Corporate Finance: Project Analysis and Investment Decisions

VerifiedAdded on 2022/08/16

|20

|4522

|19

Report

AI Summary

This report provides a comprehensive analysis of three projects (A1, A2, and B) from a Corporate Finance perspective, focusing on project evaluation and capital investment decisions. The report explores various methodologies, including Net Present Value (NPV) and Internal Rate of Return (IRR), to assess project viability. It delves into the concept of the Marginal Cost of Capital (MCC), its calculation, and its impact on investment choices. The discussion covers the MCC curve, break-even points, and the influence of dividend policy on capital investment. The report recommends which projects should be accepted or rejected, based on quantitative analysis and financial metrics, with a focus on maximizing shareholder value. The analysis includes detailed calculations and considerations from an upper-level management perspective, aligning with the assignment brief's requirements.

Running Head: CORPORATE FINANCE

Corporate Finance

Name of the University

Name of the Student

Author Name

Corporate Finance

Name of the University

Name of the Student

Author Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE FINANCE

Table of Contents

1. Introduction..................................................................................................................................2

2. Discussion....................................................................................................................................2

2.1. Project Evaluation.................................................................................................................2

2.2. Different types of methodology used for project evaluation................................................2

2.2. a NPV or Net Present Net Value..........................................................................................3

2.2.b IRR or Internal Rate of Return...........................................................................................5

2.3. Marginal Cost of Capital:.....................................................................................................6

2.4. MCC Curve and break-even.................................................................................................8

2.5. Impact on dividend policy on capital investment.................................................................9

3. Conclusion.................................................................................................................................12

References......................................................................................................................................14

Appendice......................................................................................................................................17

Table of Contents

1. Introduction..................................................................................................................................2

2. Discussion....................................................................................................................................2

2.1. Project Evaluation.................................................................................................................2

2.2. Different types of methodology used for project evaluation................................................2

2.2. a NPV or Net Present Net Value..........................................................................................3

2.2.b IRR or Internal Rate of Return...........................................................................................5

2.3. Marginal Cost of Capital:.....................................................................................................6

2.4. MCC Curve and break-even.................................................................................................8

2.5. Impact on dividend policy on capital investment.................................................................9

3. Conclusion.................................................................................................................................12

References......................................................................................................................................14

Appendice......................................................................................................................................17

2CORPORATE FINANCE

1. Introduction

This paper evaluates and discusses the three projects A1, A2 and B,which based on “the

marginal cost of capital” or “weighted average marginal cost of capital”. Evaluation and

analyzing these three projects will result in accepting which project and which project to reject.

This report discusses the types or techniques of the marginal cost of capital and its application

while evaluating the solution.There are various techniques and methodology for selecting the

desired projects. The discussion part includes evaluation and analysis of a project, computation

of Weighted Average cost of capital, and analysis of MCC curve. The recommendation will be

based on quantitative analysis.

2. Discussion

2.1. Project Evaluation

The evaluation of the project deals with a systematic assessment of the given project,

policy, investment and program along with planning, application, and monitoring the effects.

Project evaluation provides information which helps to make the decision process (Ilo.org,

2020).Its objective is to correctly distinguish the level of achievement of the project, its

efficiency, effects, and maintaining the level.

Project analysis is used to evaluate the investment and determine the value of asset or

business. However, valuation analysis is the responsibility of an investor, as cash flow valuation

is an essential part in a long term basis (Razzaq, 2018).

2.2. Different types of methodology used for project evaluation

The methodsused for project evaluation on proposed projects are (Master, 2017).

1. Introduction

This paper evaluates and discusses the three projects A1, A2 and B,which based on “the

marginal cost of capital” or “weighted average marginal cost of capital”. Evaluation and

analyzing these three projects will result in accepting which project and which project to reject.

This report discusses the types or techniques of the marginal cost of capital and its application

while evaluating the solution.There are various techniques and methodology for selecting the

desired projects. The discussion part includes evaluation and analysis of a project, computation

of Weighted Average cost of capital, and analysis of MCC curve. The recommendation will be

based on quantitative analysis.

2. Discussion

2.1. Project Evaluation

The evaluation of the project deals with a systematic assessment of the given project,

policy, investment and program along with planning, application, and monitoring the effects.

Project evaluation provides information which helps to make the decision process (Ilo.org,

2020).Its objective is to correctly distinguish the level of achievement of the project, its

efficiency, effects, and maintaining the level.

Project analysis is used to evaluate the investment and determine the value of asset or

business. However, valuation analysis is the responsibility of an investor, as cash flow valuation

is an essential part in a long term basis (Razzaq, 2018).

2.2. Different types of methodology used for project evaluation

The methodsused for project evaluation on proposed projects are (Master, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE FINANCE

NPV or “Net Present Value”

IRR or “Internal rate of return”

Profitability index

Payback method

These methods used in the proposed project to bring success and development. It shows

clarity of projects in terms of available funds and economy and a project with available debt and

shareholders' fund will reflect a good project.

The Discounted Cash flow method is used to calculate the investment value based on

future cash flow; it calculates the net present value of a project. It discounts or reduces future

value into the present value at a discounted rate (Lilford, Maybee,&Packey, 2018). This

technique used in the two methods are

NPV method

IRR methods

These two methods are conflicting in the mutually exclusive project and the independent

project, which is discussed below.

