Corporate Finance: A Detailed Report on Capital Budgeting Techniques

VerifiedAdded on 2019/10/31

|12

|2750

|290

Report

AI Summary

This report provides a detailed overview of capital budgeting techniques used in corporate finance. It begins with an introduction to capital budgeting and its importance in organizational management, highlighting its role in evaluating long-term risks and reducing operational costs. The report then delves into specific techniques, including sensitivity analysis, which assesses the impact of crucial variables on net profits; break-even analysis, used to determine the point at which profits equal costs; scenario analysis, a strategic tool for analyzing decisions under various potential outcomes; and simulation techniques, which utilize numerical data to model the standard outcome of scenario analysis. Each technique is explained with its advantages and limitations, providing managers with a comprehensive understanding to aid in decision-making for new ventures and project evaluations. The report concludes by emphasizing the importance of these tools in reducing risks and reevaluating investment decisions, offering a platform for informed strategic planning.

CORPORATE FINANCE

BACHELOR OF ACCOUNTING

INSTITUTIONAL AFFILIATION(S)

STUDENT NAME

[Pick the date]

BACHELOR OF ACCOUNTING

INSTITUTIONAL AFFILIATION(S)

STUDENT NAME

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

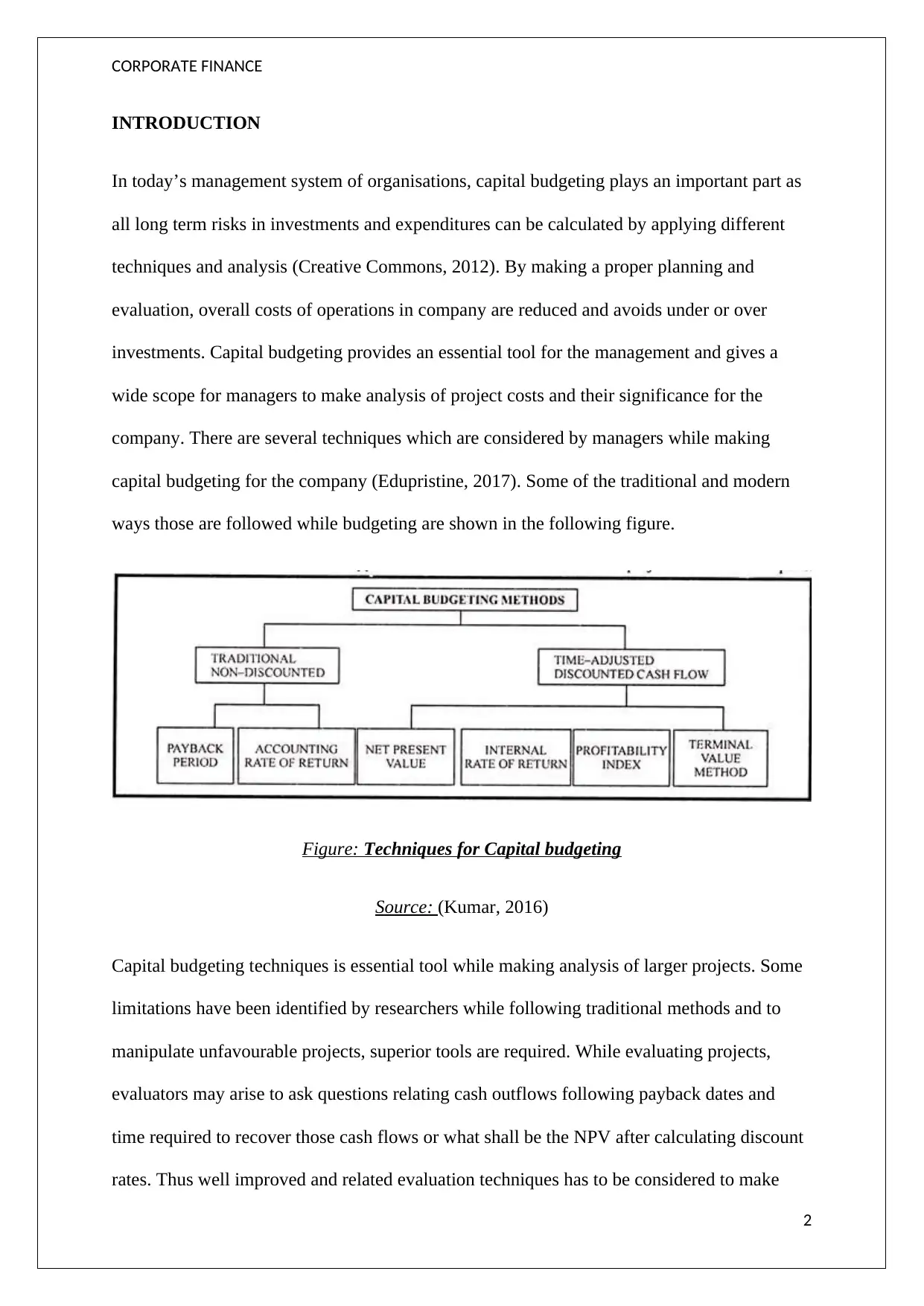

INTRODUCTION

In today’s management system of organisations, capital budgeting plays an important part as

all long term risks in investments and expenditures can be calculated by applying different

techniques and analysis (Creative Commons, 2012). By making a proper planning and

evaluation, overall costs of operations in company are reduced and avoids under or over

investments. Capital budgeting provides an essential tool for the management and gives a

wide scope for managers to make analysis of project costs and their significance for the

company. There are several techniques which are considered by managers while making

capital budgeting for the company (Edupristine, 2017). Some of the traditional and modern

ways those are followed while budgeting are shown in the following figure.

