Corporate Finance Decision Making

VerifiedAdded on 2019/12/03

|14

|2774

|29

Report

AI Summary

This report provides a comprehensive analysis of corporate finance and decision-making for General Sportswear, a private limited company facing liquidity issues. It examines various sources of finance (long-term and short-term), analyzes the cost implications of different financing options, and assesses the financial information needs of key stakeholders (shareholders, suppliers, and customers). The report includes a detailed cash budget, unit cost calculations for products, and project appraisal using payback period, net present value, and accounting rate of return methods. Furthermore, it compares the formats of financial statements for different business structures (manufacturer, sole trader, limited company) and interprets financial performance using ratio analysis, including return on capital employed, total asset turnover, gross profit ratio, net profit ratio, current ratio, quick ratio, inventory holding period, debtor's collection period, creditor's payment period, and debt-to-equity ratio. The analysis reveals that while the company generates a relatively high return on capital employed, its high debt-to-equity ratio poses a potential risk. The report concludes by emphasizing the importance of effective financial planning and cost control for improved business performance.

Corporate finance and

decision making

decision making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Sources of finance .................................................................................................................3

1.2 Implication of sources of finance...........................................................................................3

1.3Appropriate sources of finance...............................................................................................3

TASK 2............................................................................................................................................4

2.1 Analyze cost of different sources of finance..........................................................................4

2.2 Importance of finance planning.............................................................................................4

2.3 Assessing financial information needs of three main decision makers................................4

2.4 Impact of finance on financial statement...............................................................................5

TASK 3............................................................................................................................................5

3.1 Preparing cash budget............................................................................................................5

3.2 Unit cost of products..............................................................................................................5

3.3 Calculating cost of each project.............................................................................................6

TASK 4............................................................................................................................................7

4.1 Main financial statements......................................................................................................7

4.2 Compare appropriate formats of financial statements...........................................................7

4.3 Interpreting financial statements using ratio analysis..........................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Sources of finance .................................................................................................................3

1.2 Implication of sources of finance...........................................................................................3

1.3Appropriate sources of finance...............................................................................................3

TASK 2............................................................................................................................................4

2.1 Analyze cost of different sources of finance..........................................................................4

2.2 Importance of finance planning.............................................................................................4

2.3 Assessing financial information needs of three main decision makers................................4

2.4 Impact of finance on financial statement...............................................................................5

TASK 3............................................................................................................................................5

3.1 Preparing cash budget............................................................................................................5

3.2 Unit cost of products..............................................................................................................5

3.3 Calculating cost of each project.............................................................................................6

TASK 4............................................................................................................................................7

4.1 Main financial statements......................................................................................................7

4.2 Compare appropriate formats of financial statements...........................................................7

4.3 Interpreting financial statements using ratio analysis..........................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

2

ILLUSTRATION INDEX

Illustration 1: Income statement of manufacturer............................................................................8

Illustration 2: Income statement for sole trader...............................................................................9

Illustration 3: Balance sheet of limited company..........................................................................10

INDEX OF TABLES

Table 1: Cash budget.......................................................................................................................6

Table 2: Unit cost of products..........................................................................................................6

Table 3: Payback period...................................................................................................................7

Table 4: Net present value of project 1 & 2.....................................................................................7

Table 5: ARR of project 1 & 2.........................................................................................................7

Table 6: Ratio analysis...................................................................................................................11

3

Illustration 1: Income statement of manufacturer............................................................................8

Illustration 2: Income statement for sole trader...............................................................................9

Illustration 3: Balance sheet of limited company..........................................................................10

INDEX OF TABLES

Table 1: Cash budget.......................................................................................................................6

Table 2: Unit cost of products..........................................................................................................6

Table 3: Payback period...................................................................................................................7

Table 4: Net present value of project 1 & 2.....................................................................................7

Table 5: ARR of project 1 & 2.........................................................................................................7

Table 6: Ratio analysis...................................................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management of financial resources is crucial task by which company integrate all

business activities in the direction of growth and success of the firm. Present report is based on

General Sportswear private limited company which deals in sportswear of leading brands.

Corporation is having issues related to liquidity crunch and heavy overdraft. In this regard

various cost effective sources of finance are mentioned in the report. Further, budgeting and

costing as effective techniques to control cash and increase profitability have been explained.

TASK 1

1.1 Sources of finance

There are following sources of finance available for General Sportswear-

Long term

The long term sources of finance consists of bank loan, leasing companies and hire

purchase. It aids to expand business and raise long term capital in the direction of growth and

success of the corporation.

Short term

Short term sources of finance consists of retained profit, personal savings and sale of old

assets. It enables management to meet short term requirement of business and ensure consistent

flow of production (Barton, 2001).

1.2 Implication of sources of finance

As per the given scenario, it has been found that directors of General Sportswear were not

in favor of debt finance. They assumed that it merely increases cost whereby profitability go

down. This is because company has to pay cost of finance to out side party. At this juncture, it is

not important that whether corporation is getting profitability or not. This affect performance to a

great extent (Bhowmik and Saha, 2013). For example, if loan is taken by firm then management

need to pay its interest on right time. Also, principle amount need to be paid within stipulated

time.

1.3Appropriate sources of finance

According to the case study General Sportswear is planning to expand in the marketplace.

In this regard appropriate sources of finance are retained profit, leasing companies. It helps to

4

Management of financial resources is crucial task by which company integrate all

business activities in the direction of growth and success of the firm. Present report is based on

General Sportswear private limited company which deals in sportswear of leading brands.

Corporation is having issues related to liquidity crunch and heavy overdraft. In this regard

various cost effective sources of finance are mentioned in the report. Further, budgeting and

costing as effective techniques to control cash and increase profitability have been explained.

TASK 1

1.1 Sources of finance

There are following sources of finance available for General Sportswear-

Long term

The long term sources of finance consists of bank loan, leasing companies and hire

purchase. It aids to expand business and raise long term capital in the direction of growth and

success of the corporation.

Short term

Short term sources of finance consists of retained profit, personal savings and sale of old

assets. It enables management to meet short term requirement of business and ensure consistent

flow of production (Barton, 2001).

