Corporate Finance Report: FedEx Capital Structure Analysis 2013-2018

VerifiedAdded on 2020/10/22

|28

|6957

|131

Report

AI Summary

This report provides a comprehensive analysis of FedEx Corporation's capital structure from 2013 to 2018, focusing on its financing through debt and its implications. The report explores key concepts in corporate finance, including capital structure, Weighted Average Cost of Capital (WACC), and the impact of dividend payments on share prices. It examines the relationship between financial leverage, cost of equity, and tax benefits associated with debt. The analysis incorporates various scholarly perspectives on dividend policy, highlighting its signaling impact on investors and its influence on stock prices. The report also considers factors such as financial leverage, tax rates, and asset performance. The report offers insights into how dividend decisions affect a company's financial performance, market liquidity, and overall shareholder value. It also addresses the influence of external factors such as trade location and ownership on stock prices. This report is valuable for students and professionals seeking a deeper understanding of corporate finance and its practical applications.

CORPORATE FINANCE PART A

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

CAPITAL STRUCTURE................................................................................................................1

Dividend payment affect share price...........................................................................................3

Calculation of WACC.................................................................................................................7

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

APPENDIX....................................................................................................................................17

INTRODUCTION...........................................................................................................................1

CAPITAL STRUCTURE................................................................................................................1

Dividend payment affect share price...........................................................................................3

Calculation of WACC.................................................................................................................7

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

APPENDIX....................................................................................................................................17

INTRODUCTION

Corporate finance is referred as branch of finance which directly deals for sources of

funding, capital structure of particular corporations and actions which manager undertakes for

raising value of firm to the shareholders along with tool and analysis which is used for analysis

for allocating financial resources. The capital structure is referred as proportion along with

combination of equity share capital, debentures, preference share capital, long term loans and

retained earnings. In simple words, it finances overall operation and growth with application of

different sources of funds. Debt originates in form of issuing bond or long term notes payable

where equity is classified as preferred stock, retained earnings or common stock. The present

report is about FedEx Corporation between 2013-2018 along with remarkable changes in last 5

years as it is dramatically financed through debt. This report has evaluated WACC along with

obtaining optimal capital structure with reference to FedEx Corporations.

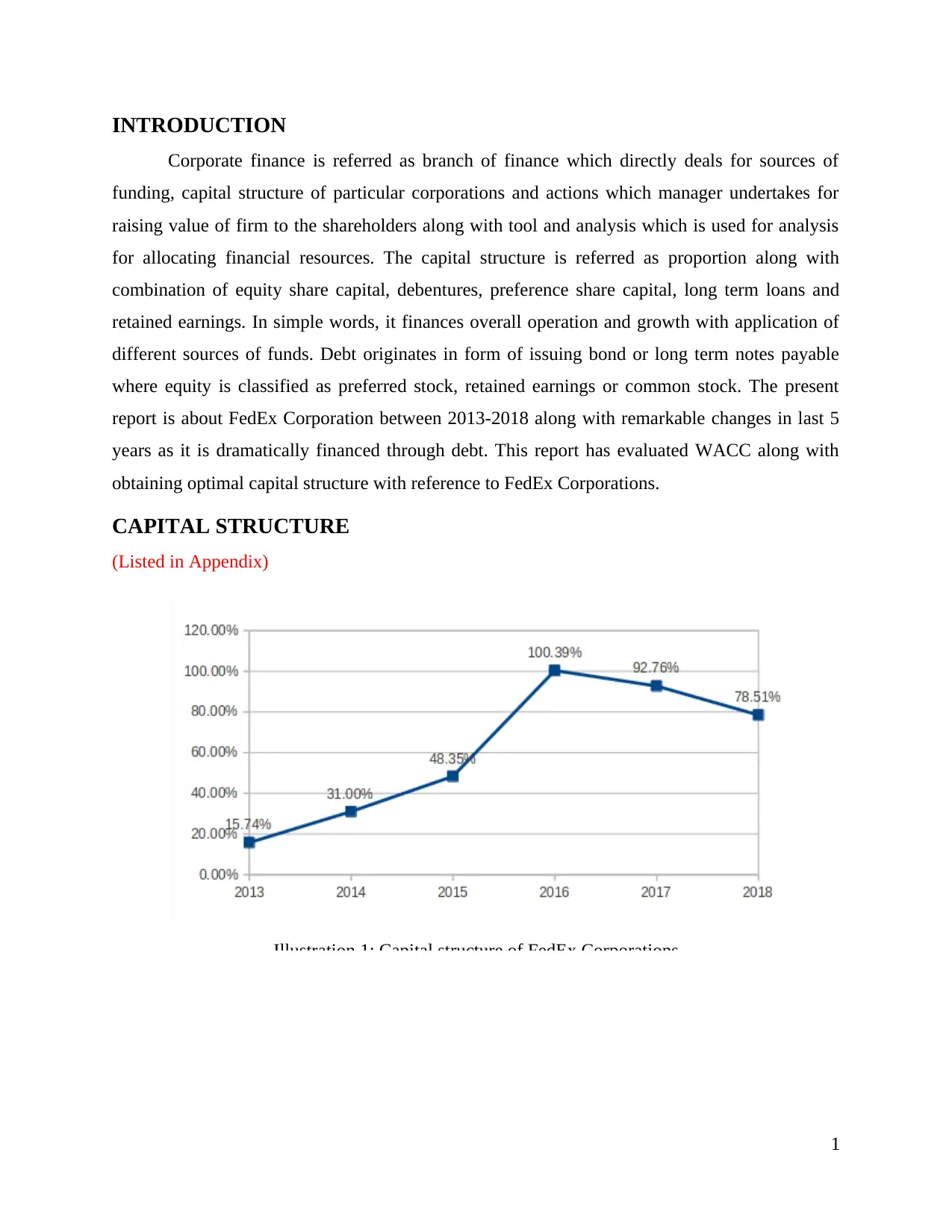

CAPITAL STRUCTURE

(Listed in Appendix)

Illustration 1: Capital structure of FedEx Corporations

1

Corporate finance is referred as branch of finance which directly deals for sources of

funding, capital structure of particular corporations and actions which manager undertakes for

raising value of firm to the shareholders along with tool and analysis which is used for analysis

for allocating financial resources. The capital structure is referred as proportion along with

combination of equity share capital, debentures, preference share capital, long term loans and

retained earnings. In simple words, it finances overall operation and growth with application of

different sources of funds. Debt originates in form of issuing bond or long term notes payable

where equity is classified as preferred stock, retained earnings or common stock. The present

report is about FedEx Corporation between 2013-2018 along with remarkable changes in last 5

years as it is dramatically financed through debt. This report has evaluated WACC along with

obtaining optimal capital structure with reference to FedEx Corporations.

