Corporate Finance: An In-Depth Analysis of Repsol-YPF Merger

VerifiedAdded on 2021/04/17

|20

|5097

|196

Report

AI Summary

This report analyzes the merger between Repsol and YPF, two major players in the oil industry. It begins by examining the strategic positions of both companies before the acquisition, including Repsol's dominance in Spain and YPF's nationalized status in Argentina. The report explores the strategic options available to both companies before the merger, the purpose behind the merger (including low crude oil prices and market trends), and the valuation of YPF as an independent company, including the calculation of Weighted Average Cost of Capital (WACC) and discounted cash flow (DCF) analysis. The report further discusses the potential of YPF after being absorbed by Repsol, the reasonable price Repsol should offer, the basis of payment, key factors affecting the acquisition's success, and potential threats to the deal. The analysis highlights the economic globalization transforming the oil industry and the need for growth, diversification, and risk reduction. The report concludes with an overview of the merger's implications and outcomes.

Running head: CORPORATE FINANCE

Corporate finance

Name of the Student

Name of the University

Author Note

Corporate finance

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

CORPORATE FINANCE

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

An analysis of the strategic position of the two companies before the acquisition:....................3

The strategic options of the companies before the merger:.........................................................4

The purpose for the merger:........................................................................................................5

Worth YPF as an independent company:....................................................................................6

The potential of YPF after being absorbed by Repsol.................................................................7

The reasonable price that Repsol should offer to acquire YPF...................................................8

The Basis of payment for the acquisition....................................................................................8

The key factors that might affect the level of success of the proposed acquisition.....................9

The threats of the proposed deal................................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

CORPORATE FINANCE

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

An analysis of the strategic position of the two companies before the acquisition:....................3

The strategic options of the companies before the merger:.........................................................4

The purpose for the merger:........................................................................................................5

Worth YPF as an independent company:....................................................................................6

The potential of YPF after being absorbed by Repsol.................................................................7

The reasonable price that Repsol should offer to acquire YPF...................................................8

The Basis of payment for the acquisition....................................................................................8

The key factors that might affect the level of success of the proposed acquisition.....................9

The threats of the proposed deal................................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3

CORPORATE FINANCE

Introduction

The discussion deals with the analysis of the merger taken place between two companies

Repsol and YPF. The merger took place in the march 1999 (Coloma 2016) The CEO of Repsol

took over the Argentinean oil company YPF by taking over 100% of its stock. On January of that

year at a public auction, the Repsol had bought 14.99% of YPF at a price of US$2 billion.

According to the transaction, the Repsol had an option buy the rest of the YPF within the next

three years. The investment of Repsol was more of a financial investment than taking of control

of the business. In order to get the full control Repsol had to take over the rest 85% of the shares

(Costamagna et al. 2015). However, there were a number of obstacles that the company had to

face. The main obstacle was the Article of Association, which states that any bid that envisaged

the control taking of more that 15% of the company’s stock, should be open to the entire

companies share and the requirement should be made in cash. This substantially increased the

level of debt and the company risk. The aim of the Repsol thus, as to swap the shares of YPF in

order to do that the Article of association had to be changed. There was a need for approval from

the YPF shareholders and need of cash to make the takeover (Fernandez 2015). In the following

three years, the changes were made and both of the companies were merged successfully. The

following discussion contains the analysis of the acquisition along with the prospects of the deal.

Discussion

An analysis of the strategic position of the two companies before the acquisition:

The company of Repsol was the largest oil company in Spain before the merge with the

company in 1999 had acquired 60% of the country’s oil refining capacity and 50% of the petrol

CORPORATE FINANCE

Introduction

The discussion deals with the analysis of the merger taken place between two companies

Repsol and YPF. The merger took place in the march 1999 (Coloma 2016) The CEO of Repsol

took over the Argentinean oil company YPF by taking over 100% of its stock. On January of that

year at a public auction, the Repsol had bought 14.99% of YPF at a price of US$2 billion.

According to the transaction, the Repsol had an option buy the rest of the YPF within the next

three years. The investment of Repsol was more of a financial investment than taking of control

of the business. In order to get the full control Repsol had to take over the rest 85% of the shares

(Costamagna et al. 2015). However, there were a number of obstacles that the company had to

face. The main obstacle was the Article of Association, which states that any bid that envisaged

the control taking of more that 15% of the company’s stock, should be open to the entire

companies share and the requirement should be made in cash. This substantially increased the

level of debt and the company risk. The aim of the Repsol thus, as to swap the shares of YPF in

order to do that the Article of association had to be changed. There was a need for approval from

the YPF shareholders and need of cash to make the takeover (Fernandez 2015). In the following

three years, the changes were made and both of the companies were merged successfully. The

following discussion contains the analysis of the acquisition along with the prospects of the deal.

Discussion

An analysis of the strategic position of the two companies before the acquisition:

The company of Repsol was the largest oil company in Spain before the merge with the

company in 1999 had acquired 60% of the country’s oil refining capacity and 50% of the petrol

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

CORPORATE FINANCE

stations (Vandenberghe and Casteele 2017). By the end of 1998 with a workforce of 23762

employees, Repsol has also dominated Spanish petrochemical industry and had 45% stake in the

country’s main gas wholesale and retail operations (Barcelona 2017). The Repsol in almost forty

years became the Spain’s largest company in terms of turnover and profits. After spending

thousand millions of pesetas, the company had created a sound brand image. In 1989, after

floating to the stock exchange with market capitalization of €721 million, Repsol negotiated

important agreements with the foreign petrol companies and Spanish banks. The number of

shares with the US and Japanese banks doubled at that time (Muñiz, Alvídrez and Téllez 2015).

