Corporate Accounting Assignment: Financial Analysis and Valuation

VerifiedAdded on 2020/04/07

|10

|2109

|62

Homework Assignment

AI Summary

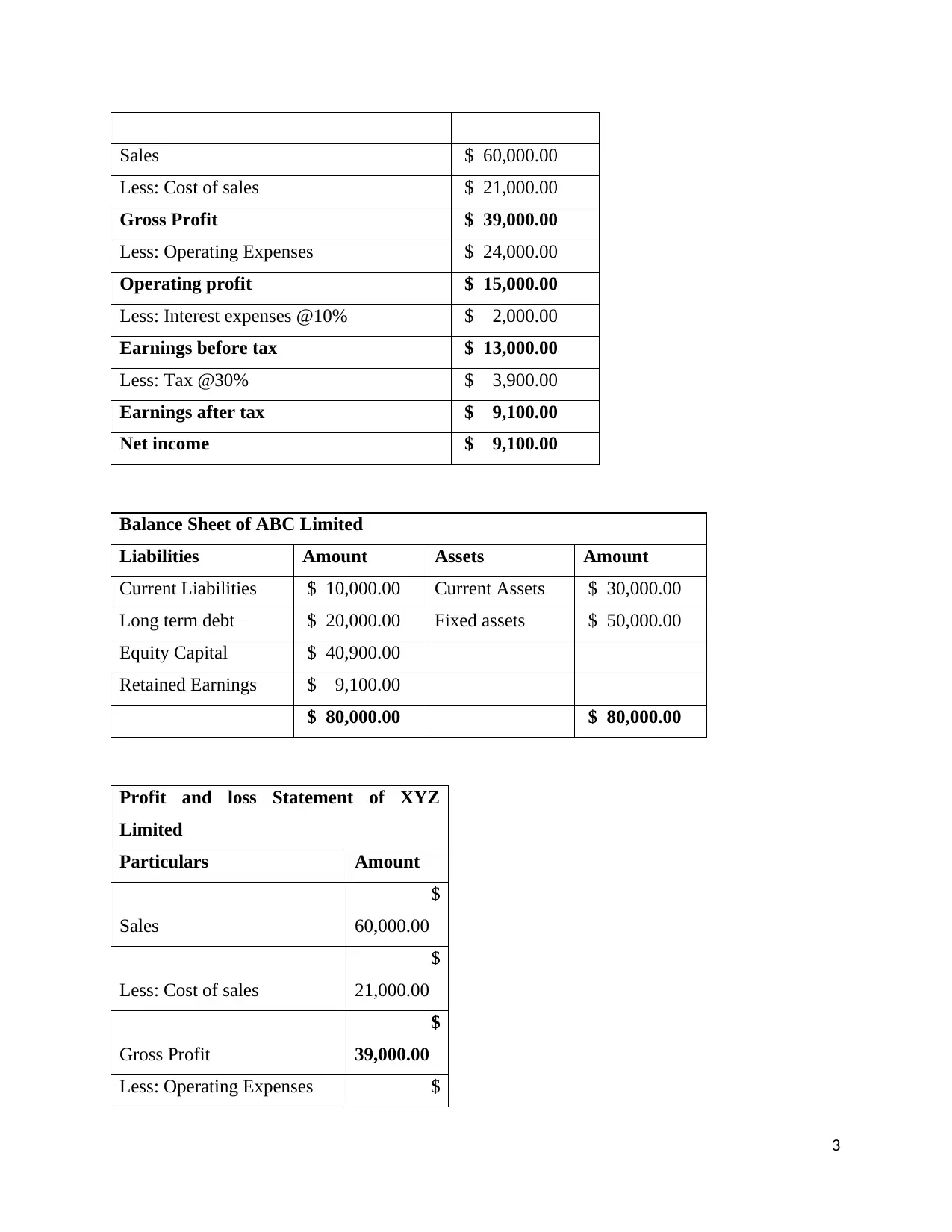

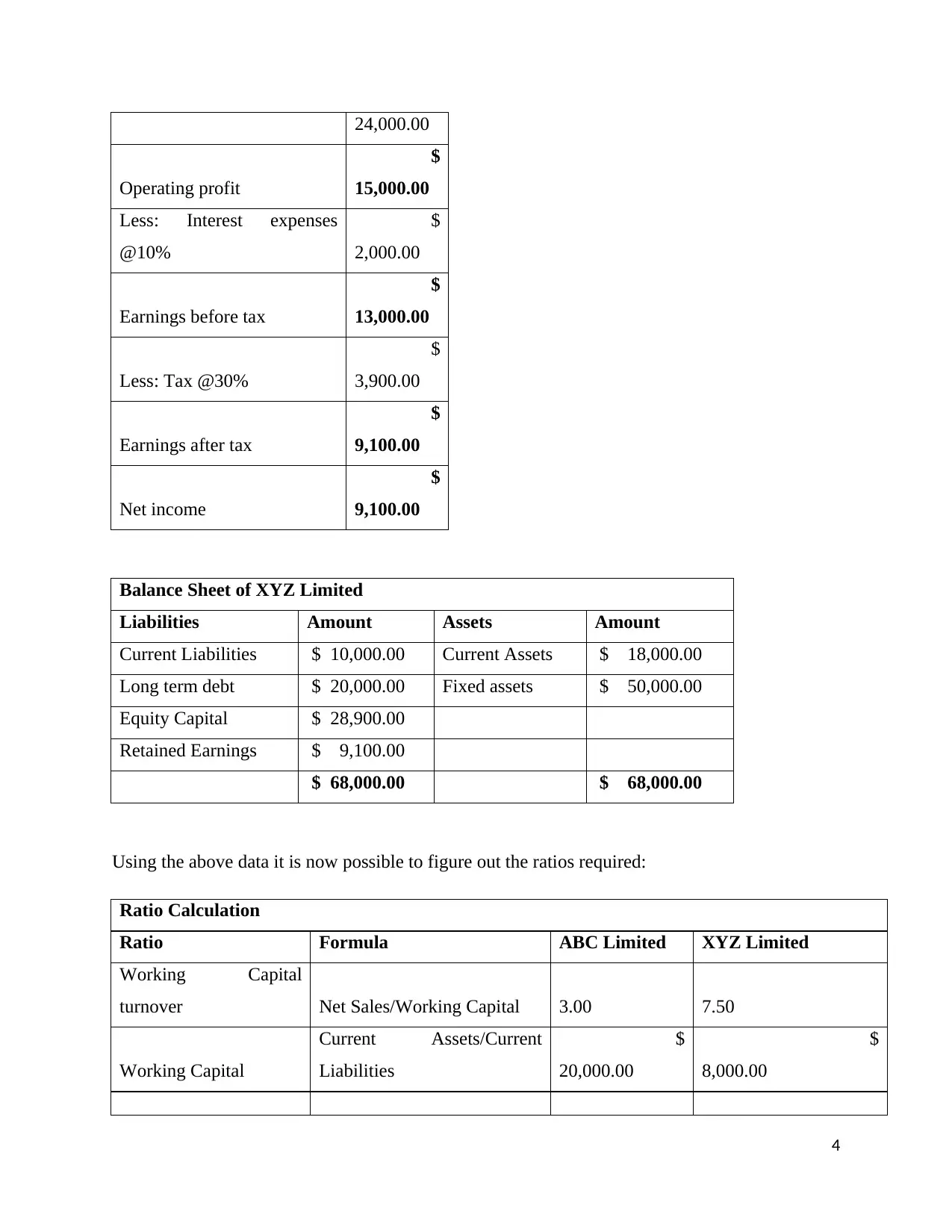

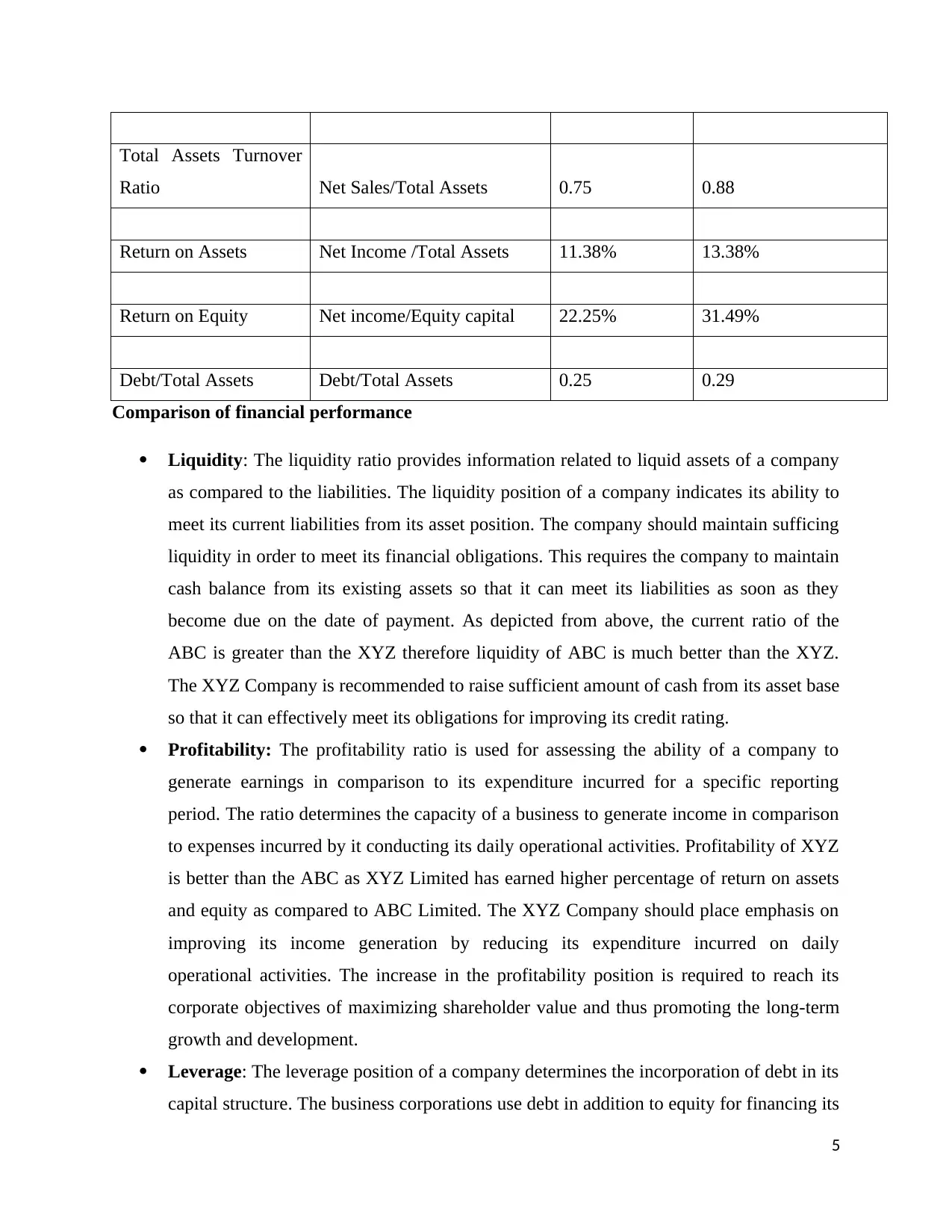

This comprehensive corporate accounting assignment delves into financial statement analysis, offering solutions to various problems. It begins by constructing hypothetical balance sheets and profit and loss statements for two companies, ABC Limited and XYZ Limited, using assumed figures to demonstrate ratio calculations. The assignment then calculates and compares key financial ratios, including working capital turnover, total assets turnover, return on assets, return on equity, and debt-to-total assets, providing insights into liquidity, profitability, leverage, and activity. Further solutions address the impact of profit distribution on debt-to-equity ratios over three years, and the market value of bonds. The assignment concludes with an exploration of factors affecting beta and strategies to reduce the current ratio, along with associated risks. References to relevant academic sources are also included.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.