Corporate and Financial Accounting Report: Fund Sources Analysis

VerifiedAdded on 2022/10/17

|13

|3279

|13

Report

AI Summary

This report analyzes the fund sources of Bellamy Australia and A2 Milk Company, focusing on equity and liabilities over a three-year period. It examines share capital, retained earnings, and reserves within owner's equity, along with borrowings, provisions, income tax payable, and trade payables in the liability section. The report highlights movements in equity and liabilities for both companies, identifying trends and changes. It also discusses the merits and demerits of different funding sources, considering implications for company ownership and financial stability. Furthermore, the report addresses the classification of companies based on size and their respective compliance and reporting requirements, providing a comprehensive overview of corporate financial accounting principles and practices. The report covers the analysis of financial statements, including equity and liability sections, and discusses the impact of financial decisions on company performance.

1

Corporate and financial accounting

Corporate and financial accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive summary

The report has been prepared for the Bellamy Australia and A2 Milk Company. In this, there is

the consideration which is given to the funds which are collected with the use of various sources.

The items of the equity have been taken into account and also the amounts which are collected

with the help of debts and borrowings have also been taken into account. There are various

changes which are made in them and the review of the same has been made in which all of them

have been identified and considered in an appropriate manner. There is the determination of the

reason for changes which have taken place. The conditions and the concepts which are involved

for the large proprietary company and small proprietary company have been taken into account

and in that the needs which will be required to be fulfilled with respect to the compliance have

also been undertaken.

Executive summary

The report has been prepared for the Bellamy Australia and A2 Milk Company. In this, there is

the consideration which is given to the funds which are collected with the use of various sources.

The items of the equity have been taken into account and also the amounts which are collected

with the help of debts and borrowings have also been taken into account. There are various

changes which are made in them and the review of the same has been made in which all of them

have been identified and considered in an appropriate manner. There is the determination of the

reason for changes which have taken place. The conditions and the concepts which are involved

for the large proprietary company and small proprietary company have been taken into account

and in that the needs which will be required to be fulfilled with respect to the compliance have

also been undertaken.

3

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................4

Part A...............................................................................................................................................4

i) Items under owners’ equity......................................................................................................4

ii) Movement in each item of equity............................................................................................5

iii) Items under the liability section.............................................................................................6

iv) Changes in items involved in liabilities.................................................................................7

v) Merits and demerits of the sources of funds............................................................................9

Part B...............................................................................................................................................9

Large and small proprietary company-related concept...............................................................9

Compliance and reporting requirements....................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Table of Contents

Executive summary.........................................................................................................................2

Introduction......................................................................................................................................4

Part A...............................................................................................................................................4

i) Items under owners’ equity......................................................................................................4

ii) Movement in each item of equity............................................................................................5

iii) Items under the liability section.............................................................................................6

iv) Changes in items involved in liabilities.................................................................................7

v) Merits and demerits of the sources of funds............................................................................9

Part B...............................................................................................................................................9

Large and small proprietary company-related concept...............................................................9

Compliance and reporting requirements....................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

In the company, there is the need to manage all of the aspects in the best possible manner and

one such concept is the maintenance of the funds which are required. This is done with the help

of proper identification and arrangement of the funds. There will be consideration of the various

sources which are available and then the decision is taken to choose the appropriate method. This

will be requiring the analysis of the current situation. Due to this, the report will be made in

which all of the funds which have been collected with different sources will be taken into

account. There are equity funds which are created in the company and in that also there are

several elements which are involved and will be taken into account. The debts which have been

taken will also be ascertained and the changes which are taking place in them from the past 3

years will be provided for. There will be various impacts which will be faced by the company

with their adoptions and all of them will be discussed. The manner in which the proper

classification of the companies can be made will be considered and all the conditions in this

respect will be provided. The company will have to face the implication of the same and that

will, therefore, be taken into use.

Part A

i) Items under owners’ equity

Equity is the main source which is used in the company for the arrangement of the funds and

meeting the requirements in an effective manner. There are several other options also in which

the complete equity is classified and all of them are discussed below. In them, there are different

components which are involved and shall be understood. This will be helping the company in

taking them in consideration for the making of the future decisions.

Share capital: This covers the capital which is raised by the company with the use of the shares.

In this company will be allowed to issue the shares to the public and they will be investing in the

same (Warusawitharana and Whited, 2015). By the help of this, an amount will be collected

which is identified to be the share capital. In this, the right on the company will be provided to

the investors and they will be able to involve in the company’s actions.