1.2 Implication of sources of finance

As per the given scenario, it has been found that directors of General Sportswear were not

in favor of debt finance. They assumed that it merely increases cost whereby profitability go

down. This is because company has to pay cost of finance to out side party. At this juncture, it is

not important that whether corporation is getting profitability or not. This affect performance to a

great extent (Bhowmik and Saha, 2013). For example, if loan is taken by firm then management

need to pay its interest on right time. Also, principle amount need to be paid within stipulated

time.

1.3Appropriate sources of finance

According to the case study General Sportswear is planning to expand in the marketplace.

In this regard appropriate sources of finance are retained profit, leasing companies. It helps to

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expand business corporation can acquire highly updated technologies from leasing companies. It

helps to reduce financial burden because assets will be provided on rental basis. Furthermore,

retained profit proves to be effective in acquiring material for the production activities (Graff,

2003). Apart from this, bank loan is also appropriate source for raising long term source for the

firm. However, it generate additional cost for the firm but it is the effective alternative for

expand business. Company can pay the bank loan back after recovery of initial investment. Apart

from this, an alternative option may be financial institutions which supper such kind of

organization. It enables General Sportswear to get finance at low interest rate and expand

business in an effectual manner.

TASK 2

2.1 Analyze cost of different sources of finance

Cost of finance can be tangible such as interest and dividends and there can be

opportunity cost as well. Here, interest is fixed at the time of giving loan and time for payment of

the same is also decided at the same time. Further, dividend is paid to shareholders wen

corporation earn profit. In addition to this, opportunity cost incur because of use of retained

earning in the expansion activities. Apart from this, tax decreases profitability of firm. This is

because corporation need to pay cost of finance at first and then tax is paid. In such as cases

profitability go down to great extent (James, Leavel and Mainam, 2002).

2.2 Importance of finance planning

Financial planning is very important for General Sportswear which gives upward

direction to business. With the help of financial planning firm can control cash and profitability

can be enhanced. Furthermore, financial planning helps management to select appropriate

sources of finance so as to achieve organizational objectives. Similarly, effective tools and

techniques like budgeting and costing are used in order to ensure optimum utilization of limited

financial resources (Wildavsky, 2006).

2.3 Assessing financial information needs of three main decision makers

The main decision makers are shareholders, suppliers and customers. These are directly

or indirectly associated with firm and want to access wide range of information of company. For

example shareholders attend board meeting so as to get detail information related to financial

5

helps to reduce financial burden because assets will be provided on rental basis. Furthermore,

retained profit proves to be effective in acquiring material for the production activities (Graff,

2003). Apart from this, bank loan is also appropriate source for raising long term source for the

firm. However, it generate additional cost for the firm but it is the effective alternative for

expand business. Company can pay the bank loan back after recovery of initial investment. Apart

from this, an alternative option may be financial institutions which supper such kind of

organization. It enables General Sportswear to get finance at low interest rate and expand

business in an effectual manner.

TASK 2

2.1 Analyze cost of different sources of finance

Cost of finance can be tangible such as interest and dividends and there can be

opportunity cost as well. Here, interest is fixed at the time of giving loan and time for payment of

the same is also decided at the same time. Further, dividend is paid to shareholders wen

corporation earn profit. In addition to this, opportunity cost incur because of use of retained

earning in the expansion activities. Apart from this, tax decreases profitability of firm. This is

because corporation need to pay cost of finance at first and then tax is paid. In such as cases

profitability go down to great extent (James, Leavel and Mainam, 2002).

2.2 Importance of finance planning

Financial planning is very important for General Sportswear which gives upward

direction to business. With the help of financial planning firm can control cash and profitability

can be enhanced. Furthermore, financial planning helps management to select appropriate

sources of finance so as to achieve organizational objectives. Similarly, effective tools and

techniques like budgeting and costing are used in order to ensure optimum utilization of limited

financial resources (Wildavsky, 2006).

2.3 Assessing financial information needs of three main decision makers

The main decision makers are shareholders, suppliers and customers. These are directly

or indirectly associated with firm and want to access wide range of information of company. For

example shareholders attend board meeting so as to get detail information related to financial

