Corporate Finance Report: Wonderpump Investment Analysis for AGT Plc

VerifiedAdded on 2019/12/28

|15

|2408

|206

Report

AI Summary

This report provides a comprehensive analysis of AGT Plc's corporate finance, focusing on the proposed investment in Wonderpump. It begins with a cash flow forecast, detailing the company's financial performance from 2012 to 2021 and calculating the Net Present Value (NPV), Internal Rate of Return (IRR), and Average Rate of Return (ARR) of the investment. The report then critically evaluates various investment appraisal techniques, including Payback Period, ARR, IRR, and NPV, highlighting their strengths and weaknesses. A sensitivity analysis is performed to assess the impact of changes in the cost of capital on the investment's viability. Furthermore, the report discusses the merits of debt and equity financing and assesses the impact of the discount rate on AGT's capital structure. The conclusion summarizes the findings and recommends that AGT Plc proceed with the Wonderpump investment.

Corporate Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

1. Preparing a cash flow forecast of Wonderpump .....................................................................3

2. Assessing the proposed investment by using the capital budgeting tools ..............................5

3. Critically evaluate the investment appraisal techniques .........................................................6

4. ..................................................................................................................................................8

a. Performing a sensitivity analysis or calculation ......................................................................8

b. Giving comment on Gunther .................................................................................................9

5. Reassessing the Wonderpump investment.............................................................................11

6. ...............................................................................................................................................12

A. Merits of debt and equity financing......................................................................................12

b. Assessing the impact of discount rate on AGT’s structure .................................................12

CONCLUSION .............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION ..........................................................................................................................3

1. Preparing a cash flow forecast of Wonderpump .....................................................................3

2. Assessing the proposed investment by using the capital budgeting tools ..............................5

3. Critically evaluate the investment appraisal techniques .........................................................6

4. ..................................................................................................................................................8

a. Performing a sensitivity analysis or calculation ......................................................................8

b. Giving comment on Gunther .................................................................................................9

5. Reassessing the Wonderpump investment.............................................................................11

6. ...............................................................................................................................................12

A. Merits of debt and equity financing......................................................................................12

b. Assessing the impact of discount rate on AGT’s structure .................................................12

CONCLUSION .............................................................................................................................13

REFERENCES .............................................................................................................................14

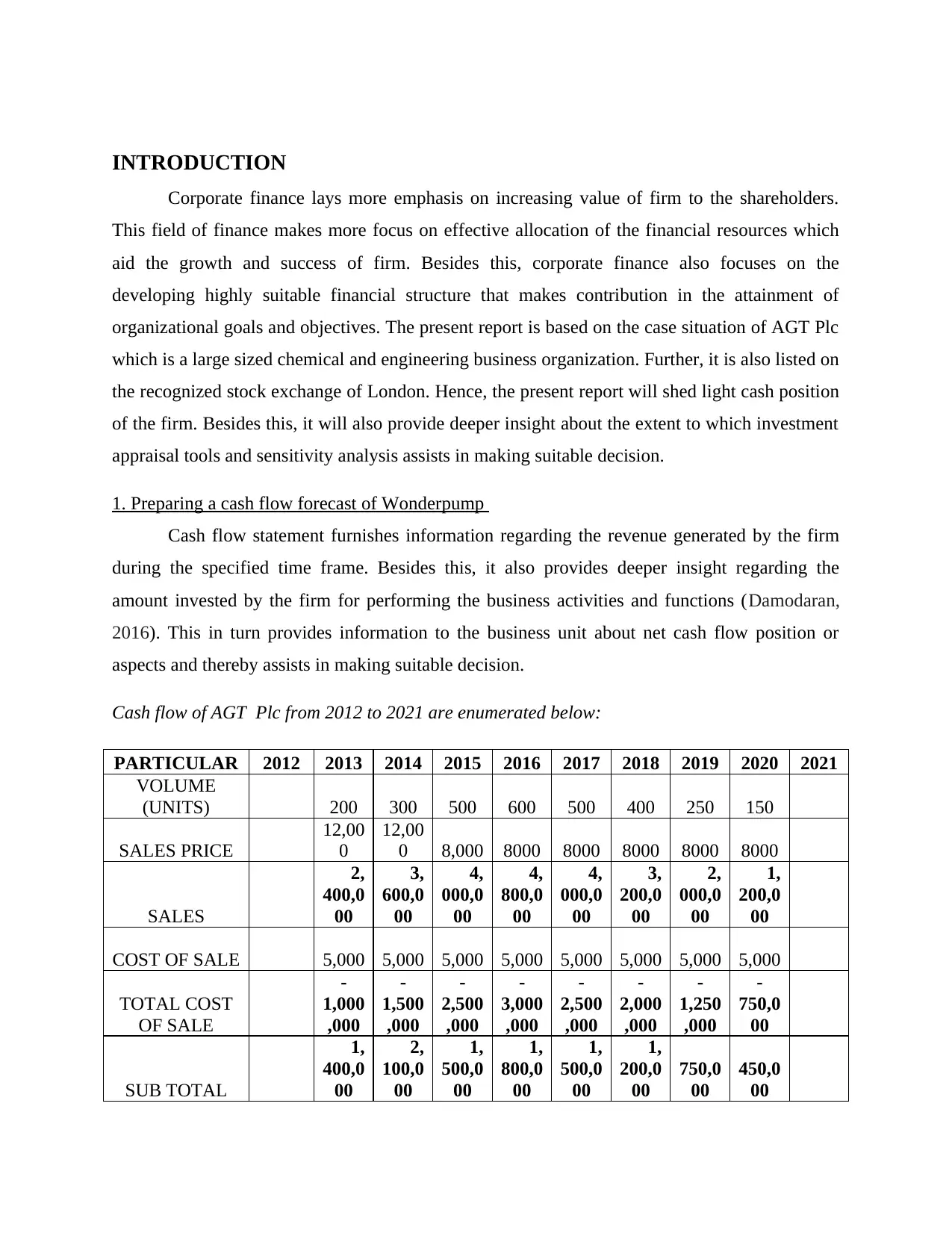

INTRODUCTION

Corporate finance lays more emphasis on increasing value of firm to the shareholders.

This field of finance makes more focus on effective allocation of the financial resources which

aid the growth and success of firm. Besides this, corporate finance also focuses on the

developing highly suitable financial structure that makes contribution in the attainment of

organizational goals and objectives. The present report is based on the case situation of AGT Plc

which is a large sized chemical and engineering business organization. Further, it is also listed on

the recognized stock exchange of London. Hence, the present report will shed light cash position

of the firm. Besides this, it will also provide deeper insight about the extent to which investment

appraisal tools and sensitivity analysis assists in making suitable decision.

1. Preparing a cash flow forecast of Wonderpump

Cash flow statement furnishes information regarding the revenue generated by the firm

during the specified time frame. Besides this, it also provides deeper insight regarding the

amount invested by the firm for performing the business activities and functions (Damodaran,

2016). This in turn provides information to the business unit about net cash flow position or

aspects and thereby assists in making suitable decision.

Cash flow of AGT Plc from 2012 to 2021 are enumerated below:

PARTICULAR 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

VOLUME

(UNITS) 200 300 500 600 500 400 250 150

SALES PRICE

12,00

0

12,00

0 8,000 8000 8000 8000 8000 8000

SALES

2,

400,0

00

3,

600,0

00

4,

000,0

00

4,

800,0

00

4,

000,0

00

3,

200,0

00

2,

000,0

00

1,

200,0

00

COST OF SALE 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000

TOTAL COST

OF SALE

-

1,000

,000

-

1,500

,000

-

2,500

,000

-

3,000

,000

-

2,500

,000

-

2,000

,000

-

1,250

,000

-

750,0

00

SUB TOTAL

1,

400,0

00

2,

100,0

00

1,

500,0

00

1,

800,0

00

1,

500,0

00

1,

200,0

00

750,0

00

450,0

00

Corporate finance lays more emphasis on increasing value of firm to the shareholders.

