Corporate Finance Report: Investment Appraisal and Valuation

VerifiedAdded on 2020/01/07

|13

|4694

|23

Report

AI Summary

This corporate finance report analyzes investment appraisal techniques and company valuation methods. Task 1 focuses on Daffodi Railways, evaluating potential franchise bids using Net Present Value (NPV) and payback period, recommending the optimal bid price based on financial analysis. Task 2 applies corporate finance theories to Wannabe Inc., computing P/E ratios, market capitalization, and enterprise value from 2011 to 2015, and explores the relationship between these metrics. The report also examines the Enterprise Value to EBITDA ratio and its implications. Task 3 evaluates the usefulness of different valuation methods used by venture capital firms and discusses the Enron Scandal. The report concludes by summarizing the findings and providing recommendations based on the financial analysis.

[Corporate finance]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

Maximum bid price on the basis of NPV........................................................................................3

Maximum bid price on the basis of payback...................................................................................4

Recommendation with justification.................................................................................................5

TASK 2.................................................................................................................................................6

Computing Wannabe’s PE ratio from 2011 to 2015........................................................................6

Market capitalization.......................................................................................................................7

Enterprise value...............................................................................................................................7

Enterprise value to EBITDA ratio...................................................................................................8

Reasons for differences in P/E and EV/EBITDA............................................................................8

Enron Scandal..................................................................................................................................9

TASK 3...............................................................................................................................................10

Research questions addressed and its answer................................................................................10

Summarizing the article results......................................................................................................10

Critically evaluating the usefulness of article findings..................................................................11

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................13

2

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

Maximum bid price on the basis of NPV........................................................................................3

Maximum bid price on the basis of payback...................................................................................4

Recommendation with justification.................................................................................................5

TASK 2.................................................................................................................................................6

Computing Wannabe’s PE ratio from 2011 to 2015........................................................................6

Market capitalization.......................................................................................................................7

Enterprise value...............................................................................................................................7

Enterprise value to EBITDA ratio...................................................................................................8

Reasons for differences in P/E and EV/EBITDA............................................................................8

Enron Scandal..................................................................................................................................9

TASK 3...............................................................................................................................................10

Research questions addressed and its answer................................................................................10

Summarizing the article results......................................................................................................10

Critically evaluating the usefulness of article findings..................................................................11

CONCLUSION..................................................................................................................................12

REFERENCES...................................................................................................................................13

2

INTRODUCTION

Every organization whether small, medium or large scales needs sufficient quantity of funds to

run their operations in the market. In this regards, the area of finance through which businesses

meet their long-term monetary requirement is known as corporate finance. Thus, it helps companies

in deciding their capital structure through the composition of both the fixed and variable capital

sources. The proposed investigation herewith emphasizes on the investment appraisal techniques

that help to identify that which project is worthwhile for the Daffodi railways. Project evaluation

methods are of huge significance because it enables firms to select the most viable project through

which overall corporate value can be maximized. Along with the practical implications, the

respective advantage and drawbacks of all the techniques will be examined. In the second part of

the report, corporate finance theories will be applied to determine the market capitalisation and

enterprise value of Wannabe Inc. In the end, the usefulness of different types of valuation methods

that are use by the venture capital firms will be evaluated.

TASK 1

Daffodi Railways is a UK-based company that operates a range of bus and rail services.

According to the scenario, in the present times, it is considering to bid for an exclusive franchise to

operate rail services from Gloucester and Cheltenham across the West part of the England. It is a

capital project which lifespan is estimated to 5 year and the infrastructure of the project is under the

government agency. However, rolling stock is necessary for the continuing the franchise throughout

the period. In the given situation, the initial investment for the new rolling stock is estimated to

£150m whereas older stock will be invested worth £50m. Henceforth, total investment will be

£150m + £50m = £200m and its residual value at the end of five year will be £50m. In this, Daffodi

Railways can use capital budgeting techniques to examine the strength and viability of the available

franchise project. It provides a sound quantitative framework to the financial management to

analyse and evaluate the worthiness of the available capital project.

Maximum bid price on the basis of NPV

This is a discounting technique which measure net yield of the project by discounting all the

expected cash flows through an appropriate discount factor. It is because, the method believed that

investment decisions which influenced the monetary cost and return to the Daffodi Railways must

be taken on the basis of present value (Rutterford, 2015). Therefore, firstly, it measures the PV of

future cash inflows by the way of discounting and thereafter, its total is subtracted from the project

cost, represented as NPV. The selection rule of this technique is based on the concept that Daffodi

3

Every organization whether small, medium or large scales needs sufficient quantity of funds to

run their operations in the market. In this regards, the area of finance through which businesses

meet their long-term monetary requirement is known as corporate finance. Thus, it helps companies

in deciding their capital structure through the composition of both the fixed and variable capital

sources. The proposed investigation herewith emphasizes on the investment appraisal techniques

that help to identify that which project is worthwhile for the Daffodi railways. Project evaluation

methods are of huge significance because it enables firms to select the most viable project through

which overall corporate value can be maximized. Along with the practical implications, the

respective advantage and drawbacks of all the techniques will be examined. In the second part of

the report, corporate finance theories will be applied to determine the market capitalisation and

enterprise value of Wannabe Inc. In the end, the usefulness of different types of valuation methods

that are use by the venture capital firms will be evaluated.

TASK 1

Daffodi Railways is a UK-based company that operates a range of bus and rail services.

According to the scenario, in the present times, it is considering to bid for an exclusive franchise to

operate rail services from Gloucester and Cheltenham across the West part of the England. It is a

capital project which lifespan is estimated to 5 year and the infrastructure of the project is under the

government agency. However, rolling stock is necessary for the continuing the franchise throughout

the period. In the given situation, the initial investment for the new rolling stock is estimated to

£150m whereas older stock will be invested worth £50m. Henceforth, total investment will be

£150m + £50m = £200m and its residual value at the end of five year will be £50m. In this, Daffodi

Railways can use capital budgeting techniques to examine the strength and viability of the available

franchise project. It provides a sound quantitative framework to the financial management to

analyse and evaluate the worthiness of the available capital project.