On the other hand, the YPF (Direccion Nacional De Yacimientos Petroliferos Fiscales)

was formed in the year 1922 when the petrol industry by the argentine government was

nationalized (Velez-Ocampo, Gonzalez-Perez. and Herrera-Cano 2017). By the end of the

nineteenth thirties, the company became dominant and contributed 68% of the company’s total

oil production. The dominance increased with time and the market share rose to 84% and the

company became a gas producer (Olivares 2015).

After years of confining its business in Spain, the Repsol in 1996 started to invest outside

the nation. Their focus was lain America, where the government was facing the major financial

problems with the institutions like World Bank, IMF, IDB (Dunlap et al. 2016). The company

also expanded in North America, Europe.

The strategic options of the companies before the merger:

Before the merger of the Respol and YPF, the Respol business was structured into four

main segments that are refining and marketing, petrochemicals, gas and electricity and E&P. In

1997, the company was first merged with Latin America and obtained a set off new objectives

CORPORATE FINANCE

stations (Vandenberghe and Casteele 2017). By the end of 1998 with a workforce of 23762

employees, Repsol has also dominated Spanish petrochemical industry and had 45% stake in the

country’s main gas wholesale and retail operations (Barcelona 2017). The Repsol in almost forty

years became the Spain’s largest company in terms of turnover and profits. After spending

thousand millions of pesetas, the company had created a sound brand image. In 1989, after

floating to the stock exchange with market capitalization of €721 million, Repsol negotiated

important agreements with the foreign petrol companies and Spanish banks. The number of

shares with the US and Japanese banks doubled at that time (Muñiz, Alvídrez and Téllez 2015).

On the other hand, the YPF (Direccion Nacional De Yacimientos Petroliferos Fiscales)

was formed in the year 1922 when the petrol industry by the argentine government was

nationalized (Velez-Ocampo, Gonzalez-Perez. and Herrera-Cano 2017). By the end of the

nineteenth thirties, the company became dominant and contributed 68% of the company’s total

oil production. The dominance increased with time and the market share rose to 84% and the

company became a gas producer (Olivares 2015).

After years of confining its business in Spain, the Repsol in 1996 started to invest outside

the nation. Their focus was lain America, where the government was facing the major financial

problems with the institutions like World Bank, IMF, IDB (Dunlap et al. 2016). The company

also expanded in North America, Europe.

The strategic options of the companies before the merger:

Before the merger of the Respol and YPF, the Respol business was structured into four

main segments that are refining and marketing, petrochemicals, gas and electricity and E&P. In

1997, the company was first merged with Latin America and obtained a set off new objectives

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

CORPORATE FINANCE

investing 10.4 billion Euros (de Matías Batalla 2015) Over the last few years, the company had

been encountering many upstream, downstream. The Respol suffered from lack of reserves, and

the crude oil price fell off sharply. While profit was increased by 18%, the sector in the Europe

fell by 36% on average. Other than the strategies, other the dominance in Spain, The Company

tried to increase the business by generating electricity and monetizing the gas reserves. This

expansion in both Europe and Latin America showed high rates of growth with new set of

business opportunities. The new electricity generating technology using the combined power

station helped in minimizing risk and was attractive economically. Although in 1999, the

investment plan changed drastically with the purchase of YPF. The value of the investment was

almost 50% more than what the company had planned for five years which was around €14.5

billion (Graham Harvey and Puri 2015). The Repsols strength was refining and marketing and

YPF involves in exploration and production, therefore both complement each other hand the

collaboration would increase the self-sufficiency of the business.

The purpose for the merger:

The economic globalization transformed the structure of the oil industry this also created

a large number of corporations, which were not only looking for economies of scale and cost

reduction but also significant investments for new business opportunities(Dunlap et al. 2016).

There was a tremendous need for growth, diversification and reduction of risk. In order to tackle

the situation many companies of the oil industries were being merged. The collaborated

companies were called oil giants who had the competitive advantage in the industry (Graham,

Harvey and Puri 2015). The idea of the merger of the Repsol and YPF would enable the

company to face the competition of the middle ranking oil companies in terms of market

capitalization; this would also allow the both to attain more growth than its competitors.

CORPORATE FINANCE

investing 10.4 billion Euros (de Matías Batalla 2015) Over the last few years, the company had

been encountering many upstream, downstream. The Respol suffered from lack of reserves, and

the crude oil price fell off sharply. While profit was increased by 18%, the sector in the Europe

fell by 36% on average. Other than the strategies, other the dominance in Spain, The Company

tried to increase the business by generating electricity and monetizing the gas reserves. This

expansion in both Europe and Latin America showed high rates of growth with new set of

business opportunities. The new electricity generating technology using the combined power

station helped in minimizing risk and was attractive economically. Although in 1999, the

investment plan changed drastically with the purchase of YPF. The value of the investment was

almost 50% more than what the company had planned for five years which was around €14.5

billion (Graham Harvey and Puri 2015). The Repsols strength was refining and marketing and

YPF involves in exploration and production, therefore both complement each other hand the

collaboration would increase the self-sufficiency of the business.

The purpose for the merger:

The economic globalization transformed the structure of the oil industry this also created

a large number of corporations, which were not only looking for economies of scale and cost

reduction but also significant investments for new business opportunities(Dunlap et al. 2016).

