Comprehensive Corporate Finance Analysis of Dechra Pharmaceuticals

VerifiedAdded on 2023/01/18

|22

|5179

|63

Report

AI Summary

This report provides a comprehensive corporate finance analysis of Dechra Pharmaceuticals, a UK-based veterinary pharmaceutical company. It begins with an introduction to corporate finance and then analyzes Dechra's current market capitalization, book value, and shareholder structure. The report delves into the company's debt-to-equity ratio, beta, and competitor information, alongside recent financial news. It examines Dechra's dividend policy, discussing its history and trends, and applies the Modigliani & Miller theories. The report calculates the Weighted Average Cost of Capital (WACC), and employs the SVA model to estimate the share value. The report further explores Dechra's recent mergers and acquisitions, focusing on potential synergies and premiums paid. Finally, the report concludes with a summary of the key findings.

Corporate Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Current Market Capitalisation of Dechra Pharmaceuticals:........................................................3

Book Value of Shareholders' fund of Dechra-Pharmaceuticals:.................................................3

Discussion on Market Value and Book Value Difference:..........................................................3

Main Shareholders of Dechra-Pharmaceuticals:..........................................................................4

Total Borrowings:........................................................................................................................5

Debt to Equity Ratio:...................................................................................................................5

Quoted Beta:................................................................................................................................6

Competitor Information:..............................................................................................................6

Recent Financial News:...............................................................................................................7

TASK 2............................................................................................................................................8

Dividend Policy:..........................................................................................................................8

Theories of Modigliani & Miller:..............................................................................................10

Practical Issues in company:......................................................................................................10

TASK 3..........................................................................................................................................11

WACC:......................................................................................................................................11

TASK 4............................................................................................................................................1

Part a) Estimation of share’s value of Dechra Pharmaceutical through SVA model..................1

Part b) Rationale for adjustment made to the particular data.......................................................3

TASK 5............................................................................................................................................5

Recent merger and acquisition by Dechra Pharmaceutical..........................................................5

Potential sources of synergy among parents and acquired company...........................................7

Premium paid for the target company..........................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Current Market Capitalisation of Dechra Pharmaceuticals:........................................................3

Book Value of Shareholders' fund of Dechra-Pharmaceuticals:.................................................3

Discussion on Market Value and Book Value Difference:..........................................................3

Main Shareholders of Dechra-Pharmaceuticals:..........................................................................4

Total Borrowings:........................................................................................................................5

Debt to Equity Ratio:...................................................................................................................5

Quoted Beta:................................................................................................................................6

Competitor Information:..............................................................................................................6

Recent Financial News:...............................................................................................................7

TASK 2............................................................................................................................................8

Dividend Policy:..........................................................................................................................8

Theories of Modigliani & Miller:..............................................................................................10

Practical Issues in company:......................................................................................................10

TASK 3..........................................................................................................................................11

WACC:......................................................................................................................................11

TASK 4............................................................................................................................................1

Part a) Estimation of share’s value of Dechra Pharmaceutical through SVA model..................1

Part b) Rationale for adjustment made to the particular data.......................................................3

TASK 5............................................................................................................................................5

Recent merger and acquisition by Dechra Pharmaceutical..........................................................5

Potential sources of synergy among parents and acquired company...........................................7

Premium paid for the target company..........................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

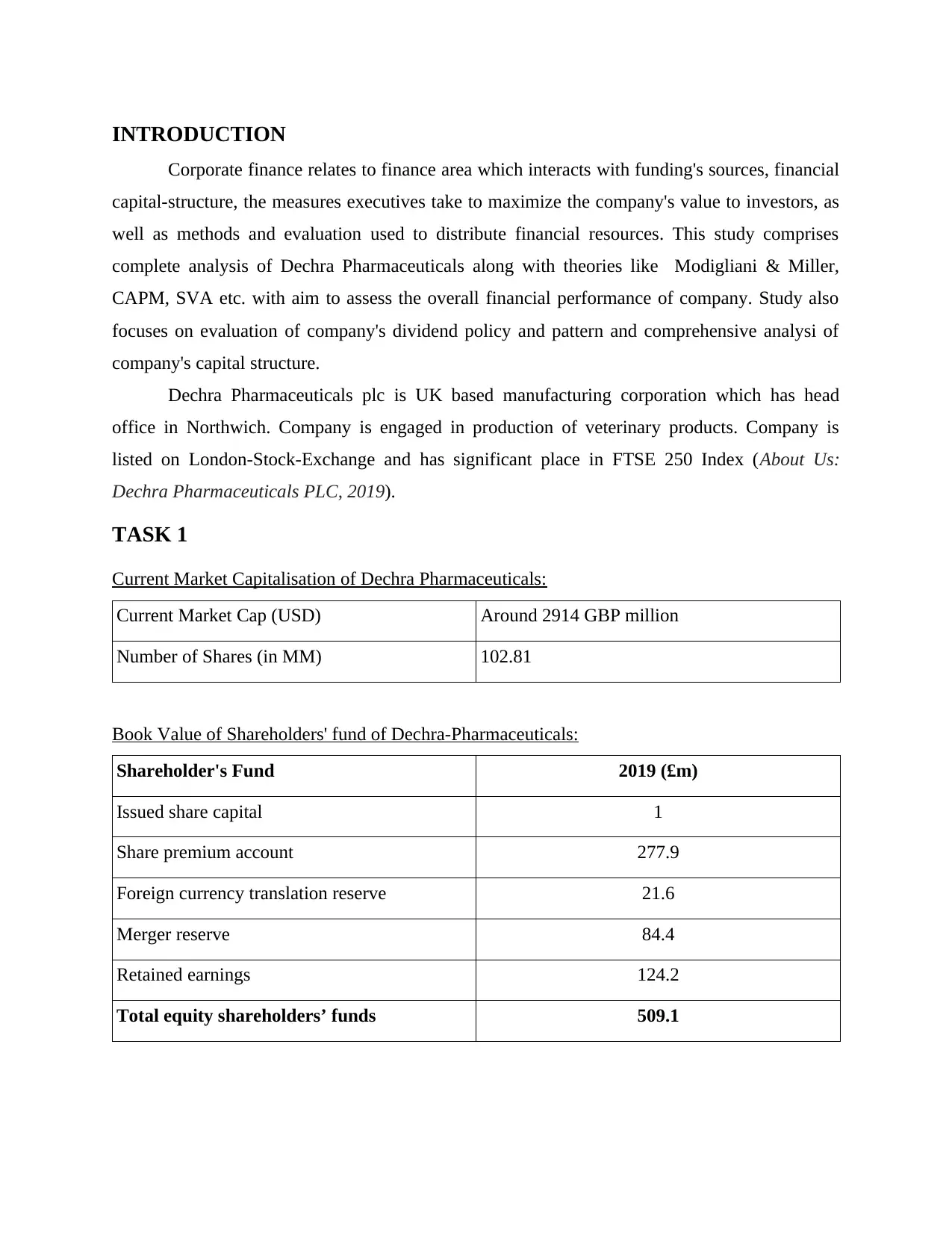

INTRODUCTION

Corporate finance relates to finance area which interacts with funding's sources, financial

capital-structure, the measures executives take to maximize the company's value to investors, as

well as methods and evaluation used to distribute financial resources. This study comprises

complete analysis of Dechra Pharmaceuticals along with theories like Modigliani & Miller,

CAPM, SVA etc. with aim to assess the overall financial performance of company. Study also

focuses on evaluation of company's dividend policy and pattern and comprehensive analysi of

company's capital structure.

