Corporate Finance: Decision-Making, Capital Budgeting, and Analysis

VerifiedAdded on 2019/11/26

|9

|3038

|184

Report

AI Summary

This report provides a comprehensive overview of corporate finance management, emphasizing the crucial role of decision-making processes within organizations. It delves into capital budgeting, a critical aspect of financial planning, and explains various techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), Discounted Cash Flow (DCF) analysis, and payback period. The report highlights the importance of these methods in evaluating investment opportunities and ensuring optimal resource allocation. Furthermore, it explores advanced analytical tools like sensitivity analysis, scenario analysis, and break-even analysis, demonstrating how these techniques aid in assessing risks and making informed financial decisions. The discussion encompasses the significance of capital budgeting in long-term business sustainability and its role in evaluating potential projects. The report also addresses the importance of understanding the differences between accounting and financial break-even analyses. By examining these concepts, the report aims to provide valuable insights into the practical application of corporate finance principles.

CORPORATE FINANCE MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

An organization is constructed on decisions made by its management. Therefore, the process of

decision making is an important part of an entity, if in any way the decision is stated to be wrong

then the output may not be appropriate and may result in a huge loss to the company in the form

of revenue or reputation. Decision means to reach the conclusion of any scenario only after

examining various fields of action and choosing the most suitable option. The main target of

decision making is to keep up with its goals. Decision making requires constant focus as business

environment is never static. As soon as one problem is eliminated, the second one comes up and

this process continues (Berman, Knight and Case, n.d.)..

The process of corporate decision-making in an entity takes place at different levels, whether

above the bottom or below the top. The implementation of corporate decision-making is made to

be done by its implementers because decisions are only effective when they are being carried out

in the best possible manner (Bruner, Eades and Schill, 2017). Implementing large plans may be

meaningless if no obligation will be presented by middle and lower management. Therefore, it is

very important for the management to maintain a good and healthy relationship with its middle

and lower level of management. Hence, corporate decisions are successful till the point it has the

power to bond which helps the leaders to be encouraged and maintain stability, otherwise, the

institution gets trapped in its own trick which leads to degradation of the competition in the

market (TULSIAN, 2016).

Capital Budgeting refers to the calculation of various expenses or investments, which are huge in

nature. The investment and expenses which need to be calculated contain projects like making of

new plant or long term investments. By capital budgeting, cash inflows and outflows for a

lifetime are being formed so that it can be evaluated to know if the potential return is meeting the

assigned target or benchmark. It is also known as 'investment appraisal'.

For an enterprise, it facilitates the use of all opportunities and projects, but because of the limited

availability of capital at a particular point of time, it forces the management to use capital

budgeting to evaluate the maximum return on all available items at a particular time.

Capital budgeting contains various methods like internal rate of return (IRR), discounted cash

flow (DCF), net present value (NPV) and payback period. They may be defined in the following

manner:

DCF Analysis: This examination is similar to the NPV analysis because it takes into

account the initial cash outflows which are needed to fund a project, cash inflows and

other future outflows in the form of servicing and other expenses. Such costs have been

discounted to the current date and thus the resulting number is called NPV (Clarke and

Clarke, 1990).

decision making is an important part of an entity, if in any way the decision is stated to be wrong

then the output may not be appropriate and may result in a huge loss to the company in the form

of revenue or reputation. Decision means to reach the conclusion of any scenario only after

examining various fields of action and choosing the most suitable option. The main target of

decision making is to keep up with its goals. Decision making requires constant focus as business

environment is never static. As soon as one problem is eliminated, the second one comes up and

this process continues (Berman, Knight and Case, n.d.)..

The process of corporate decision-making in an entity takes place at different levels, whether

above the bottom or below the top. The implementation of corporate decision-making is made to

be done by its implementers because decisions are only effective when they are being carried out

in the best possible manner (Bruner, Eades and Schill, 2017). Implementing large plans may be

meaningless if no obligation will be presented by middle and lower management. Therefore, it is

very important for the management to maintain a good and healthy relationship with its middle

and lower level of management. Hence, corporate decisions are successful till the point it has the

power to bond which helps the leaders to be encouraged and maintain stability, otherwise, the

institution gets trapped in its own trick which leads to degradation of the competition in the

market (TULSIAN, 2016).