This field of finance makes more focus on effective allocation of the financial resources which

aid the growth and success of firm. Besides this, corporate finance also focuses on the

developing highly suitable financial structure that makes contribution in the attainment of

organizational goals and objectives. The present report is based on the case situation of AGT Plc

which is a large sized chemical and engineering business organization. Further, it is also listed on

the recognized stock exchange of London. Hence, the present report will shed light cash position

of the firm. Besides this, it will also provide deeper insight about the extent to which investment

appraisal tools and sensitivity analysis assists in making suitable decision.

1. Preparing a cash flow forecast of Wonderpump

Cash flow statement furnishes information regarding the revenue generated by the firm

during the specified time frame. Besides this, it also provides deeper insight regarding the

amount invested by the firm for performing the business activities and functions (Damodaran,

2016). This in turn provides information to the business unit about net cash flow position or

aspects and thereby assists in making suitable decision.

Cash flow of AGT Plc from 2012 to 2021 are enumerated below:

PARTICULAR 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

VOLUME

(UNITS) 200 300 500 600 500 400 250 150

SALES PRICE

12,00

0

12,00

0 8,000 8000 8000 8000 8000 8000

SALES

2,

400,0

00

3,

600,0

00

4,

000,0

00

4,

800,0

00

4,

000,0

00

3,

200,0

00

2,

000,0

00

1,

200,0

00

COST OF SALE 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000

TOTAL COST

OF SALE

-

1,000

,000

-

1,500

,000

-

2,500

,000

-

3,000

,000

-

2,500

,000

-

2,000

,000

-

1,250

,000

-

750,0

00

SUB TOTAL

1,

400,0

00

2,

100,0

00

1,

500,0

00

1,

800,0

00

1,

500,0

00

1,

200,0

00

750,0

00

450,0

00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

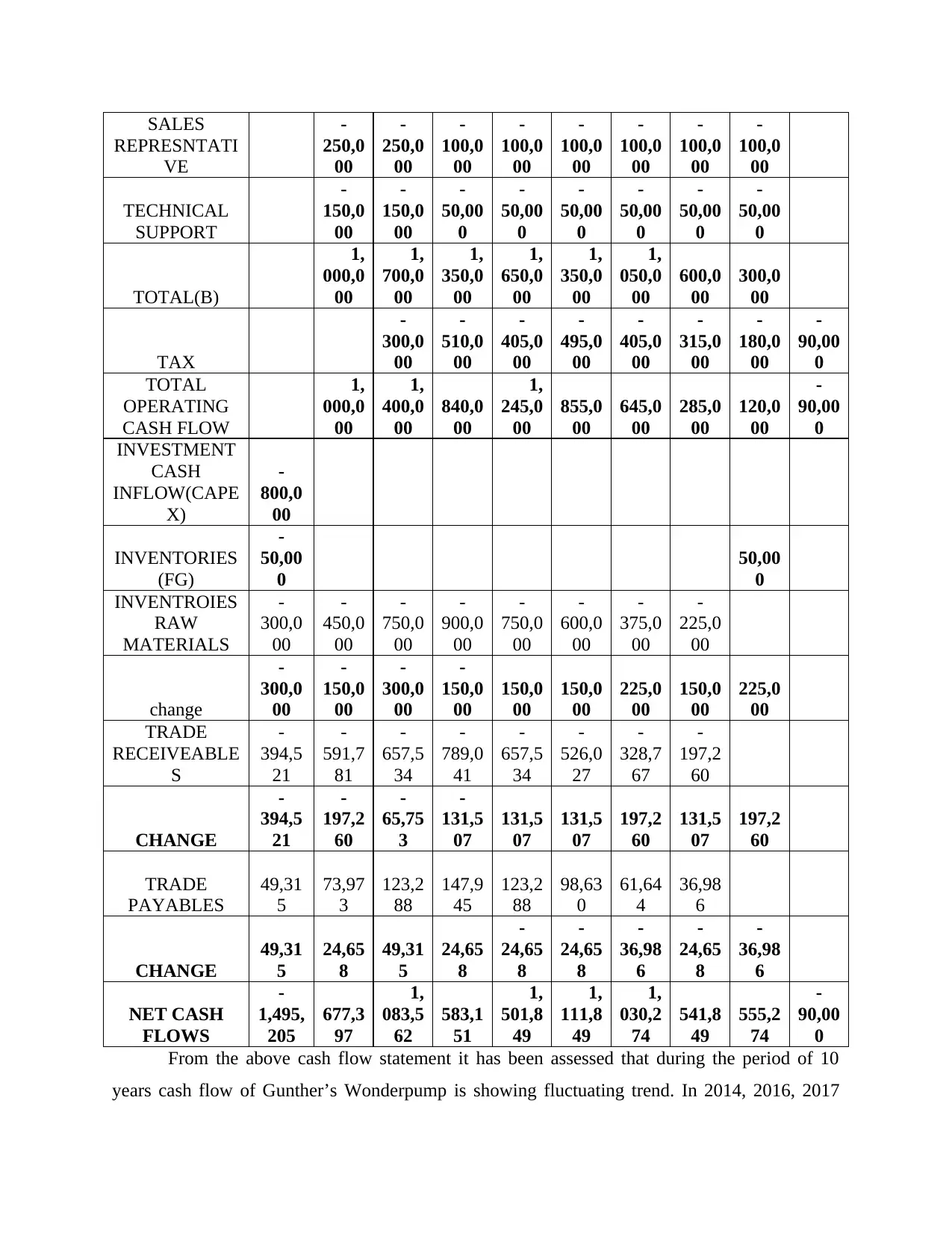

SALES

REPRESNTATI

VE

-

250,0

00

-

250,0

00

-

100,0

00

-

100,0

00

-

100,0

00

-

100,0

00

-

100,0

00

-

100,0

00

TECHNICAL

SUPPORT

-

150,0

00

-

150,0

00

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

TOTAL(B)

1,

000,0

00

1,

700,0

00

1,

350,0

00

1,

650,0

00

1,

350,0

00

1,

050,0

00

600,0

00

300,0

00

TAX

-

300,0

00

-

510,0

00

-

405,0

00

-

495,0

00

-

405,0

00

-

315,0

00

-

180,0

00

-

90,00

0

TOTAL

OPERATING

CASH FLOW

1,

000,0

00

1,

400,0

00

840,0

00

1,

245,0

00

855,0

00

645,0

00

285,0

00

120,0

00

-

90,00

0

INVESTMENT

CASH

INFLOW(CAPE

X)

-

800,0

00

INVENTORIES

(FG)

-

50,00

0

50,00

0

INVENTROIES

RAW

MATERIALS

-

300,0

00

-

450,0

00

-

750,0

00

-

900,0

00

-

750,0

00

-

600,0

00

-

375,0

00

-

225,0

00

change

-

300,0

00

-

150,0

00

-

300,0

00

-

150,0

00

150,0

00

150,0

00

225,0

00

150,0

00

225,0

00

TRADE

RECEIVEABLE

S

-

394,5

21

-

591,7

81

-

657,5

34

-

789,0

41

-

657,5

34

-

526,0

27

-

328,7

67

-

197,2

60

CHANGE

-

394,5

21

-

197,2

60

-

65,75

3

-

131,5

07

131,5

07

131,5

07

197,2

60

131,5

07

197,2

60

TRADE

PAYABLES

49,31

5

73,97

3

123,2

88

147,9

45

123,2

88

98,63

0

61,64

4

36,98

6

CHANGE

49,31

5

24,65

8

49,31

5

24,65

8

-

24,65

8

-

24,65

8

-

36,98

6

-

24,65

8

-

36,98

6

NET CASH

FLOWS

-

1,495,

205

677,3

97

1,

083,5

62

583,1

51

1,

501,8

49

1,

111,8

49

1,

030,2

74

541,8

49

555,2

74

-

90,00

0

From the above cash flow statement it has been assessed that during the period of 10

years cash flow of Gunther’s Wonderpump is showing fluctuating trend. In 2014, 2016, 2017