Dechra Pharmaceuticals plc is UK based manufacturing corporation which has head

office in Northwich. Company is engaged in production of veterinary products. Company is

listed on London-Stock-Exchange and has significant place in FTSE 250 Index (About Us:

Dechra Pharmaceuticals PLC, 2019).

TASK 1

Current Market Capitalisation of Dechra Pharmaceuticals:

Current Market Cap (USD) Around 2914 GBP million

Number of Shares (in MM) 102.81

Book Value of Shareholders' fund of Dechra-Pharmaceuticals:

Shareholder's Fund 2019 (£m)

Issued share capital 1

Share premium account 277.9

Foreign currency translation reserve 21.6

Merger reserve 84.4

Retained earnings 124.2

Total equity shareholders’ funds 509.1

Corporate finance relates to finance area which interacts with funding's sources, financial

capital-structure, the measures executives take to maximize the company's value to investors, as

well as methods and evaluation used to distribute financial resources. This study comprises

complete analysis of Dechra Pharmaceuticals along with theories like Modigliani & Miller,

CAPM, SVA etc. with aim to assess the overall financial performance of company. Study also

focuses on evaluation of company's dividend policy and pattern and comprehensive analysi of

company's capital structure.

Dechra Pharmaceuticals plc is UK based manufacturing corporation which has head

office in Northwich. Company is engaged in production of veterinary products. Company is

listed on London-Stock-Exchange and has significant place in FTSE 250 Index (About Us:

Dechra Pharmaceuticals PLC, 2019).

TASK 1

Current Market Capitalisation of Dechra Pharmaceuticals:

Current Market Cap (USD) Around 2914 GBP million

Number of Shares (in MM) 102.81

Book Value of Shareholders' fund of Dechra-Pharmaceuticals:

Shareholder's Fund 2019 (£m)

Issued share capital 1

Share premium account 277.9

Foreign currency translation reserve 21.6

Merger reserve 84.4

Retained earnings 124.2

Total equity shareholders’ funds 509.1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Discussion on Market Value and Book Value Difference:

Book value is simple difference among total assets and external liabilities. While market

value of company is assessed by multiplying market-price of each share with aggregate number

of outstanding shares. As in case of Dechra Pharmaceuticals, book value of shareholders' fund is

498.7 which is difference between company's aggregate assets and external-liabilities while

Market value is 2914 GBP million with 102.81 million outstanding share (Annual Report of

Dechra Pharmaceuticals PLC, 2019).

Main Shareholders of Dechra-Pharmaceuticals:

A shareholder is a person or entity in a publicly or private corporation which lawfully

holds one or even more securities or shares. Shareholders can be considered as corporate

members. A corporation that retains securities in a listed corporation, like a mutual-fund,

banking or insurance corporation. It really is crucial with institutional stockholders to place new

stocks and bonds issues because they can actually afford much more of entire issue than

individual shareholders (Atanasov and Black, 2016). If majority of securities in a corporation are

held by institutional shareholders, company is considered to be under institutional control

ownership. In this context following are the main shareholders of company Dechra-

Pharmaceuticals, as follows:

Company's Main Shareholders Equities

Percentage

Holding

Fidelity Management & Research Co. 8768222 8.53%

Standard Life Investments Ltd. 5597424 5.44%

Royal London Asset Management Ltd. 4396255 4.28%

Neptune Investment Management Ltd. 4255714 4.14%

Coöperatieve Centrale Raiffeisen-Boerenleenbank

(Paris Branch) 3672000 3.57%

Book value is simple difference among total assets and external liabilities. While market

value of company is assessed by multiplying market-price of each share with aggregate number

of outstanding shares. As in case of Dechra Pharmaceuticals, book value of shareholders' fund is

498.7 which is difference between company's aggregate assets and external-liabilities while

Market value is 2914 GBP million with 102.81 million outstanding share (Annual Report of

Dechra Pharmaceuticals PLC, 2019).

Main Shareholders of Dechra-Pharmaceuticals:

A shareholder is a person or entity in a publicly or private corporation which lawfully

holds one or even more securities or shares. Shareholders can be considered as corporate

members. A corporation that retains securities in a listed corporation, like a mutual-fund,

banking or insurance corporation. It really is crucial with institutional stockholders to place new

stocks and bonds issues because they can actually afford much more of entire issue than

individual shareholders (Atanasov and Black, 2016). If majority of securities in a corporation are

held by institutional shareholders, company is considered to be under institutional control

ownership. In this context following are the main shareholders of company Dechra-

Pharmaceuticals, as follows:

Company's Main Shareholders Equities

Percentage

Holding

Fidelity Management & Research Co. 8768222 8.53%

Standard Life Investments Ltd. 5597424 5.44%

Royal London Asset Management Ltd. 4396255 4.28%

Neptune Investment Management Ltd. 4255714 4.14%

Coöperatieve Centrale Raiffeisen-Boerenleenbank

(Paris Branch) 3672000 3.57%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