2.2. aNPV or Net Present Net Value

It is mainly a difference between “the present value of cash inflow” and “the present

value of cash outflow” over a period of time. It is also be termed as a discounted cash flow

method, which an essential technique in the capital is budgeting. The application of net present

value helps to accept or reject the proposal on the basis of investment or cash flow. A projected

net present value is calculated by adding the net cash flow, discounted factor of cost of capital

NPV or “Net Present Value”

IRR or “Internal rate of return”

Profitability index

Payback method

These methods used in the proposed project to bring success and development. It shows

clarity of projects in terms of available funds and economy and a project with available debt and

shareholders' fund will reflect a good project.

The Discounted Cash flow method is used to calculate the investment value based on

future cash flow; it calculates the net present value of a project. It discounts or reduces future

value into the present value at a discounted rate (Lilford, Maybee,&Packey, 2018). This

technique used in the two methods are

NPV method

IRR methods

These two methods are conflicting in the mutually exclusive project and the independent

project, which is discussed below.

2.2. aNPV or Net Present Net Value

It is mainly a difference between “the present value of cash inflow” and “the present

value of cash outflow” over a period of time. It is also be termed as a discounted cash flow

method, which an essential technique in the capital is budgeting. The application of net present

value helps to accept or reject the proposal on the basis of investment or cash flow. A projected

net present value is calculated by adding the net cash flow, discounted factor of cost of capital

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE FINANCE

and deducting the initial outlay value. Based on these decisions can be made on the projects,

whether to accept or reject (Razzaq, 2018).

The advantage of the NPV method is it reflects a clear time value of money and helps the

management to decide a better overview of the Company. The disadvantages of Net present

value is, it does not follow any guideline to evaluate the necessary rate of return, it is rank based

on the cost of the capital where the present value decline when the discountedrate increase and

vice-versa.

The net present value can be “positive” or “negative” or “zero” (Karpov,& Shevchenko-

Perepolkina, 2017). This can be explained as under

A Positive NPV is determined when the present value of cash inflow greater than the

present value of cash outflow, where the investment proposal is accepted for this case.

Because the revenue is more than the cost and investor can generate profit from this

investment proposal.

A Negative NPV is determined when the present value of cash inflow lesser than the

present value of cash outflow, then the investment proposal is to be rejected. Because the

investment is low to make any business profit.

Zero NPV is determined when the present value of cash inflow equal to the present value

of cash outflow which implies that there is no profit or no loss and this proposal can be

accepted as an investment is not making any loss, it shows that investment earns a rate of

return which is equal to a discounted rate.

In the projected cash flow project A1, A2 which are “mutually exclusive”and B project is

“independent” shows that between the two mutually exclusive projects where one project can be

and deducting the initial outlay value. Based on these decisions can be made on the projects,

whether to accept or reject (Razzaq, 2018).

The advantage of the NPV method is it reflects a clear time value of money and helps the

management to decide a better overview of the Company. The disadvantages of Net present

value is, it does not follow any guideline to evaluate the necessary rate of return, it is rank based

on the cost of the capital where the present value decline when the discountedrate increase and

vice-versa.

The net present value can be “positive” or “negative” or “zero” (Karpov,& Shevchenko-

Perepolkina, 2017). This can be explained as under

A Positive NPV is determined when the present value of cash inflow greater than the

present value of cash outflow, where the investment proposal is accepted for this case.

Because the revenue is more than the cost and investor can generate profit from this

investment proposal.

A Negative NPV is determined when the present value of cash inflow lesser than the

present value of cash outflow, then the investment proposal is to be rejected. Because the

investment is low to make any business profit.

Zero NPV is determined when the present value of cash inflow equal to the present value

of cash outflow which implies that there is no profit or no loss and this proposal can be

accepted as an investment is not making any loss, it shows that investment earns a rate of

return which is equal to a discounted rate.

In the projected cash flow project A1, A2 which are “mutually exclusive”and B project is

“independent” shows that between the two mutually exclusive projects where one project can be