Capital Budgeting refers to the calculation of various expenses or investments, which are huge in

nature. The investment and expenses which need to be calculated contain projects like making of

new plant or long term investments. By capital budgeting, cash inflows and outflows for a

lifetime are being formed so that it can be evaluated to know if the potential return is meeting the

assigned target or benchmark. It is also known as 'investment appraisal'.

For an enterprise, it facilitates the use of all opportunities and projects, but because of the limited

availability of capital at a particular point of time, it forces the management to use capital

budgeting to evaluate the maximum return on all available items at a particular time.

Capital budgeting contains various methods like internal rate of return (IRR), discounted cash

flow (DCF), net present value (NPV) and payback period. They may be defined in the following

manner:

DCF Analysis: This examination is similar to the NPV analysis because it takes into

account the initial cash outflows which are needed to fund a project, cash inflows and

other future outflows in the form of servicing and other expenses. Such costs have been

discounted to the current date and thus the resulting number is called NPV (Clarke and

Clarke, 1990).

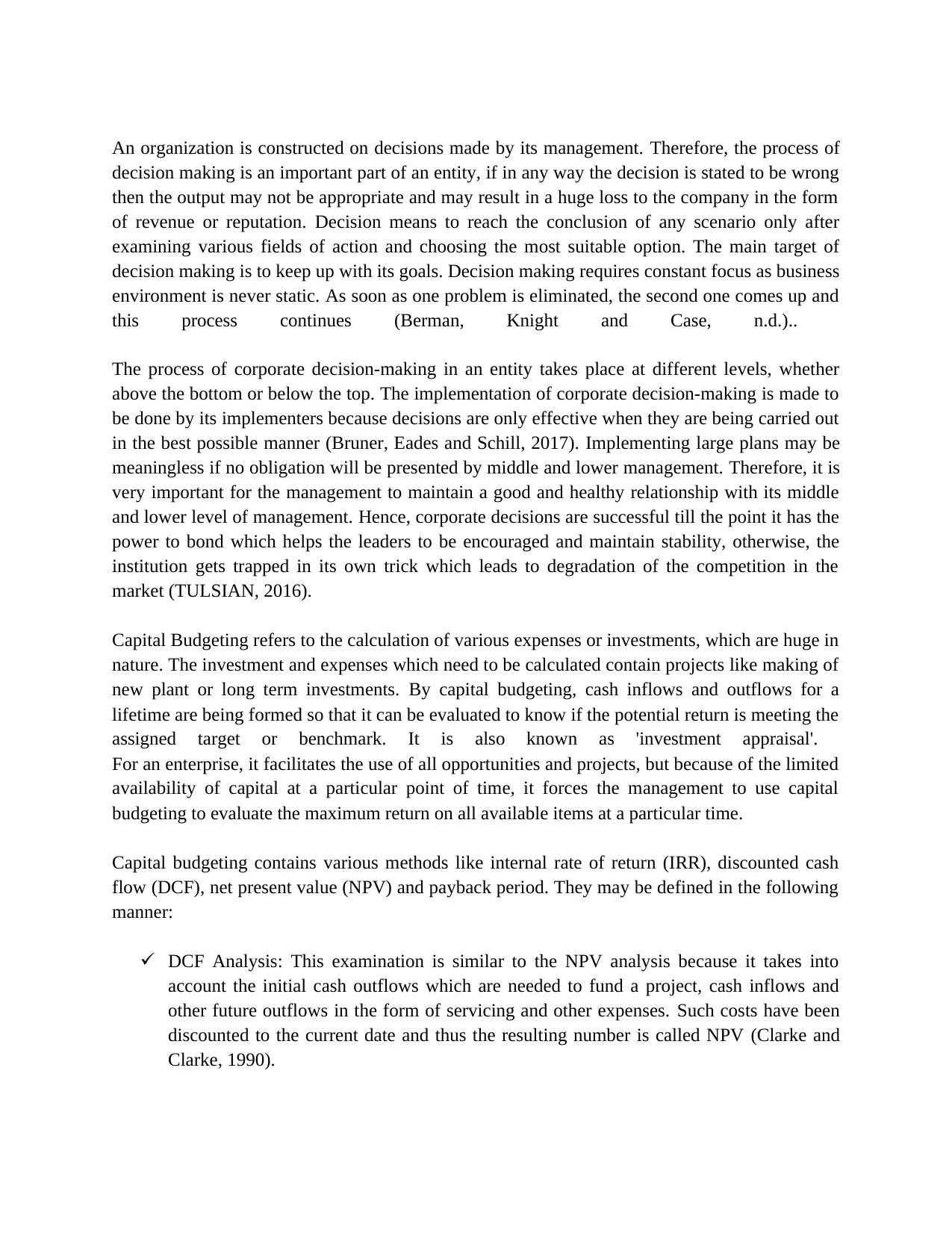

NPV: It is the distinction between the present value conditions of the cash inflow and the

outflow is used by capital budgeting to determine the profitability of the project or long

term investment.