Introduction

In the company, there is the need to manage all of the aspects in the best possible manner and

one such concept is the maintenance of the funds which are required. This is done with the help

of proper identification and arrangement of the funds. There will be consideration of the various

sources which are available and then the decision is taken to choose the appropriate method. This

will be requiring the analysis of the current situation. Due to this, the report will be made in

which all of the funds which have been collected with different sources will be taken into

account. There are equity funds which are created in the company and in that also there are

several elements which are involved and will be taken into account. The debts which have been

taken will also be ascertained and the changes which are taking place in them from the past 3

years will be provided for. There will be various impacts which will be faced by the company

with their adoptions and all of them will be discussed. The manner in which the proper

classification of the companies can be made will be considered and all the conditions in this

respect will be provided. The company will have to face the implication of the same and that

will, therefore, be taken into use.

Part A

i) Items under owners’ equity

Equity is the main source which is used in the company for the arrangement of the funds and

meeting the requirements in an effective manner. There are several other options also in which

the complete equity is classified and all of them are discussed below. In them, there are different

components which are involved and shall be understood. This will be helping the company in

taking them in consideration for the making of the future decisions.

Share capital: This covers the capital which is raised by the company with the use of the shares.

In this company will be allowed to issue the shares to the public and they will be investing in the

same (Warusawitharana and Whited, 2015). By the help of this, an amount will be collected

which is identified to be the share capital. In this, the right on the company will be provided to

the investors and they will be able to involve in the company’s actions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Retained earnings: The earnings are made in the business and it is the responsibility of the

company to use them in the most adequate manner. There are various purposes for which the

same can be used and the division of the same will be made in such manner that the best results

are obtained by the company. In this, the company will be considering that emergencies may

arise in the business and for that the amount shall be secured. This lead to the creation of the

retained earnings which will be used by the company at the time of requirement.

Reserves: They are the amounts which are kept to meet the expenses which are in relation to

some particular task. The reserves are created for a specific task and will be used only for that.

This is kept separately and will be providing the company with the security about that particular

and important activity (Boubakri et al., 2012). They are also included in the equity as they are the

funds of the company on which no charge is created.