CAPITAL STRUCTURE

(Listed in Appendix)

Illustration 1: Capital structure of FedEx Corporations

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

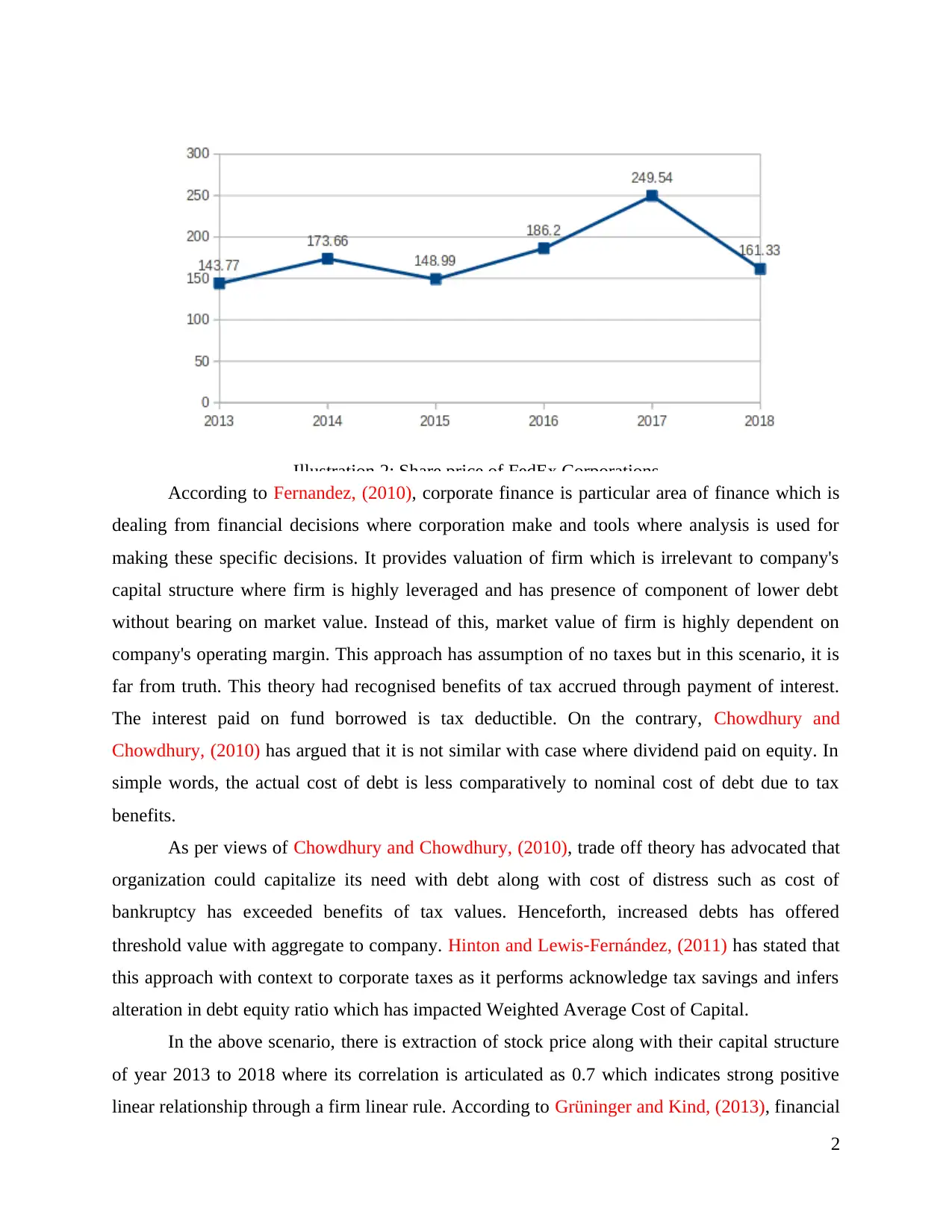

Illustration 2: Share price of FedEx Corporations

According to Fernandez, (2010), corporate finance is particular area of finance which is

dealing from financial decisions where corporation make and tools where analysis is used for

making these specific decisions. It provides valuation of firm which is irrelevant to company's

capital structure where firm is highly leveraged and has presence of component of lower debt

without bearing on market value. Instead of this, market value of firm is highly dependent on

company's operating margin. This approach has assumption of no taxes but in this scenario, it is

far from truth. This theory had recognised benefits of tax accrued through payment of interest.

The interest paid on fund borrowed is tax deductible. On the contrary, Chowdhury and

Chowdhury, (2010) has argued that it is not similar with case where dividend paid on equity. In

simple words, the actual cost of debt is less comparatively to nominal cost of debt due to tax

benefits.

As per views of Chowdhury and Chowdhury, (2010), trade off theory has advocated that

organization could capitalize its need with debt along with cost of distress such as cost of

bankruptcy has exceeded benefits of tax values. Henceforth, increased debts has offered

threshold value with aggregate to company. Hinton and Lewis‐Fernández, (2011) has stated that

this approach with context to corporate taxes as it performs acknowledge tax savings and infers

alteration in debt equity ratio which has impacted Weighted Average Cost of Capital.

In the above scenario, there is extraction of stock price along with their capital structure

of year 2013 to 2018 where its correlation is articulated as 0.7 which indicates strong positive

linear relationship through a firm linear rule. According to Grüninger and Kind, (2013), financial

2

According to Fernandez, (2010), corporate finance is particular area of finance which is

dealing from financial decisions where corporation make and tools where analysis is used for

making these specific decisions. It provides valuation of firm which is irrelevant to company's

capital structure where firm is highly leveraged and has presence of component of lower debt

without bearing on market value. Instead of this, market value of firm is highly dependent on

company's operating margin. This approach has assumption of no taxes but in this scenario, it is

far from truth. This theory had recognised benefits of tax accrued through payment of interest.