The positive NVP indicates the expected return after exceeds the cost, and the negative

NPV indicates a financial loss of the firm (Fairhurst, 2015). As an example – A and B are

two different projects with different structures of cash flow and the rate of return

required, and then the NVP of the cash will be as follows:

Year A B

0 -80000 -80000

1 20000 -

2 24000 -

3 20000 -

4 27000 65000

5 30000 75000

Required rate of Return 12%

NPV of Project A

Yea

r Cash Flow Present Value of Cash Flows

0 -80000 -80,000

1 20000 17,857

2 24000 19,133

3 20000 14,236

4 27000 17,159

5 30000 17,023

NPV 5,407

NPV of Project B

Yea

r Cash Flow Present Value of Cash Flows

0 -80000 -80000

1 - -

2 - -

3 - -

4 65000 41,309

5 75000 42,557

NPV 3,866

Discounted Payback Period:

It is a form of capital budgeting method which specifies the time period of discontinuing

outflow is used by capital budgeting to determine the profitability of the project or long

term investment.

The positive NVP indicates the expected return after exceeds the cost, and the negative

NPV indicates a financial loss of the firm (Fairhurst, 2015). As an example – A and B are

two different projects with different structures of cash flow and the rate of return

required, and then the NVP of the cash will be as follows:

Year A B

0 -80000 -80000

1 20000 -

2 24000 -

3 20000 -

4 27000 65000

5 30000 75000

Required rate of Return 12%

NPV of Project A

Yea

r Cash Flow Present Value of Cash Flows

0 -80000 -80,000

1 20000 17,857

2 24000 19,133

3 20000 14,236

4 27000 17,159

5 30000 17,023

NPV 5,407

NPV of Project B

Yea

r Cash Flow Present Value of Cash Flows

0 -80000 -80000

1 - -

2 - -

3 - -

4 65000 41,309

5 75000 42,557

NPV 3,866

Discounted Payback Period:

It is a form of capital budgeting method which specifies the time period of discontinuing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