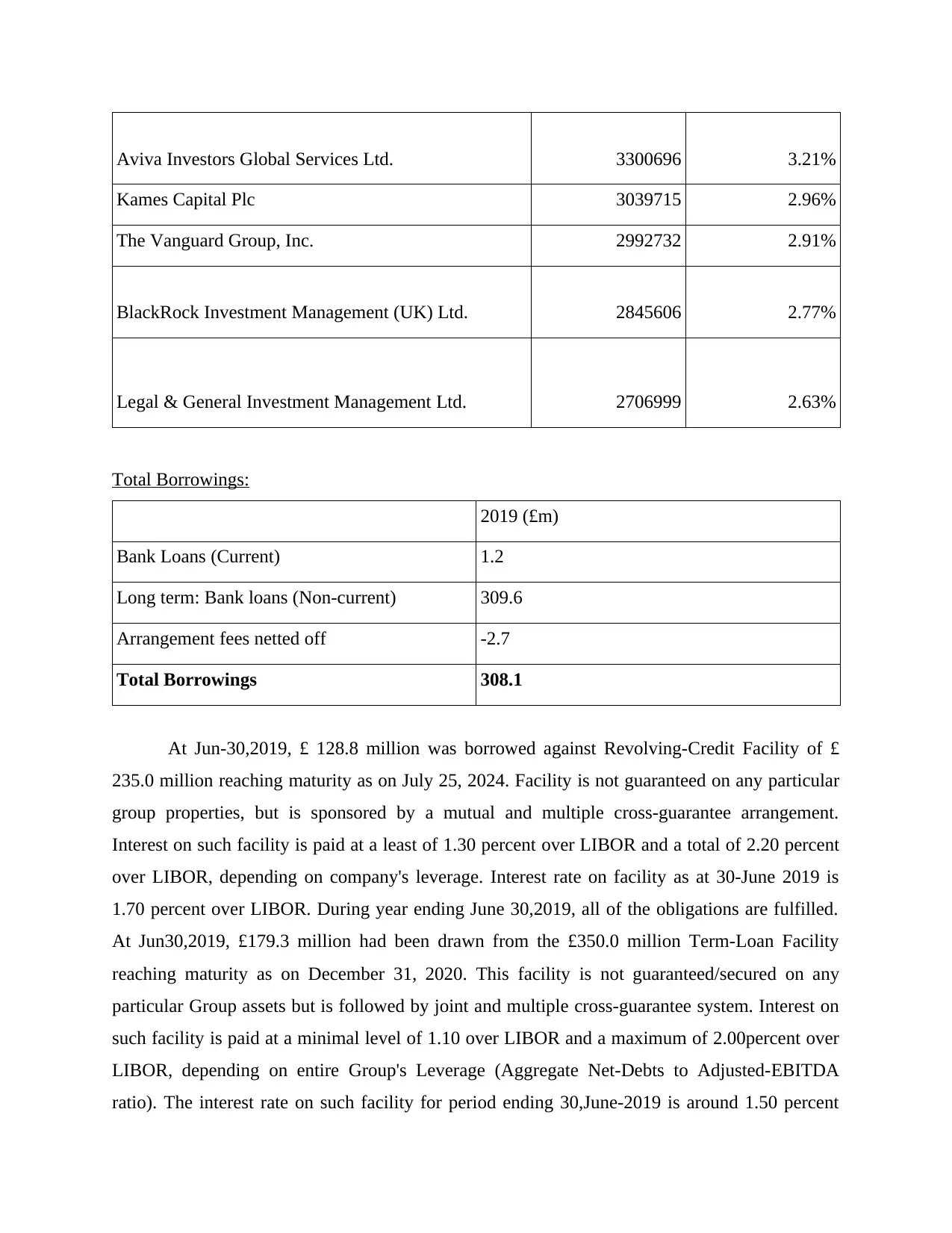

Aviva Investors Global Services Ltd. 3300696 3.21%

Kames Capital Plc 3039715 2.96%

The Vanguard Group, Inc. 2992732 2.91%

BlackRock Investment Management (UK) Ltd. 2845606 2.77%

Legal & General Investment Management Ltd. 2706999 2.63%

Total Borrowings:

2019 (£m)

Bank Loans (Current) 1.2

Long term: Bank loans (Non-current) 309.6

Arrangement fees netted off -2.7

Total Borrowings 308.1

At Jun-30,2019, £ 128.8 million was borrowed against Revolving-Credit Facility of £

235.0 million reaching maturity as on July 25, 2024. Facility is not guaranteed on any particular

group properties, but is sponsored by a mutual and multiple cross-guarantee arrangement.

Interest on such facility is paid at a least of 1.30 percent over LIBOR and a total of 2.20 percent

over LIBOR, depending on company's leverage. Interest rate on facility as at 30-June 2019 is

1.70 percent over LIBOR. During year ending June 30,2019, all of the obligations are fulfilled.

At Jun30,2019, £179.3 million had been drawn from the £350.0 million Term-Loan Facility

reaching maturity as on December 31, 2020. This facility is not guaranteed/secured on any

particular Group assets but is followed by joint and multiple cross-guarantee system. Interest on

such facility is paid at a minimal level of 1.10 over LIBOR and a maximum of 2.00percent over

LIBOR, depending on entire Group's Leverage (Aggregate Net-Debts to Adjusted-EBITDA

ratio). The interest rate on such facility for period ending 30,June-2019 is around 1.50 percent

Kames Capital Plc 3039715 2.96%

The Vanguard Group, Inc. 2992732 2.91%

BlackRock Investment Management (UK) Ltd. 2845606 2.77%

Legal & General Investment Management Ltd. 2706999 2.63%

Total Borrowings:

2019 (£m)

Bank Loans (Current) 1.2

Long term: Bank loans (Non-current) 309.6

Arrangement fees netted off -2.7

Total Borrowings 308.1

At Jun-30,2019, £ 128.8 million was borrowed against Revolving-Credit Facility of £

235.0 million reaching maturity as on July 25, 2024. Facility is not guaranteed on any particular

group properties, but is sponsored by a mutual and multiple cross-guarantee arrangement.

Interest on such facility is paid at a least of 1.30 percent over LIBOR and a total of 2.20 percent

over LIBOR, depending on company's leverage. Interest rate on facility as at 30-June 2019 is

1.70 percent over LIBOR. During year ending June 30,2019, all of the obligations are fulfilled.

At Jun30,2019, £179.3 million had been drawn from the £350.0 million Term-Loan Facility

reaching maturity as on December 31, 2020. This facility is not guaranteed/secured on any

particular Group assets but is followed by joint and multiple cross-guarantee system. Interest on

such facility is paid at a minimal level of 1.10 over LIBOR and a maximum of 2.00percent over

LIBOR, depending on entire Group's Leverage (Aggregate Net-Debts to Adjusted-EBITDA

ratio). The interest rate on such facility for period ending 30,June-2019 is around 1.50 percent

over LIBOR. During period ending June 30th-2019, all clauses are fulfilled. The Term-Loan

Facility's maturity period will end on 31st Dec.-2020.

Debt to Equity Ratio:

Year 2019 (£m) Based on Book Value Based on Market Value

Debts 539.4 539.4

Equity 509.1 2914

1.0595 0.1851

As presented in table, Dechra-Pharmaceuticals' debt to equity ratio in year 2018 based on

book value is 1.0595 while based on market value this ratio is just 0.1851 which shows that

company is financially stable as its market-based debt-to-equity ratio is below one. Company is

able to discharge all its obligations and debts though its market value of equity. While book

value of equity is not adequate to pay out its all debts and obligations.

Quoted Beta:

Beta is correlation of anticipated excess return on capital to projected excessive returns on

market. Company Dechra Pharmaceuticals' quoted beta is 0.53 (Beta of Dechra Pharmaceuticals

PLC. 2019).