There was a tremendous need for growth, diversification and reduction of risk. In order to tackle

the situation many companies of the oil industries were being merged. The collaborated

companies were called oil giants who had the competitive advantage in the industry (Graham,

Harvey and Puri 2015). The idea of the merger of the Repsol and YPF would enable the

company to face the competition of the middle ranking oil companies in terms of market

capitalization; this would also allow the both to attain more growth than its competitors.

6

CORPORATE FINANCE

The main reasons for the combining of the two companies can be jotted down as follows:

The price of the crude oil was low, therefore there was a need for the companies

to combine to increase their volume to enhance cost saving (Parola Ellis and

Golden 2015).

Change in the trend in the market and increase in competition forced them to

merge.

Progress in the technology and the extraction techniques had reduced the cost for

exploration; this educed the barriers for the competitors to enter the market.

Repsol has YPF combined to tackle the situation.

There was a need for considerable economies of scale in industry.

The need to maintain a potential growth rate and maintain a scale that would

make the company exists for a long time.

The rise in the new opportunities for vertical integration for oil companies and

anticipation for growth required considerable investment in infrastructure. The

combination was needed to help in this.

Worth YPF as an independent company:

Before the merger of the two companies, there was a valuation of the firm’s equity. This

was done to determine the price that the YPF shareholders had to offer. According to the Alfonso

Cortina, an internal team was engaged in order to value the YPF to assess the price

recommended (Capone 2015).

From the given information, the value of the YPF can be found out:

According to the data, the current price in dollars of the YPF share before acquisition was $41.85

CORPORATE FINANCE

The main reasons for the combining of the two companies can be jotted down as follows:

The price of the crude oil was low, therefore there was a need for the companies

to combine to increase their volume to enhance cost saving (Parola Ellis and

Golden 2015).

Change in the trend in the market and increase in competition forced them to

merge.

Progress in the technology and the extraction techniques had reduced the cost for

exploration; this educed the barriers for the competitors to enter the market.

Repsol has YPF combined to tackle the situation.

There was a need for considerable economies of scale in industry.

The need to maintain a potential growth rate and maintain a scale that would

make the company exists for a long time.

The rise in the new opportunities for vertical integration for oil companies and

anticipation for growth required considerable investment in infrastructure. The

combination was needed to help in this.

Worth YPF as an independent company:

Before the merger of the two companies, there was a valuation of the firm’s equity. This

was done to determine the price that the YPF shareholders had to offer. According to the Alfonso

Cortina, an internal team was engaged in order to value the YPF to assess the price

recommended (Capone 2015).

From the given information, the value of the YPF can be found out:

According to the data, the current price in dollars of the YPF share before acquisition was $41.85

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

CORPORATE FINANCE

The total no of shares (in millions) were: 353shares

Therefore, the independent value of the company in million=353*41.85=$14773.05

The various other finding of the valuation are noted down as follows:

The price of the crude oil in 1999 with a discount of 3.5% was $16.

The operation margin of the YPF in 1999 based on historic cost structure showed a

growth 1.5 % each year in the last 4 years in exploration and production. This reflects

that the company had a great efficiency.

Compared to the last year that 1998 the YPF showed a growth of 5% in the income

refining and marketing sector (Parola, Ellis and Golden 2015).

Operating margin of 16% in the year 1999 in refining and marketing was 16% with an

estimated growth of 2% per year.

Calculation of Weighted Average cost of capital

The discounting rate that is used for calculating the discounted cash flow is the WACC.

The weighted average cost of capital has two component cost of equity and cost of debt. This

components are discussed below.

The cost of equity or the expected return is calculated using the Capital Assets pricing

model. In the current case the CAPM model have been adjusted to reflect the risk involved in the

international investing. The use of the country risk premium provides a significant impact on the

valuation of the company. In the current case the country risk premium of 6.21% is used for

calculating the expected return using CAPM. The formula used for calculating the expected

return on equity is:

CORPORATE FINANCE

The total no of shares (in millions) were: 353shares

Therefore, the independent value of the company in million=353*41.85=$14773.05

The various other finding of the valuation are noted down as follows:

The price of the crude oil in 1999 with a discount of 3.5% was $16.

The operation margin of the YPF in 1999 based on historic cost structure showed a

growth 1.5 % each year in the last 4 years in exploration and production. This reflects

that the company had a great efficiency.

Compared to the last year that 1998 the YPF showed a growth of 5% in the income

refining and marketing sector (Parola, Ellis and Golden 2015).

Operating margin of 16% in the year 1999 in refining and marketing was 16% with an

estimated growth of 2% per year.

Calculation of Weighted Average cost of capital

The discounting rate that is used for calculating the discounted cash flow is the WACC.

The weighted average cost of capital has two component cost of equity and cost of debt. This

components are discussed below.

The cost of equity or the expected return is calculated using the Capital Assets pricing

model. In the current case the CAPM model have been adjusted to reflect the risk involved in the

international investing. The use of the country risk premium provides a significant impact on the

valuation of the company. In the current case the country risk premium of 6.21% is used for

calculating the expected return using CAPM. The formula used for calculating the expected

