Corporate Finance Report: Project Investment Decisions

VerifiedAdded on 2022/08/24

|14

|2949

|11

Report

AI Summary

This report provides a comprehensive analysis of corporate finance concepts, focusing on project evaluation and investment decisions. It examines the marginal cost of capital (MCC) and the weighted average cost of capital (WACC) to determine the best investment opportunities. The analysis includes a comparison of mutually exclusive projects, calculating Net Present Value (NPV) and Internal Rate of Return (IRR) to identify the most suitable projects. The report also discusses the cost of debt, equity, retained earnings, and preferred stock, and their impact on the WACC. Furthermore, it explores the concept of breakpoints in the MCC curve and how dividend policy can affect capital investment decisions, offering recommendations from an upper-level management perspective. The report concludes with a ranking of projects based on financial metrics and a discussion of funding strategies.

Running head: CORPORATE FINANCE

CORPORATE FINANCE

Name of the Student

Name of the University

Author Note:

CORPORATE FINANCE

Name of the Student

Name of the University

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE FINANCE

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Cost of Debt.....................................................................................................................................3

Cost of Equity..................................................................................................................................4

Cost of Retained Earning.................................................................................................................5

Cost of Preferred Stock....................................................................................................................6

Weighted Average Cost of Capital..................................................................................................6

Comparing Mutually Exclusive Project...........................................................................................7

Comparing Projects.........................................................................................................................9

Breaks in the MCC Curve:..............................................................................................................9

Conclusion.....................................................................................................................................11

Reference.......................................................................................................................................12

CORPORATE FINANCE

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................2

Cost of Debt.....................................................................................................................................3

Cost of Equity..................................................................................................................................4

Cost of Retained Earning.................................................................................................................5

Cost of Preferred Stock....................................................................................................................6

Weighted Average Cost of Capital..................................................................................................6

Comparing Mutually Exclusive Project...........................................................................................7

Comparing Projects.........................................................................................................................9

Breaks in the MCC Curve:..............................................................................................................9

Conclusion.....................................................................................................................................11

Reference.......................................................................................................................................12

2

CORPORATE FINANCE

Introduction

In financial term, investment is regarded as an asset acquired with the goal of the

objective of generating income. In an economic sense, investment is purchasing goods with the

objective to create wealth in future by sacrificing its consumption or use in the present.

Nowadays, investment in the real state, stocks and bonds is where the funds are put to use since

they have a tendency of providing higher returns. Similarly, in this report, we consider which is

the best project to invest from among different projects. The purpose is to find which project will

yield better returns during a given period of time and with minimum investment (Chandra, 2017)

The paper has been structured in a way showing various cost that will be incurred at the time of

issuing various stocks and debts and how will it impact in the decision making process of an

individual. Analysis of the data has been made based on the marginal cost of capital by

calculating the net present value (NPV), the weighted average cost of capital (WACC) and

internal rate of return (IRR) to identify the suitable project that will yield a higher rate of return.

Discussion

Marginal Cost of Capital (MCC) is the combined total cost of debt, equity stock and

preference stock taking into account their respective weights of the total capital of the company.

An investor seeks it as the rate of return available from the securities of the company. The

marginal cost of capital is the cost that is incurred to raise additional capital from each of the

sources defined above (Bauer & Zanjani, 2016). It is the least rate of return that an investor

expects to gain for the capital provided to the company. The investment will be worth if the

expected return on capital will be greater than the cost of capital (Frank & Shen, 2016). The

weighted average cost of capital is the most ordinary measure used while calculating the cost of

capital, and which is primarily used in the business valuation and capital budgeting (Vartiainen

CORPORATE FINANCE

Introduction

In financial term, investment is regarded as an asset acquired with the goal of the

objective of generating income. In an economic sense, investment is purchasing goods with the

objective to create wealth in future by sacrificing its consumption or use in the present.

Nowadays, investment in the real state, stocks and bonds is where the funds are put to use since

they have a tendency of providing higher returns. Similarly, in this report, we consider which is

the best project to invest from among different projects. The purpose is to find which project will

yield better returns during a given period of time and with minimum investment (Chandra, 2017)

The paper has been structured in a way showing various cost that will be incurred at the time of

issuing various stocks and debts and how will it impact in the decision making process of an

individual. Analysis of the data has been made based on the marginal cost of capital by

calculating the net present value (NPV), the weighted average cost of capital (WACC) and

internal rate of return (IRR) to identify the suitable project that will yield a higher rate of return.

Discussion

Marginal Cost of Capital (MCC) is the combined total cost of debt, equity stock and

preference stock taking into account their respective weights of the total capital of the company.

An investor seeks it as the rate of return available from the securities of the company. The

marginal cost of capital is the cost that is incurred to raise additional capital from each of the

sources defined above (Bauer & Zanjani, 2016). It is the least rate of return that an investor

expects to gain for the capital provided to the company. The investment will be worth if the

expected return on capital will be greater than the cost of capital (Frank & Shen, 2016). The

weighted average cost of capital is the most ordinary measure used while calculating the cost of

capital, and which is primarily used in the business valuation and capital budgeting (Vartiainen

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE FINANCE

et al., 2019). In the following scenario, an evaluation has been made on the two mutually

exclusive projects (Project A and Project B) to identify the most suitable and beneficial project to

invest on and thereafter comparing the beneficial project with Project B. Mutually exclusive

project are those project which cannot occur at the same time i.e. acceptance of one project will

automatically lead to rejection of the other one (Minken, 2016). The project deals with supplying

equipment. The benefits available, if the company uses the marginal cost of capital technique

(Negasa, 2016):

It changes the overall cost of capital if additional capital is raised.

It provides a base for deciding as to whether raising further funds for business expansion

or on a new project will be beneficial or not.

It also helps in deciding what type of fund is required to be raised and in which

proportion.