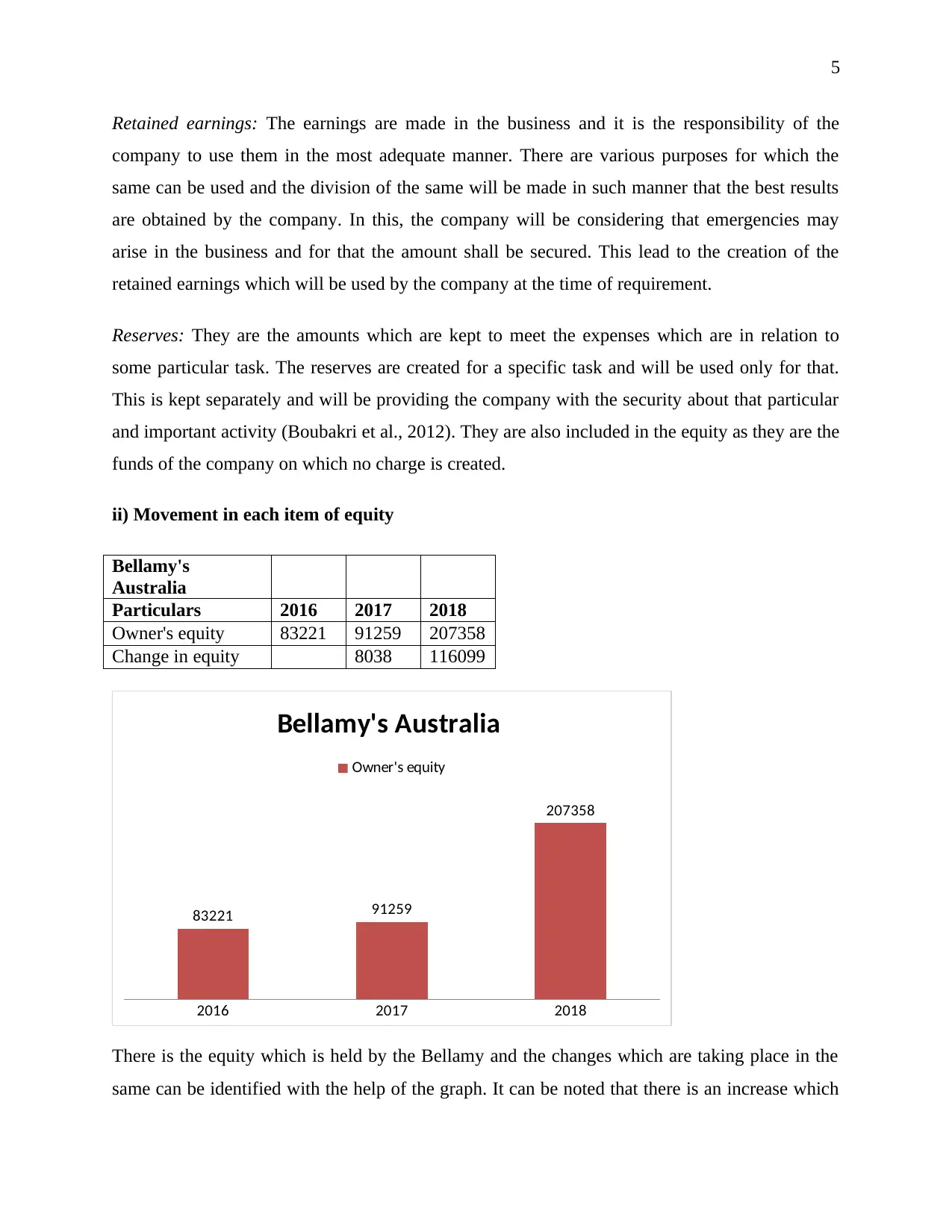

ii) Movement in each item of equity

Bellamy's

Australia

Particulars 2016 2017 2018

Owner's equity 83221 91259 207358

Change in equity 8038 116099

2016 2017 2018

83221 91259

207358

Bellamy's Australia

Owner's equity

There is the equity which is held by the Bellamy and the changes which are taking place in the

same can be identified with the help of the graph. It can be noted that there is an increase which

Retained earnings: The earnings are made in the business and it is the responsibility of the

company to use them in the most adequate manner. There are various purposes for which the

same can be used and the division of the same will be made in such manner that the best results

are obtained by the company. In this, the company will be considering that emergencies may

arise in the business and for that the amount shall be secured. This lead to the creation of the

retained earnings which will be used by the company at the time of requirement.

Reserves: They are the amounts which are kept to meet the expenses which are in relation to

some particular task. The reserves are created for a specific task and will be used only for that.

This is kept separately and will be providing the company with the security about that particular

and important activity (Boubakri et al., 2012). They are also included in the equity as they are the

funds of the company on which no charge is created.

ii) Movement in each item of equity

Bellamy's

Australia

Particulars 2016 2017 2018

Owner's equity 83221 91259 207358

Change in equity 8038 116099

2016 2017 2018

83221 91259

207358

Bellamy's Australia

Owner's equity

There is the equity which is held by the Bellamy and the changes which are taking place in the

same can be identified with the help of the graph. It can be noted that there is an increase which

6

is taking place in the same and more addition made in 2018 (Bellamy’s Australia limited, 2017).

This is because of the increase in all the categories and there are more shares which have been

issued and that raised the share capital of the company. The company has made a high income

and due to that, the retained earnings which are made by the company have also increased.