The interest paid on fund borrowed is tax deductible. On the contrary, Chowdhury and

Chowdhury, (2010) has argued that it is not similar with case where dividend paid on equity. In

simple words, the actual cost of debt is less comparatively to nominal cost of debt due to tax

benefits.

As per views of Chowdhury and Chowdhury, (2010), trade off theory has advocated that

organization could capitalize its need with debt along with cost of distress such as cost of

bankruptcy has exceeded benefits of tax values. Henceforth, increased debts has offered

threshold value with aggregate to company. Hinton and Lewis‐Fernández, (2011) has stated that

this approach with context to corporate taxes as it performs acknowledge tax savings and infers

alteration in debt equity ratio which has impacted Weighted Average Cost of Capital.

In the above scenario, there is extraction of stock price along with their capital structure

of year 2013 to 2018 where its correlation is articulated as 0.7 which indicates strong positive

linear relationship through a firm linear rule. According to Grüninger and Kind, (2013), financial

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

leverage is direct proportion to cost of equity with increment in debt component, higher risk has

been perceived with equity shareholders for organization. In order to this, shareholders expect

huge return with increment in cost of equity. In this context, key distinction with assumption

that debt shareholders have upper hand with claim on concerned earnings and cost of debt

reduces.

Dividend payment affect share price

According to author Baker, Kilincarslanand Arsal (2018), specialist of share market

would mark down price as multiple factors impact stock prices. In the same series, supply and

demand contributes major role in fall and rise of stock prices. There are various other

perspectives which plays vital role when organization pays dividend and on the contrary, stock

trading with absence of rights to a dividend is worth less comparatively to similar trading

company with dividend. With context to Miler and Modigliani theory, it has been stated that

dividends have signalling impact. The investor and potential investor has forecasted company's

margin which is influences with dividend rate.

According to the view of Blanchard and et.al., (2018) stated that dividends are having

signalling impact in the mind of customers. Thus, it is crucial that enterprise needs to distribute

dividend among the shareholders or investors. In addition to Kim, Luo and Xie, (2018) stated

that high dividend payments can be considered as positive indication of profitability by

shareholders. The information about dividends payments helps to define the scenario of entity. In

contrary to Kohler, Guschanski and Stockhammer, (2018) stated that as the dividend of firm get

disclosed it works as to enhance share prices in market. On the basis of announcement of

dividend, shareholders, investors, and potential investor can assume the position of enterprise in

context of profitability. As per the view of Magnusson and Enebrand, (2018) it can be stated that

the enhancement in payment of dividend indicate positive sign for entity as it aids to raise

goodwill and reputation in the mind of customer and it has also beneficial as price of share gets

increased. With context of Baker, Kilincarslan and Arsal, (2018) it can be stated that at time

when entity cuts the payment of dividend to customers then it shows the negative effect on

reputation of firm and it also spoils the image of firm in the mind of customers. Thus, prices of

share can also get reduced. As per the view of He and et.al., (2019) it can be stated that the

decision in related with dividend is one of crucial in financial decision of the corporate firm.

Thus, the firm which are dividend paying have more amount of liquidity in market in order to

3

been perceived with equity shareholders for organization. In order to this, shareholders expect

huge return with increment in cost of equity. In this context, key distinction with assumption

that debt shareholders have upper hand with claim on concerned earnings and cost of debt

reduces.

Dividend payment affect share price

According to author Baker, Kilincarslanand Arsal (2018), specialist of share market

would mark down price as multiple factors impact stock prices. In the same series, supply and

demand contributes major role in fall and rise of stock prices. There are various other

perspectives which plays vital role when organization pays dividend and on the contrary, stock

trading with absence of rights to a dividend is worth less comparatively to similar trading

company with dividend. With context to Miler and Modigliani theory, it has been stated that

dividends have signalling impact. The investor and potential investor has forecasted company's

margin which is influences with dividend rate.

According to the view of Blanchard and et.al., (2018) stated that dividends are having

signalling impact in the mind of customers. Thus, it is crucial that enterprise needs to distribute

dividend among the shareholders or investors. In addition to Kim, Luo and Xie, (2018) stated

that high dividend payments can be considered as positive indication of profitability by

shareholders. The information about dividends payments helps to define the scenario of entity. In

contrary to Kohler, Guschanski and Stockhammer, (2018) stated that as the dividend of firm get

disclosed it works as to enhance share prices in market. On the basis of announcement of

dividend, shareholders, investors, and potential investor can assume the position of enterprise in

context of profitability. As per the view of Magnusson and Enebrand, (2018) it can be stated that

the enhancement in payment of dividend indicate positive sign for entity as it aids to raise

goodwill and reputation in the mind of customer and it has also beneficial as price of share gets

increased. With context of Baker, Kilincarslan and Arsal, (2018) it can be stated that at time

when entity cuts the payment of dividend to customers then it shows the negative effect on

reputation of firm and it also spoils the image of firm in the mind of customers. Thus, prices of

share can also get reduced. As per the view of He and et.al., (2019) it can be stated that the

decision in related with dividend is one of crucial in financial decision of the corporate firm.

Thus, the firm which are dividend paying have more amount of liquidity in market in order to

3

measure the stock and liquidity. According to the view of Ferris, (2018) it can be stated that the

firm who is having high amount of profitability and entities with low profits have significant

prosperity in order to pay dividends. In addition to it, there are number of factors that are

affecting firm shareholders return such are as financial leverage, tax rate, assets performance,

contribution of employees and technical know etc. In contrary to Blanchard and et.al., (2018)

stated that prices of shares continually fluctuate in every second. Thus, number of firm belief that

right prices must be the present value of all the future dividends. In contrary to Kim, Luo and

Xie, (2018) stated that the prices of share usually rises before the entity announce its dividends.

Herein, it can be stated that number of factors are there that can affect the stock prices. In this

manner, supply and demand are tow factor that plays major role in rise and fall of stock prices.

Thus, dividend policy has number of detrimental factors as return on equity, price of shares and

earning per share etc. As per the view of Kohler, Guschanski and Stockhammer, (2018) stated

that dividends can have significant impact over price of underlying stock in variety of manner.