Maximum bid price on the basis of NPV

This is a discounting technique which measure net yield of the project by discounting all the

expected cash flows through an appropriate discount factor. It is because, the method believed that

investment decisions which influenced the monetary cost and return to the Daffodi Railways must

be taken on the basis of present value (Rutterford, 2015). Therefore, firstly, it measures the PV of

future cash inflows by the way of discounting and thereafter, its total is subtracted from the project

cost, represented as NPV. The selection rule of this technique is based on the concept that Daffodi

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Railways should only undertake a project if it indicates positive NPV, so that, overall wealth can be

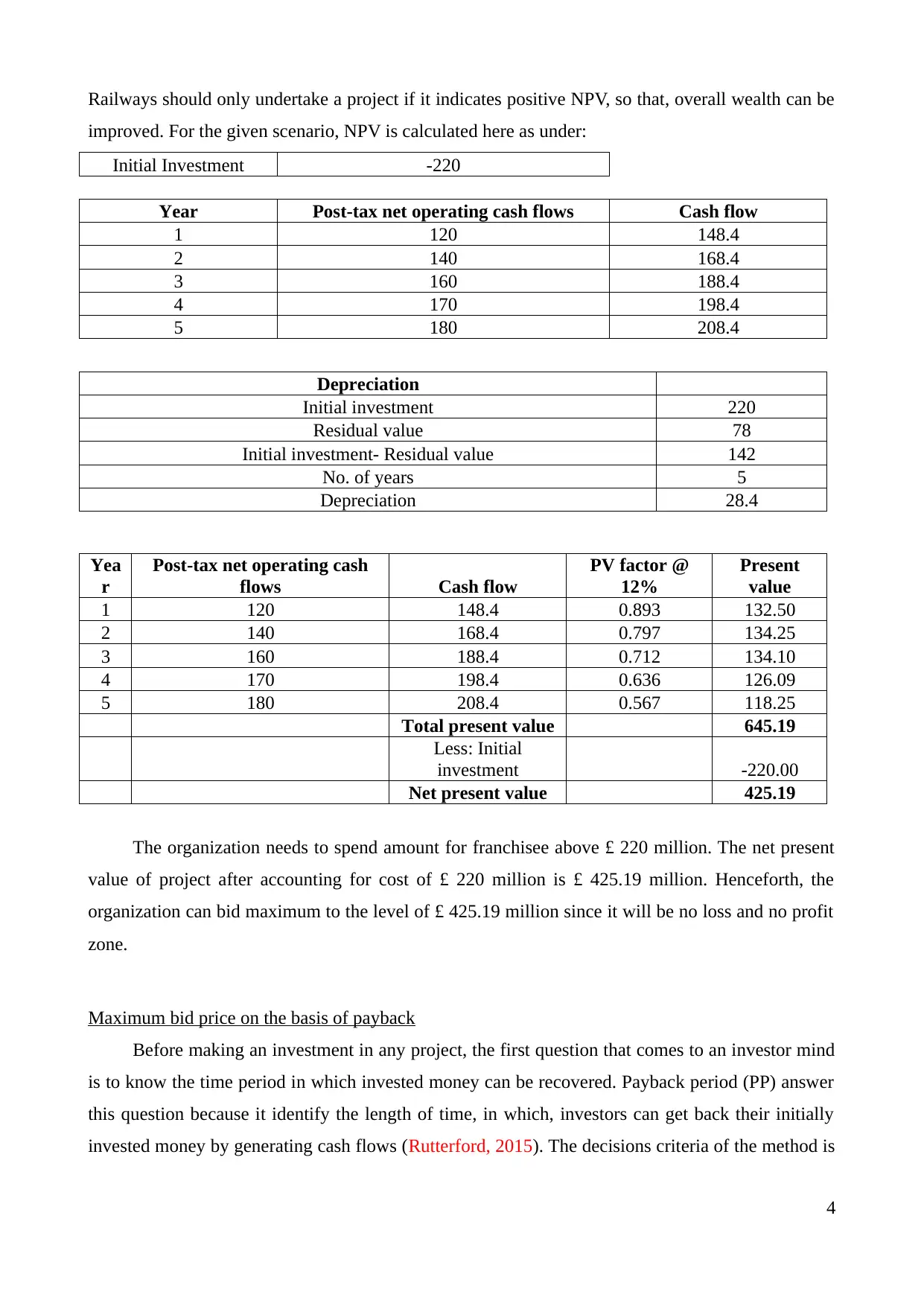

improved. For the given scenario, NPV is calculated here as under:

Initial Investment -220

Year Post-tax net operating cash flows Cash flow

1 120 148.4

2 140 168.4

3 160 188.4

4 170 198.4

5 180 208.4

Depreciation

Initial investment 220

Residual value 78

Initial investment- Residual value 142

No. of years 5

Depreciation 28.4

Yea

r

Post-tax net operating cash

flows Cash flow

PV factor @

12%

Present

value

1 120 148.4 0.893 132.50

2 140 168.4 0.797 134.25

3 160 188.4 0.712 134.10

4 170 198.4 0.636 126.09

5 180 208.4 0.567 118.25

Total present value 645.19

Less: Initial

investment -220.00

Net present value 425.19

The organization needs to spend amount for franchisee above £ 220 million. The net present

value of project after accounting for cost of £ 220 million is £ 425.19 million. Henceforth, the

organization can bid maximum to the level of £ 425.19 million since it will be no loss and no profit

zone.

Maximum bid price on the basis of payback

Before making an investment in any project, the first question that comes to an investor mind

is to know the time period in which invested money can be recovered. Payback period (PP) answer

this question because it identify the length of time, in which, investors can get back their initially

invested money by generating cash flows (Rutterford, 2015). The decisions criteria of the method is

4

improved. For the given scenario, NPV is calculated here as under:

Initial Investment -220

Year Post-tax net operating cash flows Cash flow

1 120 148.4

2 140 168.4

3 160 188.4

4 170 198.4

5 180 208.4

Depreciation

Initial investment 220

Residual value 78

Initial investment- Residual value 142

No. of years 5

Depreciation 28.4

Yea

r

Post-tax net operating cash

flows Cash flow

PV factor @

12%

Present

value

1 120 148.4 0.893 132.50

2 140 168.4 0.797 134.25

3 160 188.4 0.712 134.10

4 170 198.4 0.636 126.09

5 180 208.4 0.567 118.25

Total present value 645.19

Less: Initial

investment -220.00

Net present value 425.19

The organization needs to spend amount for franchisee above £ 220 million. The net present

value of project after accounting for cost of £ 220 million is £ 425.19 million. Henceforth, the

organization can bid maximum to the level of £ 425.19 million since it will be no loss and no profit

zone.

Maximum bid price on the basis of payback

Before making an investment in any project, the first question that comes to an investor mind

is to know the time period in which invested money can be recovered. Payback period (PP) answer

this question because it identify the length of time, in which, investors can get back their initially

invested money by generating cash flows (Rutterford, 2015). The decisions criteria of the method is