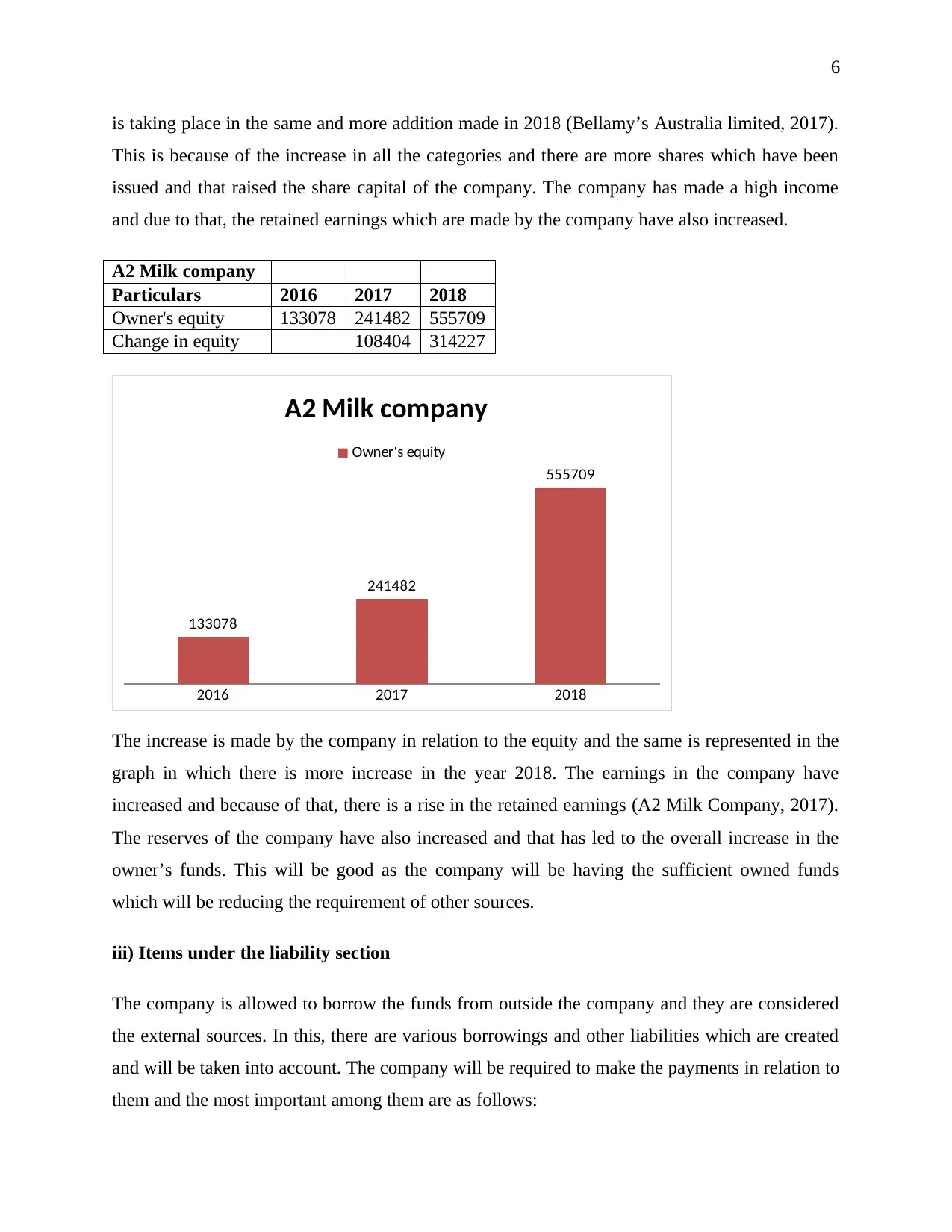

A2 Milk company

Particulars 2016 2017 2018

Owner's equity 133078 241482 555709

Change in equity 108404 314227

2016 2017 2018

133078

241482

555709

A2 Milk company

Owner's equity

The increase is made by the company in relation to the equity and the same is represented in the

graph in which there is more increase in the year 2018. The earnings in the company have

increased and because of that, there is a rise in the retained earnings (A2 Milk Company, 2017).

The reserves of the company have also increased and that has led to the overall increase in the

owner’s funds. This will be good as the company will be having the sufficient owned funds

which will be reducing the requirement of other sources.

iii) Items under the liability section

The company is allowed to borrow the funds from outside the company and they are considered

the external sources. In this, there are various borrowings and other liabilities which are created

and will be taken into account. The company will be required to make the payments in relation to

them and the most important among them are as follows:

is taking place in the same and more addition made in 2018 (Bellamy’s Australia limited, 2017).

This is because of the increase in all the categories and there are more shares which have been

issued and that raised the share capital of the company. The company has made a high income

and due to that, the retained earnings which are made by the company have also increased.

A2 Milk company

Particulars 2016 2017 2018

Owner's equity 133078 241482 555709

Change in equity 108404 314227

2016 2017 2018

133078

241482

555709

A2 Milk company

Owner's equity

The increase is made by the company in relation to the equity and the same is represented in the

graph in which there is more increase in the year 2018. The earnings in the company have

increased and because of that, there is a rise in the retained earnings (A2 Milk Company, 2017).

The reserves of the company have also increased and that has led to the overall increase in the

owner’s funds. This will be good as the company will be having the sufficient owned funds

which will be reducing the requirement of other sources.

iii) Items under the liability section

The company is allowed to borrow the funds from outside the company and they are considered

the external sources. In this, there are various borrowings and other liabilities which are created

and will be taken into account. The company will be required to make the payments in relation to

them and the most important among them are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Borrowings: Under this, the company will be taking funds from the external financial institutes

and there will be various laws which will be applicable in this respect (He and Xiong, 2012).

They will be required to pay the interest at the fixed rate which is provided in the loan

agreement. The repayment of the debt will be made as per the contract and there will be

installments which will be involved in the same.

Provisions: The Company is required to consider all of the risks which are involved in the

business for the payments which will be received in the coming period. This is done with the

help of the creation of the provisions in which an amount is secured in respect of the particular

activity. This will be maintained by the company till the risk is not eliminated and once the same

is done the provision will be written off.

Income Tax payable: There are certain legal liabilities also which are to be met by the company

and they shall be taken into account in the best possible manner. The earning which is made is

the income o the company and on the same, it is required to pay the tax which is at the fixed rate

and will be paid at the time they are due (Nassr and Wehinger, 2014). There will be an amount

which will be required for the same and it will be provided in the accounts in relation to the

same.