5CORPORATE FINANCE

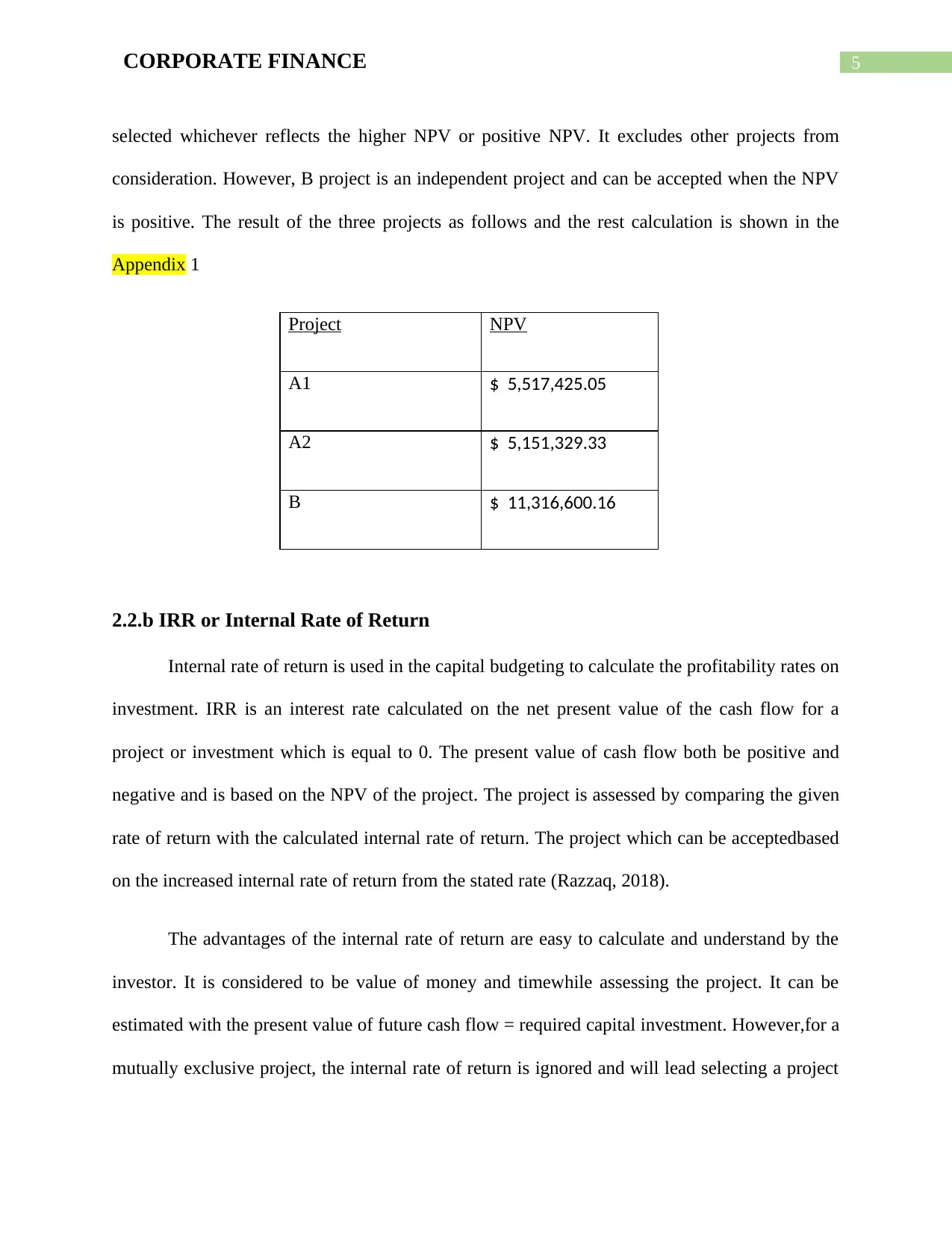

selected whichever reflects the higher NPV or positive NPV. It excludes other projects from

consideration. However, B project is an independent project and can be accepted when the NPV

is positive. The result of the three projects as follows and the rest calculation is shown in the

Appendix 1

Project NPV

A1 $ 5,517,425.05

A2 $ 5,151,329.33

B $ 11,316,600.16

2.2.b IRR or Internal Rate of Return

Internal rate of return is used in the capital budgeting to calculate the profitability rates on

investment. IRR is an interest rate calculated on the net present value of the cash flow for a

project or investment which is equal to 0. The present value of cash flow both be positive and

negative and is based on the NPV of the project. The project is assessed by comparing the given

rate of return with the calculated internal rate of return. The project which can be acceptedbased

on the increased internal rate of return from the stated rate (Razzaq, 2018).

The advantages of the internal rate of return are easy to calculate and understand by the

investor. It is considered to be value of money and timewhile assessing the project. It can be

estimated with the present value of future cash flow = required capital investment. However,for a

mutually exclusive project, the internal rate of return is ignored and will lead selecting a project

selected whichever reflects the higher NPV or positive NPV. It excludes other projects from

consideration. However, B project is an independent project and can be accepted when the NPV

is positive. The result of the three projects as follows and the rest calculation is shown in the

Appendix 1

Project NPV

A1 $ 5,517,425.05

A2 $ 5,151,329.33

B $ 11,316,600.16

2.2.b IRR or Internal Rate of Return

Internal rate of return is used in the capital budgeting to calculate the profitability rates on

investment. IRR is an interest rate calculated on the net present value of the cash flow for a

project or investment which is equal to 0. The present value of cash flow both be positive and

negative and is based on the NPV of the project. The project is assessed by comparing the given

rate of return with the calculated internal rate of return. The project which can be acceptedbased

on the increased internal rate of return from the stated rate (Razzaq, 2018).

The advantages of the internal rate of return are easy to calculate and understand by the

investor. It is considered to be value of money and timewhile assessing the project. It can be

estimated with the present value of future cash flow = required capital investment. However,for a

mutually exclusive project, the internal rate of return is ignored and will lead selecting a project

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE FINANCE

which does not maximize the shareholders' fund. For mutually exclusive project there will be a

conflict of choosing anyone or both projects like if a project which has higher NPV and another

project which has higher IRR can raise a dispute to select which project (Patrick, & French,

2016). In case of an independent project which is project B, whose IRR is 19.77% more than the

marginal cost of capital is 10.06% then the project B has to be accepted, or any other project

which is more than the cost of capital and is allowed in the budget. For a mutually exclusive

project like A1 and A2 both project IRR is more than the MCC; hence any one project can be