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

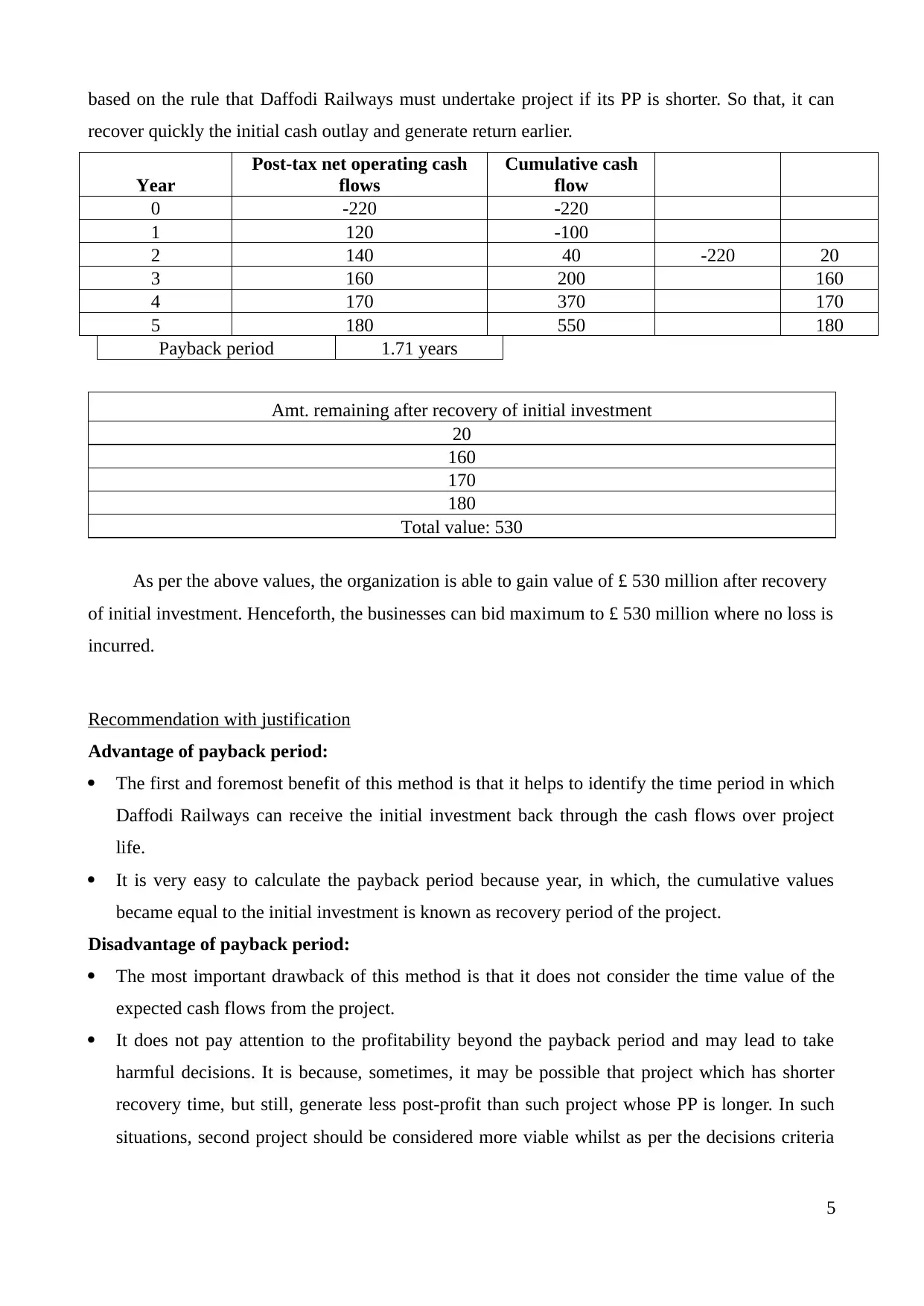

based on the rule that Daffodi Railways must undertake project if its PP is shorter. So that, it can

recover quickly the initial cash outlay and generate return earlier.

Year

Post-tax net operating cash

flows

Cumulative cash

flow

0 -220 -220

1 120 -100

2 140 40 -220 20

3 160 200 160

4 170 370 170

5 180 550 180

Payback period 1.71 years

Amt. remaining after recovery of initial investment

20

160

170

180

Total value: 530

As per the above values, the organization is able to gain value of £ 530 million after recovery

of initial investment. Henceforth, the businesses can bid maximum to £ 530 million where no loss is

incurred.

Recommendation with justification

Advantage of payback period:

The first and foremost benefit of this method is that it helps to identify the time period in which

Daffodi Railways can receive the initial investment back through the cash flows over project

life.

It is very easy to calculate the payback period because year, in which, the cumulative values

became equal to the initial investment is known as recovery period of the project.

Disadvantage of payback period:

The most important drawback of this method is that it does not consider the time value of the

expected cash flows from the project.

It does not pay attention to the profitability beyond the payback period and may lead to take

harmful decisions. It is because, sometimes, it may be possible that project which has shorter

recovery time, but still, generate less post-profit than such project whose PP is longer. In such

situations, second project should be considered more viable whilst as per the decisions criteria

5

recover quickly the initial cash outlay and generate return earlier.

Year

Post-tax net operating cash

flows

Cumulative cash

flow

0 -220 -220

1 120 -100

2 140 40 -220 20

3 160 200 160

4 170 370 170

5 180 550 180

Payback period 1.71 years

Amt. remaining after recovery of initial investment

20

160

170

180

Total value: 530

As per the above values, the organization is able to gain value of £ 530 million after recovery

of initial investment. Henceforth, the businesses can bid maximum to £ 530 million where no loss is

incurred.

Recommendation with justification

Advantage of payback period:

The first and foremost benefit of this method is that it helps to identify the time period in which

Daffodi Railways can receive the initial investment back through the cash flows over project

life.

It is very easy to calculate the payback period because year, in which, the cumulative values

became equal to the initial investment is known as recovery period of the project.

Disadvantage of payback period:

The most important drawback of this method is that it does not consider the time value of the

expected cash flows from the project.

It does not pay attention to the profitability beyond the payback period and may lead to take

harmful decisions. It is because, sometimes, it may be possible that project which has shorter

recovery time, but still, generate less post-profit than such project whose PP is longer. In such

situations, second project should be considered more viable whilst as per the decisions criteria

5

of PP; investor may chose proposal of earlier recovery period which is not good.

Advantage of NPV method:

It takes into account the use of cost of capital to determine the present value of all the projected

cash flows over the project life. In other words, it use time value concept of money, so that,

more appropriate decisions can be taken by the firm (Rutterford, 2015)..

It considers whole the life time and cash flows which help to determine the net yield from the

project. By this, Daffodi Railways can select the project only if it provides some return to the

company.

Disadvantage of NPV method:

Although it relies on the assumption that money has time value and use a discounting factor,

but still, the cost of capital may vary due to market volatility. For instance, interest rate

fluctuations greatly impact this rate, therefore, at different rate; this method will provide

different results.

Using a uniform rate overall the duration cannot be considered realistic because market

fluctuations may change the rate and NPV will be respond changes accordingly.

Taking into account the following benefits and limitations, it can be recommended to

Daffodi railways, that the bid value should be considered as per net present value since it

provides true value of the project. The technique takes into consideration time value of money

and cost of capital. Henceforth, it is considered to provide the most feasible solution.