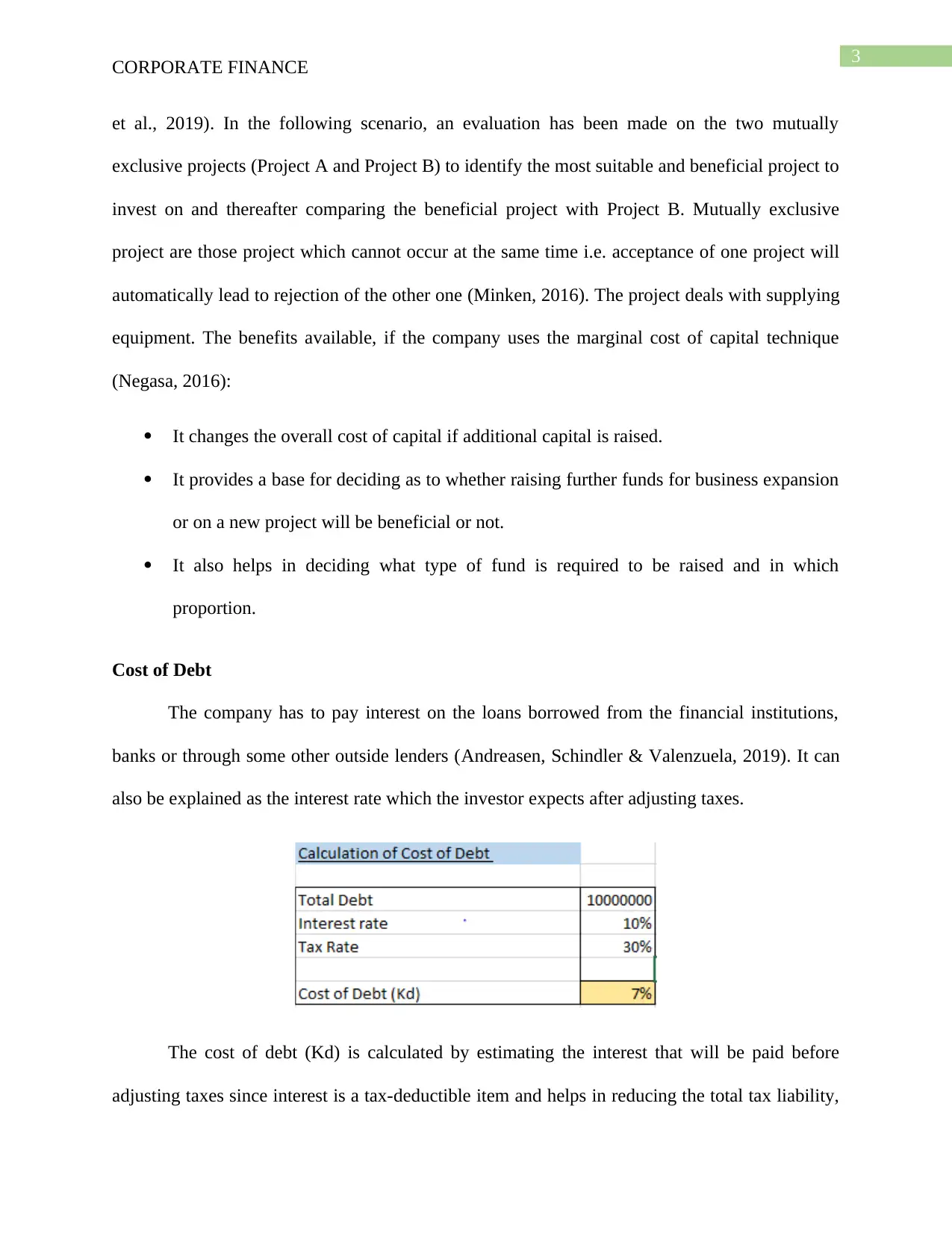

Cost of Debt

The company has to pay interest on the loans borrowed from the financial institutions,

banks or through some other outside lenders (Andreasen, Schindler & Valenzuela, 2019). It can

also be explained as the interest rate which the investor expects after adjusting taxes.

The cost of debt (Kd) is calculated by estimating the interest that will be paid before

adjusting taxes since interest is a tax-deductible item and helps in reducing the total tax liability,

CORPORATE FINANCE

et al., 2019). In the following scenario, an evaluation has been made on the two mutually

exclusive projects (Project A and Project B) to identify the most suitable and beneficial project to

invest on and thereafter comparing the beneficial project with Project B. Mutually exclusive

project are those project which cannot occur at the same time i.e. acceptance of one project will

automatically lead to rejection of the other one (Minken, 2016). The project deals with supplying

equipment. The benefits available, if the company uses the marginal cost of capital technique

(Negasa, 2016):

It changes the overall cost of capital if additional capital is raised.

It provides a base for deciding as to whether raising further funds for business expansion

or on a new project will be beneficial or not.

It also helps in deciding what type of fund is required to be raised and in which

proportion.

Cost of Debt

The company has to pay interest on the loans borrowed from the financial institutions,

banks or through some other outside lenders (Andreasen, Schindler & Valenzuela, 2019). It can

also be explained as the interest rate which the investor expects after adjusting taxes.

The cost of debt (Kd) is calculated by estimating the interest that will be paid before

adjusting taxes since interest is a tax-deductible item and helps in reducing the total tax liability,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE FINANCE

it will also reduce the cost of issuing the debt instrument. The cost of debt is calculated by

multiplying the interest, that is required to be paid, by (1-Tax rate) and dividing the numerator

with the total amount of debt raised (Osma, Gomez-Conde & de las Heras, 2018). The cost of

capital is similar for both the mutually exclusive project. The cost of debt in both the mutually

exclusive project will be the same because of similar interest rates and tax rates even though the

amount of debt differs. The rates will be identical in the case of Project B because of similar

interest rates and tax rate.

