Corporate Financial Management: IPO Valuation for No Regrets Inc.

VerifiedAdded on 2022/08/12

|12

|3161

|22

Report

AI Summary

This report provides a comprehensive analysis of the Initial Public Offering (IPO) process for No Regrets, Inc., focusing on the valuation of shares and the implications of ownership changes. It begins with an introduction to IPOs, highlighting the regulatory framework and the importance of valuation. The report then delves into the impact of an IPO on existing and future ownership, including changes in management processes, privacy considerations, and short-term financial reporting requirements. The core of the report centers on share valuation, employing the PE Range Valuation Model and the Constant Growth Model to determine an appropriate price range for the company's shares. The report includes detailed financial statements and calculations, and compares the valuation results with the company's proposed IPO price. Ultimately, the report recommends an IPO price and discusses the importance of the existing owners retaining a significant portion of the shareholding to maintain control over the company's management and future direction. The analysis considers factors such as industry norms and the need to present an attractive price to potential investors.

CORPORATE FINANCIAL MANAGEMENT REPORT

2/19/2020

2/19/2020

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction...........................................................................................................................................2

IPO and Significant areas in context of ownership................................................................................2

Valuation of the shares of the company.................................................................................................4

Other considerations..............................................................................................................................9

Bibliography........................................................................................................................................11

Introduction...........................................................................................................................................2

IPO and Significant areas in context of ownership................................................................................2

Valuation of the shares of the company.................................................................................................4

Other considerations..............................................................................................................................9

Bibliography........................................................................................................................................11

Introduction

The prime aim behind the initiation of the Initial Public Offering is the capitalization on the

varied and large base of the investors, and also on the liquid capital markets. It is significant

to note that the IPO process is regulated by the US Securities and Exchange Commission

(SEC), and the legislative rules and regulations must be mandatorily followed. The aim of the

following report is to guide the management of the entity No Regrets, Inc. on the various

aspects of security valuation and going public process.

IPO and Significant areas in context of ownership

Some of the key aspects of the IPO in relation to the impact on the existing and the future

ownership would be described in the following segment.

Change in the management processes

It has been assessed that the current owners of the above mentioned company wish to retain

20% to 25 % ownership in the company. Thus, the existing owners would be required to sell

their shares to public, to raise the capital in the company. It is to be noted that there would be

significant changes in the management processes if the new public owners would have a

75%- 80% shareholding in the company. Further to note, there would be enhanced

management processes in the newly formed public company which were absent in the case of

a private limited company. Some of the key changes in the management processes are listed

as follows.

On becoming a part of the Security Exchange regulations, the public company would be

required to file the financial statements and the annual returns on a periodic basis. In addition,

these financial statements must be audited by the independent auditors. The owners must be

careful of retaining the non-public information so as the same may not be used for the insider

trading purposes. Since the existing owners want to retain the 20% - 25% shareholding in the

company, there lies a duty to file a report relating to the disclosure of the shares possessed,

changes and transactions during the year in the said shareholding during the fiscal period, as

it is mandatory for the owners possessing more than 10 per cent of shareholding

("International Legal Business Solutions - Global Legal Insights"). The existing owners

would be still be liable for the acts of the company in the light of being the control person for

The prime aim behind the initiation of the Initial Public Offering is the capitalization on the

varied and large base of the investors, and also on the liquid capital markets. It is significant

to note that the IPO process is regulated by the US Securities and Exchange Commission

(SEC), and the legislative rules and regulations must be mandatorily followed. The aim of the

following report is to guide the management of the entity No Regrets, Inc. on the various

aspects of security valuation and going public process.

IPO and Significant areas in context of ownership

Some of the key aspects of the IPO in relation to the impact on the existing and the future

ownership would be described in the following segment.

Change in the management processes

It has been assessed that the current owners of the above mentioned company wish to retain

20% to 25 % ownership in the company. Thus, the existing owners would be required to sell

their shares to public, to raise the capital in the company. It is to be noted that there would be

significant changes in the management processes if the new public owners would have a

75%- 80% shareholding in the company. Further to note, there would be enhanced

management processes in the newly formed public company which were absent in the case of

a private limited company. Some of the key changes in the management processes are listed

as follows.

On becoming a part of the Security Exchange regulations, the public company would be

required to file the financial statements and the annual returns on a periodic basis. In addition,

these financial statements must be audited by the independent auditors. The owners must be

careful of retaining the non-public information so as the same may not be used for the insider

trading purposes. Since the existing owners want to retain the 20% - 25% shareholding in the

company, there lies a duty to file a report relating to the disclosure of the shares possessed,

changes and transactions during the year in the said shareholding during the fiscal period, as

it is mandatory for the owners possessing more than 10 per cent of shareholding

("International Legal Business Solutions - Global Legal Insights"). The existing owners

would be still be liable for the acts of the company in the light of being the control person for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the violations of the requirements as mentioned in the section 11, section and section 15 of

the act. These are in addition to the requirement relating to the appointment of the directors,

holding of the meetings of the shareholders, and other statutory processes as guided in the

act. In addition, it is significant to note that there is enhancement in the expenses on account

of finance and reporting, information technology and investor relations, internal controls and

others.

