Corporate Finance Report: CSL Limited vs COCHLEAR LIMITED Analysis

VerifiedAdded on 2023/06/05

|18

|4252

|275

Report

AI Summary

This corporate finance report provides a detailed analysis of CSL Limited and COCHLEAR LIMITED, focusing on key financial statements such as the balance sheet, cash flow statement, and comprehensive income statement. It examines the companies' owner's equity, comparing items like share capital, contributed equity, reserves, and retained earnings. The report also assesses the debt-to-equity ratio to understand the capital structure of each company. Furthermore, it analyzes cash flow statements, categorizing cash flows from operating, investing, and financing activities, and compares the effective tax rates, deferred tax liabilities, and assets. The study concludes by highlighting the similarities and differences in the financial practices of both companies, offering insights into their financial health and strategies. Desklib provides a platform to access similar solved assignments and past papers for students.

Running Head: Corporate Finance

1

Project Report: Corporate Finance

1

Project Report: Corporate Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Finance

2

Executive summary

Corporate finance report has been prepared on CSL limited and COCHLEAR

LIMITED in order to identify the uniformity in the annual report of the company. the report

focuses on the recording, presentation, disclosure policies, accounting standards, framework

etc of the companies to measure that whether the proper accounting rules have been followed

by the company or not. After conducting the research on various items of the annual report

and their impact on the financial performance and position of the companies, it has been

concluded that the same rules and procedure are followed by both the companies in order to

give proper information to shareholders and set uniformity.

2

Executive summary

Corporate finance report has been prepared on CSL limited and COCHLEAR

LIMITED in order to identify the uniformity in the annual report of the company. the report

focuses on the recording, presentation, disclosure policies, accounting standards, framework

etc of the companies to measure that whether the proper accounting rules have been followed

by the company or not. After conducting the research on various items of the annual report

and their impact on the financial performance and position of the companies, it has been

concluded that the same rules and procedure are followed by both the companies in order to

give proper information to shareholders and set uniformity.

Corporate Finance

3

Contents

Introduction.......................................................................................................................4

CSL limited and COCHLEAR LIMITED........................................................................4

Owner’s equity..................................................................................................................4

1. Items of equity statement.....................................................................................5

2. Comparative analysis...........................................................................................5

Cash flow statement..........................................................................................................6

3. Items in cash flow statement................................................................................6

4. Comparative analysis on broad categories...........................................................8

5. Comparative analysis among the companies.......................................................9

Other comprehensive income statement...........................................................................9

6. Items in comprehensive income statement..........................................................9

7. Reasons for not adding them in profit and loss a/c............................................10

8. Comparative analysis.........................................................................................10

9. Comprehensive income involvement.................................................................11

Accounting for corporate income tax.............................................................................11

10. Tax expenses in financial statement...............................................................11

11. Effective tax rate.............................................................................................12

12. Deferred tax liabilities and assets...................................................................12

13. Changes in deferred tax liabilities and assets................................................13

14. Cash tax amount.............................................................................................13

15. Cash tax rate...................................................................................................14

16. Difference among the cash and book tax rate................................................14

Conclusion......................................................................................................................14

3

Contents

Introduction.......................................................................................................................4

CSL limited and COCHLEAR LIMITED........................................................................4

Owner’s equity..................................................................................................................4

1. Items of equity statement.....................................................................................5

2. Comparative analysis...........................................................................................5

Cash flow statement..........................................................................................................6

3. Items in cash flow statement................................................................................6

4. Comparative analysis on broad categories...........................................................8

5. Comparative analysis among the companies.......................................................9

Other comprehensive income statement...........................................................................9

6. Items in comprehensive income statement..........................................................9

7. Reasons for not adding them in profit and loss a/c............................................10

8. Comparative analysis.........................................................................................10

9. Comprehensive income involvement.................................................................11

Accounting for corporate income tax.............................................................................11

10. Tax expenses in financial statement...............................................................11

11. Effective tax rate.............................................................................................12

12. Deferred tax liabilities and assets...................................................................12

13. Changes in deferred tax liabilities and assets................................................13

14. Cash tax amount.............................................................................................13

15. Cash tax rate...................................................................................................14

16. Difference among the cash and book tax rate................................................14

Conclusion......................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Finance

4

References.......................................................................................................................16

4

References.......................................................................................................................16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Finance

5

Introduction:

Evaluation on the accounting treatment of an organization is one of the essential

aspects of the corporate finance. It is essential for an entity to follow the accouning standards

and principle to recognize, record and present the accounting figures in the financial

statement and annual report of the company so that a fair value could be conveyed to the

stakeholders of the entity (Romney, Steinbart, Zhang and Xu, 2006). If an organization

follows the proper rules of accounting standards then the comparison study could also be

done in proper way among the company and the competitor company.

In the report, the main final financial statements of CSL limited and Cochlear Limited

has been taken into the context to evaluate the study. The final financial statement, cash flow

statement, balance sheet, comprehensive income statement and taxation recording process of

the company has been evalauted and compared with each other to reach over a conclusion

about the performance of the company and the importance

CSL limited and COCHLEAR LIMITED:

CSL limited is an Australian multinational company which is specialized in

biotechnology. The company mainly researches, develops, manufactures and marketing and

sales the medical solution of various disease in the market. The main motto of the business is

to prevent the serious medical issues. The product area of the company includes blood

plasma, vaccines, derivatives, antivenin and the cell cultures which are used in various

medical issues preventions (Our company, 2018). The company has been founded in the year

of 1916 in order to prevent the serious medical issues.