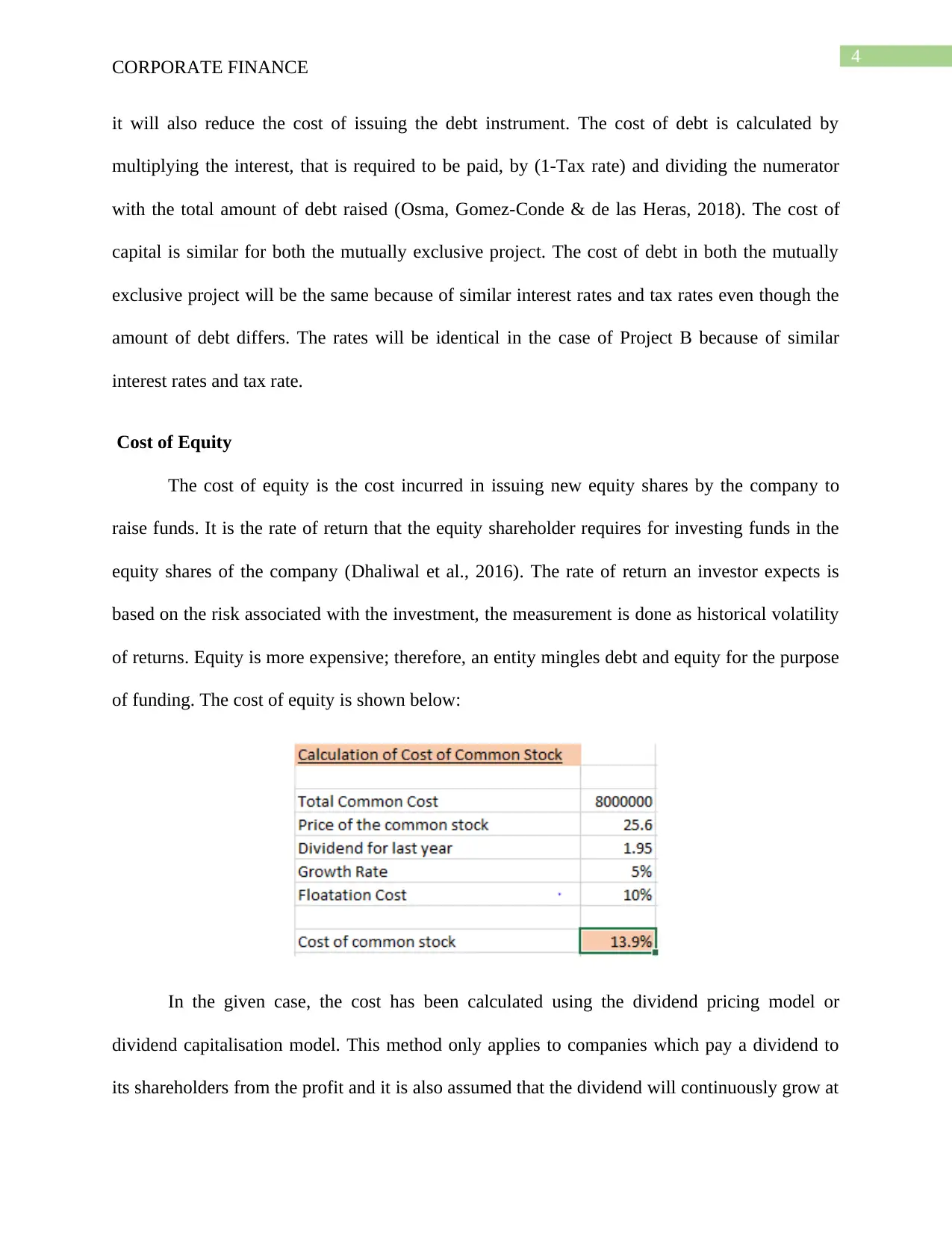

Cost of Equity

The cost of equity is the cost incurred in issuing new equity shares by the company to

raise funds. It is the rate of return that the equity shareholder requires for investing funds in the

equity shares of the company (Dhaliwal et al., 2016). The rate of return an investor expects is

based on the risk associated with the investment, the measurement is done as historical volatility

of returns. Equity is more expensive; therefore, an entity mingles debt and equity for the purpose

of funding. The cost of equity is shown below:

In the given case, the cost has been calculated using the dividend pricing model or

dividend capitalisation model. This method only applies to companies which pay a dividend to

its shareholders from the profit and it is also assumed that the dividend will continuously grow at

CORPORATE FINANCE

it will also reduce the cost of issuing the debt instrument. The cost of debt is calculated by

multiplying the interest, that is required to be paid, by (1-Tax rate) and dividing the numerator

with the total amount of debt raised (Osma, Gomez-Conde & de las Heras, 2018). The cost of

capital is similar for both the mutually exclusive project. The cost of debt in both the mutually

exclusive project will be the same because of similar interest rates and tax rates even though the

amount of debt differs. The rates will be identical in the case of Project B because of similar

interest rates and tax rate.

Cost of Equity

The cost of equity is the cost incurred in issuing new equity shares by the company to

raise funds. It is the rate of return that the equity shareholder requires for investing funds in the

equity shares of the company (Dhaliwal et al., 2016). The rate of return an investor expects is

based on the risk associated with the investment, the measurement is done as historical volatility

of returns. Equity is more expensive; therefore, an entity mingles debt and equity for the purpose

of funding. The cost of equity is shown below:

In the given case, the cost has been calculated using the dividend pricing model or

dividend capitalisation model. This method only applies to companies which pay a dividend to

its shareholders from the profit and it is also assumed that the dividend will continuously grow at

5

CORPORATE FINANCE

that rate (Pinto, 2020). This model does not account for the risk that is taken on investment as in

case of capital asset pricing model (CAPM). The formula taken for dividend pricing model is

calculated by dividing the dividend payable on shares next year (next year annual dividend) by

the current market price of the stock and adding the balancing figure with the growth rate, which

is shown below:

The cost of equity of both the project is similar because the market price, dividend,

issuance cost (floatation cost) and growth rate is similar in every cases.

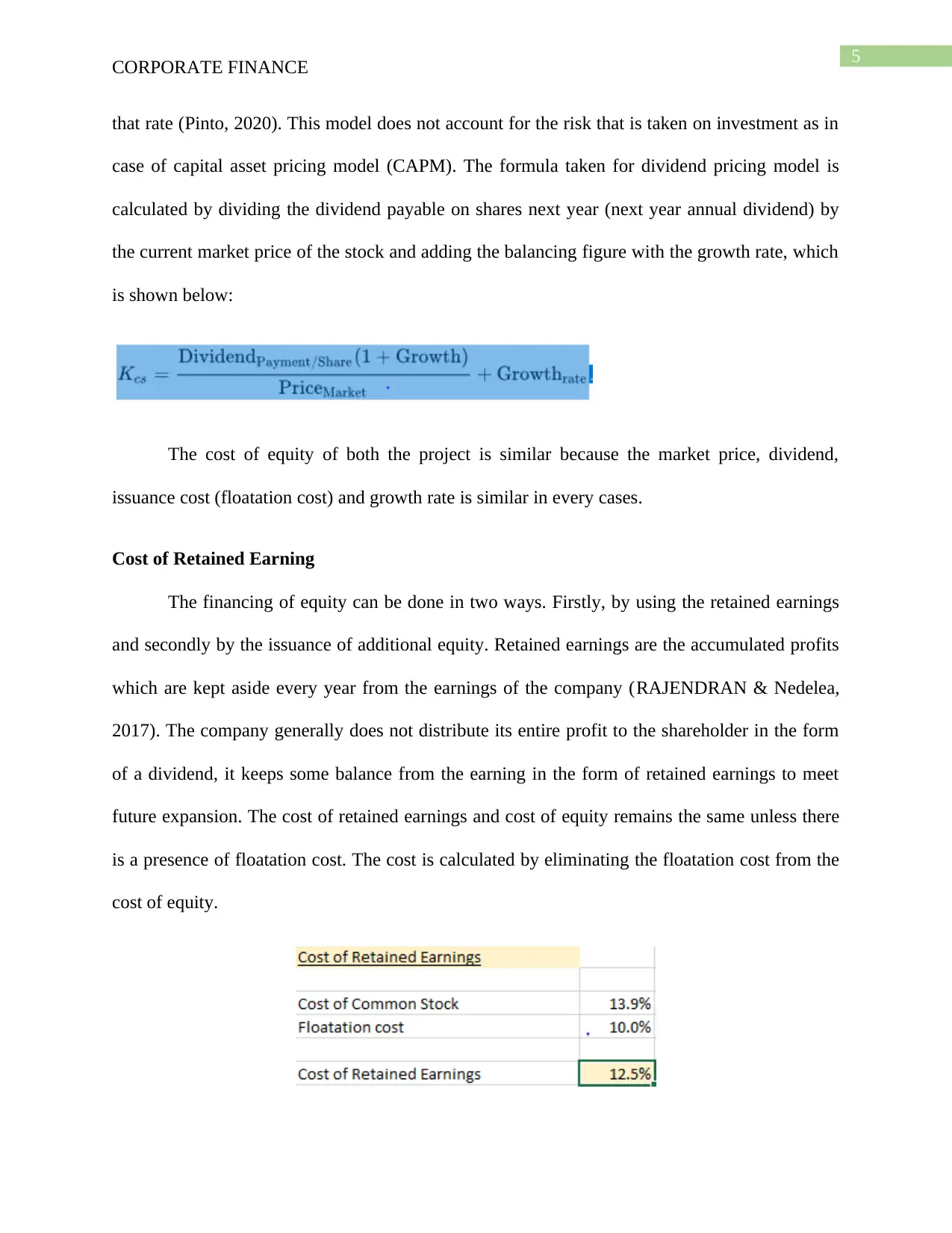

Cost of Retained Earning

The financing of equity can be done in two ways. Firstly, by using the retained earnings