Public company and the issues of privacy

It is important to be noted that the yet other prime change on the conversion of the private

company into a public company is in the form of the loss of privacy. While the most of the

information of a private company is not available in the public domain, the case is opposite in

the case of the public company, because of the statutory guidelines on the same. Some of the

key aspects that must be disclosed mandatorily are as follows, and the same would be

available not only to the stakeholders of the company, but also the competitors as well.

Financial information in the form of the financial position, related-party transactions,

data on business segments, key customers, sustainability and governance approach

and others ("SEC.Gov | Going Public").

Compensation or remuneration structure of the directors and other officers of the

company, which not only includes the compensation in cash but also deferred

compensation plans, and the stock option plans, if any.

Shareholding patterns and the changes therein for the officers, directors, and key

shareholders.

Short term financial reporting requirements

As stated in the previous parts, there are significant changes in the various business aspects

out of the conversion of the private owned company to a public listed company, including the

management processes and privacy. There are several other aspects that makes the public

company different from a private company. The short term reporting requirements are a

complex and lengthy affair for the management of an enterprise, however there is an

enhanced transparency in the reporting and business management from the point of view of

stakeholders such as regulators, investors, suppliers, customers and others. The risk is spread

by widening of the shareholder base, and not only the profits are distributed, but so the losses

as against in the private companies. The public companies are further advantageous in

the act. These are in addition to the requirement relating to the appointment of the directors,

holding of the meetings of the shareholders, and other statutory processes as guided in the

act. In addition, it is significant to note that there is enhancement in the expenses on account

of finance and reporting, information technology and investor relations, internal controls and

others.

Public company and the issues of privacy

It is important to be noted that the yet other prime change on the conversion of the private

company into a public company is in the form of the loss of privacy. While the most of the

information of a private company is not available in the public domain, the case is opposite in

the case of the public company, because of the statutory guidelines on the same. Some of the

key aspects that must be disclosed mandatorily are as follows, and the same would be

available not only to the stakeholders of the company, but also the competitors as well.

Financial information in the form of the financial position, related-party transactions,

data on business segments, key customers, sustainability and governance approach

and others ("SEC.Gov | Going Public").

Compensation or remuneration structure of the directors and other officers of the

company, which not only includes the compensation in cash but also deferred

compensation plans, and the stock option plans, if any.

Shareholding patterns and the changes therein for the officers, directors, and key

shareholders.

Short term financial reporting requirements

As stated in the previous parts, there are significant changes in the various business aspects

out of the conversion of the private owned company to a public listed company, including the

management processes and privacy. There are several other aspects that makes the public

company different from a private company. The short term reporting requirements are a

complex and lengthy affair for the management of an enterprise, however there is an

enhanced transparency in the reporting and business management from the point of view of

stakeholders such as regulators, investors, suppliers, customers and others. The risk is spread

by widening of the shareholder base, and not only the profits are distributed, but so the losses

as against in the private companies. The public companies are further advantageous in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

context of increased confidence and public trust, because of the transparent public

information of the key aspects (Korchak). Thus, there lies a greater opportunity of attracting

investments in future as well.

Valuation of the shares of the company

One of the significant activities of the Initial Public Offering is the valuation of the company

as a whole that is trying to go to public. The reason for the said significance is that there are

various methods involving various assumptions that are used to value the price of a single

share and eventually to determine the number of shares to be issued for the desired amount of

capital. Some of the key methods that are used for the valuation are that of the “Discounted

cash flow analysis method,” “comparable company analysis,” “constant growth model,” “PE

Range Valuation,” and others. The valuation models that are used in the following report are

the PE Range Valuation Model and the Constant Growth Model. The analysis of the

valuation methods, the price derived from each and the comparison is provided as follows.

PE Range Valuation Model

The model involves the valuation of the business based on the PE multiple, and the forecasted

Earning Price per Share. It is significant to note that it is vital to prepare the forecasted

financial statements taking into considerations various factors such as the inflation rates,

changes in the industry of operation, the consumer preferences, and others. It has been

assessed in the case of the company New Regret Inc. that the company is contemplating to

expand its operations from 6 stores to 30 stores. Accordingly, taking into consideration the

factor of inflation and the expansion rate, it is estimates that the sales of the company would

grow by 5 times on account on expansion, and an additional 11 percent on account of

external environment changes. The forecasted financial statements of the organization are

presented as follows, which would form the base for the PE Valuation Model.