return on equity is:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

CORPORATE FINANCE

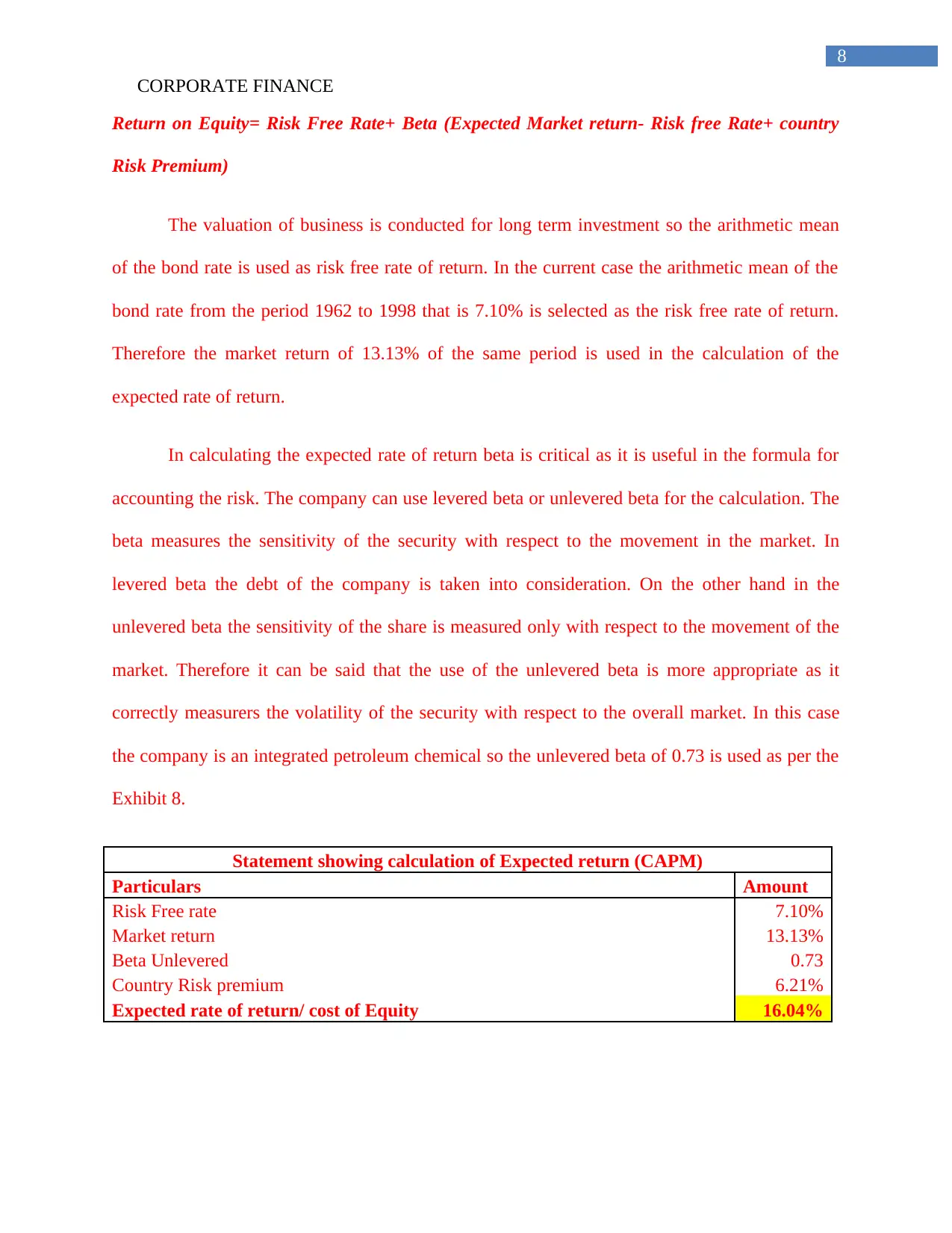

Return on Equity= Risk Free Rate+ Beta (Expected Market return- Risk free Rate+ country

Risk Premium)

The valuation of business is conducted for long term investment so the arithmetic mean

of the bond rate is used as risk free rate of return. In the current case the arithmetic mean of the

bond rate from the period 1962 to 1998 that is 7.10% is selected as the risk free rate of return.

Therefore the market return of 13.13% of the same period is used in the calculation of the

expected rate of return.

In calculating the expected rate of return beta is critical as it is useful in the formula for

accounting the risk. The company can use levered beta or unlevered beta for the calculation. The

beta measures the sensitivity of the security with respect to the movement in the market. In

levered beta the debt of the company is taken into consideration. On the other hand in the

unlevered beta the sensitivity of the share is measured only with respect to the movement of the

market. Therefore it can be said that the use of the unlevered beta is more appropriate as it

correctly measurers the volatility of the security with respect to the overall market. In this case

the company is an integrated petroleum chemical so the unlevered beta of 0.73 is used as per the

Exhibit 8.

Statement showing calculation of Expected return (CAPM)

Particulars Amount

Risk Free rate 7.10%

Market return 13.13%

Beta Unlevered 0.73

Country Risk premium 6.21%

Expected rate of return/ cost of Equity 16.04%

CORPORATE FINANCE

Return on Equity= Risk Free Rate+ Beta (Expected Market return- Risk free Rate+ country

Risk Premium)

The valuation of business is conducted for long term investment so the arithmetic mean

of the bond rate is used as risk free rate of return. In the current case the arithmetic mean of the

bond rate from the period 1962 to 1998 that is 7.10% is selected as the risk free rate of return.

Therefore the market return of 13.13% of the same period is used in the calculation of the

expected rate of return.

In calculating the expected rate of return beta is critical as it is useful in the formula for

accounting the risk. The company can use levered beta or unlevered beta for the calculation. The

beta measures the sensitivity of the security with respect to the movement in the market. In

levered beta the debt of the company is taken into consideration. On the other hand in the

unlevered beta the sensitivity of the share is measured only with respect to the movement of the

market. Therefore it can be said that the use of the unlevered beta is more appropriate as it

correctly measurers the volatility of the security with respect to the overall market. In this case

the company is an integrated petroleum chemical so the unlevered beta of 0.73 is used as per the

Exhibit 8.