REPRESNTATI

VE

-

250,0

00

-

250,0

00

-

100,0

00

-

100,0

00

-

100,0

00

-

100,0

00

-

100,0

00

-

100,0

00

TECHNICAL

SUPPORT

-

150,0

00

-

150,0

00

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

TOTAL(B)

1,

000,0

00

1,

700,0

00

1,

350,0

00

1,

650,0

00

1,

350,0

00

1,

050,0

00

600,0

00

300,0

00

TAX

-

300,0

00

-

510,0

00

-

405,0

00

-

495,0

00

-

405,0

00

-

315,0

00

-

180,0

00

-

90,00

0

TOTAL

OPERATING

CASH FLOW

1,

000,0

00

1,

400,0

00

840,0

00

1,

245,0

00

855,0

00

645,0

00

285,0

00

120,0

00

-

90,00

0

INVESTMENT

CASH

INFLOW(CAPE

X)

-

800,0

00

INVENTORIES

(FG)

-

50,00

0

50,00

0

INVENTROIES

RAW

MATERIALS

-

300,0

00

-

450,0

00

-

750,0

00

-

900,0

00

-

750,0

00

-

600,0

00

-

375,0

00

-

225,0

00

change

-

300,0

00

-

150,0

00

-

300,0

00

-

150,0

00

150,0

00

150,0

00

225,0

00

150,0

00

225,0

00

TRADE

RECEIVEABLE

S

-

394,5

21

-

591,7

81

-

657,5

34

-

789,0

41

-

657,5

34

-

526,0

27

-

328,7

67

-

197,2

60

CHANGE

-

394,5

21

-

197,2

60

-

65,75

3

-

131,5

07

131,5

07

131,5

07

197,2

60

131,5

07

197,2

60

TRADE

PAYABLES

49,31

5

73,97

3

123,2

88

147,9

45

123,2

88

98,63

0

61,64

4

36,98

6

CHANGE

49,31

5

24,65

8

49,31

5

24,65

8

-

24,65

8

-

24,65

8

-

36,98

6

-

24,65

8

-

36,98

6

NET CASH

FLOWS

-

1,495,

205

677,3

97

1,

083,5

62

583,1

51

1,

501,8

49

1,

111,8

49

1,

030,2

74

541,8

49

555,2

74

-

90,00

0

From the above cash flow statement it has been assessed that during the period of 10

years cash flow of Gunther’s Wonderpump is showing fluctuating trend. In 2014, 2016, 2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

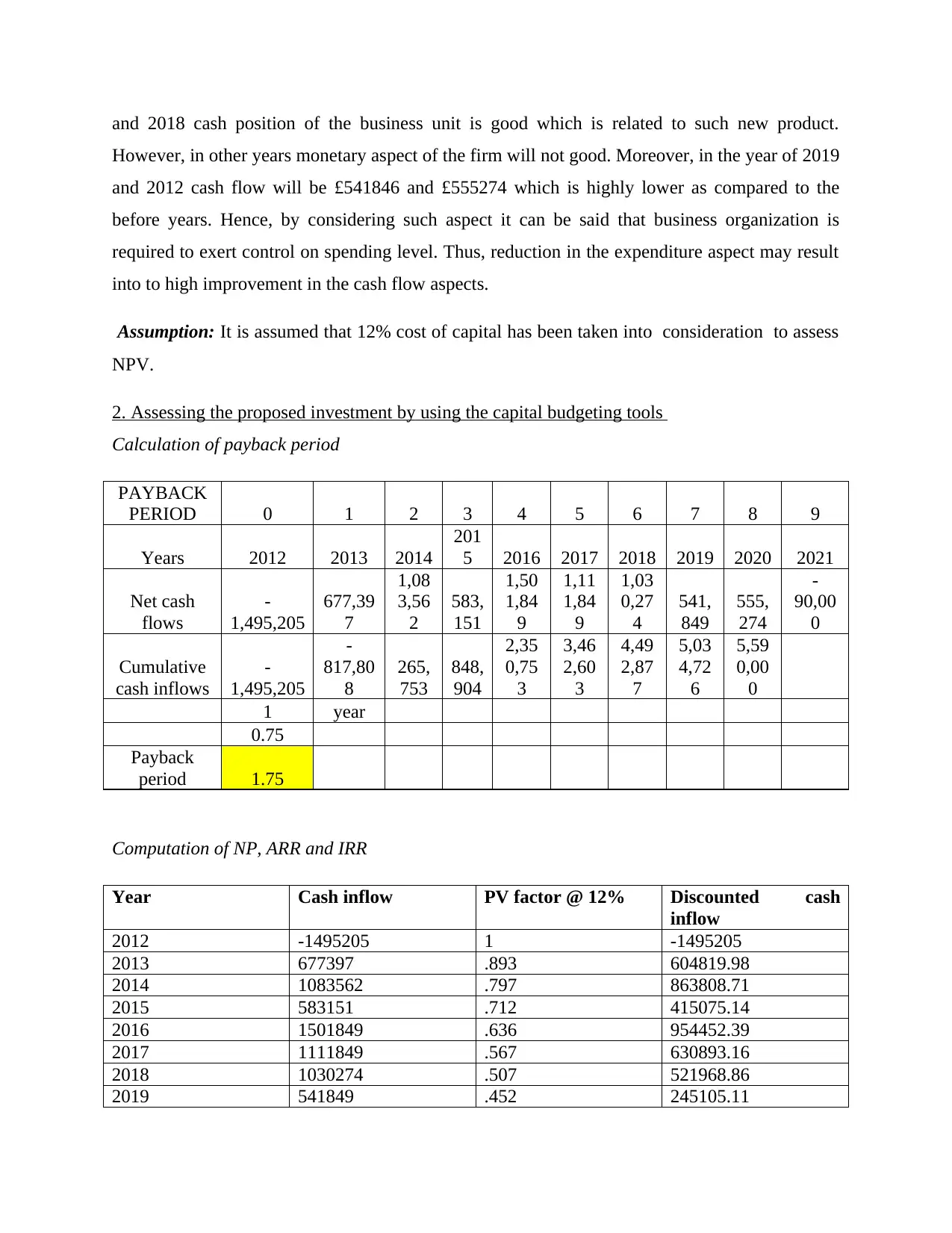

and 2018 cash position of the business unit is good which is related to such new product.

However, in other years monetary aspect of the firm will not good. Moreover, in the year of 2019

and 2012 cash flow will be £541846 and £555274 which is highly lower as compared to the

before years. Hence, by considering such aspect it can be said that business organization is

required to exert control on spending level. Thus, reduction in the expenditure aspect may result

into to high improvement in the cash flow aspects.

Assumption: It is assumed that 12% cost of capital has been taken into consideration to assess

NPV.

2. Assessing the proposed investment by using the capital budgeting tools

Calculation of payback period

PAYBACK

PERIOD 0 1 2 3 4 5 6 7 8 9

Years 2012 2013 2014

201

5 2016 2017 2018 2019 2020 2021

Net cash

flows

-

1,495,205

677,39

7

1,08

3,56

2

583,

151

1,50

1,84

9

1,11

1,84

9

1,03

0,27

4

541,

849

555,

274

-

90,00

0

Cumulative

cash inflows

-

1,495,205

-

817,80

8

265,

753

848,

904

2,35

0,75

3

3,46

2,60

3

4,49

2,87

7

5,03

4,72

6

5,59

0,00

0

1 year

0.75

Payback

period 1.75

Computation of NP, ARR and IRR

Year Cash inflow PV factor @ 12% Discounted cash

inflow

2012 -1495205 1 -1495205

2013 677397 .893 604819.98

2014 1083562 .797 863808.71

2015 583151 .712 415075.14

2016 1501849 .636 954452.39

2017 1111849 .567 630893.16

2018 1030274 .507 521968.86

2019 541849 .452 245105.11

However, in other years monetary aspect of the firm will not good. Moreover, in the year of 2019

and 2012 cash flow will be £541846 and £555274 which is highly lower as compared to the

before years. Hence, by considering such aspect it can be said that business organization is

required to exert control on spending level. Thus, reduction in the expenditure aspect may result

into to high improvement in the cash flow aspects.