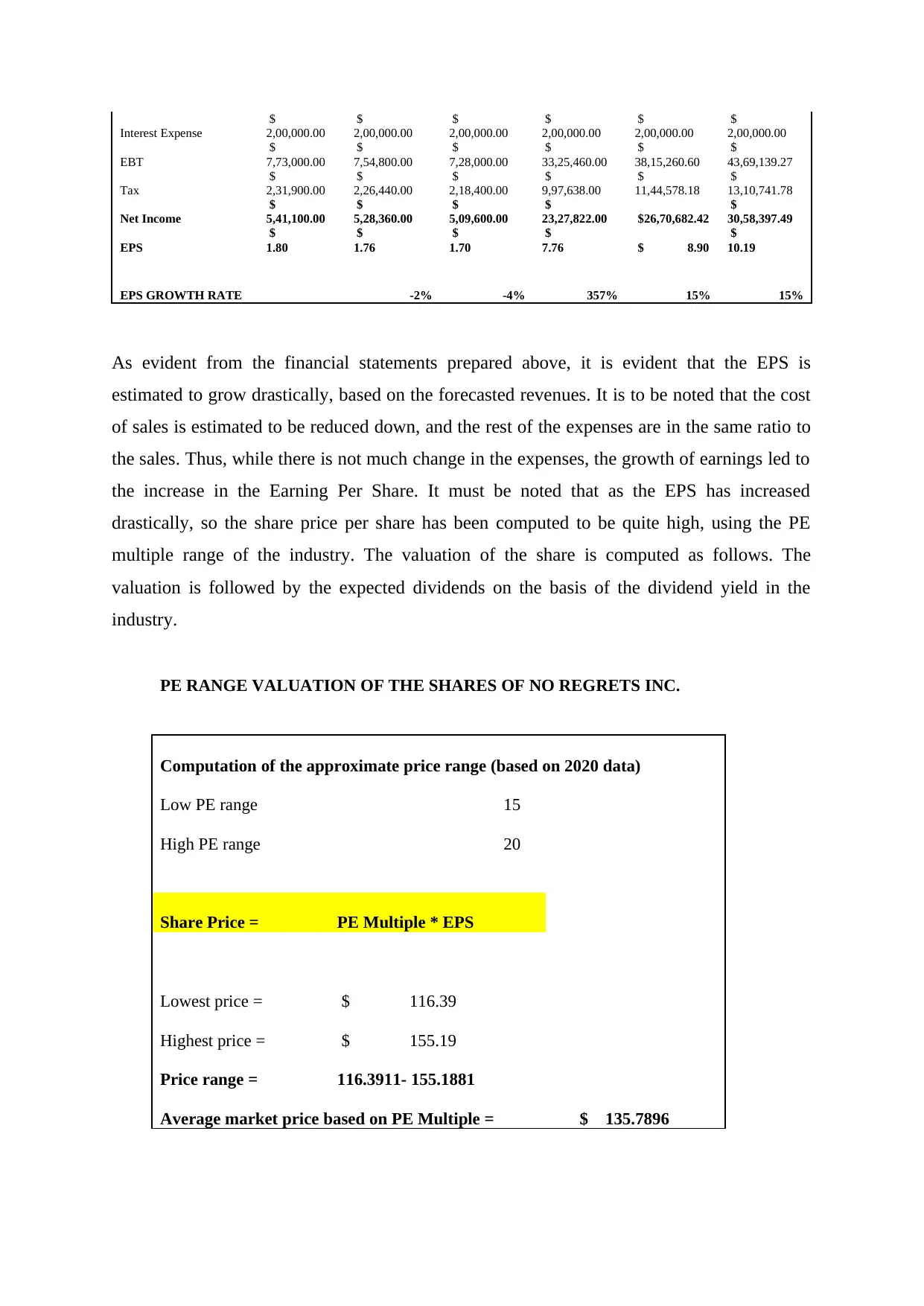

New Regret Inc.

Forecasted Income Statement (For the years ended on… )

Description Dec-17 Dec-18 Dec-19 Dec-20 Dec-21 Dec-22

Sales

$

67,80,000.00

$

72,20,000.00

$

79,00,000.00

$

4,03,69,000.00

$

4,48,09,590.00

$

4,97,38,644.90

Cost of sales

$

44,07,000.00

$

47,65,200.00

$

53,72,000.00

$

2,66,43,540.00

$

2,95,74,329.40

$

3,28,27,505.63

Cost of sales percentage 65% 66% 68% 66% 66% 66%

Other Operating costs

$

14,00,000.00

$

15,00,000.00

$

16,00,000.00

$

1,02,00,000.00

$

1,12,20,000.00

$

1,23,42,000.00

EBIT (Net operating

income)

$

9,73,000.00

$

9,54,800.00

$

9,28,000.00

$

35,25,460.00

$

40,15,260.60

$

45,69,139.27

information of the key aspects (Korchak). Thus, there lies a greater opportunity of attracting

investments in future as well.

Valuation of the shares of the company

One of the significant activities of the Initial Public Offering is the valuation of the company

as a whole that is trying to go to public. The reason for the said significance is that there are

various methods involving various assumptions that are used to value the price of a single

share and eventually to determine the number of shares to be issued for the desired amount of

capital. Some of the key methods that are used for the valuation are that of the “Discounted

cash flow analysis method,” “comparable company analysis,” “constant growth model,” “PE

Range Valuation,” and others. The valuation models that are used in the following report are

the PE Range Valuation Model and the Constant Growth Model. The analysis of the

valuation methods, the price derived from each and the comparison is provided as follows.