Figure: Techniques for Capital budgeting

Source: (Kumar, 2016)

Capital budgeting techniques is essential tool while making analysis of larger projects. Some

limitations have been identified by researchers while following traditional methods and to

manipulate unfavourable projects, superior tools are required. While evaluating projects,

evaluators may arise to ask questions relating cash outflows following payback dates and

time required to recover those cash flows or what shall be the NPV after calculating discount

rates. Thus well improved and related evaluation techniques has to be considered to make

2

INTRODUCTION

In today’s management system of organisations, capital budgeting plays an important part as

all long term risks in investments and expenditures can be calculated by applying different

techniques and analysis (Creative Commons, 2012). By making a proper planning and

evaluation, overall costs of operations in company are reduced and avoids under or over

investments. Capital budgeting provides an essential tool for the management and gives a

wide scope for managers to make analysis of project costs and their significance for the

company. There are several techniques which are considered by managers while making

capital budgeting for the company (Edupristine, 2017). Some of the traditional and modern

ways those are followed while budgeting are shown in the following figure.

Figure: Techniques for Capital budgeting

Source: (Kumar, 2016)

Capital budgeting techniques is essential tool while making analysis of larger projects. Some

limitations have been identified by researchers while following traditional methods and to

manipulate unfavourable projects, superior tools are required. While evaluating projects,

evaluators may arise to ask questions relating cash outflows following payback dates and

time required to recover those cash flows or what shall be the NPV after calculating discount

rates. Thus well improved and related evaluation techniques has to be considered to make

2

CORPORATE FINANCE

appropriate assumptions like Sensitivity analysis, scenario analysis, simulation techniques

and break-down analysis. These are few modern techniques which are used by the financial

management of today’s business and to understand these tools, a detailed research have been

made in this paper to provide assistance to managers while preparing capital budgets for the

company (Lawrence, n.d.).

SENSITIVITY ANALYSIS

Sensitivity analysis is one of the management tools that are used to analyse organisations

scenarios to evaluate crucial and non crucial variables on the net profits of the company.

Sensitivity analysis is also used by management while decision making to ascertain possible

relationship between components of proposed venture’s involvement in profitability, liquidity

and working capital of the company. To determine the receptiveness of net present value

(NPV) to variables those are utilised for calculating it is the main task of sensitivity analysis

along with measuring risks. This is due to the process of evaluating investment prospects

using NPV is supported by assumptions based on forecasting, therefore making it tentative.

Sensitivity analysis can also measure the changes in variables and assumptions that can bear

force on bottom lining of cash flow and profiteering of venture. Managers can have an idea

about venture’s success for the business while evaluating the assurance of resources for new

project. Some professionals also assumes sensitivity analysis as risk assessment tool and

claims that since this method is based on assumptions, ambiguity into investments is probable

while incorporating this tool in decision making (Pannel, 2017).

Sensitivity analysis carries simple features and uncomplicated theory unlike other accounting

theories where there is a need for detailed study. This theory identifies crucial areas while

attaining organisational goals as stated in vision of the company statement and thus helps

managements in concentrating while discharging duties to the employees. It also helps in

3

appropriate assumptions like Sensitivity analysis, scenario analysis, simulation techniques

and break-down analysis. These are few modern techniques which are used by the financial

management of today’s business and to understand these tools, a detailed research have been

made in this paper to provide assistance to managers while preparing capital budgets for the

company (Lawrence, n.d.).

SENSITIVITY ANALYSIS

Sensitivity analysis is one of the management tools that are used to analyse organisations

scenarios to evaluate crucial and non crucial variables on the net profits of the company.

Sensitivity analysis is also used by management while decision making to ascertain possible

relationship between components of proposed venture’s involvement in profitability, liquidity

and working capital of the company. To determine the receptiveness of net present value

(NPV) to variables those are utilised for calculating it is the main task of sensitivity analysis

along with measuring risks. This is due to the process of evaluating investment prospects

using NPV is supported by assumptions based on forecasting, therefore making it tentative.

Sensitivity analysis can also measure the changes in variables and assumptions that can bear

force on bottom lining of cash flow and profiteering of venture. Managers can have an idea

about venture’s success for the business while evaluating the assurance of resources for new

project. Some professionals also assumes sensitivity analysis as risk assessment tool and

claims that since this method is based on assumptions, ambiguity into investments is probable

while incorporating this tool in decision making (Pannel, 2017).