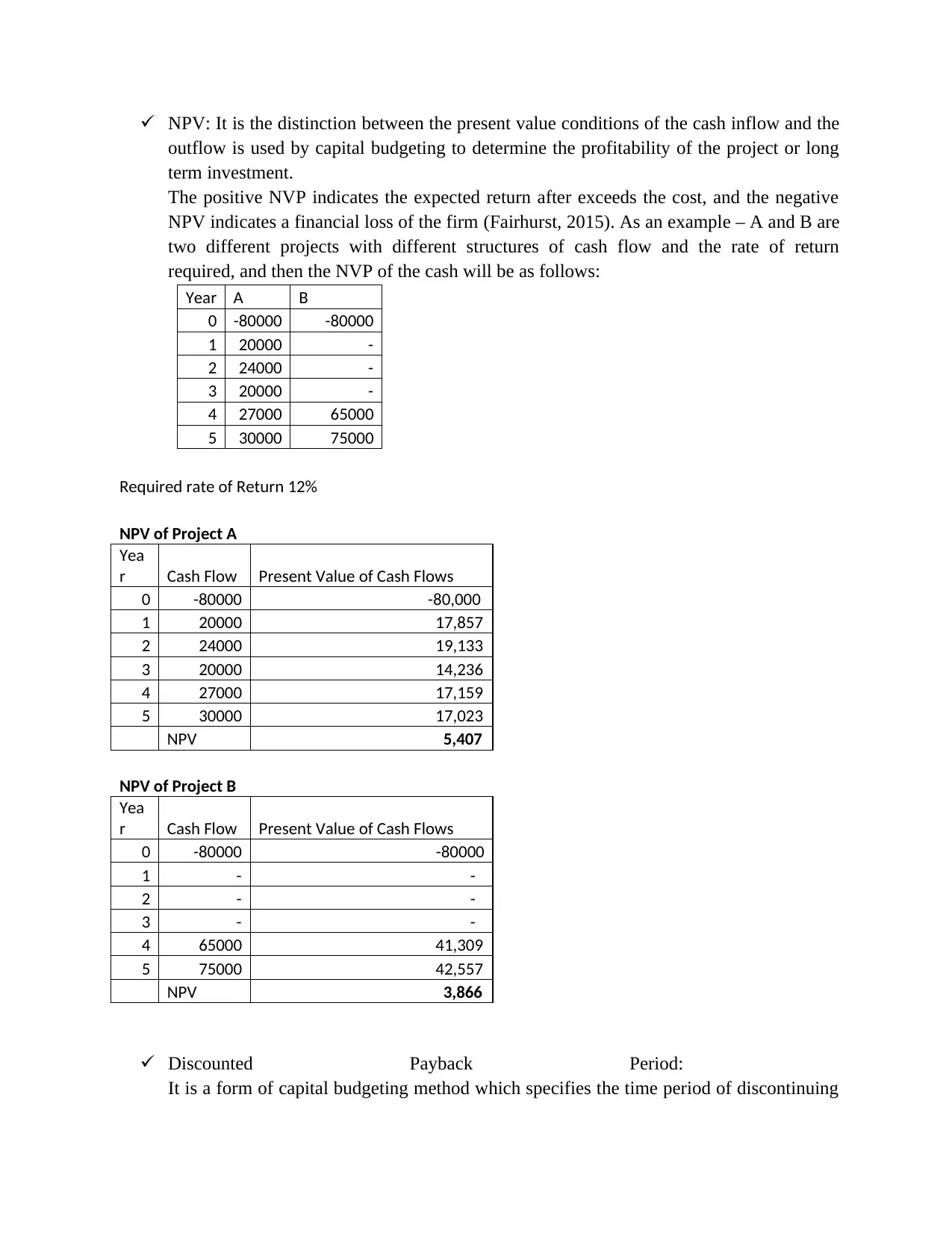

the initial expense by discounting future cash flows and the time value of money.The rule

states that the project will be taken with the discounted payback period offered against

the target period (Taylor, 2008).

IRR: IRR can be defined as the interest rate at which NVP of all the cash flows is zero for

a given project or long term investment. This can be used to measure the attractiveness of

the investments.

The rule says that if the project is satisfactory, then the IRR of a new project will exceed

the required rate of return fixed by the company (Galbraith, Downey and Kates, 2002).

From the same example that is taken for NPV we are also calculating IRR:

For Project A:

For Calculation of IRR, Inflow=Outflow

Let be IRR 14.50% then

PV of Inflows

Year Cash Flow Present Value of Cash Flows

1 20000 17,467

2 24000 18,306

3 20000 13,323

4 27000 15,709

5 30000 15,244

80,049

Therefore, at 14.50% Pv of Inflows = PV of Outflows (80,000). Hence IRR is 14.50%

For Project B:

For Calculation of IRR, Inflow=Outflow

Let be IRR 13.15% then

PV of Inflows

Year Cash Flow Present Value of Cash Flows

1 - -

2 - -

3 - -

4 65000 39,655

5 75000 40,438

80,093

Therefore, at 13.15% Pv of Inflows = PV of Outflows (80,000). Hence IRR is 13.15%

states that the project will be taken with the discounted payback period offered against

the target period (Taylor, 2008).

IRR: IRR can be defined as the interest rate at which NVP of all the cash flows is zero for

a given project or long term investment. This can be used to measure the attractiveness of

the investments.

The rule says that if the project is satisfactory, then the IRR of a new project will exceed

the required rate of return fixed by the company (Galbraith, Downey and Kates, 2002).

From the same example that is taken for NPV we are also calculating IRR:

For Project A:

For Calculation of IRR, Inflow=Outflow

Let be IRR 14.50% then

PV of Inflows

Year Cash Flow Present Value of Cash Flows

1 20000 17,467

2 24000 18,306

3 20000 13,323

4 27000 15,709

5 30000 15,244

80,049

Therefore, at 14.50% Pv of Inflows = PV of Outflows (80,000). Hence IRR is 14.50%

For Project B:

For Calculation of IRR, Inflow=Outflow

Let be IRR 13.15% then

PV of Inflows

Year Cash Flow Present Value of Cash Flows

1 - -

2 - -

3 - -

4 65000 39,655

5 75000 40,438

80,093

Therefore, at 13.15% Pv of Inflows = PV of Outflows (80,000). Hence IRR is 13.15%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital budgeting techniques have the following importance:

Evaluation of risk: Long-term investment or capital expenditure are costs that are

identifiable and significant financial risks. Hence, capital budgeting is necessary for

perfect planning.