Statement showing calculation of Expected return (CAPM)

Particulars Amount

Risk Free rate 7.10%

Market return 13.13%

Beta Unlevered 0.73

Country Risk premium 6.21%

Expected rate of return/ cost of Equity 16.04%

9

CORPORATE FINANCE

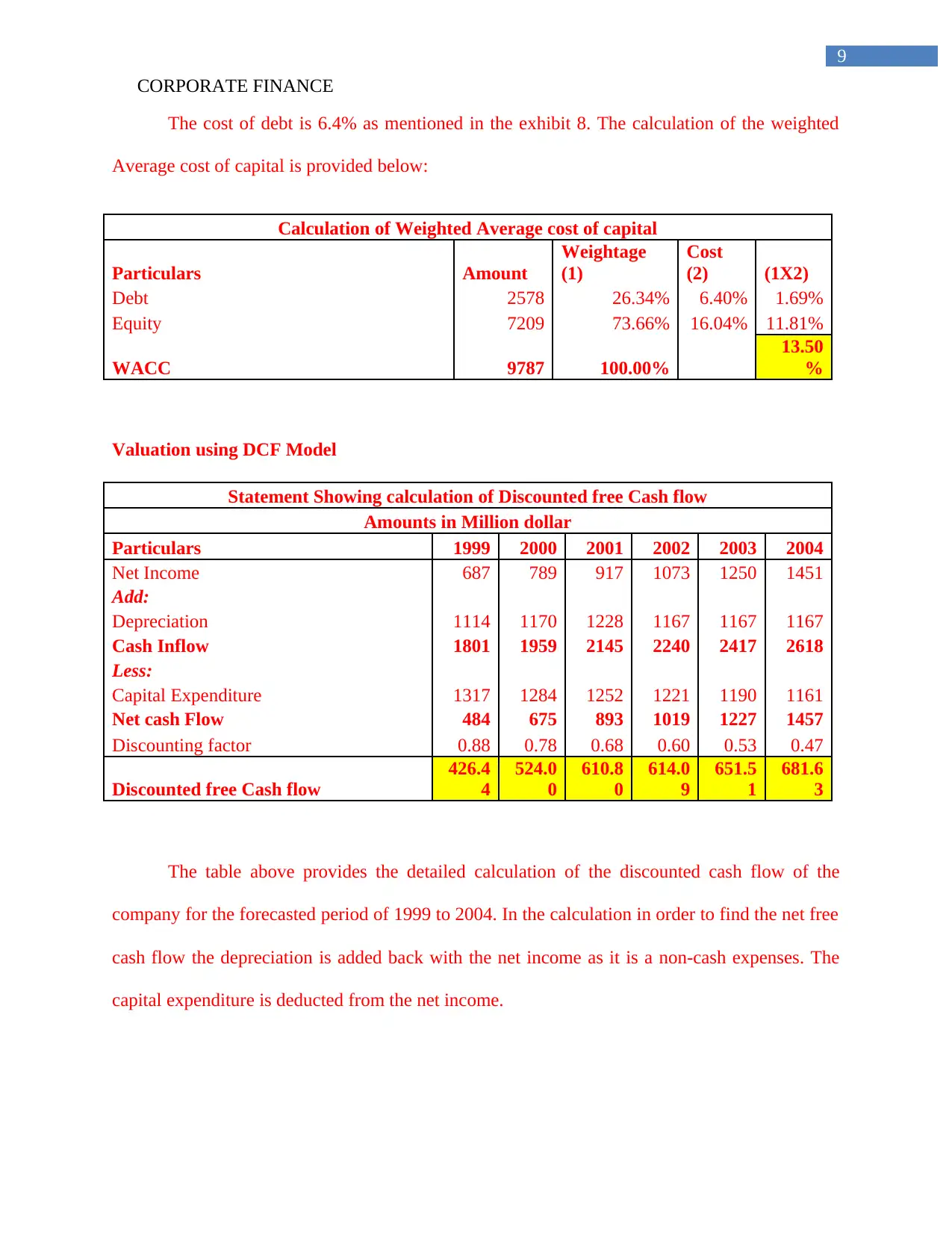

The cost of debt is 6.4% as mentioned in the exhibit 8. The calculation of the weighted

Average cost of capital is provided below:

Calculation of Weighted Average cost of capital

Particulars Amount

Weightage

(1)

Cost

(2) (1X2)

Debt 2578 26.34% 6.40% 1.69%

Equity 7209 73.66% 16.04% 11.81%

WACC 9787 100.00%

13.50

%

Valuation using DCF Model

Statement Showing calculation of Discounted free Cash flow

Amounts in Million dollar

Particulars 1999 2000 2001 2002 2003 2004

Net Income 687 789 917 1073 1250 1451

Add:

Depreciation 1114 1170 1228 1167 1167 1167

Cash Inflow 1801 1959 2145 2240 2417 2618

Less:

Capital Expenditure 1317 1284 1252 1221 1190 1161

Net cash Flow 484 675 893 1019 1227 1457

Discounting factor 0.88 0.78 0.68 0.60 0.53 0.47

Discounted free Cash flow

426.4

4

524.0

0

610.8

0

614.0

9

651.5

1

681.6

3

The table above provides the detailed calculation of the discounted cash flow of the

company for the forecasted period of 1999 to 2004. In the calculation in order to find the net free

cash flow the depreciation is added back with the net income as it is a non-cash expenses. The

capital expenditure is deducted from the net income.