TASK 2

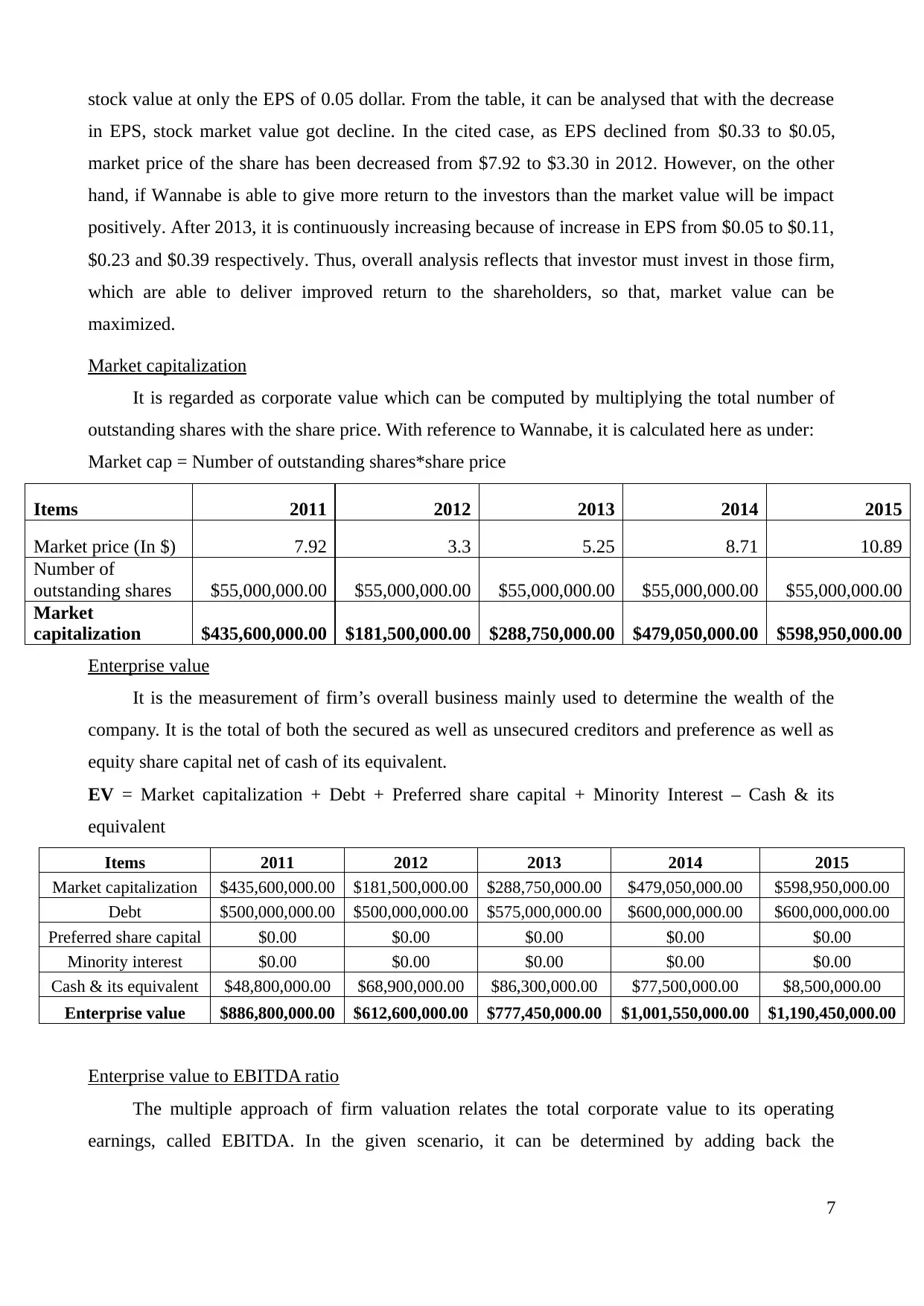

Computing Wannabe’s PE ratio from 2011 to 2015

Price earnings ratio, shortened to PE indicates the relationship between market price and

earning on each holding. It is a valuation measure that is used by the enterprises to compare the

stock prices with the earning per share. Investors can use this ratio to examine the market price of

the share on the basis of EPS.

P/E ratio = Market price / EPS

Items 2011 2012 2013 2014 2015

Market price (In dollar) $7.92 $3.30 $5.25 $8.71 $10.89

EPS (In dollar) $0.33 $0.05 $0.11 $0.23 $0.39

Price to earnings ratio

(P/E)

24 66 47.7272727

3

37.8695652

2

27.9230769

2

According to the presented table, it can be seen that P/E ratio from 2011 to 2015 are 24, 66,

47.73, 37.87 and 27.92 respectively. Thus, it is highest in the year 2012 to 66 because of very less

6

Advantage of NPV method:

It takes into account the use of cost of capital to determine the present value of all the projected

cash flows over the project life. In other words, it use time value concept of money, so that,

more appropriate decisions can be taken by the firm (Rutterford, 2015)..

It considers whole the life time and cash flows which help to determine the net yield from the

project. By this, Daffodi Railways can select the project only if it provides some return to the

company.

Disadvantage of NPV method:

Although it relies on the assumption that money has time value and use a discounting factor,

but still, the cost of capital may vary due to market volatility. For instance, interest rate

fluctuations greatly impact this rate, therefore, at different rate; this method will provide

different results.

Using a uniform rate overall the duration cannot be considered realistic because market

fluctuations may change the rate and NPV will be respond changes accordingly.

Taking into account the following benefits and limitations, it can be recommended to

Daffodi railways, that the bid value should be considered as per net present value since it

provides true value of the project. The technique takes into consideration time value of money

and cost of capital. Henceforth, it is considered to provide the most feasible solution.

TASK 2

Computing Wannabe’s PE ratio from 2011 to 2015

Price earnings ratio, shortened to PE indicates the relationship between market price and

earning on each holding. It is a valuation measure that is used by the enterprises to compare the

stock prices with the earning per share. Investors can use this ratio to examine the market price of

the share on the basis of EPS.

P/E ratio = Market price / EPS

Items 2011 2012 2013 2014 2015

Market price (In dollar) $7.92 $3.30 $5.25 $8.71 $10.89

EPS (In dollar) $0.33 $0.05 $0.11 $0.23 $0.39

Price to earnings ratio

(P/E)

24 66 47.7272727

3

37.8695652

2

27.9230769

2

According to the presented table, it can be seen that P/E ratio from 2011 to 2015 are 24, 66,

47.73, 37.87 and 27.92 respectively. Thus, it is highest in the year 2012 to 66 because of very less

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

stock value at only the EPS of 0.05 dollar. From the table, it can be analysed that with the decrease

in EPS, stock market value got decline. In the cited case, as EPS declined from $0.33 to $0.05,

market price of the share has been decreased from $7.92 to $3.30 in 2012. However, on the other

hand, if Wannabe is able to give more return to the investors than the market value will be impact

positively. After 2013, it is continuously increasing because of increase in EPS from $0.05 to $0.11,

$0.23 and $0.39 respectively. Thus, overall analysis reflects that investor must invest in those firm,

which are able to deliver improved return to the shareholders, so that, market value can be

maximized.