Competitor Information:

Shire Otonomy Zoetis Kindred

Description Biopharmaceutica

l company

biopharmaceutica

l corporation

engaged in

development and

Producer of

medicinal drug

and vaccinations

for pets and

Veterinary

biotechnology

corporation which

focuses on

Facility's maturity period will end on 31st Dec.-2020.

Debt to Equity Ratio:

Year 2019 (£m) Based on Book Value Based on Market Value

Debts 539.4 539.4

Equity 509.1 2914

1.0595 0.1851

As presented in table, Dechra-Pharmaceuticals' debt to equity ratio in year 2018 based on

book value is 1.0595 while based on market value this ratio is just 0.1851 which shows that

company is financially stable as its market-based debt-to-equity ratio is below one. Company is

able to discharge all its obligations and debts though its market value of equity. While book

value of equity is not adequate to pay out its all debts and obligations.

Quoted Beta:

Beta is correlation of anticipated excess return on capital to projected excessive returns on

market. Company Dechra Pharmaceuticals' quoted beta is 0.53 (Beta of Dechra Pharmaceuticals

PLC. 2019).

Competitor Information:

Shire Otonomy Zoetis Kindred

Description Biopharmaceutica

l company

biopharmaceutica

l corporation

engaged in

development and

Producer of

medicinal drug

and vaccinations

for pets and

Veterinary

biotechnology

corporation which

focuses on

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

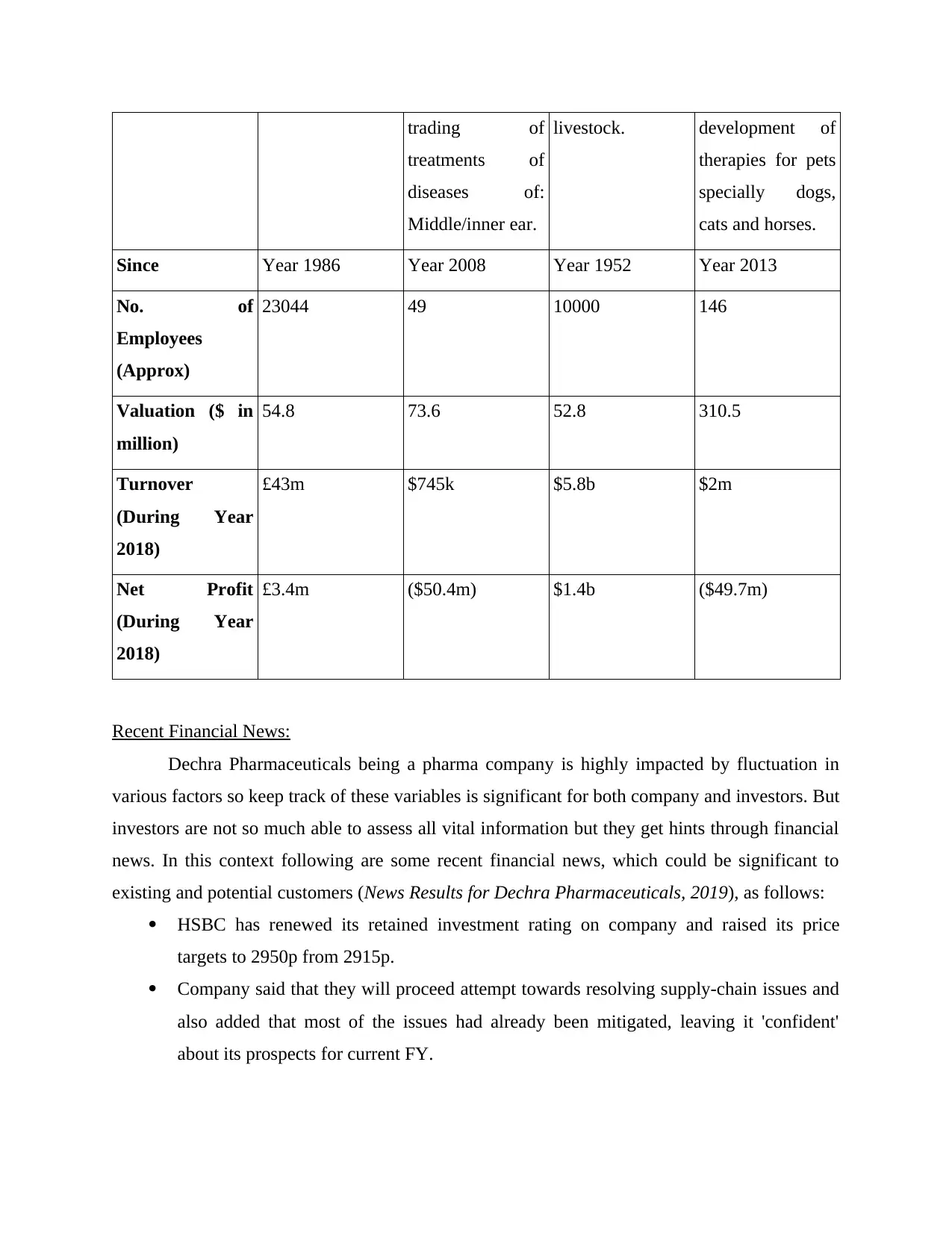

trading of

treatments of

diseases of:

Middle/inner ear.

livestock. development of

therapies for pets

specially dogs,

cats and horses.

Since Year 1986 Year 2008 Year 1952 Year 2013

No. of

Employees

(Approx)

23044 49 10000 146

Valuation ($ in

million)

54.8 73.6 52.8 310.5

Turnover

(During Year

2018)

£43m $745k $5.8b $2m

Net Profit

(During Year

2018)

£3.4m ($50.4m) $1.4b ($49.7m)

Recent Financial News:

Dechra Pharmaceuticals being a pharma company is highly impacted by fluctuation in

various factors so keep track of these variables is significant for both company and investors. But

investors are not so much able to assess all vital information but they get hints through financial

news. In this context following are some recent financial news, which could be significant to

existing and potential customers (News Results for Dechra Pharmaceuticals, 2019), as follows:

HSBC has renewed its retained investment rating on company and raised its price

targets to 2950p from 2915p.

Company said that they will proceed attempt towards resolving supply-chain issues and

also added that most of the issues had already been mitigated, leaving it 'confident'

about its prospects for current FY.

treatments of

diseases of:

Middle/inner ear.

livestock. development of

therapies for pets

specially dogs,

cats and horses.