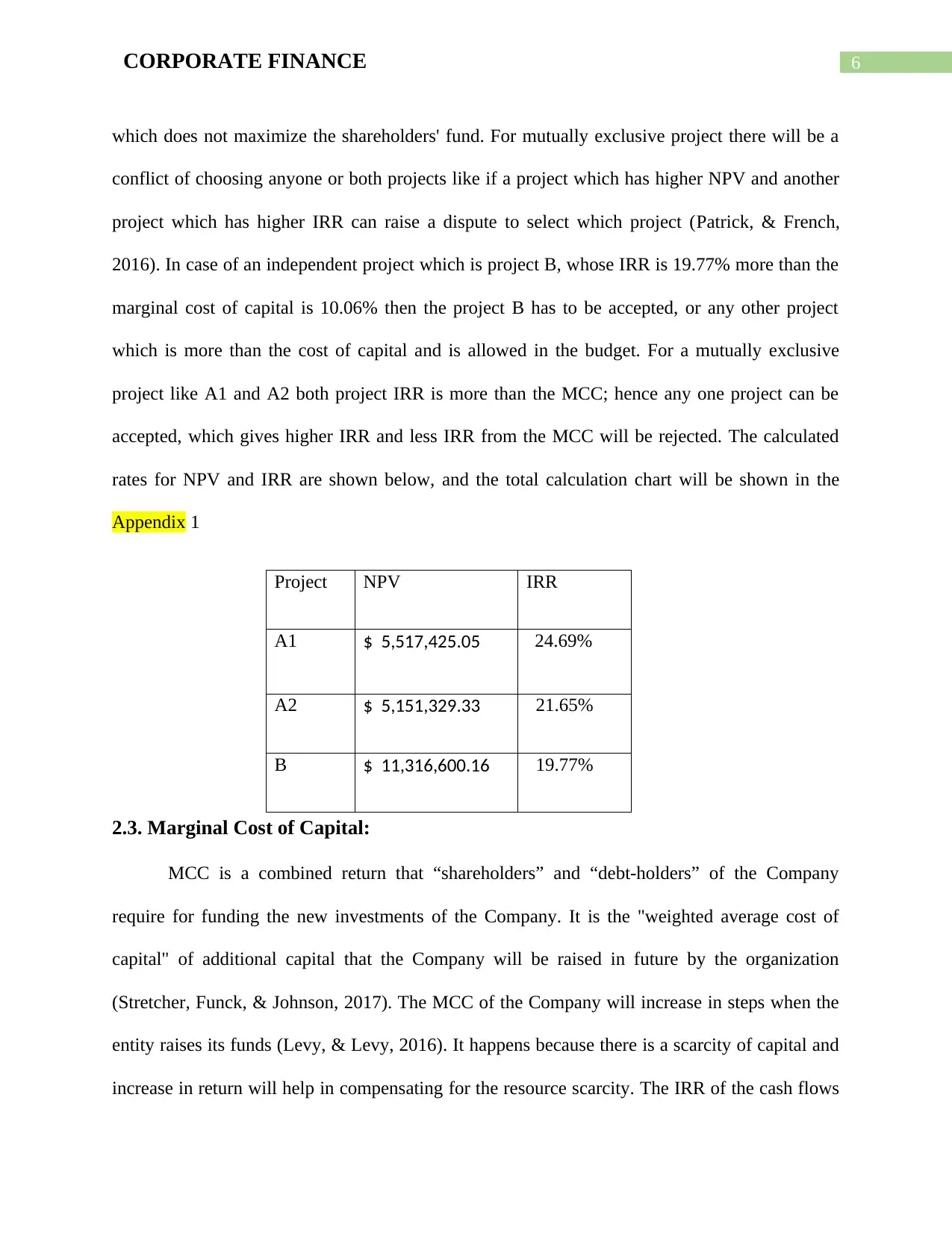

accepted, which gives higher IRR and less IRR from the MCC will be rejected. The calculated

rates for NPV and IRR are shown below, and the total calculation chart will be shown in the

Appendix 1

Project NPV IRR

A1 $ 5,517,425.05 24.69%

A2 $ 5,151,329.33 21.65%

B $ 11,316,600.16 19.77%

2.3. Marginal Cost of Capital:

MCC is a combined return that “shareholders” and “debt-holders” of the Company

require for funding the new investments of the Company. It is the "weighted average cost of

capital" of additional capital that the Company will be raised in future by the organization

(Stretcher, Funck, & Johnson, 2017). The MCC of the Company will increase in steps when the

entity raises its funds (Levy, & Levy, 2016). It happens because there is a scarcity of capital and

increase in return will help in compensating for the resource scarcity. The IRR of the cash flows

which does not maximize the shareholders' fund. For mutually exclusive project there will be a

conflict of choosing anyone or both projects like if a project which has higher NPV and another

project which has higher IRR can raise a dispute to select which project (Patrick, & French,

2016). In case of an independent project which is project B, whose IRR is 19.77% more than the

marginal cost of capital is 10.06% then the project B has to be accepted, or any other project

which is more than the cost of capital and is allowed in the budget. For a mutually exclusive

project like A1 and A2 both project IRR is more than the MCC; hence any one project can be

accepted, which gives higher IRR and less IRR from the MCC will be rejected. The calculated

rates for NPV and IRR are shown below, and the total calculation chart will be shown in the

