BAP53 Corporate Finance Project Report: Bega Cheese Analysis

VerifiedAdded on 2023/06/09

|8

|1702

|495

Project

AI Summary

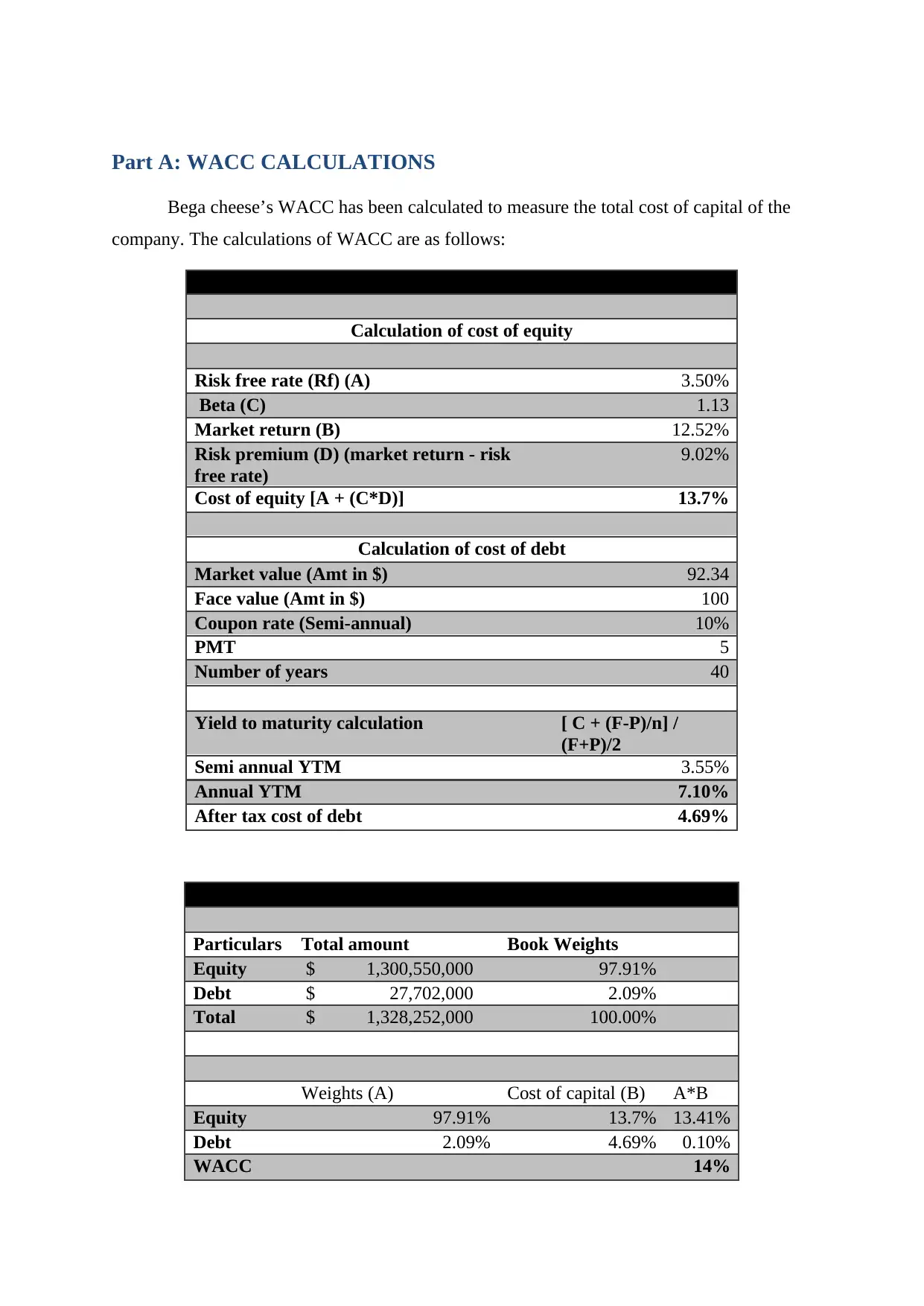

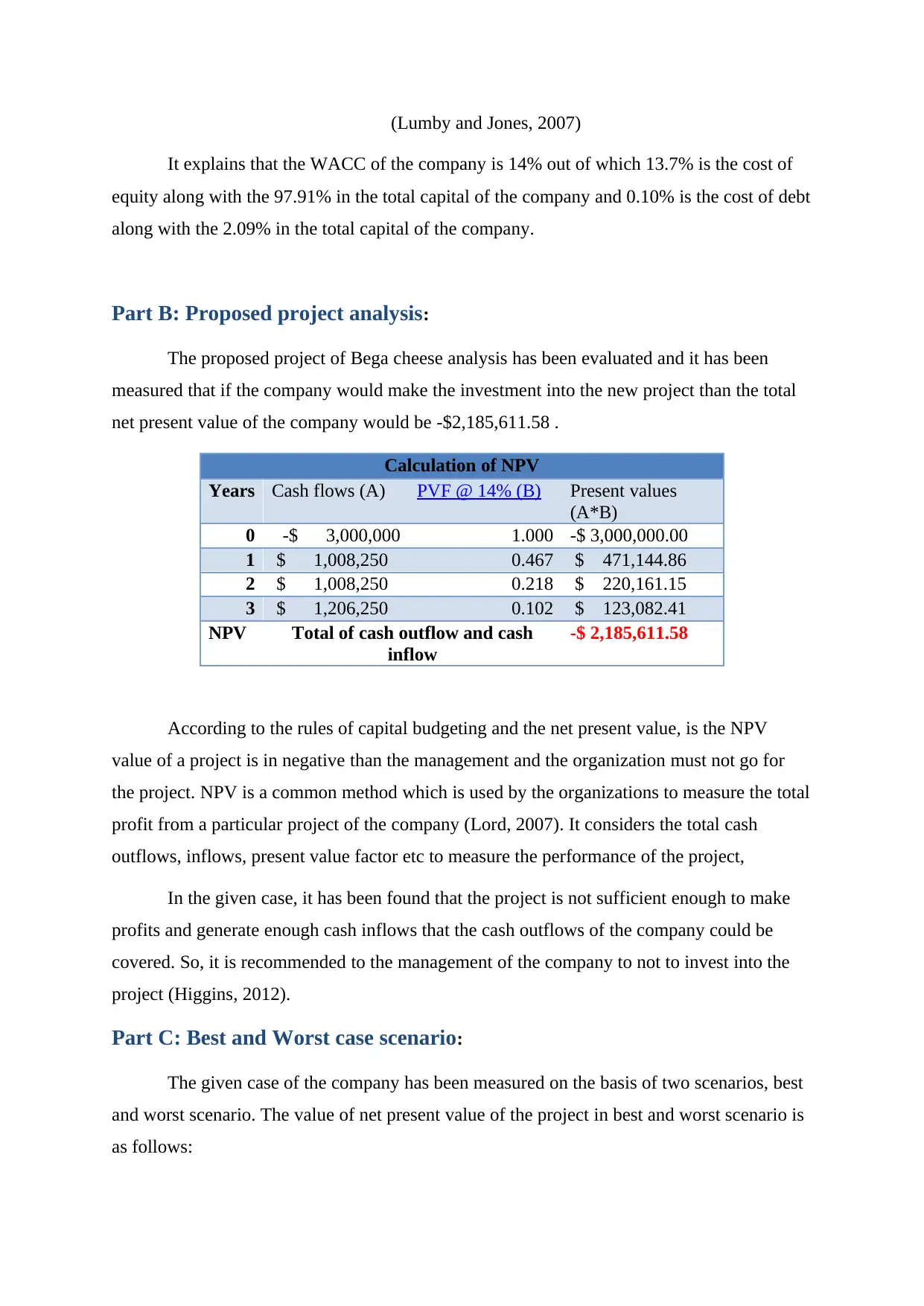

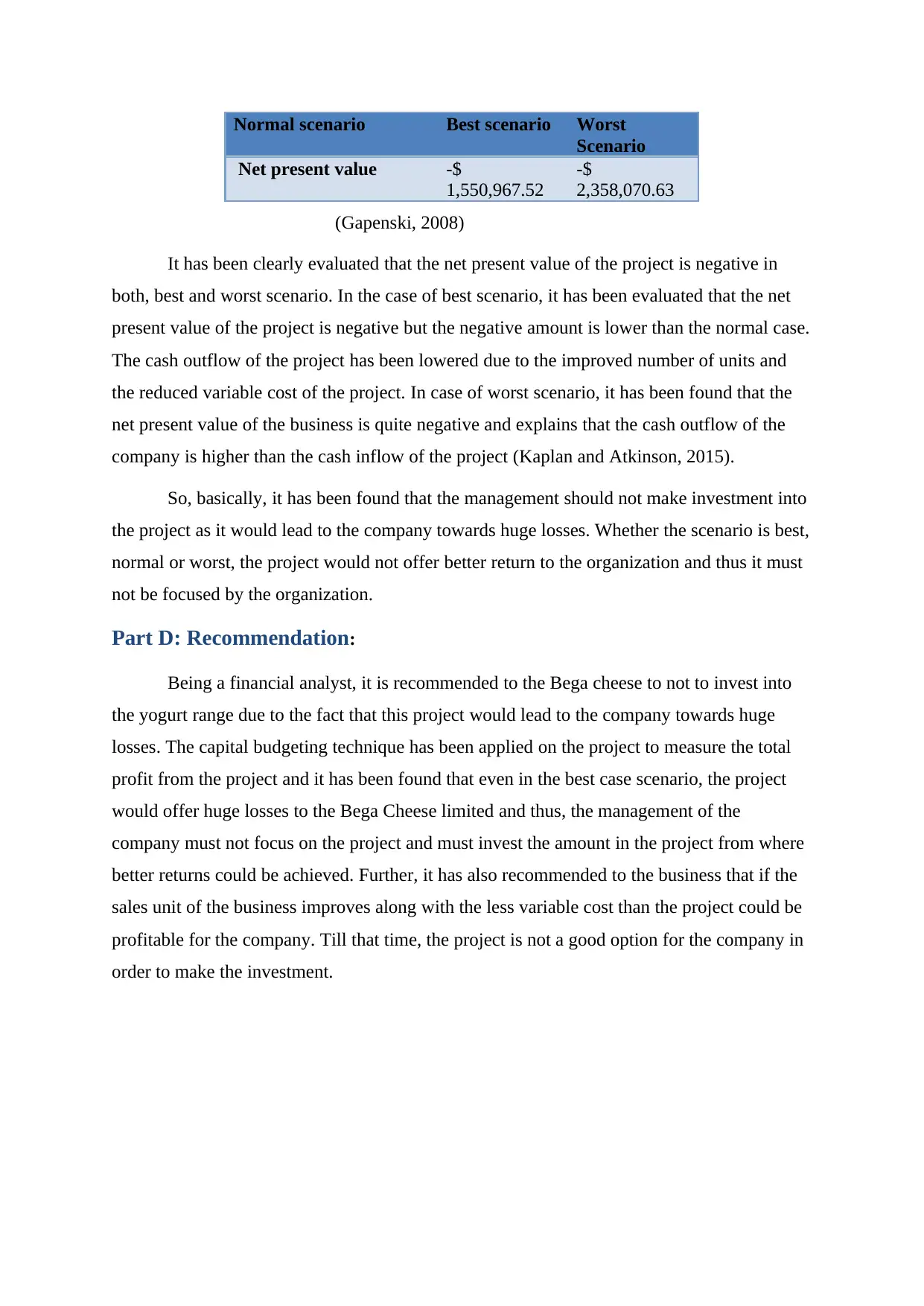

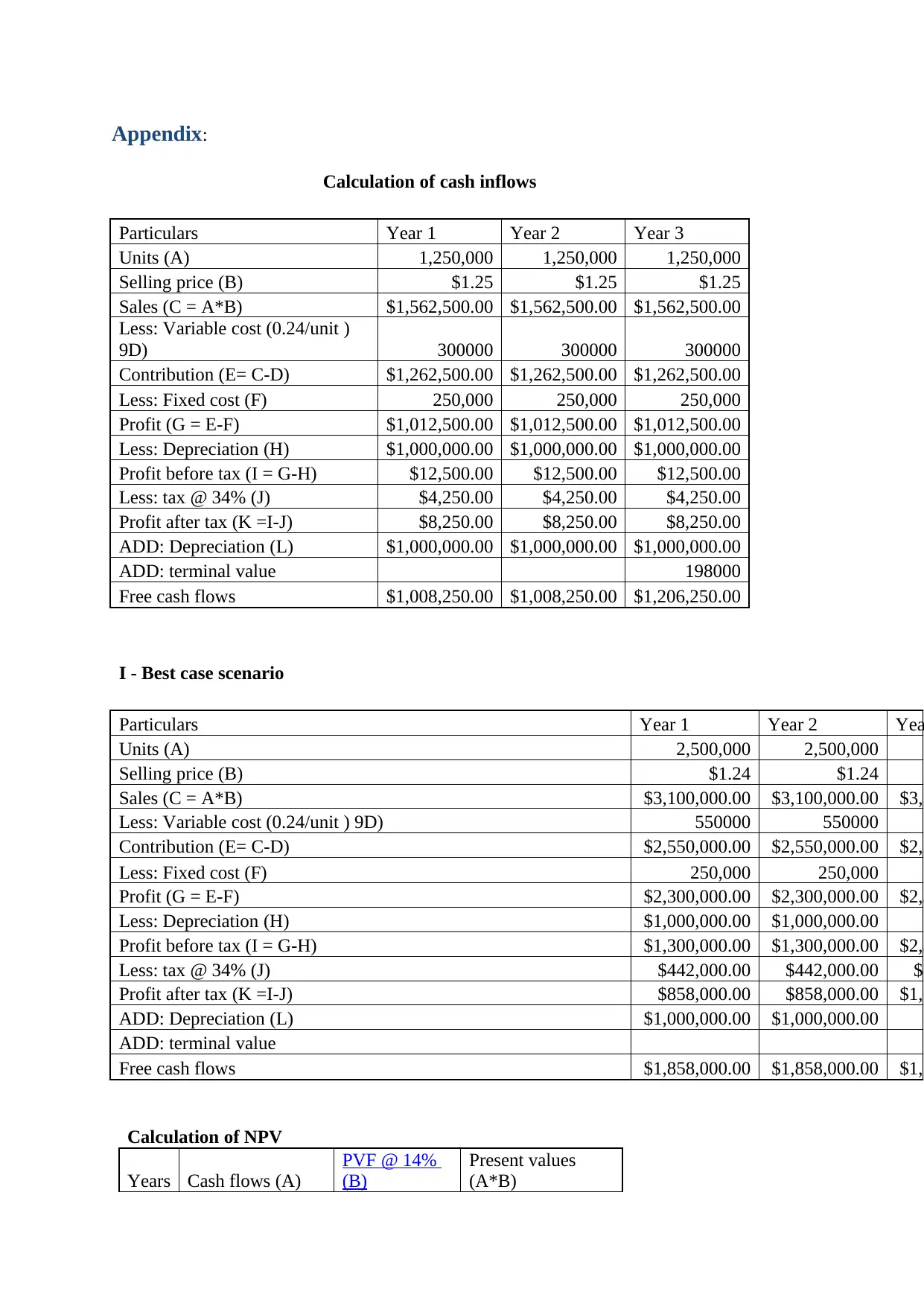