Assumption: It is assumed that 12% cost of capital has been taken into consideration to assess

NPV.

2. Assessing the proposed investment by using the capital budgeting tools

Calculation of payback period

PAYBACK

PERIOD 0 1 2 3 4 5 6 7 8 9

Years 2012 2013 2014

201

5 2016 2017 2018 2019 2020 2021

Net cash

flows

-

1,495,205

677,39

7

1,08

3,56

2

583,

151

1,50

1,84

9

1,11

1,84

9

1,03

0,27

4

541,

849

555,

274

-

90,00

0

Cumulative

cash inflows

-

1,495,205

-

817,80

8

265,

753

848,

904

2,35

0,75

3

3,46

2,60

3

4,49

2,87

7

5,03

4,72

6

5,59

0,00

0

1 year

0.75

Payback

period 1.75

Computation of NP, ARR and IRR

Year Cash inflow PV factor @ 12% Discounted cash

inflow

2012 -1495205 1 -1495205

2013 677397 .893 604819.98

2014 1083562 .797 863808.71

2015 583151 .712 415075.14

2016 1501849 .636 954452.39

2017 1111849 .567 630893.16

2018 1030274 .507 521968.86

2019 541849 .452 245105.11

2020 555274 .404 224265.84

2021 -90000 .361 -32454.90

Total discounted cash

inflow

4427933.29

Less: initial

investment

1495205

NPV (Total

discounted cash

inflow – initial

investment)

2932728

Internal rate of

return

57%

Average profit 1495205

Average rate of

return

43%

From the investment appraisal analysis, it has been identified that AGT Plc will take 1

year and 8 months to recover the initial amount. Besides this, ARR and IRR of Gunther is 43%

and 57% which is higher than the average industry level. Further, NPV of the proposed

investment is positive and greater than the initial investment such as £2932728. Hence, by

keeping all such factors in mind it can be said that AGT plc should invest money in such project

which will prove to be more beneficial for it (Shen, Firth and Poon, 2016).

3. Critically evaluate the investment appraisal techniques

Payback period

This method provides information about the time frame within which business

organization would become able to recoup the initial investment. In this way, by calculating the

payback period company can assess the period after which it would become able to generate

enough amount of profit margin (Wilson, 2016). However, on the critical note, it can be said that

it does not provide managers with highly appropriate information for decision making. The

rationale behind this, it completely ignores the time value of money concept which have high

level of importance in the strategic business environment. Along with this, it does not provide

information about the cash flow which will be generated by the firm after the recovery of initial

investment. Hence, it is another main reasons which create difficulty in developing highly

competent plan for the upcoming time period.

Average rate of return (ARR)

2021 -90000 .361 -32454.90

Total discounted cash

inflow

4427933.29

Less: initial

investment

1495205

NPV (Total

discounted cash

inflow – initial

investment)

2932728

Internal rate of

return

57%

Average profit 1495205

Average rate of

return

43%

From the investment appraisal analysis, it has been identified that AGT Plc will take 1

year and 8 months to recover the initial amount. Besides this, ARR and IRR of Gunther is 43%

and 57% which is higher than the average industry level. Further, NPV of the proposed

investment is positive and greater than the initial investment such as £2932728. Hence, by

keeping all such factors in mind it can be said that AGT plc should invest money in such project

which will prove to be more beneficial for it (Shen, Firth and Poon, 2016).

3. Critically evaluate the investment appraisal techniques

Payback period

This method provides information about the time frame within which business

organization would become able to recoup the initial investment. In this way, by calculating the

payback period company can assess the period after which it would become able to generate

enough amount of profit margin (Wilson, 2016). However, on the critical note, it can be said that

it does not provide managers with highly appropriate information for decision making. The

rationale behind this, it completely ignores the time value of money concept which have high

level of importance in the strategic business environment. Along with this, it does not provide

information about the cash flow which will be generated by the firm after the recovery of initial

investment. Hence, it is another main reasons which create difficulty in developing highly

competent plan for the upcoming time period.

Average rate of return (ARR)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ARR renders information about the average profit which business entity will generate

from Gunther Wonder pipes product. On the other side, it can be said that outcome of evaluation

is highly based on the profit level rather than cash flows. This is one of the main drawbacks of

such method because cash flows can be forecasted easily in comparison to the profit aspect

(Jacob and et.al., 2016). Further, it also avoids time value of money concept because discounting

factors or rates can be applied on the cash flows not on profit.

Internal rate of return (IRR)

Such discounting investment appraisal tool renders information about the return which

will be earned by AGT Plc from the proposed investment in terms of percentage. However, in

this, analyst has to take two discounting factors which are highly difficult and time consuming

(Greene, 2015). This in turn closely influences the significance such method and its outcome.

Such project does not provide assistance in making comparison between the projects which are

highly exclusive. Besides this, for the calculation of IRR business entity has to select two rates

for determining the suitable output. In this regard, if manager fails to select suitable rates then it

may result into unrealistic framework for decision making.

Net present value (NPV)

This method of investment appraisal helps in making analysis of the extent to which

proposed project will prove to be profitable for the firm in monetary terms. Besides this,

according to such method viability of Gunther is assessed by taking into consideration the 12%

cost of capital. Hence, time value of money concept provides assistance in making suitable

decision in the dynamic business arena (Dang, Kim and Shin, 2015). However, it is to be

critically evaluated that if owner of AGT Plc failed to assess suitable cost of capital then it may

result into unrealistic evaluation for the judgment.

Hence, by keeping all such aspects in mind it can be said that discounting methods assist

in making highly appropriate and profitable decisions.

from Gunther Wonder pipes product. On the other side, it can be said that outcome of evaluation

is highly based on the profit level rather than cash flows. This is one of the main drawbacks of

such method because cash flows can be forecasted easily in comparison to the profit aspect

(Jacob and et.al., 2016). Further, it also avoids time value of money concept because discounting

factors or rates can be applied on the cash flows not on profit.

Internal rate of return (IRR)

Such discounting investment appraisal tool renders information about the return which

will be earned by AGT Plc from the proposed investment in terms of percentage. However, in

this, analyst has to take two discounting factors which are highly difficult and time consuming

(Greene, 2015). This in turn closely influences the significance such method and its outcome.

Such project does not provide assistance in making comparison between the projects which are

highly exclusive. Besides this, for the calculation of IRR business entity has to select two rates

for determining the suitable output. In this regard, if manager fails to select suitable rates then it

may result into unrealistic framework for decision making.

Net present value (NPV)

This method of investment appraisal helps in making analysis of the extent to which

proposed project will prove to be profitable for the firm in monetary terms. Besides this,

according to such method viability of Gunther is assessed by taking into consideration the 12%

cost of capital. Hence, time value of money concept provides assistance in making suitable

decision in the dynamic business arena (Dang, Kim and Shin, 2015). However, it is to be

critically evaluated that if owner of AGT Plc failed to assess suitable cost of capital then it may

result into unrealistic evaluation for the judgment.