Sensitivity analysis carries simple features and uncomplicated theory unlike other accounting

theories where there is a need for detailed study. This theory identifies crucial areas while

attaining organisational goals as stated in vision of the company statement and thus helps

managements in concentrating while discharging duties to the employees. It also helps in

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

identifying susceptible areas which can be directly scrutinized. The data processed while

making analysis can enable professional judgement while allocating managerial

responsibilities. Sensitivity analysis software’s that are available in the market can perform

calculations in simpler and fast manner by putting in the variables and getting results that can

help in making quick decisions. Thus by evaluating future results, the management can give

attention in implementing eminence control to determine the success in their investment on

ventures. The weakness sensitivity analysis contains is that it is not fundamental in nature as

it judges only changes made in variables. Taking into account the possibility of changes in

variables are not made in analysis. Thus sensitivity analysis alone cannot judge and make

final decisions in budgeting and provides only the information’s that can be interpreted in

further analysis (Chinweike, 2013).

BREAK-EVEN ANALYSIS

Break-Even analysis is one another important tool used by managers to evaluate economic

viability of new venture. The point in which profits are equal to costs is called the breakeven

point and at that time no profit or loss is assumed. It can also be interpreted in sales i.e. break

even sales unit required to cover overall costs. Sales which are found below cost levels are

resulted losses and sales above cost levels are deemed profits made by company. Not always

breakeven point is determined in producing products to cross sales level but sometimes

certain profit returns are desired in investments. If it is not realised then selling substantial

amount of products may result in assuming loss for the company (Holland, 1998). Thus

breakeven can prove an effective tool in making decisions regarding quantity of goods to be

produced in new venture to gain revenue. Fixed costs and variable costs are utilised in

making break-even analysis in which fixed costs are those overhead costs those are invariable

and does not change even if there is a change in output level. Variable costs are opposite in

nature and changes with level of outputs and are inconstant and frequently settled on per unit

4

identifying susceptible areas which can be directly scrutinized. The data processed while

making analysis can enable professional judgement while allocating managerial

responsibilities. Sensitivity analysis software’s that are available in the market can perform

calculations in simpler and fast manner by putting in the variables and getting results that can

help in making quick decisions. Thus by evaluating future results, the management can give

attention in implementing eminence control to determine the success in their investment on

ventures. The weakness sensitivity analysis contains is that it is not fundamental in nature as

it judges only changes made in variables. Taking into account the possibility of changes in

variables are not made in analysis. Thus sensitivity analysis alone cannot judge and make

final decisions in budgeting and provides only the information’s that can be interpreted in

further analysis (Chinweike, 2013).

BREAK-EVEN ANALYSIS

Break-Even analysis is one another important tool used by managers to evaluate economic

viability of new venture. The point in which profits are equal to costs is called the breakeven

point and at that time no profit or loss is assumed. It can also be interpreted in sales i.e. break

even sales unit required to cover overall costs. Sales which are found below cost levels are

resulted losses and sales above cost levels are deemed profits made by company. Not always

breakeven point is determined in producing products to cross sales level but sometimes

certain profit returns are desired in investments. If it is not realised then selling substantial

amount of products may result in assuming loss for the company (Holland, 1998). Thus

breakeven can prove an effective tool in making decisions regarding quantity of goods to be

produced in new venture to gain revenue. Fixed costs and variable costs are utilised in

making break-even analysis in which fixed costs are those overhead costs those are invariable

and does not change even if there is a change in output level. Variable costs are opposite in

nature and changes with level of outputs and are inconstant and frequently settled on per unit