Cochlear Limited researches, develops, manufactures and marketing and sales the

pharmaceuticals grade cannabis and hemp based nutra-ceuticals treatment and products for

the human and animal helath in the Australian market. It also provides its services in the

Switzerland and Slovakia. The company mainly involves in the hemp growing operations,

cannabidiol product sales activities etc. (Home, 2018). The company also offers branded

premium cannabis chocolate and beverage in the market to improve the health issues in the

market.

Owner’s equity:

5

Introduction:

Evaluation on the accounting treatment of an organization is one of the essential

aspects of the corporate finance. It is essential for an entity to follow the accouning standards

and principle to recognize, record and present the accounting figures in the financial

statement and annual report of the company so that a fair value could be conveyed to the

stakeholders of the entity (Romney, Steinbart, Zhang and Xu, 2006). If an organization

follows the proper rules of accounting standards then the comparison study could also be

done in proper way among the company and the competitor company.

In the report, the main final financial statements of CSL limited and Cochlear Limited

has been taken into the context to evaluate the study. The final financial statement, cash flow

statement, balance sheet, comprehensive income statement and taxation recording process of

the company has been evalauted and compared with each other to reach over a conclusion

about the performance of the company and the importance

CSL limited and COCHLEAR LIMITED:

CSL limited is an Australian multinational company which is specialized in

biotechnology. The company mainly researches, develops, manufactures and marketing and

sales the medical solution of various disease in the market. The main motto of the business is

to prevent the serious medical issues. The product area of the company includes blood

plasma, vaccines, derivatives, antivenin and the cell cultures which are used in various

medical issues preventions (Our company, 2018). The company has been founded in the year

of 1916 in order to prevent the serious medical issues.

Cochlear Limited researches, develops, manufactures and marketing and sales the

pharmaceuticals grade cannabis and hemp based nutra-ceuticals treatment and products for

the human and animal helath in the Australian market. It also provides its services in the

Switzerland and Slovakia. The company mainly involves in the hemp growing operations,

cannabidiol product sales activities etc. (Home, 2018). The company also offers branded

premium cannabis chocolate and beverage in the market to improve the health issues in the

market.

Owner’s equity:

Corporate Finance

6

Owner’s equity of the business represent the total equity amount which has been

generated and retained by the company for the long term investment and to run the business

for a long period (Kaplan and Atkinson, 2015). The owner’s equity evaluation on CSL

limited and COCHLEAR LIMITED is as follows:

1. Items of equity statement:

The annual report of both the companies has been studied and evaluated and the

following result has been found:

Equity Items

CSL limited Cochlear Limited

AUD in million

2018-

06

2017-

06 Changes

2018-

06

2017-

06 Changes

Stockholders' equity

Share capital 173 169 2.37%

Contributed equity

-

4634.5

-

4534.3 2.21%

Reserves 224.2 294.2 -23.79% -33.8 -12.9 162.02%

Retained earnings 8490.2 7403.9 14.67% 471.6 387.1 21.83%

Total stockholder's

equity 4079.9 3163.8 28.96% 610.8 543.2 12.44%

(Annual report, 2018)

The above table represent the different items of both the companies which have been

recorded to present the total equity fund of the company. Share capital is the total funds

which have been raised by the company through issuing the shares in the capital market. The

share capital of Cochlear limited has been improved by 2.37% in 2018. Further, the

contributed equity depicts the total cash which has been raised. In case of CSL limited, the

2.21% decrement has been seen in the equity position because of internal changes.

Further, the reserves are the amount which is keep by the business aside for the

betterment of the business and to save from any sudden consequences. In both the companies,

the reserve amount has bee decreased because of the better industry level. Further, the

retained earnings depict the retained amount from the profit level for the future uncertainties

of the business (Fernandes, Lynch and Netemeyer, 2014). This level has been improved by

both the companies through reducing the dividend payout %.

2. Comparative analysis:

6

Owner’s equity of the business represent the total equity amount which has been

generated and retained by the company for the long term investment and to run the business

for a long period (Kaplan and Atkinson, 2015). The owner’s equity evaluation on CSL

limited and COCHLEAR LIMITED is as follows:

1. Items of equity statement:

The annual report of both the companies has been studied and evaluated and the

following result has been found:

Equity Items

CSL limited Cochlear Limited

AUD in million

2018-

06

2017-

06 Changes

2018-

06

2017-

06 Changes

Stockholders' equity

Share capital 173 169 2.37%

Contributed equity

-

4634.5

-

4534.3 2.21%

Reserves 224.2 294.2 -23.79% -33.8 -12.9 162.02%

Retained earnings 8490.2 7403.9 14.67% 471.6 387.1 21.83%

Total stockholder's

equity 4079.9 3163.8 28.96% 610.8 543.2 12.44%

(Annual report, 2018)

The above table represent the different items of both the companies which have been

recorded to present the total equity fund of the company. Share capital is the total funds

which have been raised by the company through issuing the shares in the capital market. The

share capital of Cochlear limited has been improved by 2.37% in 2018. Further, the

contributed equity depicts the total cash which has been raised. In case of CSL limited, the

2.21% decrement has been seen in the equity position because of internal changes.