Hence, by keeping all such aspects in mind it can be said that discounting methods assist

in making highly appropriate and profitable decisions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

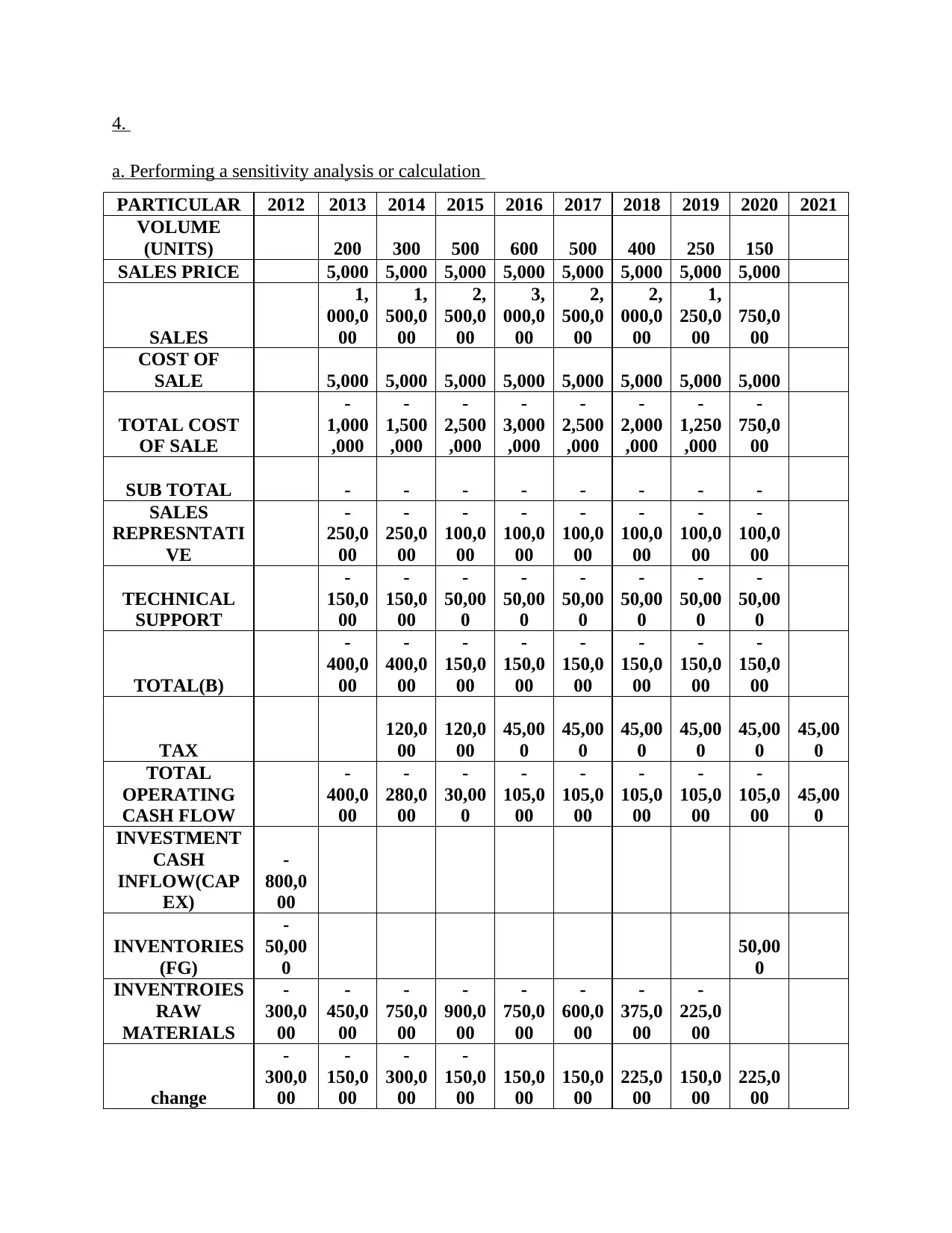

4.

a. Performing a sensitivity analysis or calculation

PARTICULAR 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

VOLUME

(UNITS) 200 300 500 600 500 400 250 150

SALES PRICE 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000

SALES

1,

000,0

00

1,

500,0

00

2,

500,0

00

3,

000,0

00

2,

500,0

00

2,

000,0

00

1,

250,0

00

750,0

00

COST OF

SALE 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000

TOTAL COST

OF SALE

-

1,000

,000

-

1,500

,000

-

2,500

,000

-

3,000

,000

-

2,500

,000

-

2,000

,000

-

1,250

,000

-

750,0

00

SUB TOTAL - - - - - - - -

SALES

REPRESNTATI

VE

-

250,0

00

-

250,0

00

-

100,0

00

-

100,0

00

-

100,0

00

-

100,0

00

-

100,0

00

-

100,0

00

TECHNICAL

SUPPORT

-

150,0

00

-

150,0

00

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

TOTAL(B)

-

400,0

00

-

400,0

00

-

150,0

00

-

150,0

00

-

150,0

00

-

150,0

00

-

150,0

00

-

150,0

00

TAX

120,0

00

120,0

00

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

TOTAL

OPERATING

CASH FLOW

-

400,0

00

-

280,0

00

-

30,00

0

-

105,0

00

-

105,0

00

-

105,0

00

-

105,0

00

-

105,0

00

45,00

0

INVESTMENT

CASH

INFLOW(CAP

EX)

-

800,0

00

INVENTORIES

(FG)

-

50,00

0

50,00

0

INVENTROIES

RAW

MATERIALS

-

300,0

00

-

450,0

00

-

750,0

00

-

900,0

00

-

750,0

00

-

600,0

00

-

375,0

00

-

225,0

00

change

-

300,0

00

-

150,0

00

-

300,0

00

-

150,0

00

150,0

00

150,0

00

225,0

00

150,0

00

225,0

00

a. Performing a sensitivity analysis or calculation

PARTICULAR 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

VOLUME

(UNITS) 200 300 500 600 500 400 250 150

SALES PRICE 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000

SALES

1,

000,0

00

1,

500,0

00

2,

500,0

00

3,

000,0

00

2,

500,0

00

2,

000,0

00

1,

250,0

00

750,0

00

COST OF

SALE 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000

TOTAL COST

OF SALE

-

1,000

,000

-

1,500

,000

-

2,500

,000

-

3,000

,000

-

2,500

,000

-

2,000

,000

-

1,250

,000

-

750,0

00

SUB TOTAL - - - - - - - -

SALES

REPRESNTATI

VE

-

250,0

00

-

250,0

00

-

100,0

00

-

100,0

00

-

100,0

00

-

100,0

00

-

100,0

00

-

100,0

00

TECHNICAL

SUPPORT

-

150,0

00

-

150,0

00

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

TOTAL(B)

-

400,0

00

-

400,0

00

-

150,0

00

-

150,0

00

-

150,0

00

-

150,0

00

-

150,0

00

-

150,0

00

TAX

120,0

00

120,0

00

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

45,00

0

TOTAL

OPERATING

CASH FLOW

-

400,0

00

-

280,0

00

-

30,00

0

-

105,0

00

-

105,0

00

-

105,0

00

-

105,0

00

-

105,0

00

45,00

0

INVESTMENT

CASH

INFLOW(CAP

EX)

-

800,0

00

INVENTORIES

(FG)