As per the view of Sharif, Purohit and Pillai (2015), dividend decision is one of the importance

financial decision of for a corporation. The firms paying the dividend are having more liquid

market one their stock and the strokes are measured to positivity. This directly effect the

profitably of the business of the dividend payer. The cumulative excess returns are significant

and positive for those firms which pay dividends for more than 30 days form the data of

announcements of the dividends, this reflects how that even with declaration of the dividend the

pieces of the shards gets a boost up. The profit momentum of the firms paying dividend is lower

than the forms which are non paying the dividends. There is direct and positive relation between

the dividends, retained earnings, earning per share and stock prices of an organisation. This is

because the dividend payout directly reflect the performance of the business. However, the

author Belousova and et.al., (2016), present a point of view that the question is still unsolved

over the matter that weather the dividend police of a business directly effects its shareholders

wealth or not. The authors stated that profits is one of the main economic driver for an

organisation and it presents two dimension one is that to retain the profits and to invest it in

expansion and growth of the business. Other is that to retain a small amount and distribute the

maximum part to the shareholders as dividend. To distribute the dividend to the shareholders

symbolizes the strength of the organisation and gives information about the prospect of the

organisation in context of its developments and grasping more values in the industry. This

4

firm who is having high amount of profitability and entities with low profits have significant

prosperity in order to pay dividends. In addition to it, there are number of factors that are

affecting firm shareholders return such are as financial leverage, tax rate, assets performance,

contribution of employees and technical know etc. In contrary to Blanchard and et.al., (2018)

stated that prices of shares continually fluctuate in every second. Thus, number of firm belief that

right prices must be the present value of all the future dividends. In contrary to Kim, Luo and

Xie, (2018) stated that the prices of share usually rises before the entity announce its dividends.

Herein, it can be stated that number of factors are there that can affect the stock prices. In this

manner, supply and demand are tow factor that plays major role in rise and fall of stock prices.

Thus, dividend policy has number of detrimental factors as return on equity, price of shares and

earning per share etc. As per the view of Kohler, Guschanski and Stockhammer, (2018) stated

that dividends can have significant impact over price of underlying stock in variety of manner.

As per the view of Sharif, Purohit and Pillai (2015), dividend decision is one of the importance

financial decision of for a corporation. The firms paying the dividend are having more liquid

market one their stock and the strokes are measured to positivity. This directly effect the

profitably of the business of the dividend payer. The cumulative excess returns are significant

and positive for those firms which pay dividends for more than 30 days form the data of

announcements of the dividends, this reflects how that even with declaration of the dividend the

pieces of the shards gets a boost up. The profit momentum of the firms paying dividend is lower

than the forms which are non paying the dividends. There is direct and positive relation between

the dividends, retained earnings, earning per share and stock prices of an organisation. This is

because the dividend payout directly reflect the performance of the business. However, the

author Belousova and et.al., (2016), present a point of view that the question is still unsolved

over the matter that weather the dividend police of a business directly effects its shareholders

wealth or not. The authors stated that profits is one of the main economic driver for an

organisation and it presents two dimension one is that to retain the profits and to invest it in

expansion and growth of the business. Other is that to retain a small amount and distribute the

maximum part to the shareholders as dividend. To distribute the dividend to the shareholders

symbolizes the strength of the organisation and gives information about the prospect of the

organisation in context of its developments and grasping more values in the industry. This

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

directly effect the share prices of the firm as company with constant dividend distributive shows

that it is operating at good financial position in the industry.

According to the view of Baker, Kilincarslanand Arsal (2018), stated that dividend and

stock prices are directly connected with each other, both effect each in other opposite manner. As

when the company reduces the dividend on its stock the share becomes less attractive to the

shareholders and to the potential investors as well. This means the prices of stock are likely

reduce. So to receive dividend but in smaller amount directly effects the share price to fall. This

states the facts the market changes very quickly to the changes in the dividend. Even a slight

hint to the public about reduction in the dividends can let the shares prices to fall. The author

stated the facts that the share market plays on thin ice and the dividends payments are the thinner

part of that ice. A small pressures can break the ice letting the prices of shares to fall to lower

level instantly without taking much time. Conversely, Duke, Nneji and Nkamare (2015) stated

that with a hike in the amount and ratio of the dividend distribution of a firm the stock becomes

more attracting and wanting to the public, the demand suddenly increases as with the purchase of

share every shareholder will get hight amount of the dividend. In such situation the shares are

held back causing the seller to increase the demand and leading to rise in the prices of to gain

more profits. Investors generally consider rising dividends a sign of a company's good health.

Always make sure the company that issues the dividend stock reports growing profits along with

the increased dividend. The author present the fact that an investor should Avoid companies that

raise their dividends without increased profits to make their stock look more attractive, because

those companies may not be able to pay the increased dividend over time. This means dividend

distribution and share prices are inversely proportionate to each other.

However, Ofori‐Sasu, Abor and Osei, (2017) stated that the dividends do not directly

effects the intrinsic value of the firm but they have a potential to change or alter the valuation of

the stock of the business. The dividend activity and dividend yield can certainly effect the

sentiments of the investors allowing it to move in the practice of share either upwards or

downwards, hence changing the valuation of the share. Stock market specialists will mark down

the price of a stock on its ex-dividend date by the amount of the dividend. The companies

usually pay dividend every quarter, an investor who buys on the ex-dividend date may get the

stock at lower price but will still be entitled to a dividend three months late. Here if the dividend

is more than the previous quarter leads to increment in the prices of share and if the dividend

5

that it is operating at good financial position in the industry.

According to the view of Baker, Kilincarslanand Arsal (2018), stated that dividend and

stock prices are directly connected with each other, both effect each in other opposite manner. As

when the company reduces the dividend on its stock the share becomes less attractive to the

shareholders and to the potential investors as well. This means the prices of stock are likely

reduce. So to receive dividend but in smaller amount directly effects the share price to fall. This

states the facts the market changes very quickly to the changes in the dividend. Even a slight

hint to the public about reduction in the dividends can let the shares prices to fall. The author

stated the facts that the share market plays on thin ice and the dividends payments are the thinner

part of that ice. A small pressures can break the ice letting the prices of shares to fall to lower

level instantly without taking much time. Conversely, Duke, Nneji and Nkamare (2015) stated

that with a hike in the amount and ratio of the dividend distribution of a firm the stock becomes

more attracting and wanting to the public, the demand suddenly increases as with the purchase of

share every shareholder will get hight amount of the dividend. In such situation the shares are

held back causing the seller to increase the demand and leading to rise in the prices of to gain

more profits. Investors generally consider rising dividends a sign of a company's good health.