and secondly by the issuance of additional equity. Retained earnings are the accumulated profits

which are kept aside every year from the earnings of the company (RAJENDRAN & Nedelea,

2017). The company generally does not distribute its entire profit to the shareholder in the form

of a dividend, it keeps some balance from the earning in the form of retained earnings to meet

future expansion. The cost of retained earnings and cost of equity remains the same unless there

is a presence of floatation cost. The cost is calculated by eliminating the floatation cost from the

cost of equity.

CORPORATE FINANCE

that rate (Pinto, 2020). This model does not account for the risk that is taken on investment as in

case of capital asset pricing model (CAPM). The formula taken for dividend pricing model is

calculated by dividing the dividend payable on shares next year (next year annual dividend) by

the current market price of the stock and adding the balancing figure with the growth rate, which

is shown below:

The cost of equity of both the project is similar because the market price, dividend,

issuance cost (floatation cost) and growth rate is similar in every cases.

Cost of Retained Earning

The financing of equity can be done in two ways. Firstly, by using the retained earnings

and secondly by the issuance of additional equity. Retained earnings are the accumulated profits

which are kept aside every year from the earnings of the company (RAJENDRAN & Nedelea,

2017). The company generally does not distribute its entire profit to the shareholder in the form

of a dividend, it keeps some balance from the earning in the form of retained earnings to meet

future expansion. The cost of retained earnings and cost of equity remains the same unless there

is a presence of floatation cost. The cost is calculated by eliminating the floatation cost from the

cost of equity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE FINANCE

The cost of retained earnings has also been similar in all the project since the information

regarding cost of equity and percentage of floatation cost is similar in all the project.

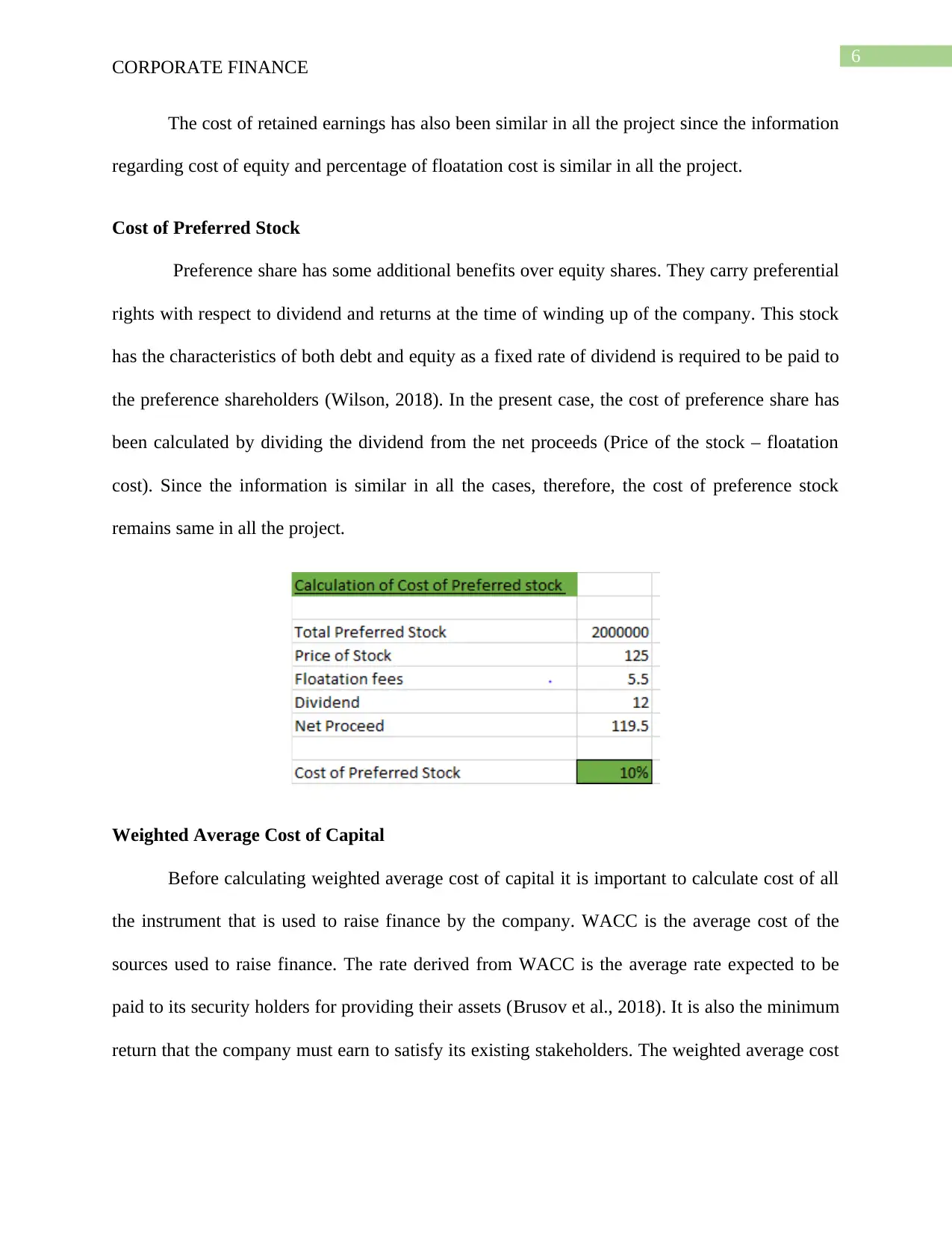

Cost of Preferred Stock

Preference share has some additional benefits over equity shares. They carry preferential

rights with respect to dividend and returns at the time of winding up of the company. This stock

has the characteristics of both debt and equity as a fixed rate of dividend is required to be paid to

the preference shareholders (Wilson, 2018). In the present case, the cost of preference share has

been calculated by dividing the dividend from the net proceeds (Price of the stock – floatation

cost). Since the information is similar in all the cases, therefore, the cost of preference stock

remains same in all the project.