Further, the reserves are the amount which is keep by the business aside for the

betterment of the business and to save from any sudden consequences. In both the companies,

the reserve amount has bee decreased because of the better industry level. Further, the

retained earnings depict the retained amount from the profit level for the future uncertainties

of the business (Fernandes, Lynch and Netemeyer, 2014). This level has been improved by

both the companies through reducing the dividend payout %.

2. Comparative analysis:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Finance

7

Further, the study has been done on capital structure level of both the companies. In

order to identify the capital structure position, debt equity level has been compared. The

below table depict about debt/ equity position of the companies:

Equity Items

CSL

limited

Cochlear

Limited

AUD in

million 2018-06 2018-06

Long term

debt 4779.9 258.4

Equity 4079.9 610.8

Debt / Equity 117.16% 42.31%

(Annual report, 2017)

The table represent the 11.7.16% debt against the equity position of CSL limited and

42.31% debt level in case of Cochlear Limited. The CSL limited is focusing on the debt level

more to improve the funds. It impacts higher risk position of the company. Though, the cost

position of the company gets lower (Du and Girma, 2009). Further, in case of Cochlear

Limited, the company mainly focuses on the equity funds to reduce the risk level of the

company. It represents that Cochlear Limited is required to improve the debt level a bit and

CSL limited is suggested to reduce the debt level.

Cash flow statement:

Cash flow statement of the business represents the total cash inflow and cash outflow

position which has been generated by the company in particular time period (Deegan, 2013).

The evaluation on cash flow statement on CSL limited and COCHLEAR LIMITED is as

follows:

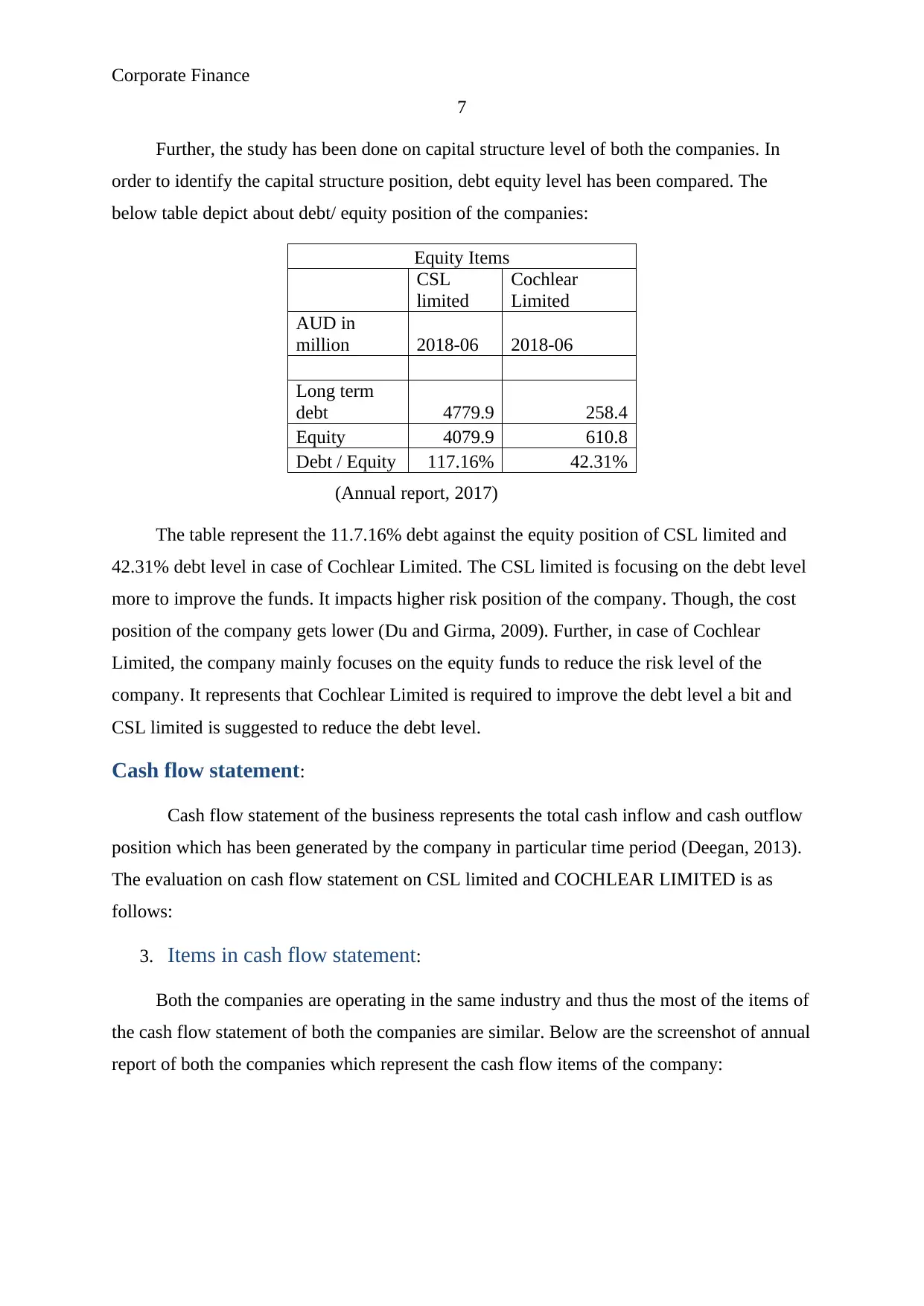

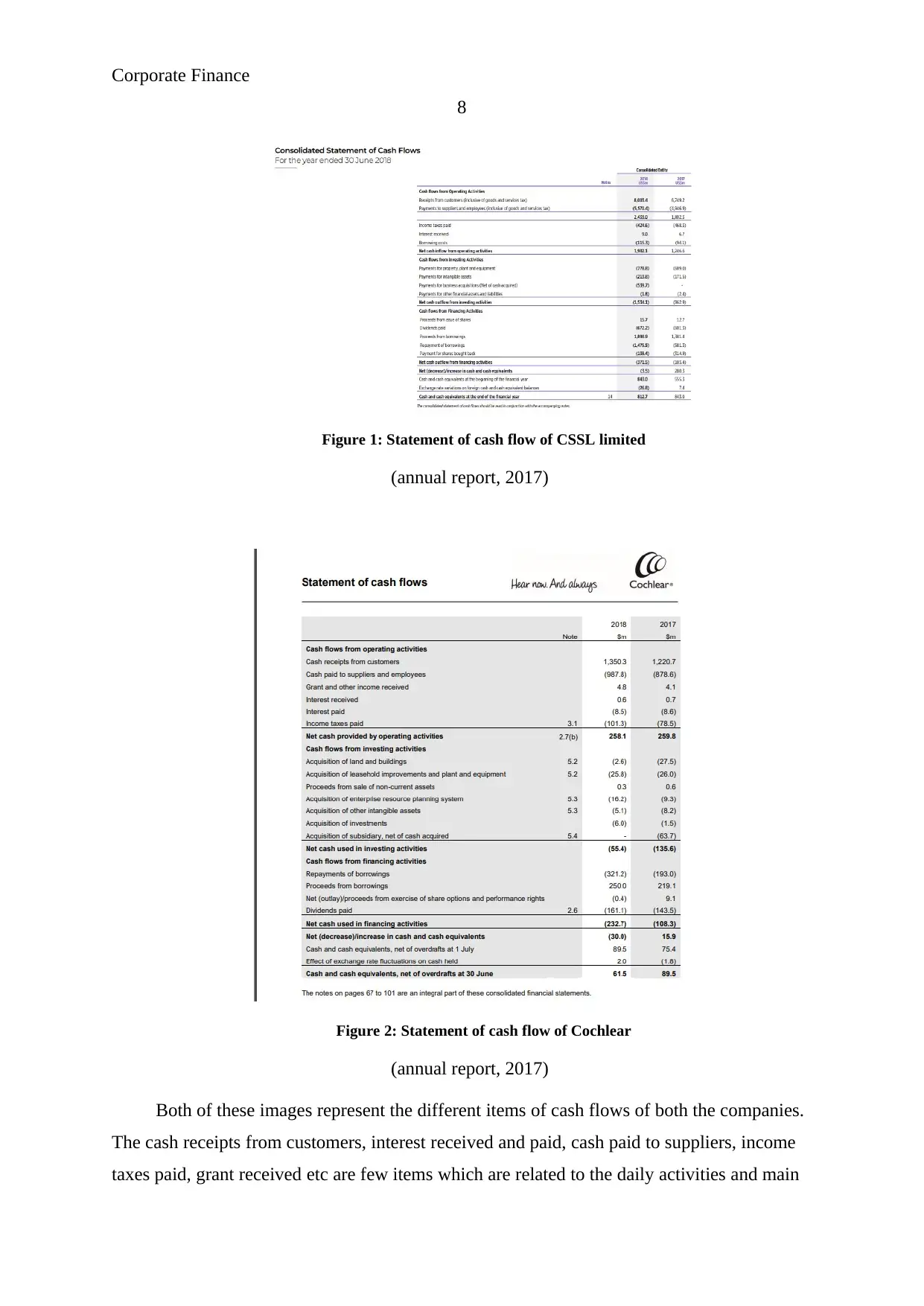

3. Items in cash flow statement:

Both the companies are operating in the same industry and thus the most of the items of

the cash flow statement of both the companies are similar. Below are the screenshot of annual

report of both the companies which represent the cash flow items of the company:

7

Further, the study has been done on capital structure level of both the companies. In

order to identify the capital structure position, debt equity level has been compared. The

below table depict about debt/ equity position of the companies:

Equity Items

CSL

limited

Cochlear

Limited

AUD in

million 2018-06 2018-06

Long term

debt 4779.9 258.4

Equity 4079.9 610.8

Debt / Equity 117.16% 42.31%

(Annual report, 2017)

The table represent the 11.7.16% debt against the equity position of CSL limited and

42.31% debt level in case of Cochlear Limited. The CSL limited is focusing on the debt level

more to improve the funds. It impacts higher risk position of the company. Though, the cost

position of the company gets lower (Du and Girma, 2009). Further, in case of Cochlear

Limited, the company mainly focuses on the equity funds to reduce the risk level of the

company. It represents that Cochlear Limited is required to improve the debt level a bit and

CSL limited is suggested to reduce the debt level.