Always make sure the company that issues the dividend stock reports growing profits along with

the increased dividend. The author present the fact that an investor should Avoid companies that

raise their dividends without increased profits to make their stock look more attractive, because

those companies may not be able to pay the increased dividend over time. This means dividend

distribution and share prices are inversely proportionate to each other.

However, Ofori‐Sasu, Abor and Osei, (2017) stated that the dividends do not directly

effects the intrinsic value of the firm but they have a potential to change or alter the valuation of

the stock of the business. The dividend activity and dividend yield can certainly effect the

sentiments of the investors allowing it to move in the practice of share either upwards or

downwards, hence changing the valuation of the share. Stock market specialists will mark down

the price of a stock on its ex-dividend date by the amount of the dividend. The companies

usually pay dividend every quarter, an investor who buys on the ex-dividend date may get the

stock at lower price but will still be entitled to a dividend three months late. Here if the dividend

is more than the previous quarter leads to increment in the prices of share and if the dividend

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

amount is less than the previously distributed amount the prices of the share definitely falls. In

accordance with the views of the author Kibet, Jagongo and Ndede (2016), location of the trade

and ownership appeared to be the factors affecting the prices of the shares having a great

influence over them. He reflected the fact that the largest multinational and most liquid

organization of the world are also signification influenced by the location factor. This means the

places where the organisation is located and carry out its business effect the share prices as per

the changing environmental condition having impact on business operation, this includes both

internal as well the external factors existing in a specific area or operation. This can explained

with the example of currency valuation of each nation and their changing values. As an

appreciation the value of dollar against the pound the prices of Royla dutch tends to increase in

comparison to that of shell. However, (Grennan, 2018) have a perception that a firm if pays

regularly dividend which is equal to half of its normal earning is at equivalent position to those

firms which pay no dividend and probably never pay in future as well. This reflects the fact that

an organisation need to pay more than half of its earning to the shareholder in from of divined in

order to make a fluctuation in the prices of its stock. The lesser amount distribution can lead to

fall in the share prices of the business.

Thus, stock plays essential role in its popularity, declaration and payment of dividend has

specific and significant impact on market prices. So, the dividend can be paid in cash but it can

also issue in manner as additional shares of stock. The amount of dividends do not guarantee on

common stock. Before paying the dividend the issuing firm must declare the amount of dividend

and date when it will be paid. Thus, it can be stated that declaration of dividend can encourage

investor to purchase stock. As per the view of Magnusson and Enebrand, (2018) stated that the

dividend payments is also inclusive of cash outflows to the shareholders and it has major impact

on cash as it gets reduced in company books. There are many individuals that invest in certain

stock at certain times in order to collect the payments of dividend. Sometimes, the prices of stock

falls sue to reserve of entity going down.

MM I has argued that hypothesized scenario which reflects actual market equilibrium

which is particularly appraised market value. It has been reasoned by MM that existence of

arbitrage opportunity with increment in overall returns with absence of incurring any additional

risk. In the same series, perfect capital market would not allow opportunities of riskless arbitrage

to exist. There is presence of presumption of issuing firm in financially sound along with absence

6

accordance with the views of the author Kibet, Jagongo and Ndede (2016), location of the trade

and ownership appeared to be the factors affecting the prices of the shares having a great

influence over them. He reflected the fact that the largest multinational and most liquid

organization of the world are also signification influenced by the location factor. This means the

places where the organisation is located and carry out its business effect the share prices as per

the changing environmental condition having impact on business operation, this includes both

internal as well the external factors existing in a specific area or operation. This can explained

with the example of currency valuation of each nation and their changing values. As an

appreciation the value of dollar against the pound the prices of Royla dutch tends to increase in

comparison to that of shell. However, (Grennan, 2018) have a perception that a firm if pays

regularly dividend which is equal to half of its normal earning is at equivalent position to those

firms which pay no dividend and probably never pay in future as well. This reflects the fact that

an organisation need to pay more than half of its earning to the shareholder in from of divined in

order to make a fluctuation in the prices of its stock. The lesser amount distribution can lead to

fall in the share prices of the business.

Thus, stock plays essential role in its popularity, declaration and payment of dividend has

specific and significant impact on market prices. So, the dividend can be paid in cash but it can

also issue in manner as additional shares of stock. The amount of dividends do not guarantee on

common stock. Before paying the dividend the issuing firm must declare the amount of dividend

and date when it will be paid. Thus, it can be stated that declaration of dividend can encourage

investor to purchase stock. As per the view of Magnusson and Enebrand, (2018) stated that the

dividend payments is also inclusive of cash outflows to the shareholders and it has major impact

on cash as it gets reduced in company books. There are many individuals that invest in certain

stock at certain times in order to collect the payments of dividend. Sometimes, the prices of stock

falls sue to reserve of entity going down.

MM I has argued that hypothesized scenario which reflects actual market equilibrium

which is particularly appraised market value. It has been reasoned by MM that existence of

arbitrage opportunity with increment in overall returns with absence of incurring any additional

risk. In the same series, perfect capital market would not allow opportunities of riskless arbitrage

to exist. There is presence of presumption of issuing firm in financially sound along with absence

6

of financial leverage risk. There is absence of consideration of cost of debt which should be debt

to coverage ratio decline and firm draws nearer to bankruptcy and default. Not even MM I allow

for alteration on agency costs or transaction cost incur in less than perfect market. It also

invalidates usefulness of MM I but does relegate about applicability which is revenant range. On

the contrary, MM I have fair weather cost of capital model and could not be expected for

generating meaningful outcome for those organizations where potential with context of financial

distress ranks higher.

Usually, high dividend results to higher stock prices as brand equity of company enhances

and vice versa. However, raising dividend might not raise stock price due to less earnings which

might be invested back into organization and directly impedes growth. The increment in

dividend would always reduce stock prices due firm depleting internal funding resources. On the

other side, the psychological impact has been addressed in various cases such as investors

analyse that the firm in offering higher dividend rate which will be profitable for them in having

better proportion of profits. While if the company is offering less dividends that there will be

issues in recovering the amount of invested capital. However, the changes in share price due to

changes in dividend policy as listed in Appendix.