PE Range Valuation Model

The model involves the valuation of the business based on the PE multiple, and the forecasted

Earning Price per Share. It is significant to note that it is vital to prepare the forecasted

financial statements taking into considerations various factors such as the inflation rates,

changes in the industry of operation, the consumer preferences, and others. It has been

assessed in the case of the company New Regret Inc. that the company is contemplating to

expand its operations from 6 stores to 30 stores. Accordingly, taking into consideration the

factor of inflation and the expansion rate, it is estimates that the sales of the company would

grow by 5 times on account on expansion, and an additional 11 percent on account of

external environment changes. The forecasted financial statements of the organization are

presented as follows, which would form the base for the PE Valuation Model.

New Regret Inc.

Forecasted Income Statement (For the years ended on… )

Description Dec-17 Dec-18 Dec-19 Dec-20 Dec-21 Dec-22

Sales

$

67,80,000.00

$

72,20,000.00

$

79,00,000.00

$

4,03,69,000.00

$

4,48,09,590.00

$

4,97,38,644.90

Cost of sales

$

44,07,000.00

$

47,65,200.00

$

53,72,000.00

$

2,66,43,540.00

$

2,95,74,329.40

$

3,28,27,505.63

Cost of sales percentage 65% 66% 68% 66% 66% 66%

Other Operating costs

$

14,00,000.00

$

15,00,000.00

$

16,00,000.00

$

1,02,00,000.00

$

1,12,20,000.00

$

1,23,42,000.00

EBIT (Net operating

income)

$

9,73,000.00

$

9,54,800.00

$

9,28,000.00

$

35,25,460.00

$

40,15,260.60

$

45,69,139.27

Interest Expense

$

2,00,000.00

$

2,00,000.00

$

2,00,000.00

$

2,00,000.00

$

2,00,000.00

$

2,00,000.00

EBT

$

7,73,000.00

$

7,54,800.00

$

7,28,000.00

$

33,25,460.00

$

38,15,260.60

$

43,69,139.27

Tax

$

2,31,900.00

$

2,26,440.00

$

2,18,400.00

$

9,97,638.00

$

11,44,578.18

$

13,10,741.78

Net Income

$

5,41,100.00

$

5,28,360.00

$

5,09,600.00

$

23,27,822.00 $26,70,682.42

$

30,58,397.49

EPS

$

1.80

$

1.76

$

1.70

$

7.76 $ 8.90

$

10.19

EPS GROWTH RATE -2% -4% 357% 15% 15%

As evident from the financial statements prepared above, it is evident that the EPS is

estimated to grow drastically, based on the forecasted revenues. It is to be noted that the cost

of sales is estimated to be reduced down, and the rest of the expenses are in the same ratio to

the sales. Thus, while there is not much change in the expenses, the growth of earnings led to

the increase in the Earning Per Share. It must be noted that as the EPS has increased

drastically, so the share price per share has been computed to be quite high, using the PE

multiple range of the industry. The valuation of the share is computed as follows. The

valuation is followed by the expected dividends on the basis of the dividend yield in the

industry.

PE RANGE VALUATION OF THE SHARES OF NO REGRETS INC.

Computation of the approximate price range (based on 2020 data)

Low PE range 15

High PE range 20

Share Price = PE Multiple * EPS

Lowest price = $ 116.39

Highest price = $ 155.19

Price range = 116.3911- 155.1881

Average market price based on PE Multiple = $ 135.7896

$

2,00,000.00

$

2,00,000.00

$

2,00,000.00

$

2,00,000.00

$

2,00,000.00

$

2,00,000.00

EBT

$

7,73,000.00

$

7,54,800.00

$

7,28,000.00

$

33,25,460.00

$

38,15,260.60

$

43,69,139.27

Tax

$

2,31,900.00

$

2,26,440.00

$

2,18,400.00

$

9,97,638.00

$

11,44,578.18

$

13,10,741.78

Net Income

$

5,41,100.00

$

5,28,360.00

$

5,09,600.00

$

23,27,822.00 $26,70,682.42

$

30,58,397.49

EPS

$

1.80

$

1.76

$

1.70

$

7.76 $ 8.90

$

10.19

EPS GROWTH RATE -2% -4% 357% 15% 15%

As evident from the financial statements prepared above, it is evident that the EPS is

estimated to grow drastically, based on the forecasted revenues. It is to be noted that the cost

of sales is estimated to be reduced down, and the rest of the expenses are in the same ratio to

the sales. Thus, while there is not much change in the expenses, the growth of earnings led to

the increase in the Earning Per Share. It must be noted that as the EPS has increased

drastically, so the share price per share has been computed to be quite high, using the PE

multiple range of the industry. The valuation of the share is computed as follows. The

valuation is followed by the expected dividends on the basis of the dividend yield in the

industry.

PE RANGE VALUATION OF THE SHARES OF NO REGRETS INC.