Trade payable: There are various parties to whom the amount is payable on the purchases which

are made from them. The company does not have that amount of cash to make all the purchases

by the same. Due to the same, the company will be required to make the credit purchases and an

amount will be due on them which are identified as the trade payables. With the help of this, the

funds are available on a temporary basis or it can be said that company cam purchase without

making the payment instantly.

iv) Changes in items involved in liabilities

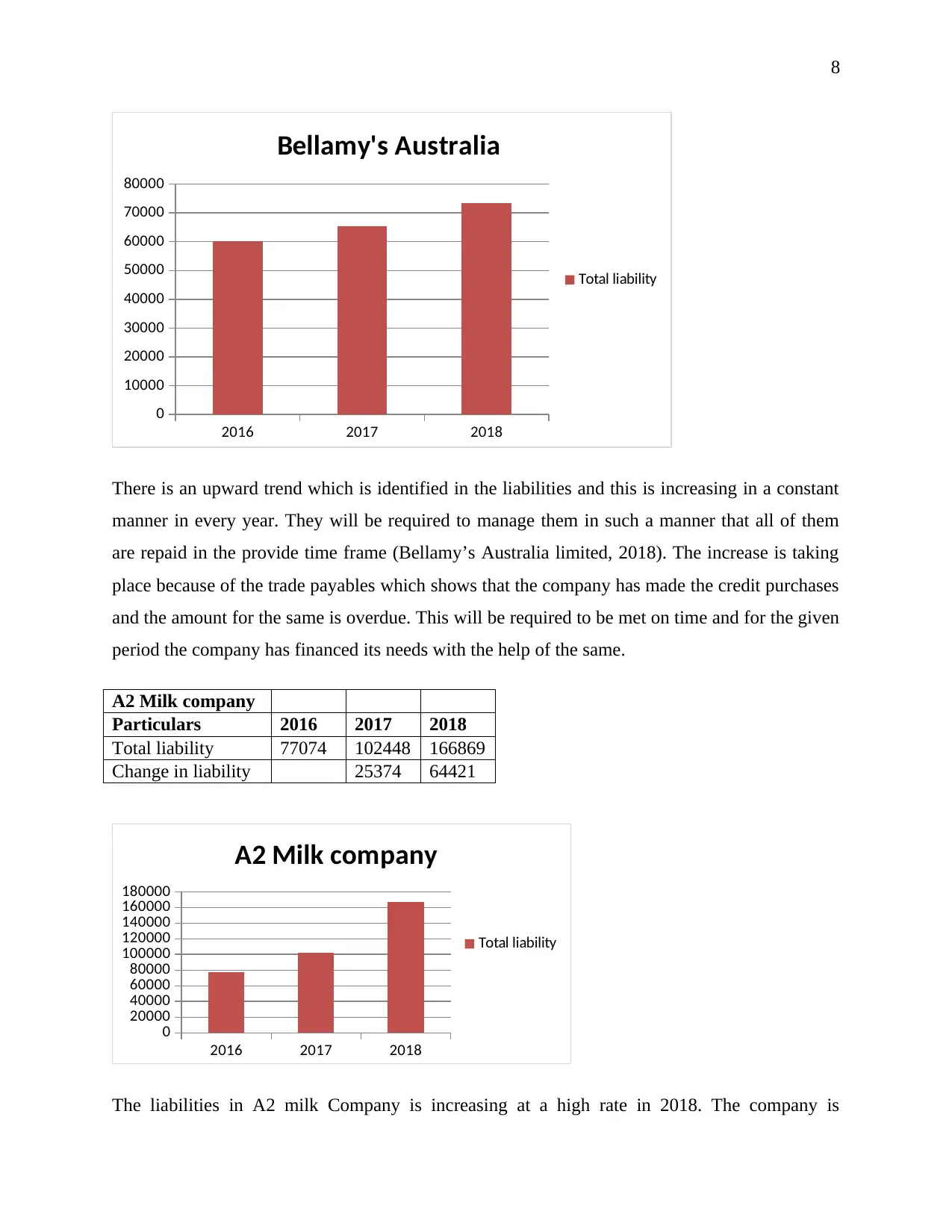

Bellamy's

Australia

Particulars 2016 2017 2018

Total liability 60280 65382 73454

Change in liability 5102 8072

Borrowings: Under this, the company will be taking funds from the external financial institutes

and there will be various laws which will be applicable in this respect (He and Xiong, 2012).

They will be required to pay the interest at the fixed rate which is provided in the loan

agreement. The repayment of the debt will be made as per the contract and there will be

installments which will be involved in the same.

Provisions: The Company is required to consider all of the risks which are involved in the

business for the payments which will be received in the coming period. This is done with the

help of the creation of the provisions in which an amount is secured in respect of the particular

activity. This will be maintained by the company till the risk is not eliminated and once the same

is done the provision will be written off.

Income Tax payable: There are certain legal liabilities also which are to be met by the company

and they shall be taken into account in the best possible manner. The earning which is made is

the income o the company and on the same, it is required to pay the tax which is at the fixed rate

and will be paid at the time they are due (Nassr and Wehinger, 2014). There will be an amount

which will be required for the same and it will be provided in the accounts in relation to the

same.