-

50,00

0

50,00

0

INVENTROIES

RAW

MATERIALS

-

300,0

00

-

450,0

00

-

750,0

00

-

900,0

00

-

750,0

00

-

600,0

00

-

375,0

00

-

225,0

00

change

-

300,0

00

-

150,0

00

-

300,0

00

-

150,0

00

150,0

00

150,0

00

225,0

00

150,0

00

225,0

00

TRADE

RECEIVEABL

ES

-

164,3

84

-

246,5

75

-

410,9

59

-

493,1

51

-

410,9

59

-

328,7

67

-

205,4

79

-

123,2

88

CHANGE -

164,3

84

-

82,19

2

-

164,3

84

-

82,19

2

82,19

2

82,19

2

123,2

88

82,19

2

123,2

88

TRADE

PAYABLES

49,31

5

73,97

3

123,2

88

147,9

45

123,2

88

98,63

0

61,64

4

36,98

6

CHANGE

49,31

5

24,65

8

49,31

5

24,65

8

-

24,65

8

-

24,65

8

-

36,98

6

-

24,65

8

-

36,98

6

NET CASH

FLOWS

-

1,265,

068

-

607,5

34

-

695,0

68

-

237,5

34

102,5

34

102,5

34

206,3

01

102,5

34

256,3

01

45,00

0

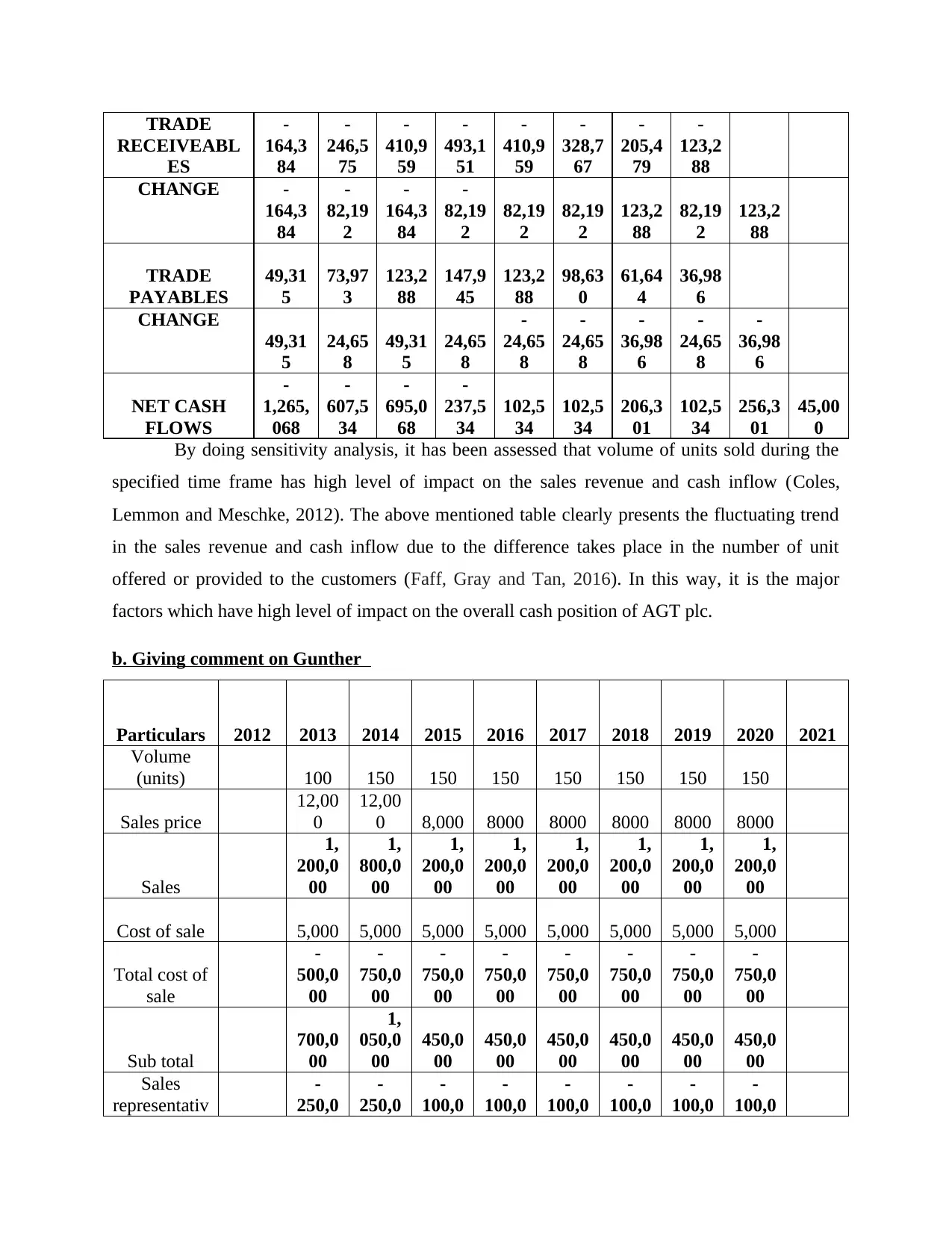

By doing sensitivity analysis, it has been assessed that volume of units sold during the

specified time frame has high level of impact on the sales revenue and cash inflow (Coles,

Lemmon and Meschke, 2012). The above mentioned table clearly presents the fluctuating trend

in the sales revenue and cash inflow due to the difference takes place in the number of unit

offered or provided to the customers (Faff, Gray and Tan, 2016). In this way, it is the major

factors which have high level of impact on the overall cash position of AGT plc.

b. Giving comment on Gunther

Particulars 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Volume

(units) 100 150 150 150 150 150 150 150

Sales price

12,00

0

12,00

0 8,000 8000 8000 8000 8000 8000

Sales

1,

200,0

00

1,

800,0

00

1,

200,0

00

1,

200,0

00

1,

200,0

00

1,

200,0

00

1,

200,0

00

1,

200,0

00

Cost of sale 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000

Total cost of

sale

-

500,0

00

-

750,0

00

-

750,0

00

-

750,0

00

-

750,0

00

-

750,0

00

-

750,0

00

-

750,0

00

Sub total

700,0

00

1,

050,0

00

450,0

00

450,0

00

450,0

00

450,0

00

450,0

00

450,0

00

Sales

representativ

-

250,0

-

250,0

-

100,0

-

100,0

-

100,0

-

100,0

-

100,0

-

100,0

RECEIVEABL

ES

-

164,3

84

-

246,5

75

-

410,9

59

-

493,1

51

-

410,9

59

-

328,7

67

-

205,4

79

-

123,2

88

CHANGE -

164,3

84

-

82,19

2

-

164,3

84

-

82,19

2

82,19

2

82,19

2

123,2

88

82,19

2

123,2

88

TRADE

PAYABLES

49,31

5

73,97

3

123,2

88

147,9

45

123,2

88

98,63

0

61,64

4

36,98

6

CHANGE

49,31

5

24,65

8

49,31

5

24,65

8

-

24,65

8

-

24,65

8

-

36,98

6

-

24,65

8

-

36,98

6

NET CASH

FLOWS

-

1,265,

068

-

607,5

34

-

695,0

68

-

237,5

34

102,5

34

102,5

34

206,3

01

102,5

34

256,3

01

45,00

0

By doing sensitivity analysis, it has been assessed that volume of units sold during the

specified time frame has high level of impact on the sales revenue and cash inflow (Coles,

Lemmon and Meschke, 2012). The above mentioned table clearly presents the fluctuating trend

in the sales revenue and cash inflow due to the difference takes place in the number of unit

offered or provided to the customers (Faff, Gray and Tan, 2016). In this way, it is the major

factors which have high level of impact on the overall cash position of AGT plc.