5

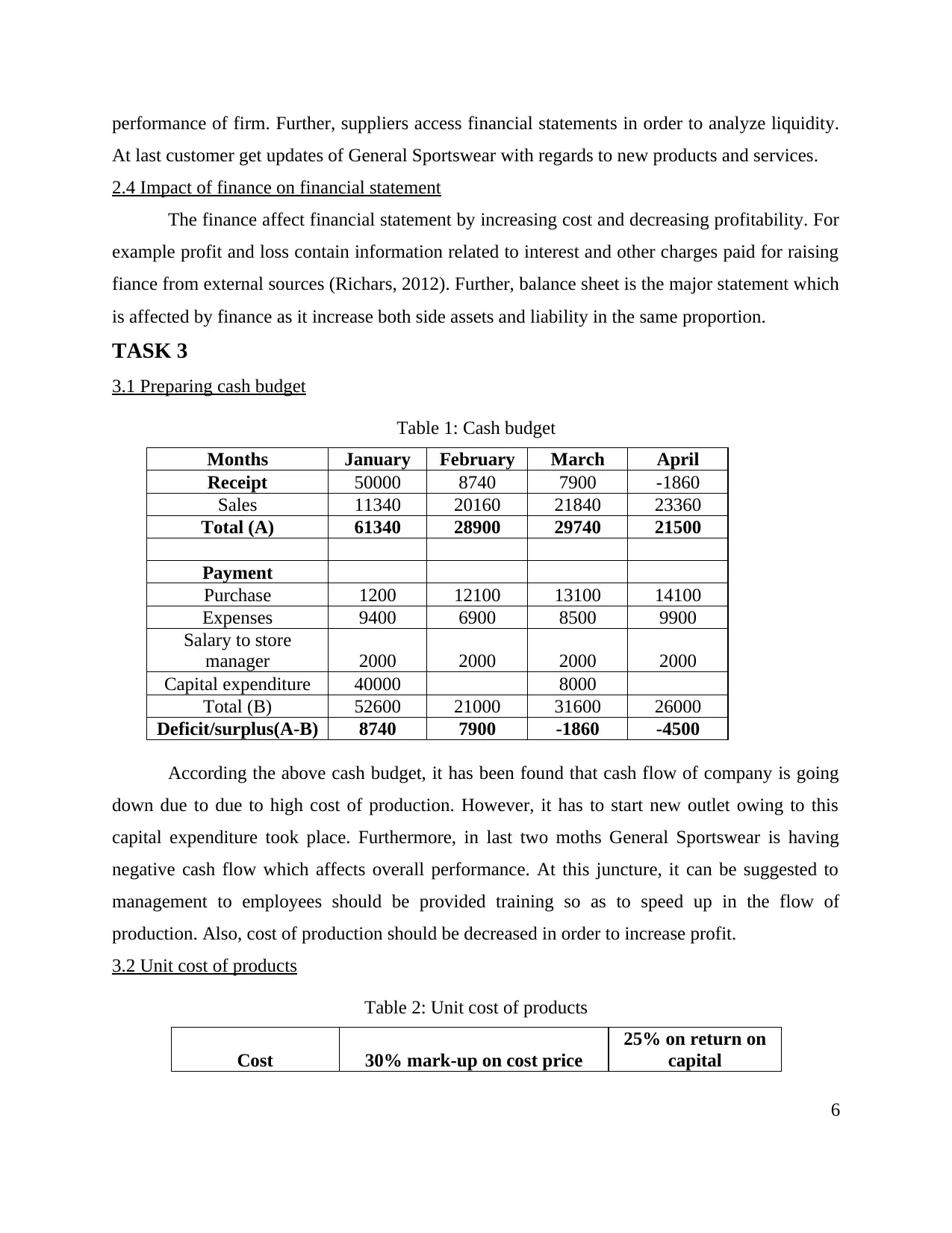

performance of firm. Further, suppliers access financial statements in order to analyze liquidity.

At last customer get updates of General Sportswear with regards to new products and services.

2.4 Impact of finance on financial statement

The finance affect financial statement by increasing cost and decreasing profitability. For

example profit and loss contain information related to interest and other charges paid for raising

fiance from external sources (Richars, 2012). Further, balance sheet is the major statement which

is affected by finance as it increase both side assets and liability in the same proportion.

TASK 3

3.1 Preparing cash budget

Table 1: Cash budget

Months January February March April

Receipt 50000 8740 7900 -1860

Sales 11340 20160 21840 23360

Total (A) 61340 28900 29740 21500

Payment

Purchase 1200 12100 13100 14100

Expenses 9400 6900 8500 9900

Salary to store

manager 2000 2000 2000 2000

Capital expenditure 40000 8000

Total (B) 52600 21000 31600 26000

Deficit/surplus(A-B) 8740 7900 -1860 -4500

According the above cash budget, it has been found that cash flow of company is going

down due to due to high cost of production. However, it has to start new outlet owing to this

capital expenditure took place. Furthermore, in last two moths General Sportswear is having

negative cash flow which affects overall performance. At this juncture, it can be suggested to

management to employees should be provided training so as to speed up in the flow of

production. Also, cost of production should be decreased in order to increase profit.

3.2 Unit cost of products

Table 2: Unit cost of products

Cost 30% mark-up on cost price

25% on return on

capital

6

At last customer get updates of General Sportswear with regards to new products and services.

2.4 Impact of finance on financial statement

The finance affect financial statement by increasing cost and decreasing profitability. For

example profit and loss contain information related to interest and other charges paid for raising

fiance from external sources (Richars, 2012). Further, balance sheet is the major statement which

is affected by finance as it increase both side assets and liability in the same proportion.

TASK 3

3.1 Preparing cash budget

Table 1: Cash budget

Months January February March April

Receipt 50000 8740 7900 -1860

Sales 11340 20160 21840 23360

Total (A) 61340 28900 29740 21500

Payment

Purchase 1200 12100 13100 14100

Expenses 9400 6900 8500 9900

Salary to store

manager 2000 2000 2000 2000

Capital expenditure 40000 8000

Total (B) 52600 21000 31600 26000

Deficit/surplus(A-B) 8740 7900 -1860 -4500

According the above cash budget, it has been found that cash flow of company is going

down due to due to high cost of production. However, it has to start new outlet owing to this

capital expenditure took place. Furthermore, in last two moths General Sportswear is having

negative cash flow which affects overall performance. At this juncture, it can be suggested to

management to employees should be provided training so as to speed up in the flow of

production. Also, cost of production should be decreased in order to increase profit.