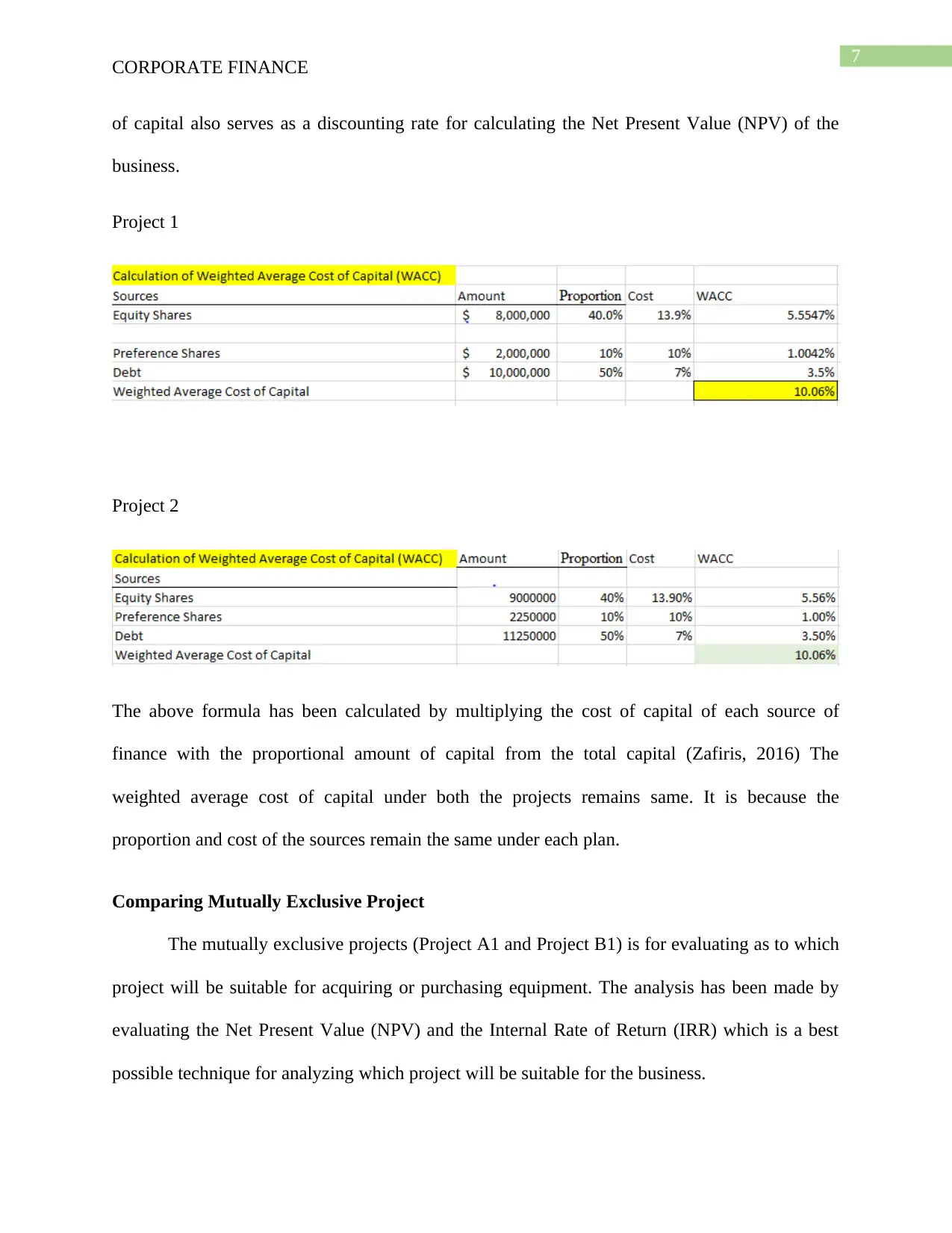

Weighted Average Cost of Capital

Before calculating weighted average cost of capital it is important to calculate cost of all

the instrument that is used to raise finance by the company. WACC is the average cost of the

sources used to raise finance. The rate derived from WACC is the average rate expected to be

paid to its security holders for providing their assets (Brusov et al., 2018). It is also the minimum

return that the company must earn to satisfy its existing stakeholders. The weighted average cost

CORPORATE FINANCE

The cost of retained earnings has also been similar in all the project since the information

regarding cost of equity and percentage of floatation cost is similar in all the project.

Cost of Preferred Stock

Preference share has some additional benefits over equity shares. They carry preferential

rights with respect to dividend and returns at the time of winding up of the company. This stock

has the characteristics of both debt and equity as a fixed rate of dividend is required to be paid to

the preference shareholders (Wilson, 2018). In the present case, the cost of preference share has

been calculated by dividing the dividend from the net proceeds (Price of the stock – floatation

cost). Since the information is similar in all the cases, therefore, the cost of preference stock

remains same in all the project.

Weighted Average Cost of Capital

Before calculating weighted average cost of capital it is important to calculate cost of all

the instrument that is used to raise finance by the company. WACC is the average cost of the

sources used to raise finance. The rate derived from WACC is the average rate expected to be

paid to its security holders for providing their assets (Brusov et al., 2018). It is also the minimum

return that the company must earn to satisfy its existing stakeholders. The weighted average cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE FINANCE

of capital also serves as a discounting rate for calculating the Net Present Value (NPV) of the

business.

Project 1

Project 2

The above formula has been calculated by multiplying the cost of capital of each source of

finance with the proportional amount of capital from the total capital (Zafiris, 2016) The

weighted average cost of capital under both the projects remains same. It is because the

proportion and cost of the sources remain the same under each plan.

Comparing Mutually Exclusive Project

The mutually exclusive projects (Project A1 and Project B1) is for evaluating as to which

project will be suitable for acquiring or purchasing equipment. The analysis has been made by

evaluating the Net Present Value (NPV) and the Internal Rate of Return (IRR) which is a best

possible technique for analyzing which project will be suitable for the business.

CORPORATE FINANCE

of capital also serves as a discounting rate for calculating the Net Present Value (NPV) of the

business.

Project 1

Project 2

The above formula has been calculated by multiplying the cost of capital of each source of

finance with the proportional amount of capital from the total capital (Zafiris, 2016) The

weighted average cost of capital under both the projects remains same. It is because the

proportion and cost of the sources remain the same under each plan.

Comparing Mutually Exclusive Project

The mutually exclusive projects (Project A1 and Project B1) is for evaluating as to which

project will be suitable for acquiring or purchasing equipment. The analysis has been made by

evaluating the Net Present Value (NPV) and the Internal Rate of Return (IRR) which is a best

possible technique for analyzing which project will be suitable for the business.