Trade payable: There are various parties to whom the amount is payable on the purchases which

are made from them. The company does not have that amount of cash to make all the purchases

by the same. Due to the same, the company will be required to make the credit purchases and an

amount will be due on them which are identified as the trade payables. With the help of this, the

funds are available on a temporary basis or it can be said that company cam purchase without

making the payment instantly.

iv) Changes in items involved in liabilities

Bellamy's

Australia

Particulars 2016 2017 2018

Total liability 60280 65382 73454

Change in liability 5102 8072

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

2016 2017 2018

0

10000

20000

30000

40000

50000

60000

70000

80000

Bellamy's Australia

Total liability

There is an upward trend which is identified in the liabilities and this is increasing in a constant

manner in every year. They will be required to manage them in such a manner that all of them

are repaid in the provide time frame (Bellamy’s Australia limited, 2018). The increase is taking

place because of the trade payables which shows that the company has made the credit purchases

and the amount for the same is overdue. This will be required to be met on time and for the given

period the company has financed its needs with the help of the same.

A2 Milk company

Particulars 2016 2017 2018

Total liability 77074 102448 166869

Change in liability 25374 64421

2016 2017 2018

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

A2 Milk company

Total liability

The liabilities in A2 milk Company is increasing at a high rate in 2018. The company is

2016 2017 2018

0

10000

20000

30000

40000

50000

60000

70000

80000

Bellamy's Australia

Total liability

There is an upward trend which is identified in the liabilities and this is increasing in a constant

manner in every year. They will be required to manage them in such a manner that all of them

are repaid in the provide time frame (Bellamy’s Australia limited, 2018). The increase is taking

place because of the trade payables which shows that the company has made the credit purchases

and the amount for the same is overdue. This will be required to be met on time and for the given

period the company has financed its needs with the help of the same.

A2 Milk company

Particulars 2016 2017 2018

Total liability 77074 102448 166869

Change in liability 25374 64421

2016 2017 2018

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

A2 Milk company

Total liability

The liabilities in A2 milk Company is increasing at a high rate in 2018. The company is

9

involving the accounts payable in its accounts and they are increasing rapidly. The company will

be required to make the proper steps by which the situation can be controlled (A2 Milk

Company, 2018). There is also the increase in the tax payable which is because of the increase in

the earnings which is made by the company.

v) Merits and demerits of the sources of funds

The sources which are used by the company have several impacts on the business and that is

required to be taken into consideration so that the decisions can be made by the company in

relation to that. The consideration will be given and the source which will be providing the

company with the additional benefits will be taken into account. There is the more use of the

equity which is beneficial as there is no additional payment which needs to be made in the same.

There will be the owner of the company but the company will need to maintain the appropriate

level under this. If there will be more issue which will be made then the ownership of the

business will be in danger (Abdulsaleh and Worthington, 2013). To control the same there will

be adequate analysis and then the appropriate amount will be issues in public. If the liabilities an

into account then the company will have to consider the coverage ratio and will have to identify

the amount for which the liability can be borne in a proper manner. There is the payment of the

interest which will be made and so the amount of the liability shall be such for which the interest

can be paid with the available earnings (Chinaemerem and Anayochukwu, 2013). The company

has the option to raise a high amount with this but this will be creating the liability for the

company.

All of these are the important parts and needs to be considered in the making of any decision.

The company is required to choose the funds in a very correct manner and for that they will be

required to take the advantages as well as the disadvantages in consideration. By that benefits

will be made and there will be no issues which will be faced for the coming period. The decision

shall be such which will be overall cost of the funds will be reduced and company will be able to

save the additional funds.

involving the accounts payable in its accounts and they are increasing rapidly. The company will

be required to make the proper steps by which the situation can be controlled (A2 Milk

Company, 2018). There is also the increase in the tax payable which is because of the increase in

the earnings which is made by the company.

v) Merits and demerits of the sources of funds

The sources which are used by the company have several impacts on the business and that is

required to be taken into consideration so that the decisions can be made by the company in

relation to that. The consideration will be given and the source which will be providing the

company with the additional benefits will be taken into account. There is the more use of the

equity which is beneficial as there is no additional payment which needs to be made in the same.

There will be the owner of the company but the company will need to maintain the appropriate

level under this. If there will be more issue which will be made then the ownership of the

business will be in danger (Abdulsaleh and Worthington, 2013). To control the same there will

be adequate analysis and then the appropriate amount will be issues in public. If the liabilities an

into account then the company will have to consider the coverage ratio and will have to identify

the amount for which the liability can be borne in a proper manner. There is the payment of the

interest which will be made and so the amount of the liability shall be such for which the interest

can be paid with the available earnings (Chinaemerem and Anayochukwu, 2013). The company

has the option to raise a high amount with this but this will be creating the liability for the

company.