3.2 Unit cost of products

Table 2: Unit cost of products

Cost 30% mark-up on cost price

25% on return on

capital

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

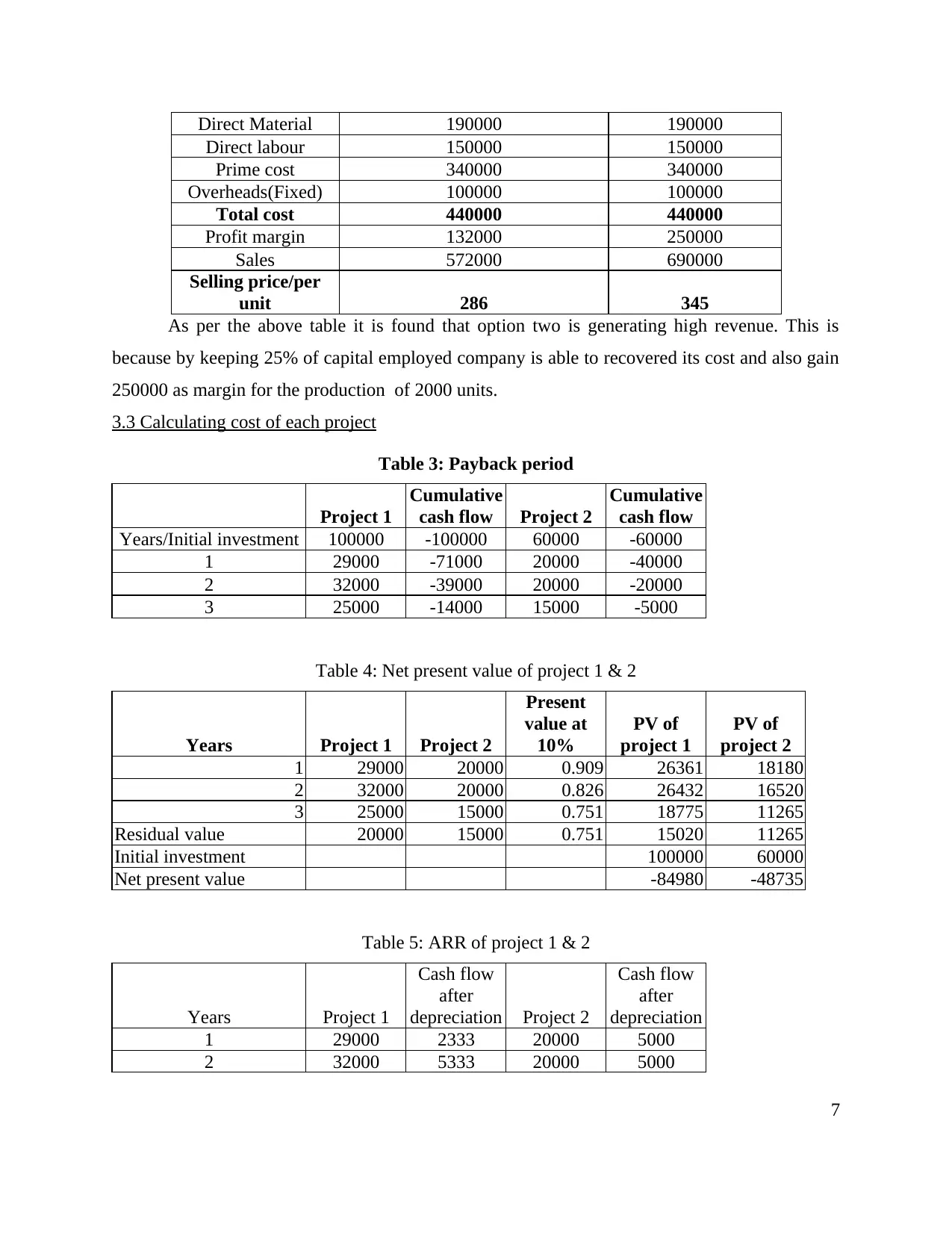

Direct Material 190000 190000

Direct labour 150000 150000

Prime cost 340000 340000

Overheads(Fixed) 100000 100000

Total cost 440000 440000

Profit margin 132000 250000

Sales 572000 690000

Selling price/per

unit 286 345

As per the above table it is found that option two is generating high revenue. This is

because by keeping 25% of capital employed company is able to recovered its cost and also gain

250000 as margin for the production of 2000 units.

3.3 Calculating cost of each project

Table 3: Payback period

Project 1

Cumulative

cash flow Project 2

Cumulative

cash flow

Years/Initial investment 100000 -100000 60000 -60000

1 29000 -71000 20000 -40000

2 32000 -39000 20000 -20000

3 25000 -14000 15000 -5000

Table 4: Net present value of project 1 & 2

Years Project 1 Project 2

Present

value at

10%

PV of

project 1

PV of

project 2

1 29000 20000 0.909 26361 18180

2 32000 20000 0.826 26432 16520

3 25000 15000 0.751 18775 11265

Residual value 20000 15000 0.751 15020 11265

Initial investment 100000 60000

Net present value -84980 -48735

Table 5: ARR of project 1 & 2

Years Project 1

Cash flow

after

depreciation Project 2

Cash flow

after

depreciation

1 29000 2333 20000 5000

2 32000 5333 20000 5000

7

Direct labour 150000 150000

Prime cost 340000 340000

Overheads(Fixed) 100000 100000

Total cost 440000 440000

Profit margin 132000 250000

Sales 572000 690000

Selling price/per

unit 286 345

As per the above table it is found that option two is generating high revenue. This is

because by keeping 25% of capital employed company is able to recovered its cost and also gain

250000 as margin for the production of 2000 units.