Market capitalization

It is regarded as corporate value which can be computed by multiplying the total number of

outstanding shares with the share price. With reference to Wannabe, it is calculated here as under:

Market cap = Number of outstanding shares*share price

Items 2011 2012 2013 2014 2015

Market price (In $) 7.92 3.3 5.25 8.71 10.89

Number of

outstanding shares $55,000,000.00 $55,000,000.00 $55,000,000.00 $55,000,000.00 $55,000,000.00

Market

capitalization $435,600,000.00 $181,500,000.00 $288,750,000.00 $479,050,000.00 $598,950,000.00

Enterprise value

It is the measurement of firm’s overall business mainly used to determine the wealth of the

company. It is the total of both the secured as well as unsecured creditors and preference as well as

equity share capital net of cash of its equivalent.

EV = Market capitalization + Debt + Preferred share capital + Minority Interest – Cash & its

equivalent

Items 2011 2012 2013 2014 2015

Market capitalization $435,600,000.00 $181,500,000.00 $288,750,000.00 $479,050,000.00 $598,950,000.00

Debt $500,000,000.00 $500,000,000.00 $575,000,000.00 $600,000,000.00 $600,000,000.00

Preferred share capital $0.00 $0.00 $0.00 $0.00 $0.00

Minority interest $0.00 $0.00 $0.00 $0.00 $0.00

Cash & its equivalent $48,800,000.00 $68,900,000.00 $86,300,000.00 $77,500,000.00 $8,500,000.00

Enterprise value $886,800,000.00 $612,600,000.00 $777,450,000.00 $1,001,550,000.00 $1,190,450,000.00

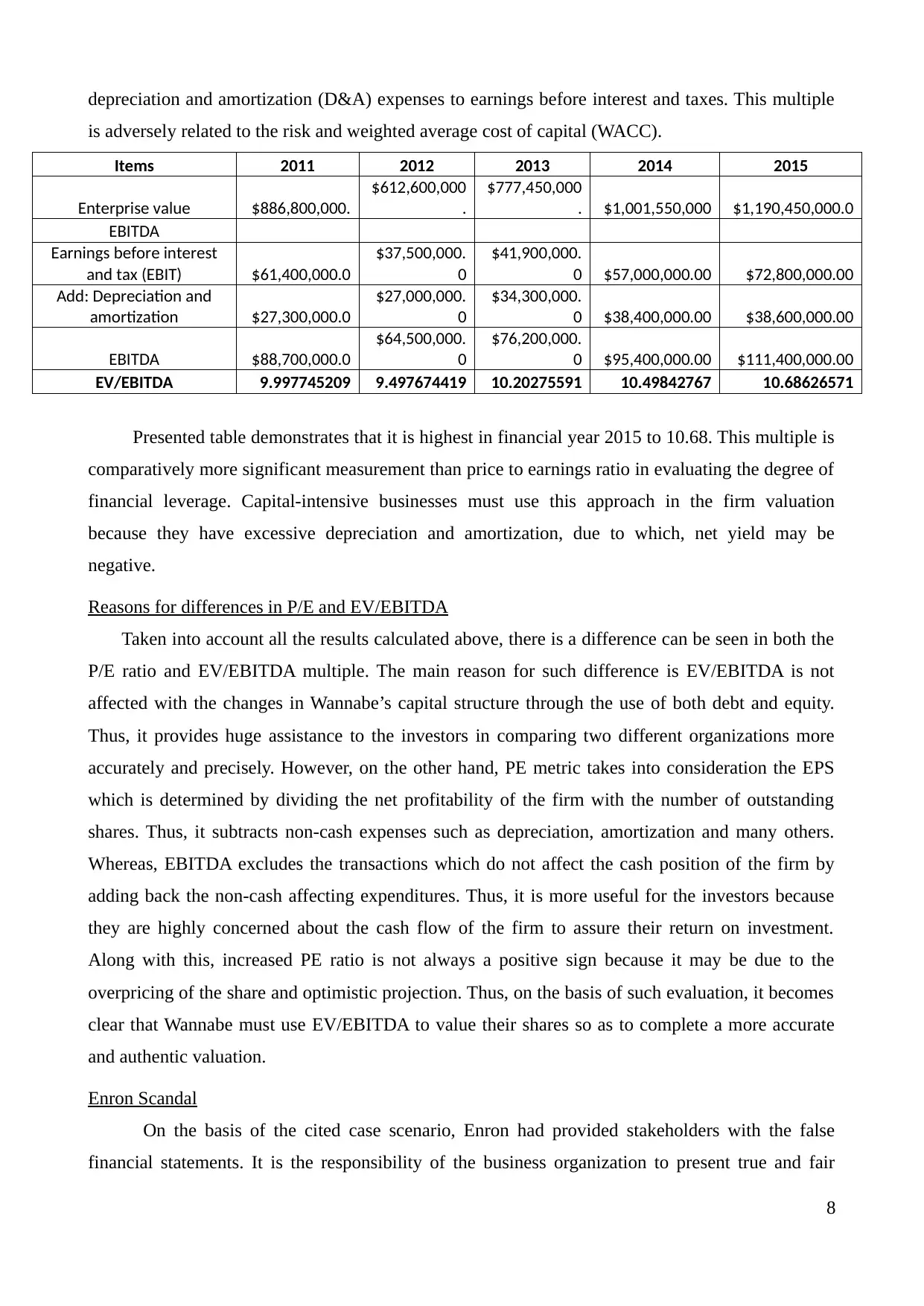

Enterprise value to EBITDA ratio

The multiple approach of firm valuation relates the total corporate value to its operating

earnings, called EBITDA. In the given scenario, it can be determined by adding back the

7

in EPS, stock market value got decline. In the cited case, as EPS declined from $0.33 to $0.05,

market price of the share has been decreased from $7.92 to $3.30 in 2012. However, on the other

hand, if Wannabe is able to give more return to the investors than the market value will be impact

positively. After 2013, it is continuously increasing because of increase in EPS from $0.05 to $0.11,

$0.23 and $0.39 respectively. Thus, overall analysis reflects that investor must invest in those firm,

which are able to deliver improved return to the shareholders, so that, market value can be

maximized.

Market capitalization

It is regarded as corporate value which can be computed by multiplying the total number of

outstanding shares with the share price. With reference to Wannabe, it is calculated here as under:

Market cap = Number of outstanding shares*share price

Items 2011 2012 2013 2014 2015

Market price (In $) 7.92 3.3 5.25 8.71 10.89

Number of

outstanding shares $55,000,000.00 $55,000,000.00 $55,000,000.00 $55,000,000.00 $55,000,000.00

Market

capitalization $435,600,000.00 $181,500,000.00 $288,750,000.00 $479,050,000.00 $598,950,000.00

Enterprise value

It is the measurement of firm’s overall business mainly used to determine the wealth of the

company. It is the total of both the secured as well as unsecured creditors and preference as well as

equity share capital net of cash of its equivalent.