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

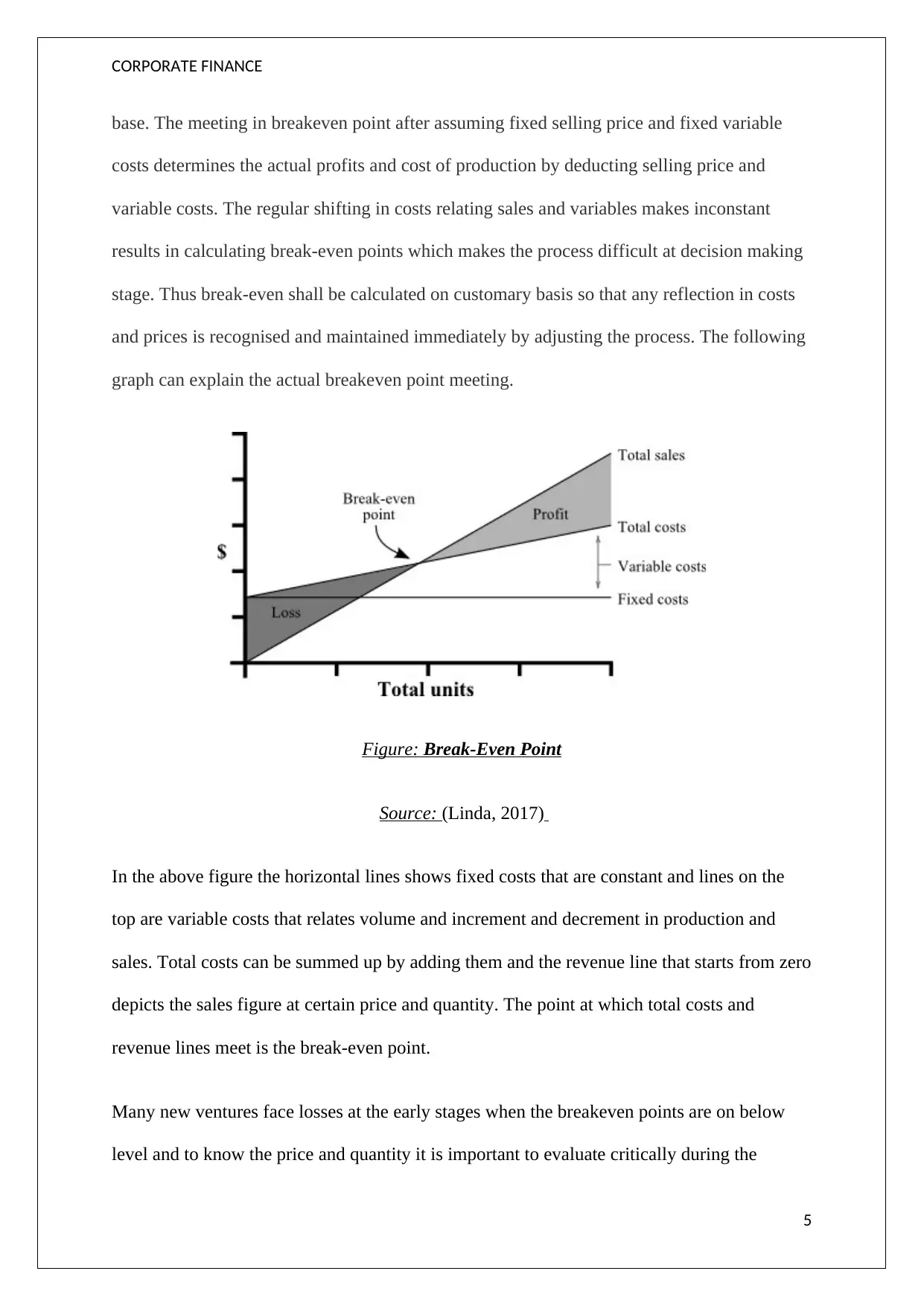

base. The meeting in breakeven point after assuming fixed selling price and fixed variable

costs determines the actual profits and cost of production by deducting selling price and

variable costs. The regular shifting in costs relating sales and variables makes inconstant

results in calculating break-even points which makes the process difficult at decision making

stage. Thus break-even shall be calculated on customary basis so that any reflection in costs

and prices is recognised and maintained immediately by adjusting the process. The following

graph can explain the actual breakeven point meeting.

Figure: Break-Even Point

Source: (Linda, 2017)

In the above figure the horizontal lines shows fixed costs that are constant and lines on the

top are variable costs that relates volume and increment and decrement in production and

sales. Total costs can be summed up by adding them and the revenue line that starts from zero

depicts the sales figure at certain price and quantity. The point at which total costs and

revenue lines meet is the break-even point.

Many new ventures face losses at the early stages when the breakeven points are on below

level and to know the price and quantity it is important to evaluate critically during the

5

base. The meeting in breakeven point after assuming fixed selling price and fixed variable

costs determines the actual profits and cost of production by deducting selling price and

variable costs. The regular shifting in costs relating sales and variables makes inconstant

results in calculating break-even points which makes the process difficult at decision making

stage. Thus break-even shall be calculated on customary basis so that any reflection in costs

and prices is recognised and maintained immediately by adjusting the process. The following

graph can explain the actual breakeven point meeting.

Figure: Break-Even Point

Source: (Linda, 2017)

In the above figure the horizontal lines shows fixed costs that are constant and lines on the

top are variable costs that relates volume and increment and decrement in production and

sales. Total costs can be summed up by adding them and the revenue line that starts from zero

depicts the sales figure at certain price and quantity. The point at which total costs and

revenue lines meet is the break-even point.

Many new ventures face losses at the early stages when the breakeven points are on below

level and to know the price and quantity it is important to evaluate critically during the

5

CORPORATE FINANCE

decision making time so that losses are analysed before handed. This analysis can help in

evaluating short term company’s goals and since cost analysis is mandatory it focuses in

keeping association between manufacturing and selling. One drawback that breakeven

analysis is that claim is supposed to be inelastic and states that high price will make profit

curvature steeper and lesser the breakeven point. There are times when customers agrees in

paying high rates but the conditions may depend on other factors like alternative availability

and cost of switching products. Therefore break even analysis is helpful in assuming the

volume of sales and revenues but not demand in products or services of new venture

(Tsorakidis, n.d.)

SCENARIO ANALYSIS

Scenario analysis is a strategic tool to analyse decisions after considering several factors and

probable outcomes. This tool is not a prognostic method but an analytical management tool to

manage business ambiguity. For example it can reflect how NPV would fluctuate under

elevated or stumpy inflations by investments. It can also help managers to make out actual

amount of outcomes that can be realised. Scenario analysis can be further differentiated into

three scenarios i.e. base case, worst case and best case that depends on the circumstances of

the scenarios. Decision making is a complex process and to make investment budget

decisions is the most delicate and significant part as long term implications depends entirely

on it (Brzaković, 2016). On other hand it can also be said that budgeting process is

unpredictability of cash flow of ventures while relating to cash flow expectation. The major

risk factors associated in budgeting are determined in scenario analysis as any sensitivity to

change in major factors and possibility of their changes are analysed. If the factors in venture

is of interdependent nature, an insight into its amalgamation of factors are provided by

scenario analysis that also shows how can the venture look dissimilar in other scenarios. Thus

6

decision making time so that losses are analysed before handed. This analysis can help in

evaluating short term company’s goals and since cost analysis is mandatory it focuses in

keeping association between manufacturing and selling. One drawback that breakeven

analysis is that claim is supposed to be inelastic and states that high price will make profit

curvature steeper and lesser the breakeven point. There are times when customers agrees in

paying high rates but the conditions may depend on other factors like alternative availability

and cost of switching products. Therefore break even analysis is helpful in assuming the

volume of sales and revenues but not demand in products or services of new venture

(Tsorakidis, n.d.)