b. Giving comment on Gunther

Particulars 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Volume

(units) 100 150 150 150 150 150 150 150

Sales price

12,00

0

12,00

0 8,000 8000 8000 8000 8000 8000

Sales

1,

200,0

00

1,

800,0

00

1,

200,0

00

1,

200,0

00

1,

200,0

00

1,

200,0

00

1,

200,0

00

1,

200,0

00

Cost of sale 5,000 5,000 5,000 5,000 5,000 5,000 5,000 5,000

Total cost of

sale

-

500,0

00

-

750,0

00

-

750,0

00

-

750,0

00

-

750,0

00

-

750,0

00

-

750,0

00

-

750,0

00

Sub total

700,0

00

1,

050,0

00

450,0

00

450,0

00

450,0

00

450,0

00

450,0

00

450,0

00

Sales

representativ

-

250,0

-

250,0

-

100,0

-

100,0

-

100,0

-

100,0

-

100,0

-

100,0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

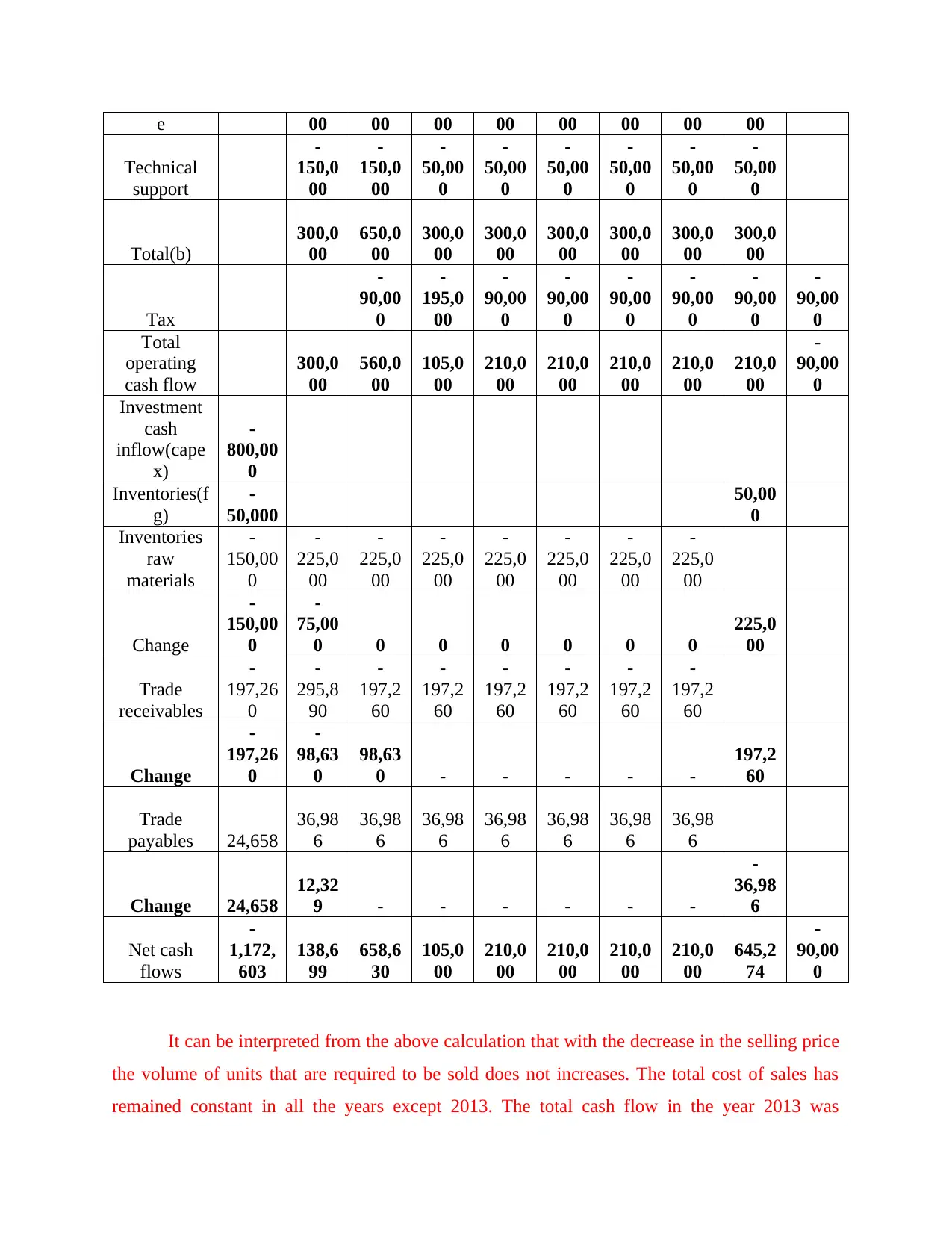

e 00 00 00 00 00 00 00 00

Technical

support

-

150,0

00

-

150,0

00

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

Total(b)

300,0

00

650,0

00

300,0

00

300,0

00

300,0

00

300,0

00

300,0

00

300,0

00

Tax

-

90,00

0

-

195,0

00

-

90,00

0

-

90,00

0

-

90,00

0

-

90,00

0

-

90,00

0

-

90,00

0

Total

operating

cash flow

300,0

00

560,0

00

105,0

00

210,0

00

210,0

00

210,0

00

210,0

00

210,0

00

-

90,00

0

Investment

cash

inflow(cape

x)

-

800,00

0

Inventories(f

g)

-

50,000

50,00

0

Inventories

raw

materials

-

150,00

0

-

225,0

00

-

225,0

00

-

225,0

00

-

225,0

00

-

225,0

00

-

225,0

00

-

225,0

00

Change

-

150,00

0

-

75,00

0 0 0 0 0 0 0

225,0

00

Trade

receivables

-

197,26

0

-

295,8

90

-

197,2

60

-

197,2

60

-

197,2

60

-

197,2

60

-

197,2

60

-

197,2

60

Change

-

197,26

0

-

98,63

0

98,63

0 - - - - -

197,2

60

Trade

payables 24,658

36,98

6

36,98

6

36,98

6

36,98

6

36,98

6

36,98

6

36,98

6

Change 24,658

12,32

9 - - - - - -

-

36,98

6

Net cash

flows

-

1,172,

603

138,6

99

658,6

30

105,0

00

210,0

00

210,0

00

210,0

00

210,0

00

645,2

74

-

90,00

0

It can be interpreted from the above calculation that with the decrease in the selling price

the volume of units that are required to be sold does not increases. The total cost of sales has

remained constant in all the years except 2013. The total cash flow in the year 2013 was

Technical

support

-

150,0

00

-

150,0

00

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

-

50,00

0

Total(b)

300,0

00

650,0

00

300,0

00

300,0

00

300,0

00

300,0

00

300,0

00

300,0

00

Tax

-

90,00

0

-

195,0

00

-

90,00

0

-

90,00

0

-

90,00

0

-

90,00

0

-

90,00

0

-

90,00

0

Total

operating

cash flow

300,0

00

560,0

00

105,0

00

210,0

00

210,0

00

210,0

00

210,0

00

210,0

00

-

90,00

0

Investment

cash

inflow(cape

x)

-

800,00

0

Inventories(f

g)

-

50,000

50,00

0

Inventories

raw

materials

-

150,00

0

-

225,0

00

-

225,0

00

-

225,0

00

-

225,0

00

-

225,0

00

-

225,0

00

-

225,0

00

Change

-

150,00

0

-

75,00

0 0 0 0 0 0 0

225,0

00

Trade

receivables

-

197,26

0

-

295,8

90

-

197,2

60

-

197,2

60

-

197,2

60

-

197,2

60

-

197,2

60

-

197,2

60

Change

-

197,26

0

-

98,63

0

98,63

0 - - - - -

197,2

60

Trade

payables 24,658

36,98

6

36,98

6

36,98

6

36,98

6

36,98

6

36,98

6

36,98

6

Change 24,658

12,32

9 - - - - - -

-

36,98

6

Net cash

flows

-

1,172,

603

138,6

99

658,6

30

105,0

00

210,0

00

210,0

00

210,0

00

210,0

00

645,2

74

-

90,00

0

It can be interpreted from the above calculation that with the decrease in the selling price

the volume of units that are required to be sold does not increases. The total cost of sales has

remained constant in all the years except 2013. The total cash flow in the year 2013 was

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1172603. This has decreased in the following year that is 2013. Along with this in the highest net

cash flow is in the year 2014. However this has increasing in the years to come but not to a

greater extent. It has been assessed that trade receivables is higher in comparison with trade

payables. This presents that liability of the business is less as compared with the asset. This

implies that financial position of the company is sound which would enable it in attaining its

targets in an effective manner. The technical support of the company in the initial years was

maximum. This has declined to a significant level. This has been gained that it has remained

constant from the year 2015. The cost of sales representative has decline to a greater extent. This

has greater impact on the overall decline in the cost of the firm.