Since Year 1986 Year 2008 Year 1952 Year 2013

No. of

Employees

(Approx)

23044 49 10000 146

Valuation ($ in

million)

54.8 73.6 52.8 310.5

Turnover

(During Year

2018)

£43m $745k $5.8b $2m

Net Profit

(During Year

2018)

£3.4m ($50.4m) $1.4b ($49.7m)

Recent Financial News:

Dechra Pharmaceuticals being a pharma company is highly impacted by fluctuation in

various factors so keep track of these variables is significant for both company and investors. But

investors are not so much able to assess all vital information but they get hints through financial

news. In this context following are some recent financial news, which could be significant to

existing and potential customers (News Results for Dechra Pharmaceuticals, 2019), as follows:

HSBC has renewed its retained investment rating on company and raised its price

targets to 2950p from 2915p.

Company said that they will proceed attempt towards resolving supply-chain issues and

also added that most of the issues had already been mitigated, leaving it 'confident'

about its prospects for current FY.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

On 19-Sep. 2019 Chief Executive Officer of company Lan Page has exercised

73,260shares at price of 0.00p and holding reached to 659,910 shares. And on 20th

September 2019, he has sold post-exercise 34,536shares at price of around 2789.37p.

Dechra Pharmaceutical announced a small decrease in earnings, even though the

animal-drug manufacturer outperformed in markets, including United States, where

organic-growth was extraordinary.

TASK 2

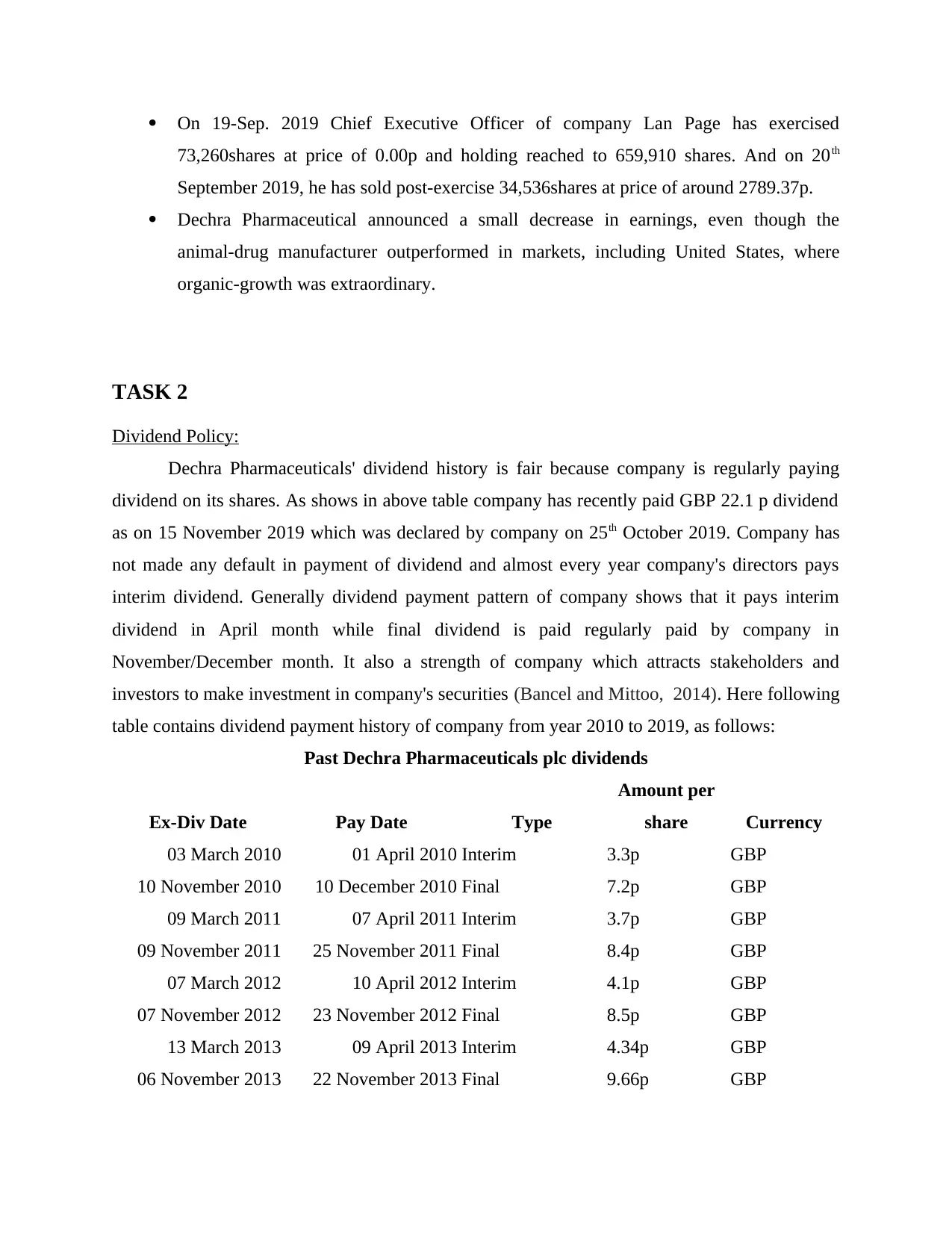

Dividend Policy:

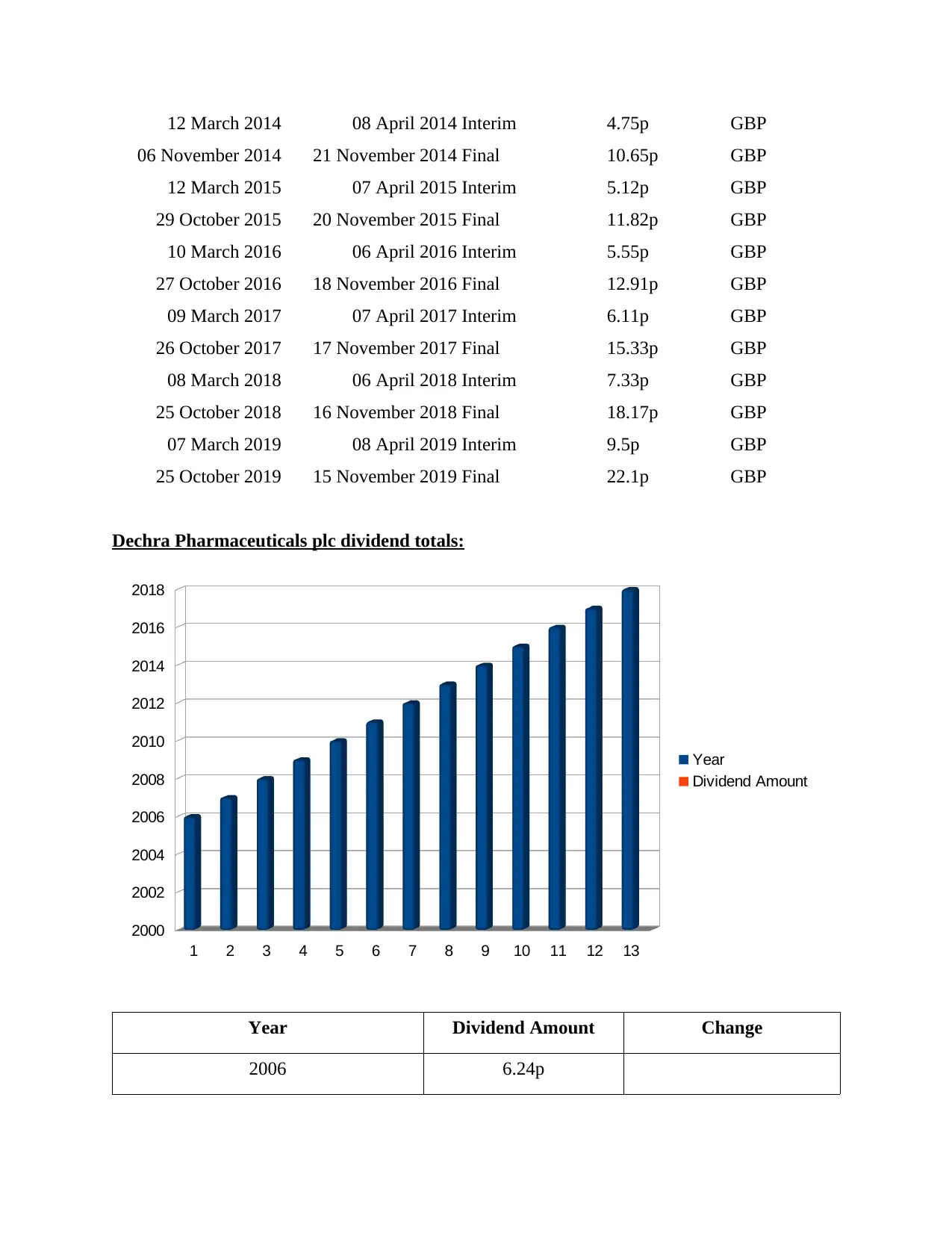

Dechra Pharmaceuticals' dividend history is fair because company is regularly paying

dividend on its shares. As shows in above table company has recently paid GBP 22.1 p dividend

as on 15 November 2019 which was declared by company on 25th October 2019. Company has

not made any default in payment of dividend and almost every year company's directors pays

interim dividend. Generally dividend payment pattern of company shows that it pays interim

dividend in April month while final dividend is paid regularly paid by company in

November/December month. It also a strength of company which attracts stakeholders and

investors to make investment in company's securities (Bancel and Mittoo, 2014). Here following

table contains dividend payment history of company from year 2010 to 2019, as follows:

Past Dechra Pharmaceuticals plc dividends

Ex-Div Date Pay Date Type

Amount per

share Currency

03 March 2010 01 April 2010 Interim 3.3p GBP

10 November 2010 10 December 2010 Final 7.2p GBP

09 March 2011 07 April 2011 Interim 3.7p GBP

09 November 2011 25 November 2011 Final 8.4p GBP

07 March 2012 10 April 2012 Interim 4.1p GBP

07 November 2012 23 November 2012 Final 8.5p GBP

13 March 2013 09 April 2013 Interim 4.34p GBP

06 November 2013 22 November 2013 Final 9.66p GBP

73,260shares at price of 0.00p and holding reached to 659,910 shares. And on 20th

September 2019, he has sold post-exercise 34,536shares at price of around 2789.37p.

Dechra Pharmaceutical announced a small decrease in earnings, even though the

animal-drug manufacturer outperformed in markets, including United States, where

organic-growth was extraordinary.

TASK 2

Dividend Policy:

Dechra Pharmaceuticals' dividend history is fair because company is regularly paying

dividend on its shares. As shows in above table company has recently paid GBP 22.1 p dividend

as on 15 November 2019 which was declared by company on 25th October 2019. Company has

not made any default in payment of dividend and almost every year company's directors pays

interim dividend. Generally dividend payment pattern of company shows that it pays interim

dividend in April month while final dividend is paid regularly paid by company in

November/December month. It also a strength of company which attracts stakeholders and

investors to make investment in company's securities (Bancel and Mittoo, 2014). Here following

table contains dividend payment history of company from year 2010 to 2019, as follows:

Past Dechra Pharmaceuticals plc dividends

Ex-Div Date Pay Date Type

Amount per

share Currency

03 March 2010 01 April 2010 Interim 3.3p GBP

10 November 2010 10 December 2010 Final 7.2p GBP

09 March 2011 07 April 2011 Interim 3.7p GBP

09 November 2011 25 November 2011 Final 8.4p GBP

07 March 2012 10 April 2012 Interim 4.1p GBP

07 November 2012 23 November 2012 Final 8.5p GBP

13 March 2013 09 April 2013 Interim 4.34p GBP

06 November 2013 22 November 2013 Final 9.66p GBP

12 March 2014 08 April 2014 Interim 4.75p GBP

06 November 2014 21 November 2014 Final 10.65p GBP

12 March 2015 07 April 2015 Interim 5.12p GBP

29 October 2015 20 November 2015 Final 11.82p GBP

10 March 2016 06 April 2016 Interim 5.55p GBP

27 October 2016 18 November 2016 Final 12.91p GBP

09 March 2017 07 April 2017 Interim 6.11p GBP

26 October 2017 17 November 2017 Final 15.33p GBP

08 March 2018 06 April 2018 Interim 7.33p GBP

25 October 2018 16 November 2018 Final 18.17p GBP

07 March 2019 08 April 2019 Interim 9.5p GBP

25 October 2019 15 November 2019 Final 22.1p GBP

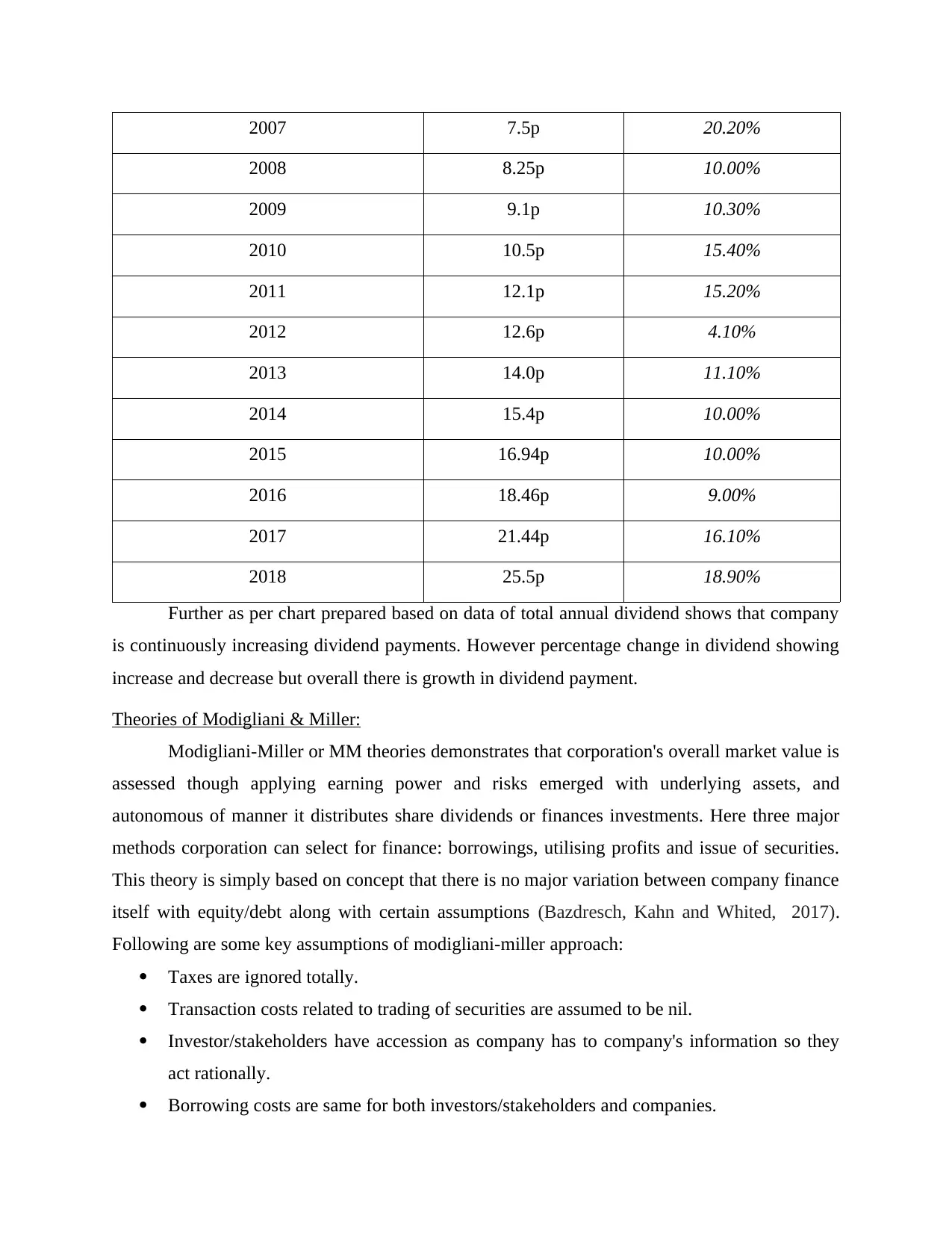

Dechra Pharmaceuticals plc dividend totals:

Year Dividend Amount Change

2006 6.24p

1 2 3 4 5 6 7 8 9 10 11 12 13

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

Year

Dividend Amount

06 November 2014 21 November 2014 Final 10.65p GBP

12 March 2015 07 April 2015 Interim 5.12p GBP

29 October 2015 20 November 2015 Final 11.82p GBP

10 March 2016 06 April 2016 Interim 5.55p GBP

27 October 2016 18 November 2016 Final 12.91p GBP

09 March 2017 07 April 2017 Interim 6.11p GBP

26 October 2017 17 November 2017 Final 15.33p GBP

08 March 2018 06 April 2018 Interim 7.33p GBP

25 October 2018 16 November 2018 Final 18.17p GBP

07 March 2019 08 April 2019 Interim 9.5p GBP

25 October 2019 15 November 2019 Final 22.1p GBP

Dechra Pharmaceuticals plc dividend totals:

Year Dividend Amount Change

2006 6.24p

1 2 3 4 5 6 7 8 9 10 11 12 13

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

Year

Dividend Amount

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2007 7.5p 20.20%

2008 8.25p 10.00%

2009 9.1p 10.30%

2010 10.5p 15.40%

2011 12.1p 15.20%

2012 12.6p 4.10%

2013 14.0p 11.10%

2014 15.4p 10.00%

2015 16.94p 10.00%

2016 18.46p 9.00%

2017 21.44p 16.10%

2018 25.5p 18.90%

Further as per chart prepared based on data of total annual dividend shows that company

is continuously increasing dividend payments. However percentage change in dividend showing

increase and decrease but overall there is growth in dividend payment.

Theories of Modigliani & Miller:

Modigliani-Miller or MM theories demonstrates that corporation's overall market value is

assessed though applying earning power and risks emerged with underlying assets, and

autonomous of manner it distributes share dividends or finances investments. Here three major

methods corporation can select for finance: borrowings, utilising profits and issue of securities.

This theory is simply based on concept that there is no major variation between company finance

itself with equity/debt along with certain assumptions (Bazdresch, Kahn and Whited, 2017).

Following are some key assumptions of modigliani-miller approach:

Taxes are ignored totally.

Transaction costs related to trading of securities are assumed to be nil.

Investor/stakeholders have accession as company has to company's information so they

act rationally.

Borrowing costs are same for both investors/stakeholders and companies.

2008 8.25p 10.00%

2009 9.1p 10.30%

2010 10.5p 15.40%

2011 12.1p 15.20%

2012 12.6p 4.10%

2013 14.0p 11.10%

2014 15.4p 10.00%

2015 16.94p 10.00%

2016 18.46p 9.00%

2017 21.44p 16.10%

2018 25.5p 18.90%

Further as per chart prepared based on data of total annual dividend shows that company

is continuously increasing dividend payments. However percentage change in dividend showing

increase and decrease but overall there is growth in dividend payment.

Theories of Modigliani & Miller:

Modigliani-Miller or MM theories demonstrates that corporation's overall market value is

assessed though applying earning power and risks emerged with underlying assets, and

autonomous of manner it distributes share dividends or finances investments. Here three major

methods corporation can select for finance: borrowings, utilising profits and issue of securities.

This theory is simply based on concept that there is no major variation between company finance

itself with equity/debt along with certain assumptions (Bazdresch, Kahn and Whited, 2017).

Following are some key assumptions of modigliani-miller approach:

Taxes are ignored totally.

Transaction costs related to trading of securities are assumed to be nil.

Investor/stakeholders have accession as company has to company's information so they

act rationally.

Borrowing costs are same for both investors/stakeholders and companies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Floatation cost is considered as nil like underwriting commissions, expenses towards

merchant bankers, promotional expenses etc.

Also here no corporate-dividend tax exists.

As in case of Dechra Pharmaceuticals this theory points that value of leveraged-company

has both debts and equities, is same if company is considered as unleveraged by considering only

equity when overall operating profits and future projection are matched. Company's capital

structure is proper and company is leveraged-firm which has both debt funds and equity funds

(Berg, Saunders and Steffen, 2016).