Appendix 1

Project NPV IRR

A1 $ 5,517,425.05 24.69%

A2 $ 5,151,329.33 21.65%

B $ 11,316,600.16 19.77%

2.3. Marginal Cost of Capital:

MCC is a combined return that “shareholders” and “debt-holders” of the Company

require for funding the new investments of the Company. It is the "weighted average cost of

capital" of additional capital that the Company will be raised in future by the organization

(Stretcher, Funck, & Johnson, 2017). The MCC of the Company will increase in steps when the

entity raises its funds (Levy, & Levy, 2016). It happens because there is a scarcity of capital and

increase in return will help in compensating for the resource scarcity. The IRR of the cash flows

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE FINANCE

will be compared to the MCC to evaluate the projects and where the NPV of projects is more

than 0, the IRR will be higher than the cost of capital and project will be selected whose IRR is

higher, and provides higher NPV (Lilford, Maybee, &Packey, 2018). The Company should raise

additional funds or not for investing in the new project is evaluated by the help of MCC.

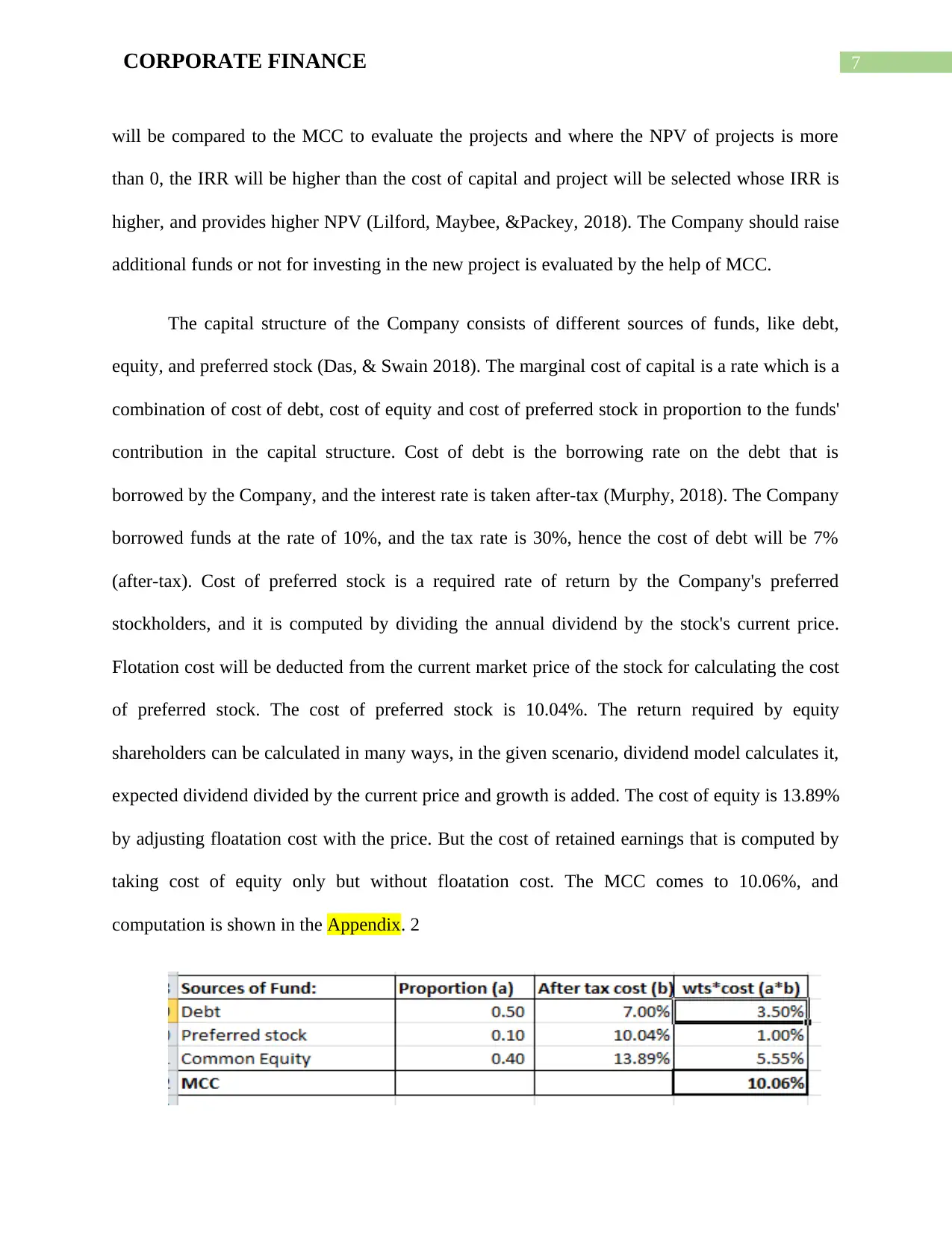

The capital structure of the Company consists of different sources of funds, like debt,

equity, and preferred stock (Das, & Swain 2018). The marginal cost of capital is a rate which is a

combination of cost of debt, cost of equity and cost of preferred stock in proportion to the funds'

contribution in the capital structure. Cost of debt is the borrowing rate on the debt that is

borrowed by the Company, and the interest rate is taken after-tax (Murphy, 2018). The Company

borrowed funds at the rate of 10%, and the tax rate is 30%, hence the cost of debt will be 7%

(after-tax). Cost of preferred stock is a required rate of return by the Company's preferred

stockholders, and it is computed by dividing the annual dividend by the stock's current price.

