Corporate Finance Assignment: Valuation and NPV Analysis

VerifiedAdded on 2022/09/07

|7

|1254

|15

Report

AI Summary

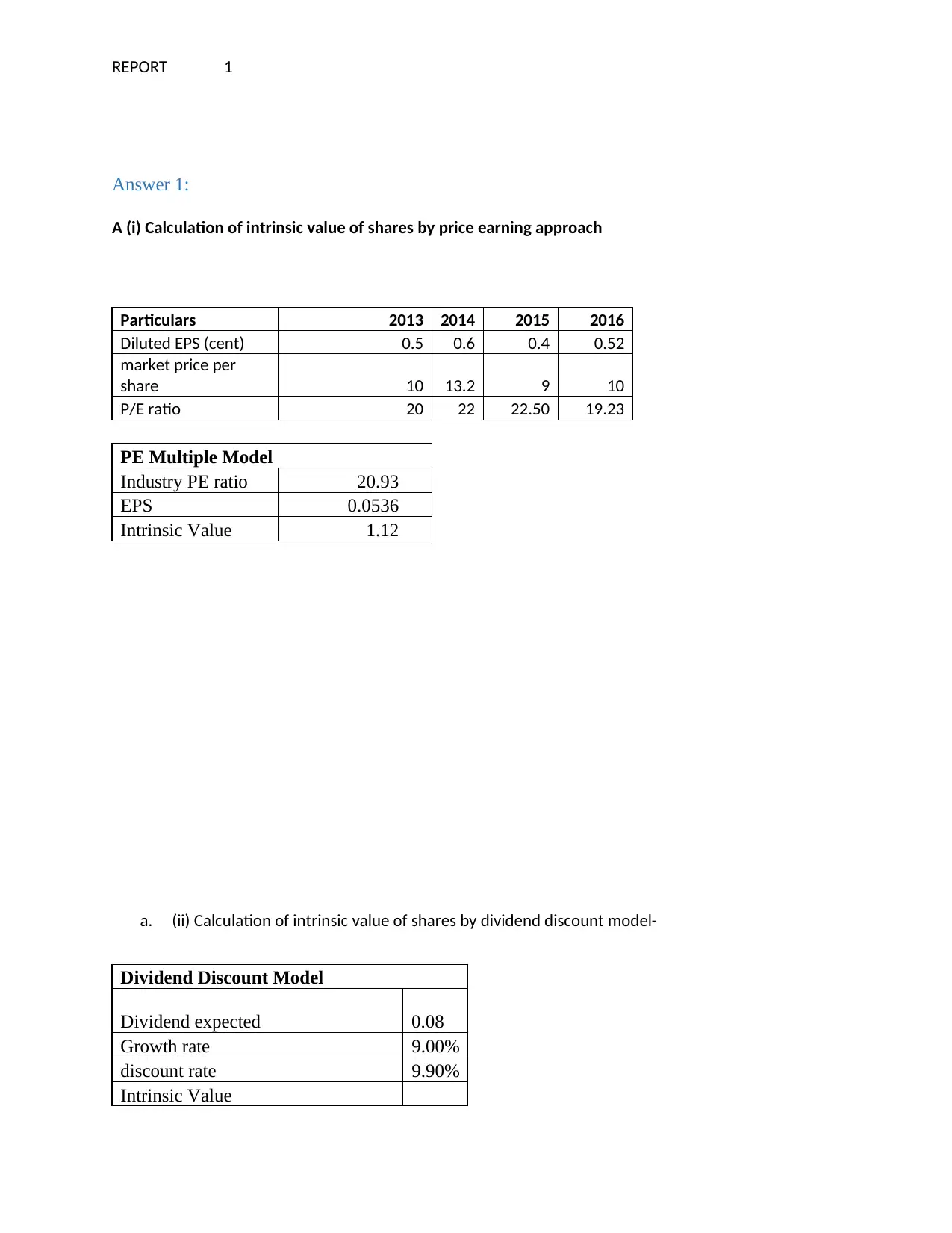

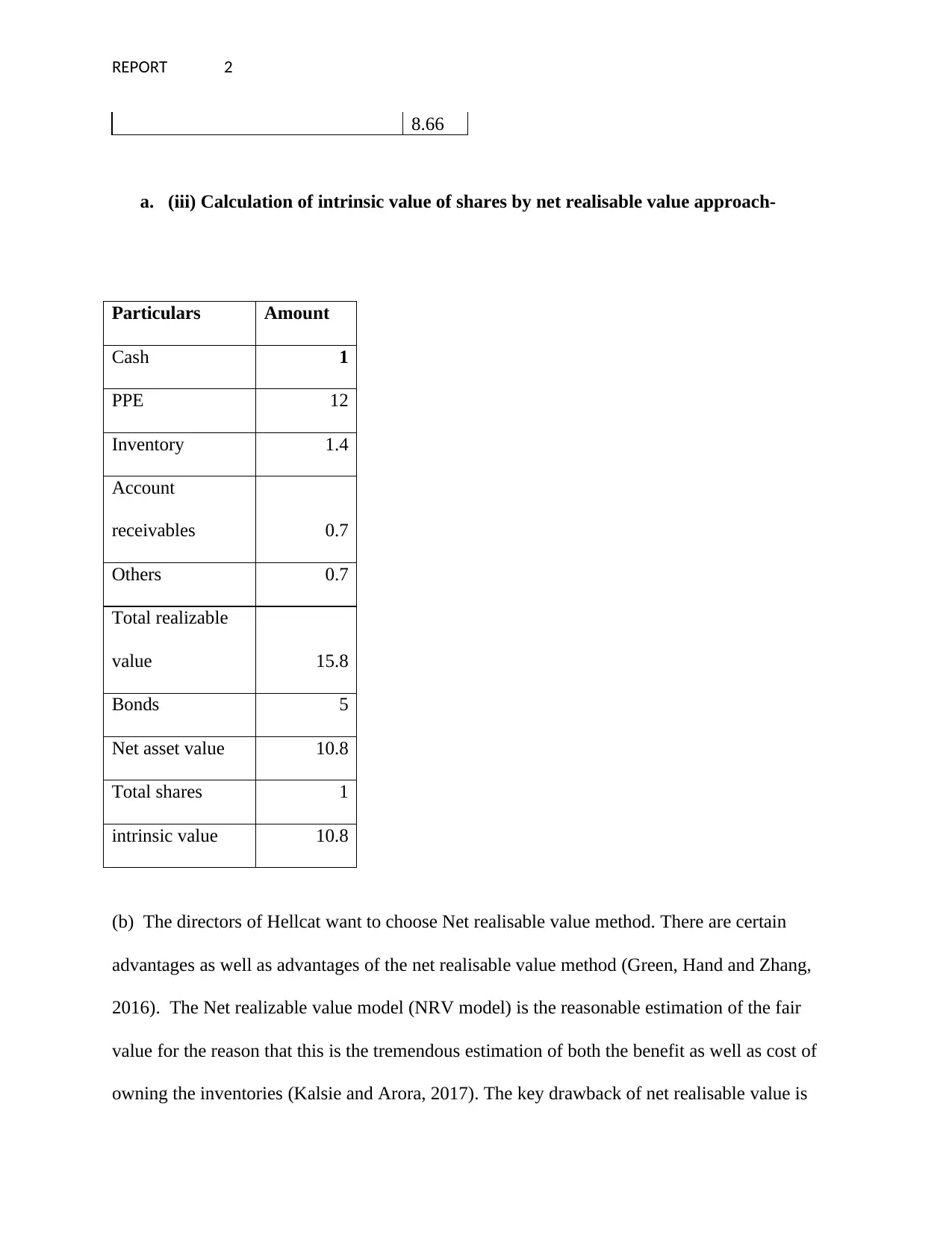

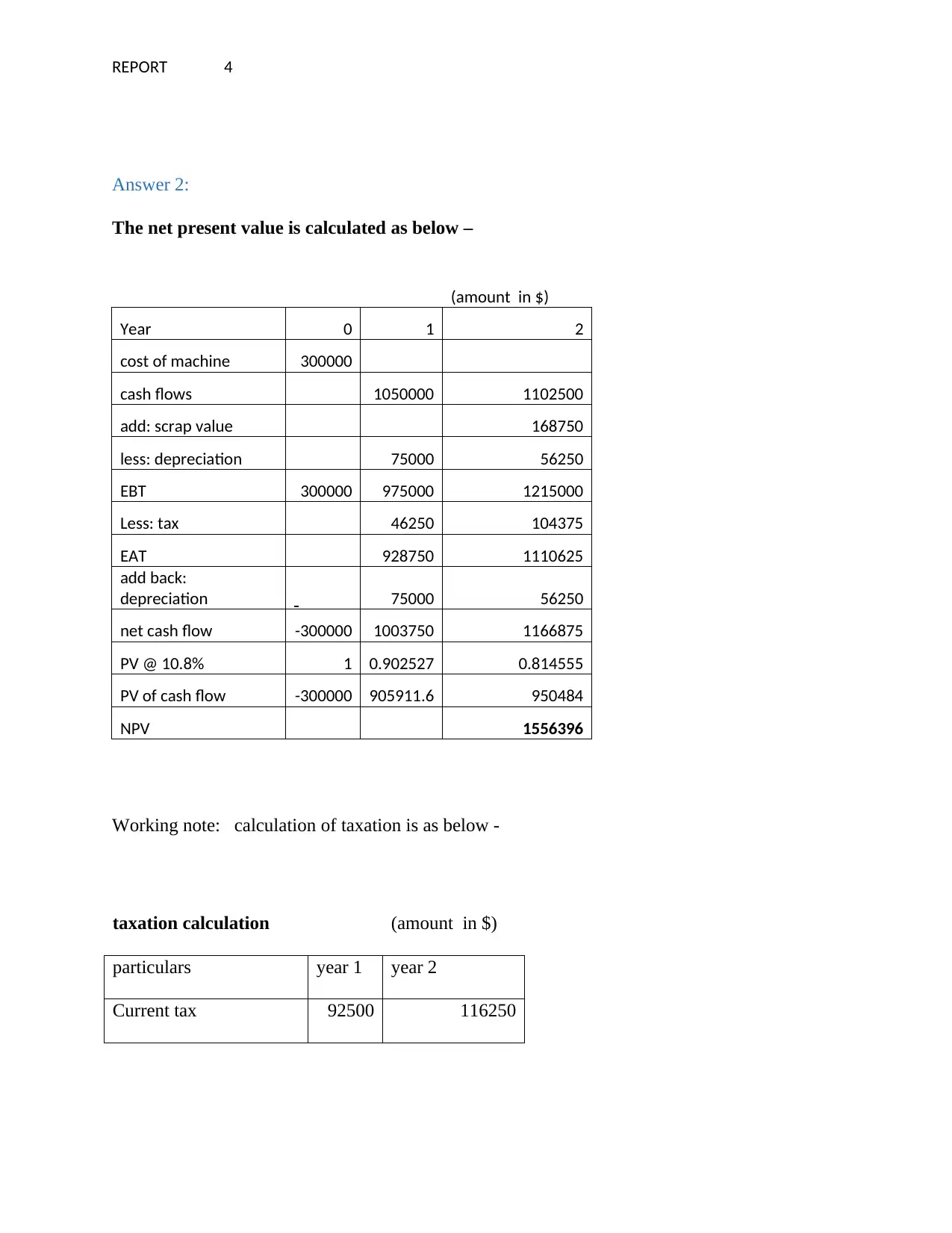

This report presents a comprehensive solution to a corporate finance assignment. It begins by calculating the intrinsic value of shares using the price-earnings approach, dividend discount model, and net realisable value approach. The report then analyzes the advantages and disadvantages of each method, with a specialist recommending the dividend discount model. The second part of the report calculates the Net Present Value (NPV) of a project, including cash flows, depreciation, taxation, and scrap value. The report concludes with a decision on whether to accept the project based on the positive NPV and provides references. The assignment covers key corporate finance concepts such as valuation, NPV, and financial analysis, and provides detailed calculations and explanations.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.