Computation of the approximate price range (based on 2020 data)

Low PE range 15

High PE range 20

Share Price = PE Multiple * EPS

Lowest price = $ 116.39

Highest price = $ 155.19

Price range = 116.3911- 155.1881

Average market price based on PE Multiple = $ 135.7896

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

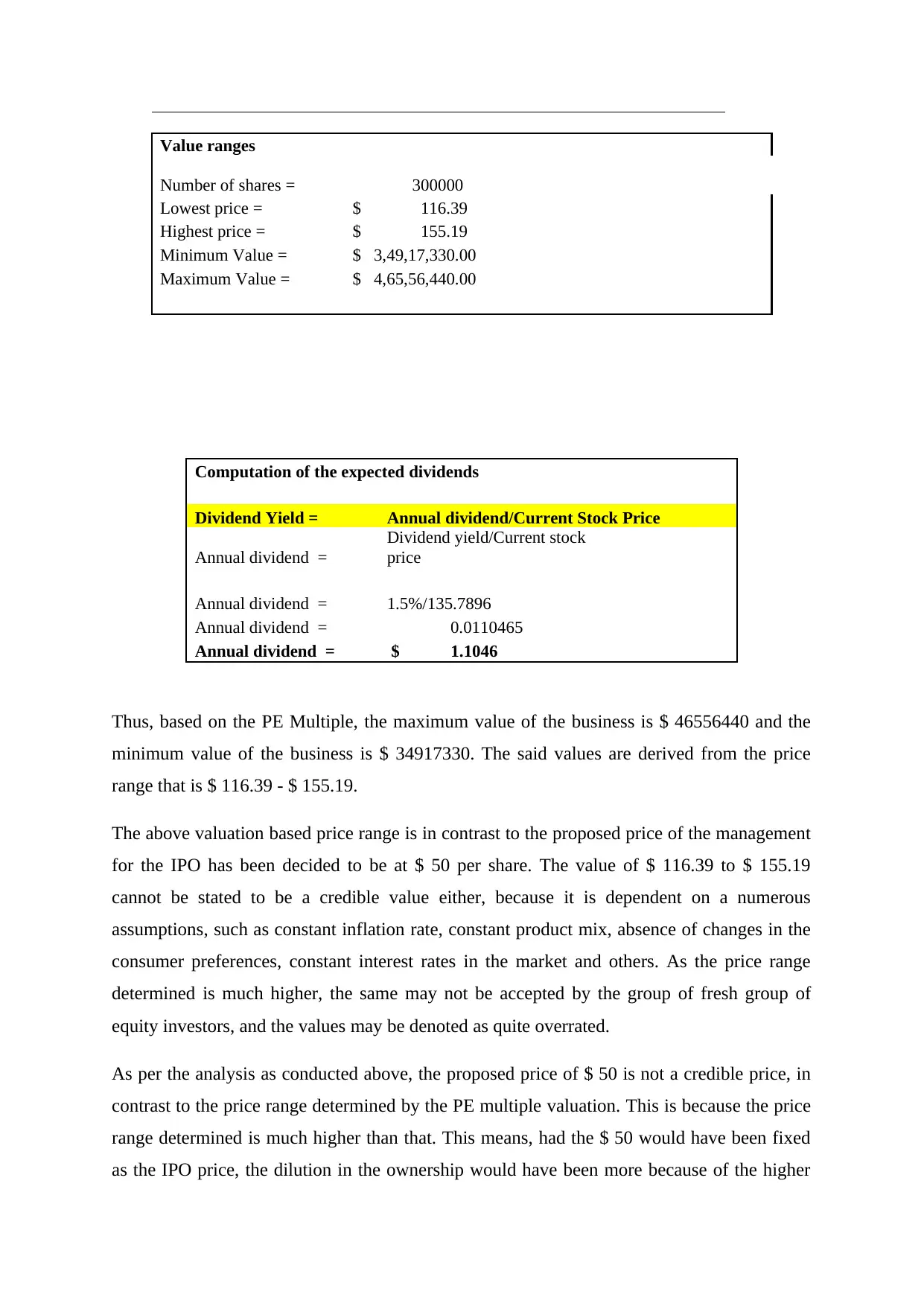

Value ranges

Number of shares = 300000

Lowest price = $ 116.39

Highest price = $ 155.19

Minimum Value = $ 3,49,17,330.00

Maximum Value = $ 4,65,56,440.00

Computation of the expected dividends

Dividend Yield = Annual dividend/Current Stock Price

Annual dividend =

Dividend yield/Current stock

price

Annual dividend = 1.5%/135.7896

Annual dividend = 0.0110465

Annual dividend = $ 1.1046

Thus, based on the PE Multiple, the maximum value of the business is $ 46556440 and the

minimum value of the business is $ 34917330. The said values are derived from the price

range that is $ 116.39 - $ 155.19.

The above valuation based price range is in contrast to the proposed price of the management

for the IPO has been decided to be at $ 50 per share. The value of $ 116.39 to $ 155.19

cannot be stated to be a credible value either, because it is dependent on a numerous

assumptions, such as constant inflation rate, constant product mix, absence of changes in the

consumer preferences, constant interest rates in the market and others. As the price range

determined is much higher, the same may not be accepted by the group of fresh group of

equity investors, and the values may be denoted as quite overrated.