Cash flow statement:

Cash flow statement of the business represents the total cash inflow and cash outflow

position which has been generated by the company in particular time period (Deegan, 2013).

The evaluation on cash flow statement on CSL limited and COCHLEAR LIMITED is as

follows:

3. Items in cash flow statement:

Both the companies are operating in the same industry and thus the most of the items of

the cash flow statement of both the companies are similar. Below are the screenshot of annual

report of both the companies which represent the cash flow items of the company:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Finance

8

Figure 1: Statement of cash flow of CSSL limited

(annual report, 2017)

Figure 2: Statement of cash flow of Cochlear

(annual report, 2017)

Both of these images represent the different items of cash flows of both the companies.

The cash receipts from customers, interest received and paid, cash paid to suppliers, income

taxes paid, grant received etc are few items which are related to the daily activities and main

8

Figure 1: Statement of cash flow of CSSL limited

(annual report, 2017)

Figure 2: Statement of cash flow of Cochlear

(annual report, 2017)

Both of these images represent the different items of cash flows of both the companies.

The cash receipts from customers, interest received and paid, cash paid to suppliers, income

taxes paid, grant received etc are few items which are related to the daily activities and main

Corporate Finance

9

operations of the business and thus it has been represented under the operating cash flows of

the company. In case of Cochlear, the revenue level has been improved along with that the

supplier amount and the taxes of the company has also been improved with a great level

which has affected the operating level of the business. In case of CSL limited, the huge

increment has been seen in the receipts from the customers due to which the payment has also

been improved but the growth rate on revenue is higher because of the huge demand of the

products in the market (Kieso, Weygandt and Warfield, 2010).

Further, the payment for the new PPE, sales of PPE, payment for acquisition and

intangible assets, payment for other financial liabilities and assets are few items which are

related to the resources and the investment of the business because it affect the business for

long term and thus it has been represented under the investing cash flows of the company. In

case of Cochlear and CSL limited, the great changes have been seen in the cash flows

because of the less investment by Cochlear and huge investment by CSL limited.

Lastly, the issue of new shares in the market, payment of dividend, repayment of

borrowings, issue of debt, share brought back etc are few items which are related to the

capital position and investment position of the company in the market and thus it is

represented in the financial activities head of cash flow statement (Annual report, 2017). In

case of Cochlear and CSL limited, the great changes have been seen in the cash flows

because of fewer changes into the capital structure position of the companies.

4. Comparative analysis on broad categories:

Further, the study has been done on the main categories of the cash flow statement of

both the companies. In case of Cochlear Limited, great increment has been seen in operating

cash flows of the business with an improved growth rate in last 2 years because of higher

turnover and great demand of the products in the market. The investment level has been

improved by the company because of investment in new PPE (Annual report, 2017). The

financial activities of the business have been compared further and an increment in the cash

outflow of the business has been seen.

CSL limited

AUD in million 2018-06 2017-06 2016-06

Net cash used for operating activities 1902.1 1246.6 1090.9

Net cash used for investing activities -1534.1 -862.9 -965.4

Net cash provided by (used for) financing -371.5 -103.4 -115.8

9

operations of the business and thus it has been represented under the operating cash flows of

the company. In case of Cochlear, the revenue level has been improved along with that the

supplier amount and the taxes of the company has also been improved with a great level

which has affected the operating level of the business. In case of CSL limited, the huge

increment has been seen in the receipts from the customers due to which the payment has also

been improved but the growth rate on revenue is higher because of the huge demand of the

products in the market (Kieso, Weygandt and Warfield, 2010).

Further, the payment for the new PPE, sales of PPE, payment for acquisition and

intangible assets, payment for other financial liabilities and assets are few items which are

related to the resources and the investment of the business because it affect the business for

long term and thus it has been represented under the investing cash flows of the company. In

case of Cochlear and CSL limited, the great changes have been seen in the cash flows

because of the less investment by Cochlear and huge investment by CSL limited.

Lastly, the issue of new shares in the market, payment of dividend, repayment of

borrowings, issue of debt, share brought back etc are few items which are related to the

capital position and investment position of the company in the market and thus it is

represented in the financial activities head of cash flow statement (Annual report, 2017). In

case of Cochlear and CSL limited, the great changes have been seen in the cash flows

because of fewer changes into the capital structure position of the companies.

4. Comparative analysis on broad categories:

Further, the study has been done on the main categories of the cash flow statement of

both the companies. In case of Cochlear Limited, great increment has been seen in operating

cash flows of the business with an improved growth rate in last 2 years because of higher

turnover and great demand of the products in the market. The investment level has been

improved by the company because of investment in new PPE (Annual report, 2017). The

financial activities of the business have been compared further and an increment in the cash

outflow of the business has been seen.