Choosing of the best course of action: It helps a company to select the perfect investment

project, which will provide top possible returns based on examining each and every

potential course of action. It concentrates on growing the stakeholder's wealth and also

helps the company to gain an edge in the market (Shim and Siegel, 2008).

Long run of the business: Besides reducing the costs, capital budgeting also helps in

determining company's maximum profits. As it helps in determining the over or under

investments, proper planning and analysis through capital budgeting help to stabilize

business for long run activities…

Irreversible Investments: It requires huge investments even after the funds being limited.

The firm does not have an option of recovering the fund or decision, so, it is advised to

carefully make a decision on investment of money by analyzing and summarizing all the

possible aspects which may create a problem in near future (Hassani, 2016).

Various types of capital budgeting techniques are present. They are as follows:

Sensitivity Analysis: It is a type of analysis for determining the results of a decision using

a different range of variables. Analysts define variables in dependable variables due to

the different values of separate variables that constitute certain constant conditions. This

is also called as what if analysis. Any type of decision like family matter or corporate

level decisions may require analysis for proper functioning. In simple words, it means

determining the sensitivity in output because of change in one input keeping other inputs

constant.

The steps for conducting sensitivity analysis are as follows:

There is a defined base case output; like NPV at some particular point has an input value

(V1) for which sensitivity is to be measured keeping all other input values constant.

A new value of input helps to find the value of output keeping other input values same.

After that, the % change in output and input is calculated.

Dividing the %change in output by the % change in input helps to calculate the

sensitivity.

Evaluation of risk: Long-term investment or capital expenditure are costs that are

identifiable and significant financial risks. Hence, capital budgeting is necessary for

perfect planning.

Choosing of the best course of action: It helps a company to select the perfect investment

project, which will provide top possible returns based on examining each and every

potential course of action. It concentrates on growing the stakeholder's wealth and also

helps the company to gain an edge in the market (Shim and Siegel, 2008).

Long run of the business: Besides reducing the costs, capital budgeting also helps in

determining company's maximum profits. As it helps in determining the over or under

investments, proper planning and analysis through capital budgeting help to stabilize

business for long run activities…

Irreversible Investments: It requires huge investments even after the funds being limited.

The firm does not have an option of recovering the fund or decision, so, it is advised to

carefully make a decision on investment of money by analyzing and summarizing all the

possible aspects which may create a problem in near future (Hassani, 2016).

Various types of capital budgeting techniques are present. They are as follows:

Sensitivity Analysis: It is a type of analysis for determining the results of a decision using

a different range of variables. Analysts define variables in dependable variables due to

the different values of separate variables that constitute certain constant conditions. This

is also called as what if analysis. Any type of decision like family matter or corporate

level decisions may require analysis for proper functioning. In simple words, it means

determining the sensitivity in output because of change in one input keeping other inputs

constant.

The steps for conducting sensitivity analysis are as follows:

There is a defined base case output; like NPV at some particular point has an input value

(V1) for which sensitivity is to be measured keeping all other input values constant.

A new value of input helps to find the value of output keeping other input values same.

After that, the % change in output and input is calculated.

Dividing the %change in output by the % change in input helps to calculate the

sensitivity.

All the above factors help to conclude by determining that higher the sensitivity figure is, the

more sensitive output is to any change in that respective input and vice-versa.

Scenario analysis: It is a process of determining the 'expected value' of an investment at a

specific time after considering the specific changes in the factors such as fixed rate,

interest rate, etc.

As a strategy, this type of analysis needs an analyst to count different reinvestment rates

for determining expected profit that is invested again and again in a specific period. This

analysis, in general, determines the difference between the changes in the values of the

portfolio in different situations and it also follows the rule of “What If” analysis. This

assessment is used to determine the potential risk which consists within a given amount

of investment as related to a different variety of potential events, which may have both

high and low probabilities. By this analysis, an investor can determine the amount of risk

he may undertake.