As per the analysis as conducted above, the proposed price of $ 50 is not a credible price, in

contrast to the price range determined by the PE multiple valuation. This is because the price

range determined is much higher than that. This means, had the $ 50 would have been fixed

as the IPO price, the dilution in the ownership would have been more because of the higher

Number of shares = 300000

Lowest price = $ 116.39

Highest price = $ 155.19

Minimum Value = $ 3,49,17,330.00

Maximum Value = $ 4,65,56,440.00

Computation of the expected dividends

Dividend Yield = Annual dividend/Current Stock Price

Annual dividend =

Dividend yield/Current stock

price

Annual dividend = 1.5%/135.7896

Annual dividend = 0.0110465

Annual dividend = $ 1.1046

Thus, based on the PE Multiple, the maximum value of the business is $ 46556440 and the

minimum value of the business is $ 34917330. The said values are derived from the price

range that is $ 116.39 - $ 155.19.

The above valuation based price range is in contrast to the proposed price of the management

for the IPO has been decided to be at $ 50 per share. The value of $ 116.39 to $ 155.19

cannot be stated to be a credible value either, because it is dependent on a numerous

assumptions, such as constant inflation rate, constant product mix, absence of changes in the

consumer preferences, constant interest rates in the market and others. As the price range

determined is much higher, the same may not be accepted by the group of fresh group of

equity investors, and the values may be denoted as quite overrated.

As per the analysis as conducted above, the proposed price of $ 50 is not a credible price, in

contrast to the price range determined by the PE multiple valuation. This is because the price

range determined is much higher than that. This means, had the $ 50 would have been fixed

as the IPO price, the dilution in the ownership would have been more because of the higher

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

number of shares to be issued by the company to raise the additional amount for expansion of

$ 48000000. Taking into consideration, the other factors, the IPO price suggested to the

management of the entity is $ 116 that is the lowest price in the price range. According to

this price, the number of shares to be issued to raise the amount of expansion of $ 48000000

is 413793 shares ($48000000/$116). It is to be noted that it is reasonable to further hold a 25

per cent of shareholding in the company. However, it is suggested that the owners must opt to

hold more shares so as to retain the control over the activities, objectives and other aspects of

the company management. This is because if 413793 shares are issued to the new investors

and that the same account for 75 – 80 percent of the total holding, the existing shareholders

may not have any say in the company management, as a special resolution requires minimum

of 75 percent of voting which would already be composed of the new shareholders itself.

Apart from this, there are number of factors that have led to the suggestion of a price that is

not on the higher side of the valuation range. These factors are that of industry norms,

presenting an attractive price to the potential investors and other legislative and industrial

aspects. It must be noted that the IPO price proposed must be such that the same not only

satisfies the current owners, but also the prospective owners (Bell, Igor and Ruth 303). In

addition, the current industry norms must be considered as well, which would be available on

analyzing the recent IPOs in the industry of operation.

The pros and cons for the price point that is selected for the company, that is $ 116 are stated

as follows. It is important to note that the suggested price is the lowest minimum price that

must be accepted by the company. The rationale behind the said price being suggested is that

it has been assumed that the market is a bearish market, in the light of the US China Trade

Tensions, Brexit, and the other political and economic disturbances in the exchange market.

The result of the same would be that the market window would tend to close and there is

slowness in the IPO activity. The pros of the chosen price would be that the same would not

only be attractive to the new and existing investor groups, but also would be an attractive

choice in the light of the declining market. The yet another benefit is that the company can

take advantages of its existing goodwill because of existing stores, and can avail the cash

needed form this price, by generating investor demand at low price range. The cons of the

said price can be stated to be that the same may still seem to be on a higher side, as per the

industry norms and the current market sentiments, and the investors may not invest in the

company at such a price too. The control may be diluted more as the price suggested is on

$ 48000000. Taking into consideration, the other factors, the IPO price suggested to the

management of the entity is $ 116 that is the lowest price in the price range. According to

this price, the number of shares to be issued to raise the amount of expansion of $ 48000000

is 413793 shares ($48000000/$116). It is to be noted that it is reasonable to further hold a 25

per cent of shareholding in the company. However, it is suggested that the owners must opt to

hold more shares so as to retain the control over the activities, objectives and other aspects of

the company management. This is because if 413793 shares are issued to the new investors

and that the same account for 75 – 80 percent of the total holding, the existing shareholders

may not have any say in the company management, as a special resolution requires minimum

of 75 percent of voting which would already be composed of the new shareholders itself.

Apart from this, there are number of factors that have led to the suggestion of a price that is

not on the higher side of the valuation range. These factors are that of industry norms,

presenting an attractive price to the potential investors and other legislative and industrial

aspects. It must be noted that the IPO price proposed must be such that the same not only

satisfies the current owners, but also the prospective owners (Bell, Igor and Ruth 303). In

addition, the current industry norms must be considered as well, which would be available on

analyzing the recent IPOs in the industry of operation.

The pros and cons for the price point that is selected for the company, that is $ 116 are stated

as follows. It is important to note that the suggested price is the lowest minimum price that

must be accepted by the company. The rationale behind the said price being suggested is that

it has been assumed that the market is a bearish market, in the light of the US China Trade

Tensions, Brexit, and the other political and economic disturbances in the exchange market.

The result of the same would be that the market window would tend to close and there is

slowness in the IPO activity. The pros of the chosen price would be that the same would not

only be attractive to the new and existing investor groups, but also would be an attractive

choice in the light of the declining market. The yet another benefit is that the company can

take advantages of its existing goodwill because of existing stores, and can avail the cash

needed form this price, by generating investor demand at low price range. The cons of the

said price can be stated to be that the same may still seem to be on a higher side, as per the

industry norms and the current market sentiments, and the investors may not invest in the

company at such a price too. The control may be diluted more as the price suggested is on

low range and number of shares to be issued would be more unlike in case of price on a

higher side.