CSL limited

AUD in million 2018-06 2017-06 2016-06

Net cash used for operating activities 1902.1 1246.6 1090.9

Net cash used for investing activities -1534.1 -862.9 -965.4

Net cash provided by (used for) financing -371.5 -103.4 -115.8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Finance

10

activities

(Annual report, 2017)

In case of Cochlear Limited, great increment has been seen in operating cash flows of

the business because of higher turnover. The investment level has also been reduced by the

company to manage the cash position and reduce the liquidity level of the business. The

financial activities of the business have been compared further to identify the changes into

company and a great decrement has been seen in the company because of repayment of

borrowings and huge dividend to the shareholders.

Cochlear Limited

AUD in million

2018-

06

2017-

06

2016-

06

Net cash used for operating activities 258.1 259.8 185.1

Net cash used for investing activities -55.4 -135.6 -50.1

Net cash provided by (used for)

financing activities -232.7 -108.3

-

130.89

(Annual report, 2017)

5. Comparative analysis among the companies:

On the basis of the comparison on both the companies, it has been found that the

increment in the operating cash flow of CSL limited is 52.58% which is quite higher than

cochlear limited. Further the investing level explains the better position of Cochlear limited in

order to improve the cash level of the company and the financing activities brief increased

cash outflow of both the companies (Annual report, 2018). Though, the level of Cochlear

limited is lower. It explains that the overall cash position of CSL limited is better.

CSL limited Cochlear Limited

AUD in million 2018-06 2017-06 Changes 2018-06 2017-06 Changes

Net cash used for operating

activities 1902.1 1246.6 52.58% 258.1 259.8 -0.65%

Net cash used for investing

activities -1534.1 -862.9 77.78% -55.4 -135.6 -59.14%

Net cash provided by (used

for) financing activities -371.5 -103.4 259.28% -232.7 -108.3 114.87%

(Annual report, 2017)

Other comprehensive income statement:

10

activities

(Annual report, 2017)

In case of Cochlear Limited, great increment has been seen in operating cash flows of

the business because of higher turnover. The investment level has also been reduced by the

company to manage the cash position and reduce the liquidity level of the business. The

financial activities of the business have been compared further to identify the changes into

company and a great decrement has been seen in the company because of repayment of

borrowings and huge dividend to the shareholders.

Cochlear Limited

AUD in million

2018-

06

2017-

06

2016-

06

Net cash used for operating activities 258.1 259.8 185.1

Net cash used for investing activities -55.4 -135.6 -50.1

Net cash provided by (used for)

financing activities -232.7 -108.3

-

130.89

(Annual report, 2017)

5. Comparative analysis among the companies:

On the basis of the comparison on both the companies, it has been found that the

increment in the operating cash flow of CSL limited is 52.58% which is quite higher than

cochlear limited. Further the investing level explains the better position of Cochlear limited in

order to improve the cash level of the company and the financing activities brief increased

cash outflow of both the companies (Annual report, 2018). Though, the level of Cochlear

limited is lower. It explains that the overall cash position of CSL limited is better.

CSL limited Cochlear Limited

AUD in million 2018-06 2017-06 Changes 2018-06 2017-06 Changes

Net cash used for operating

activities 1902.1 1246.6 52.58% 258.1 259.8 -0.65%

Net cash used for investing

activities -1534.1 -862.9 77.78% -55.4 -135.6 -59.14%

Net cash provided by (used

for) financing activities -371.5 -103.4 259.28% -232.7 -108.3 114.87%

(Annual report, 2017)

Other comprehensive income statement:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Finance

11

Comprehensive income statement of the business represents the items which have not

been shown in the income statement of the business. The evaluation on Comprehensive

income statement on CSL limited and COCHLEAR LIMITED is as follows:

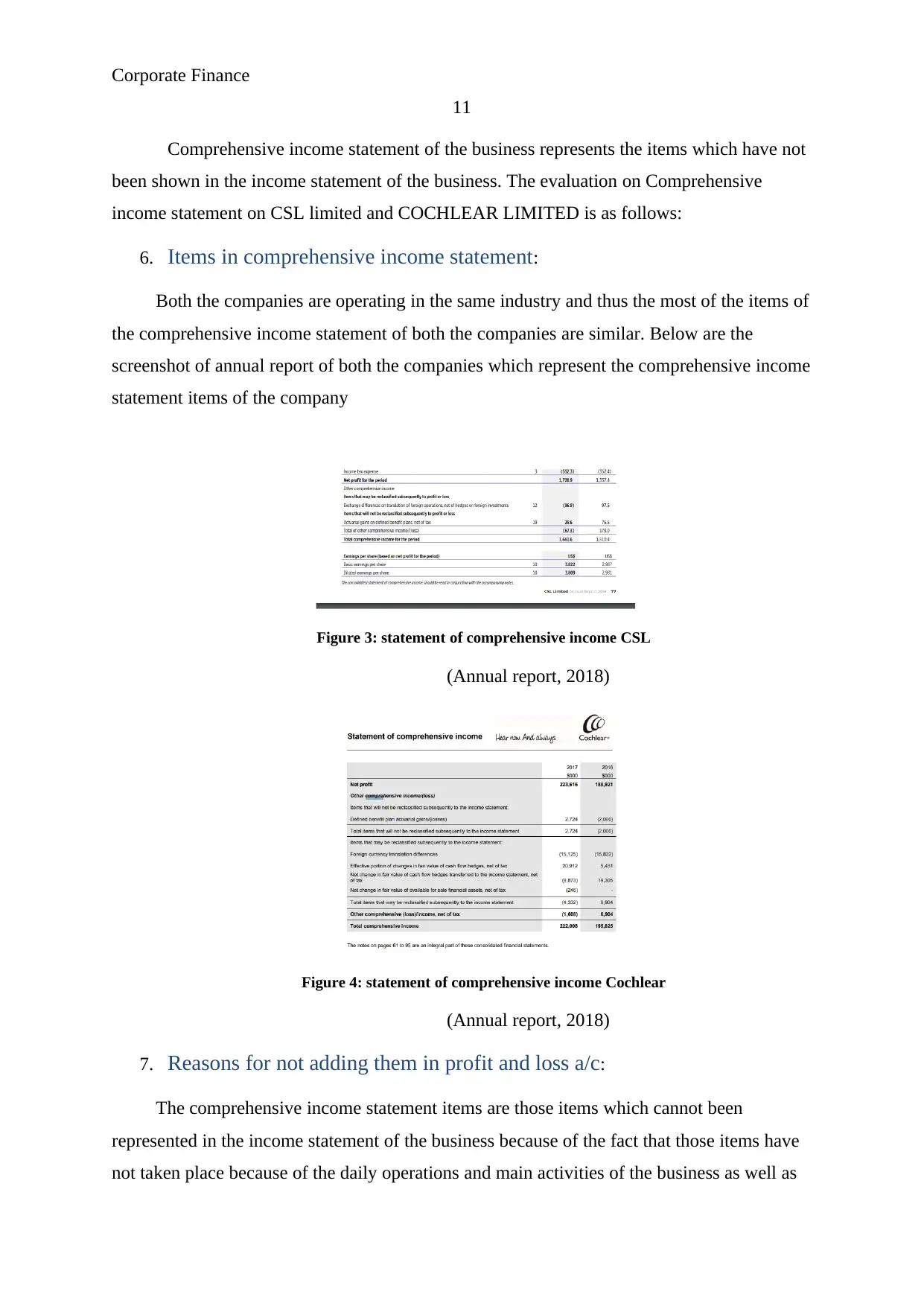

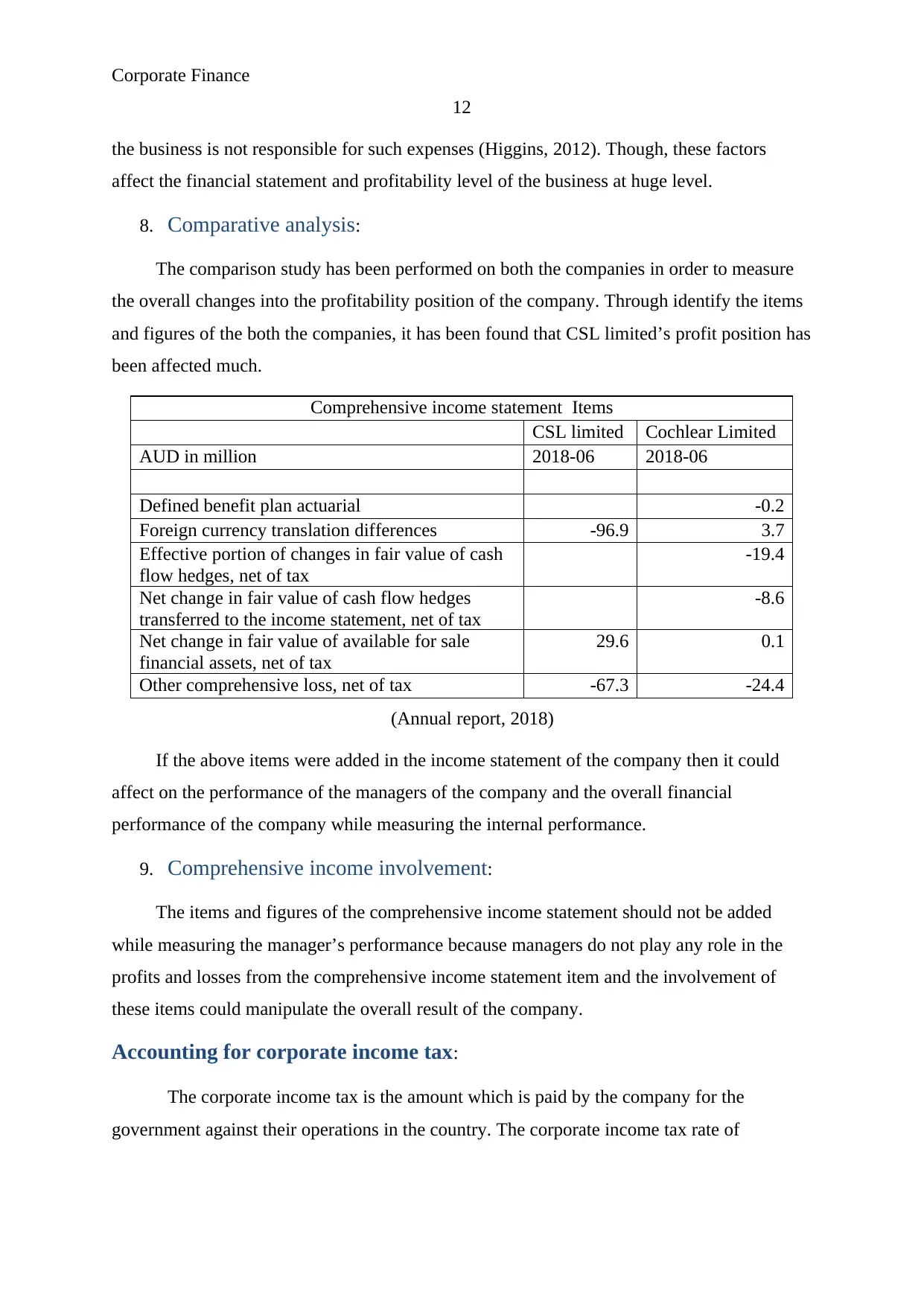

6. Items in comprehensive income statement:

Both the companies are operating in the same industry and thus the most of the items of

the comprehensive income statement of both the companies are similar. Below are the

screenshot of annual report of both the companies which represent the comprehensive income

statement items of the company

Figure 3: statement of comprehensive income CSL

(Annual report, 2018)

Figure 4: statement of comprehensive income Cochlear

(Annual report, 2018)

7. Reasons for not adding them in profit and loss a/c:

The comprehensive income statement items are those items which cannot been

represented in the income statement of the business because of the fact that those items have

not taken place because of the daily operations and main activities of the business as well as

11

Comprehensive income statement of the business represents the items which have not

been shown in the income statement of the business. The evaluation on Comprehensive

income statement on CSL limited and COCHLEAR LIMITED is as follows:

6. Items in comprehensive income statement:

Both the companies are operating in the same industry and thus the most of the items of

the comprehensive income statement of both the companies are similar. Below are the

screenshot of annual report of both the companies which represent the comprehensive income

statement items of the company

Figure 3: statement of comprehensive income CSL

(Annual report, 2018)

Figure 4: statement of comprehensive income Cochlear

(Annual report, 2018)

7. Reasons for not adding them in profit and loss a/c:

The comprehensive income statement items are those items which cannot been

represented in the income statement of the business because of the fact that those items have

not taken place because of the daily operations and main activities of the business as well as

Corporate Finance

12

the business is not responsible for such expenses (Higgins, 2012). Though, these factors

affect the financial statement and profitability level of the business at huge level.

8. Comparative analysis:

The comparison study has been performed on both the companies in order to measure

the overall changes into the profitability position of the company. Through identify the items

and figures of the both the companies, it has been found that CSL limited’s profit position has

been affected much.

Comprehensive income statement Items

CSL limited Cochlear Limited

AUD in million 2018-06 2018-06

Defined benefit plan actuarial -0.2

Foreign currency translation differences -96.9 3.7

Effective portion of changes in fair value of cash

flow hedges, net of tax

-19.4

Net change in fair value of cash flow hedges

transferred to the income statement, net of tax

-8.6