EV = Market capitalization + Debt + Preferred share capital + Minority Interest – Cash & its

equivalent

Items 2011 2012 2013 2014 2015

Market capitalization $435,600,000.00 $181,500,000.00 $288,750,000.00 $479,050,000.00 $598,950,000.00

Debt $500,000,000.00 $500,000,000.00 $575,000,000.00 $600,000,000.00 $600,000,000.00

Preferred share capital $0.00 $0.00 $0.00 $0.00 $0.00

Minority interest $0.00 $0.00 $0.00 $0.00 $0.00

Cash & its equivalent $48,800,000.00 $68,900,000.00 $86,300,000.00 $77,500,000.00 $8,500,000.00

Enterprise value $886,800,000.00 $612,600,000.00 $777,450,000.00 $1,001,550,000.00 $1,190,450,000.00

Enterprise value to EBITDA ratio

The multiple approach of firm valuation relates the total corporate value to its operating

earnings, called EBITDA. In the given scenario, it can be determined by adding back the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

depreciation and amortization (D&A) expenses to earnings before interest and taxes. This multiple

is adversely related to the risk and weighted average cost of capital (WACC).

Items 2011 2012 2013 2014 2015

Enterprise value $886,800,000.

$612,600,000

.

$777,450,000

. $1,001,550,000 $1,190,450,000.0

EBITDA

Earnings before interest

and tax (EBIT) $61,400,000.0

$37,500,000.

0

$41,900,000.

0 $57,000,000.00 $72,800,000.00

Add: Depreciation and

amortization $27,300,000.0

$27,000,000.

0

$34,300,000.

0 $38,400,000.00 $38,600,000.00

EBITDA $88,700,000.0

$64,500,000.

0

$76,200,000.

0 $95,400,000.00 $111,400,000.00

EV/EBITDA 9.997745209 9.497674419 10.20275591 10.49842767 10.68626571

Presented table demonstrates that it is highest in financial year 2015 to 10.68. This multiple is

comparatively more significant measurement than price to earnings ratio in evaluating the degree of

financial leverage. Capital-intensive businesses must use this approach in the firm valuation

because they have excessive depreciation and amortization, due to which, net yield may be

negative.

Reasons for differences in P/E and EV/EBITDA

Taken into account all the results calculated above, there is a difference can be seen in both the

P/E ratio and EV/EBITDA multiple. The main reason for such difference is EV/EBITDA is not

affected with the changes in Wannabe’s capital structure through the use of both debt and equity.

Thus, it provides huge assistance to the investors in comparing two different organizations more

accurately and precisely. However, on the other hand, PE metric takes into consideration the EPS

which is determined by dividing the net profitability of the firm with the number of outstanding

shares. Thus, it subtracts non-cash expenses such as depreciation, amortization and many others.

Whereas, EBITDA excludes the transactions which do not affect the cash position of the firm by

adding back the non-cash affecting expenditures. Thus, it is more useful for the investors because

they are highly concerned about the cash flow of the firm to assure their return on investment.

Along with this, increased PE ratio is not always a positive sign because it may be due to the

overpricing of the share and optimistic projection. Thus, on the basis of such evaluation, it becomes

clear that Wannabe must use EV/EBITDA to value their shares so as to complete a more accurate

and authentic valuation.

Enron Scandal

On the basis of the cited case scenario, Enron had provided stakeholders with the false

financial statements. It is the responsibility of the business organization to present true and fair

8

is adversely related to the risk and weighted average cost of capital (WACC).

Items 2011 2012 2013 2014 2015

Enterprise value $886,800,000.

$612,600,000

.

$777,450,000

. $1,001,550,000 $1,190,450,000.0

EBITDA

Earnings before interest

and tax (EBIT) $61,400,000.0

$37,500,000.

0

$41,900,000.

0 $57,000,000.00 $72,800,000.00

Add: Depreciation and

amortization $27,300,000.0

$27,000,000.

0

$34,300,000.

0 $38,400,000.00 $38,600,000.00

EBITDA $88,700,000.0

$64,500,000.

0

$76,200,000.

0 $95,400,000.00 $111,400,000.00

EV/EBITDA 9.997745209 9.497674419 10.20275591 10.49842767 10.68626571

Presented table demonstrates that it is highest in financial year 2015 to 10.68. This multiple is

comparatively more significant measurement than price to earnings ratio in evaluating the degree of

financial leverage. Capital-intensive businesses must use this approach in the firm valuation

because they have excessive depreciation and amortization, due to which, net yield may be

negative.

Reasons for differences in P/E and EV/EBITDA

Taken into account all the results calculated above, there is a difference can be seen in both the

P/E ratio and EV/EBITDA multiple. The main reason for such difference is EV/EBITDA is not

affected with the changes in Wannabe’s capital structure through the use of both debt and equity.

Thus, it provides huge assistance to the investors in comparing two different organizations more

accurately and precisely. However, on the other hand, PE metric takes into consideration the EPS

which is determined by dividing the net profitability of the firm with the number of outstanding

shares. Thus, it subtracts non-cash expenses such as depreciation, amortization and many others.

Whereas, EBITDA excludes the transactions which do not affect the cash position of the firm by

adding back the non-cash affecting expenditures. Thus, it is more useful for the investors because

they are highly concerned about the cash flow of the firm to assure their return on investment.

Along with this, increased PE ratio is not always a positive sign because it may be due to the

overpricing of the share and optimistic projection. Thus, on the basis of such evaluation, it becomes

clear that Wannabe must use EV/EBITDA to value their shares so as to complete a more accurate

and authentic valuation.

Enron Scandal

On the basis of the cited case scenario, Enron had provided stakeholders with the false

financial statements. It is the responsibility of the business organization to present true and fair

8

picture of the financial statements in front of the stakeholders by taking into account IFRS. In the

previous year’s Enron management was considered as an innovative and aggressive by the market.

Hence, business model of Enron had raised demand of the investors for the company's stock.

During the period of 1997 to September 2000 prices of the stock of Enron was significantly

inclined. Along with this, during the period of 1991-996 tandem move was seen in the income

aspect. However, after this period, there was high level of inclined in the profitability aspect of the

firm. By taking into account the higher profitability aspect investors have decided to invest high

amount money in the firms operations. Hence, attracting large number of investors was one of the

main objectives of Chief Officers of Enron. Due to this, they were provided investors and other

stakeholders with the false profitability statement.

By applying Beneish model it had been assessed that significant manipulation did by Enron

in its financial statements. From evaluation it has been identified that manipulation had made by

Enron in days sales, gross receivable, asset quality and depreciation and SG&A index. From the

period 1995 to 2000 company presented higher gross profit margin which was greater than the

specific limit such as 1. This aspect shows that manipulation had made by the firm in the profit

margin. Moreover, Beneish model stated that when index is more than 1 then it reflects the situation

of manipulation. In the accounting year 1998 and 2000 Enron exceeded the limit of 1 which shows

that company had manipulated the statements to hide its poorer performance (Catanach and

Rhoades-Catanach, 2003).