There are many methods to determine it including one of the most common approaches called

standard deviation of monthly or daily security returns and then calculating the expected value of

the portfolio if each savings generate income that are either two or three standard deviations

below or above the average income. In this way, an analyst determines reasonable assurances

about the change in the value of the portfolio in a particular time period (Holland and

Torregrosa, 2008).

It should be noted that the above two analysis are not the same. A better way to understand is to

take an example. For example, an Equity Analyst wants to manage both sensitivity and scenario

analysis to consider the impact of the Earning Per Share (EPS) impact on company's relative

valuation using price to earnings (P / E) multiples.

The valuation of Sensitivity analysis depends on the variables disturbing valuations, which may

be shown by variables' value and EPS. With the help of this analysis, all the possible outcome

ranges are being recorded. On a different note, scenario analysis is implemented by finding the

outcomes based on a scenario (Khan and Jain, 2014). The analysts should try and set a specific

scenario such as changing market conditions or industry regulations. Then he uses different

variables of that same model that matches the scenario. If these things are gathered and

combined, then there is a wide range of outcomes for the analyst to study with all the cases and

different results that are used in different set of real-life perspectives.

Break Even Analysis: The breakeven point of the company means a point where the

company is making sufficient income to bear all the expenses taking place during that

accounting period. By the definition, if a firm’s net revenue is zero, then there is no profit

and no loss. It is important to mention that the company's debt settlement is not used to

find breakeven points because the lending period is skeptical of the number of return

more sensitive output is to any change in that respective input and vice-versa.

Scenario analysis: It is a process of determining the 'expected value' of an investment at a

specific time after considering the specific changes in the factors such as fixed rate,

interest rate, etc.

As a strategy, this type of analysis needs an analyst to count different reinvestment rates

for determining expected profit that is invested again and again in a specific period. This

analysis, in general, determines the difference between the changes in the values of the

portfolio in different situations and it also follows the rule of “What If” analysis. This

assessment is used to determine the potential risk which consists within a given amount

of investment as related to a different variety of potential events, which may have both

high and low probabilities. By this analysis, an investor can determine the amount of risk

he may undertake.

There are many methods to determine it including one of the most common approaches called

standard deviation of monthly or daily security returns and then calculating the expected value of

the portfolio if each savings generate income that are either two or three standard deviations

below or above the average income. In this way, an analyst determines reasonable assurances

about the change in the value of the portfolio in a particular time period (Holland and

Torregrosa, 2008).

It should be noted that the above two analysis are not the same. A better way to understand is to

take an example. For example, an Equity Analyst wants to manage both sensitivity and scenario

analysis to consider the impact of the Earning Per Share (EPS) impact on company's relative

valuation using price to earnings (P / E) multiples.

The valuation of Sensitivity analysis depends on the variables disturbing valuations, which may

be shown by variables' value and EPS. With the help of this analysis, all the possible outcome

ranges are being recorded. On a different note, scenario analysis is implemented by finding the

outcomes based on a scenario (Khan and Jain, 2014). The analysts should try and set a specific

scenario such as changing market conditions or industry regulations. Then he uses different

variables of that same model that matches the scenario. If these things are gathered and

combined, then there is a wide range of outcomes for the analyst to study with all the cases and

different results that are used in different set of real-life perspectives.

Break Even Analysis: The breakeven point of the company means a point where the

company is making sufficient income to bear all the expenses taking place during that

accounting period. By the definition, if a firm’s net revenue is zero, then there is no profit

and no loss. It is important to mention that the company's debt settlement is not used to

find breakeven points because the lending period is skeptical of the number of return

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

periods for the initial investment, and the breakeven points are equivalent to revenue and

expenses and total cost with zero net revenue (Saunders and Cornett, 2017). This analysis

shows how much sales we need to pay off the cost of doing business. The following two

points should be considered:

Accounting breakeven analysis: An accounting breakeven total cost will be equal to the

total revenue because of which the profit tends to be zero. This can be achieved by

calculating the ratio of variable cost to sales. For example, the ratio is 0.65 so that means

the contribution of every rupee of each unit sold is 0.35. Therefore the ratio of

contribution margin is equal to 0.35. Hence, the breakeven point can be calculated using:

BEP = (Fixed Cost + Depreciation) /Contribution Margin Ratio.

If the depreciation is not added by us, the similar BEP is known as cash breakeven point. The

project reached the solution of breakeven point and recognizes that there is zero return. So, only

the invested value may be recovered.