SCENARIO ANALYSIS

Scenario analysis is a strategic tool to analyse decisions after considering several factors and

probable outcomes. This tool is not a prognostic method but an analytical management tool to

manage business ambiguity. For example it can reflect how NPV would fluctuate under

elevated or stumpy inflations by investments. It can also help managers to make out actual

amount of outcomes that can be realised. Scenario analysis can be further differentiated into

three scenarios i.e. base case, worst case and best case that depends on the circumstances of

the scenarios. Decision making is a complex process and to make investment budget

decisions is the most delicate and significant part as long term implications depends entirely

on it (Brzaković, 2016). On other hand it can also be said that budgeting process is

unpredictability of cash flow of ventures while relating to cash flow expectation. The major

risk factors associated in budgeting are determined in scenario analysis as any sensitivity to

change in major factors and possibility of their changes are analysed. If the factors in venture

is of interdependent nature, an insight into its amalgamation of factors are provided by

scenario analysis that also shows how can the venture look dissimilar in other scenarios. Thus

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

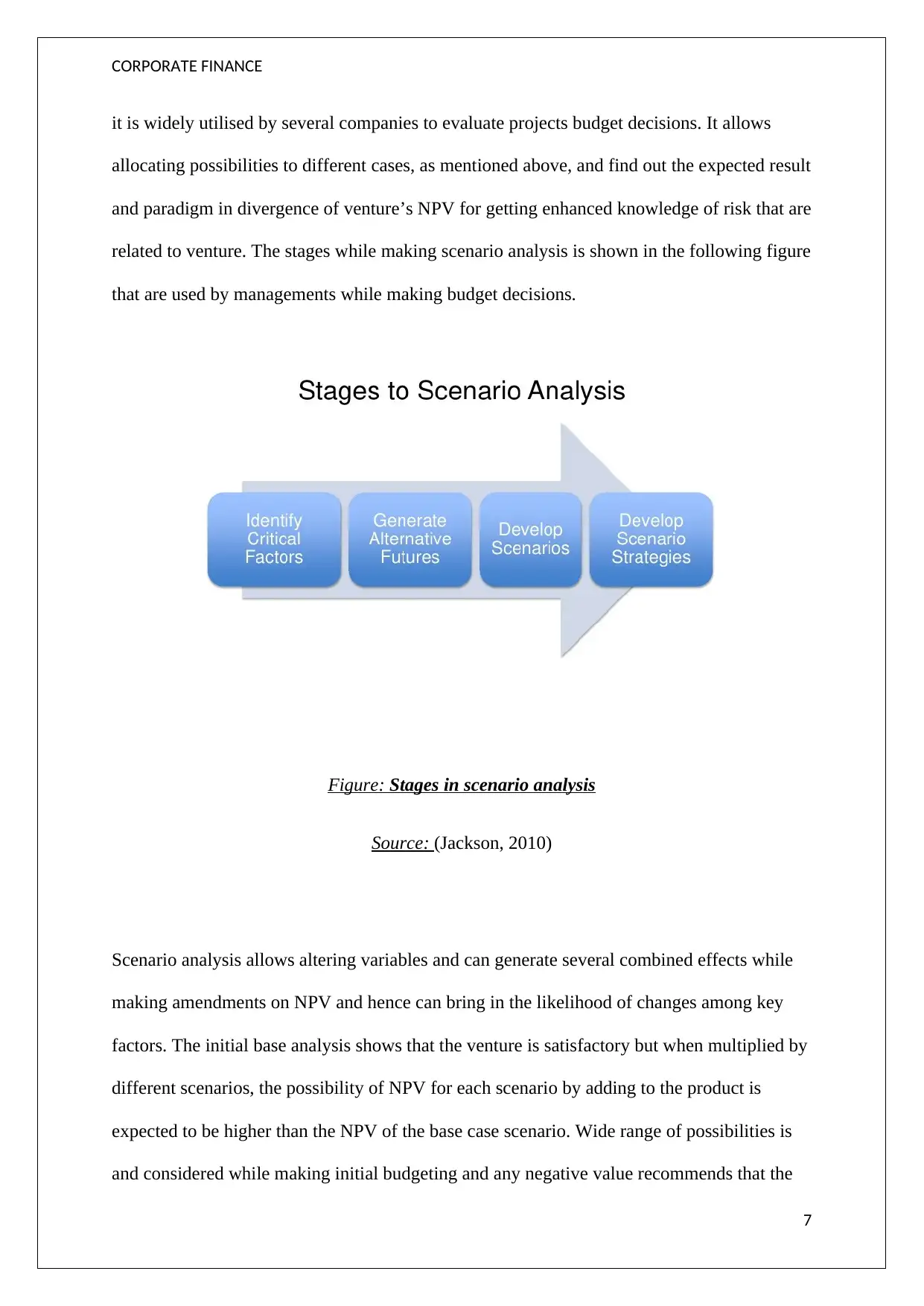

it is widely utilised by several companies to evaluate projects budget decisions. It allows

allocating possibilities to different cases, as mentioned above, and find out the expected result

and paradigm in divergence of venture’s NPV for getting enhanced knowledge of risk that are

related to venture. The stages while making scenario analysis is shown in the following figure

that are used by managements while making budget decisions.