3.3 Calculating cost of each project

Table 3: Payback period

Project 1

Cumulative

cash flow Project 2

Cumulative

cash flow

Years/Initial investment 100000 -100000 60000 -60000

1 29000 -71000 20000 -40000

2 32000 -39000 20000 -20000

3 25000 -14000 15000 -5000

Table 4: Net present value of project 1 & 2

Years Project 1 Project 2

Present

value at

10%

PV of

project 1

PV of

project 2

1 29000 20000 0.909 26361 18180

2 32000 20000 0.826 26432 16520

3 25000 15000 0.751 18775 11265

Residual value 20000 15000 0.751 15020 11265

Initial investment 100000 60000

Net present value -84980 -48735

Table 5: ARR of project 1 & 2

Years Project 1

Cash flow

after

depreciation Project 2

Cash flow

after

depreciation

1 29000 2333 20000 5000

2 32000 5333 20000 5000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

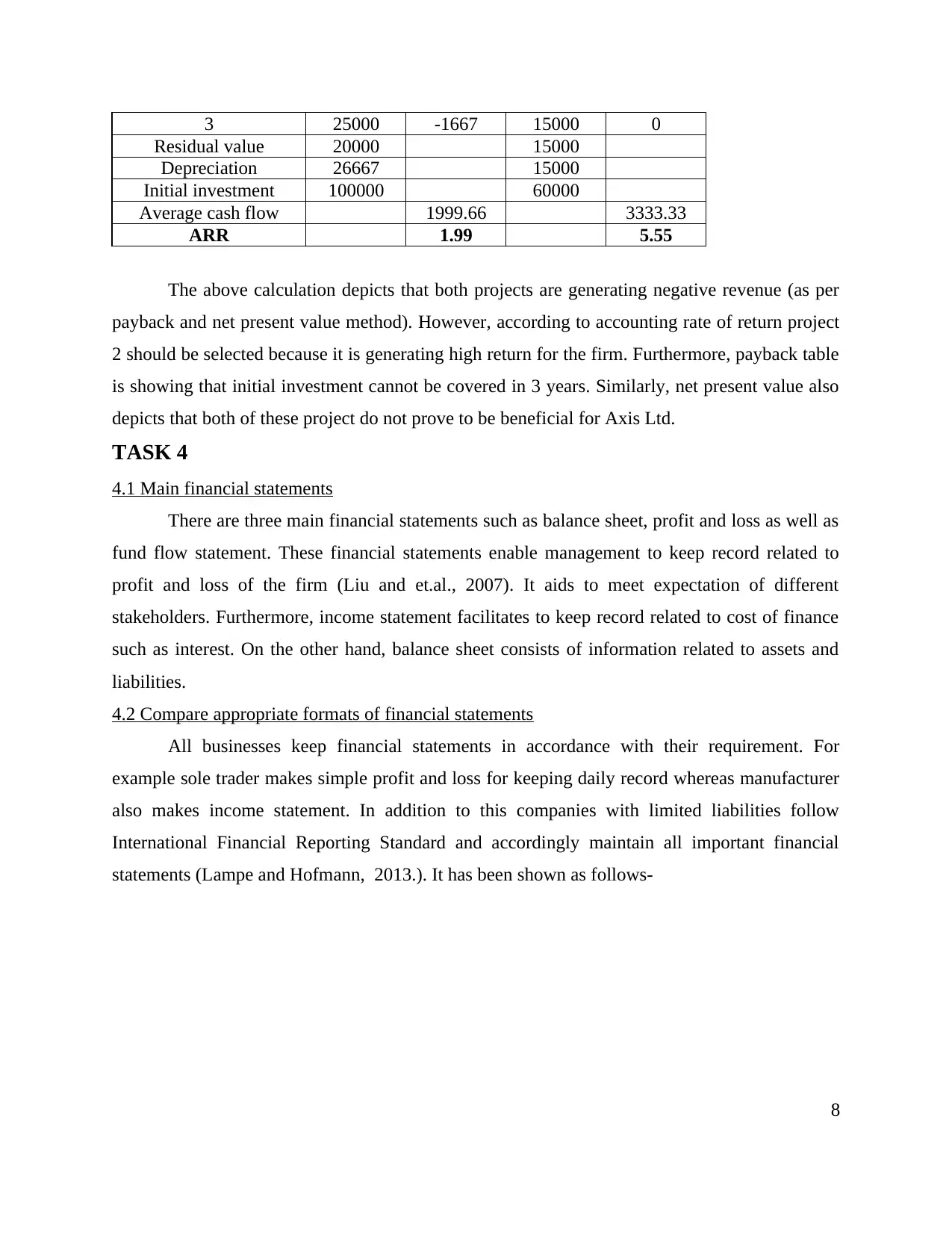

3 25000 -1667 15000 0

Residual value 20000 15000

Depreciation 26667 15000

Initial investment 100000 60000

Average cash flow 1999.66 3333.33

ARR 1.99 5.55

The above calculation depicts that both projects are generating negative revenue (as per

payback and net present value method). However, according to accounting rate of return project

2 should be selected because it is generating high return for the firm. Furthermore, payback table

is showing that initial investment cannot be covered in 3 years. Similarly, net present value also

depicts that both of these project do not prove to be beneficial for Axis Ltd.

TASK 4

4.1 Main financial statements

There are three main financial statements such as balance sheet, profit and loss as well as

fund flow statement. These financial statements enable management to keep record related to

profit and loss of the firm (Liu and et.al., 2007). It aids to meet expectation of different

stakeholders. Furthermore, income statement facilitates to keep record related to cost of finance

such as interest. On the other hand, balance sheet consists of information related to assets and

liabilities.