Furthermore, business organization had recorded low expenses in comparison to the actual

made by it. In addition to this, in the annual report Enron has presented higher sales in comparison

to the actual generated by it. In the financial statements, company also showed that huge amount of

sales was made by it on case basis rather than on credit terms. In this way, manipulation had made

by Enron in its financial position. Investors and stock or financial market analysts can make

assessment of reliability aspect of the financial statements by taking into account Beneish model.

Moreover, such mathematical model provides deeper and fair information regarding the company's

performance by taking into consideration ratios and 8 other factors. Thus, by following such model

analysts can make idea regarding the potentials in relation to the firm’s bankruptcy to the large

extent.

TASK 3

Research questions addressed and its answer

In the article of “venture capitalists, investment appraisal and accounting information,

comparative study of France, Belgium, USA, UK and Holland”, research issue is that writer desire

9

previous year’s Enron management was considered as an innovative and aggressive by the market.

Hence, business model of Enron had raised demand of the investors for the company's stock.

During the period of 1997 to September 2000 prices of the stock of Enron was significantly

inclined. Along with this, during the period of 1991-996 tandem move was seen in the income

aspect. However, after this period, there was high level of inclined in the profitability aspect of the

firm. By taking into account the higher profitability aspect investors have decided to invest high

amount money in the firms operations. Hence, attracting large number of investors was one of the

main objectives of Chief Officers of Enron. Due to this, they were provided investors and other

stakeholders with the false profitability statement.

By applying Beneish model it had been assessed that significant manipulation did by Enron

in its financial statements. From evaluation it has been identified that manipulation had made by

Enron in days sales, gross receivable, asset quality and depreciation and SG&A index. From the

period 1995 to 2000 company presented higher gross profit margin which was greater than the

specific limit such as 1. This aspect shows that manipulation had made by the firm in the profit

margin. Moreover, Beneish model stated that when index is more than 1 then it reflects the situation

of manipulation. In the accounting year 1998 and 2000 Enron exceeded the limit of 1 which shows

that company had manipulated the statements to hide its poorer performance (Catanach and

Rhoades-Catanach, 2003).

Furthermore, business organization had recorded low expenses in comparison to the actual

made by it. In addition to this, in the annual report Enron has presented higher sales in comparison

to the actual generated by it. In the financial statements, company also showed that huge amount of

sales was made by it on case basis rather than on credit terms. In this way, manipulation had made

by Enron in its financial position. Investors and stock or financial market analysts can make

assessment of reliability aspect of the financial statements by taking into account Beneish model.

Moreover, such mathematical model provides deeper and fair information regarding the company's

performance by taking into consideration ratios and 8 other factors. Thus, by following such model

analysts can make idea regarding the potentials in relation to the firm’s bankruptcy to the large

extent.

TASK 3

Research questions addressed and its answer

In the article of “venture capitalists, investment appraisal and accounting information,

comparative study of France, Belgium, USA, UK and Holland”, research issue is that writer desire

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to bridge the research gap by identifying the differences in valuation methods used by VC of all the

5 countries. However, in the other article, writer wishes to identify various methods of valuation

used by the VC of European countries. The main focus of both these articles is to analyse the

relative importance of all the valuations techniques. They are greatly motivated to determine the

most appropriate method of firm valuation. This research questions are addressed by the writer

through conducting the thoroughly study of different methods and techniques such as accounting

based, earning multiples, discounted cash flows, rule of thumb and many others. Despite this, article

also identified the advantages and drawbacks of each and every method with its practical uses by

the investors of different nations.

Summarizing the article results

According to the articles, it has been identified that venture capitalists of all the five nations,

that are USA, UK, France, Belgium and Holland used different kinds of valuation methods. As per

the article, broadly, there are three valuation methods based on expected cash flows, thumb rule and

accounting measures. Out of these, Discounted Cash Flow (DCF) is the most frequently use

technique which is use by the number of capitalists, especially in Belgium and Netherland. Along

with this, Dutch VC also makes use of this technique in their valuation. Moreover, some other

textbook methods are available that are dividend yield and payback methods, but still, it is

comparatively gains less importance than EBITDA, price to earnings ratio and EBIT multiples.

Apart from this, there are some other methods available to an investor such as relationship-based

and accounting-based techniques. In such respect, the responses to solicit bids for future investee

and rule of thumb of industries are the relationship-oriented techniques which are greatly used by

France. In this regards, rule of thumb represents the idle industrial ratios, also known as standard

ratios. For instance, current ratio of 2:1 is considered idle; however, 1:1 acid test ratio is generally

taken as standard ratio. Contrary to this, book value and liquidation prices are the accounting

measures to valuation. Article presented that in UK, large number of VC makes use of historical

prices to earnings multiples in their process of valuation. However, USA and France mainly use

EBIT multiples and current transactions prices whilst in UK, earning multiple methods gain huge

importance. Moreover, after studying both the articles, I have founded that less developed countries

greatly make use of corporate finance theories such as DCF and dividend yield. However, in the

valuation process of network- based economies like France and Belgium, entrepreneur’s

personality, information provided by management and personal references plays a more important

role. USA and UK based VC greatly relies on the own due diligence. Apart from this, assets value

method is not usually appealed by VC, henceforth, considered as impractical method due to less

10

5 countries. However, in the other article, writer wishes to identify various methods of valuation

used by the VC of European countries. The main focus of both these articles is to analyse the

relative importance of all the valuations techniques. They are greatly motivated to determine the

most appropriate method of firm valuation. This research questions are addressed by the writer

through conducting the thoroughly study of different methods and techniques such as accounting

based, earning multiples, discounted cash flows, rule of thumb and many others. Despite this, article

also identified the advantages and drawbacks of each and every method with its practical uses by

the investors of different nations.

Summarizing the article results

According to the articles, it has been identified that venture capitalists of all the five nations,

that are USA, UK, France, Belgium and Holland used different kinds of valuation methods. As per

the article, broadly, there are three valuation methods based on expected cash flows, thumb rule and

accounting measures. Out of these, Discounted Cash Flow (DCF) is the most frequently use

technique which is use by the number of capitalists, especially in Belgium and Netherland. Along

with this, Dutch VC also makes use of this technique in their valuation. Moreover, some other

textbook methods are available that are dividend yield and payback methods, but still, it is

comparatively gains less importance than EBITDA, price to earnings ratio and EBIT multiples.