Figure: Stages in scenario analysis

Source: (Jackson, 2010)

Scenario analysis allows altering variables and can generate several combined effects while

making amendments on NPV and hence can bring in the likelihood of changes among key

factors. The initial base analysis shows that the venture is satisfactory but when multiplied by

different scenarios, the possibility of NPV for each scenario by adding to the product is

expected to be higher than the NPV of the base case scenario. Wide range of possibilities is

and considered while making initial budgeting and any negative value recommends that the

7

it is widely utilised by several companies to evaluate projects budget decisions. It allows

allocating possibilities to different cases, as mentioned above, and find out the expected result

and paradigm in divergence of venture’s NPV for getting enhanced knowledge of risk that are

related to venture. The stages while making scenario analysis is shown in the following figure

that are used by managements while making budget decisions.

Figure: Stages in scenario analysis

Source: (Jackson, 2010)

Scenario analysis allows altering variables and can generate several combined effects while

making amendments on NPV and hence can bring in the likelihood of changes among key

factors. The initial base analysis shows that the venture is satisfactory but when multiplied by

different scenarios, the possibility of NPV for each scenario by adding to the product is

expected to be higher than the NPV of the base case scenario. Wide range of possibilities is

and considered while making initial budgeting and any negative value recommends that the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

venture is risk oriented. Since scenario analysis normally shows higher risks, to accept the

venture or not becomes questionable for the managers. Thus simulation analysis shall be

carried to find acceptable answer.

SIMULATION TECHNIQUE

Simulation techniques utilises numerical data to stature the standard outcome of scenario

analysis. Different statistical inputs like inflation rate, market risk, etc. are distributed and

estimated by running simulations to check the way they changes according to their

distributions and ultimate affects. The estimated output is found out after averaging the

statistical data outputs. Simulation techniques are used widely where multiple inputs changes

constantly which can also be unrelated. Simulation analysis are also used for estimating bond

prices but are majorly used while making initial budgeting i.e. the base case (DENT, 2012).

Managements utilises statistical methods when accounts becomes complex and all

interconnected factors those affects financial outcomes becomes inflexible. This method

deciphers problems by stimulating the highlighted processes and calculates the average

outcome of the method (Ray, 2014). Simulation technique can be further divided into two

phase in which factual system is build and then research is made on that model. The phase of

modelling can prove useful as it helps in gaining enhanced perceptive of the formation and its

process in complex systems. The experimental phase of simulation technique is also

beneficial as inter related and sequential aspects of complicated methods can be integrated in

the model. Simulation techniques does not solves models like other linear and dynamic

programming techniques and thus this technique is not used for defining process of most

favourable operational strategy. This technique can stimulate several sources of improbability

like market changes, default risk, inflation, etc. which affects the company portfolio or

budget investments and estimates a representative value. On the other hand it can also be said

that this technique helps in finding the average outcome after alteration is made in the inputs.

8

venture is risk oriented. Since scenario analysis normally shows higher risks, to accept the

venture or not becomes questionable for the managers. Thus simulation analysis shall be

carried to find acceptable answer.

SIMULATION TECHNIQUE

Simulation techniques utilises numerical data to stature the standard outcome of scenario

analysis. Different statistical inputs like inflation rate, market risk, etc. are distributed and

estimated by running simulations to check the way they changes according to their

distributions and ultimate affects. The estimated output is found out after averaging the

statistical data outputs. Simulation techniques are used widely where multiple inputs changes

constantly which can also be unrelated. Simulation analysis are also used for estimating bond

prices but are majorly used while making initial budgeting i.e. the base case (DENT, 2012).

Managements utilises statistical methods when accounts becomes complex and all

interconnected factors those affects financial outcomes becomes inflexible. This method

deciphers problems by stimulating the highlighted processes and calculates the average

outcome of the method (Ray, 2014). Simulation technique can be further divided into two

phase in which factual system is build and then research is made on that model. The phase of

modelling can prove useful as it helps in gaining enhanced perceptive of the formation and its

process in complex systems. The experimental phase of simulation technique is also

beneficial as inter related and sequential aspects of complicated methods can be integrated in

the model. Simulation techniques does not solves models like other linear and dynamic

programming techniques and thus this technique is not used for defining process of most

favourable operational strategy. This technique can stimulate several sources of improbability

like market changes, default risk, inflation, etc. which affects the company portfolio or

budget investments and estimates a representative value. On the other hand it can also be said

that this technique helps in finding the average outcome after alteration is made in the inputs.