8

CORPORATE FINANCE

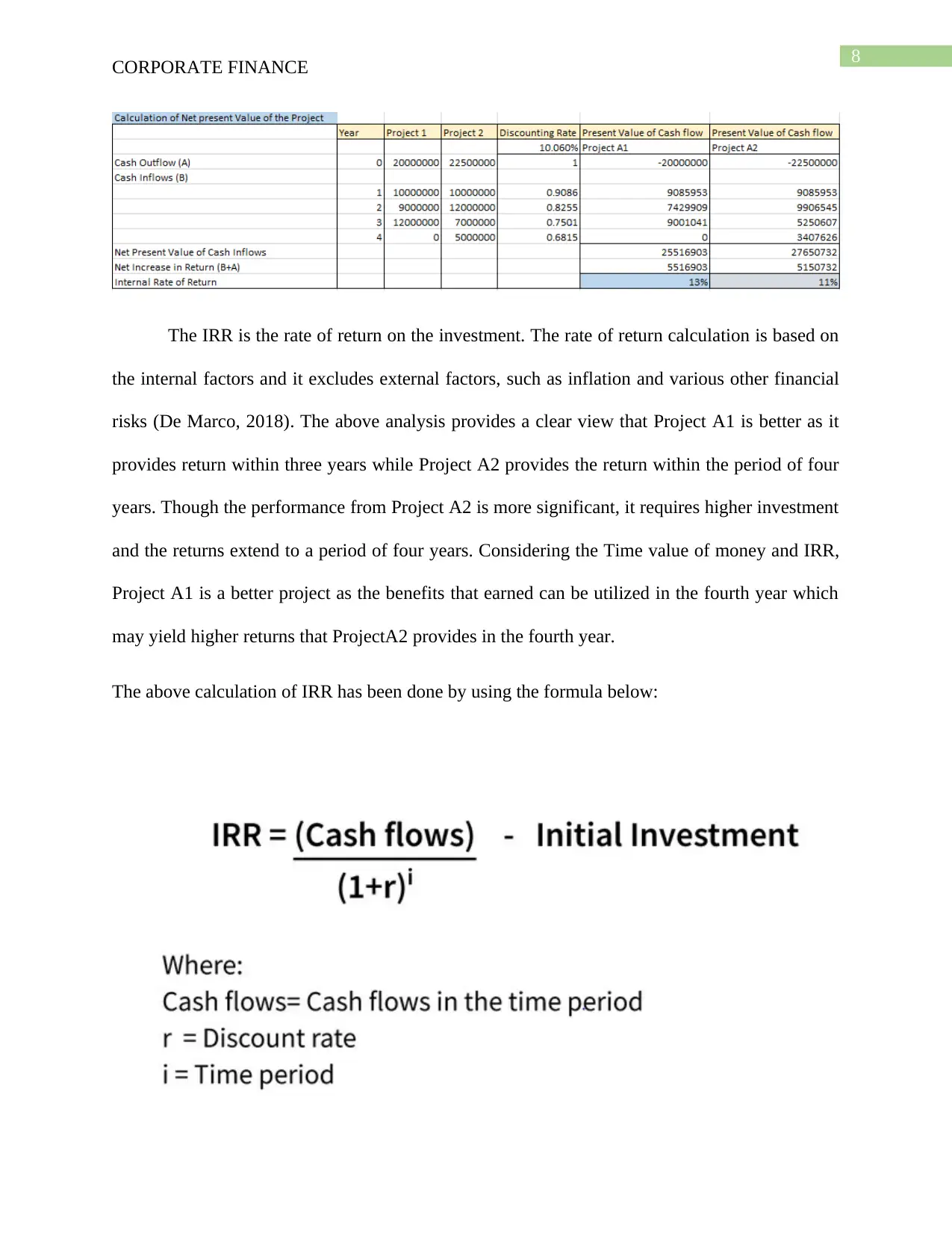

The IRR is the rate of return on the investment. The rate of return calculation is based on

the internal factors and it excludes external factors, such as inflation and various other financial

risks (De Marco, 2018). The above analysis provides a clear view that Project A1 is better as it

provides return within three years while Project A2 provides the return within the period of four

years. Though the performance from Project A2 is more significant, it requires higher investment

and the returns extend to a period of four years. Considering the Time value of money and IRR,

Project A1 is a better project as the benefits that earned can be utilized in the fourth year which

may yield higher returns that ProjectA2 provides in the fourth year.

The above calculation of IRR has been done by using the formula below:

CORPORATE FINANCE

The IRR is the rate of return on the investment. The rate of return calculation is based on

the internal factors and it excludes external factors, such as inflation and various other financial

risks (De Marco, 2018). The above analysis provides a clear view that Project A1 is better as it

provides return within three years while Project A2 provides the return within the period of four

years. Though the performance from Project A2 is more significant, it requires higher investment

and the returns extend to a period of four years. Considering the Time value of money and IRR,

Project A1 is a better project as the benefits that earned can be utilized in the fourth year which

may yield higher returns that ProjectA2 provides in the fourth year.

The above calculation of IRR has been done by using the formula below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE FINANCE