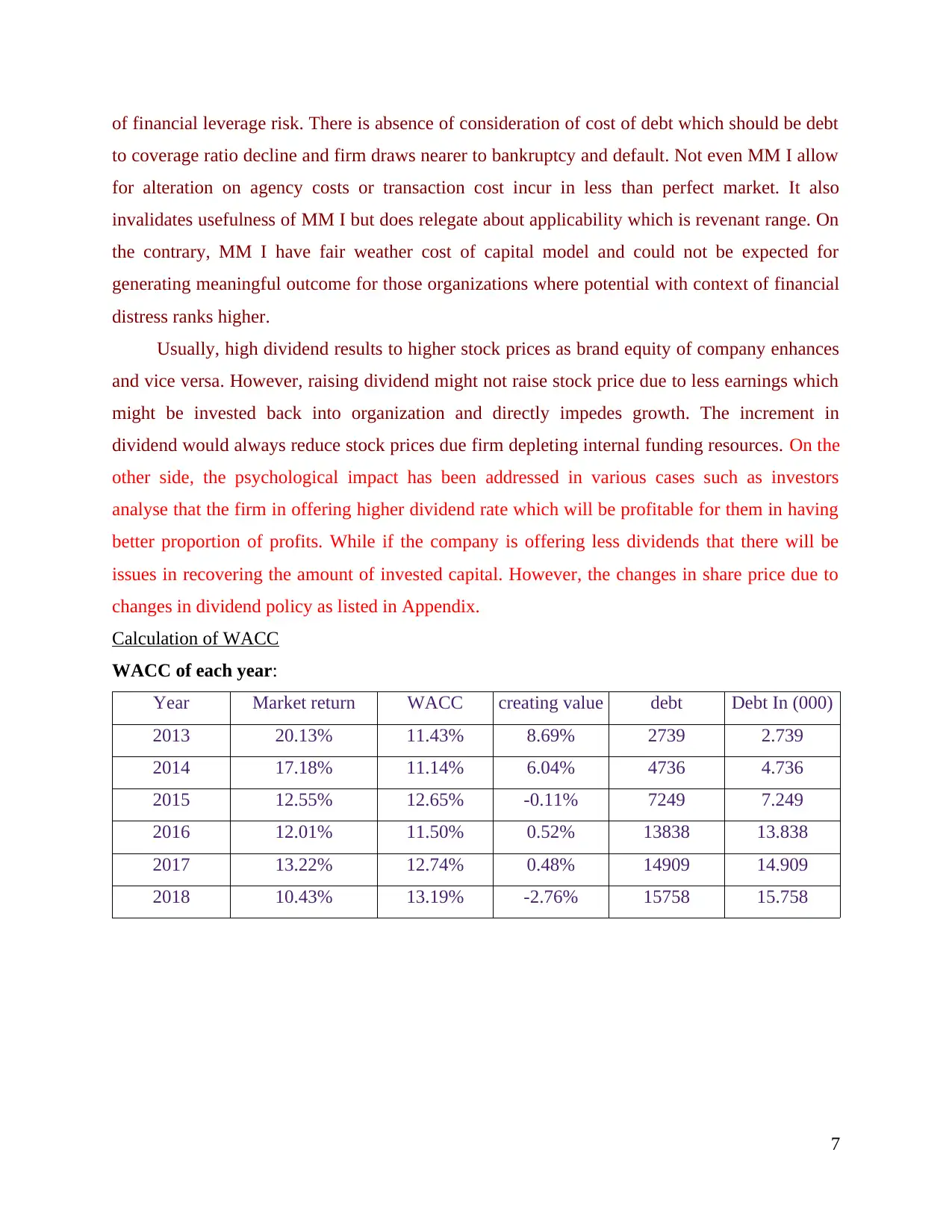

Calculation of WACC

WACC of each year:

Year Market return WACC creating value debt Debt In (000)

2013 20.13% 11.43% 8.69% 2739 2.739

2014 17.18% 11.14% 6.04% 4736 4.736

2015 12.55% 12.65% -0.11% 7249 7.249

2016 12.01% 11.50% 0.52% 13838 13.838

2017 13.22% 12.74% 0.48% 14909 14.909

2018 10.43% 13.19% -2.76% 15758 15.758

7

to coverage ratio decline and firm draws nearer to bankruptcy and default. Not even MM I allow

for alteration on agency costs or transaction cost incur in less than perfect market. It also

invalidates usefulness of MM I but does relegate about applicability which is revenant range. On

the contrary, MM I have fair weather cost of capital model and could not be expected for

generating meaningful outcome for those organizations where potential with context of financial

distress ranks higher.

Usually, high dividend results to higher stock prices as brand equity of company enhances

and vice versa. However, raising dividend might not raise stock price due to less earnings which

might be invested back into organization and directly impedes growth. The increment in

dividend would always reduce stock prices due firm depleting internal funding resources. On the

other side, the psychological impact has been addressed in various cases such as investors

analyse that the firm in offering higher dividend rate which will be profitable for them in having

better proportion of profits. While if the company is offering less dividends that there will be

issues in recovering the amount of invested capital. However, the changes in share price due to

changes in dividend policy as listed in Appendix.

Calculation of WACC

WACC of each year:

Year Market return WACC creating value debt Debt In (000)