8

CORPORATE FINANCE

For using simulation techniques, many computer software packages are utilised by the

managers in which NPV’s are calculated by picking randomly selected variables and then

calculates mean and standard deviation. This mean or standard deviation value is used by

managers to determine the expected NPV of new venture and risk associated in them. This

technique is more precise as compared to sensitivity analysis as sensitivity analysis utilises

restricted number of cases (Montazer, 2003).

CONCLUSION

Thus by utilising different techniques and analysis tools, managers can gain the opportunity

of reducing risks and revaluate decisions about their ventures. It helps managers to decide

whether to invest in new projects or to terminate any existing unprofitable project. In this

research paper the techniques utilised for risk determination in capital budgeting and to

evaluate future prospects of projects have been stated (Karanovic, 2010). These can give

managers a platform to make a selection of alternative techniques according to their project.

By predicting cash flow values, mangers can predict analysed risks and also make out

decisions after applying different project values to change the estimated risks. Thus they are

enabled to decide whether to take a project or not since observations regarding risks and

probability are made before implementations (Chambers, 2017).

9

For using simulation techniques, many computer software packages are utilised by the

managers in which NPV’s are calculated by picking randomly selected variables and then

calculates mean and standard deviation. This mean or standard deviation value is used by

managers to determine the expected NPV of new venture and risk associated in them. This

technique is more precise as compared to sensitivity analysis as sensitivity analysis utilises

restricted number of cases (Montazer, 2003).

CONCLUSION

Thus by utilising different techniques and analysis tools, managers can gain the opportunity

of reducing risks and revaluate decisions about their ventures. It helps managers to decide

whether to invest in new projects or to terminate any existing unprofitable project. In this

research paper the techniques utilised for risk determination in capital budgeting and to

evaluate future prospects of projects have been stated (Karanovic, 2010). These can give

managers a platform to make a selection of alternative techniques according to their project.

By predicting cash flow values, mangers can predict analysed risks and also make out

decisions after applying different project values to change the estimated risks. Thus they are

enabled to decide whether to take a project or not since observations regarding risks and

probability are made before implementations (Chambers, 2017).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

REFERENCES

Chinweike, 2013. What is Sensitivity Analysis? [Online] Available at:

http://www.accountantnextdoor.com/what-is-sensitivity-analysis/ [Accessed 12 September

2017].

Creative Commons, 2012. Capital Budgeting Decision Making. [Online] Available at:

https://2012books.lardbucket.org/books/finance-for-managers/s13-capital-budgeting-

decision-mak.html [Accessed 12 September 2017].

DENT, A.W.a.J.B., 2012. THE APPLICATION OF SIMULATION TECHNIQUES TO THE

STUDY OF GRAZING SYSTEMS. [Online] Available at:

http://onlinelibrary.wiley.com/doi/10.1111/j.1467-8489.1969.tb00062.x/pdf [Accessed 12

September 2017].

Edupristine, 2017. Capital Budgeting: Techniques & Importance. [Online] Available at:

http://www.edupristine.com/blog/capital-budgeting-techniques [Accessed 12 September

2017].

Goran Karanovic, S.B.a.S.B., 2010. TECHNIQUES FOR MANAGING PROJECTS RISK IN

CAPITAL BUDGETING PROCESS. [Online] Available at:

https://www.econstor.eu/obitstream/10419/49182/1/666054274.pdf [Accessed 12 September

2017].

Holland, R., 1998. Break-Even Analysis. [Online] Available at:

https://ag.tennessee.edu/cpa/Information%20Sheets/adc3.pdf [Accessed 12 September 2017].

Jackson, A., 2010. Scenario Analysis: Planning for Uncertain Futures. [Online] Available at:

https://www.slideshare.net/8of12/scenario-analysis-planning-for-uncertain-futures [Accessed

12 September 2017].

10

REFERENCES

Chinweike, 2013. What is Sensitivity Analysis? [Online] Available at:

http://www.accountantnextdoor.com/what-is-sensitivity-analysis/ [Accessed 12 September

2017].

Creative Commons, 2012. Capital Budgeting Decision Making. [Online] Available at:

https://2012books.lardbucket.org/books/finance-for-managers/s13-capital-budgeting-

decision-mak.html [Accessed 12 September 2017].

DENT, A.W.a.J.B., 2012. THE APPLICATION OF SIMULATION TECHNIQUES TO THE

STUDY OF GRAZING SYSTEMS. [Online] Available at:

http://onlinelibrary.wiley.com/doi/10.1111/j.1467-8489.1969.tb00062.x/pdf [Accessed 12

September 2017].

Edupristine, 2017. Capital Budgeting: Techniques & Importance. [Online] Available at:

http://www.edupristine.com/blog/capital-budgeting-techniques [Accessed 12 September

2017].

Goran Karanovic, S.B.a.S.B., 2010. TECHNIQUES FOR MANAGING PROJECTS RISK IN

CAPITAL BUDGETING PROCESS. [Online] Available at:

https://www.econstor.eu/obitstream/10419/49182/1/666054274.pdf [Accessed 12 September

2017].

Holland, R., 1998. Break-Even Analysis. [Online] Available at:

https://ag.tennessee.edu/cpa/Information%20Sheets/adc3.pdf [Accessed 12 September 2017].