Practical Issues in company:

During September-2019 month after publishing full-year outcomes/results about

performance company indicated that it is struggling with supply-chain problems at several sites

or units and with contract-manufacturers. As company has wider range of distributors and

suppliers along with contractual manufacture, managing and tracking them is tuff task for

company. In several units company's inventories are lost, improper supply and excessive storage

which is directly affecting company's operating cost. Company is also faced problem of shortage

of supply which impacted company's sales in respective area.

TASK 3

WACC:

Weighted Average Cost-of-capital or WACC implies to assessment of corporation's cost

of capital whereby each class or form of capital is proportionally classified or weighted. Origin

of capital involves company's common stocks, preferred stocks, bond issued and other long-term

debts are generally used in WACC computation (Damodaran, 2016). With increment in WACC

percent, company's beta as well as return percentage on equity employed also increases since

increment in WACC leads to decline in company's valuation and increment in involved risk.

Following is key formula for deriving WACC, as follows:

WACC = VE x Re + VD x Rd x (1− t)

Here in in above formula:

Re (%) = Cost-of equity

Rd (%) = Cost-of debt

E indicates to Market-value of corporation's equity

merchant bankers, promotional expenses etc.

Also here no corporate-dividend tax exists.

As in case of Dechra Pharmaceuticals this theory points that value of leveraged-company

has both debts and equities, is same if company is considered as unleveraged by considering only

equity when overall operating profits and future projection are matched. Company's capital

structure is proper and company is leveraged-firm which has both debt funds and equity funds

(Berg, Saunders and Steffen, 2016).

Practical Issues in company:

During September-2019 month after publishing full-year outcomes/results about

performance company indicated that it is struggling with supply-chain problems at several sites

or units and with contract-manufacturers. As company has wider range of distributors and

suppliers along with contractual manufacture, managing and tracking them is tuff task for

company. In several units company's inventories are lost, improper supply and excessive storage

which is directly affecting company's operating cost. Company is also faced problem of shortage

of supply which impacted company's sales in respective area.

TASK 3

WACC:

Weighted Average Cost-of-capital or WACC implies to assessment of corporation's cost

of capital whereby each class or form of capital is proportionally classified or weighted. Origin

of capital involves company's common stocks, preferred stocks, bond issued and other long-term

debts are generally used in WACC computation (Damodaran, 2016). With increment in WACC

percent, company's beta as well as return percentage on equity employed also increases since

increment in WACC leads to decline in company's valuation and increment in involved risk.

Following is key formula for deriving WACC, as follows:

WACC = VE x Re + VD x Rd x (1− t)

Here in in above formula:

Re (%) = Cost-of equity

Rd (%) = Cost-of debt

E indicates to Market-value of corporation's equity

D is Market-value of the corporation's debt

V => E+D => Aggregate market-value of company's capital structure

E/V = % of financing through equity

D/V = % of financing though debt

t = Average Tax Rate

Cost of Debt: It simply regarded as rate or percentage a corporation pays against its overall

debts, like term loans, bonds. Crucial difference in cost-of-debt and cost-of-debt(after-tax) is

concept that interest-costs are tax-deductible. It is denoted by Rd and for computation of it

company's average interest rate is assessed first (Dang and Yang, 2018). Following is

computation of cost of debt of company Dechra Pharmaceuticals, as follows:

Interest expense (As of June,2019) = $ 13.3079847909 Million

While company's overall Book Value of Debt (D)= $ 388.797680204 Million

Cost of Debt = 13.3079847909/ 388.797680204

= 3.4229%.

Cost of Equity: It relates to return in percentage form a corporation requires to determine in case

investments meets targets of capital return. Corporation generally apply it as tool of capital

budgeting with respect to required/expected rate of return. Corporation's cost-of-equity shows

compensation market-demands with exchange for asset and ownership-risk. Generally CAPM

model is applied to assess the cost of equity (Dang and Shin, 2015). Following is formula for

deriving cost-of equity as follows:

Cost of Equity = Rf (Risk-Free Rate of Return) + Beta of Asset * (Expected Return of the

Market - Risk-Free Rate of Return)

In this context here is the computation of cost-of-equity of Dechra Pharmaceuticals, as follows:

Current risk-free rate = 0.63730000%

Beta = 0.53

Market Premium or (Expected Return of the Market - Risk-Free Rate of Return)= 6%

Cost of Equity = 0.63730000% + 0.53 * 6% = 3.8173%

Based on the outcomes of cost-of-debt and cost of equity following is computation of WACC of

Dechra Pharmaceuticals, as follows:

Weighted equity = E/(E +D) = 3686.796 / (3686.796 + 388.797680204) = 0.9046

Weighted debt = D /(E +D) = 388.797680204 / (3686.796} + 388.797680204) = 0.0954

V => E+D => Aggregate market-value of company's capital structure

E/V = % of financing through equity

D/V = % of financing though debt

t = Average Tax Rate

Cost of Debt: It simply regarded as rate or percentage a corporation pays against its overall

debts, like term loans, bonds. Crucial difference in cost-of-debt and cost-of-debt(after-tax) is

concept that interest-costs are tax-deductible. It is denoted by Rd and for computation of it

company's average interest rate is assessed first (Dang and Yang, 2018). Following is

computation of cost of debt of company Dechra Pharmaceuticals, as follows:

Interest expense (As of June,2019) = $ 13.3079847909 Million

While company's overall Book Value of Debt (D)= $ 388.797680204 Million

Cost of Debt = 13.3079847909/ 388.797680204

= 3.4229%.

Cost of Equity: It relates to return in percentage form a corporation requires to determine in case

investments meets targets of capital return. Corporation generally apply it as tool of capital

budgeting with respect to required/expected rate of return. Corporation's cost-of-equity shows

compensation market-demands with exchange for asset and ownership-risk. Generally CAPM

model is applied to assess the cost of equity (Dang and Shin, 2015). Following is formula for

deriving cost-of equity as follows:

Cost of Equity = Rf (Risk-Free Rate of Return) + Beta of Asset * (Expected Return of the

Market - Risk-Free Rate of Return)

In this context here is the computation of cost-of-equity of Dechra Pharmaceuticals, as follows:

Current risk-free rate = 0.63730000%

Beta = 0.53

Market Premium or (Expected Return of the Market - Risk-Free Rate of Return)= 6%

Cost of Equity = 0.63730000% + 0.53 * 6% = 3.8173%

Based on the outcomes of cost-of-debt and cost of equity following is computation of WACC of

Dechra Pharmaceuticals, as follows:

Weighted equity = E/(E +D) = 3686.796 / (3686.796 + 388.797680204) = 0.9046

Weighted debt = D /(E +D) = 388.797680204 / (3686.796} + 388.797680204) = 0.0954

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.