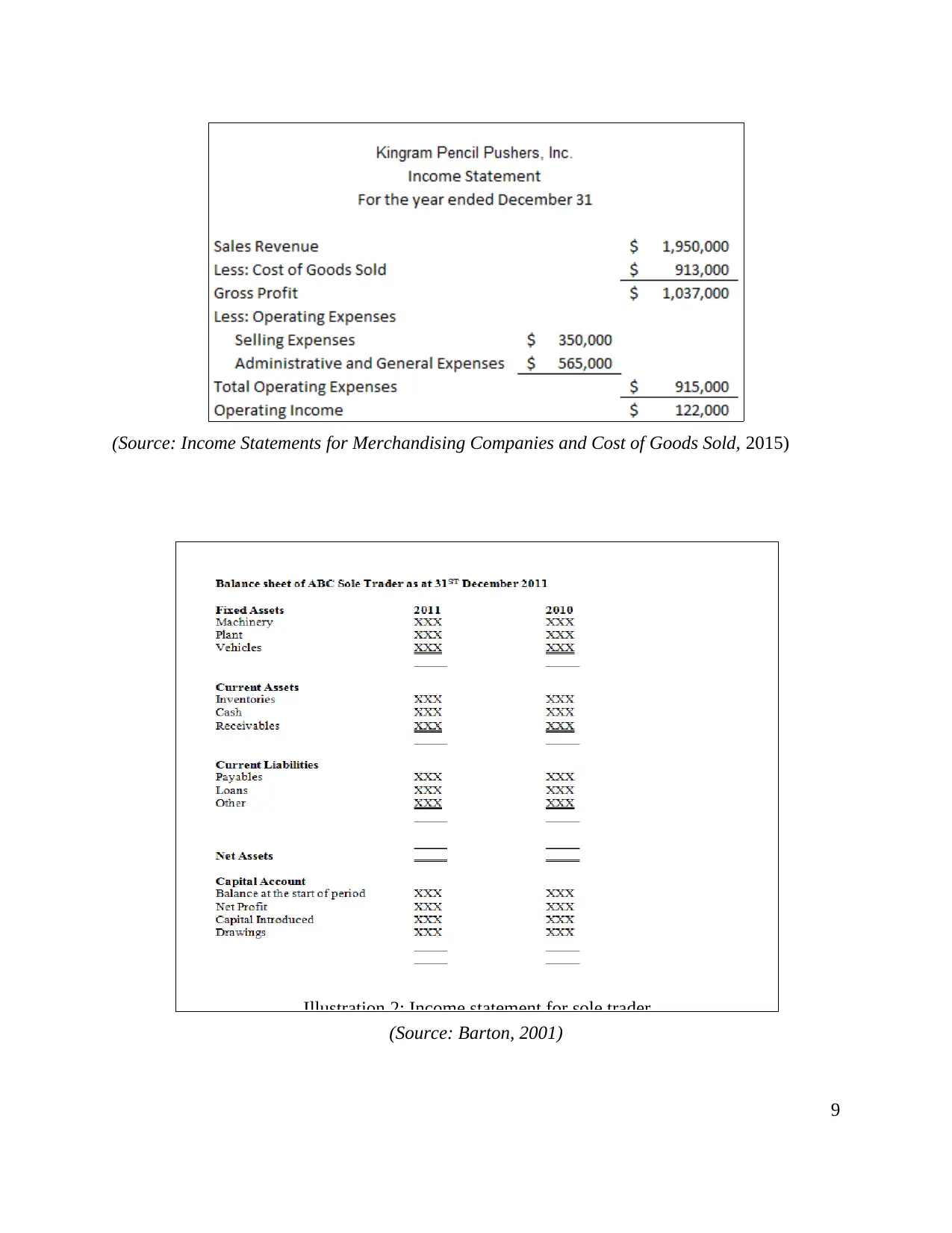

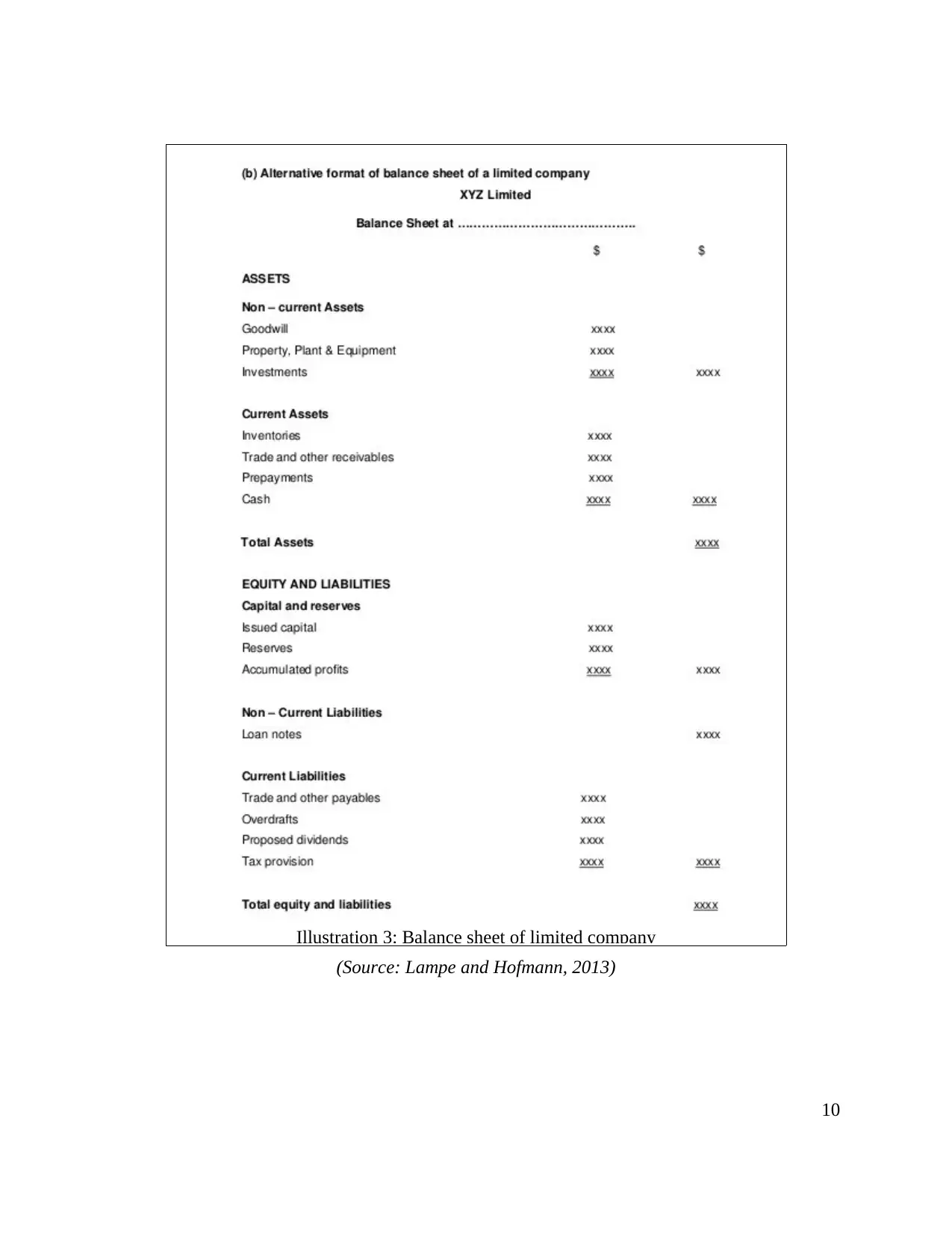

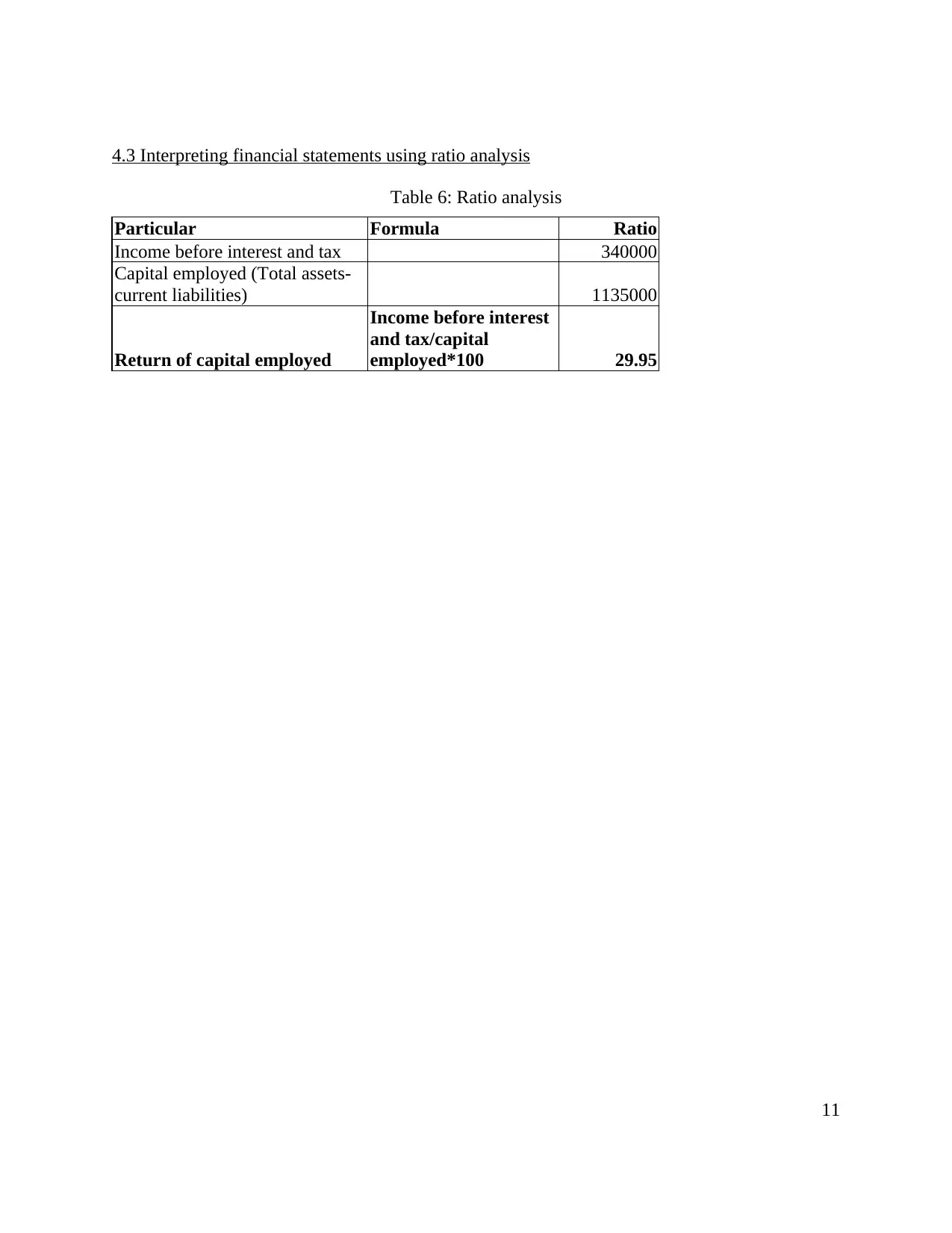

4.2 Compare appropriate formats of financial statements

All businesses keep financial statements in accordance with their requirement. For

example sole trader makes simple profit and loss for keeping daily record whereas manufacturer

also makes income statement. In addition to this companies with limited liabilities follow

International Financial Reporting Standard and accordingly maintain all important financial

statements (Lampe and Hofmann, 2013.). It has been shown as follows-

8

Residual value 20000 15000

Depreciation 26667 15000

Initial investment 100000 60000

Average cash flow 1999.66 3333.33

ARR 1.99 5.55

The above calculation depicts that both projects are generating negative revenue (as per

payback and net present value method). However, according to accounting rate of return project

2 should be selected because it is generating high return for the firm. Furthermore, payback table

is showing that initial investment cannot be covered in 3 years. Similarly, net present value also

depicts that both of these project do not prove to be beneficial for Axis Ltd.

TASK 4

4.1 Main financial statements

There are three main financial statements such as balance sheet, profit and loss as well as

fund flow statement. These financial statements enable management to keep record related to

profit and loss of the firm (Liu and et.al., 2007). It aids to meet expectation of different

stakeholders. Furthermore, income statement facilitates to keep record related to cost of finance

such as interest. On the other hand, balance sheet consists of information related to assets and

liabilities.

4.2 Compare appropriate formats of financial statements

All businesses keep financial statements in accordance with their requirement. For

example sole trader makes simple profit and loss for keeping daily record whereas manufacturer

also makes income statement. In addition to this companies with limited liabilities follow

International Financial Reporting Standard and accordingly maintain all important financial

statements (Lampe and Hofmann, 2013.). It has been shown as follows-

8

(Source: Income Statements for Merchandising Companies and Cost of Goods Sold, 2015)

(Source: Barton, 2001)

9

Illustration 2: Income statement for sole trader

(Source: Barton, 2001)

9

Illustration 2: Income statement for sole trader

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Source: Lampe and Hofmann, 2013)

10

Illustration 3: Balance sheet of limited company

10

Illustration 3: Balance sheet of limited company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

