Corporate Finance Report: Valuation, Mergers, and Investment Analysis

VerifiedAdded on 2022/09/07

|10

|1343

|17

Report

AI Summary

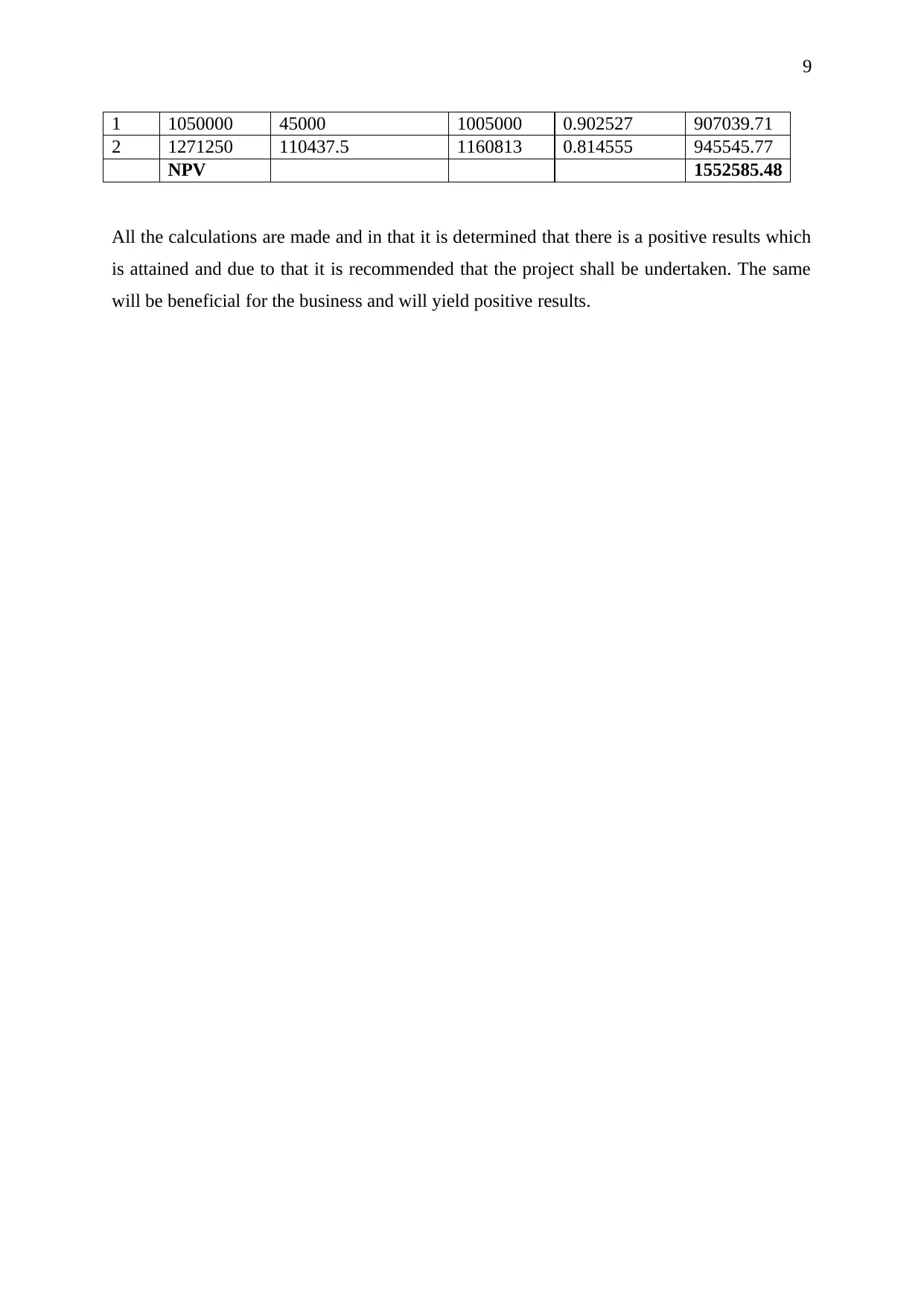

This report addresses a corporate finance assignment focusing on share valuation, investment decisions, and project analysis. The report begins by calculating the intrinsic value of a share using the price-earnings approach, dividend discount model, and net realizable value approach. It then discusses the perspectives of a takeover specialist and a director regarding valuation methods. The report further analyzes the use of equity approaches and discounted cash flow in merger decisions, emphasizing the superiority of the latter. Finally, the report evaluates a project using the net present value (NPV) approach, incorporating capital allowances, tax savings, and cash flows to determine its viability. The analysis concludes with a recommendation based on the positive NPV result.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.