CORPORATE FINANCE

The cost of debt is 6.4% as mentioned in the exhibit 8. The calculation of the weighted

Average cost of capital is provided below:

Calculation of Weighted Average cost of capital

Particulars Amount

Weightage

(1)

Cost

(2) (1X2)

Debt 2578 26.34% 6.40% 1.69%

Equity 7209 73.66% 16.04% 11.81%

WACC 9787 100.00%

13.50

%

Valuation using DCF Model

Statement Showing calculation of Discounted free Cash flow

Amounts in Million dollar

Particulars 1999 2000 2001 2002 2003 2004

Net Income 687 789 917 1073 1250 1451

Add:

Depreciation 1114 1170 1228 1167 1167 1167

Cash Inflow 1801 1959 2145 2240 2417 2618

Less:

Capital Expenditure 1317 1284 1252 1221 1190 1161

Net cash Flow 484 675 893 1019 1227 1457

Discounting factor 0.88 0.78 0.68 0.60 0.53 0.47

Discounted free Cash flow

426.4

4

524.0

0

610.8

0

614.0

9

651.5

1

681.6

3

The table above provides the detailed calculation of the discounted cash flow of the

company for the forecasted period of 1999 to 2004. In the calculation in order to find the net free

cash flow the depreciation is added back with the net income as it is a non-cash expenses. The

capital expenditure is deducted from the net income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

CORPORATE FINANCE

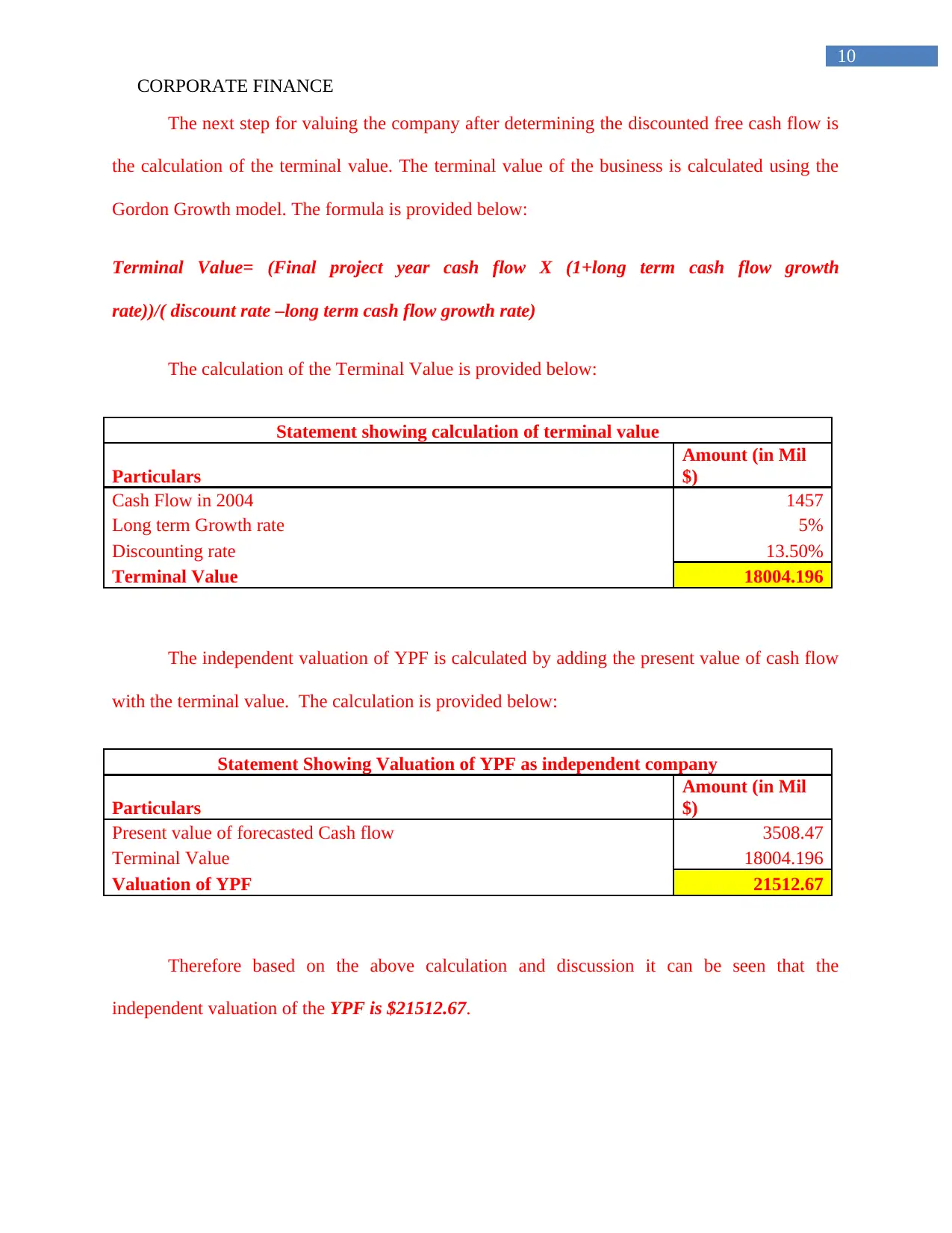

The next step for valuing the company after determining the discounted free cash flow is

the calculation of the terminal value. The terminal value of the business is calculated using the

Gordon Growth model. The formula is provided below:

Terminal Value= (Final project year cash flow X (1+long term cash flow growth

rate))/( discount rate –long term cash flow growth rate)

The calculation of the Terminal Value is provided below:

Statement showing calculation of terminal value

Particulars

Amount (in Mil

$)

Cash Flow in 2004 1457

Long term Growth rate 5%

Discounting rate 13.50%

Terminal Value 18004.196

The independent valuation of YPF is calculated by adding the present value of cash flow

with the terminal value. The calculation is provided below:

Statement Showing Valuation of YPF as independent company

Particulars

Amount (in Mil

$)

Present value of forecasted Cash flow 3508.47

Terminal Value 18004.196

Valuation of YPF 21512.67

Therefore based on the above calculation and discussion it can be seen that the

independent valuation of the YPF is $21512.67.