Net change in fair value of available for sale

financial assets, net of tax

29.6 0.1

Other comprehensive loss, net of tax -67.3 -24.4

(Annual report, 2018)

If the above items were added in the income statement of the company then it could

affect on the performance of the managers of the company and the overall financial

performance of the company while measuring the internal performance.

9. Comprehensive income involvement:

The items and figures of the comprehensive income statement should not be added

while measuring the manager’s performance because managers do not play any role in the

profits and losses from the comprehensive income statement item and the involvement of

these items could manipulate the overall result of the company.

Accounting for corporate income tax:

The corporate income tax is the amount which is paid by the company for the

government against their operations in the country. The corporate income tax rate of

12

the business is not responsible for such expenses (Higgins, 2012). Though, these factors

affect the financial statement and profitability level of the business at huge level.

8. Comparative analysis:

The comparison study has been performed on both the companies in order to measure

the overall changes into the profitability position of the company. Through identify the items

and figures of the both the companies, it has been found that CSL limited’s profit position has

been affected much.

Comprehensive income statement Items

CSL limited Cochlear Limited

AUD in million 2018-06 2018-06

Defined benefit plan actuarial -0.2

Foreign currency translation differences -96.9 3.7

Effective portion of changes in fair value of cash

flow hedges, net of tax

-19.4

Net change in fair value of cash flow hedges

transferred to the income statement, net of tax

-8.6

Net change in fair value of available for sale

financial assets, net of tax

29.6 0.1

Other comprehensive loss, net of tax -67.3 -24.4

(Annual report, 2018)

If the above items were added in the income statement of the company then it could

affect on the performance of the managers of the company and the overall financial

performance of the company while measuring the internal performance.

9. Comprehensive income involvement:

The items and figures of the comprehensive income statement should not be added

while measuring the manager’s performance because managers do not play any role in the

profits and losses from the comprehensive income statement item and the involvement of

these items could manipulate the overall result of the company.

Accounting for corporate income tax:

The corporate income tax is the amount which is paid by the company for the

government against their operations in the country. The corporate income tax rate of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.