Apart from this, there are some other methods available to an investor such as relationship-based

and accounting-based techniques. In such respect, the responses to solicit bids for future investee

and rule of thumb of industries are the relationship-oriented techniques which are greatly used by

France. In this regards, rule of thumb represents the idle industrial ratios, also known as standard

ratios. For instance, current ratio of 2:1 is considered idle; however, 1:1 acid test ratio is generally

taken as standard ratio. Contrary to this, book value and liquidation prices are the accounting

measures to valuation. Article presented that in UK, large number of VC makes use of historical

prices to earnings multiples in their process of valuation. However, USA and France mainly use

EBIT multiples and current transactions prices whilst in UK, earning multiple methods gain huge

importance. Moreover, after studying both the articles, I have founded that less developed countries

greatly make use of corporate finance theories such as DCF and dividend yield. However, in the

valuation process of network- based economies like France and Belgium, entrepreneur’s

personality, information provided by management and personal references plays a more important

role. USA and UK based VC greatly relies on the own due diligence. Apart from this, assets value

method is not usually appealed by VC, henceforth, considered as impractical method due to less

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

theoretical importance (Manigart and et.al., 1997). Thus, from the empirical findings of the

research, it can be summarized that Cluster analysis covers five distinct measurements in the

valuation process that are presented below:

Earnings multiples which consider capitalized maintainable profits such as price to earnings as

well as earnings before interest and tax multiple

Discounted estimated cash flow

Dividend yield

Sector or industry specific ratio i.e. rule of thumb

Assets value i.e. liquidation value, cost of replacing an asset, historical cost and book value etc.

As per the article, the most important reasons for differences in the use of valuations methods is

that British VC have more experience so they expected higher rate of return on their invested

comparison to that of Dutch, Belgian and French as they desire to earn minimum return.

Critically evaluating the usefulness of article findings

This article is of huge importance for the today’s business managers because it presents the in-

depth evaluation and analysis of different kinds of investment appraisal and valuation process

techniques to examine and assess the associated risk and return with their investment. The article

evaluated the entire investment process which includes the information gathering activities to

forecast the future cash flows and profits at a certain level of risk. Thereafter, capitalists can use the

valuation techniques to determine corporate value by combining all the elements that are risk,

return, profitability and cash flows as well. Each and every method has certain advantage as well as

drawbacks that must be examined before making use of any of the techniques. Although, DCF is

considered best method because it does not use historical results to make projections which is

helpful mainly for the new ventures, but still, it has certain limitations. One of the most important

limitations is that in the real market, when things are changing at faster pace, it is not very easy for

the investors to forecast the future cash flow. Moreover, the slightly increase in growth percentage

can impact the entire firm valuation. Due to these limitations, multiples approach is considered best

for the current managers because it use price to earnings ratio and EBIT to value firm. In such

respect, managers can use P/E on both historical and prospective basis and the method is very

popular in UK and continental countries. Thus, this valuation technique takes into account both the

market price of the stock and earnings per share as well. But still, it has only one limitation that is it

cannot be use when the financial statements of the company report losses (Manigart and et.al.,

2000). However, other methods such as assets based, dividend yield and rule of thumb are identified

less important. From the overall examination, it can be said that current managers must use multiple

11

research, it can be summarized that Cluster analysis covers five distinct measurements in the

valuation process that are presented below:

Earnings multiples which consider capitalized maintainable profits such as price to earnings as

well as earnings before interest and tax multiple

Discounted estimated cash flow

Dividend yield

Sector or industry specific ratio i.e. rule of thumb

Assets value i.e. liquidation value, cost of replacing an asset, historical cost and book value etc.

As per the article, the most important reasons for differences in the use of valuations methods is

that British VC have more experience so they expected higher rate of return on their invested

comparison to that of Dutch, Belgian and French as they desire to earn minimum return.

Critically evaluating the usefulness of article findings

This article is of huge importance for the today’s business managers because it presents the in-

depth evaluation and analysis of different kinds of investment appraisal and valuation process

techniques to examine and assess the associated risk and return with their investment. The article

evaluated the entire investment process which includes the information gathering activities to

forecast the future cash flows and profits at a certain level of risk. Thereafter, capitalists can use the

valuation techniques to determine corporate value by combining all the elements that are risk,

return, profitability and cash flows as well. Each and every method has certain advantage as well as

drawbacks that must be examined before making use of any of the techniques. Although, DCF is

considered best method because it does not use historical results to make projections which is

helpful mainly for the new ventures, but still, it has certain limitations. One of the most important

limitations is that in the real market, when things are changing at faster pace, it is not very easy for

the investors to forecast the future cash flow. Moreover, the slightly increase in growth percentage

can impact the entire firm valuation. Due to these limitations, multiples approach is considered best

for the current managers because it use price to earnings ratio and EBIT to value firm. In such

respect, managers can use P/E on both historical and prospective basis and the method is very

popular in UK and continental countries. Thus, this valuation technique takes into account both the

market price of the stock and earnings per share as well. But still, it has only one limitation that is it

cannot be use when the financial statements of the company report losses (Manigart and et.al.,

2000). However, other methods such as assets based, dividend yield and rule of thumb are identified

less important. From the overall examination, it can be said that current managers must use multiple

11

approach to value their firm. Moreover, it must be noted that in the present times, market multiple is

also considered as appropriate technique for the managers for the firm valuation.

Strengths:

Helpful for me to improve my financial skills through the in-depth study of various valuation

techniques

Improve my own knowledge to practically applying the techniques and value firm.

Enhancement of analytical skills through the comparative study of all the valuation methods.

Weaknesses:

It is quite difficult for me to determine the best method because every method has certain good

and bad points. Therefore, it seems to be very complex for me to identify the best method in

different business situations.

Lack of information about the detailed analysis, advantages and drawbacks of all the

techniques is also a weakness of the article in relation to improve my managerial skills.

CONCLUSION

In conclusion of the entire report, it can be said that Daffodi Railways must use NPV method to

bid the maximum price for the franchise agreement because it considers the monetary value via

discounting. While, the middle part of the report identified that EV/EBITDA is the most accurate

method to determine corporate value. It is mainly because of excluding the non-cash affecting

elements such as depreciations and amortization and use cash flows about which investors are more

concerned. At the end, the article bring forth the fact that DCF and earning multiple are two majorly

used techniques which are used by large number of venture capitalists to assess their risk and return.

12

also considered as appropriate technique for the managers for the firm valuation.

Strengths:

Helpful for me to improve my financial skills through the in-depth study of various valuation

techniques

Improve my own knowledge to practically applying the techniques and value firm.

Enhancement of analytical skills through the comparative study of all the valuation methods.

Weaknesses:

It is quite difficult for me to determine the best method because every method has certain good

and bad points. Therefore, it seems to be very complex for me to identify the best method in

different business situations.

Lack of information about the detailed analysis, advantages and drawbacks of all the

techniques is also a weakness of the article in relation to improve my managerial skills.

CONCLUSION

In conclusion of the entire report, it can be said that Daffodi Railways must use NPV method to

bid the maximum price for the franchise agreement because it considers the monetary value via

discounting. While, the middle part of the report identified that EV/EBITDA is the most accurate

method to determine corporate value. It is mainly because of excluding the non-cash affecting

elements such as depreciations and amortization and use cash flows about which investors are more

concerned. At the end, the article bring forth the fact that DCF and earning multiple are two majorly

used techniques which are used by large number of venture capitalists to assess their risk and return.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.