CORPORATE FINANCE

The next step for valuing the company after determining the discounted free cash flow is

the calculation of the terminal value. The terminal value of the business is calculated using the

Gordon Growth model. The formula is provided below:

Terminal Value= (Final project year cash flow X (1+long term cash flow growth

rate))/( discount rate –long term cash flow growth rate)

The calculation of the Terminal Value is provided below:

Statement showing calculation of terminal value

Particulars

Amount (in Mil

$)

Cash Flow in 2004 1457

Long term Growth rate 5%

Discounting rate 13.50%

Terminal Value 18004.196

The independent valuation of YPF is calculated by adding the present value of cash flow

with the terminal value. The calculation is provided below:

Statement Showing Valuation of YPF as independent company

Particulars

Amount (in Mil

$)

Present value of forecasted Cash flow 3508.47

Terminal Value 18004.196

Valuation of YPF 21512.67

Therefore based on the above calculation and discussion it can be seen that the

independent valuation of the YPF is $21512.67.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

CORPORATE FINANCE

The potential of YPF after being absorbed by Repsol

The Repsol’s acquisition of YPF since acquisition in 1999 has demonstrated a full

success in financial and operational management. The rate of sales has increased annually by

24% as a result the net profit increased by 16% per year (Fernandez 2015). The base year is

taken as 1999 and the current year is taken as 2011 in the current analysis. However, the rate of

profit isn’t equivalent to the rate of sales. This is due to the increase of the cost of sales as more

crude oil was purchased from producers at higher prices than the local oil refiners and producers

(Henson. and Sandberg 2017). The consolidation has also enhanced the import of manufacturing

premium gasoil and standard car oil. This import was done to meet the higher demand for the

products in the local market and comply with the applicable regulatory requirements of the

area(Holburn and Vanden Bergh 2014). The YPFs new financial controller states that the there

were several risks in the financial system of the company as the YPF offered 100% of its profit

to the shareholders. The Repsol invested US$12 billion and a got a return of US$2 billion.

Therefore, the YPF had a great potential in terms of profit and the acquisition was a great success

for both the companies.

In order to calculate the potential value of YPF after is acquired by Repsol the discounted

cash flow model for valuation is used. In this case it should noted that after YPF is absorbed by

Repsol then combined valuation of the company should be made. In this model the expected rate

of return of the shareholders are assumed to be the same. The cost of debt combined is 7.4% as

provided in the exhibit 8. In order to calculate the WACC the debt and equity of both the

company is combined for the year 1998 to determine the weightage. The calculation of WACC is

provided below:

CORPORATE FINANCE

The potential of YPF after being absorbed by Repsol

The Repsol’s acquisition of YPF since acquisition in 1999 has demonstrated a full

success in financial and operational management. The rate of sales has increased annually by

24% as a result the net profit increased by 16% per year (Fernandez 2015). The base year is

taken as 1999 and the current year is taken as 2011 in the current analysis. However, the rate of

profit isn’t equivalent to the rate of sales. This is due to the increase of the cost of sales as more

crude oil was purchased from producers at higher prices than the local oil refiners and producers

(Henson. and Sandberg 2017). The consolidation has also enhanced the import of manufacturing

premium gasoil and standard car oil. This import was done to meet the higher demand for the

products in the local market and comply with the applicable regulatory requirements of the

area(Holburn and Vanden Bergh 2014). The YPFs new financial controller states that the there

were several risks in the financial system of the company as the YPF offered 100% of its profit

to the shareholders. The Repsol invested US$12 billion and a got a return of US$2 billion.

Therefore, the YPF had a great potential in terms of profit and the acquisition was a great success

for both the companies.

In order to calculate the potential value of YPF after is acquired by Repsol the discounted

cash flow model for valuation is used. In this case it should noted that after YPF is absorbed by

Repsol then combined valuation of the company should be made. In this model the expected rate

of return of the shareholders are assumed to be the same. The cost of debt combined is 7.4% as

provided in the exhibit 8. In order to calculate the WACC the debt and equity of both the

company is combined for the year 1998 to determine the weightage. The calculation of WACC is

provided below:

12

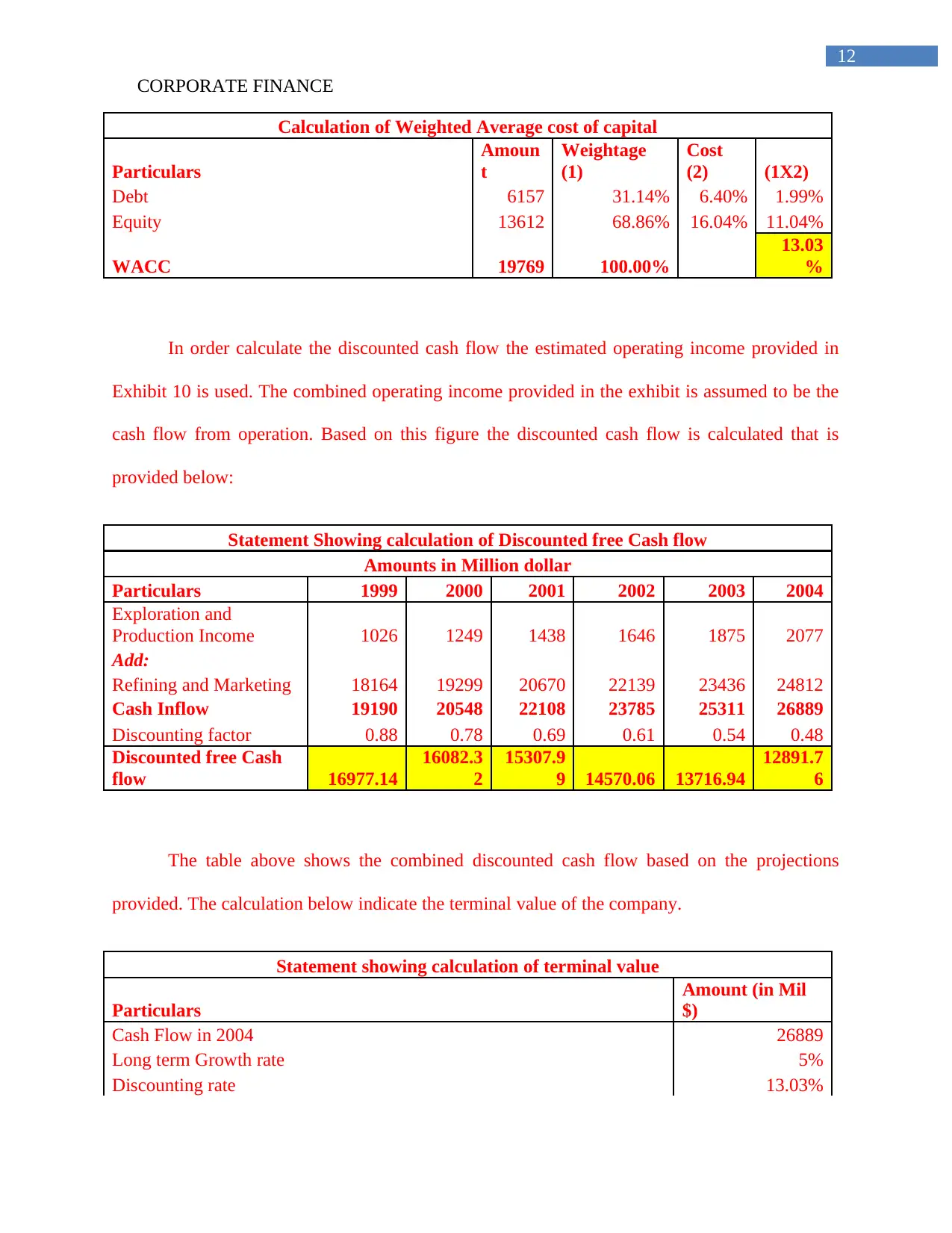

CORPORATE FINANCE

Calculation of Weighted Average cost of capital

Particulars

Amoun

t

Weightage

(1)

Cost

(2) (1X2)

Debt 6157 31.14% 6.40% 1.99%

Equity 13612 68.86% 16.04% 11.04%

WACC 19769 100.00%

13.03

%

In order calculate the discounted cash flow the estimated operating income provided in

Exhibit 10 is used. The combined operating income provided in the exhibit is assumed to be the

cash flow from operation. Based on this figure the discounted cash flow is calculated that is

provided below:

Statement Showing calculation of Discounted free Cash flow

Amounts in Million dollar

Particulars 1999 2000 2001 2002 2003 2004

Exploration and

Production Income 1026 1249 1438 1646 1875 2077

Add:

Refining and Marketing 18164 19299 20670 22139 23436 24812

Cash Inflow 19190 20548 22108 23785 25311 26889

Discounting factor 0.88 0.78 0.69 0.61 0.54 0.48

Discounted free Cash

flow 16977.14

16082.3

2

15307.9

9 14570.06 13716.94

12891.7

6

The table above shows the combined discounted cash flow based on the projections

provided. The calculation below indicate the terminal value of the company.

Statement showing calculation of terminal value

Particulars

Amount (in Mil

$)

Cash Flow in 2004 26889

Long term Growth rate 5%

Discounting rate 13.03%

CORPORATE FINANCE

Calculation of Weighted Average cost of capital

Particulars

Amoun

t

Weightage

(1)

Cost

(2) (1X2)

Debt 6157 31.14% 6.40% 1.99%

Equity 13612 68.86% 16.04% 11.04%

WACC 19769 100.00%

13.03

%

In order calculate the discounted cash flow the estimated operating income provided in

Exhibit 10 is used. The combined operating income provided in the exhibit is assumed to be the

cash flow from operation. Based on this figure the discounted cash flow is calculated that is

provided below:

Statement Showing calculation of Discounted free Cash flow

Amounts in Million dollar

Particulars 1999 2000 2001 2002 2003 2004

Exploration and

Production Income 1026 1249 1438 1646 1875 2077

Add:

Refining and Marketing 18164 19299 20670 22139 23436 24812

Cash Inflow 19190 20548 22108 23785 25311 26889

Discounting factor 0.88 0.78 0.69 0.61 0.54 0.48

Discounted free Cash

flow 16977.14

16082.3

2

15307.9

9 14570.06 13716.94

12891.7

6

The table above shows the combined discounted cash flow based on the projections

provided. The calculation below indicate the terminal value of the company.

Statement showing calculation of terminal value

Particulars

Amount (in Mil

$)

Cash Flow in 2004 26889

Long term Growth rate 5%

Discounting rate 13.03%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.