Jackson, A., 2010. Scenario Analysis: Planning for Uncertain Futures. [Online] Available at:

https://www.slideshare.net/8of12/scenario-analysis-planning-for-uncertain-futures [Accessed

12 September 2017].

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

John C. Chambers, S.K.M.a.D.D.S., 2017. How to Choose the Right Forecasting Technique.

[Online] Available at: https://hbr.org/1971/07/how-to-choose-the-right-forecasting-technique

[Accessed 12 September 2017].

Kumar, S., 2016. 3 Traditional Methods of Capital Budgeting | Financial Analysis. [Online]

Available at: (http://www.yourarticlelibrary.com/accounting/capital-budgeting/methods-of-

evaluation/3-traditional-methods-of-capital-budgeting-financial-analysis/68012/ [Accessed

12 September 2017].

Lawrence, H., n.d. The Use of Modern Capital Budgeting Techniques. [Online] Available at:

http://www.maesc.org/maesc02/FullPapers/b5-1-doc.pdf [Accessed 12 September 2017].

Linda, 2017. Break Even Analysis. [Online] Available at: http://www.essay.uk.com/free-

essays/accounting/break-even-analysis.php [Accessed 12 September 2017].

M. Ali Montazer, K.E.a.H.A., 2003. SIMULATION MODELING IN OPERATIONS

MANAGEMENT: A Sampling of Applications. [Online] Available at:

https://www.pomsmeetings.org/ConfProceedings/001/Papers/PSC-04.4.pdf [Accessed 12

September 2017].

Nikolaos Tsorakidis, S.P.M.Z.a.C.Z., n.d. Break Even Analysis. [Online] Available at:

http://ebooks.bharathuniv.ac.in/gdlc1/gdlc4/Arts_and_Science_Books/commerce/

economics/Business%20Economics/Books/Break%20Even%20Analysis.pdf [Accessed 12

September 2017].

Pannel, D.J., 2017. Sensitivity analysis: strategies, methods, concepts, examples. [Online]

Available at: http://dpannell.fnas.uwa.edu.au/dpap971f.htm [Accessed 12 September 2017].

Ray, P., 2014. Applications of simulation in Business with Example. [Online] Available at:

https://www.slideshare.net/PratimaRay/applications-of-simulation-in-business-with-example

11

John C. Chambers, S.K.M.a.D.D.S., 2017. How to Choose the Right Forecasting Technique.

[Online] Available at: https://hbr.org/1971/07/how-to-choose-the-right-forecasting-technique

[Accessed 12 September 2017].

Kumar, S., 2016. 3 Traditional Methods of Capital Budgeting | Financial Analysis. [Online]

Available at: (http://www.yourarticlelibrary.com/accounting/capital-budgeting/methods-of-

evaluation/3-traditional-methods-of-capital-budgeting-financial-analysis/68012/ [Accessed

12 September 2017].

Lawrence, H., n.d. The Use of Modern Capital Budgeting Techniques. [Online] Available at:

http://www.maesc.org/maesc02/FullPapers/b5-1-doc.pdf [Accessed 12 September 2017].

Linda, 2017. Break Even Analysis. [Online] Available at: http://www.essay.uk.com/free-

essays/accounting/break-even-analysis.php [Accessed 12 September 2017].

M. Ali Montazer, K.E.a.H.A., 2003. SIMULATION MODELING IN OPERATIONS

MANAGEMENT: A Sampling of Applications. [Online] Available at:

https://www.pomsmeetings.org/ConfProceedings/001/Papers/PSC-04.4.pdf [Accessed 12

September 2017].

Nikolaos Tsorakidis, S.P.M.Z.a.C.Z., n.d. Break Even Analysis. [Online] Available at:

http://ebooks.bharathuniv.ac.in/gdlc1/gdlc4/Arts_and_Science_Books/commerce/

economics/Business%20Economics/Books/Break%20Even%20Analysis.pdf [Accessed 12

September 2017].

Pannel, D.J., 2017. Sensitivity analysis: strategies, methods, concepts, examples. [Online]

Available at: http://dpannell.fnas.uwa.edu.au/dpap971f.htm [Accessed 12 September 2017].

Ray, P., 2014. Applications of simulation in Business with Example. [Online] Available at:

https://www.slideshare.net/PratimaRay/applications-of-simulation-in-business-with-example

11

CORPORATE FINANCE

[Accessed 12 September 2017].

Tomislav Brzaković, A.B.a.J.P., 2016. APPLICATION OF SCENARIO ANALYSIS IN THE

INVESTMENT PROJECTS EVALUATION. [Online] Available at:

http://www.ea.bg.ac.rs/images/Arhiva/2016/Broj%202/10%20EP%202%202016.pdf

[Accessed 12 September 2017].

12

[Accessed 12 September 2017].

Tomislav Brzaković, A.B.a.J.P., 2016. APPLICATION OF SCENARIO ANALYSIS IN THE

INVESTMENT PROJECTS EVALUATION. [Online] Available at:

http://www.ea.bg.ac.rs/images/Arhiva/2016/Broj%202/10%20EP%202%202016.pdf

[Accessed 12 September 2017].

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.