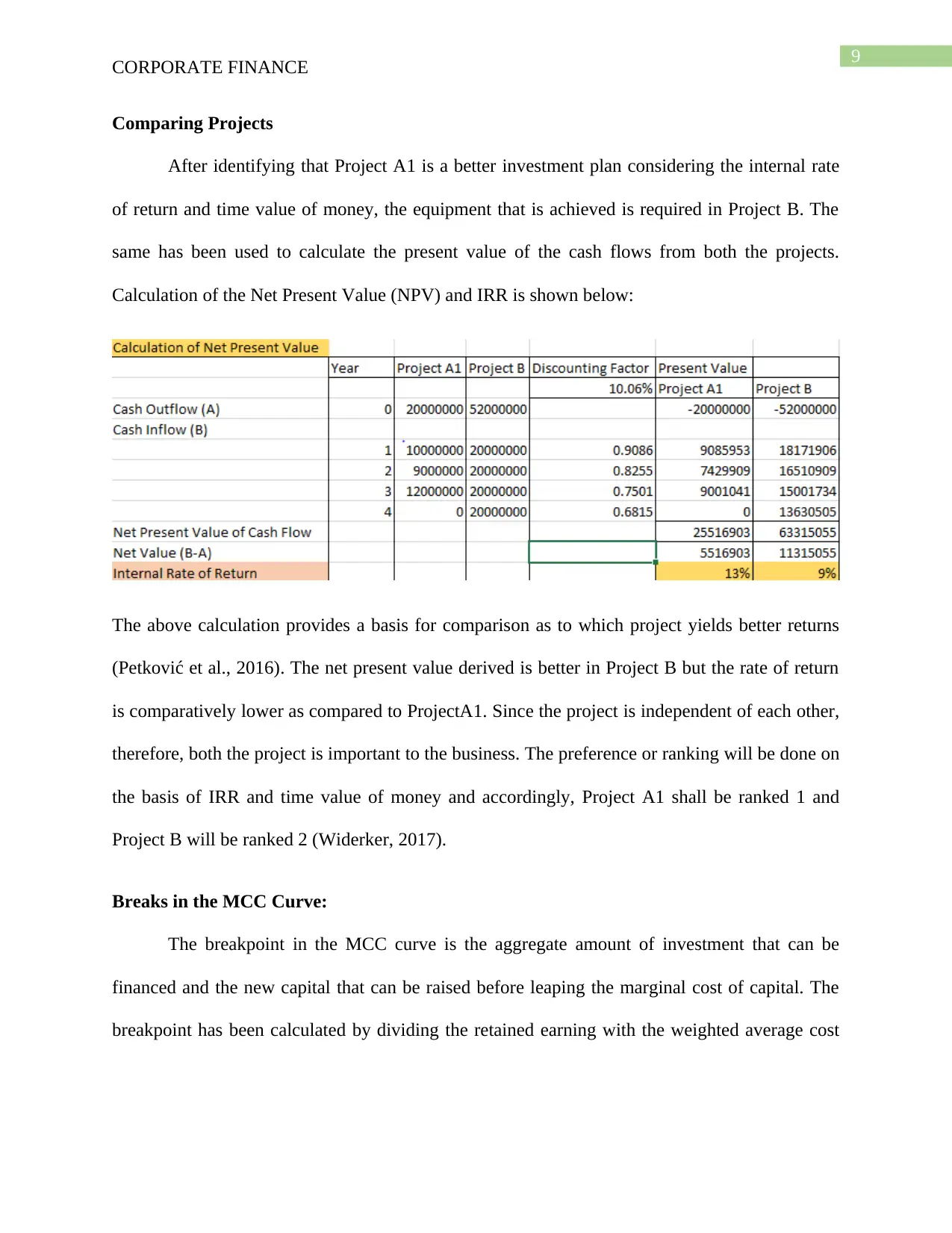

Comparing Projects

After identifying that Project A1 is a better investment plan considering the internal rate

of return and time value of money, the equipment that is achieved is required in Project B. The

same has been used to calculate the present value of the cash flows from both the projects.

Calculation of the Net Present Value (NPV) and IRR is shown below:

The above calculation provides a basis for comparison as to which project yields better returns

(Petković et al., 2016). The net present value derived is better in Project B but the rate of return

is comparatively lower as compared to ProjectA1. Since the project is independent of each other,

therefore, both the project is important to the business. The preference or ranking will be done on

the basis of IRR and time value of money and accordingly, Project A1 shall be ranked 1 and

Project B will be ranked 2 (Widerker, 2017).

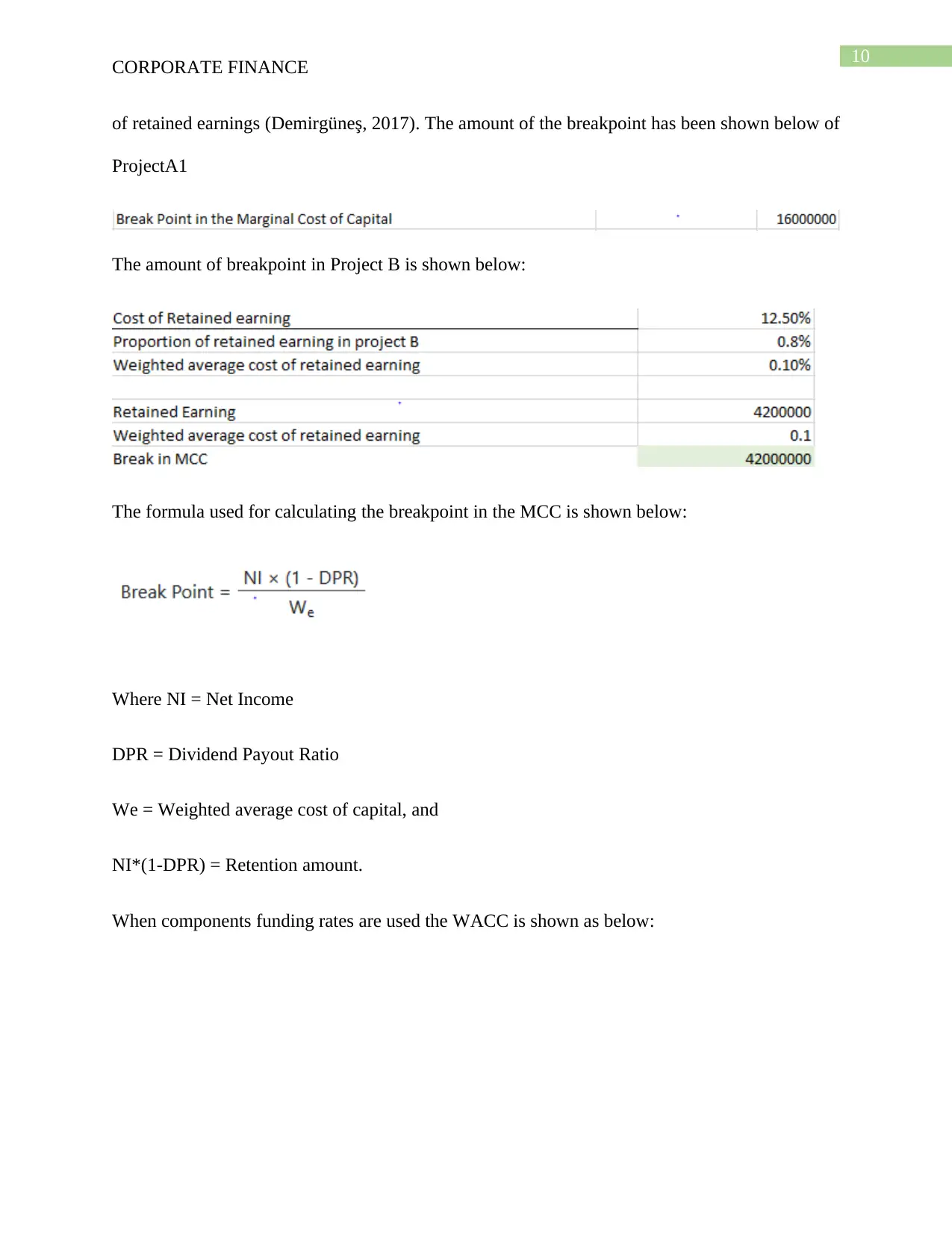

Breaks in the MCC Curve:

The breakpoint in the MCC curve is the aggregate amount of investment that can be

financed and the new capital that can be raised before leaping the marginal cost of capital. The

breakpoint has been calculated by dividing the retained earning with the weighted average cost

CORPORATE FINANCE

Comparing Projects

After identifying that Project A1 is a better investment plan considering the internal rate

of return and time value of money, the equipment that is achieved is required in Project B. The

same has been used to calculate the present value of the cash flows from both the projects.

Calculation of the Net Present Value (NPV) and IRR is shown below:

The above calculation provides a basis for comparison as to which project yields better returns

(Petković et al., 2016). The net present value derived is better in Project B but the rate of return

is comparatively lower as compared to ProjectA1. Since the project is independent of each other,

therefore, both the project is important to the business. The preference or ranking will be done on

the basis of IRR and time value of money and accordingly, Project A1 shall be ranked 1 and

Project B will be ranked 2 (Widerker, 2017).

