Corporate Finance Assignment: Risk, Return, and Capital Structure

VerifiedAdded on 2021/04/21

|14

|3138

|53

Homework Assignment

AI Summary

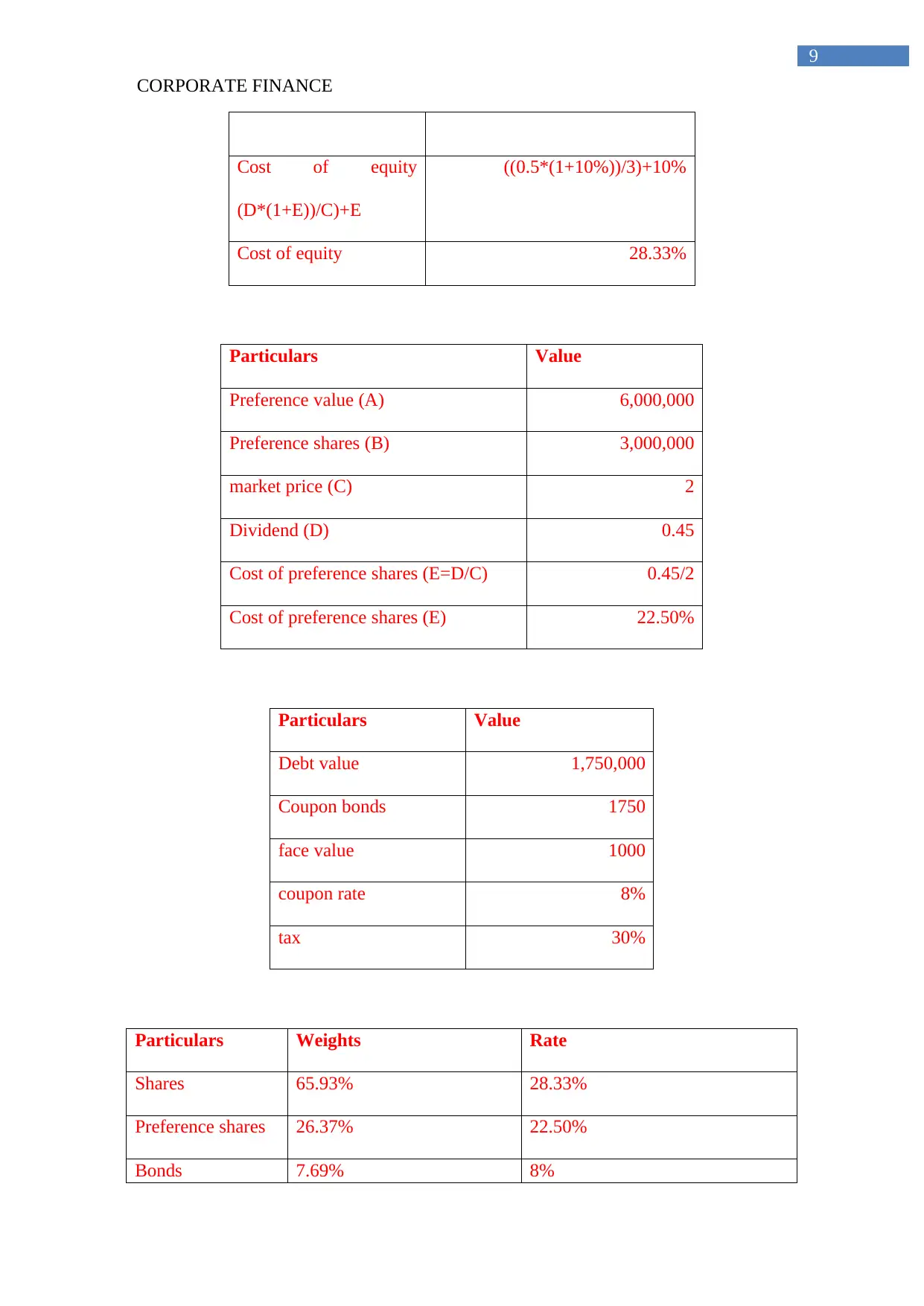

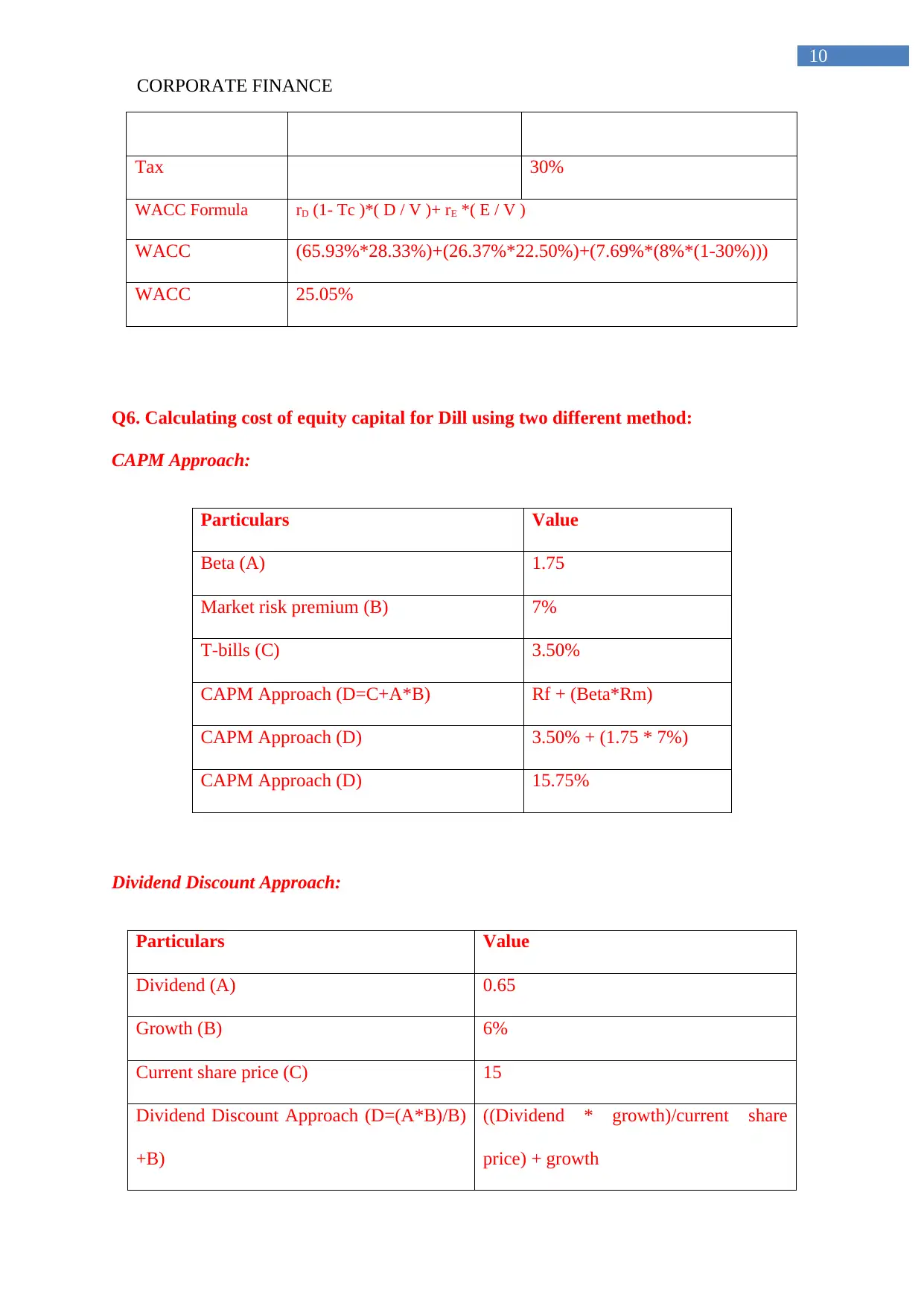

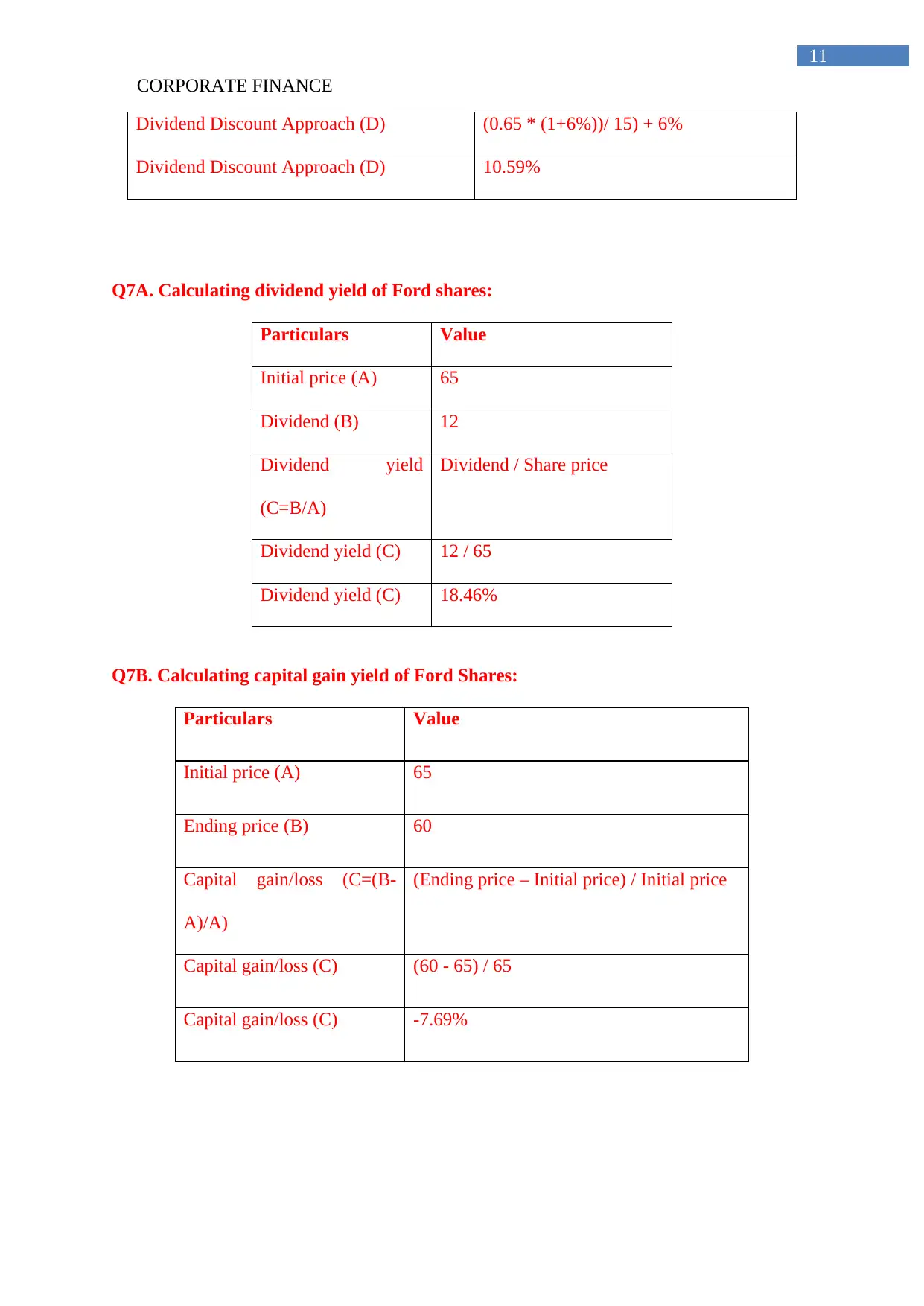

This corporate finance assignment comprehensively addresses key concepts in financial management. It begins by examining factors influencing option premiums, differentiating between various derivative types (futures, forwards, options, and swaps), and contrasting American and European options. The assignment then delves into optimal capital structure, illustrating it with a graph, and explains the Capital Asset Pricing Model (CAPM) through a graphical representation. Furthermore, the assignment explores the residual-dividend theory and the expectations theory of dividend policy. It proceeds to analyze call and put options, determining whether they are in-the-money, at-the-money, or out-of-the-money, and calculating their exercise and time values. The assignment also involves calculating the weighted average cost of capital (WACC) for Google and the cost of equity for Dill using two distinct methods (CAPM and dividend discount model). Finally, it calculates dividend and capital gain yields for Ford shares and discusses the benefits of diversification for investors, including the key factors that determine the extent of these benefits. The assignment utilizes graphs, tables, and calculations to provide detailed explanations and analyses.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.