It is further to be noted that as the amount needed for the expansion is even more than higher

range of the total valuation based on PE Multiple, the giving up of 75 – 80 percent of the

control is legitimate. However, risk of completed dilution of the control on the affairs of the

company still remains.

Constant Growth Valuation Model

In addition to the above valuation, the constant growth model has also been used to analyze

the value of the firm and the various aspects of the IPO, as this being one of the most

renowned valuation models. The valuation is conducted as under.

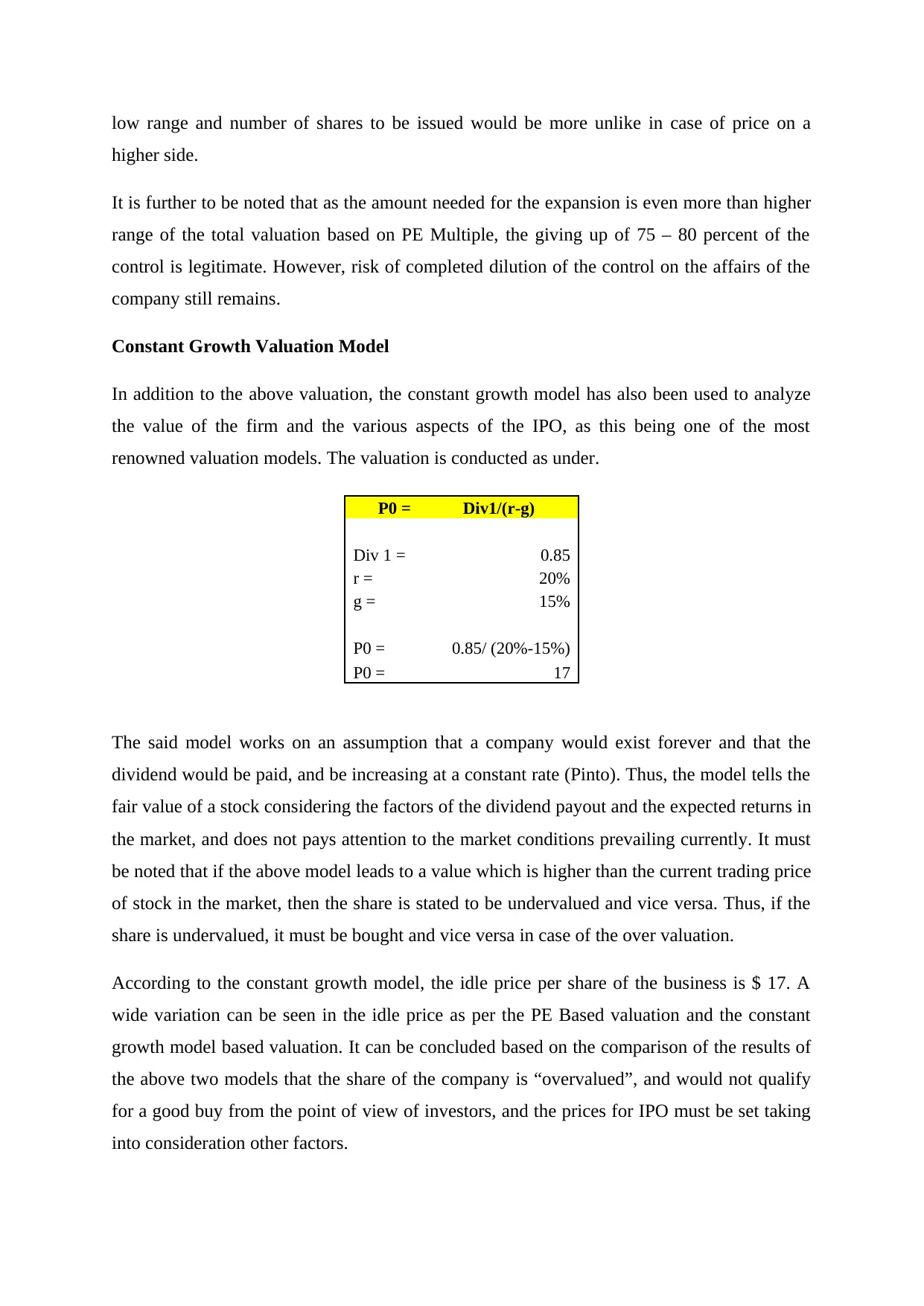

P0 = Div1/(r-g)

Div 1 = 0.85

r = 20%

g = 15%

P0 = 0.85/ (20%-15%)

P0 = 17

The said model works on an assumption that a company would exist forever and that the

dividend would be paid, and be increasing at a constant rate (Pinto). Thus, the model tells the

fair value of a stock considering the factors of the dividend payout and the expected returns in

the market, and does not pays attention to the market conditions prevailing currently. It must

be noted that if the above model leads to a value which is higher than the current trading price

of stock in the market, then the share is stated to be undervalued and vice versa. Thus, if the

share is undervalued, it must be bought and vice versa in case of the over valuation.