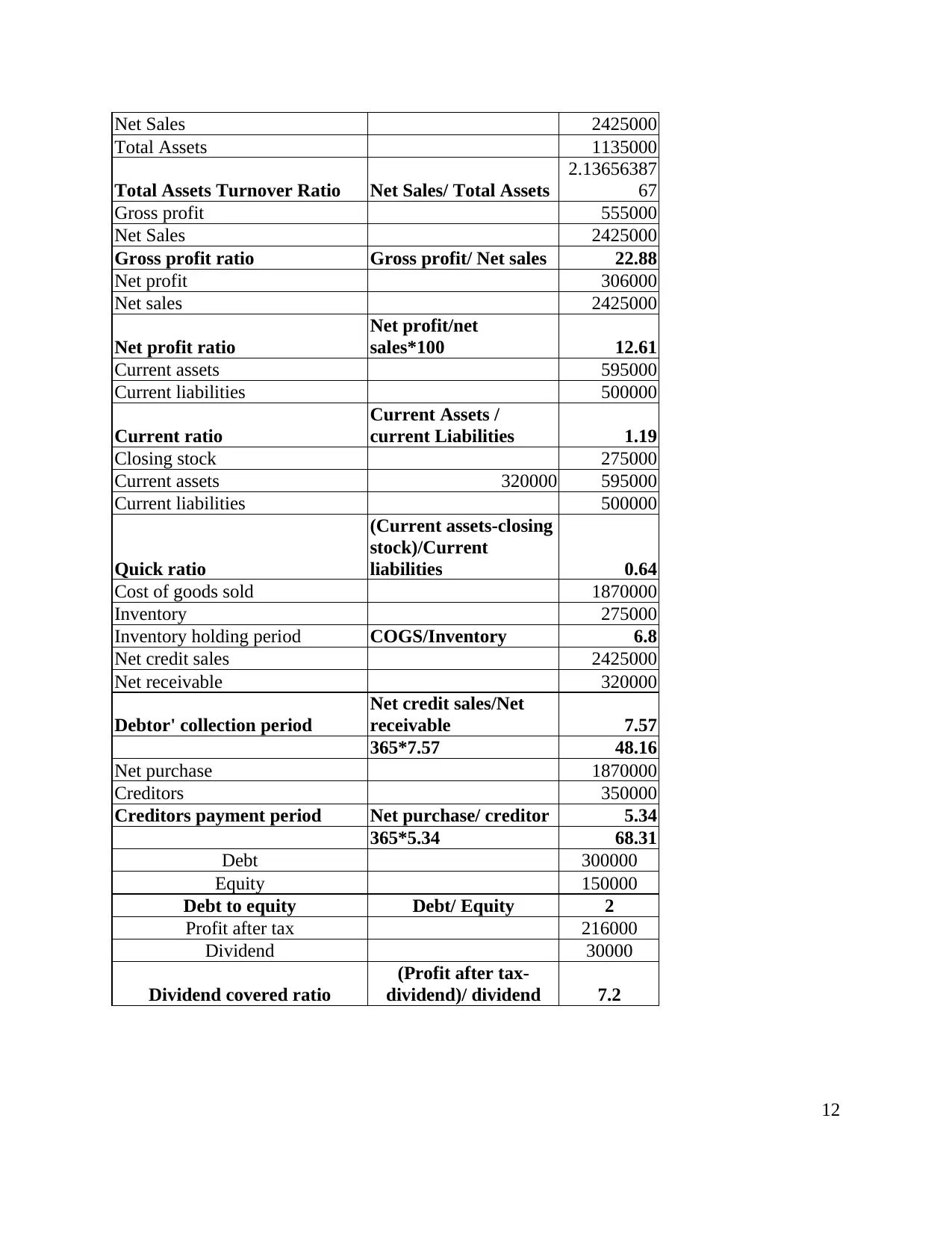

4.3 Interpreting financial statements using ratio analysis

Table 6: Ratio analysis

Particular Formula Ratio

Income before interest and tax 340000

Capital employed (Total assets-

current liabilities) 1135000

Return of capital employed

Income before interest

and tax/capital

employed*100 29.95

11

Table 6: Ratio analysis

Particular Formula Ratio

Income before interest and tax 340000

Capital employed (Total assets-

current liabilities) 1135000

Return of capital employed

Income before interest

and tax/capital

employed*100 29.95

11

Net Sales 2425000

Total Assets 1135000

Total Assets Turnover Ratio Net Sales/ Total Assets

2.13656387

67

Gross profit 555000

Net Sales 2425000

Gross profit ratio Gross profit/ Net sales 22.88

Net profit 306000

Net sales 2425000

Net profit ratio

Net profit/net

sales*100 12.61

Current assets 595000

Current liabilities 500000

Current ratio

Current Assets /

current Liabilities 1.19

Closing stock 275000

Current assets 320000 595000

Current liabilities 500000

Quick ratio

(Current assets-closing

stock)/Current

liabilities 0.64

Cost of goods sold 1870000

Inventory 275000

Inventory holding period COGS/Inventory 6.8

Net credit sales 2425000

Net receivable 320000

Debtor' collection period

Net credit sales/Net

receivable 7.57

365*7.57 48.16

Net purchase 1870000

Creditors 350000

Creditors payment period Net purchase/ creditor 5.34

365*5.34 68.31

Debt 300000

Equity 150000

Debt to equity Debt/ Equity 2

Profit after tax 216000

Dividend 30000

Dividend covered ratio

(Profit after tax-

dividend)/ dividend 7.2

12

Total Assets 1135000

Total Assets Turnover Ratio Net Sales/ Total Assets

2.13656387

67

Gross profit 555000

Net Sales 2425000

Gross profit ratio Gross profit/ Net sales 22.88

Net profit 306000

Net sales 2425000

Net profit ratio

Net profit/net

sales*100 12.61

Current assets 595000

Current liabilities 500000

Current ratio

Current Assets /

current Liabilities 1.19

Closing stock 275000

Current assets 320000 595000

Current liabilities 500000

Quick ratio

(Current assets-closing

stock)/Current

liabilities 0.64

Cost of goods sold 1870000

Inventory 275000

Inventory holding period COGS/Inventory 6.8

Net credit sales 2425000

Net receivable 320000

Debtor' collection period

Net credit sales/Net

receivable 7.57

365*7.57 48.16

Net purchase 1870000

Creditors 350000

Creditors payment period Net purchase/ creditor 5.34

365*5.34 68.31

Debt 300000

Equity 150000

Debt to equity Debt/ Equity 2

Profit after tax 216000

Dividend 30000

Dividend covered ratio

(Profit after tax-

dividend)/ dividend 7.2

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.