2013 20.13% 11.43% 8.69% 2739 2.739

2014 17.18% 11.14% 6.04% 4736 4.736

2015 12.55% 12.65% -0.11% 7249 7.249

2016 12.01% 11.50% 0.52% 13838 13.838

2017 13.22% 12.74% 0.48% 14909 14.909

2018 10.43% 13.19% -2.76% 15758 15.758

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

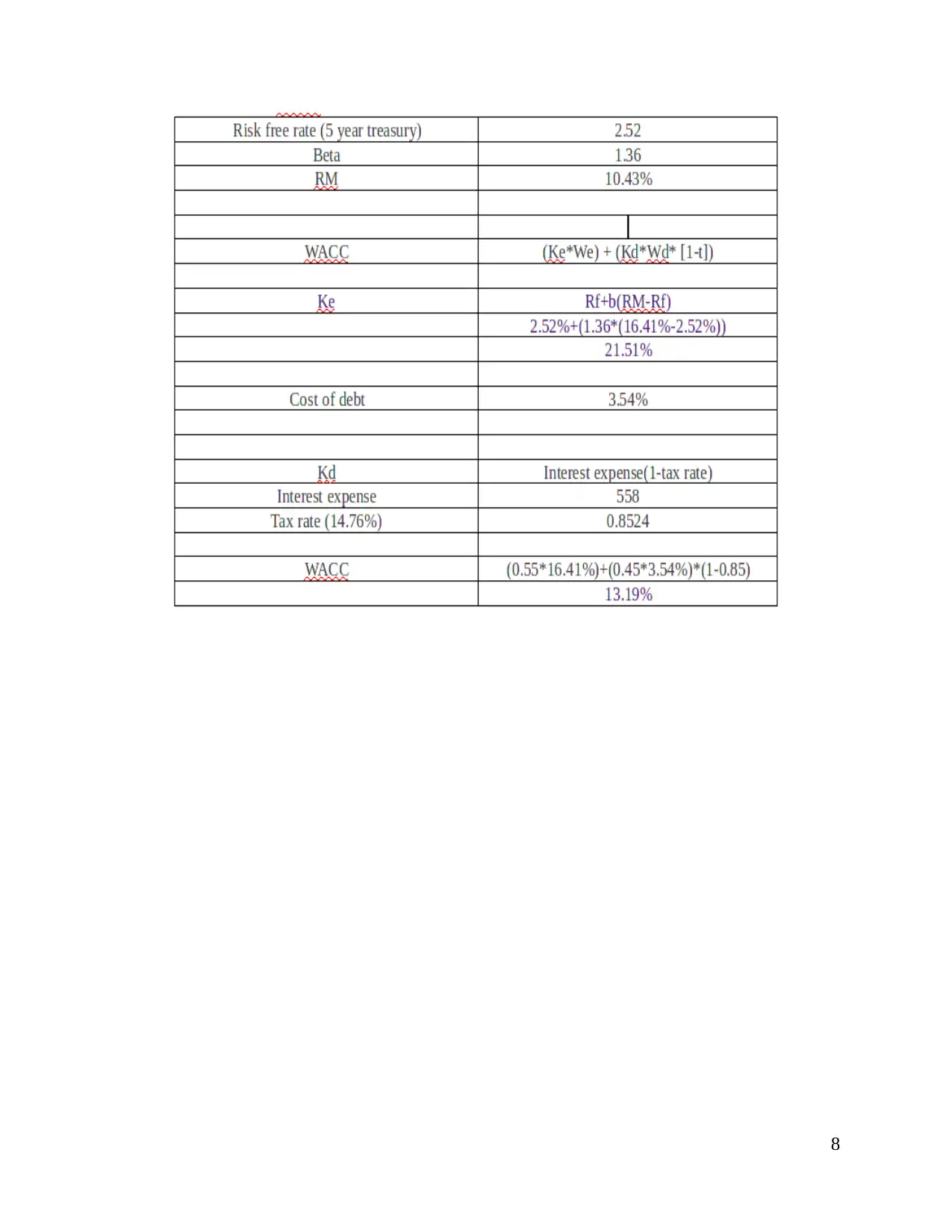

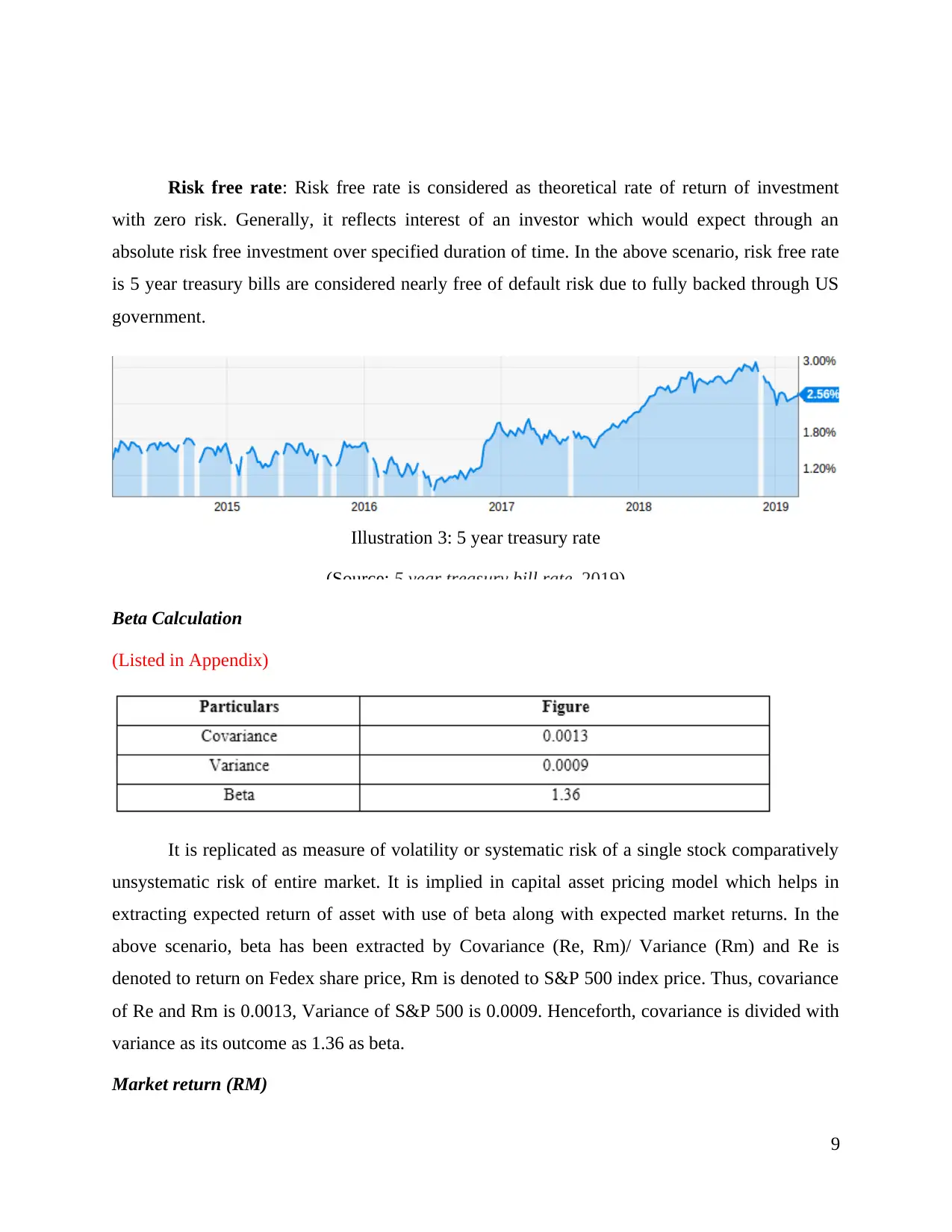

Risk free rate: Risk free rate is considered as theoretical rate of return of investment

with zero risk. Generally, it reflects interest of an investor which would expect through an

absolute risk free investment over specified duration of time. In the above scenario, risk free rate

is 5 year treasury bills are considered nearly free of default risk due to fully backed through US

government.