Flotation cost will be deducted from the current market price of the stock for calculating the cost

of preferred stock. The cost of preferred stock is 10.04%. The return required by equity

shareholders can be calculated in many ways, in the given scenario, dividend model calculates it,

expected dividend divided by the current price and growth is added. The cost of equity is 13.89%

by adjusting floatation cost with the price. But the cost of retained earnings that is computed by

taking cost of equity only but without floatation cost. The MCC comes to 10.06%, and

computation is shown in the Appendix. 2

will be compared to the MCC to evaluate the projects and where the NPV of projects is more

than 0, the IRR will be higher than the cost of capital and project will be selected whose IRR is

higher, and provides higher NPV (Lilford, Maybee, &Packey, 2018). The Company should raise

additional funds or not for investing in the new project is evaluated by the help of MCC.

The capital structure of the Company consists of different sources of funds, like debt,

equity, and preferred stock (Das, & Swain 2018). The marginal cost of capital is a rate which is a

combination of cost of debt, cost of equity and cost of preferred stock in proportion to the funds'

contribution in the capital structure. Cost of debt is the borrowing rate on the debt that is

borrowed by the Company, and the interest rate is taken after-tax (Murphy, 2018). The Company

borrowed funds at the rate of 10%, and the tax rate is 30%, hence the cost of debt will be 7%

(after-tax). Cost of preferred stock is a required rate of return by the Company's preferred

stockholders, and it is computed by dividing the annual dividend by the stock's current price.

Flotation cost will be deducted from the current market price of the stock for calculating the cost

of preferred stock. The cost of preferred stock is 10.04%. The return required by equity

shareholders can be calculated in many ways, in the given scenario, dividend model calculates it,

expected dividend divided by the current price and growth is added. The cost of equity is 13.89%

by adjusting floatation cost with the price. But the cost of retained earnings that is computed by

taking cost of equity only but without floatation cost. The MCC comes to 10.06%, and

computation is shown in the Appendix. 2

8CORPORATE FINANCE

IRR will help in evaluating the profitability of potential projects (Kulakov, &Kastro,

2017). The IRR for the three projects is calculated by considering the net cash flows for the

given period of time for each project separately. IRR among Project A1 and A2 is higher for

Project A1 since these two projects are mutually exclusive. In the given scenario, IRR for the

respective projects are:

Project A1 24.69%

Project A2 21.65%

Project A3 19.77%

The IRR is higher than the MCC calculated above, and hence the recommendation will

be based on a comparison of MCC and IRR (Magni, 2020). The cash flows are discounted at the

MCC rate (10.06%) to assess the Net Present Value of the project and also help in deciding the

proportion in which funds should be raised further.

2.4. MCC Curve and break-even:

When the additional capital is raised, there will be changes in the costs and return of the

Company, the MCC schedule shows the changes in the cost due to an increase in further funds.

The break-even point is referred to that point which causes changes in WACC due to the

requirement of additional sources of funds, a point where the weighted average cost of capital

changes for the capital amount (Zafiris, 2016). The break-even point isused to calculate by the

following formula–

IRR will help in evaluating the profitability of potential projects (Kulakov, &Kastro,

2017). The IRR for the three projects is calculated by considering the net cash flows for the

given period of time for each project separately. IRR among Project A1 and A2 is higher for

Project A1 since these two projects are mutually exclusive. In the given scenario, IRR for the

respective projects are:

Project A1 24.69%

Project A2 21.65%

Project A3 19.77%

The IRR is higher than the MCC calculated above, and hence the recommendation will

be based on a comparison of MCC and IRR (Magni, 2020). The cash flows are discounted at the

MCC rate (10.06%) to assess the Net Present Value of the project and also help in deciding the

proportion in which funds should be raised further.

2.4. MCC Curve and break-even:

When the additional capital is raised, there will be changes in the costs and return of the

Company, the MCC schedule shows the changes in the cost due to an increase in further funds.

The break-even point is referred to that point which causes changes in WACC due to the

requirement of additional sources of funds, a point where the weighted average cost of capital

changes for the capital amount (Zafiris, 2016). The break-even point isused to calculate by the