Financial breakeven analysis: An NPV breakeven takes place when the cash flow is

equivalent to the initial investment which means NPV is zero (Palepu, Healy and Peek,

2016).

So, to reach the breakeven point, analysts have made an analysis of reaching another

level of sales, where the NPV of the project is zero.

Simulation Analysis: The word 'simulation' implies imitation of a thing or some kind of

action.

Monte Carlo Simulation is a study of imitations of real materials or star of affairs or

many different ways that represent the key feature of a random number using the system

(Phillips, 2014).

It basically adds up the level of dynamic analysis of the capital budget, because it is

created in various different situations that are relevant to the analyst's key assumptions

concerning risk. It considers the probability and interactions of variable variations of the

data. The following steps need to be involved in this type of analysis:

The variables need to be found out for both cash inflows and outflow (Reilly and Brown,

2012).

The formula is referred to as associated with all variables and then, for each variable, a

probability distribution will be needed to be determined.

expenses and total cost with zero net revenue (Saunders and Cornett, 2017). This analysis

shows how much sales we need to pay off the cost of doing business. The following two

points should be considered:

Accounting breakeven analysis: An accounting breakeven total cost will be equal to the

total revenue because of which the profit tends to be zero. This can be achieved by

calculating the ratio of variable cost to sales. For example, the ratio is 0.65 so that means

the contribution of every rupee of each unit sold is 0.35. Therefore the ratio of

contribution margin is equal to 0.35. Hence, the breakeven point can be calculated using:

BEP = (Fixed Cost + Depreciation) /Contribution Margin Ratio.

If the depreciation is not added by us, the similar BEP is known as cash breakeven point. The

project reached the solution of breakeven point and recognizes that there is zero return. So, only

the invested value may be recovered.

Financial breakeven analysis: An NPV breakeven takes place when the cash flow is

equivalent to the initial investment which means NPV is zero (Palepu, Healy and Peek,

2016).

So, to reach the breakeven point, analysts have made an analysis of reaching another

level of sales, where the NPV of the project is zero.

Simulation Analysis: The word 'simulation' implies imitation of a thing or some kind of

action.

Monte Carlo Simulation is a study of imitations of real materials or star of affairs or

many different ways that represent the key feature of a random number using the system

(Phillips, 2014).

It basically adds up the level of dynamic analysis of the capital budget, because it is

created in various different situations that are relevant to the analyst's key assumptions

concerning risk. It considers the probability and interactions of variable variations of the

data. The following steps need to be involved in this type of analysis:

The variables need to be found out for both cash inflows and outflow (Reilly and Brown,

2012).

The formula is referred to as associated with all variables and then, for each variable, a

probability distribution will be needed to be determined.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Now, a computer program will be developed so that one can randomly select a value

from the probability distribution of each and every variable and defines the NPV of the

project using this value.

The outcome of this is not the result of single-value results, but a feasibility distribution

of all potential returns.

Simulation analysis is an effective tool that may be helpful to understand the depth of the capital

budgeting so that the investment decisions can be improved. It is still unable to deal with the

uncertainties (Saltelli, Chan and Scott, 2008). Also, such an analysis is not a remedy for all

problems, such as significant inter-relationship scenarios in variables can lead to wrong

consequences and misleading conclusions.

Even capital budgeting is so important, still, it has certain limitations in the corporate world.

Some of them are as follows:

Since it is a long-term perspective, it cannot be used for short-term effects. Also, if

decisions made on the basis of capital budgeting are wrong, then the business may face

adverse effects on the long-term basis of survival in the market. It leads to increase in

operating costs.

The inadequate and inaccurate investment makes the right budget and right capital

formation difficult.

Such decisions usually include large amounts, and if decisions are taken, they need to be

carefully crafted as it cannot be changed afterward.

from the probability distribution of each and every variable and defines the NPV of the

project using this value.

The outcome of this is not the result of single-value results, but a feasibility distribution

of all potential returns.

Simulation analysis is an effective tool that may be helpful to understand the depth of the capital

budgeting so that the investment decisions can be improved. It is still unable to deal with the

uncertainties (Saltelli, Chan and Scott, 2008). Also, such an analysis is not a remedy for all

problems, such as significant inter-relationship scenarios in variables can lead to wrong

consequences and misleading conclusions.

Even capital budgeting is so important, still, it has certain limitations in the corporate world.