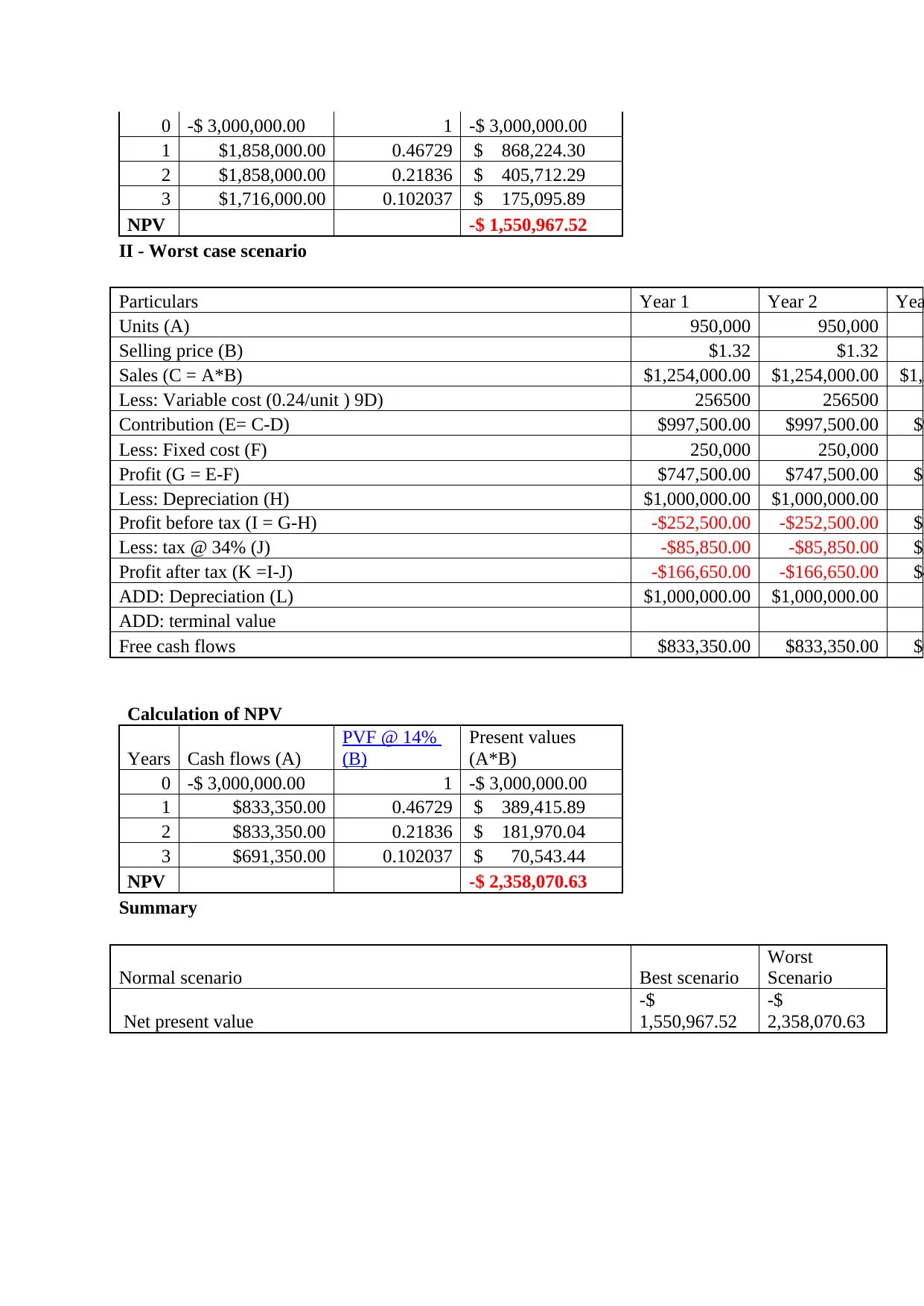

This project report provides a comprehensive financial analysis of Bega Cheese's proposed project, focusing on the yogurt range. The report begins with the calculation of the company's Weighted Average Cost of Capital (WACC), which is determined to be 14%, with 13.7% being the cost of equity and 0.10% being the cost of debt. The analysis then proceeds to evaluate the project's Net Present Value (NPV), revealing a negative NPV of -$2,185,611.58, indicating that the project is not financially viable. The report further examines the best and worst-case scenarios, both of which also yield negative NPVs, solidifying the recommendation against the investment. The financial analyst recommends that Bega Cheese should not invest in the yogurt range because the project would lead to significant losses. The report includes detailed calculations of cash inflows, along with the NPV calculations for all scenarios. The report recommends against investing in the project, as the financial analysis indicates that it is not likely to generate sufficient returns. The project's failure to generate positive returns is consistent across different scenarios and is not recommended for investment.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.