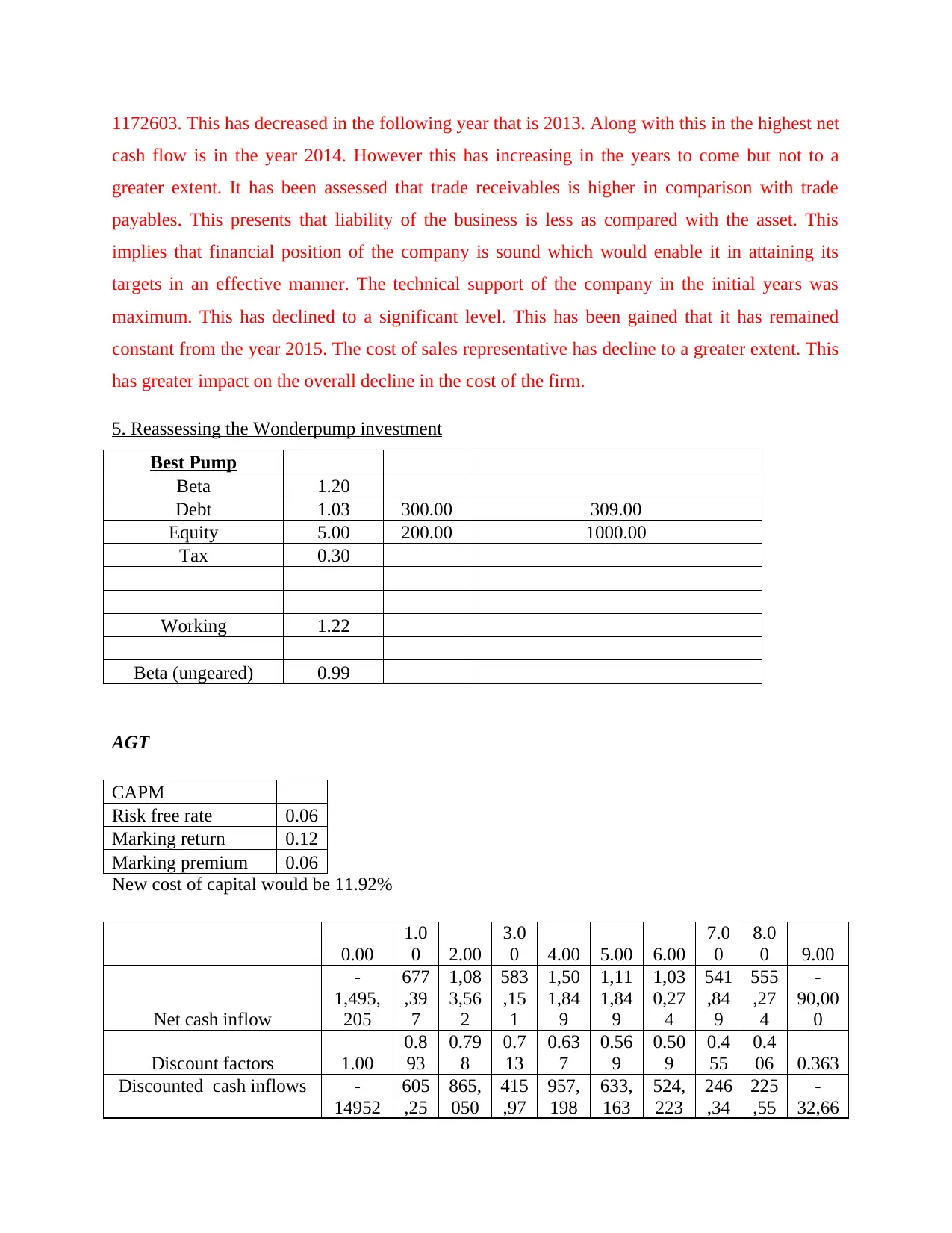

5. Reassessing the Wonderpump investment

Best Pump

Beta 1.20

Debt 1.03 300.00 309.00

Equity 5.00 200.00 1000.00

Tax 0.30

Working 1.22

Beta (ungeared) 0.99

AGT

CAPM

Risk free rate 0.06

Marking return 0.12

Marking premium 0.06

New cost of capital would be 11.92%

0.00

1.0

0 2.00

3.0

0 4.00 5.00 6.00

7.0

0

8.0

0 9.00

Net cash inflow

-

1,495,

205

677

,39

7

1,08

3,56

2

583

,15

1

1,50

1,84

9

1,11

1,84

9

1,03

0,27

4

541

,84

9

555

,27

4

-

90,00

0

Discount factors 1.00

0.8

93

0.79

8

0.7

13

0.63

7

0.56

9

0.50

9

0.4

55

0.4

06 0.363

Discounted cash inflows -

14952

605

,25

865,

050

415

,97

957,

198

633,

163

524,

223

246

,34

225

,55

-

32,66

cash flow is in the year 2014. However this has increasing in the years to come but not to a

greater extent. It has been assessed that trade receivables is higher in comparison with trade

payables. This presents that liability of the business is less as compared with the asset. This

implies that financial position of the company is sound which would enable it in attaining its

targets in an effective manner. The technical support of the company in the initial years was

maximum. This has declined to a significant level. This has been gained that it has remained

constant from the year 2015. The cost of sales representative has decline to a greater extent. This

has greater impact on the overall decline in the cost of the firm.

5. Reassessing the Wonderpump investment

Best Pump

Beta 1.20

Debt 1.03 300.00 309.00

Equity 5.00 200.00 1000.00

Tax 0.30

Working 1.22

Beta (ungeared) 0.99

AGT

CAPM

Risk free rate 0.06

Marking return 0.12

Marking premium 0.06

New cost of capital would be 11.92%

0.00

1.0

0 2.00

3.0

0 4.00 5.00 6.00

7.0

0

8.0

0 9.00

Net cash inflow

-

1,495,

205

677

,39

7

1,08

3,56

2

583

,15

1

1,50

1,84

9

1,11

1,84

9

1,03

0,27

4

541

,84

9

555

,27

4

-

90,00

0

Discount factors 1.00

0.8

93

0.79

8

0.7

13

0.63

7

0.56

9

0.50

9

0.4

55

0.4

06 0.363

Discounted cash inflows -

14952

605

,25

865,

050

415

,97

957,

198

633,

163

524,

223

246

,34

225

,55

-

32,66

05.48 4 0 0 8 5

NPV (Total discounted

cash inflow – initial

investment)

2,932,

728

Assumptions: It has been assessed that new beta is 11.2% which have little impact on NPV.

From the above analysis it has been assessed that there is no significant difference takes

place in the NPV when cost of capital reduced from 12% to 11.2%. Hence, by considering such

aspect it can be said business organization will earn positive return of £2932728 over the initial

investment. On the basis of such aspect AGT Plc will achieve success by making selection of the

investment proposal in relation to Wonder pipes (Brealey and et.al., 2012). Further, such method

offers solution by considering the time value of money concept. In this way, such proposed

investment will offer high level of benefits to the company in terms of financials.

6.

A. Merits of debt and equity financing

Both debt and equity financing is highly required for developing highly effective as well

as balanced financial structure. There are several advantages which are associated with the debt

and equity financing are as follows:

Benefits of debt financing

In this, amount which is paid by the firm in terms of interest is tax deductible. In this,

source of finance helps in getting benefits in terms of tax brackets (Coles, Lemmon and

Meschke, 2012).

Further, debt financing reduces the control of debt holders in the decision making aspect

because it does not offer ownership to them (Advantages and disadvantages of debt

financing, 2016).

Merits of equity financing

One of the main benefits which are offered by equity financing is that AGT plc is not

obliged to repay such amount after the specified time frame (Huang and Kisgen, 2013).

NPV (Total discounted

cash inflow – initial

investment)

2,932,

728

Assumptions: It has been assessed that new beta is 11.2% which have little impact on NPV.

From the above analysis it has been assessed that there is no significant difference takes

place in the NPV when cost of capital reduced from 12% to 11.2%. Hence, by considering such

aspect it can be said business organization will earn positive return of £2932728 over the initial

investment. On the basis of such aspect AGT Plc will achieve success by making selection of the

investment proposal in relation to Wonder pipes (Brealey and et.al., 2012). Further, such method

offers solution by considering the time value of money concept. In this way, such proposed

investment will offer high level of benefits to the company in terms of financials.

6.

A. Merits of debt and equity financing

Both debt and equity financing is highly required for developing highly effective as well

as balanced financial structure. There are several advantages which are associated with the debt

and equity financing are as follows:

Benefits of debt financing

In this, amount which is paid by the firm in terms of interest is tax deductible. In this,

source of finance helps in getting benefits in terms of tax brackets (Coles, Lemmon and

Meschke, 2012).

Further, debt financing reduces the control of debt holders in the decision making aspect

because it does not offer ownership to them (Advantages and disadvantages of debt

financing, 2016).

Merits of equity financing

One of the main benefits which are offered by equity financing is that AGT plc is not

obliged to repay such amount after the specified time frame (Huang and Kisgen, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.