Corporate Financial Management: Project Valuation and Merger Analysis

VerifiedAdded on 2020/05/28

|9

|2087

|92

Report

AI Summary

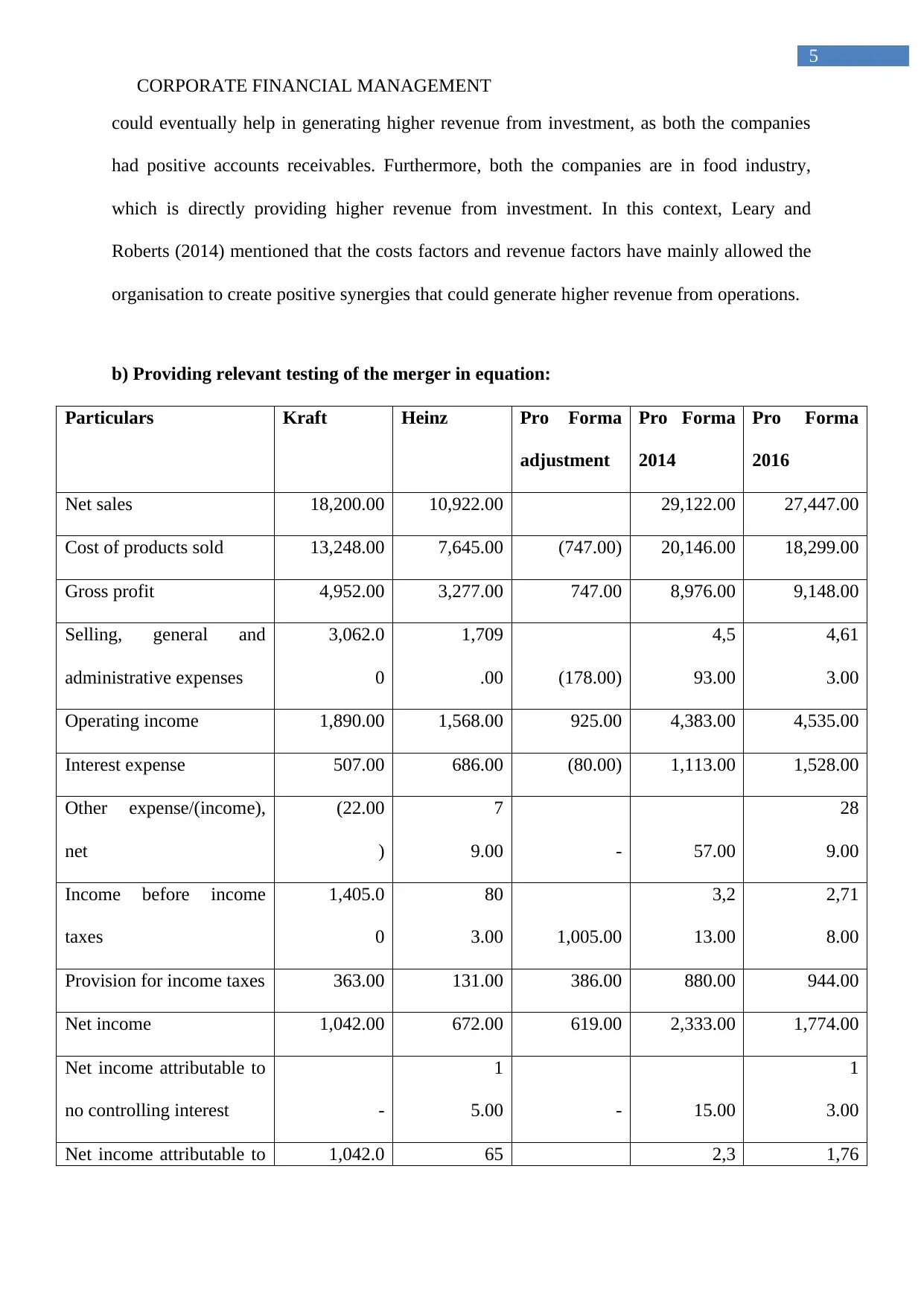

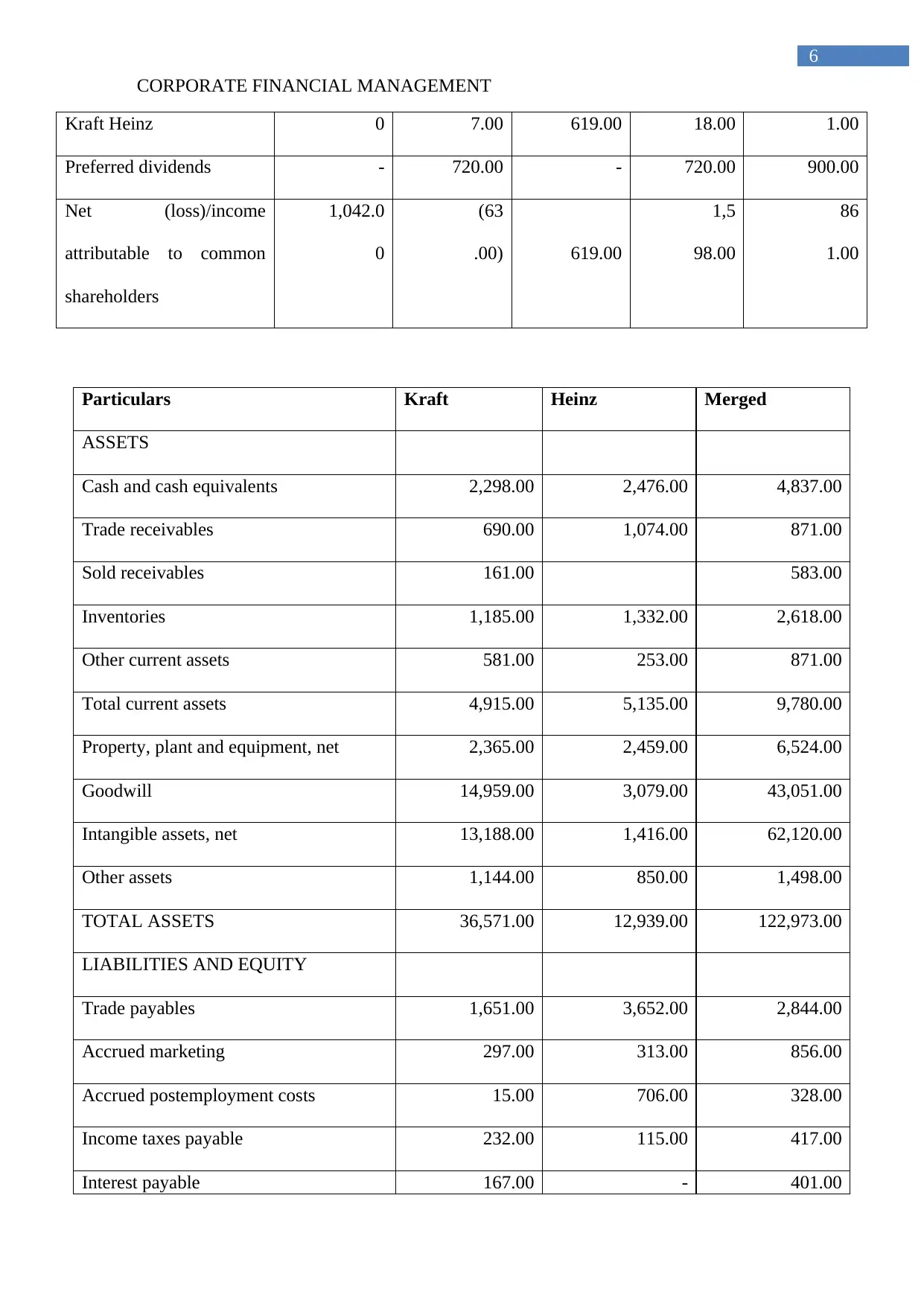

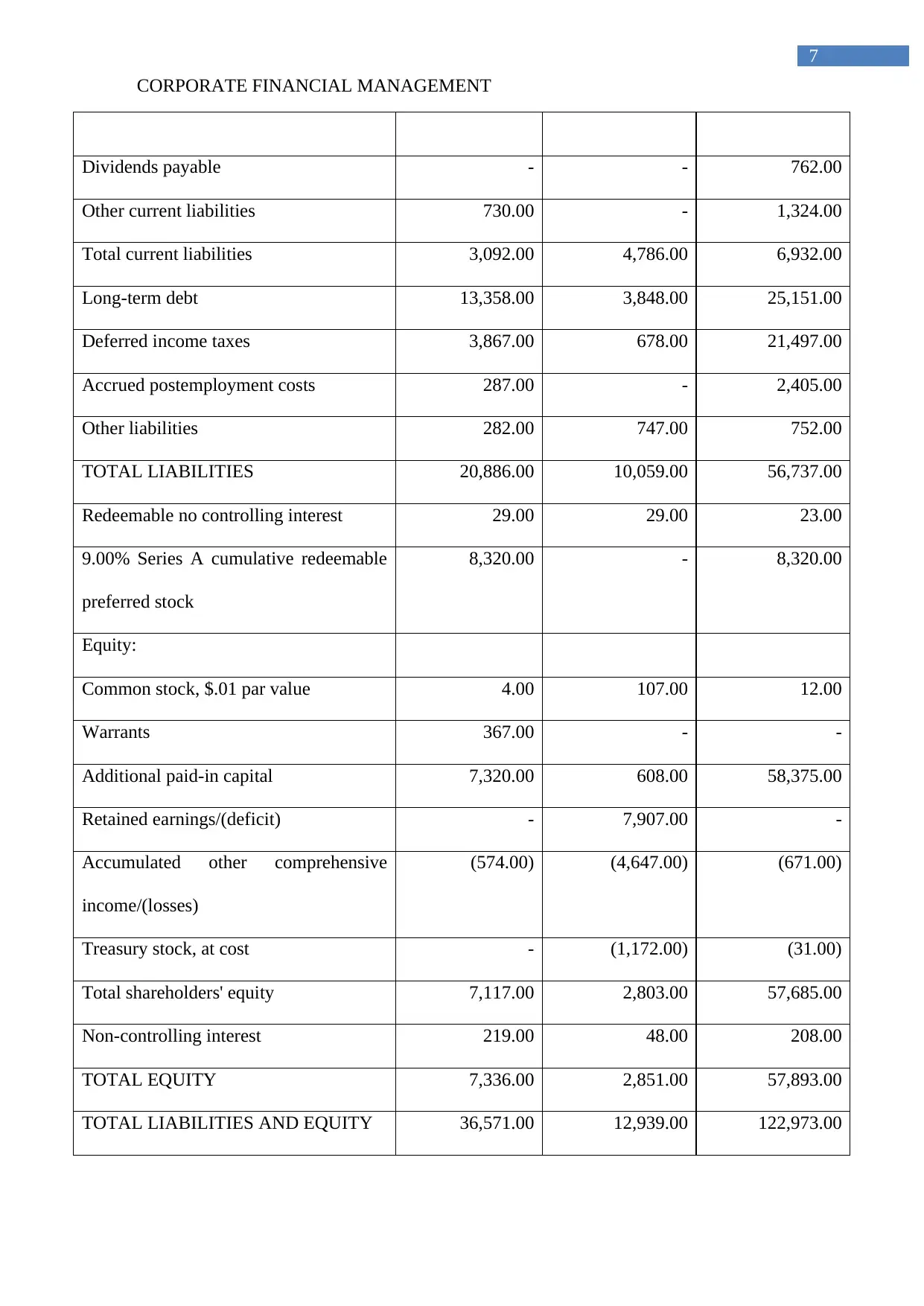

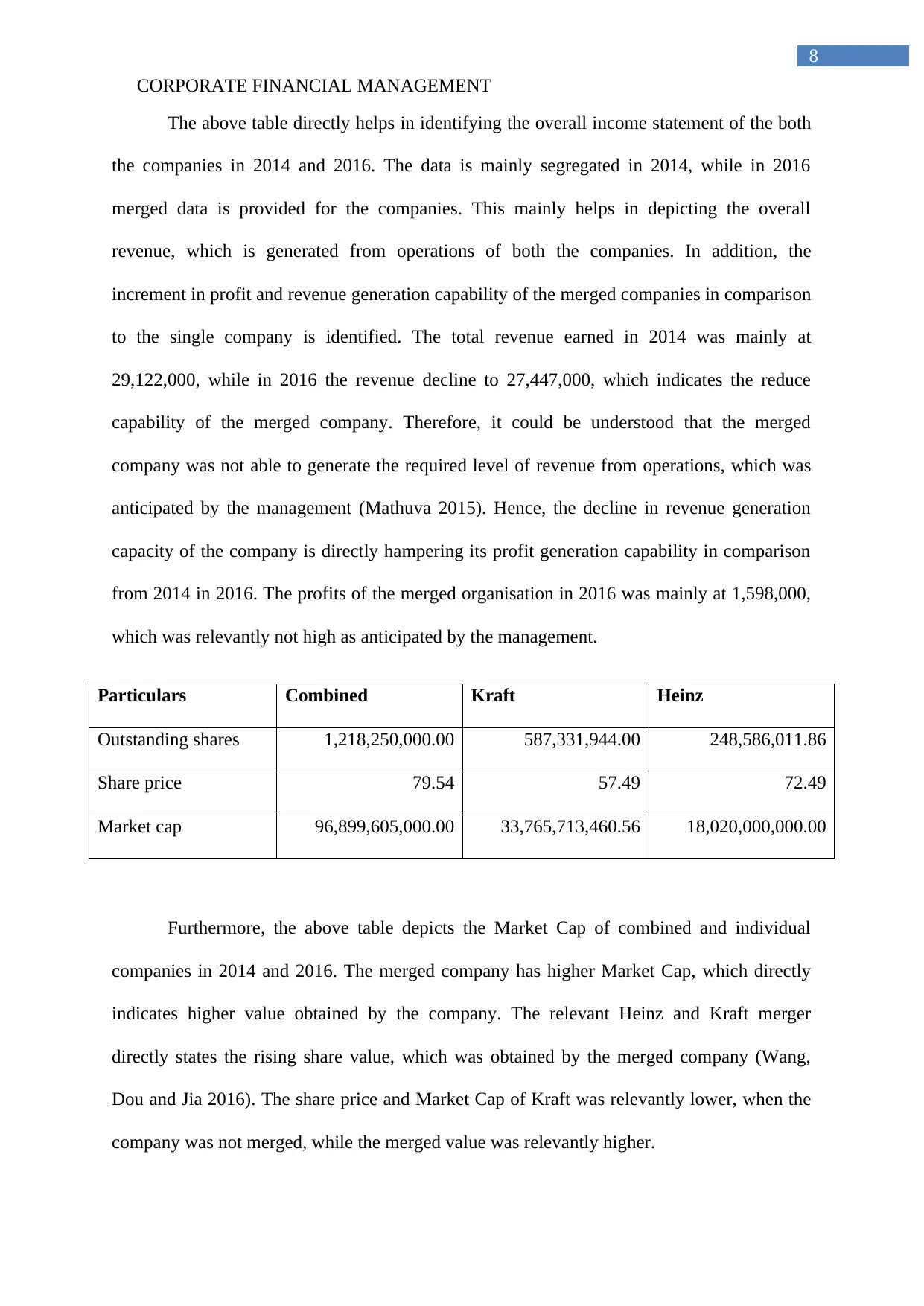

This report provides a comprehensive analysis of corporate financial management, beginning with the computation of Net Present Value (NPV) for a project, and a comparison of the Capital Asset Pricing Model (CAPM) with multivariate models like the Arbitrage Pricing Model (APM). The report then evaluates the synergies resulting from the Heinz and Kraft merger, including cost reductions, revenue increases, and historical transaction evaluations. It presents financial data, including income statements and balance sheets, to assess the merger's impact on financial performance and market capitalization. The analysis includes a discussion of the benefits and drawbacks of the merger, supported by relevant literature. The report examines key financial metrics, outstanding shares, share prices, and market capitalization to demonstrate the effects of the merger. Finally, it provides a detailed reference list of cited sources.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.