Illustration 3: 5 year treasury rate

(Source: 5 year treasury bill rate, 2019)

Beta Calculation

(Listed in Appendix)

It is replicated as measure of volatility or systematic risk of a single stock comparatively

unsystematic risk of entire market. It is implied in capital asset pricing model which helps in

extracting expected return of asset with use of beta along with expected market returns. In the

above scenario, beta has been extracted by Covariance (Re, Rm)/ Variance (Rm) and Re is

denoted to return on Fedex share price, Rm is denoted to S&P 500 index price. Thus, covariance

of Re and Rm is 0.0013, Variance of S&P 500 is 0.0009. Henceforth, covariance is divided with

variance as its outcome as 1.36 as beta.

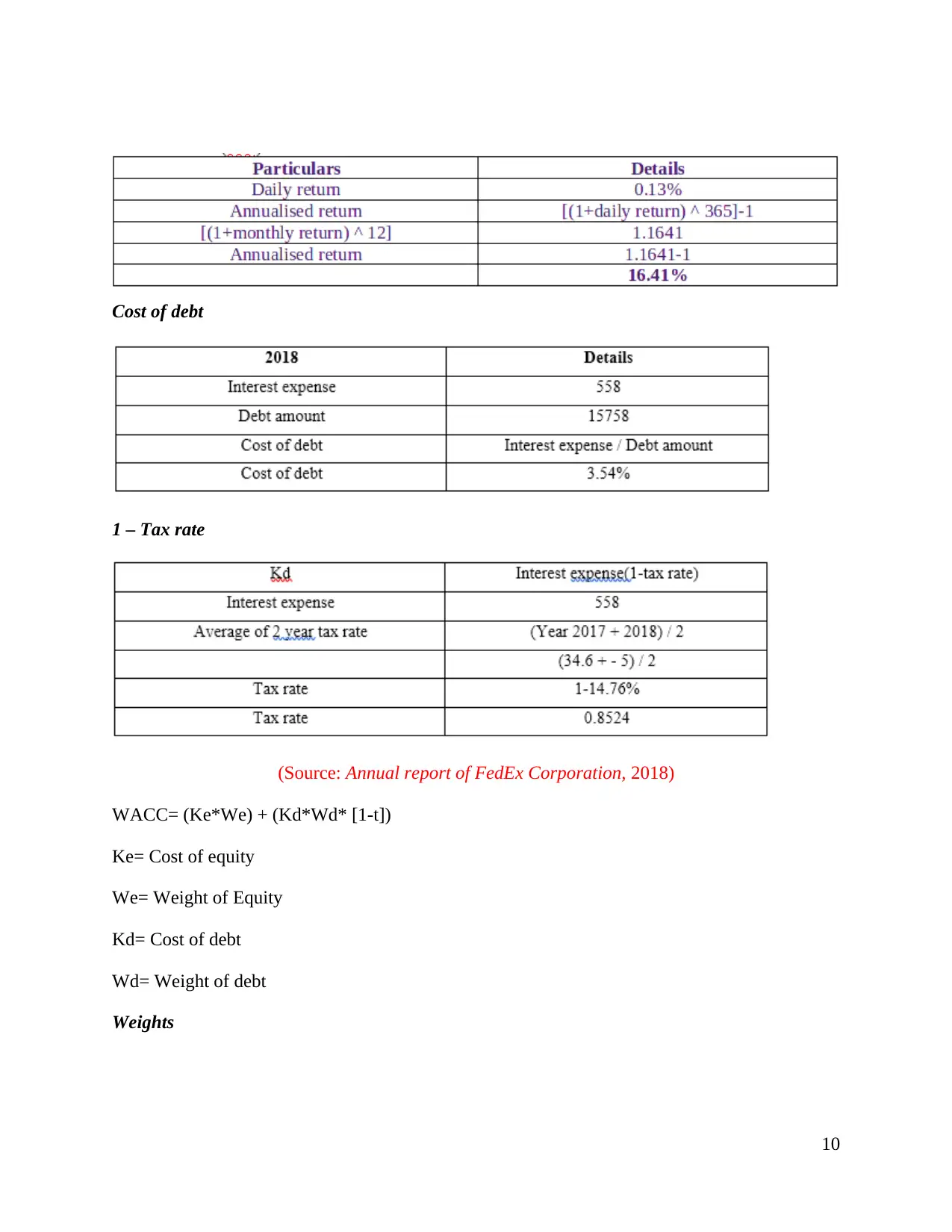

Market return (RM)

9

with zero risk. Generally, it reflects interest of an investor which would expect through an

absolute risk free investment over specified duration of time. In the above scenario, risk free rate

is 5 year treasury bills are considered nearly free of default risk due to fully backed through US

government.

Illustration 3: 5 year treasury rate

(Source: 5 year treasury bill rate, 2019)

Beta Calculation

(Listed in Appendix)

It is replicated as measure of volatility or systematic risk of a single stock comparatively

unsystematic risk of entire market. It is implied in capital asset pricing model which helps in

extracting expected return of asset with use of beta along with expected market returns. In the

above scenario, beta has been extracted by Covariance (Re, Rm)/ Variance (Rm) and Re is

denoted to return on Fedex share price, Rm is denoted to S&P 500 index price. Thus, covariance

of Re and Rm is 0.0013, Variance of S&P 500 is 0.0009. Henceforth, covariance is divided with

variance as its outcome as 1.36 as beta.

Market return (RM)

9

Cost of debt

1 – Tax rate

(Source: Annual report of FedEx Corporation, 2018)

WACC= (Ke*We) + (Kd*Wd* [1-t])

Ke= Cost of equity

We= Weight of Equity

Kd= Cost of debt

Wd= Weight of debt

Weights

10

1 – Tax rate

(Source: Annual report of FedEx Corporation, 2018)

WACC= (Ke*We) + (Kd*Wd* [1-t])

Ke= Cost of equity

We= Weight of Equity

Kd= Cost of debt

Wd= Weight of debt

Weights

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.