following formula–

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

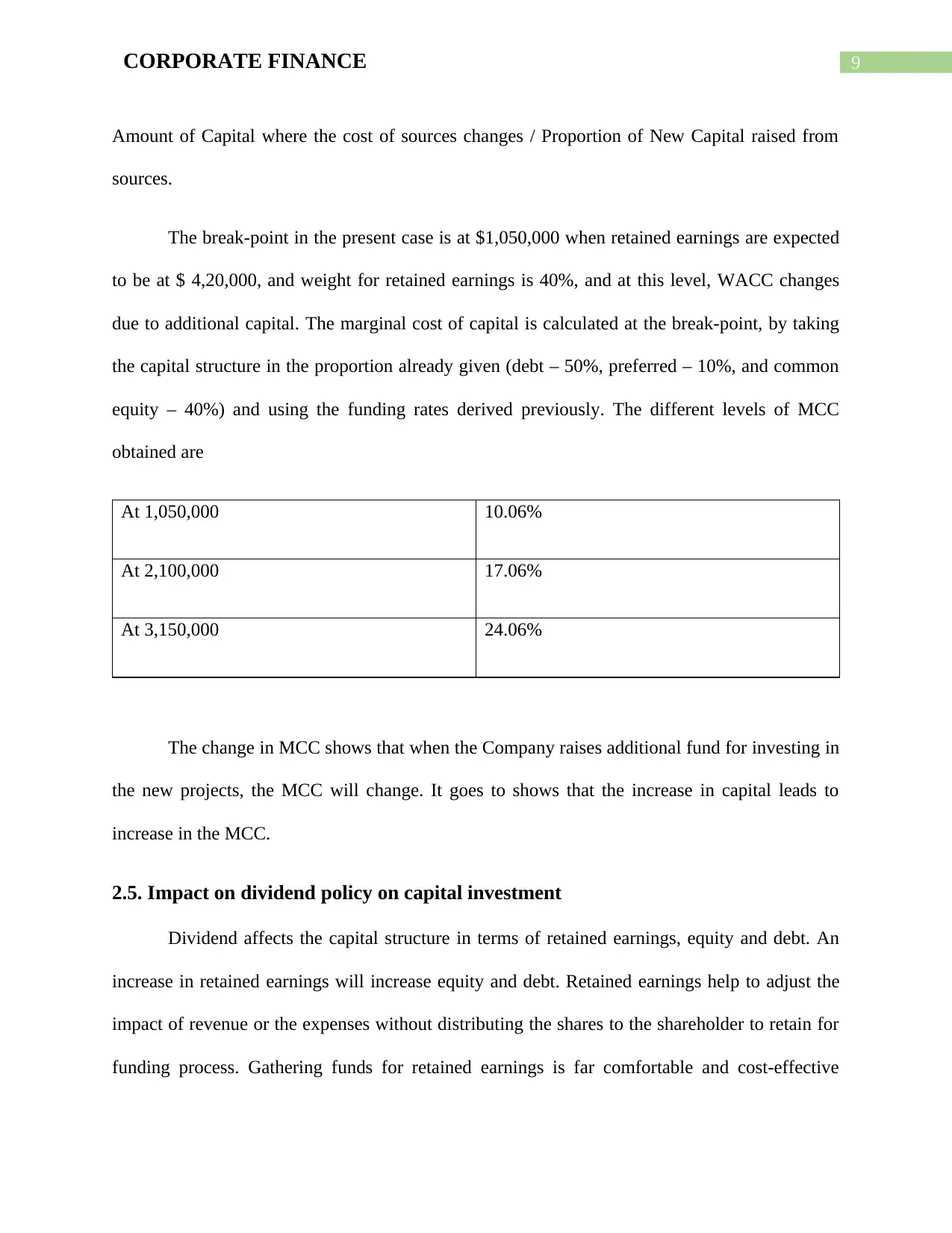

9CORPORATE FINANCE

Amount of Capital where the cost of sources changes / Proportion of New Capital raised from

sources.

The break-point in the present case is at $1,050,000 when retained earnings are expected

to be at $ 4,20,000, and weight for retained earnings is 40%, and at this level, WACC changes

due to additional capital. The marginal cost of capital is calculated at the break-point, by taking

the capital structure in the proportion already given (debt – 50%, preferred – 10%, and common

equity – 40%) and using the funding rates derived previously. The different levels of MCC

obtained are

At 1,050,000 10.06%

At 2,100,000 17.06%

At 3,150,000 24.06%

The change in MCC shows that when the Company raises additional fund for investing in

the new projects, the MCC will change. It goes to shows that the increase in capital leads to

increase in the MCC.

2.5. Impact on dividend policy on capital investment

Dividend affects the capital structure in terms of retained earnings, equity and debt. An

increase in retained earnings will increase equity and debt. Retained earnings help to adjust the

impact of revenue or the expenses without distributing the shares to the shareholder to retain for

funding process. Gathering funds for retained earnings is far comfortable and cost-effective

Amount of Capital where the cost of sources changes / Proportion of New Capital raised from

sources.

The break-point in the present case is at $1,050,000 when retained earnings are expected

to be at $ 4,20,000, and weight for retained earnings is 40%, and at this level, WACC changes

due to additional capital. The marginal cost of capital is calculated at the break-point, by taking

the capital structure in the proportion already given (debt – 50%, preferred – 10%, and common

equity – 40%) and using the funding rates derived previously. The different levels of MCC

obtained are

At 1,050,000 10.06%

At 2,100,000 17.06%

At 3,150,000 24.06%

The change in MCC shows that when the Company raises additional fund for investing in

the new projects, the MCC will change. It goes to shows that the increase in capital leads to

increase in the MCC.

2.5. Impact on dividend policy on capital investment

Dividend affects the capital structure in terms of retained earnings, equity and debt. An

increase in retained earnings will increase equity and debt. Retained earnings help to adjust the

impact of revenue or the expenses without distributing the shares to the shareholder to retain for

funding process. Gathering funds for retained earnings is far comfortable and cost-effective

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE FINANCE

rather than issuing new equity. Utilizing the retained earning for the fund will not be the cost for

the company and capital budget because company using its own funds to maintain the expense

and reduce the cost of the company.