All of these are the important parts and needs to be considered in the making of any decision.

The company is required to choose the funds in a very correct manner and for that they will be

required to take the advantages as well as the disadvantages in consideration. By that benefits

will be made and there will be no issues which will be faced for the coming period. The decision

shall be such which will be overall cost of the funds will be reduced and company will be able to

save the additional funds.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Part B

Large and small proprietary company-related concept

The classification of the company is made in various categories and in that there is the need for

the proper identification of the conditions which are responsible for the same. There are various

laws which are applicable and in that the conditions are specified according to which the

classification of the large proprietary company and the small proprietary company will be made

(ASIC, 2019). The conditions which will be describing the large companies are as provided

below:

The revenue before 1 July 2019 should be 25 million or more and after this date, the revenue

will be made at the $50 million or more.

The employees count shall be more than 50 before 1 July 2019 and after that, it shall be

maintained at 100 or more employees.

The limit for the gross total assets is also specified and in that there will be the maintenance

of the assets at or above the level of $25 million after 1 July 2019 and before that at $12.5

million.

There will be the maintenance of the conditions which are provided above and with the

completion of any of two, there will be the identification of the company as the large proprietary.

If this will not be made possible then the company will be a small proprietary company. These

conditions will be taken into account and decisions will be made accordingly. In the given the

case, there is the fulfillment of the conditions and the company will be considered as the large

proprietary company.

Compliance and reporting requirements

The company will be categorized in any of the class and with that, there will be various

obligations which will be created on them. There are several requirements which need to be

followed by the company and the compliance will be made when the identification of the

reporting requirements will be made. It has been identified that the company which will be

considered as the large proprietary company will be making all of the financial and director’s

reports. They will be preparing them in an adequate manner and then the same will be provided

Part B

Large and small proprietary company-related concept

The classification of the company is made in various categories and in that there is the need for

the proper identification of the conditions which are responsible for the same. There are various

laws which are applicable and in that the conditions are specified according to which the

classification of the large proprietary company and the small proprietary company will be made

(ASIC, 2019). The conditions which will be describing the large companies are as provided

below:

The revenue before 1 July 2019 should be 25 million or more and after this date, the revenue

will be made at the $50 million or more.

The employees count shall be more than 50 before 1 July 2019 and after that, it shall be

maintained at 100 or more employees.

The limit for the gross total assets is also specified and in that there will be the maintenance

of the assets at or above the level of $25 million after 1 July 2019 and before that at $12.5

million.

There will be the maintenance of the conditions which are provided above and with the

completion of any of two, there will be the identification of the company as the large proprietary.

If this will not be made possible then the company will be a small proprietary company. These

conditions will be taken into account and decisions will be made accordingly. In the given the

case, there is the fulfillment of the conditions and the company will be considered as the large

proprietary company.

Compliance and reporting requirements

The company will be categorized in any of the class and with that, there will be various

obligations which will be created on them. There are several requirements which need to be

followed by the company and the compliance will be made when the identification of the

reporting requirements will be made. It has been identified that the company which will be

considered as the large proprietary company will be making all of the financial and director’s

reports. They will be preparing them in an adequate manner and then the same will be provided

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

to the specified authorities. There will be proper submission which will be made and the time

limit is made which will be followed in relation to them for all the years. It will also be required

to undertake the audit procedure which is mandatory and in that all of the accounts will be

considered in the process of auditing (Yang and Jia, 2012). This will be required to be performed

in a compulsory manner and the company will have to follow them until the relaxation is

provided by ASIC.

The conditions and compliance requirements which are specified will be applicable to the large

company in a compulsory manner bur the small company has the option to consider them or not.

If they wish to carry the provided procedure then no restriction is imposed but it will not be

mandatory for them to undertake the provided process. It is always of the benefit for the

company if the requirements are fulfilled and the accounts are kept in an appropriate manner.

Due to this it shall be noted by all that there are various steps which are taken and by the help of

them the best of the results will be attained.

Conclusion

The analysis of the equity and liabilities has been made in the report for the A2 milk Company

and Bellamy Australia Company. In that, all of the elements which are involved have been

identified and considered in the report. The categorization of them is made in an effective

manner and the fluctuations which are taking place have been taken into account into an account

in an appropriate manner. The reasons for the fluctuations have also been identified and given in

the report. There is the description of all the liabilities which are involved and with that, the

obligations which are faced by the company are incorporated appropriately. There is the

identification of the concept which is applicable to the large and small companies. The

compliance requirement for them which needs to be fulfilled has also been identified.

to the specified authorities. There will be proper submission which will be made and the time

limit is made which will be followed in relation to them for all the years. It will also be required

to undertake the audit procedure which is mandatory and in that all of the accounts will be

considered in the process of auditing (Yang and Jia, 2012). This will be required to be performed

in a compulsory manner and the company will have to follow them until the relaxation is

provided by ASIC.