Some of them are as follows:

Since it is a long-term perspective, it cannot be used for short-term effects. Also, if

decisions made on the basis of capital budgeting are wrong, then the business may face

adverse effects on the long-term basis of survival in the market. It leads to increase in

operating costs.

The inadequate and inaccurate investment makes the right budget and right capital

formation difficult.

Such decisions usually include large amounts, and if decisions are taken, they need to be

carefully crafted as it cannot be changed afterward.

REFERENCES:

Berman, K., Knight, J. and Case, J. (n.d.). Financial intelligence for HR professionals.

Bruner, R., Eades, K. and Schill, M. (2017). Case studies in finance. Dubuque, IA: McGraw-Hill

Education.

Clarke, R. and Clarke, R. (1990). Strategic financial management. Homewood, Ill.: R.D. Irwin.

Fairhurst, D. (2015). Using Excel for Business Analysis A Guide to Financial Modelling

Fundamenta. John Wiley & Sons.

Galbraith, J., Downey, D. and Kates, A. (2002). Designing dynamic organizations. New York:

AMACOM.

Hassani, B. (2016). Scenario analysis in risk management. Cham: Springer International

Publishing.

Holland, J. and Torregrosa, D. (2008). Capital budgeting. [Washington, D.C.]: Congress of the

U.S., Congressional Budget Office.

Khan, M. and Jain, P. (2014). Financial management. New Delhi: McGraw Hill Education.

Palepu, K., Healy, P. and Peek, E. (2016). Business analysis and valuation. Andover, Hampshire,

United Kingdom: Cengage Learning EMEA.

Phillips, J. (2014). Capm / pmp. New York: McGraw Hill.

Reilly, F. and Brown, K. (2012). Investment analysis & portfolio management. Mason, OH:

South-Western Cengage Learning.

Saltelli, A., Chan, K. and Scott, E. (2008). Sensitivity analysis. Chichester: John Wiley & Sons,

Ltd.

Saunders, A. and Cornett, M. (2017). Financial institutions management. New York: McGraw-

Hill Education.

Shim, J. and Siegel, J. (2008). Financial management. Hauppauge, N.Y.: Barron's Educational

Series.

Taylor, S. (2008). Modelling financial time series. New Jersey: World Scientific.

TULSIAN, B. (2016). TULSIAN'S FINANCIAL MANAGEMENT FOR CA-IPC (GROUP-I).

[S.l.]: S CHAND & CO LTD.

Berman, K., Knight, J. and Case, J. (n.d.). Financial intelligence for HR professionals.

Bruner, R., Eades, K. and Schill, M. (2017). Case studies in finance. Dubuque, IA: McGraw-Hill

Education.

Clarke, R. and Clarke, R. (1990). Strategic financial management. Homewood, Ill.: R.D. Irwin.

Fairhurst, D. (2015). Using Excel for Business Analysis A Guide to Financial Modelling

Fundamenta. John Wiley & Sons.

Galbraith, J., Downey, D. and Kates, A. (2002). Designing dynamic organizations. New York:

AMACOM.

Hassani, B. (2016). Scenario analysis in risk management. Cham: Springer International

Publishing.

Holland, J. and Torregrosa, D. (2008). Capital budgeting. [Washington, D.C.]: Congress of the

U.S., Congressional Budget Office.

Khan, M. and Jain, P. (2014). Financial management. New Delhi: McGraw Hill Education.

Palepu, K., Healy, P. and Peek, E. (2016). Business analysis and valuation. Andover, Hampshire,

United Kingdom: Cengage Learning EMEA.

Phillips, J. (2014). Capm / pmp. New York: McGraw Hill.

Reilly, F. and Brown, K. (2012). Investment analysis & portfolio management. Mason, OH:

South-Western Cengage Learning.

Saltelli, A., Chan, K. and Scott, E. (2008). Sensitivity analysis. Chichester: John Wiley & Sons,

Ltd.

Saunders, A. and Cornett, M. (2017). Financial institutions management. New York: McGraw-

Hill Education.

Shim, J. and Siegel, J. (2008). Financial management. Hauppauge, N.Y.: Barron's Educational

Series.

Taylor, S. (2008). Modelling financial time series. New Jersey: World Scientific.

TULSIAN, B. (2016). TULSIAN'S FINANCIAL MANAGEMENT FOR CA-IPC (GROUP-I).

[S.l.]: S CHAND & CO LTD.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.