However, some researcher believes in the theories that the dividend policy is irrelevant

because the investor can use their share and sell them to get funds when in need. The theory like

“Modigliani and Miller theorem” says “the dividend policy is irrelevant for the Company's cost

of capital structure” and will “not affect the stock price of the Company” (Dividend.com, 2020).

This theorem assumes that there is no tax, no floatation cost, no transaction cost which can

impact on capital budgeting. Investors can predict the future easily from the required information

and leverage has zero impact on the cost of capital (Brusov et al., 2018).

Effect of dividend on preferred stock

Preferred stock is a first pay dividend to the preferred shareholder before paying to a

common shareholder or other shareholder (Hussain, Ghani,&Razimi, 2019). It is the fixed

dividend paid to the preferred holder. It is calculated on the number of shares issued and

outstanding share.

In case of bankruptcy of a company, the preferred stockholder received the share prior to the

common stockholder (Ibrahim et al., 2019).Preferred stockholder receivesa higher dividend yield

without any actual capital gain. It implies that the owner utilized the capital gain after purchasing

the preferred stock before reducing the interest rate, and this will raise the value of the preferred

stock and the company. The cost of preferred stock is calculated based on the dividend, current

price and the floatation cost.

rather than issuing new equity. Utilizing the retained earning for the fund will not be the cost for

the company and capital budget because company using its own funds to maintain the expense

and reduce the cost of the company.

However, some researcher believes in the theories that the dividend policy is irrelevant

because the investor can use their share and sell them to get funds when in need. The theory like

“Modigliani and Miller theorem” says “the dividend policy is irrelevant for the Company's cost

of capital structure” and will “not affect the stock price of the Company” (Dividend.com, 2020).

This theorem assumes that there is no tax, no floatation cost, no transaction cost which can

impact on capital budgeting. Investors can predict the future easily from the required information

and leverage has zero impact on the cost of capital (Brusov et al., 2018).

Effect of dividend on preferred stock

Preferred stock is a first pay dividend to the preferred shareholder before paying to a

common shareholder or other shareholder (Hussain, Ghani,&Razimi, 2019). It is the fixed

dividend paid to the preferred holder. It is calculated on the number of shares issued and

outstanding share.

In case of bankruptcy of a company, the preferred stockholder received the share prior to the

common stockholder (Ibrahim et al., 2019).Preferred stockholder receivesa higher dividend yield

without any actual capital gain. It implies that the owner utilized the capital gain after purchasing

the preferred stock before reducing the interest rate, and this will raise the value of the preferred

stock and the company. The cost of preferred stock is calculated based on the dividend, current

price and the floatation cost.

11CORPORATE FINANCE

Effect of dividend on the cost of equity

Cost of equity has a massive impact on the dividend policy because when a company

makes profit, it gets distributed among the shareholders or stockholders equally as per their

sharein an organization or a company. They can also reinvest those shares into the Company as

retained earnings or can divide evenly among them as per their share in stock as a dividend

(Larkin, Leary,&Michaely, 2017). It increasesthe investors and the shareholders’ value of the

Company, which increase the retained earnings. However for the Company which needs fund

has to reinvest the shares into the Company for long term financing the funds and to generate the

profit and growth of the Company (Acharya, Byoun, &Xu, 2019). After making sufficient profit,

shareholders can divide the shares to maximize the share.

There are few things before deciding on dividend policy of a company or organization

Retained earnings is an earning of a company which is retained as funds to Help

Company's growth and other operations. It generates after distributing the dividend to all

the preferred shareholder, and the rest is shared among the common shareholder. As it

does not increase the debt cost, also it does not devalue the existing funds that help in the

growth and operation of the Company which increases the equity and the cost of equity.

In most instances, retained earnings are not sufficient to fund the project and thus need

other capital sources to fulfil the requirement. However, a company cannot use the

retained earnings for any extra cost for its growth without generating any future revenue

and compel to declare the dividend on earnings (Koussis, Martzoukos, &Trigeorgis,

2017).

Effect of dividend on the cost of equity

Cost of equity has a massive impact on the dividend policy because when a company

makes profit, it gets distributed among the shareholders or stockholders equally as per their

sharein an organization or a company. They can also reinvest those shares into the Company as

retained earnings or can divide evenly among them as per their share in stock as a dividend

(Larkin, Leary,&Michaely, 2017). It increasesthe investors and the shareholders’ value of the

Company, which increase the retained earnings. However for the Company which needs fund

has to reinvest the shares into the Company for long term financing the funds and to generate the

profit and growth of the Company (Acharya, Byoun, &Xu, 2019). After making sufficient profit,

shareholders can divide the shares to maximize the share.

There are few things before deciding on dividend policy of a company or organization

Retained earnings is an earning of a company which is retained as funds to Help

Company's growth and other operations. It generates after distributing the dividend to all

the preferred shareholder, and the rest is shared among the common shareholder. As it

does not increase the debt cost, also it does not devalue the existing funds that help in the

growth and operation of the Company which increases the equity and the cost of equity.

In most instances, retained earnings are not sufficient to fund the project and thus need

other capital sources to fulfil the requirement. However, a company cannot use the

retained earnings for any extra cost for its growth without generating any future revenue

and compel to declare the dividend on earnings (Koussis, Martzoukos, &Trigeorgis,

2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.