The conditions and compliance requirements which are specified will be applicable to the large

company in a compulsory manner bur the small company has the option to consider them or not.

If they wish to carry the provided procedure then no restriction is imposed but it will not be

mandatory for them to undertake the provided process. It is always of the benefit for the

company if the requirements are fulfilled and the accounts are kept in an appropriate manner.

Due to this it shall be noted by all that there are various steps which are taken and by the help of

them the best of the results will be attained.

Conclusion

The analysis of the equity and liabilities has been made in the report for the A2 milk Company

and Bellamy Australia Company. In that, all of the elements which are involved have been

identified and considered in the report. The categorization of them is made in an effective

manner and the fluctuations which are taking place have been taken into account into an account

in an appropriate manner. The reasons for the fluctuations have also been identified and given in

the report. There is the description of all the liabilities which are involved and with that, the

obligations which are faced by the company are incorporated appropriately. There is the

identification of the concept which is applicable to the large and small companies. The

compliance requirement for them which needs to be fulfilled has also been identified.

12

References

A2 Milk Company. (2017) annual report. [Online] Available at:

https://thea2milkcompany.com/wp-content/uploads/The-a2-Milk-2016-2017-Annual-Report-

spreads.pdf [Accessed 24 September 2019]

A2 Milk Company. (2018) annual report. [Online] Available at:

https://thea2milkcompany.com/wp-content/uploads/A2M-Annual-Report-FY18.pdf [Accessed

24 September 2019]

Abdulsaleh, A.M. and Worthington, A.C. (2013) Small and medium-sized enterprises financing:

A review of literature. International Journal of Business and Management, 8(14), p.36.

ASIC. (2019) Are you a large or small proprietary company. [Online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-financial-

reports/are-you-a-large-or-small-proprietary-company/ [Accessed 24 September 2019]

Bellamy’s Australia limited. (2017) annual report. [Online] Available at:

http://www.annualreports.com/HostedData/AnnualReportArchive/B/ASX_BAL_2017.pdf

[Accessed 24 September 2019]

Bellamy’s Australia limited. (2018) annual report. [Online] Available at:

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_BAL_2018.pdf [Accessed

24 September 2019]

Boubakri, N., Guedhami, O., Mishra, D. and Saffar, W. (2012) Political connections and the cost

of equity capital. Journal of corporate finance, 18(3), pp.541-559.

Chinaemerem, O.C. and Anayochukwu, O.B. (2013) Impact of external debt financing on

economic development in Nigeria. Research Journal of Finance and Accounting, 4(4), pp.92-98.

He, Z. and Xiong, W. (2012) Debt financing in asset markets. American Economic

Review, 102(3), pp.88-94.

Nassr, I.K. and Wehinger, G. (2014) Non-bank debt financing for SMEs. OECD Journal:

References

A2 Milk Company. (2017) annual report. [Online] Available at:

https://thea2milkcompany.com/wp-content/uploads/The-a2-Milk-2016-2017-Annual-Report-

spreads.pdf [Accessed 24 September 2019]

A2 Milk Company. (2018) annual report. [Online] Available at:

https://thea2milkcompany.com/wp-content/uploads/A2M-Annual-Report-FY18.pdf [Accessed

24 September 2019]

Abdulsaleh, A.M. and Worthington, A.C. (2013) Small and medium-sized enterprises financing:

A review of literature. International Journal of Business and Management, 8(14), p.36.

ASIC. (2019) Are you a large or small proprietary company. [Online] Available at:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/preparers-of-financial-

reports/are-you-a-large-or-small-proprietary-company/ [Accessed 24 September 2019]

Bellamy’s Australia limited. (2017) annual report. [Online] Available at:

http://www.annualreports.com/HostedData/AnnualReportArchive/B/ASX_BAL_2017.pdf

[Accessed 24 September 2019]

Bellamy’s Australia limited. (2018) annual report. [Online] Available at:

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_BAL_2018.pdf [Accessed

24 September 2019]

Boubakri, N., Guedhami, O., Mishra, D. and Saffar, W. (2012) Political connections and the cost

of equity capital. Journal of corporate finance, 18(3), pp.541-559.

Chinaemerem, O.C. and Anayochukwu, O.B. (2013) Impact of external debt financing on

economic development in Nigeria. Research Journal of Finance and Accounting, 4(4), pp.92-98.

He, Z. and Xiong, W. (2012) Debt financing in asset markets. American Economic

Review, 102(3), pp.88-94.

Nassr, I.K. and Wehinger, G. (2014) Non-bank debt financing for SMEs. OECD Journal:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.