According to the constant growth model, the idle price per share of the business is $ 17. A

wide variation can be seen in the idle price as per the PE Based valuation and the constant

growth model based valuation. It can be concluded based on the comparison of the results of

the above two models that the share of the company is “overvalued”, and would not qualify

for a good buy from the point of view of investors, and the prices for IPO must be set taking

into consideration other factors.

higher side.

It is further to be noted that as the amount needed for the expansion is even more than higher

range of the total valuation based on PE Multiple, the giving up of 75 – 80 percent of the

control is legitimate. However, risk of completed dilution of the control on the affairs of the

company still remains.

Constant Growth Valuation Model

In addition to the above valuation, the constant growth model has also been used to analyze

the value of the firm and the various aspects of the IPO, as this being one of the most

renowned valuation models. The valuation is conducted as under.

P0 = Div1/(r-g)

Div 1 = 0.85

r = 20%

g = 15%

P0 = 0.85/ (20%-15%)

P0 = 17

The said model works on an assumption that a company would exist forever and that the

dividend would be paid, and be increasing at a constant rate (Pinto). Thus, the model tells the

fair value of a stock considering the factors of the dividend payout and the expected returns in

the market, and does not pays attention to the market conditions prevailing currently. It must

be noted that if the above model leads to a value which is higher than the current trading price

of stock in the market, then the share is stated to be undervalued and vice versa. Thus, if the

share is undervalued, it must be bought and vice versa in case of the over valuation.

According to the constant growth model, the idle price per share of the business is $ 17. A

wide variation can be seen in the idle price as per the PE Based valuation and the constant

growth model based valuation. It can be concluded based on the comparison of the results of

the above two models that the share of the company is “overvalued”, and would not qualify

for a good buy from the point of view of investors, and the prices for IPO must be set taking

into consideration other factors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Other considerations

Apart from the financial aspects of valuation of the business and the fixation of the price for

the IPO, there are several other factors that must be considered by the management of the

entity No Regrets Inc. It is suggested to the management to avail a professional evaluation of

the following factors at length before deciding on the execution of the IPO.

(Source: "Roadmap For An IPO - A Guide To Going Public")

Thus, it is vital to get a professional review done of the above aspects as well, before

deciding to convert to a public limited company.

Apart from the financial aspects of valuation of the business and the fixation of the price for

the IPO, there are several other factors that must be considered by the management of the

entity No Regrets Inc. It is suggested to the management to avail a professional evaluation of

the following factors at length before deciding on the execution of the IPO.

(Source: "Roadmap For An IPO - A Guide To Going Public")

Thus, it is vital to get a professional review done of the above aspects as well, before

deciding to convert to a public limited company.

Bibliography

"International Legal Business Solutions - Global Legal Insights". GLI - Global Legal

Insightsinternational Legal Business Solutions, 2020,

https://www.globallegalinsights.com/practice-areas/initial-public-offerings-laws-and-

regulations/02-going-public-in-the-usa-an-overview-of-the-regulatory-framework-and-

capital-markets-process-for-ipos. Accessed 19 Feb 2020.

"Roadmap For An IPO - A Guide To Going Public". Pwc.Com, 2017,

https://www.pwc.com/hu/hu/szolgaltatasok/konyvvizsgalat/szamviteli-tanacsadas/

kiadvanyok/roadmap_for_an_ipo.pdf. Accessed 19 Feb 2020.

"SEC.Gov | Going Public". Sec.Gov, 2020, https://www.sec.gov/smallbusiness/goingpublic.

Accessed 20 Feb 2020.

Bell, R. Greg, Igor Filatotchev, and Ruth V. Aguilera. "Corporate governance and investors'

perceptions of foreign IPO value: An institutional perspective." Academy of Management

Journal 57.1 (2014): 301-320.

Pinto, Jerald E. Equity asset valuation. John Wiley & Sons, 2020.

"International Legal Business Solutions - Global Legal Insights". GLI - Global Legal

Insightsinternational Legal Business Solutions, 2020,

https://www.globallegalinsights.com/practice-areas/initial-public-offerings-laws-and-

regulations/02-going-public-in-the-usa-an-overview-of-the-regulatory-framework-and-

capital-markets-process-for-ipos. Accessed 19 Feb 2020.

"Roadmap For An IPO - A Guide To Going Public". Pwc.Com, 2017,

https://www.pwc.com/hu/hu/szolgaltatasok/konyvvizsgalat/szamviteli-tanacsadas/

kiadvanyok/roadmap_for_an_ipo.pdf. Accessed 19 Feb 2020.

"SEC.Gov | Going Public". Sec.Gov, 2020, https://www.sec.gov/smallbusiness/goingpublic.

Accessed 20 Feb 2020.

Bell, R. Greg, Igor Filatotchev, and Ruth V. Aguilera. "Corporate governance and investors'

perceptions of foreign IPO value: An institutional perspective." Academy of Management

Journal 57.1 (2014): 301-320.

Pinto, Jerald E. Equity asset valuation. John Wiley & Sons, 2020.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.