Breaks in the MCC Curve:

The breakpoint in the MCC curve is the aggregate amount of investment that can be

financed and the new capital that can be raised before leaping the marginal cost of capital. The

breakpoint has been calculated by dividing the retained earning with the weighted average cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE FINANCE

of retained earnings (Demirgüneş, 2017). The amount of the breakpoint has been shown below of

ProjectA1

The amount of breakpoint in Project B is shown below:

The formula used for calculating the breakpoint in the MCC is shown below:

Where NI = Net Income

DPR = Dividend Payout Ratio

We = Weighted average cost of capital, and

NI*(1-DPR) = Retention amount.

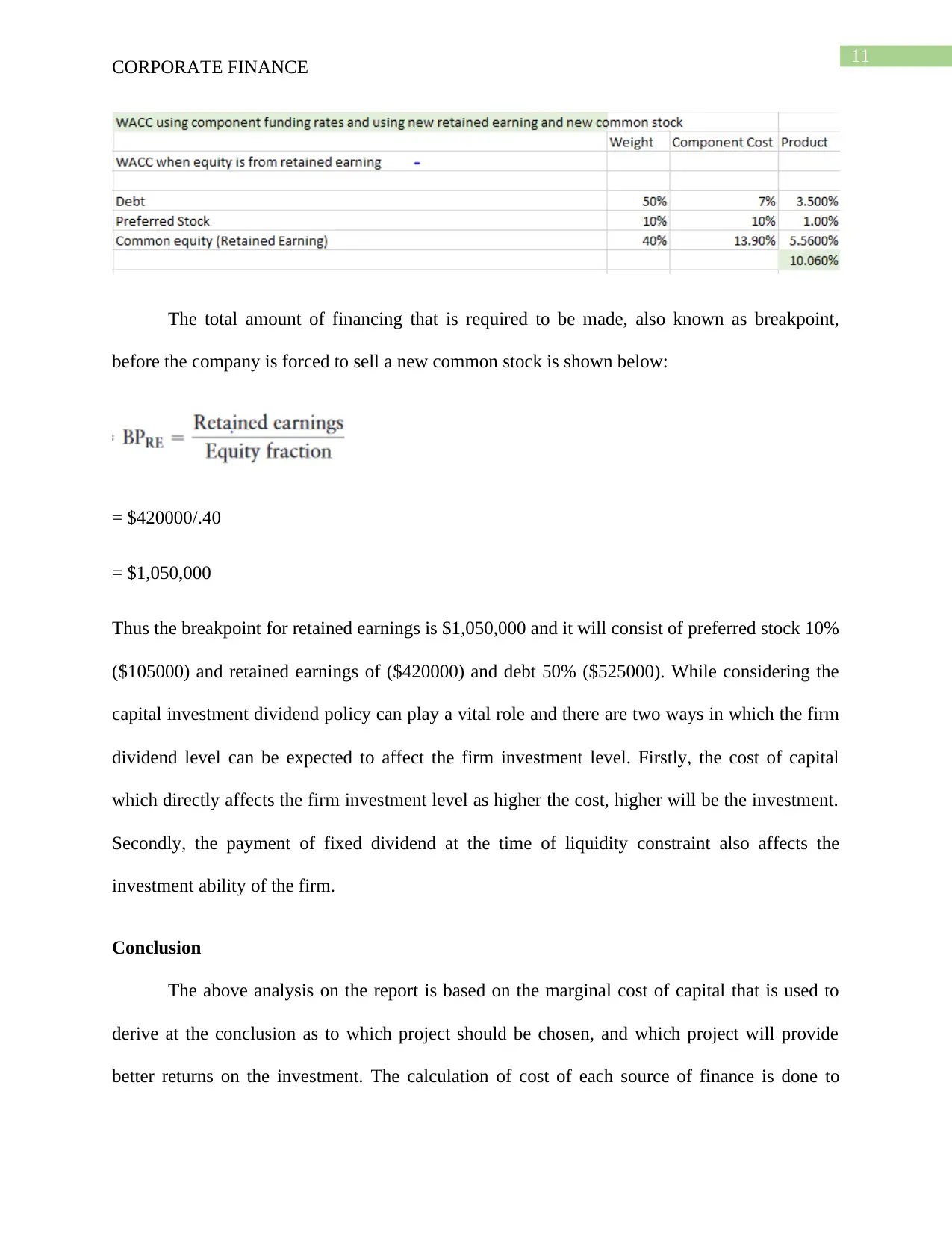

When components funding rates are used the WACC is shown as below:

CORPORATE FINANCE

of retained earnings (Demirgüneş, 2017). The amount of the breakpoint has been shown below of

ProjectA1

The amount of breakpoint in Project B is shown below:

The formula used for calculating the breakpoint in the MCC is shown below:

Where NI = Net Income

DPR = Dividend Payout Ratio

We = Weighted average cost of capital, and

NI*(1-DPR) = Retention amount.

When components funding rates are used the WACC is shown as below:

11

CORPORATE FINANCE

The total amount of financing that is required to be made, also known as breakpoint,

before the company is forced to sell a new common stock is shown below:

= $420000/.40

= $1,050,000

Thus the breakpoint for retained earnings is $1,050,000 and it will consist of preferred stock 10%

($105000) and retained earnings of ($420000) and debt 50% ($525000). While considering the

capital investment dividend policy can play a vital role and there are two ways in which the firm

dividend level can be expected to affect the firm investment level. Firstly, the cost of capital

which directly affects the firm investment level as higher the cost, higher will be the investment.

Secondly, the payment of fixed dividend at the time of liquidity constraint also affects the

investment ability of the firm.

Conclusion

The above analysis on the report is based on the marginal cost of capital that is used to

derive at the conclusion as to which project should be chosen, and which project will provide

better returns on the investment. The calculation of cost of each source of finance is done to

CORPORATE FINANCE

The total amount of financing that is required to be made, also known as breakpoint,

before the company is forced to sell a new common stock is shown below:

= $420000/.40

= $1,050,000

Thus the breakpoint for retained earnings is $1,050,000 and it will consist of preferred stock 10%

($105000) and retained earnings of ($420000) and debt 50% ($525000). While considering the

capital investment dividend policy can play a vital role and there are two ways in which the firm

dividend level can be expected to affect the firm investment level. Firstly, the cost of capital

which directly affects the firm investment level as higher the cost, higher will be the investment.

Secondly, the payment of fixed dividend at the time of liquidity constraint also affects the

investment ability of the firm.

Conclusion

The above analysis on the report is based on the marginal cost of capital that is used to

derive at the conclusion as to which project should be chosen, and which project will provide

better returns on the investment. The calculation of cost of each source of finance is done to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.