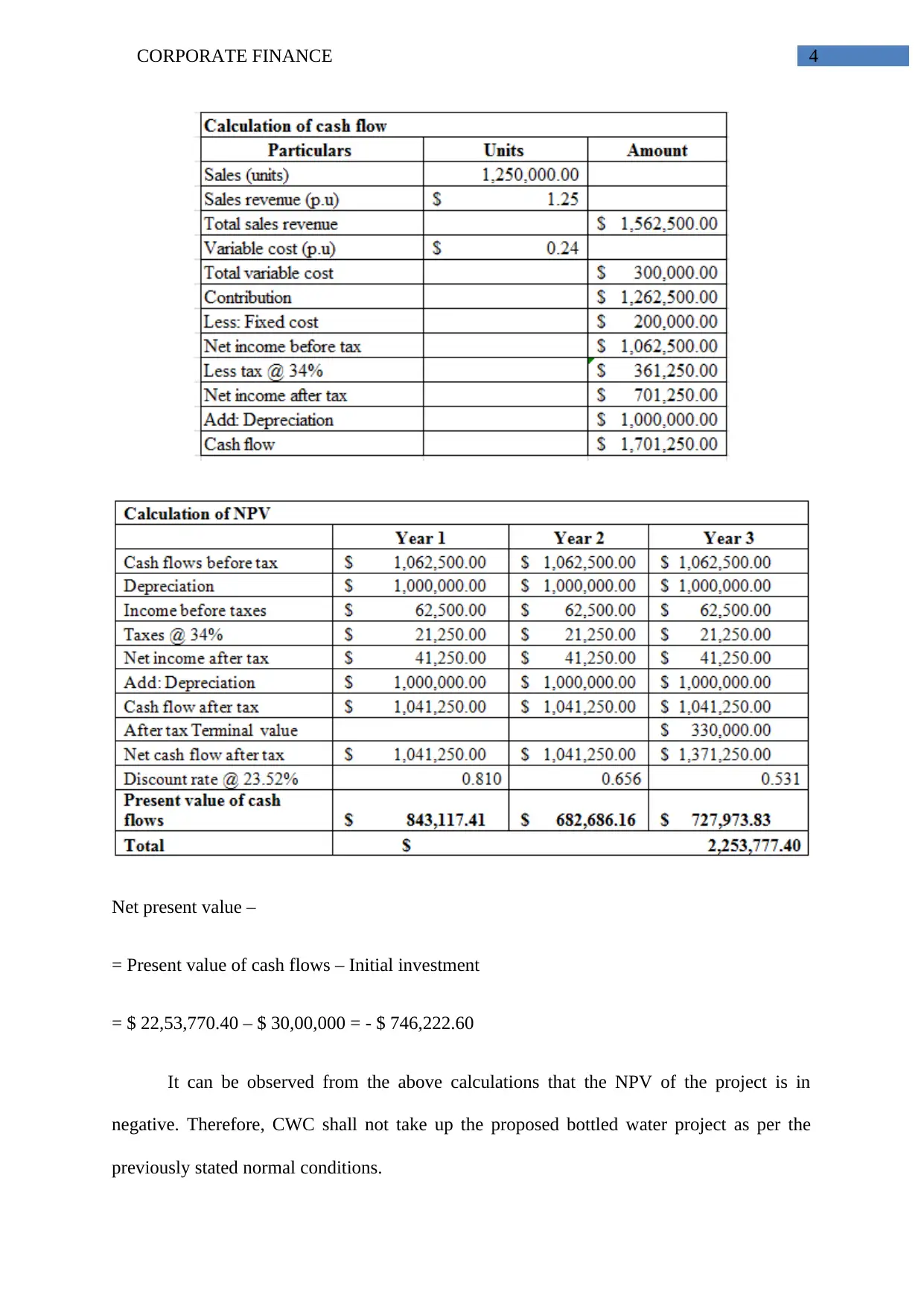

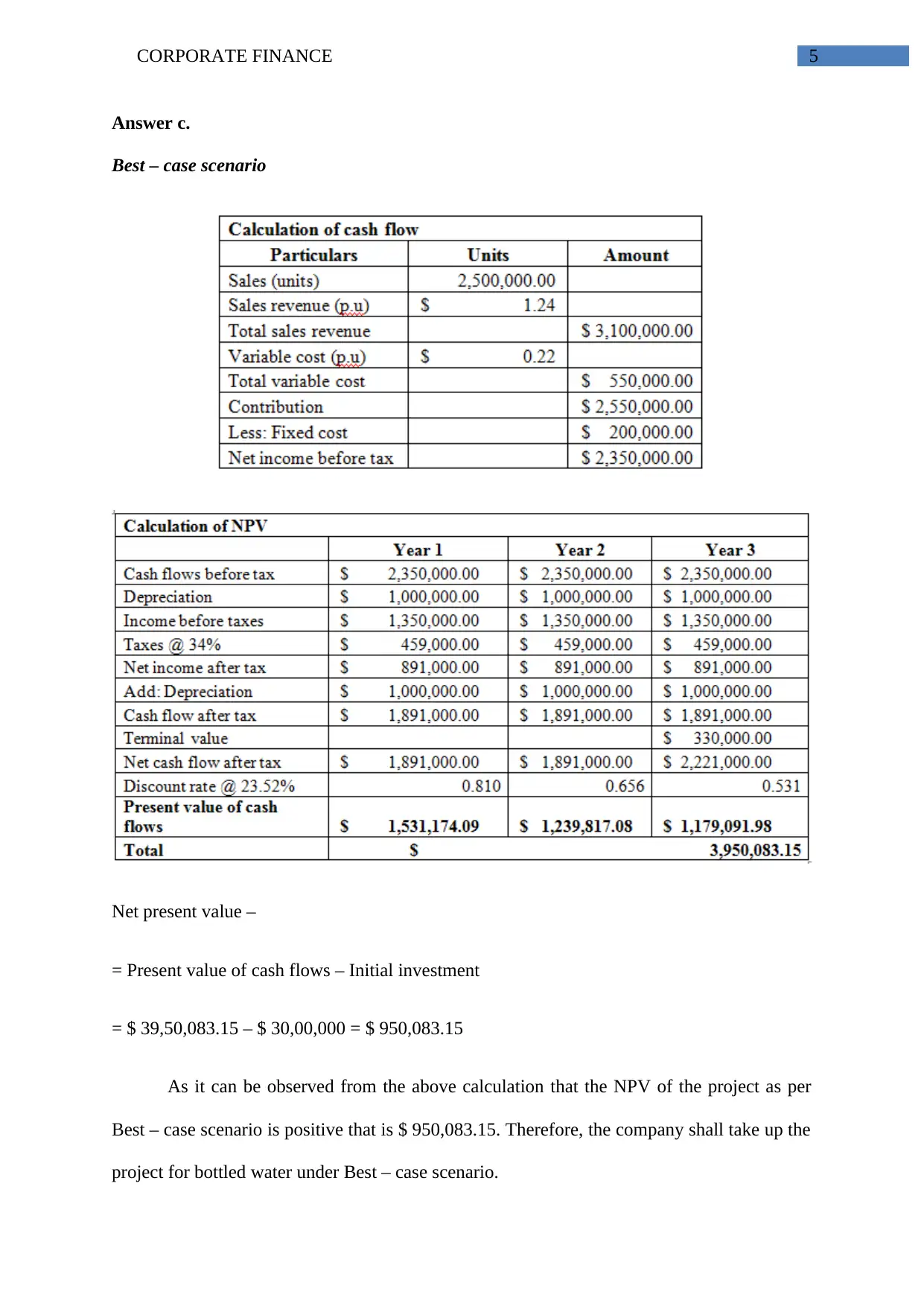

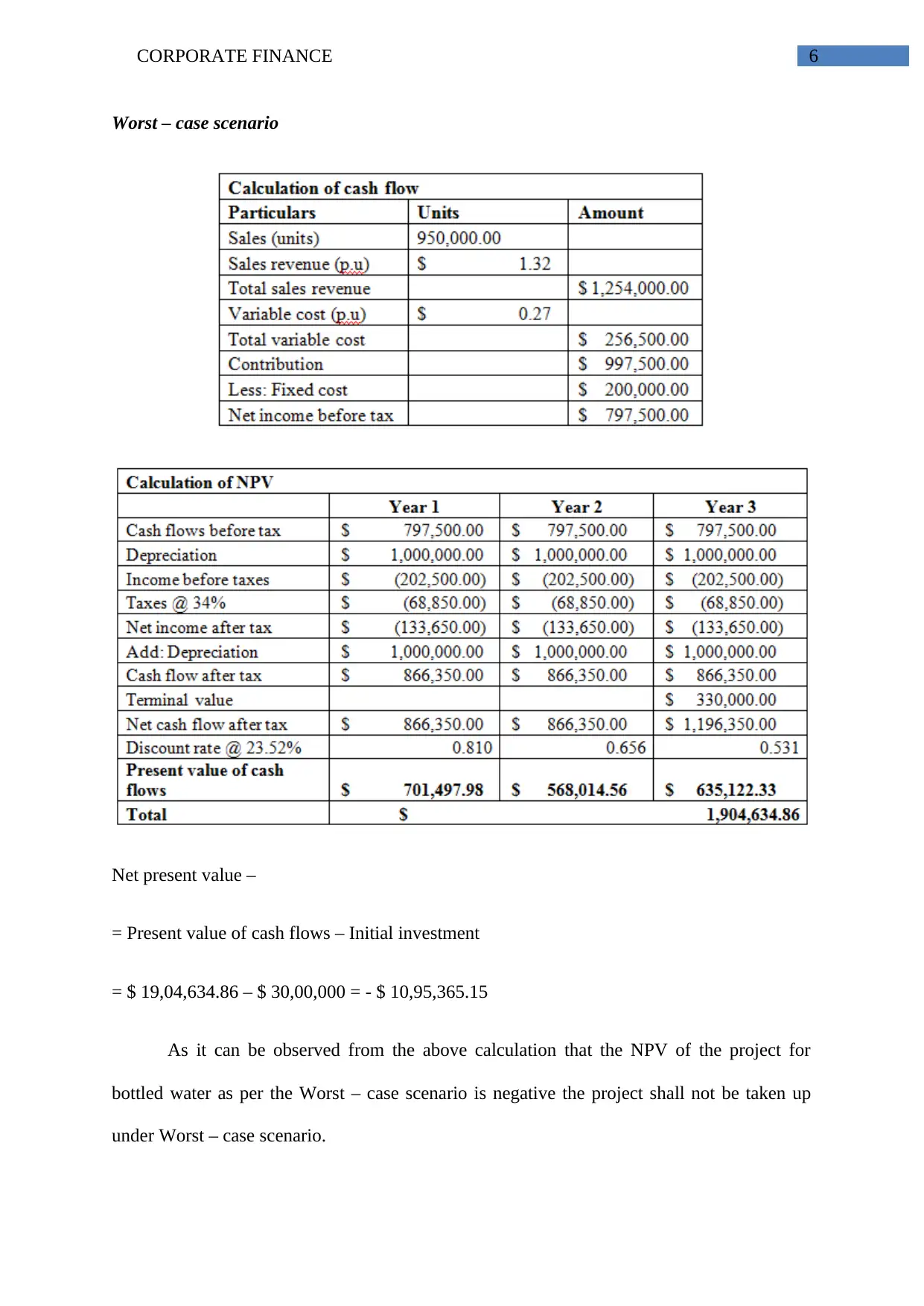

This assignment analyzes a corporate finance problem for CWC, evaluating a potential bottled water project. It begins with calculating the value of shares and determining the Weighted Average Cost of Capital (WACC) using the cost of equity and the cost of bonds. The solution then assesses the project's feasibility by calculating depreciation and Net Present Value (NPV) under different scenarios (current, best-case, and worst-case), concluding that the project is only acceptable under the best-case scenario. The document also discusses the importance of NPV as a tool for financial analysts, emphasizing the consideration of the time value of money and the need for analysts to gather information from management regarding their preferences before making recommendations. Finally, the assignment references several sources that support the calculations and conclusions.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.